Key Insights

The Latin America Rigid Plastic Packaging market is experiencing steady growth, projected to reach a significant size over the forecast period (2025-2033). A Compound Annual Growth Rate (CAGR) of 3.47% indicates a consistent expansion, driven primarily by the increasing demand for packaged goods across various sectors, including food and beverages, personal care, and pharmaceuticals. Rising disposable incomes and a growing middle class in several Latin American countries fuel this demand, pushing for convenient and cost-effective packaging solutions. Furthermore, advancements in plastic packaging technology, including lighter-weight, more sustainable options, contribute to market expansion. However, environmental concerns regarding plastic waste and stringent government regulations aimed at reducing plastic pollution pose challenges to the market's growth. These regulations are prompting manufacturers to explore eco-friendly alternatives and improve recycling infrastructure, influencing market trends toward biodegradable and recyclable plastics. The competitive landscape is comprised of both established multinational corporations like Amcor, Berry Global, and Silgan Holdings, and smaller regional players. Established companies leverage their extensive distribution networks and advanced technologies, while emerging companies often focus on niche markets or innovative sustainable packaging solutions. The market segmentation is primarily based on packaging type (bottles, containers, films, etc.) and end-use application, with considerable variation in growth rates across segments depending on consumer preferences and industry-specific trends. Regional variations exist, with certain countries exhibiting higher growth potential due to factors like economic development and infrastructure improvements.

The market’s future growth depends largely on the balance between increasing demand and environmental concerns. Strategies focusing on sustainable packaging solutions, such as increased use of recycled materials and the development of biodegradable plastics, will be key to navigating these challenges. The competitive landscape will likely see increased consolidation as larger companies acquire smaller players to expand their market share and product offerings. Furthermore, collaboration across the value chain – from raw material suppliers to recyclers – will be vital for fostering a more circular economy and mitigating the environmental impact of plastic packaging. This approach will involve adopting advanced recycling technologies and promoting greater consumer awareness of responsible waste management practices. Success in the Latin American rigid plastic packaging market requires adaptability, innovation, and a strong commitment to environmental sustainability.

This dynamic report provides a detailed analysis of the Latin America Rigid Plastic Packaging market, offering invaluable insights for businesses, investors, and stakeholders. With a comprehensive study period spanning 2019-2033 (Base Year: 2025, Forecast Period: 2025-2033), this report leverages extensive data and expert analysis to paint a clear picture of current market dynamics and future growth trajectories. Expect in-depth coverage of market size, leading segments, key players, emerging trends, and challenges, all crucial for navigating this rapidly evolving landscape. The market is projected to reach xx Million by 2033, exhibiting a robust CAGR.

Latin America Rigid Plastic Packaging Market Structure & Competitive Landscape

The Latin American Rigid Plastic Packaging market exhibits a moderately concentrated structure, with a Herfindahl-Hirschman Index (HHI) estimated at xx in 2025. Key players, including Amcor Group GmbH, Berry Global Inc, Alpla Werke Alwin Lehner GmbH & Co KG, Silgan Holdings Inc, and Sealed Air Corporation, hold significant market share, driven by economies of scale and established distribution networks. However, smaller, regional players are also gaining traction, particularly those focusing on sustainable and innovative packaging solutions.

- Market Concentration: The HHI indicates a moderately consolidated market, with room for both established and emerging players.

- Innovation Drivers: Growing demand for lightweight, functional, and sustainable packaging is stimulating innovation in materials, design, and manufacturing processes.

- Regulatory Impacts: Stringent environmental regulations are pushing manufacturers toward eco-friendly options, impacting material choices and recycling initiatives.

- Product Substitutes: The market faces competition from alternative packaging materials like paperboard and flexible plastics, requiring continuous adaptation.

- End-User Segmentation: The market caters to diverse sectors, including food and beverage, personal care, pharmaceuticals, and industrial goods, each with unique packaging requirements.

- M&A Trends: Consolidation through mergers and acquisitions is evident, reflecting the industry's quest for scale, technological advancements, and geographic expansion. The estimated M&A volume in 2024 was xx Million, indicating a dynamic competitive landscape.

Latin America Rigid Plastic Packaging Market Market Trends & Opportunities

The Latin America Rigid Plastic Packaging market is experiencing significant growth, driven by expanding consumer base, rising disposable incomes, and increasing demand across diverse end-use sectors. The market size reached xx Million in 2024 and is projected to reach xx Million by 2033, demonstrating a substantial CAGR of xx%. Key growth drivers include:

- Technological Advancements: The adoption of lightweighting technologies and advanced materials is improving packaging efficiency and reducing environmental impact. Barrier technology enhancements are also key.

- E-commerce Boom: The surge in online shopping is fueling demand for robust and protective packaging for e-commerce deliveries.

- Changing Consumer Preferences: Consumers are increasingly demanding sustainable, convenient, and aesthetically appealing packaging, influencing product innovation.

- Competitive Dynamics: Increased competition is fostering innovation and efficiency improvements, benefiting consumers and stimulating market growth.

- Market Penetration Rates: The penetration rate for rigid plastic packaging in key segments like food and beverage is expected to grow from xx% in 2024 to xx% by 2033.

Dominant Markets & Segments in Latin America Rigid Plastic Packaging Market

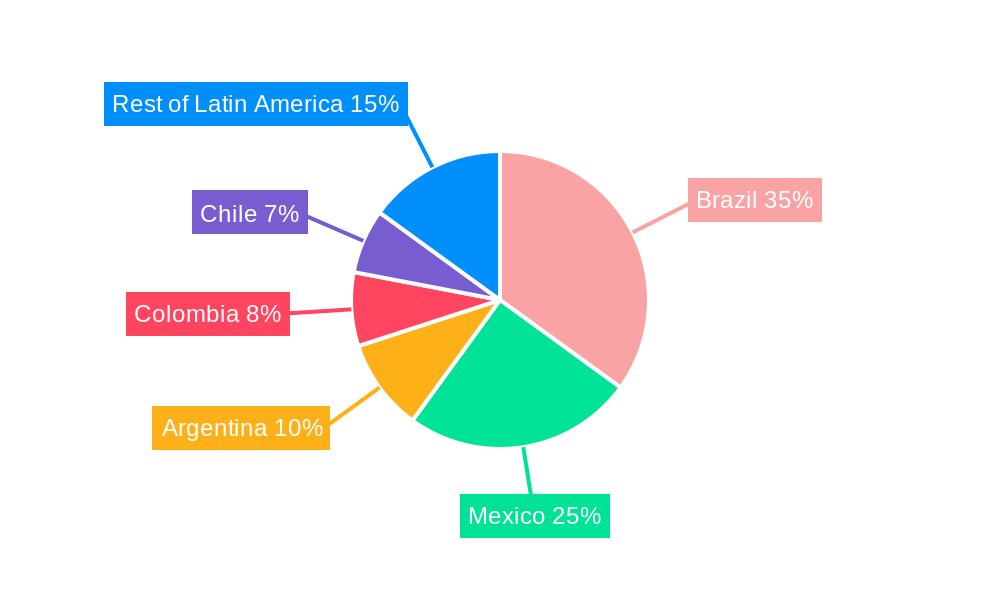

Brazil and Mexico represent the dominant markets within the Latin American Rigid Plastic Packaging sector, accounting for a combined xx% of the total market value in 2024.

- Brazil: Large population, robust consumer goods sector, and substantial industrial activity contribute to Brazil's market dominance.

- * Key Growth Drivers: Expanding middle class, increasing disposable incomes, and government initiatives promoting local manufacturing.

- Mexico: Strong economic growth, proximity to the US market, and a diversified industrial base drive market growth.

- * Key Growth Drivers: Foreign direct investment in manufacturing, robust food and beverage industry, and rising demand for consumer goods.

- Other Key Markets: Argentina, Colombia, and Chile also contribute significantly, although at a smaller scale compared to Brazil and Mexico.

The food and beverage segment is the largest consumer of rigid plastic packaging in Latin America, followed by personal care and pharmaceuticals. The growth in these sectors is expected to drive demand for innovative packaging solutions.

Latin America Rigid Plastic Packaging Market Product Analysis

Technological advancements in rigid plastic packaging are focused on enhancing barrier properties, lightweighting materials, and incorporating features that improve product preservation and consumer convenience. Recycled content incorporation is a major theme. Competition is driven by the ability to offer customized solutions, superior performance characteristics, and cost-effectiveness.

Key Drivers, Barriers & Challenges in Latin America Rigid Plastic Packaging Market

Key Drivers: Growing consumer demand, increasing urbanization, and a thriving food and beverage industry are major drivers. Government initiatives promoting local manufacturing and infrastructure development are also pushing market growth.

Challenges: Fluctuations in raw material prices, stringent environmental regulations, and competition from alternative packaging materials pose significant challenges. Supply chain disruptions and the need for robust recycling infrastructure are also critical factors impacting growth. These challenges lead to an estimated xx% reduction in potential market growth annually.

Growth Drivers in the Latin America Rigid Plastic Packaging Market

The market is fueled by the growth of the consumer goods sector, urbanization, rising disposable incomes, and evolving consumer preferences towards convenient and sustainable packaging options. Government support for local manufacturing and infrastructure investments further accelerates market expansion.

Challenges Impacting Latin America Rigid Plastic Packaging Market Growth

Significant challenges include the volatility of raw material prices (e.g., fluctuation of resin prices up to xx%), complex regulatory landscapes, and the need for improved recycling infrastructure. These factors collectively restrain market growth. Supply chain vulnerabilities add to these challenges.

Key Players Shaping the Latin America Rigid Plastic Packaging Market

- Amcor Group GmbH

- Berry Global Inc

- Alpla Werke Alwin Lehner GmbH & Co KG

- Silgan Holdings Inc

- Sealed Air Corporation

- Plastipak Holding Inc

- Sonoco Products Company

- Albea Group

- Greiner Packaging International GmbH

- BERICAP Holding GmbH

- Rioplastic

- IPACKCHEM GROUP

Significant Latin America Rigid Plastic Packaging Market Industry Milestones

- June 2024: Method's shift to 100% recycled coastal plastic bottles signifies a rising trend toward sustainable packaging. This collaboration with SC Johnson and Plastic Bank highlights the growing influence of circular economy initiatives.

- August 2023: Indorama Ventures' USD 20 Million investment in Brazilian recycling facilities emphasizes the industry's commitment to increasing the recycled PET resin supply. This move signals increasing focus on sustainable material sourcing.

- May 2023: Greenback's new recycling facility in Mexico, in partnership with Nestle, represents a significant advancement in plastic recycling technology and promises to circularize previously non-recyclable materials.

Future Outlook for Latin America Rigid Plastic Packaging Market

The Latin American Rigid Plastic Packaging market is poised for continued growth, driven by robust economic expansion, urbanization, and the increasing adoption of sustainable packaging solutions. Strategic investments in recycling infrastructure, innovation in materials and design, and collaboration across the value chain will unlock significant market potential and shape a more sustainable future for the industry. The market holds substantial growth opportunities for companies investing in sustainable materials, advanced technologies, and regional expansion strategies.

Latin America Rigid Plastic Packaging Market Segmentation

-

1. Resin

-

1.1. Polyethylene (PE)

- 1.1.1. LDPE and LLDPE

- 1.1.2. HDPE

- 1.2. Polyethylene terephthalate (PET)

- 1.3. Polypropylene (PP)

- 1.4. Polystyrene (PS) and Expanded polystyrene (EPS)

- 1.5. Polyvinyl chloride (PVC)

- 1.6. Other Re

-

1.1. Polyethylene (PE)

-

2. Product Type

- 2.1. Bottles and Jars

- 2.2. Trays and Containers

- 2.3. Caps and Closures

- 2.4. Intermediate Bulk Containers (IBCs)

- 2.5. Drums

- 2.6. Pallets

- 2.7. Other Pr

-

3. End-user Industry

-

3.1. Food**

- 3.1.1. Candy and Confectionery

- 3.1.2. Frozen Foods

- 3.1.3. Fresh Produce

- 3.1.4. Dairy Products

- 3.1.5. Dry Foods

- 3.1.6. Meat, Poultry, and Seafood

- 3.1.7. Pet Food

- 3.1.8. Other Fo

-

3.2. Foodservice**

- 3.2.1. Quick Service Restaurants (QSRs)

- 3.2.2. Full-Service Restaurants (FSRs)

- 3.2.3. Coffee and Snack Outlets

- 3.2.4. Retail Establishments

- 3.2.5. Institutional

- 3.2.6. Hospitality

- 3.2.7. Other Foodservice

- 3.3. Beverage

- 3.4. Healthcare

- 3.5. Cosmetics and Personal Care

- 3.6. Industri

- 3.7. Building and Construction

- 3.8. Automotive

- 3.9. Other En

-

3.1. Food**

Latin America Rigid Plastic Packaging Market Segmentation By Geography

-

1. Latin America

- 1.1. Brazil

- 1.2. Argentina

- 1.3. Chile

- 1.4. Colombia

- 1.5. Mexico

- 1.6. Peru

- 1.7. Venezuela

- 1.8. Ecuador

- 1.9. Bolivia

- 1.10. Paraguay

Latin America Rigid Plastic Packaging Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 3.47% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Rising Demand for Sustainable and Innovative Food Packaging Products; Increasing Consumption of Cosmetic Products

- 3.3. Market Restrains

- 3.3.1. Rising Demand for Sustainable and Innovative Food Packaging Products; Increasing Consumption of Cosmetic Products

- 3.4. Market Trends

- 3.4.1. Food and Beverage Occupies the Largest Market Share

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Latin America Rigid Plastic Packaging Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Resin

- 5.1.1. Polyethylene (PE)

- 5.1.1.1. LDPE and LLDPE

- 5.1.1.2. HDPE

- 5.1.2. Polyethylene terephthalate (PET)

- 5.1.3. Polypropylene (PP)

- 5.1.4. Polystyrene (PS) and Expanded polystyrene (EPS)

- 5.1.5. Polyvinyl chloride (PVC)

- 5.1.6. Other Re

- 5.1.1. Polyethylene (PE)

- 5.2. Market Analysis, Insights and Forecast - by Product Type

- 5.2.1. Bottles and Jars

- 5.2.2. Trays and Containers

- 5.2.3. Caps and Closures

- 5.2.4. Intermediate Bulk Containers (IBCs)

- 5.2.5. Drums

- 5.2.6. Pallets

- 5.2.7. Other Pr

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. Food**

- 5.3.1.1. Candy and Confectionery

- 5.3.1.2. Frozen Foods

- 5.3.1.3. Fresh Produce

- 5.3.1.4. Dairy Products

- 5.3.1.5. Dry Foods

- 5.3.1.6. Meat, Poultry, and Seafood

- 5.3.1.7. Pet Food

- 5.3.1.8. Other Fo

- 5.3.2. Foodservice**

- 5.3.2.1. Quick Service Restaurants (QSRs)

- 5.3.2.2. Full-Service Restaurants (FSRs)

- 5.3.2.3. Coffee and Snack Outlets

- 5.3.2.4. Retail Establishments

- 5.3.2.5. Institutional

- 5.3.2.6. Hospitality

- 5.3.2.7. Other Foodservice

- 5.3.3. Beverage

- 5.3.4. Healthcare

- 5.3.5. Cosmetics and Personal Care

- 5.3.6. Industri

- 5.3.7. Building and Construction

- 5.3.8. Automotive

- 5.3.9. Other En

- 5.3.1. Food**

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Latin America

- 5.1. Market Analysis, Insights and Forecast - by Resin

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 Amcor Group GmbH

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Berry Global Inc

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Alpla Werke Alwin Lehner GmbH & Co KG

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Silgan Holdings Inc

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Sealed Air Corporation

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Plastipak Holding Inc

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Sonoco Products Company

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Albea Group

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Greiner Packaging International GmbH

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 BERICAP Holding GmbH

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 Rioplastic

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.12 IPACKCHEM GROUP*List Not Exhaustive 7 2 Heat Map Analysis7 3 Competitor Analysis - Emerging vs Established Player

- 6.2.12.1. Overview

- 6.2.12.2. Products

- 6.2.12.3. SWOT Analysis

- 6.2.12.4. Recent Developments

- 6.2.12.5. Financials (Based on Availability)

- 6.2.1 Amcor Group GmbH

List of Figures

- Figure 1: Latin America Rigid Plastic Packaging Market Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Latin America Rigid Plastic Packaging Market Share (%) by Company 2024

List of Tables

- Table 1: Latin America Rigid Plastic Packaging Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Latin America Rigid Plastic Packaging Market Revenue Million Forecast, by Resin 2019 & 2032

- Table 3: Latin America Rigid Plastic Packaging Market Revenue Million Forecast, by Product Type 2019 & 2032

- Table 4: Latin America Rigid Plastic Packaging Market Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 5: Latin America Rigid Plastic Packaging Market Revenue Million Forecast, by Region 2019 & 2032

- Table 6: Latin America Rigid Plastic Packaging Market Revenue Million Forecast, by Resin 2019 & 2032

- Table 7: Latin America Rigid Plastic Packaging Market Revenue Million Forecast, by Product Type 2019 & 2032

- Table 8: Latin America Rigid Plastic Packaging Market Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 9: Latin America Rigid Plastic Packaging Market Revenue Million Forecast, by Country 2019 & 2032

- Table 10: Brazil Latin America Rigid Plastic Packaging Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Argentina Latin America Rigid Plastic Packaging Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Chile Latin America Rigid Plastic Packaging Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Colombia Latin America Rigid Plastic Packaging Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Mexico Latin America Rigid Plastic Packaging Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Peru Latin America Rigid Plastic Packaging Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Venezuela Latin America Rigid Plastic Packaging Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: Ecuador Latin America Rigid Plastic Packaging Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Bolivia Latin America Rigid Plastic Packaging Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Paraguay Latin America Rigid Plastic Packaging Market Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Latin America Rigid Plastic Packaging Market?

The projected CAGR is approximately 3.47%.

2. Which companies are prominent players in the Latin America Rigid Plastic Packaging Market?

Key companies in the market include Amcor Group GmbH, Berry Global Inc, Alpla Werke Alwin Lehner GmbH & Co KG, Silgan Holdings Inc, Sealed Air Corporation, Plastipak Holding Inc, Sonoco Products Company, Albea Group, Greiner Packaging International GmbH, BERICAP Holding GmbH, Rioplastic, IPACKCHEM GROUP*List Not Exhaustive 7 2 Heat Map Analysis7 3 Competitor Analysis - Emerging vs Established Player.

3. What are the main segments of the Latin America Rigid Plastic Packaging Market?

The market segments include Resin, Product Type, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Demand for Sustainable and Innovative Food Packaging Products; Increasing Consumption of Cosmetic Products.

6. What are the notable trends driving market growth?

Food and Beverage Occupies the Largest Market Share.

7. Are there any restraints impacting market growth?

Rising Demand for Sustainable and Innovative Food Packaging Products; Increasing Consumption of Cosmetic Products.

8. Can you provide examples of recent developments in the market?

June 2024: Method, a producer of environmentally conscious cleaning and personal care items, announced a significant shift: all its transparent plastic bottles are crafted entirely from 100% recycled coastal plastic. This move stems from a strategic alliance with SC Johnson and Plastic Bank. Since 2018, SC Johnson, in tandem with Plastic Bank, has overseen the inception of over 550 plastic collection sites, notably in nations like Indonesia, the Philippines, Thailand, and Brazil.August 2023: Indorama Ventures, a player in the production of recycled PET (rePET) resin, extended its recycling operations in Brazil by investing USD 20 million to modernize the facility's operations and purchase new equipment, including washing machines, to facilitate the removal of labels, the grinding of bottles in water, and a 70% reduction in water consumption.May 2023: Greenback claimed to have completed the recycling cycle with its first state-of-the-art plastic recycling facility, which was set to commence operations in collaboration with Nestle, located in the Mexican city of Cuautla. The recycling technology is designed to circularize non-recyclable plastics and trace the origin of the material.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Latin America Rigid Plastic Packaging Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Latin America Rigid Plastic Packaging Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Latin America Rigid Plastic Packaging Market?

To stay informed about further developments, trends, and reports in the Latin America Rigid Plastic Packaging Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence