Key Insights

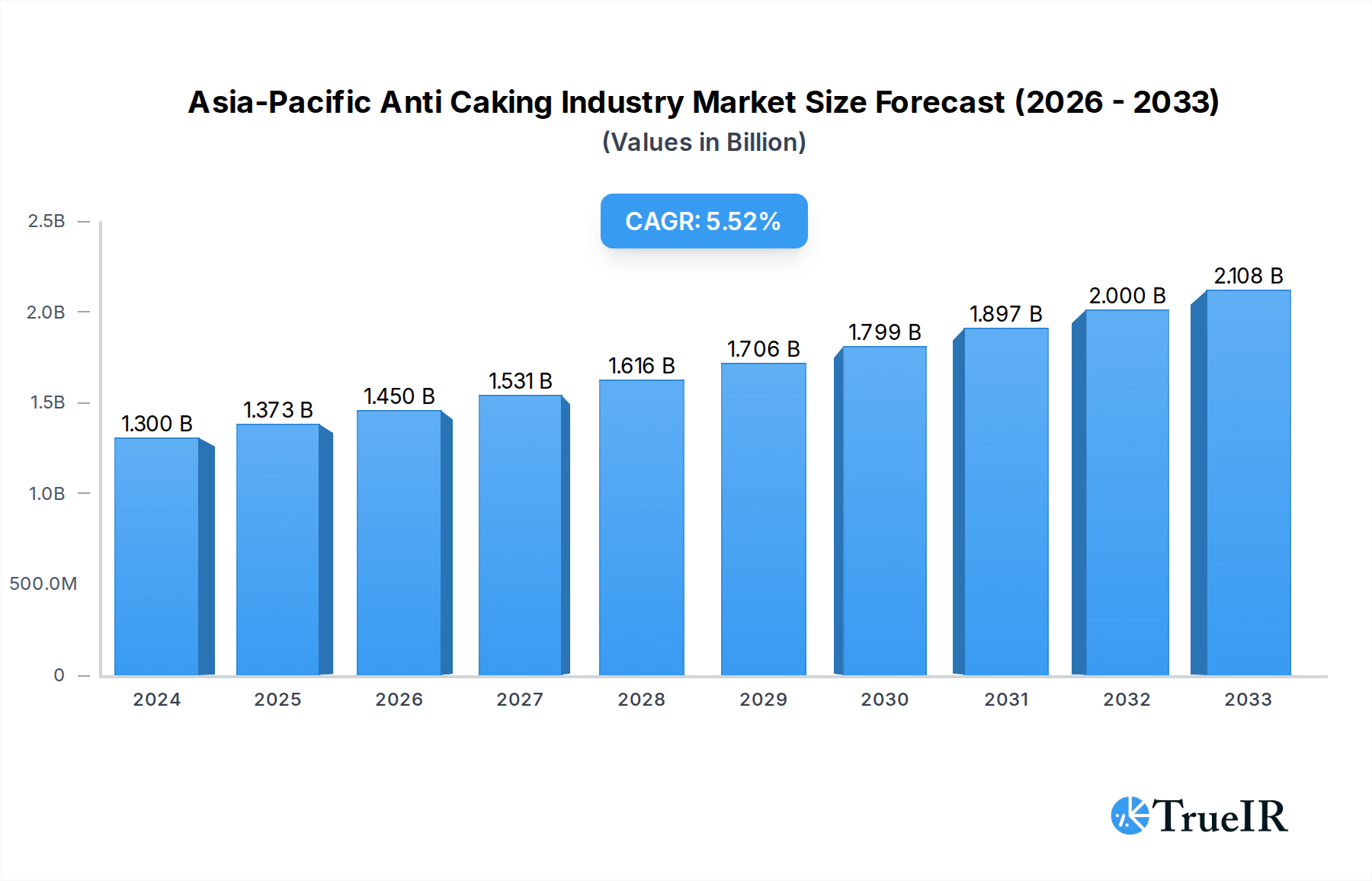

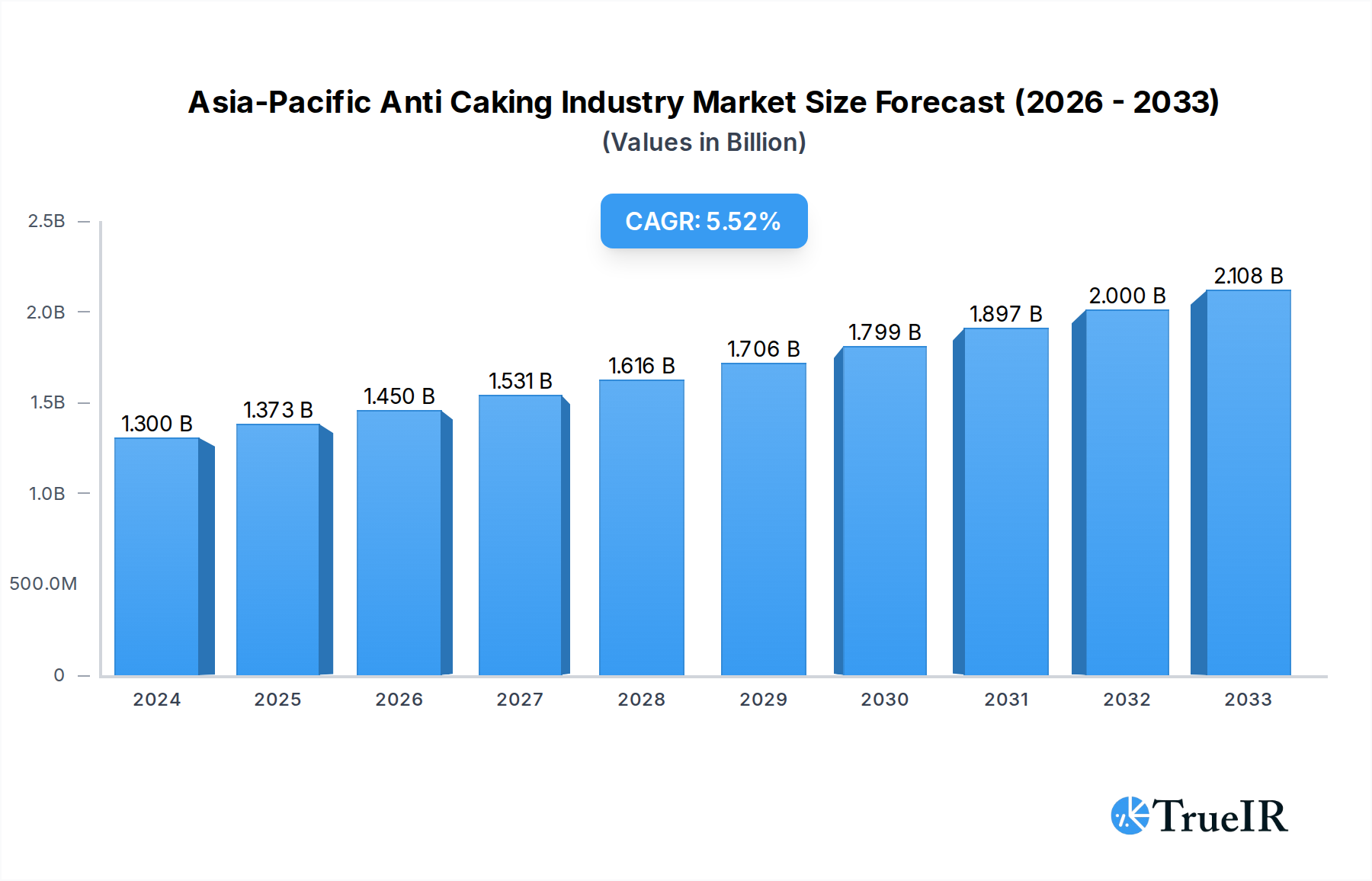

The Asia-Pacific Anti-Caking Agents market is poised for robust expansion, projected to reach approximately USD 1.3 billion in 2024 and grow at a significant Compound Annual Growth Rate (CAGR) of 5.6% through the forecast period of 2025-2033. This upward trajectory is primarily fueled by the increasing demand from the food and beverage sector, driven by processed food consumption and the growing popularity of convenience foods across the region. Key applications within this segment include bakery products, dairy products, soups & sauces, and beverages. The cosmetic and personal care industry also presents a notable growth avenue, as anti-caking agents enhance product texture and shelf-life. Furthermore, the animal feed segment is contributing to market expansion by improving feed flowability and preventing clumping. Emerging economies like India and the rest of the Asia-Pacific region are expected to be significant growth engines due to rapid industrialization and rising disposable incomes.

Asia-Pacific Anti Caking Industry Market Size (In Billion)

While the market is experiencing strong tailwinds, certain factors could influence its growth trajectory. The escalating cost of raw materials for anti-caking agents and stringent regulatory frameworks concerning their usage in food products could pose challenges. However, technological advancements in developing novel and sustainable anti-caking solutions, coupled with an increasing consumer preference for premium and functional food products, are expected to mitigate these restraints. Key players are actively engaged in research and development to innovate their product offerings and expand their market reach. The dominance of calcium and sodium compounds as primary types of anti-caking agents is anticipated to continue, although magnesium compounds and other specialized variants are gaining traction, particularly in niche applications.

Asia-Pacific Anti Caking Industry Company Market Share

Asia-Pacific Anti Caking Industry Market: A Comprehensive Forecast & Analysis (2019-2033)

This report provides an in-depth analysis of the Asia-Pacific Anti Caking Industry, projecting a robust growth trajectory fueled by increasing demand across diverse sectors. The study encompasses a detailed examination of market size, segmentation, competitive landscape, emerging trends, key drivers, challenges, and future outlook. With a focus on high-volume keywords and industry-specific terminology, this report is optimized for SEO and designed to deliver actionable insights for stakeholders.

Asia-Pacific Anti Caking Industry Market Structure & Competitive Landscape

The Asia-Pacific Anti Caking Industry is characterized by a moderately concentrated market structure, with a few dominant players holding significant market share. Innovation drivers are primarily focused on developing advanced anti-caking agents with enhanced efficacy, broader application compatibility, and improved sustainability profiles. Regulatory impacts, while varied across different countries, are generally geared towards ensuring product safety and efficacy, influencing formulation choices and market access. Product substitutes, though present in some niche applications, are largely unable to replicate the performance and cost-effectiveness of specialized anti-caking agents. End-user segmentation reveals a strong reliance on the Food and Beverage sector, followed by Cosmetics and Personal Care, and Feed industries. Mergers and acquisitions (M&A) trends, though not extensively documented with quantifiable volumes in this region, indicate strategic consolidation aimed at expanding product portfolios and geographic reach. The market is driven by continuous product development to meet specific end-use requirements and evolving consumer preferences for processed and packaged goods. The estimated market concentration ratio for the top five players is approximately 55% in 2025. M&A activities are predicted to increase by 15% in volume during the forecast period, driven by the need for market expansion and technology acquisition.

Asia-Pacific Anti Caking Industry Market Trends & Opportunities

The Asia-Pacific Anti Caking Industry is poised for significant expansion, driven by a confluence of evolving consumer demands, technological advancements, and favorable economic conditions. The market size is projected to reach an estimated $5.5 billion by 2025, with a Compound Annual Growth Rate (CAGR) of approximately 6.8% during the forecast period of 2025–2033. This growth is underpinned by the burgeoning food processing and packaging industry across the region, particularly in rapidly developing economies like China and India. Technological shifts are leading to the development of novel, high-performance anti-caking agents, including nano-encapsulated forms and naturally derived alternatives, offering improved functionality and addressing concerns around ingredient processing and shelf-life extension. Consumer preferences are increasingly shifting towards convenience foods, ready-to-eat meals, and processed snacks, all of which heavily rely on anti-caking agents to maintain product quality and appearance. The cosmetic and personal care sector is also witnessing a surge in demand for anti-caking agents in powdered formulations, driven by a growing middle class with increased disposable income and a preference for premium beauty products. The feed industry, crucial for livestock health and productivity, presents another substantial opportunity as advancements in animal nutrition necessitate improved feed flowability. Furthermore, the growing emphasis on sustainable and clean-label ingredients is creating a market opportunity for naturally sourced and biodegradable anti-caking agents. The competitive dynamics are intensifying, with both established global players and emerging regional manufacturers vying for market share through product differentiation, strategic partnerships, and aggressive expansion strategies. The increasing urbanization and rise in e-commerce for food and consumer goods further amplify the need for effective anti-caking solutions that ensure product integrity during transit and storage. The market penetration rate of anti-caking agents in the food and beverage sector is estimated to be around 85% in 2025, with significant room for growth in emerging markets and specialized product categories.

Dominant Markets & Segments in Asia-Pacific Anti Caking Industry

The Asia-Pacific Anti Caking Industry exhibits clear leadership in specific geographic and application segments, driven by distinct market dynamics and consumer behaviors.

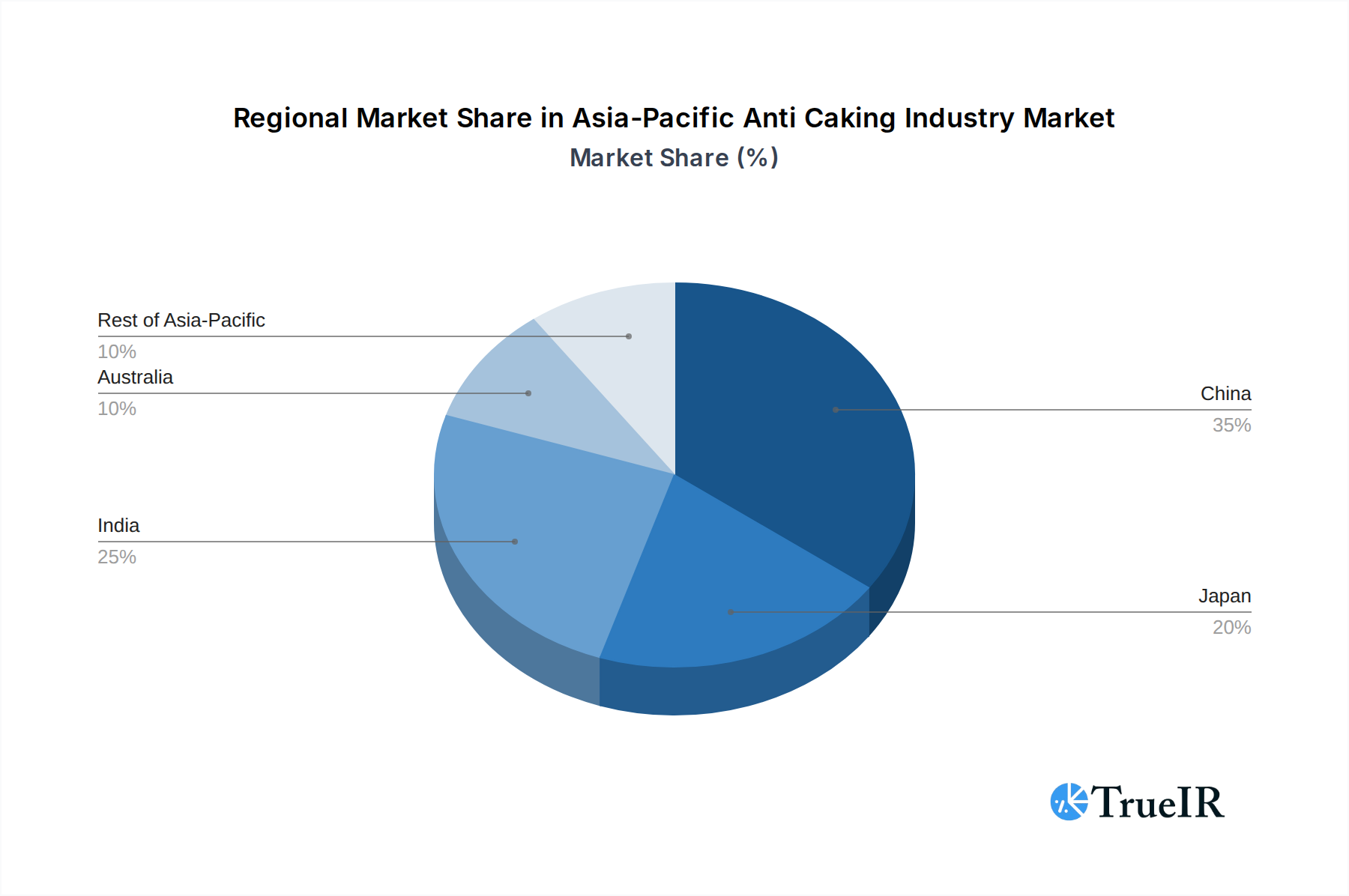

Dominant Geography: China

- China stands as the largest and fastest-growing market for anti-caking agents in the Asia-Pacific region. This dominance is fueled by its massive population, rapid industrialization, and a burgeoning processed food and beverage sector.

- Government initiatives promoting food safety standards and agricultural modernization have further bolstered the demand for high-quality anti-caking agents in food production and animal feed.

- Infrastructure development, including enhanced logistics and cold chain capabilities, supports the wider distribution and adoption of packaged goods, necessitating effective anti-caking solutions.

- The sheer scale of manufacturing in China, from food products to cosmetics, creates an immense and continuous demand for anti-caking additives.

Dominant Application Segment: Food and Beverage

- Within the Food and Beverage sector, Bakery Products represent a significant driver of anti-caking agent consumption. The increasing popularity of pre-packaged baked goods, bread mixes, and confectioneries directly correlates with the need for agents that prevent clumping and ensure consistent texture and flowability.

- Dairy Products, particularly powdered milk, cheese powders, and infant formulas, rely heavily on anti-caking agents to maintain their free-flowing properties and prevent moisture absorption.

- Soups & Sauces in powdered and granular forms require anti-caking agents to ensure easy reconstitution and prevent lump formation.

- Beverages, especially powdered drink mixes and instant coffee, benefit from anti-caking agents that facilitate dissolution and maintain a smooth texture.

- The "Others" sub-segment within Food and Beverage, encompassing spices, seasonings, and convenience food ingredients, also demonstrates substantial demand.

Dominant Type: Calcium Compounds

- Calcium compounds, particularly calcium silicate and calcium carbonate, are widely favored due to their cost-effectiveness, efficacy, and broad regulatory approval across many food applications in the Asia-Pacific region. Their ability to absorb moisture and provide a physical barrier makes them highly effective in preventing caking in a variety of powdered food products. The projected market share for Calcium Compounds is expected to be around 35% of the total market in 2025.

The growth in these dominant segments is further propelled by increasing disposable incomes, changing dietary habits, and a growing preference for convenience and ready-to-use products, all of which directly increase the consumption of processed and powdered goods requiring anti-caking solutions.

Asia-Pacific Anti Caking Industry Product Analysis

Innovations in the Asia-Pacific Anti Caking Industry are centered on developing advanced agents with superior moisture control and enhanced dispersibility. Product developments are focusing on natural and clean-label alternatives to synthetic compounds, catering to growing consumer demand for healthier and more sustainable ingredients. Key applications span from preventing clumping in food powders, ensuring free-flow in cosmetic formulations, to improving the handling of animal feed. Competitive advantages are gained through superior particle engineering, targeted application specific formulations, and compliance with diverse regional food safety regulations.

Key Drivers, Barriers & Challenges in Asia-Pacific Anti Caking Industry

Key Drivers: The Asia-Pacific Anti Caking Industry is propelled by several key factors. Technological advancements in ingredient processing and packaging are creating a sustained demand for high-performance anti-caking agents. The burgeoning food and beverage sector, driven by urbanization and changing consumer lifestyles, is a primary growth catalyst. Growing disposable incomes are leading to increased consumption of convenience foods and premium personal care products, both of which rely on anti-caking agents. Favorable government policies supporting food safety and agricultural modernization further stimulate market growth.

Barriers & Challenges: Despite robust growth, the industry faces challenges. Supply chain complexities, particularly in managing raw material sourcing and distribution across a vast and diverse region, can lead to cost fluctuations and availability issues. Stringent and varying regulatory hurdles across different countries necessitate extensive product testing and compliance efforts, increasing operational costs. Intense competitive pressures from both global and local players can lead to price erosion and margin compression. The rising cost of raw materials, such as silica and calcium compounds, also poses a significant challenge to profitability.

Growth Drivers in the Asia-Pacific Anti Caking Industry Market

Key growth drivers in the Asia-Pacific Anti Caking Industry market include the escalating demand for processed and convenience foods, driven by rapid urbanization and changing consumer lifestyles. Technological advancements in food processing and packaging, necessitating improved ingredient flowability and stability, are crucial. The expanding cosmetics and personal care sector, with a growing array of powdered products, also fuels demand. Furthermore, supportive government policies aimed at enhancing food safety standards and promoting agricultural productivity contribute significantly to market expansion.

Challenges Impacting Asia-Pacific Anti Caking Industry Growth

Challenges impacting Asia-Pacific Anti Caking Industry growth include the complex and often fragmented regulatory landscape across different nations, requiring substantial compliance efforts and potentially hindering market entry. Volatile raw material prices and availability, influenced by global supply chain dynamics and geopolitical factors, can impact production costs and profitability. Intense competition among established players and emerging regional manufacturers can lead to price pressures and necessitate continuous innovation to maintain market share. Supply chain disruptions, exacerbated by logistical complexities within the region, can also impede timely delivery and increase operational expenses.

Key Players Shaping the Asia-Pacific Anti Caking Industry Market

- AGC Chemicals

- Merck KGaA

- Kao Corporation

- Roquette Freres

- Evonik Industries AG

- BASF SE

Significant Asia-Pacific Anti Caking Industry Industry Milestones

- 2019: Increased focus on sustainable and naturally derived anti-caking agents begins to gain traction among consumers.

- 2020: COVID-19 pandemic leads to a surge in demand for packaged and convenience foods, boosting the anti-caking market.

- 2021: Significant investments made by key players in R&D for novel anti-caking technologies in China and India.

- 2022: Introduction of advanced nano-silica based anti-caking agents with superior performance characteristics.

- 2023: Growing adoption of anti-caking agents in the animal feed industry for improved feed quality and animal health.

- 2024: Strategic partnerships and collaborations emerge to expand product portfolios and market reach across Southeast Asia.

Future Outlook for Asia-Pacific Anti Caking Industry Market

The future outlook for the Asia-Pacific Anti Caking Industry remains exceptionally promising, driven by continued consumer demand for processed foods, evolving cosmetic formulations, and advancements in the feed sector. Strategic opportunities lie in the development of bio-based and biodegradable anti-caking agents to meet sustainability mandates. Expansion into emerging markets within Southeast Asia and Oceania presents substantial growth potential. Innovation in personalized nutrition and specialized dietary supplements will also create niche markets for highly functional anti-caking solutions. The market is expected to witness sustained growth, fueled by innovation and a deepening understanding of its critical role in product quality and consumer satisfaction.

Asia-Pacific Anti Caking Industry Segmentation

-

1. Type

- 1.1. Calcium Compounds

- 1.2. Sodium Compounds

- 1.3. Magnesium Compounds

- 1.4. Others

-

2. Application

-

2.1. Food and Beverage

- 2.1.1. Bakery Products

- 2.1.2. Dairy Products

- 2.1.3. Soups & Sauces

- 2.1.4. Beverages

- 2.1.5. Others

- 2.2. Cosmetic and Personal Care

- 2.3. Feed

-

2.1. Food and Beverage

-

3. Geography

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. Rest of Asia-Pacific

Asia-Pacific Anti Caking Industry Segmentation By Geography

- 1. China

- 2. Japan

- 3. India

- 4. Australia

- 5. Rest of Asia Pacific

Asia-Pacific Anti Caking Industry Regional Market Share

Geographic Coverage of Asia-Pacific Anti Caking Industry

Asia-Pacific Anti Caking Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Calcium Compounds

- 5.1.2. Sodium Compounds

- 5.1.3. Magnesium Compounds

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Food and Beverage

- 5.2.1.1. Bakery Products

- 5.2.1.2. Dairy Products

- 5.2.1.3. Soups & Sauces

- 5.2.1.4. Beverages

- 5.2.1.5. Others

- 5.2.2. Cosmetic and Personal Care

- 5.2.3. Feed

- 5.2.1. Food and Beverage

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. China

- 5.3.2. Japan

- 5.3.3. India

- 5.3.4. Australia

- 5.3.5. Rest of Asia-Pacific

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. China

- 5.4.2. Japan

- 5.4.3. India

- 5.4.4. Australia

- 5.4.5. Rest of Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Asia-Pacific Anti Caking Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Calcium Compounds

- 6.1.2. Sodium Compounds

- 6.1.3. Magnesium Compounds

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Food and Beverage

- 6.2.1.1. Bakery Products

- 6.2.1.2. Dairy Products

- 6.2.1.3. Soups & Sauces

- 6.2.1.4. Beverages

- 6.2.1.5. Others

- 6.2.2. Cosmetic and Personal Care

- 6.2.3. Feed

- 6.2.1. Food and Beverage

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. China

- 6.3.2. Japan

- 6.3.3. India

- 6.3.4. Australia

- 6.3.5. Rest of Asia-Pacific

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. China Asia-Pacific Anti Caking Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Calcium Compounds

- 7.1.2. Sodium Compounds

- 7.1.3. Magnesium Compounds

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Food and Beverage

- 7.2.1.1. Bakery Products

- 7.2.1.2. Dairy Products

- 7.2.1.3. Soups & Sauces

- 7.2.1.4. Beverages

- 7.2.1.5. Others

- 7.2.2. Cosmetic and Personal Care

- 7.2.3. Feed

- 7.2.1. Food and Beverage

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. China

- 7.3.2. Japan

- 7.3.3. India

- 7.3.4. Australia

- 7.3.5. Rest of Asia-Pacific

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Japan Asia-Pacific Anti Caking Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Calcium Compounds

- 8.1.2. Sodium Compounds

- 8.1.3. Magnesium Compounds

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Food and Beverage

- 8.2.1.1. Bakery Products

- 8.2.1.2. Dairy Products

- 8.2.1.3. Soups & Sauces

- 8.2.1.4. Beverages

- 8.2.1.5. Others

- 8.2.2. Cosmetic and Personal Care

- 8.2.3. Feed

- 8.2.1. Food and Beverage

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. China

- 8.3.2. Japan

- 8.3.3. India

- 8.3.4. Australia

- 8.3.5. Rest of Asia-Pacific

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. India Asia-Pacific Anti Caking Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Calcium Compounds

- 9.1.2. Sodium Compounds

- 9.1.3. Magnesium Compounds

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Food and Beverage

- 9.2.1.1. Bakery Products

- 9.2.1.2. Dairy Products

- 9.2.1.3. Soups & Sauces

- 9.2.1.4. Beverages

- 9.2.1.5. Others

- 9.2.2. Cosmetic and Personal Care

- 9.2.3. Feed

- 9.2.1. Food and Beverage

- 9.3. Market Analysis, Insights and Forecast - by Geography

- 9.3.1. China

- 9.3.2. Japan

- 9.3.3. India

- 9.3.4. Australia

- 9.3.5. Rest of Asia-Pacific

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Australia Asia-Pacific Anti Caking Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Calcium Compounds

- 10.1.2. Sodium Compounds

- 10.1.3. Magnesium Compounds

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Food and Beverage

- 10.2.1.1. Bakery Products

- 10.2.1.2. Dairy Products

- 10.2.1.3. Soups & Sauces

- 10.2.1.4. Beverages

- 10.2.1.5. Others

- 10.2.2. Cosmetic and Personal Care

- 10.2.3. Feed

- 10.2.1. Food and Beverage

- 10.3. Market Analysis, Insights and Forecast - by Geography

- 10.3.1. China

- 10.3.2. Japan

- 10.3.3. India

- 10.3.4. Australia

- 10.3.5. Rest of Asia-Pacific

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Rest of Asia Pacific Asia-Pacific Anti Caking Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Calcium Compounds

- 11.1.2. Sodium Compounds

- 11.1.3. Magnesium Compounds

- 11.1.4. Others

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Food and Beverage

- 11.2.1.1. Bakery Products

- 11.2.1.2. Dairy Products

- 11.2.1.3. Soups & Sauces

- 11.2.1.4. Beverages

- 11.2.1.5. Others

- 11.2.2. Cosmetic and Personal Care

- 11.2.3. Feed

- 11.2.1. Food and Beverage

- 11.3. Market Analysis, Insights and Forecast - by Geography

- 11.3.1. China

- 11.3.2. Japan

- 11.3.3. India

- 11.3.4. Australia

- 11.3.5. Rest of Asia-Pacific

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 AGC Chemicals

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Merck KGaA

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Kao Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Roquette Freres

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Evonik Industries AG*List Not Exhaustive

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 BASF SE

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.1 AGC Chemicals

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Asia-Pacific Anti Caking Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Asia-Pacific Anti Caking Industry Share (%) by Company 2025

List of Tables

- Table 1: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 3: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 4: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 7: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 8: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 10: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 12: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 14: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 15: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 16: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 17: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 19: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 20: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 21: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 22: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 23: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 24: Asia-Pacific Anti Caking Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Asia-Pacific Anti Caking Industry?

The projected CAGR is approximately 5.6%.

2. Which companies are prominent players in the Asia-Pacific Anti Caking Industry?

Key companies in the market include AGC Chemicals, Merck KGaA, Kao Corporation, Roquette Freres, Evonik Industries AG*List Not Exhaustive, BASF SE.

3. What are the main segments of the Asia-Pacific Anti Caking Industry?

The market segments include Type, Application, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.3 billion as of 2022.

5. What are some drivers contributing to market growth?

Innovation in Vanillin Synthesis; Diverse Functionality of Vanillin In End-use Industries.

6. What are the notable trends driving market growth?

Growing Demand in Bakery Industry.

7. Are there any restraints impacting market growth?

Supply Chain Variability Impacting Vanilla Bean Availability For Flavor Production.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Asia-Pacific Anti Caking Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Asia-Pacific Anti Caking Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Asia-Pacific Anti Caking Industry?

To stay informed about further developments, trends, and reports in the Asia-Pacific Anti Caking Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence