Key Insights

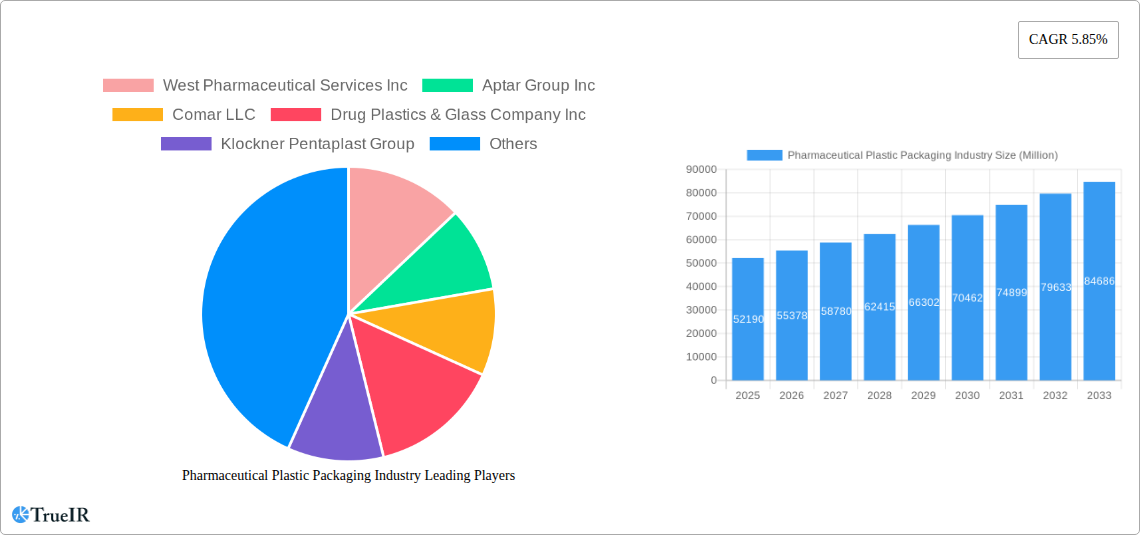

The pharmaceutical plastic packaging market, valued at $52.19 billion in 2025, is projected to experience robust growth, driven by several key factors. The increasing demand for pharmaceutical products globally, coupled with the rising preference for convenient and cost-effective plastic packaging solutions, is a major catalyst. Furthermore, advancements in plastic materials, offering enhanced barrier properties, improved durability, and tamper-evident features, are fueling market expansion. Stringent regulatory requirements regarding drug safety and packaging integrity are also driving innovation and adoption of sophisticated plastic packaging technologies. The market is segmented by product type (solid containers, dropper bottles, nasal spray bottles, etc.) and raw material (polypropylene, polyethylene terephthalate, etc.), with polypropylene and polyethylene likely holding significant market shares due to their cost-effectiveness and versatility. Growth is expected across all regions, with North America and Europe maintaining substantial market shares owing to established pharmaceutical industries and advanced healthcare infrastructure. However, the Asia-Pacific region is anticipated to witness the fastest growth rate, fueled by increasing pharmaceutical production and rising disposable incomes. Challenges include concerns about environmental sustainability and the need for recycling solutions, as well as fluctuations in raw material prices.

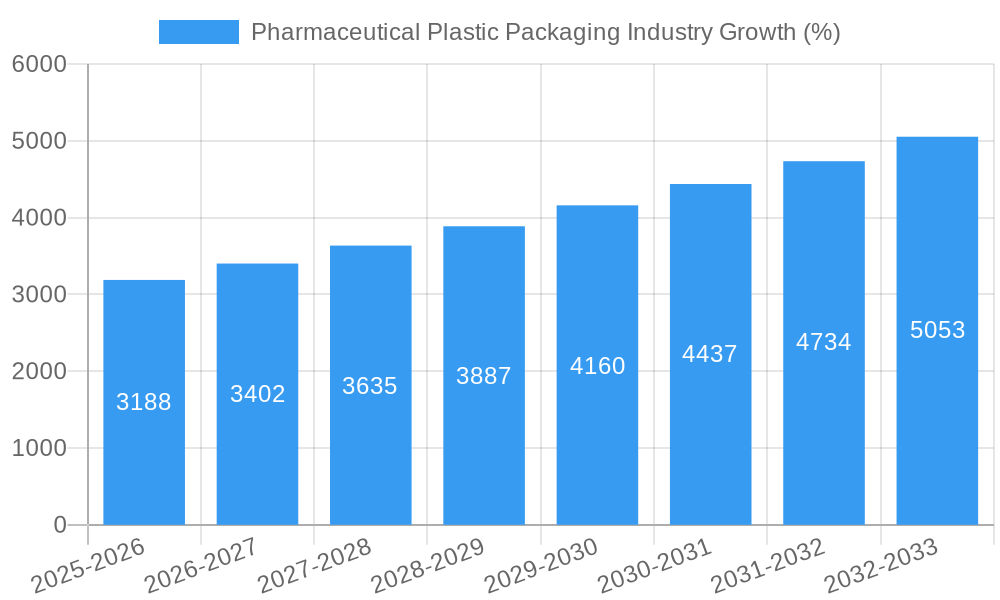

The forecast period (2025-2033) anticipates a continuation of this growth trajectory, with a Compound Annual Growth Rate (CAGR) of 5.85%. This sustained growth will be influenced by factors such as the development of innovative packaging solutions for specialized drug delivery systems (e.g., inhalers, injectables), increasing focus on patient convenience and safety, and ongoing efforts to improve the sustainability profile of pharmaceutical packaging. Competitive landscape analysis reveals that major players such as West Pharmaceutical Services Inc., Aptar Group Inc., and Amcor are strategically investing in research and development to maintain their market positions. These companies are focusing on developing sustainable and innovative packaging solutions, including recyclable and biodegradable options, to meet evolving consumer and regulatory demands. The market is expected to further consolidate as larger players acquire smaller companies to gain access to new technologies and expand their product portfolios.

Pharmaceutical Plastic Packaging Industry Report: 2019-2033

This comprehensive report provides a detailed analysis of the global Pharmaceutical Plastic Packaging market, offering invaluable insights for stakeholders across the value chain. From market sizing and segmentation to competitive dynamics and future trends, this report covers all crucial aspects of this dynamic industry, with a focus on driving strategic decision-making. The study period spans 2019-2033, with 2025 serving as the base and estimated year. The forecast period is 2025-2033, while the historical period covers 2019-2024. The market is valued at xx Million in 2025 and is projected to reach xx Million by 2033, exhibiting a CAGR of xx%.

Pharmaceutical Plastic Packaging Industry Market Structure & Competitive Landscape

The pharmaceutical plastic packaging market is characterized by a moderately concentrated structure, with several large multinational corporations and a significant number of smaller, regional players. The top 10 companies account for approximately xx% of the global market share in 2025. Key players such as West Pharmaceutical Services Inc, Aptar Group Inc, Comar LLC, Drug Plastics & Glass Company Inc, Klockner Pentaplast Group, Pretium Packaging LLC, Amcor Group GmbH, O Berk Company LLC, Gil Pack Group, Berry Global Inc, and Gerresheimer AG contribute significantly to the market's overall growth.

Market Concentration: The Herfindahl-Hirschman Index (HHI) is estimated at xx in 2025, suggesting a moderately concentrated market.

Innovation Drivers: Technological advancements in materials science (e.g., biodegradable plastics), packaging design (e.g., tamper-evident closures), and automation are driving innovation.

Regulatory Impacts: Stringent regulations concerning material safety, packaging integrity, and environmental sustainability significantly influence industry practices and investment decisions. Compliance costs are a significant factor.

Product Substitutes: While glass remains a significant competitor, the superior cost-effectiveness, lightweight nature, and versatility of plastic packaging have made it dominant in many pharmaceutical applications.

End-User Segmentation: The market is segmented by various end-users including pharmaceutical manufacturers, contract packagers, and hospitals.

M&A Trends: The pharmaceutical packaging industry has witnessed significant M&A activity in recent years, driven by a need for scale, diversification, and access to new technologies. The total value of M&A transactions in 2024 reached approximately xx Million.

Pharmaceutical Plastic Packaging Industry Market Trends & Opportunities

The pharmaceutical plastic packaging market is experiencing robust growth, driven by several key trends. The increasing prevalence of chronic diseases globally and the consequent rise in pharmaceutical consumption are primary growth drivers. Technological advancements, including the introduction of innovative materials and packaging designs, are further expanding market opportunities. The market has witnessed a significant shift towards sustainable and eco-friendly packaging solutions. This is fueled by growing environmental concerns and stricter regulations. Consumers are increasingly demanding sustainable packaging options, creating opportunities for companies that offer biodegradable and recyclable alternatives. The adoption of advanced technologies like smart packaging, which can enhance product traceability and tamper evidence, is also gaining traction. Competitive dynamics are largely characterized by product innovation, price competitiveness, and strategic partnerships. A significant opportunity lies in expanding into emerging markets where pharmaceutical consumption is rapidly increasing.

Dominant Markets & Segments in Pharmaceutical Plastic Packaging Industry

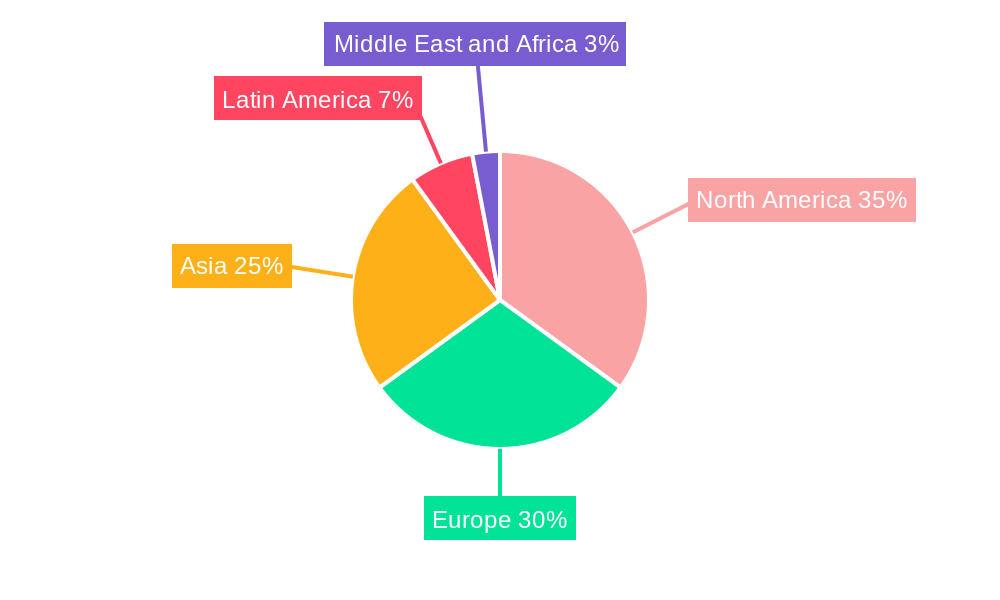

The North American and European regions currently dominate the global pharmaceutical plastic packaging market, driven by factors such as strong pharmaceutical industries, high per capita healthcare spending, and robust regulatory frameworks. However, significant growth potential exists in emerging markets such as Asia-Pacific and Latin America.

By Product Type:

- Solid Containers: Solid containers, including blister packs and bottles, constitute the largest segment owing to their widespread use in packaging tablets and capsules.

- Liquid Bottles: Liquid bottles represent a substantial segment due to the prevalence of liquid medications.

- Vials and Ampoules: The vials and ampoules segment benefits from demand for injectables and sterile formulations.

By Raw Material:

- Polypropylene (PP): PP’s versatility and chemical resistance makes it a leading raw material.

- Polyethylene Terephthalate (PET): PET's clarity and recyclability contribute to its market share.

- High-Density Polyethylene (HDPE): HDPE is favored for its durability and strength, often used in bottles for various applications.

Key Growth Drivers (by region):

- North America: Strong pharmaceutical industry, high healthcare expenditure, and robust regulatory frameworks drive market growth.

- Europe: Similar to North America, strong pharmaceutical industry, regulatory focus and stringent quality standards are key drivers.

- Asia-Pacific: Rapidly growing pharmaceutical industry, increasing healthcare expenditure, and a large population base.

Pharmaceutical Plastic Packaging Industry Product Analysis

Recent innovations focus on enhancing barrier properties, improving recyclability, and incorporating smart features into packaging. For example, the development of PETG Square Media Bottles by Savillex and the introduction of Tekni-Plex’s 30% post-consumer recycled content pharmaceutical-grade blister film are examples of significant progress in the industry. These advancements enhance product protection, sustainability, and patient convenience, thereby strengthening market competitiveness.

Key Drivers, Barriers & Challenges in Pharmaceutical Plastic Packaging Industry

Key Drivers:

- Increasing demand for pharmaceuticals globally.

- Growing preference for convenient and safe packaging.

- Rise in the adoption of advanced packaging technologies.

- Stringent regulatory requirements driving innovation in materials and designs.

Challenges:

- Fluctuating raw material prices.

- Stringent regulatory compliance requirements leading to increased costs.

- Growing environmental concerns and sustainability pressures.

- Intense competition among manufacturers. The market is estimated to be xx% fragmented, presenting substantial competitive pressures.

Growth Drivers in the Pharmaceutical Plastic Packaging Industry Market

The major drivers include the expanding pharmaceutical industry, the growing demand for convenient and tamper-evident packaging, the rise in technological advancements in materials and design, and the increasing focus on sustainable and environmentally friendly packaging solutions. Stringent government regulations also push innovation and improvement in the industry.

Challenges Impacting Pharmaceutical Plastic Packaging Industry Growth

Key challenges include the volatility of raw material prices, stringent regulatory compliance costs, environmental concerns and the pressure to adopt sustainable practices, and intense competition in a fragmented market.

Key Players Shaping the Pharmaceutical Plastic Packaging Industry Market

- West Pharmaceutical Services Inc

- Aptar Group Inc

- Comar LLC

- Drug Plastics & Glass Company Inc

- Klockner Pentaplast Group

- Pretium Packaging LLC

- Amcor Group GmbH

- O Berk Company LLC

- Gil Pack Group

- Berry Global Inc

- Gerresheimer AG

Significant Pharmaceutical Plastic Packaging Industry Industry Milestones

- January 2024: Savillex launched its Purillex brand PETG Square Media Bottles for critical life science applications, produced in an ISO Class 7 facility. This signifies a focus on high-quality, controlled manufacturing processes.

- January 2024: Tekni-Plex Inc. partnered with Alpek Polyester to introduce the world's first 30% post-consumer recycled content pharmaceutical-grade blister film, enhancing sustainability and meeting stringent regulatory standards. This is a significant step towards environmentally responsible packaging.

Future Outlook for Pharmaceutical Plastic Packaging Industry Market

The pharmaceutical plastic packaging market is poised for continued growth driven by technological advancements, increasing demand for sustainable solutions, and expansion into emerging markets. Opportunities exist in developing innovative materials, designing smart packaging solutions, and focusing on regulatory compliance. The market is projected to experience substantial growth over the forecast period, with significant opportunities for companies that can effectively navigate the regulatory landscape and meet the evolving needs of the pharmaceutical industry.

Pharmaceutical Plastic Packaging Industry Segmentation

-

1. Raw Material

- 1.1. Polypropylene (PP)

- 1.2. Polyethylene Terephthalate (PET)

- 1.3. Low Density Polyethylene (LDPE)

- 1.4. High Density Polyethylene (HDPE)

- 1.5. Other Raw Materials

-

2. Product Type

- 2.1. Solid Containers

- 2.2. Dropper Bottles

- 2.3. Nasal Spray Bottles

- 2.4. Liquid Bottles

- 2.5. Oral Care

- 2.6. Pouches

- 2.7. Vials and Ampoules

- 2.8. Cartridges

- 2.9. Syringes

- 2.10. Caps and Closures

- 2.11. Other Product Types

Pharmaceutical Plastic Packaging Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. United Kingdom

- 2.2. Germany

- 2.3. France

- 2.4. Spain

- 2.5. Italy

-

3. Asia

- 3.1. China

- 3.2. India

- 3.3. Japan

- 3.4. Australia and New Zealand

-

4. Latin America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Mexico

-

5. Middle East and Africa

- 5.1. United Arab Emirates

- 5.2. Saudi Arabia

- 5.3. South Africa

Pharmaceutical Plastic Packaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 5.85% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Demand for Rigid and Flexible Pharmaceutical Plastic Products; Development of Better and More Advanced Healthcare Infrastructure

- 3.3. Market Restrains

- 3.3.1. Regulations Restricting the Sales and Availability of Pharmaceutical Plastic Products; Fluctuations in Raw Material Cost

- 3.4. Market Trends

- 3.4.1. Increasing Adoption of Polyethylene Terephthalate (PET) Packaging for Pharmaceutical Products

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Pharmaceutical Plastic Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Raw Material

- 5.1.1. Polypropylene (PP)

- 5.1.2. Polyethylene Terephthalate (PET)

- 5.1.3. Low Density Polyethylene (LDPE)

- 5.1.4. High Density Polyethylene (HDPE)

- 5.1.5. Other Raw Materials

- 5.2. Market Analysis, Insights and Forecast - by Product Type

- 5.2.1. Solid Containers

- 5.2.2. Dropper Bottles

- 5.2.3. Nasal Spray Bottles

- 5.2.4. Liquid Bottles

- 5.2.5. Oral Care

- 5.2.6. Pouches

- 5.2.7. Vials and Ampoules

- 5.2.8. Cartridges

- 5.2.9. Syringes

- 5.2.10. Caps and Closures

- 5.2.11. Other Product Types

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia

- 5.3.4. Latin America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Raw Material

- 6. North America Pharmaceutical Plastic Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Raw Material

- 6.1.1. Polypropylene (PP)

- 6.1.2. Polyethylene Terephthalate (PET)

- 6.1.3. Low Density Polyethylene (LDPE)

- 6.1.4. High Density Polyethylene (HDPE)

- 6.1.5. Other Raw Materials

- 6.2. Market Analysis, Insights and Forecast - by Product Type

- 6.2.1. Solid Containers

- 6.2.2. Dropper Bottles

- 6.2.3. Nasal Spray Bottles

- 6.2.4. Liquid Bottles

- 6.2.5. Oral Care

- 6.2.6. Pouches

- 6.2.7. Vials and Ampoules

- 6.2.8. Cartridges

- 6.2.9. Syringes

- 6.2.10. Caps and Closures

- 6.2.11. Other Product Types

- 6.1. Market Analysis, Insights and Forecast - by Raw Material

- 7. Europe Pharmaceutical Plastic Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Raw Material

- 7.1.1. Polypropylene (PP)

- 7.1.2. Polyethylene Terephthalate (PET)

- 7.1.3. Low Density Polyethylene (LDPE)

- 7.1.4. High Density Polyethylene (HDPE)

- 7.1.5. Other Raw Materials

- 7.2. Market Analysis, Insights and Forecast - by Product Type

- 7.2.1. Solid Containers

- 7.2.2. Dropper Bottles

- 7.2.3. Nasal Spray Bottles

- 7.2.4. Liquid Bottles

- 7.2.5. Oral Care

- 7.2.6. Pouches

- 7.2.7. Vials and Ampoules

- 7.2.8. Cartridges

- 7.2.9. Syringes

- 7.2.10. Caps and Closures

- 7.2.11. Other Product Types

- 7.1. Market Analysis, Insights and Forecast - by Raw Material

- 8. Asia Pharmaceutical Plastic Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Raw Material

- 8.1.1. Polypropylene (PP)

- 8.1.2. Polyethylene Terephthalate (PET)

- 8.1.3. Low Density Polyethylene (LDPE)

- 8.1.4. High Density Polyethylene (HDPE)

- 8.1.5. Other Raw Materials

- 8.2. Market Analysis, Insights and Forecast - by Product Type

- 8.2.1. Solid Containers

- 8.2.2. Dropper Bottles

- 8.2.3. Nasal Spray Bottles

- 8.2.4. Liquid Bottles

- 8.2.5. Oral Care

- 8.2.6. Pouches

- 8.2.7. Vials and Ampoules

- 8.2.8. Cartridges

- 8.2.9. Syringes

- 8.2.10. Caps and Closures

- 8.2.11. Other Product Types

- 8.1. Market Analysis, Insights and Forecast - by Raw Material

- 9. Latin America Pharmaceutical Plastic Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Raw Material

- 9.1.1. Polypropylene (PP)

- 9.1.2. Polyethylene Terephthalate (PET)

- 9.1.3. Low Density Polyethylene (LDPE)

- 9.1.4. High Density Polyethylene (HDPE)

- 9.1.5. Other Raw Materials

- 9.2. Market Analysis, Insights and Forecast - by Product Type

- 9.2.1. Solid Containers

- 9.2.2. Dropper Bottles

- 9.2.3. Nasal Spray Bottles

- 9.2.4. Liquid Bottles

- 9.2.5. Oral Care

- 9.2.6. Pouches

- 9.2.7. Vials and Ampoules

- 9.2.8. Cartridges

- 9.2.9. Syringes

- 9.2.10. Caps and Closures

- 9.2.11. Other Product Types

- 9.1. Market Analysis, Insights and Forecast - by Raw Material

- 10. Middle East and Africa Pharmaceutical Plastic Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Raw Material

- 10.1.1. Polypropylene (PP)

- 10.1.2. Polyethylene Terephthalate (PET)

- 10.1.3. Low Density Polyethylene (LDPE)

- 10.1.4. High Density Polyethylene (HDPE)

- 10.1.5. Other Raw Materials

- 10.2. Market Analysis, Insights and Forecast - by Product Type

- 10.2.1. Solid Containers

- 10.2.2. Dropper Bottles

- 10.2.3. Nasal Spray Bottles

- 10.2.4. Liquid Bottles

- 10.2.5. Oral Care

- 10.2.6. Pouches

- 10.2.7. Vials and Ampoules

- 10.2.8. Cartridges

- 10.2.9. Syringes

- 10.2.10. Caps and Closures

- 10.2.11. Other Product Types

- 10.1. Market Analysis, Insights and Forecast - by Raw Material

- 11. North America Pharmaceutical Plastic Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 11.1.1 United States

- 11.1.2 Canada

- 12. Europe Pharmaceutical Plastic Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 12.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 12.1.1 United Kingdom

- 12.1.2 Germany

- 12.1.3 France

- 12.1.4 Spain

- 12.1.5 Italy

- 13. Asia Pharmaceutical Plastic Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 13.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 13.1.1 China

- 13.1.2 India

- 13.1.3 Japan

- 13.1.4 Australia and New Zealand

- 14. Latin America Pharmaceutical Plastic Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 14.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 14.1.1 Brazil

- 14.1.2 Argentina

- 14.1.3 Mexico

- 15. Middle East and Africa Pharmaceutical Plastic Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 15.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 15.1.1 United Arab Emirates

- 15.1.2 Saudi Arabia

- 15.1.3 South Africa

- 16. Competitive Analysis

- 16.1. Global Market Share Analysis 2024

- 16.2. Company Profiles

- 16.2.1 West Pharmaceutical Services Inc

- 16.2.1.1. Overview

- 16.2.1.2. Products

- 16.2.1.3. SWOT Analysis

- 16.2.1.4. Recent Developments

- 16.2.1.5. Financials (Based on Availability)

- 16.2.2 Aptar Group Inc

- 16.2.2.1. Overview

- 16.2.2.2. Products

- 16.2.2.3. SWOT Analysis

- 16.2.2.4. Recent Developments

- 16.2.2.5. Financials (Based on Availability)

- 16.2.3 Comar LLC

- 16.2.3.1. Overview

- 16.2.3.2. Products

- 16.2.3.3. SWOT Analysis

- 16.2.3.4. Recent Developments

- 16.2.3.5. Financials (Based on Availability)

- 16.2.4 Drug Plastics & Glass Company Inc

- 16.2.4.1. Overview

- 16.2.4.2. Products

- 16.2.4.3. SWOT Analysis

- 16.2.4.4. Recent Developments

- 16.2.4.5. Financials (Based on Availability)

- 16.2.5 Klockner Pentaplast Group

- 16.2.5.1. Overview

- 16.2.5.2. Products

- 16.2.5.3. SWOT Analysis

- 16.2.5.4. Recent Developments

- 16.2.5.5. Financials (Based on Availability)

- 16.2.6 Pretium Packaging LLC

- 16.2.6.1. Overview

- 16.2.6.2. Products

- 16.2.6.3. SWOT Analysis

- 16.2.6.4. Recent Developments

- 16.2.6.5. Financials (Based on Availability)

- 16.2.7 Amcor Group GmbH

- 16.2.7.1. Overview

- 16.2.7.2. Products

- 16.2.7.3. SWOT Analysis

- 16.2.7.4. Recent Developments

- 16.2.7.5. Financials (Based on Availability)

- 16.2.8 O Berk Company LLC

- 16.2.8.1. Overview

- 16.2.8.2. Products

- 16.2.8.3. SWOT Analysis

- 16.2.8.4. Recent Developments

- 16.2.8.5. Financials (Based on Availability)

- 16.2.9 Gil Pack Group

- 16.2.9.1. Overview

- 16.2.9.2. Products

- 16.2.9.3. SWOT Analysis

- 16.2.9.4. Recent Developments

- 16.2.9.5. Financials (Based on Availability)

- 16.2.10 Berry Global Inc

- 16.2.10.1. Overview

- 16.2.10.2. Products

- 16.2.10.3. SWOT Analysis

- 16.2.10.4. Recent Developments

- 16.2.10.5. Financials (Based on Availability)

- 16.2.11 Gerresheimer AG

- 16.2.11.1. Overview

- 16.2.11.2. Products

- 16.2.11.3. SWOT Analysis

- 16.2.11.4. Recent Developments

- 16.2.11.5. Financials (Based on Availability)

- 16.2.1 West Pharmaceutical Services Inc

List of Figures

- Figure 1: Global Pharmaceutical Plastic Packaging Industry Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: North America Pharmaceutical Plastic Packaging Industry Revenue (Million), by Country 2024 & 2032

- Figure 3: North America Pharmaceutical Plastic Packaging Industry Revenue Share (%), by Country 2024 & 2032

- Figure 4: Europe Pharmaceutical Plastic Packaging Industry Revenue (Million), by Country 2024 & 2032

- Figure 5: Europe Pharmaceutical Plastic Packaging Industry Revenue Share (%), by Country 2024 & 2032

- Figure 6: Asia Pharmaceutical Plastic Packaging Industry Revenue (Million), by Country 2024 & 2032

- Figure 7: Asia Pharmaceutical Plastic Packaging Industry Revenue Share (%), by Country 2024 & 2032

- Figure 8: Latin America Pharmaceutical Plastic Packaging Industry Revenue (Million), by Country 2024 & 2032

- Figure 9: Latin America Pharmaceutical Plastic Packaging Industry Revenue Share (%), by Country 2024 & 2032

- Figure 10: Middle East and Africa Pharmaceutical Plastic Packaging Industry Revenue (Million), by Country 2024 & 2032

- Figure 11: Middle East and Africa Pharmaceutical Plastic Packaging Industry Revenue Share (%), by Country 2024 & 2032

- Figure 12: North America Pharmaceutical Plastic Packaging Industry Revenue (Million), by Raw Material 2024 & 2032

- Figure 13: North America Pharmaceutical Plastic Packaging Industry Revenue Share (%), by Raw Material 2024 & 2032

- Figure 14: North America Pharmaceutical Plastic Packaging Industry Revenue (Million), by Product Type 2024 & 2032

- Figure 15: North America Pharmaceutical Plastic Packaging Industry Revenue Share (%), by Product Type 2024 & 2032

- Figure 16: North America Pharmaceutical Plastic Packaging Industry Revenue (Million), by Country 2024 & 2032

- Figure 17: North America Pharmaceutical Plastic Packaging Industry Revenue Share (%), by Country 2024 & 2032

- Figure 18: Europe Pharmaceutical Plastic Packaging Industry Revenue (Million), by Raw Material 2024 & 2032

- Figure 19: Europe Pharmaceutical Plastic Packaging Industry Revenue Share (%), by Raw Material 2024 & 2032

- Figure 20: Europe Pharmaceutical Plastic Packaging Industry Revenue (Million), by Product Type 2024 & 2032

- Figure 21: Europe Pharmaceutical Plastic Packaging Industry Revenue Share (%), by Product Type 2024 & 2032

- Figure 22: Europe Pharmaceutical Plastic Packaging Industry Revenue (Million), by Country 2024 & 2032

- Figure 23: Europe Pharmaceutical Plastic Packaging Industry Revenue Share (%), by Country 2024 & 2032

- Figure 24: Asia Pharmaceutical Plastic Packaging Industry Revenue (Million), by Raw Material 2024 & 2032

- Figure 25: Asia Pharmaceutical Plastic Packaging Industry Revenue Share (%), by Raw Material 2024 & 2032

- Figure 26: Asia Pharmaceutical Plastic Packaging Industry Revenue (Million), by Product Type 2024 & 2032

- Figure 27: Asia Pharmaceutical Plastic Packaging Industry Revenue Share (%), by Product Type 2024 & 2032

- Figure 28: Asia Pharmaceutical Plastic Packaging Industry Revenue (Million), by Country 2024 & 2032

- Figure 29: Asia Pharmaceutical Plastic Packaging Industry Revenue Share (%), by Country 2024 & 2032

- Figure 30: Latin America Pharmaceutical Plastic Packaging Industry Revenue (Million), by Raw Material 2024 & 2032

- Figure 31: Latin America Pharmaceutical Plastic Packaging Industry Revenue Share (%), by Raw Material 2024 & 2032

- Figure 32: Latin America Pharmaceutical Plastic Packaging Industry Revenue (Million), by Product Type 2024 & 2032

- Figure 33: Latin America Pharmaceutical Plastic Packaging Industry Revenue Share (%), by Product Type 2024 & 2032

- Figure 34: Latin America Pharmaceutical Plastic Packaging Industry Revenue (Million), by Country 2024 & 2032

- Figure 35: Latin America Pharmaceutical Plastic Packaging Industry Revenue Share (%), by Country 2024 & 2032

- Figure 36: Middle East and Africa Pharmaceutical Plastic Packaging Industry Revenue (Million), by Raw Material 2024 & 2032

- Figure 37: Middle East and Africa Pharmaceutical Plastic Packaging Industry Revenue Share (%), by Raw Material 2024 & 2032

- Figure 38: Middle East and Africa Pharmaceutical Plastic Packaging Industry Revenue (Million), by Product Type 2024 & 2032

- Figure 39: Middle East and Africa Pharmaceutical Plastic Packaging Industry Revenue Share (%), by Product Type 2024 & 2032

- Figure 40: Middle East and Africa Pharmaceutical Plastic Packaging Industry Revenue (Million), by Country 2024 & 2032

- Figure 41: Middle East and Africa Pharmaceutical Plastic Packaging Industry Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Pharmaceutical Plastic Packaging Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global Pharmaceutical Plastic Packaging Industry Revenue Million Forecast, by Raw Material 2019 & 2032

- Table 3: Global Pharmaceutical Plastic Packaging Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 4: Global Pharmaceutical Plastic Packaging Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Global Pharmaceutical Plastic Packaging Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: United States Pharmaceutical Plastic Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Canada Pharmaceutical Plastic Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Global Pharmaceutical Plastic Packaging Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 9: United Kingdom Pharmaceutical Plastic Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Germany Pharmaceutical Plastic Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: France Pharmaceutical Plastic Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Spain Pharmaceutical Plastic Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Italy Pharmaceutical Plastic Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Global Pharmaceutical Plastic Packaging Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 15: China Pharmaceutical Plastic Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: India Pharmaceutical Plastic Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: Japan Pharmaceutical Plastic Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Australia and New Zealand Pharmaceutical Plastic Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Global Pharmaceutical Plastic Packaging Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 20: Brazil Pharmaceutical Plastic Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Argentina Pharmaceutical Plastic Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Mexico Pharmaceutical Plastic Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Global Pharmaceutical Plastic Packaging Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 24: United Arab Emirates Pharmaceutical Plastic Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 25: Saudi Arabia Pharmaceutical Plastic Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: South Africa Pharmaceutical Plastic Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 27: Global Pharmaceutical Plastic Packaging Industry Revenue Million Forecast, by Raw Material 2019 & 2032

- Table 28: Global Pharmaceutical Plastic Packaging Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 29: Global Pharmaceutical Plastic Packaging Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 30: United States Pharmaceutical Plastic Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 31: Canada Pharmaceutical Plastic Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 32: Global Pharmaceutical Plastic Packaging Industry Revenue Million Forecast, by Raw Material 2019 & 2032

- Table 33: Global Pharmaceutical Plastic Packaging Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 34: Global Pharmaceutical Plastic Packaging Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 35: United Kingdom Pharmaceutical Plastic Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 36: Germany Pharmaceutical Plastic Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 37: France Pharmaceutical Plastic Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 38: Spain Pharmaceutical Plastic Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 39: Italy Pharmaceutical Plastic Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 40: Global Pharmaceutical Plastic Packaging Industry Revenue Million Forecast, by Raw Material 2019 & 2032

- Table 41: Global Pharmaceutical Plastic Packaging Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 42: Global Pharmaceutical Plastic Packaging Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 43: China Pharmaceutical Plastic Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 44: India Pharmaceutical Plastic Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 45: Japan Pharmaceutical Plastic Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 46: Australia and New Zealand Pharmaceutical Plastic Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 47: Global Pharmaceutical Plastic Packaging Industry Revenue Million Forecast, by Raw Material 2019 & 2032

- Table 48: Global Pharmaceutical Plastic Packaging Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 49: Global Pharmaceutical Plastic Packaging Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 50: Brazil Pharmaceutical Plastic Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 51: Argentina Pharmaceutical Plastic Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 52: Mexico Pharmaceutical Plastic Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 53: Global Pharmaceutical Plastic Packaging Industry Revenue Million Forecast, by Raw Material 2019 & 2032

- Table 54: Global Pharmaceutical Plastic Packaging Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 55: Global Pharmaceutical Plastic Packaging Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 56: United Arab Emirates Pharmaceutical Plastic Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 57: Saudi Arabia Pharmaceutical Plastic Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 58: South Africa Pharmaceutical Plastic Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Pharmaceutical Plastic Packaging Industry?

The projected CAGR is approximately 5.85%.

2. Which companies are prominent players in the Pharmaceutical Plastic Packaging Industry?

Key companies in the market include West Pharmaceutical Services Inc, Aptar Group Inc, Comar LLC, Drug Plastics & Glass Company Inc, Klockner Pentaplast Group, Pretium Packaging LLC, Amcor Group GmbH, O Berk Company LLC, Gil Pack Group, Berry Global Inc, Gerresheimer AG.

3. What are the main segments of the Pharmaceutical Plastic Packaging Industry?

The market segments include Raw Material, Product Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 52.19 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand for Rigid and Flexible Pharmaceutical Plastic Products; Development of Better and More Advanced Healthcare Infrastructure.

6. What are the notable trends driving market growth?

Increasing Adoption of Polyethylene Terephthalate (PET) Packaging for Pharmaceutical Products.

7. Are there any restraints impacting market growth?

Regulations Restricting the Sales and Availability of Pharmaceutical Plastic Products; Fluctuations in Raw Material Cost.

8. Can you provide examples of recent developments in the market?

January 2024: Savillex, a container and containment solutions provider, has unveiled its latest product line under the Purillex brand PETG Square Media Bottles. These bottles are designed for critical life sciences applications and are produced in Savillex's ISO Class 7 facility in the United States.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Pharmaceutical Plastic Packaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Pharmaceutical Plastic Packaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Pharmaceutical Plastic Packaging Industry?

To stay informed about further developments, trends, and reports in the Pharmaceutical Plastic Packaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence