Key Insights

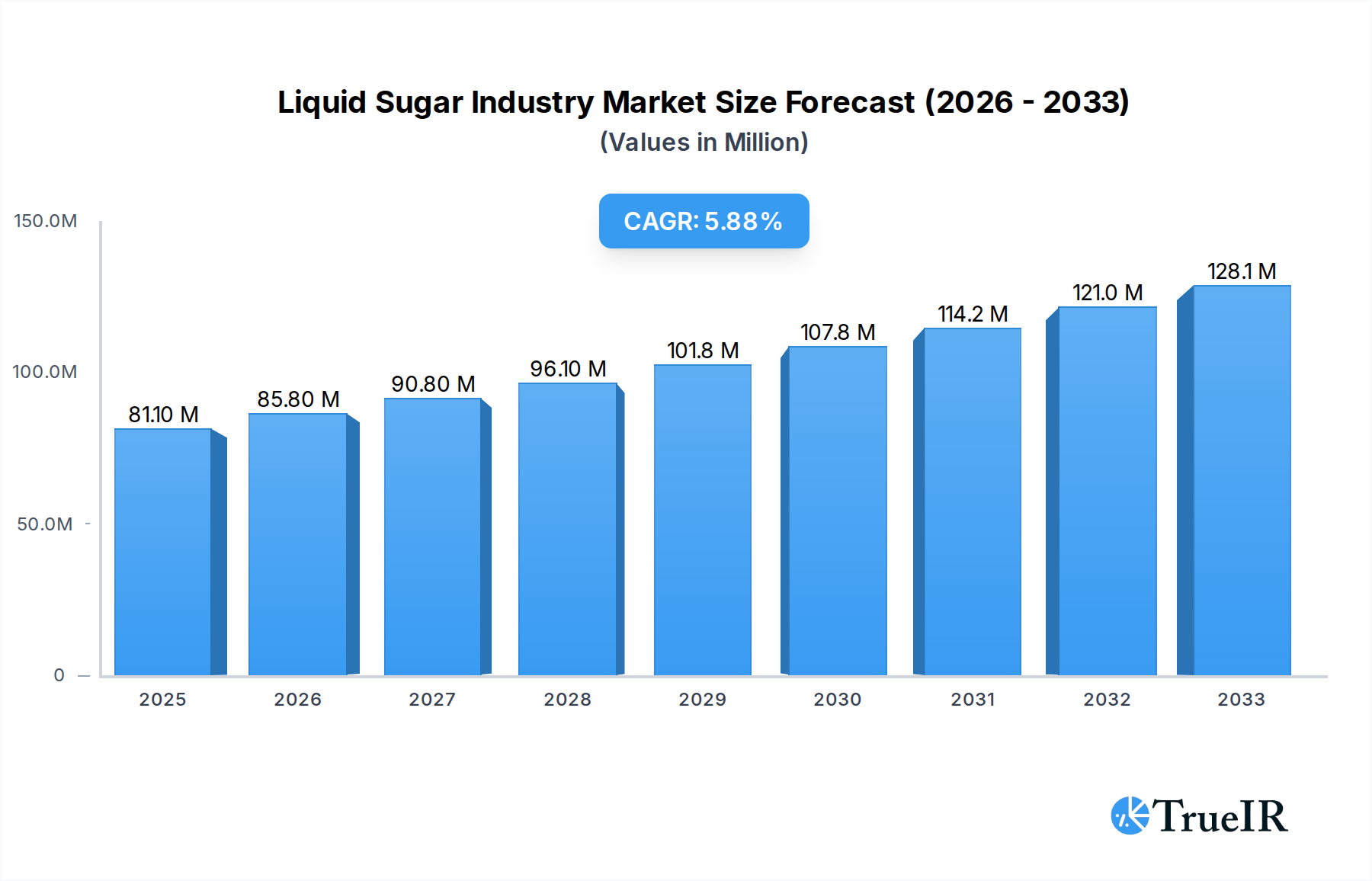

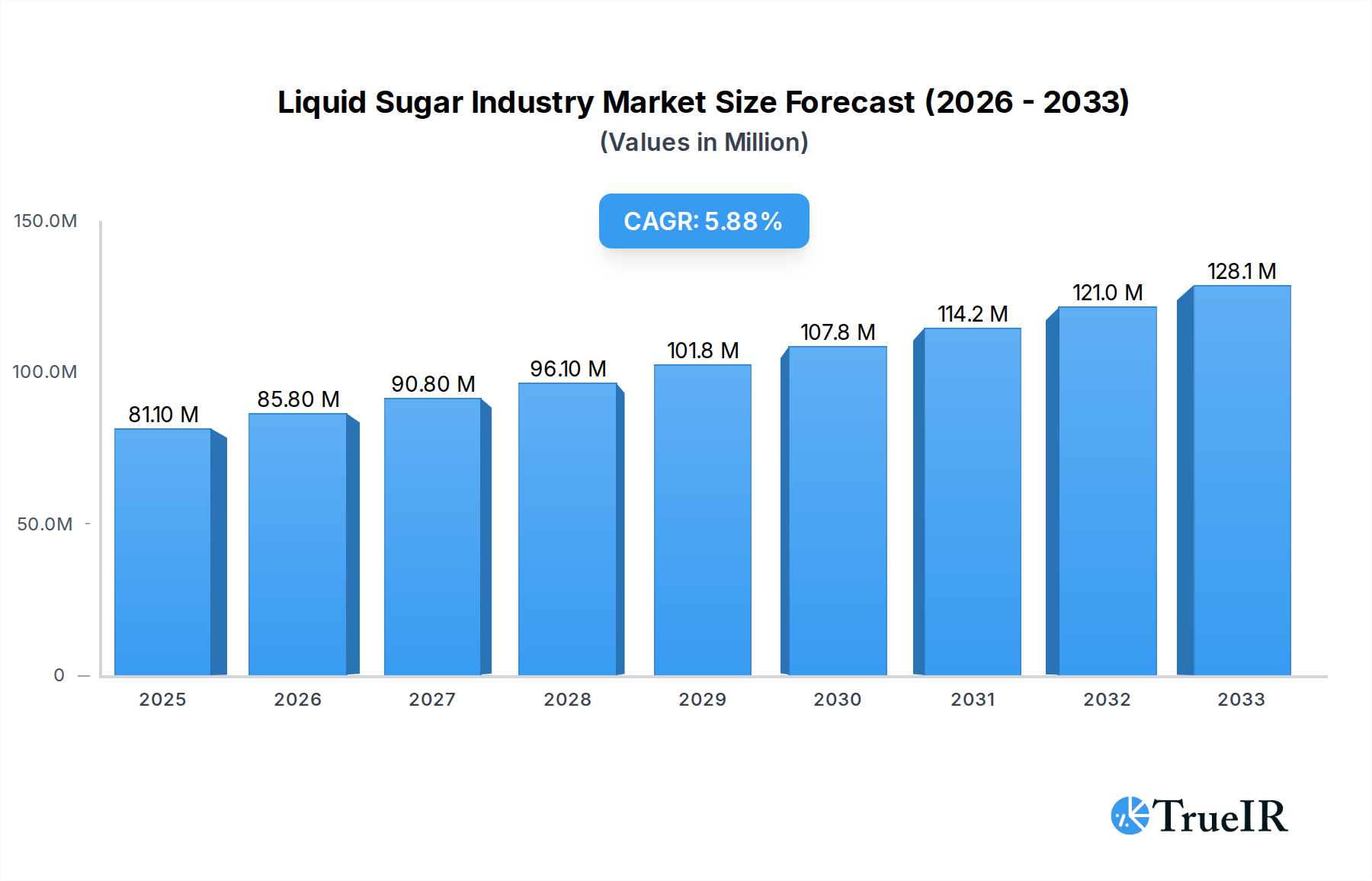

The global liquid sugar market is poised for significant expansion, projected to reach $81.1 million in 2025 and grow at a robust CAGR of 5.8% through 2033. This upward trajectory is underpinned by several powerful drivers, primarily the increasing consumer preference for convenience and the growing demand for processed foods and beverages. Liquid sugar’s inherent advantages, such as easier handling, precise dosing, and extended shelf life compared to granulated sugar, make it an attractive ingredient for manufacturers across various sectors. The confectionery and bakery industries, in particular, are major consumers, leveraging liquid sugar for consistent texture and quality in their products. Furthermore, the burgeoning demand for beverages, from soft drinks to functional drinks and dairy-based products, also significantly contributes to the market’s growth. The rise in the baby food segment, demanding safe and easily incorporated ingredients, further bolsters this trend.

Liquid Sugar Industry Market Size (In Million)

Emerging trends are also shaping the liquid sugar landscape. The increasing emphasis on health and wellness is fueling a demand for organic and naturally derived liquid sugars, signaling a shift towards premium and sustainable options. While the market demonstrates strong growth potential, certain restraints could influence its pace. Volatility in raw material prices, particularly for sugarcane and sugar beets, can impact production costs and pricing strategies. Moreover, evolving regulatory frameworks concerning sugar consumption and labeling in different regions may present challenges. Despite these factors, the market's inherent versatility, coupled with ongoing innovation in processing and product development, ensures its continued expansion and relevance in the global food and beverage industry. Key players like Cargill Incorporated, Archer Daniels Midland Company, and Tate & Lyle PLC are actively investing in R&D and expanding their production capacities to meet this growing demand.

Liquid Sugar Industry Company Market Share

Unlocking the Sweet Potential: Comprehensive Report on the Global Liquid Sugar Industry (2019-2033)

This in-depth report provides an indispensable analysis of the global liquid sugar market, a dynamic sector projected to witness significant growth and innovation. Covering the historical period of 2019-2024 and extending to a comprehensive forecast period of 2025-2033, with a base year of 2025, this study delves into the intricate market structure, evolving trends, dominant segments, and key players shaping the liquid sweetener industry. Leveraging high-volume SEO keywords such as "liquid sugar market," "sweetener solutions," "food ingredient trends," and "beverage sweeteners," this report is optimized for maximum visibility and engagement within the industry. Explore critical insights into organic liquid sugar, conventional liquid sugar, and its diverse applications in bakery, confectionery, beverages, and baby foods. Discover emerging opportunities, understand growth drivers and challenges, and gain a strategic advantage in this rapidly expanding market.

Liquid Sugar Industry Market Structure & Competitive Landscape

The liquid sugar market exhibits a moderately concentrated structure, with a few dominant players holding significant market share, alongside a growing number of specialized manufacturers. Key innovation drivers stem from advancements in processing technologies that enhance sweetness, viscosity, and shelf-life, as well as the increasing consumer demand for natural and healthier sweetening alternatives. Regulatory impacts, particularly concerning sugar content, labeling, and health guidelines, play a crucial role in shaping product development and market access. Product substitutes, including high-fructose corn syrup (HFCS), artificial sweeteners, and emerging natural low-calorie sweeteners, pose a constant competitive pressure. End-user segmentation reveals a strong reliance on the beverage industry, followed closely by confectionery and bakery applications. Mergers and acquisitions (M&A) trends indicate strategic consolidation as larger entities aim to broaden their product portfolios and expand their geographic reach within the food ingredient market. For instance, the industry has witnessed M&A activities aiming to secure raw material supply chains and integrate innovative sweetener technologies. While specific quantitative M&A volumes are not publicly disclosed, the strategic intent points towards market expansion and competitive advantage. The concentration ratio, though variable by region, generally indicates a presence of key global players alongside strong regional contenders.

Liquid Sugar Industry Market Trends & Opportunities

The liquid sugar industry is experiencing robust growth, driven by a confluence of evolving consumer preferences, technological advancements, and expanding applications. The global market size is projected to grow at a compound annual growth rate (CAGR) of approximately 4.5% from 2025 to 2033, reaching an estimated valuation of over 50 million dollars by the end of the forecast period. This expansion is fueled by the increasing demand for convenience and versatility in food and beverage formulations. Consumers are increasingly seeking out ingredients that offer ease of use and consistent performance, which liquid sugars readily provide.

Technological shifts are playing a pivotal role, with innovations focusing on improved extraction methods, purification techniques, and the development of specialized liquid sugar profiles tailored to specific applications. This includes advancements in enzymatic hydrolysis and membrane filtration, enhancing the purity and functional properties of liquid sweeteners. Furthermore, the industry is witnessing a growing emphasis on sustainability and natural sourcing. The demand for organic liquid sugar is on the rise, as manufacturers respond to consumer desire for clean-label products.

Competitive dynamics are intensifying, with companies investing heavily in research and development to create novel liquid sweetener solutions. This includes exploring alternative raw materials and developing liquid sugar variants with reduced glycemic impact. The food ingredient market is witnessing a paradigm shift towards healthier alternatives, and liquid sugars are positioned to capitalize on this trend by offering options with controlled sugar profiles and functional benefits.

Opportunities abound in the expansion of liquid sugar applications across various sectors. The beverage industry remains a dominant consumer, but significant growth is also anticipated in baby foods, where manufacturers are seeking shelf-stable, easily digestible sweetening agents. The confectionery and bakery sectors continue to be strong markets, with liquid sugars offering advantages in texture, moisture retention, and crystallization control. Emerging applications in pharmaceuticals and animal feed also present untapped potential. The sweetener solutions landscape is becoming increasingly sophisticated, with a focus on functionality beyond mere sweetness, such as humectancy and browning properties.

Dominant Markets & Segments in Liquid Sugar Industry

The liquid sugar market is characterized by a dynamic interplay of regional dominance and segment-specific growth. Globally, conventional liquid sugar continues to hold the largest market share due to its cost-effectiveness and widespread availability. However, the organic liquid sugar segment is experiencing a significantly higher growth rate, driven by increasing consumer awareness regarding health and wellness, and a growing preference for natural and sustainably sourced ingredients. This trend is particularly pronounced in developed economies.

In terms of applications, the beverage industry stands as the dominant consumer of liquid sugars, accounting for over 35% of the market demand. This is attributed to the ease with which liquid sugars can be incorporated into liquid formulations, offering consistent sweetness and flavor profiles in soft drinks, juices, and alcoholic beverages. The confectionery segment follows closely, leveraging liquid sugars for their ability to control crystallization, enhance texture, and improve shelf-life in candies, chocolates, and other sweet treats. The bakery sector also represents a significant market, with liquid sugars contributing to dough conditioning, moisture retention, and crust browning in breads, cakes, and pastries. The baby foods segment, while smaller in volume, is a high-growth area, as manufacturers seek clean-label, easily digestible sweetening options for infant nutrition.

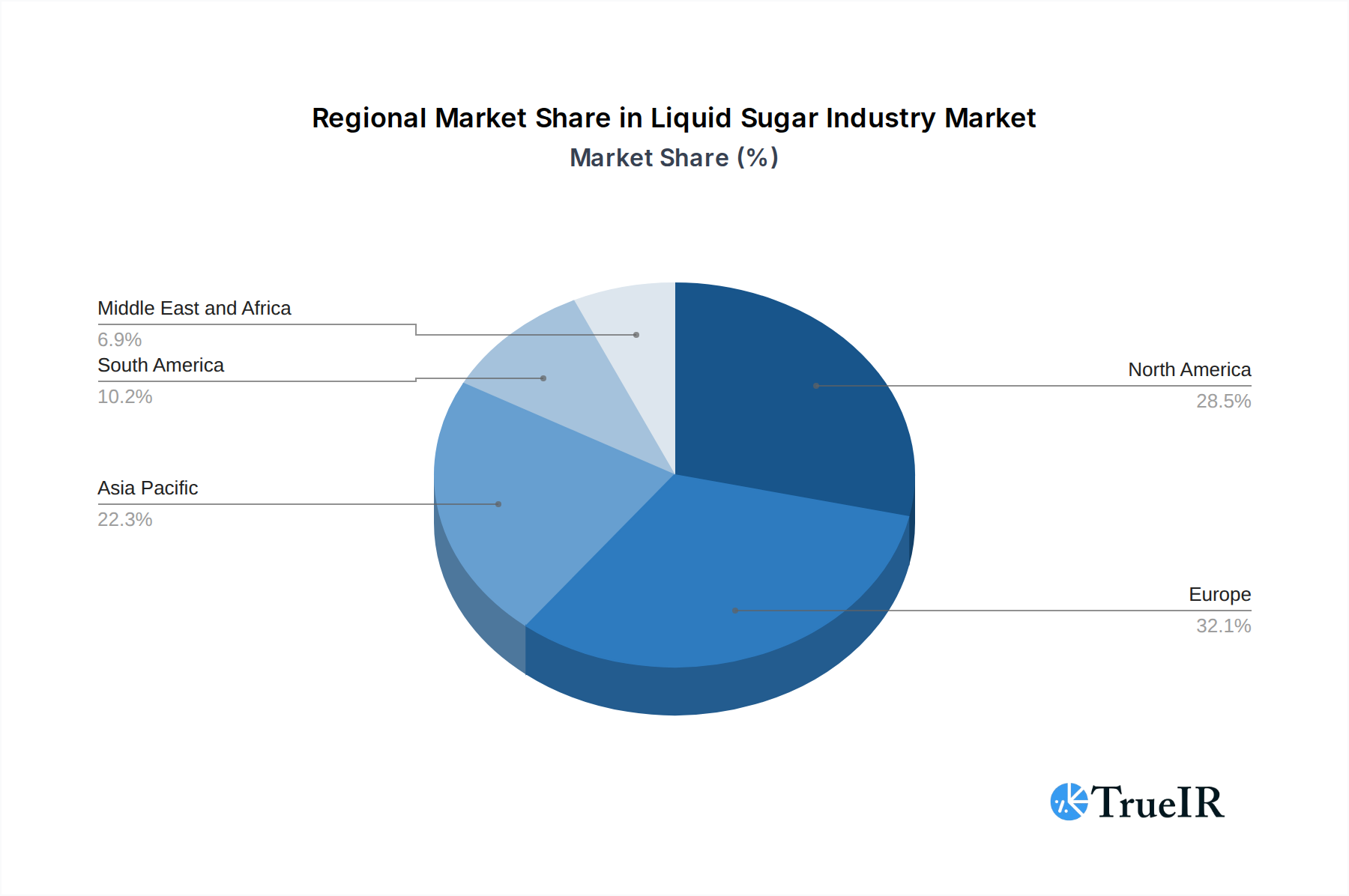

Geographically, North America and Europe are leading markets for liquid sugars, driven by established food and beverage industries and a strong consumer demand for processed foods. However, the Asia-Pacific region is emerging as a powerhouse of growth, fueled by rapid industrialization, a burgeoning middle class, and increasing adoption of Western dietary patterns. Government initiatives promoting food processing and exports within these regions are also contributing to market expansion. Policies supporting the agricultural sector and food innovation are critical growth drivers in these dominant markets.

Liquid Sugar Industry Product Analysis

The liquid sugar industry is continuously evolving with product innovations focused on enhancing functionality, health benefits, and sustainability. Key advancements include the development of specialized liquid sugar blends with tailored sweetness profiles and improved solubility for specific applications. Innovations in processing, such as enzymatic treatments, allow for the creation of liquid sugars with reduced glycemic indices or unique flavor notes. Competitive advantages are derived from superior product purity, consistent quality, and cost-effectiveness, alongside the growing demand for organic liquid sugar and sustainably sourced alternatives. The market is witnessing a trend towards the development of liquid sweeteners derived from a wider range of raw materials, expanding application possibilities.

Key Drivers, Barriers & Challenges in Liquid Sugar Industry

Key Drivers, Barriers & Challenges in Liquid Sugar Industry

The liquid sugar market is propelled by several key drivers. Technological advancements in extraction and processing offer improved efficiency and purity, while the growing consumer preference for convenient and versatile food ingredients fuels demand. Furthermore, the expanding food and beverage industry, particularly in emerging economies, presents significant growth opportunities.

However, the industry faces notable barriers and challenges. Fluctuations in raw material prices, such as sugarcane and beet prices, can impact production costs. Stringent regulatory frameworks concerning sugar content, labeling, and health claims can also pose hurdles. Intense competition from alternative sweeteners, both natural and artificial, necessitates continuous innovation and cost management. Supply chain disruptions, exacerbated by climate change or geopolitical events, can affect the availability and cost of raw materials.

Growth Drivers in the Liquid Sugar Industry Market

Growth in the liquid sugar industry is primarily driven by increasing consumer demand for convenience and versatile food ingredients. Technological advancements in processing and purification are leading to higher quality and more specialized liquid sugar products. The expanding global food and beverage sector, particularly in emerging economies, presents a significant market opportunity. Furthermore, the growing trend towards natural and organic ingredients is boosting the demand for organic liquid sugar. Government support for agricultural innovation and food processing industries in various regions also acts as a key growth catalyst.

Challenges Impacting Liquid Sugar Industry Growth

Despite its growth trajectory, the liquid sugar industry faces several challenges. Volatility in the prices of agricultural commodities like sugarcane and sugar beets can impact profitability. Evolving regulatory landscapes concerning sugar consumption, health claims, and food labeling requirements necessitate constant adaptation and compliance. Intense competition from alternative sweeteners, including artificial and natural low-calorie options, pressures manufacturers to innovate and maintain competitive pricing. Supply chain vulnerabilities, including disruptions due to climate change, transportation issues, and geopolitical factors, can affect raw material availability and cost.

Key Players Shaping the Liquid Sugar Industry Market

- Cargill Incorporated

- Boettger Gruppe

- Toyo Sugar Refining Co Ltd

- Archer Daniels Midland Company

- Tate & Lyle PLC

- Sucroliq S A P I DE C V

- Galam Group

- Zukan S L U

- Nordzucker AG

- Sugar Australia Company Ltd

Significant Liquid Sugar Industry Industry Milestones

- January 2024: North Carolina-based Elo Life Systems closed a USD 20.5 million Series A2 round to accelerate the development of a natural high-intensity sweetener and Cavendish bananas engineered to resist the devastating Fusarium wilt fungal disease (TR4). The company aims to introduce a liquid sweetener from watermelon juice by 2026 and powdered sweeteners from sugar beets by 2027.

- September 2022: Archer Daniels Midland Company opened its first science and technology center in China. This center was opened for technology, innovation, and product development in the nutrition and health industry.

- August 2022: The National Sugar Institute of Kanpur launched sugar syrup from jowar stem. The sugar syrup has been prepared after three years of research and tastes like honey, per the institution. Further, it is claimed that the syrup has a significant amount of sucrose and fructose equivalent to honey.

Future Outlook for Liquid Sugar Industry Market

The future outlook for the liquid sugar market is highly promising, driven by sustained demand from the food and beverage sector and continuous innovation. The growing emphasis on natural and healthier sweetening options will further propel the organic liquid sugar segment. Emerging markets in Asia-Pacific and Latin America are expected to be key growth engines, supported by increasing disposable incomes and evolving dietary habits. Strategic investments in R&D, focusing on developing functional liquid sweeteners with added health benefits and exploring novel raw material sources, will be crucial for market expansion. The industry is poised to witness increased consolidation and strategic partnerships to enhance market reach and technological capabilities, solidifying its position as a vital ingredient in the global food system.

Liquid Sugar Industry Segmentation

-

1. Origin

- 1.1. Organic

- 1.2. Conventional

-

2. Application

- 2.1. Bakery

- 2.2. Confectionery

- 2.3. Beverages

- 2.4. Baby Foods

- 2.5. Other Applications

Liquid Sugar Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

- 1.4. Rest of North America

-

2. Europe

- 2.1. Spain

- 2.2. United Kingdom

- 2.3. Germany

- 2.4. France

- 2.5. Italy

- 2.6. Russia

- 2.7. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. Rest of Asia Pacific

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

-

5. Middle East and Africa

- 5.1. South Africa

- 5.2. Saudi Arabia

- 5.3. Rest of Middle East and Africa

Liquid Sugar Industry Regional Market Share

Geographic Coverage of Liquid Sugar Industry

Liquid Sugar Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Origin

- 5.1.1. Organic

- 5.1.2. Conventional

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Bakery

- 5.2.2. Confectionery

- 5.2.3. Beverages

- 5.2.4. Baby Foods

- 5.2.5. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. South America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Origin

- 6. Global Liquid Sugar Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Origin

- 6.1.1. Organic

- 6.1.2. Conventional

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Bakery

- 6.2.2. Confectionery

- 6.2.3. Beverages

- 6.2.4. Baby Foods

- 6.2.5. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Origin

- 7. North America Liquid Sugar Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Origin

- 7.1.1. Organic

- 7.1.2. Conventional

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Bakery

- 7.2.2. Confectionery

- 7.2.3. Beverages

- 7.2.4. Baby Foods

- 7.2.5. Other Applications

- 7.1. Market Analysis, Insights and Forecast - by Origin

- 8. Europe Liquid Sugar Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Origin

- 8.1.1. Organic

- 8.1.2. Conventional

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Bakery

- 8.2.2. Confectionery

- 8.2.3. Beverages

- 8.2.4. Baby Foods

- 8.2.5. Other Applications

- 8.1. Market Analysis, Insights and Forecast - by Origin

- 9. Asia Pacific Liquid Sugar Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Origin

- 9.1.1. Organic

- 9.1.2. Conventional

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Bakery

- 9.2.2. Confectionery

- 9.2.3. Beverages

- 9.2.4. Baby Foods

- 9.2.5. Other Applications

- 9.1. Market Analysis, Insights and Forecast - by Origin

- 10. South America Liquid Sugar Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Origin

- 10.1.1. Organic

- 10.1.2. Conventional

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Bakery

- 10.2.2. Confectionery

- 10.2.3. Beverages

- 10.2.4. Baby Foods

- 10.2.5. Other Applications

- 10.1. Market Analysis, Insights and Forecast - by Origin

- 11. Middle East and Africa Liquid Sugar Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Origin

- 11.1.1. Organic

- 11.1.2. Conventional

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Bakery

- 11.2.2. Confectionery

- 11.2.3. Beverages

- 11.2.4. Baby Foods

- 11.2.5. Other Applications

- 11.1. Market Analysis, Insights and Forecast - by Origin

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Cargill Incorporated

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Boettger Gruppe

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Toyo Sugar Refining Co Ltd

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Archer Daniels Midland Company

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Tate & Lyle PLC

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Sucroliq S A P I DE C V *List Not Exhaustive

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Galam Group

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Zukan S L U

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Nordzucker AG

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Sugar Australia Company Ltd

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Cargill Incorporated

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Liquid Sugar Industry Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Liquid Sugar Industry Revenue (million), by Origin 2025 & 2033

- Figure 3: North America Liquid Sugar Industry Revenue Share (%), by Origin 2025 & 2033

- Figure 4: North America Liquid Sugar Industry Revenue (million), by Application 2025 & 2033

- Figure 5: North America Liquid Sugar Industry Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Liquid Sugar Industry Revenue (million), by Country 2025 & 2033

- Figure 7: North America Liquid Sugar Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Liquid Sugar Industry Revenue (million), by Origin 2025 & 2033

- Figure 9: Europe Liquid Sugar Industry Revenue Share (%), by Origin 2025 & 2033

- Figure 10: Europe Liquid Sugar Industry Revenue (million), by Application 2025 & 2033

- Figure 11: Europe Liquid Sugar Industry Revenue Share (%), by Application 2025 & 2033

- Figure 12: Europe Liquid Sugar Industry Revenue (million), by Country 2025 & 2033

- Figure 13: Europe Liquid Sugar Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Liquid Sugar Industry Revenue (million), by Origin 2025 & 2033

- Figure 15: Asia Pacific Liquid Sugar Industry Revenue Share (%), by Origin 2025 & 2033

- Figure 16: Asia Pacific Liquid Sugar Industry Revenue (million), by Application 2025 & 2033

- Figure 17: Asia Pacific Liquid Sugar Industry Revenue Share (%), by Application 2025 & 2033

- Figure 18: Asia Pacific Liquid Sugar Industry Revenue (million), by Country 2025 & 2033

- Figure 19: Asia Pacific Liquid Sugar Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: South America Liquid Sugar Industry Revenue (million), by Origin 2025 & 2033

- Figure 21: South America Liquid Sugar Industry Revenue Share (%), by Origin 2025 & 2033

- Figure 22: South America Liquid Sugar Industry Revenue (million), by Application 2025 & 2033

- Figure 23: South America Liquid Sugar Industry Revenue Share (%), by Application 2025 & 2033

- Figure 24: South America Liquid Sugar Industry Revenue (million), by Country 2025 & 2033

- Figure 25: South America Liquid Sugar Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Liquid Sugar Industry Revenue (million), by Origin 2025 & 2033

- Figure 27: Middle East and Africa Liquid Sugar Industry Revenue Share (%), by Origin 2025 & 2033

- Figure 28: Middle East and Africa Liquid Sugar Industry Revenue (million), by Application 2025 & 2033

- Figure 29: Middle East and Africa Liquid Sugar Industry Revenue Share (%), by Application 2025 & 2033

- Figure 30: Middle East and Africa Liquid Sugar Industry Revenue (million), by Country 2025 & 2033

- Figure 31: Middle East and Africa Liquid Sugar Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Liquid Sugar Industry Revenue million Forecast, by Origin 2020 & 2033

- Table 2: Global Liquid Sugar Industry Revenue million Forecast, by Application 2020 & 2033

- Table 3: Global Liquid Sugar Industry Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Liquid Sugar Industry Revenue million Forecast, by Origin 2020 & 2033

- Table 5: Global Liquid Sugar Industry Revenue million Forecast, by Application 2020 & 2033

- Table 6: Global Liquid Sugar Industry Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Liquid Sugar Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Liquid Sugar Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Liquid Sugar Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Rest of North America Liquid Sugar Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 11: Global Liquid Sugar Industry Revenue million Forecast, by Origin 2020 & 2033

- Table 12: Global Liquid Sugar Industry Revenue million Forecast, by Application 2020 & 2033

- Table 13: Global Liquid Sugar Industry Revenue million Forecast, by Country 2020 & 2033

- Table 14: Spain Liquid Sugar Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: United Kingdom Liquid Sugar Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Germany Liquid Sugar Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 17: France Liquid Sugar Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 18: Italy Liquid Sugar Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 19: Russia Liquid Sugar Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Rest of Europe Liquid Sugar Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: Global Liquid Sugar Industry Revenue million Forecast, by Origin 2020 & 2033

- Table 22: Global Liquid Sugar Industry Revenue million Forecast, by Application 2020 & 2033

- Table 23: Global Liquid Sugar Industry Revenue million Forecast, by Country 2020 & 2033

- Table 24: China Liquid Sugar Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Japan Liquid Sugar Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: India Liquid Sugar Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Australia Liquid Sugar Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Rest of Asia Pacific Liquid Sugar Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 29: Global Liquid Sugar Industry Revenue million Forecast, by Origin 2020 & 2033

- Table 30: Global Liquid Sugar Industry Revenue million Forecast, by Application 2020 & 2033

- Table 31: Global Liquid Sugar Industry Revenue million Forecast, by Country 2020 & 2033

- Table 32: Brazil Liquid Sugar Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: Argentina Liquid Sugar Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: Rest of South America Liquid Sugar Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: Global Liquid Sugar Industry Revenue million Forecast, by Origin 2020 & 2033

- Table 36: Global Liquid Sugar Industry Revenue million Forecast, by Application 2020 & 2033

- Table 37: Global Liquid Sugar Industry Revenue million Forecast, by Country 2020 & 2033

- Table 38: South Africa Liquid Sugar Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 39: Saudi Arabia Liquid Sugar Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 40: Rest of Middle East and Africa Liquid Sugar Industry Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Liquid Sugar Industry?

The projected CAGR is approximately 5.8%.

2. Which companies are prominent players in the Liquid Sugar Industry?

Key companies in the market include Cargill Incorporated, Boettger Gruppe, Toyo Sugar Refining Co Ltd, Archer Daniels Midland Company, Tate & Lyle PLC, Sucroliq S A P I DE C V *List Not Exhaustive, Galam Group, Zukan S L U, Nordzucker AG, Sugar Australia Company Ltd.

3. What are the main segments of the Liquid Sugar Industry?

The market segments include Origin, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 81.1 million as of 2022.

5. What are some drivers contributing to market growth?

Demand for Organic Variants; Thriving Food and Beverage Industry.

6. What are the notable trends driving market growth?

Escalating Demand for Organic Variants.

7. Are there any restraints impacting market growth?

Sugar Under Scrutiny with New Taxes and Label Regulations.

8. Can you provide examples of recent developments in the market?

January 2024: North Carolina-based Elo Life Systems closed a USD 20.5 million Series A2 round to accelerate the development of a natural high-intensity sweetener and Cavendish bananas engineered to resist the devastating Fusarium wilt fungal disease (TR4). The company aims to introduce a liquid sweetener from watermelon juice by 2026 and powdered sweeteners from sugar beets by 2027.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Liquid Sugar Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Liquid Sugar Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Liquid Sugar Industry?

To stay informed about further developments, trends, and reports in the Liquid Sugar Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence