Key Insights

The European bakery products market, including cakes, pastries, biscuits, bread, and morning goods, offers significant growth potential. Driven by escalating consumer demand for convenient, on-the-go food solutions and the increasing appeal of artisanal and premium offerings, the market is experiencing robust expansion. Convenience stores and online retail channels are key growth drivers, mirroring evolving consumer purchasing habits and the accessibility of digital grocery platforms. Market maturity is being offset by innovation in product development, such as healthier, organic, and gluten-free alternatives, which are fueling further expansion. Leading companies, including Grupo Bimbo, Warburtons, and Mondelēz International, are strategically investing in product diversification and distribution network enhancements. The market's fragmented nature, particularly among specialized bakeries, presents both opportunities and challenges, fostering a dynamic competitive environment. Germany, France, and the UK are the primary national markets, contributing substantially to the overall market size. While economic uncertainties and fluctuating raw material costs pose restraints, the long-term outlook for the European bakery products market remains positive, projecting sustained growth.

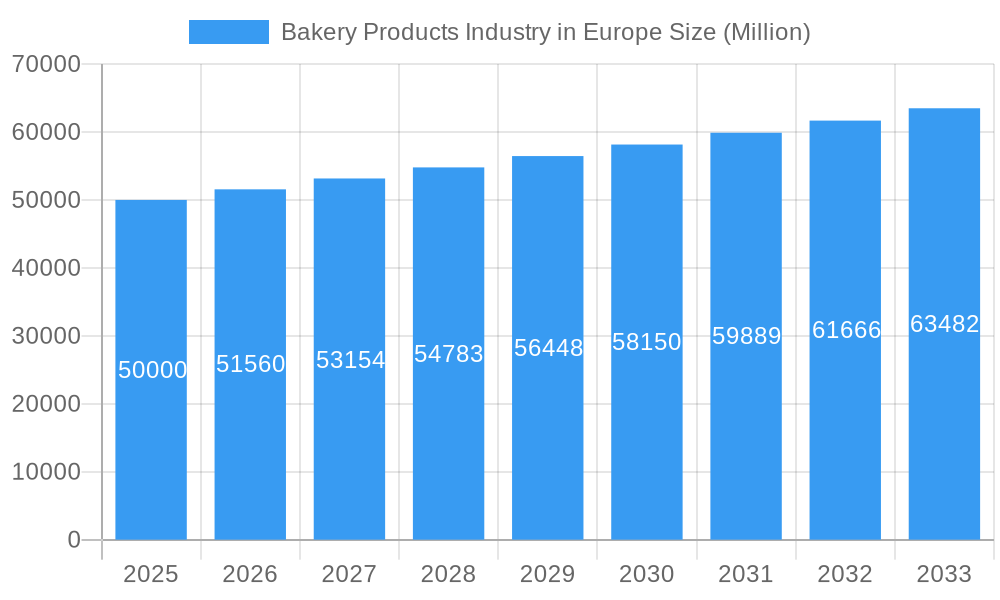

Bakery Products Industry in Europe Market Size (In Billion)

The market is projected to grow at a Compound Annual Growth Rate (CAGR) of 0.7%. With an estimated market size of 173.5 billion in the 2025 base year, this indicates a consistent growth trajectory. Key factors influencing this expansion include shifting consumer preferences towards healthier and more convenient food choices, alongside the ongoing premiumization trend, where consumers increasingly value higher-quality ingredients and artisanal products. Competitive pressures and rising raw material costs, such as wheat and sugar, are significant considerations that will shape future growth. The industry's strategic response to these challenges will be crucial for maintaining this growth rate and ensuring sustained success within the European bakery products sector.

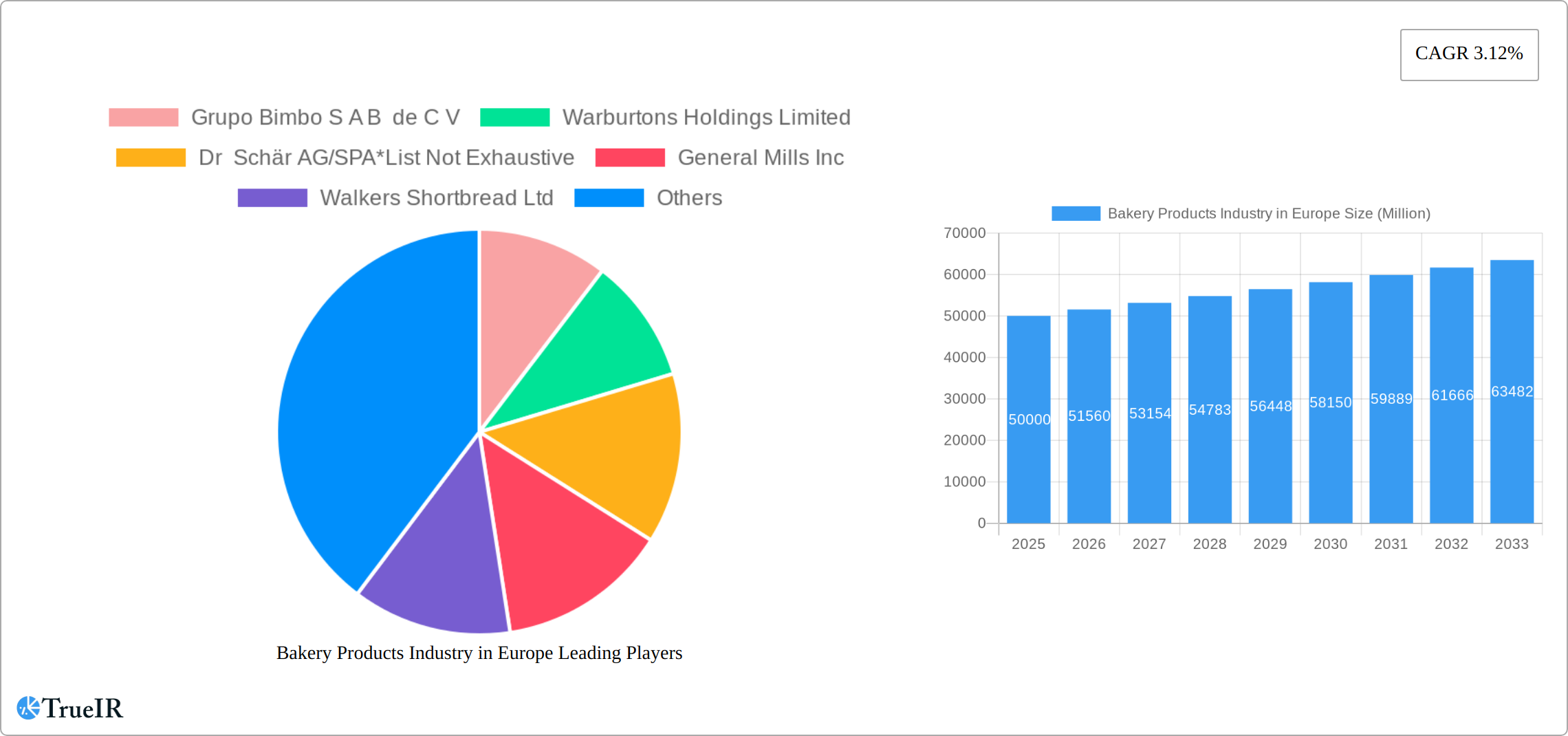

Bakery Products Industry in Europe Company Market Share

Bakery Products Industry in Europe: A Comprehensive Market Report (2019-2033)

This dynamic report provides a detailed analysis of the European bakery products market, offering invaluable insights for businesses, investors, and industry stakeholders. With a comprehensive study period spanning 2019-2033, including a base year of 2025 and a forecast period of 2025-2033, this report leverages robust data and expert analysis to illuminate current market trends and future growth potential. The European bakery market, valued at €XX Million in 2025, is poised for significant expansion, driven by evolving consumer preferences and technological advancements.

Bakery Products Industry in Europe Market Structure & Competitive Landscape

The European bakery products market presents a moderately concentrated structure, characterized by a dynamic interplay between multinational corporations and regional players vying for market dominance. While the precise Herfindahl-Hirschman Index (HHI) requires specific data for accurate calculation, the market's competitive landscape is evident, offering opportunities for both established industry giants and emerging brands. Innovation within the sector is significantly fueled by the increasing consumer preference for healthier products, a growing emphasis on sustainable practices, and the rise of personalized dietary choices. The stringent food safety regulations enforced by the European Union (EU) play a crucial role, driving the implementation of higher quality standards and robust traceability systems across the supply chain. The industry faces consistent challenges from substitute products, such as protein bars and various other snack alternatives, demanding continuous innovation and adaptation to maintain market share. Market segmentation is primarily defined by end-users, encompassing household consumption and the food service sector, with household consumption currently accounting for a substantial portion (XX%) of the overall market volume. Mergers and acquisitions (M&A) have been a notable feature of recent market activity, with a total transaction value exceeding XX million over the past five years, signifying ongoing consolidation and strategic repositioning within the industry.

- Key Players: Grupo Bimbo S A B de C V, Warburtons Holdings Limited, Dr Schär AG/SPA, General Mills Inc, Walkers Shortbread Ltd, Associated British Foods Plc, Mondelēz International Inc, Alpha Baking Company Inc, Kellogg Company, Britannia Industries Limited (and many others).

- Market Concentration: The market exhibits a moderately concentrated structure, although precise quantification via the HHI requires further data analysis.

- M&A Activity: Significant M&A activity observed, with transactions totaling over XX million (2019-2024), reflecting industry consolidation and strategic growth initiatives.

Bakery Products Industry in Europe Market Trends & Opportunities

The European bakery products market is experiencing robust growth, with a projected Compound Annual Growth Rate (CAGR) of XX% from 2025 to 2033. This expansion is fueled by several key factors. The rising disposable incomes in many European countries, coupled with changing lifestyles and increased demand for convenient and ready-to-eat options, are significantly boosting market growth. Technological advancements such as automation in production and improved packaging techniques enhance efficiency and product shelf life. Consumer preferences are shifting towards healthier and more natural products, with increasing demand for gluten-free, organic, and low-sugar options. This has led to significant innovation in product development and a greater focus on ingredient sourcing. The competitive landscape is characterized by fierce rivalry, compelling companies to continuously innovate and adapt to the evolving consumer landscape. Market penetration rates for various segments vary, with online retail showing significant growth but still lagging behind traditional channels like supermarkets and hypermarkets. The growing popularity of artisanal and specialty breads and pastries presents a niche market opportunity with high growth potential.

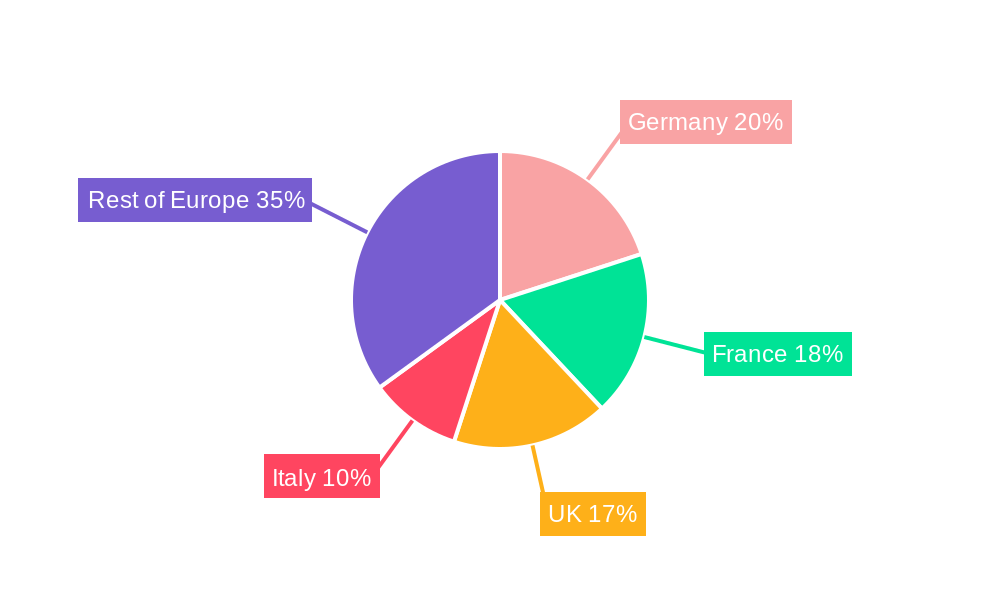

Dominant Markets & Segments in Bakery Products Industry in Europe

The largest segment within the European bakery market is bread, accounting for XX% of the total value. Germany and the UK are the leading national markets, driven by high consumption levels and strong retail infrastructure. Supermarkets/hypermarkets remain the dominant distribution channel, although online retail is exhibiting rapid growth.

Key Growth Drivers:

- Germany & UK: High per capita consumption, established retail infrastructure, strong consumer demand.

- Bread Segment: Staple food, widespread consumption, diverse product offerings (artisanal, industrial).

- Supermarkets/Hypermarkets: Wide reach, established distribution networks, promotional activities.

- Online Retail: Growing convenience, expanding delivery services, targeted marketing.

Market Dominance Analysis: Germany and the UK benefit from strong consumer demand and advanced retail infrastructure. Bread's dominance stems from its status as a staple food across Europe. Supermarkets and hypermarkets' market share reflects their efficient distribution networks. The rise of online retail is driven by increasing convenience and broader reach.

Bakery Products Industry in Europe Product Analysis

The European bakery market showcases a diverse range of products, from traditional breads and pastries to innovative gluten-free and organic options. Technological advancements in automated production lines, advanced ingredient formulations (e.g., improved sourdough starters), and smart packaging technologies are significantly impacting product quality, shelf life, and cost-effectiveness. Manufacturers are focusing on enhancing the sensory experience of their products, including taste, texture, and aroma, to meet the evolving demands of consumers. The market is highly competitive, forcing manufacturers to differentiate their products through innovative offerings and strong brand building.

Key Drivers, Barriers & Challenges in Bakery Products Industry in Europe

Key Drivers:

- Rising Disposable Incomes: Increased purchasing power fuels demand for premium and convenient bakery options, driving growth in higher-margin product segments.

- Changing Lifestyles: Busy lifestyles and the prevalence of dual-income households stimulate demand for ready-to-eat and convenient bakery products.

- Health & Wellness Trends: A heightened awareness of health and wellness drives significant growth in demand for healthier alternatives, including gluten-free, organic, and low-sugar bakery products.

- Technological Advancements: Automation, improved production techniques, and innovative packaging solutions enhance efficiency, improve product quality, and extend shelf life, increasing both profitability and consumer satisfaction.

Key Challenges:

- Fluctuating Raw Material Prices: The volatility in raw material costs, particularly for key ingredients like wheat and sugar, significantly impacts production costs and overall profitability. (Estimated impact: XX% increase in production costs over the past 5 years.)

- Stringent Regulatory Environment: Meeting the EU's stringent food safety and labeling regulations necessitates substantial investments in compliance, impacting operating costs.

- Intense Competition: The presence of numerous established players and emerging brands creates intense competition, placing pressure on profit margins and necessitating continuous innovation.

- Supply Chain Disruptions: Global supply chain vulnerabilities lead to production delays, increased costs, and potential shortages of raw materials. (XX% reported delays in 2022).

Growth Drivers in the Bakery Products Industry in Europe Market

Technological advancements, encompassing automated production lines and innovative packaging solutions, are pivotal in driving efficiency improvements and cost reductions. The widespread adoption of healthier eating habits is fueling innovation within the sector, particularly in the development and marketing of gluten-free, organic, and low-sugar products. Evolving consumer preferences for convenience are significantly boosting demand for ready-to-eat options and the growth of online retail channels for bakery products.

Challenges Impacting Bakery Products Industry in Europe Growth

Stringent regulations regarding food safety and labeling increase compliance costs. Supply chain vulnerabilities, as highlighted by recent disruptions, lead to production delays and price volatility. Intense competition from both large multinational corporations and smaller artisanal bakeries creates pressure on pricing and innovation.

Key Players Shaping the Bakery Products Industry in Europe Market

- Grupo Bimbo S A B de C V

- Warburtons Holdings Limited

- Dr Schär AG/SPA

- General Mills Inc

- Walkers Shortbread Ltd

- Associated British Foods Plc

- Mondelēz International Inc

- Alpha Baking Company Inc

- Kellogg Company

- Britannia Industries Limited

Significant Bakery Products Industry in Europe Industry Milestones

- April 2021: Walker's Shortbread expands its gluten-free range, exclusively at Sainsbury's.

- February 2022: Dr Schär acquires Just: Gluten Free Bakery, expanding its gluten-free product portfolio.

- August 2022: Mondelēz International innovates to create new non-HFSS products across several brands.

Future Outlook for Bakery Products Industry in Europe Market

The European bakery products market is poised for sustained growth, driven by the confluence of several key factors: the ongoing trend towards healthier eating habits, continuous technological innovation within the sector, and the evolution of consumer preferences. Significant opportunities exist for expansion within specialized market segments (e.g., gluten-free, organic products) and through the strategic leveraging of e-commerce channels. The long-term success of market participants will hinge on their ability to effectively adapt to the dynamic evolution of consumer demands, navigate the complexities of the regulatory landscape, and effectively manage the inherent vulnerabilities within global supply chains.

Bakery Products Industry in Europe Segmentation

-

1. Product Type

- 1.1. Cakes and Pastries

- 1.2. Biscuits

- 1.3. Bread

- 1.4. Morning Goods

- 1.5. Other Product Types

-

2. Distribution Channel

- 2.1. Supermarkets/Hypermarkets

- 2.2. Convenience Stores

- 2.3. Speciality Stores

- 2.4. Online Retail Stores

- 2.5. Other Distribution Channel

Bakery Products Industry in Europe Segmentation By Geography

- 1. United Kingdom

- 2. Germany

- 3. France

- 4. Russia

- 5. Italy

- 6. Spain

- 7. Rest of Europe

Bakery Products Industry in Europe Regional Market Share

Geographic Coverage of Bakery Products Industry in Europe

Bakery Products Industry in Europe REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 0.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increase in Number Of Social Event Celebration; Innovations In Designs And Flavors

- 3.3. Market Restrains

- 3.3.1. Health Concerns Related To Ingredients

- 3.4. Market Trends

- 3.4.1. Augmented Demand for Convenient Food Products

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Bakery Products Industry in Europe Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Cakes and Pastries

- 5.1.2. Biscuits

- 5.1.3. Bread

- 5.1.4. Morning Goods

- 5.1.5. Other Product Types

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Supermarkets/Hypermarkets

- 5.2.2. Convenience Stores

- 5.2.3. Speciality Stores

- 5.2.4. Online Retail Stores

- 5.2.5. Other Distribution Channel

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. United Kingdom

- 5.3.2. Germany

- 5.3.3. France

- 5.3.4. Russia

- 5.3.5. Italy

- 5.3.6. Spain

- 5.3.7. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. United Kingdom Bakery Products Industry in Europe Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Cakes and Pastries

- 6.1.2. Biscuits

- 6.1.3. Bread

- 6.1.4. Morning Goods

- 6.1.5. Other Product Types

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Supermarkets/Hypermarkets

- 6.2.2. Convenience Stores

- 6.2.3. Speciality Stores

- 6.2.4. Online Retail Stores

- 6.2.5. Other Distribution Channel

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Germany Bakery Products Industry in Europe Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Cakes and Pastries

- 7.1.2. Biscuits

- 7.1.3. Bread

- 7.1.4. Morning Goods

- 7.1.5. Other Product Types

- 7.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.2.1. Supermarkets/Hypermarkets

- 7.2.2. Convenience Stores

- 7.2.3. Speciality Stores

- 7.2.4. Online Retail Stores

- 7.2.5. Other Distribution Channel

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. France Bakery Products Industry in Europe Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Cakes and Pastries

- 8.1.2. Biscuits

- 8.1.3. Bread

- 8.1.4. Morning Goods

- 8.1.5. Other Product Types

- 8.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.2.1. Supermarkets/Hypermarkets

- 8.2.2. Convenience Stores

- 8.2.3. Speciality Stores

- 8.2.4. Online Retail Stores

- 8.2.5. Other Distribution Channel

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Russia Bakery Products Industry in Europe Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Cakes and Pastries

- 9.1.2. Biscuits

- 9.1.3. Bread

- 9.1.4. Morning Goods

- 9.1.5. Other Product Types

- 9.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.2.1. Supermarkets/Hypermarkets

- 9.2.2. Convenience Stores

- 9.2.3. Speciality Stores

- 9.2.4. Online Retail Stores

- 9.2.5. Other Distribution Channel

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. Italy Bakery Products Industry in Europe Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 10.1.1. Cakes and Pastries

- 10.1.2. Biscuits

- 10.1.3. Bread

- 10.1.4. Morning Goods

- 10.1.5. Other Product Types

- 10.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.2.1. Supermarkets/Hypermarkets

- 10.2.2. Convenience Stores

- 10.2.3. Speciality Stores

- 10.2.4. Online Retail Stores

- 10.2.5. Other Distribution Channel

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 11. Spain Bakery Products Industry in Europe Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 11.1.1. Cakes and Pastries

- 11.1.2. Biscuits

- 11.1.3. Bread

- 11.1.4. Morning Goods

- 11.1.5. Other Product Types

- 11.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 11.2.1. Supermarkets/Hypermarkets

- 11.2.2. Convenience Stores

- 11.2.3. Speciality Stores

- 11.2.4. Online Retail Stores

- 11.2.5. Other Distribution Channel

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 12. Rest of Europe Bakery Products Industry in Europe Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Product Type

- 12.1.1. Cakes and Pastries

- 12.1.2. Biscuits

- 12.1.3. Bread

- 12.1.4. Morning Goods

- 12.1.5. Other Product Types

- 12.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 12.2.1. Supermarkets/Hypermarkets

- 12.2.2. Convenience Stores

- 12.2.3. Speciality Stores

- 12.2.4. Online Retail Stores

- 12.2.5. Other Distribution Channel

- 12.1. Market Analysis, Insights and Forecast - by Product Type

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2025

- 13.2. Company Profiles

- 13.2.1 Grupo Bimbo S A B de C V

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 Warburtons Holdings Limited

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 Dr Schär AG/SPA*List Not Exhaustive

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 General Mills Inc

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 Walkers Shortbread Ltd

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 Associated British Foods Plc

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 Mondelēz International Inc

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 Alpha Baking Company Inc

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.9 Kellogg Company

- 13.2.9.1. Overview

- 13.2.9.2. Products

- 13.2.9.3. SWOT Analysis

- 13.2.9.4. Recent Developments

- 13.2.9.5. Financials (Based on Availability)

- 13.2.10 Britannia Industries Limited

- 13.2.10.1. Overview

- 13.2.10.2. Products

- 13.2.10.3. SWOT Analysis

- 13.2.10.4. Recent Developments

- 13.2.10.5. Financials (Based on Availability)

- 13.2.1 Grupo Bimbo S A B de C V

List of Figures

- Figure 1: Bakery Products Industry in Europe Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Bakery Products Industry in Europe Share (%) by Company 2025

List of Tables

- Table 1: Bakery Products Industry in Europe Revenue billion Forecast, by Product Type 2020 & 2033

- Table 2: Bakery Products Industry in Europe Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 3: Bakery Products Industry in Europe Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Bakery Products Industry in Europe Revenue billion Forecast, by Product Type 2020 & 2033

- Table 5: Bakery Products Industry in Europe Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 6: Bakery Products Industry in Europe Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Bakery Products Industry in Europe Revenue billion Forecast, by Product Type 2020 & 2033

- Table 8: Bakery Products Industry in Europe Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 9: Bakery Products Industry in Europe Revenue billion Forecast, by Country 2020 & 2033

- Table 10: Bakery Products Industry in Europe Revenue billion Forecast, by Product Type 2020 & 2033

- Table 11: Bakery Products Industry in Europe Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 12: Bakery Products Industry in Europe Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Bakery Products Industry in Europe Revenue billion Forecast, by Product Type 2020 & 2033

- Table 14: Bakery Products Industry in Europe Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 15: Bakery Products Industry in Europe Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Bakery Products Industry in Europe Revenue billion Forecast, by Product Type 2020 & 2033

- Table 17: Bakery Products Industry in Europe Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 18: Bakery Products Industry in Europe Revenue billion Forecast, by Country 2020 & 2033

- Table 19: Bakery Products Industry in Europe Revenue billion Forecast, by Product Type 2020 & 2033

- Table 20: Bakery Products Industry in Europe Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 21: Bakery Products Industry in Europe Revenue billion Forecast, by Country 2020 & 2033

- Table 22: Bakery Products Industry in Europe Revenue billion Forecast, by Product Type 2020 & 2033

- Table 23: Bakery Products Industry in Europe Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 24: Bakery Products Industry in Europe Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Bakery Products Industry in Europe?

The projected CAGR is approximately 0.7%.

2. Which companies are prominent players in the Bakery Products Industry in Europe?

Key companies in the market include Grupo Bimbo S A B de C V, Warburtons Holdings Limited, Dr Schär AG/SPA*List Not Exhaustive, General Mills Inc, Walkers Shortbread Ltd, Associated British Foods Plc, Mondelēz International Inc, Alpha Baking Company Inc, Kellogg Company, Britannia Industries Limited.

3. What are the main segments of the Bakery Products Industry in Europe?

The market segments include Product Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 173.5 billion as of 2022.

5. What are some drivers contributing to market growth?

Increase in Number Of Social Event Celebration; Innovations In Designs And Flavors.

6. What are the notable trends driving market growth?

Augmented Demand for Convenient Food Products.

7. Are there any restraints impacting market growth?

Health Concerns Related To Ingredients.

8. Can you provide examples of recent developments in the market?

August 2022: Mondelēz International, Inc. continued its strong track record of offering a wide range of snacking options for consumers by innovating to create new products or reformulating products that will not be classified as high in fat, salt, or sugar (HFSS) from beloved brands including belVita, Cadbury Drinking Chocolate, Maynards Bassetts and The Natural Confectionery Company.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Bakery Products Industry in Europe," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Bakery Products Industry in Europe report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Bakery Products Industry in Europe?

To stay informed about further developments, trends, and reports in the Bakery Products Industry in Europe, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence