Key Insights

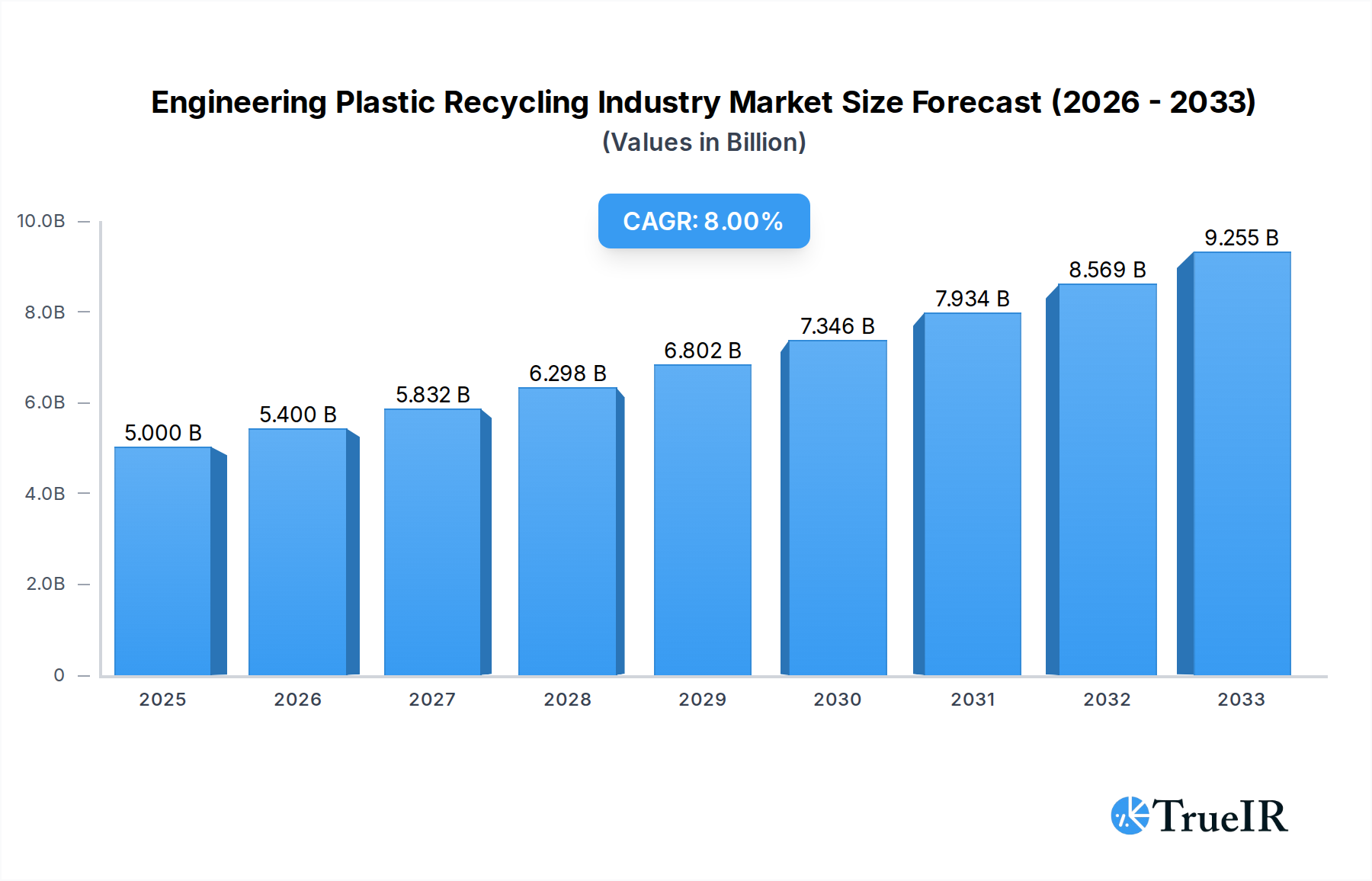

The global engineering plastic recycling market is poised for substantial growth, projected to reach USD 5 billion in 2025, driven by an anticipated CAGR of 8% throughout the forecast period of 2025-2033. This robust expansion is primarily fueled by increasing environmental consciousness among consumers and regulatory bodies, demanding sustainable solutions and a circular economy for plastics. Key drivers include stringent government regulations promoting recycled content in products, a growing demand for high-performance recycled plastics in various industries, and advancements in recycling technologies that enhance the quality and applicability of recovered materials. The escalating prices of virgin plastics also make recycled alternatives more economically attractive, further bolstering market adoption.

Engineering Plastic Recycling Industry Market Size (In Billion)

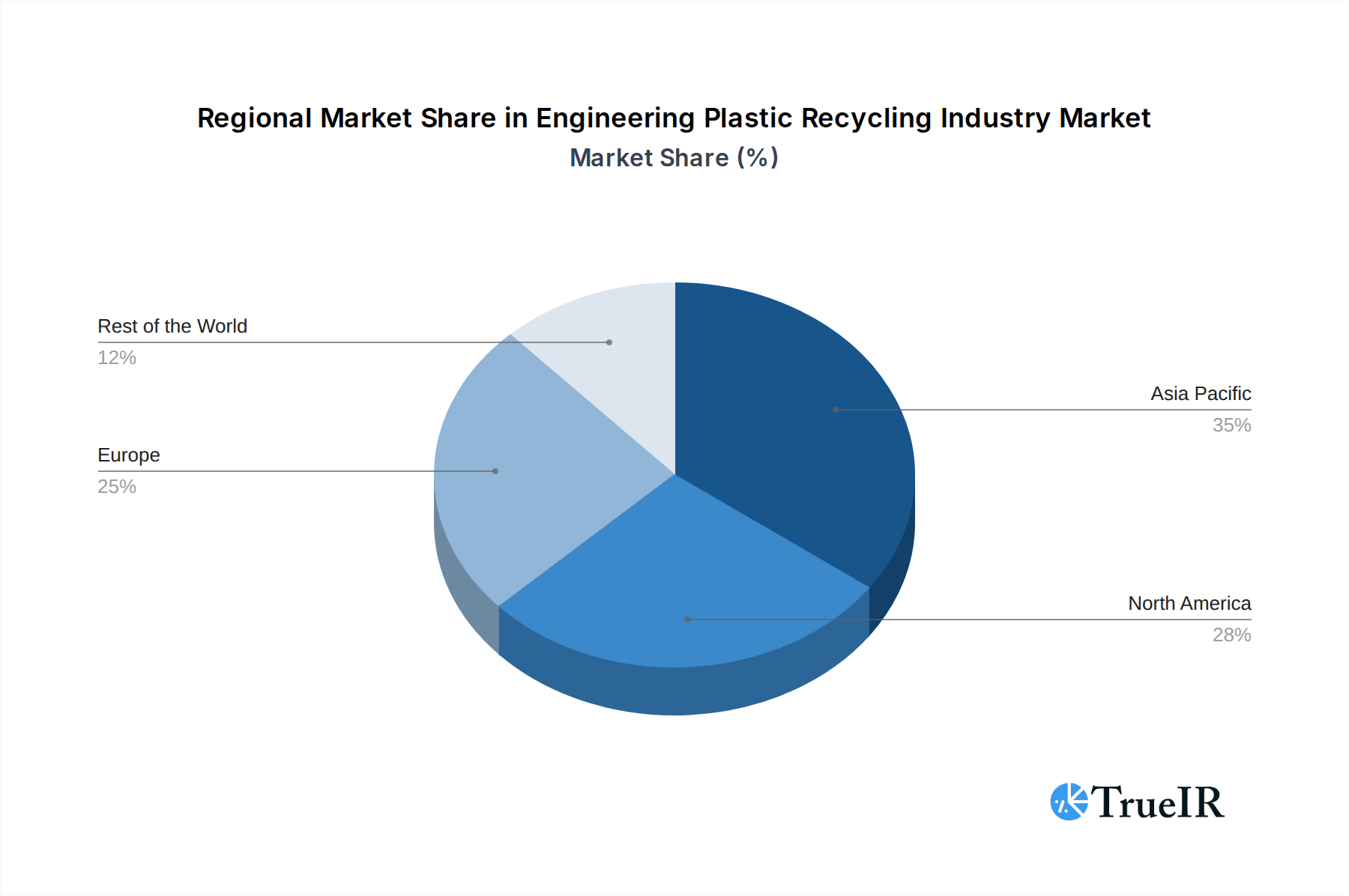

The market is segmented across various plastic types, with Polycarbonate and Polyethylene Terephthalate (PET) anticipated to lead in demand due to their widespread use and established recycling infrastructure. The Packaging and Industrial Yarn sectors are expected to remain the largest end-user industries, though significant growth is also foreseen in Electrical and Electronics and other niche industrial applications as manufacturers increasingly opt for sustainable materials. Geographically, the Asia Pacific region, particularly China and India, is emerging as a dominant force, owing to rapid industrialization and supportive government initiatives for waste management and recycling. North America and Europe are also key markets, characterized by mature recycling frameworks and a strong consumer push for eco-friendly products. Despite the promising outlook, challenges such as the complex sorting of mixed plastic waste and the need for consistent quality of recycled materials may present some restraints to a more rapid expansion.

Engineering Plastic Recycling Industry Company Market Share

Unlocking the Billion-Dollar Potential: Comprehensive Engineering Plastic Recycling Industry Market Report (2019-2033)

This definitive report dives deep into the engineering plastic recycling industry, offering a data-driven analysis of its evolving landscape, market dynamics, and future trajectory. With a study period spanning from 2019 to 2033, this comprehensive resource provides actionable insights for stakeholders seeking to capitalize on this burgeoning billion-dollar market. Leveraging high-volume keywords such as "plastic recycling," "PET recycling," "engineering plastics," "sustainable materials," and "circular economy," this report is meticulously optimized for search engines and designed to engage industry professionals.

Engineering Plastic Recycling Industry Market Structure & Competitive Landscape

The engineering plastic recycling industry is characterized by a moderate to high market concentration, driven by significant capital investments in advanced recycling technologies and infrastructure. Innovation remains a key differentiator, with companies investing heavily in R&D to improve sorting, purification, and material reprocessing techniques, thereby enhancing the quality and applicability of recycled engineering plastics. Regulatory frameworks globally are increasingly favoring the adoption of recycled content, with mandates and incentives playing a crucial role in shaping market dynamics. The threat of product substitutes, while present from virgin plastics, is diminishing as recycled engineering plastics achieve parity in performance and cost-effectiveness. End-user segmentation is diverse, with the packaging sector and industrial yarn applications demonstrating robust demand. Mergers and Acquisitions (M&A) are a significant trend, with major players consolidating their market positions and expanding their recycling capacities. For instance, the acquisition of UCY Polymers CZ s.r.o. by Indorama Ventures signifies a strategic move to bolster its PET recycling operations. Estimated M&A volumes are projected to reach hundreds of billions in the coming forecast period, reflecting the industry's growth potential.

Engineering Plastic Recycling Industry Market Trends & Opportunities

The engineering plastic recycling industry is poised for substantial growth, driven by a confluence of environmental consciousness, regulatory pressures, and technological advancements. The global market size is projected to expand from an estimated hundreds of billions in the base year of 2025, exhibiting a compound annual growth rate (CAGR) of approximately xx% during the forecast period of 2025–2033. Technological shifts, including the development of advanced chemical recycling methods and enhanced mechanical recycling processes, are enabling the recovery of higher-quality engineering plastics like Polycarbonate and Polyethylene Terephthalate (PET), thereby expanding their applications into more demanding sectors such as automotive and electronics. Consumer preferences are increasingly leaning towards sustainable products, creating a pull for recycled content across various end-user industries. Competitive dynamics are intensifying, with established chemical companies and specialized recycling firms vying for market share. Opportunities abound for companies that can offer integrated recycling solutions, develop novel applications for recycled engineering plastics, and establish robust collection and sorting networks. The market penetration rate for recycled engineering plastics is steadily increasing, driven by supportive government policies and corporate sustainability commitments, further fueling market expansion.

Dominant Markets & Segments in Engineering Plastic Recycling Industry

The Polyethylene Terephthalate (PET) segment currently dominates the engineering plastic recycling landscape, driven by its widespread use in packaging and the increasing availability of post-consumer PET bottles. The Packaging end-user industry represents the largest consumer of recycled PET, with significant investments in bottle-to-bottle recycling initiatives. The Asia Pacific region, particularly China and Southeast Asian nations, is a dominant market due to its large manufacturing base and growing awareness regarding plastic waste management. However, Europe is also a significant player, propelled by stringent recycling regulations and a strong focus on the circular economy.

Plastic Type Dominance:

- Polyethylene Terephthalate (PET): Leading segment due to high recycling rates and extensive use in beverage packaging. Growth is fueled by advanced recycling technologies and brand owner commitments.

- Polycarbonate: Growing demand in automotive and electronics sectors due to its high impact resistance and optical clarity. Innovations in chemical recycling are expanding its recyclability.

- Styrene Copolymers (ABS and SAN): Applications in consumer goods and automotive interiors. Challenges in sorting and reprocessing are being addressed by advanced technologies.

- Polyamide: Strong presence in textiles and automotive components. Increasing focus on recovering high-value polyamide waste streams.

- Other Engineering Plastics: Emerging demand for specialized engineering plastics as recycling capabilities expand.

End-user Industry Dominance:

- Packaging: The largest and most dynamic end-user industry, with a strong emphasis on food-grade recycled PET and a push for circular packaging solutions.

- Industrial Yarn: A consistent demand driver, particularly for recycled PET in textiles and industrial applications.

- Electrical and Electronics: Growing demand for recycled Polycarbonate and other engineering plastics in appliance casings and components, driven by eco-design regulations.

- Other End-user Industries: Includes automotive, construction, and medical devices, where the adoption of recycled engineering plastics is on an upward trajectory.

Engineering Plastic Recycling Industry Product Analysis

Product innovation in the engineering plastic recycling industry is centered on enhancing the quality and expanding the applications of recycled materials. Advanced purification techniques are producing recycled engineering plastics with properties comparable to virgin grades, enabling their use in more demanding sectors. For instance, the development of closed-loop recycling systems for Polycarbonate in the automotive industry and the successful implementation of bottle-to-bottle PET recycling are key advancements. These innovations provide competitive advantages by offering sustainable alternatives that meet stringent performance requirements, reduce carbon footprints, and align with corporate sustainability goals.

Key Drivers, Barriers & Challenges in Engineering Plastic Recycling Industry

Key Drivers, Barriers & Challenges in Engineering Plastic Recycling Industry

Key Drivers:

- Growing environmental awareness and consumer demand for sustainable products are compelling manufacturers to incorporate recycled content.

- Stringent government regulations and policies, including Extended Producer Responsibility (EPR) schemes and recycled content mandates, are significant market accelerators.

- Technological advancements in sorting, purification, and chemical recycling are improving the quality and expanding the range of recyclable engineering plastics.

- Corporate sustainability commitments and ESG (Environmental, Social, and Governance) goals are driving investments and demand for recycled materials.

- The rising cost of virgin plastics and fluctuating oil prices make recycled alternatives more economically attractive.

Barriers & Challenges:

- Inconsistent quality and availability of post-consumer plastic waste due to contamination and inefficient collection systems pose supply chain challenges.

- High initial investment costs for advanced recycling infrastructure can be a barrier to entry for smaller players.

- Complexity in sorting mixed plastic streams, especially for multi-layer packaging and composite materials, requires sophisticated technological solutions.

- Regulatory hurdles and differing standards across regions can complicate market access and scalability.

- Perception challenges and performance concerns regarding recycled plastics, though diminishing, still exist in certain high-specification applications.

Growth Drivers in the Engineering Plastic Recycling Industry Market

The engineering plastic recycling industry is propelled by several key growth drivers. Technologically, innovations in chemical recycling are enabling the recovery of valuable monomers from complex plastic waste, opening up new avenues for high-quality recycled materials. Economically, the increasing price volatility of virgin polymers and the growing demand for cost-effective, sustainable solutions make recycled engineering plastics a compelling choice for manufacturers. Regulatory drivers, such as government mandates for recycled content in packaging and electronics, are creating a guaranteed market for recycled materials and encouraging significant investment in recycling infrastructure. For example, the growing emphasis on a circular economy framework by many governments globally is a substantial catalyst.

Challenges Impacting Engineering Plastic Recycling Industry Growth

Several challenges impact the growth of the engineering plastic recycling industry. Regulatory complexities, including differing definitions of "recyclable" and varying EPR schemes across jurisdictions, create market fragmentation and operational hurdles. Supply chain issues, such as inconsistent feedstock quality and the logistical challenges of collecting and transporting large volumes of post-consumer waste, can hinder production efficiency. Competitive pressures from virgin plastic producers, who often benefit from established economies of scale and lower production costs, remain a significant restraint. Furthermore, public perception and the need for consumer education regarding the quality and benefits of recycled engineering plastics also play a role in market adoption.

Key Players Shaping the Engineering Plastic Recycling Industry Market

- REPRO-PET

- Placon

- Euresi Plastics SL

- PolyClean Technologies

- Indorama Ventures Public Company Limited

- Reliance Industries Limited

- Krones AG

- Petco

- Clean Tech UK Ltd

- JFC Group

- Far Eastern New Century Corporation (Phoenix Technologies)

- TEIJIN LIMITED

- UltrePET LLC

- Alpek S A B de C V

- EF Plastics UK Ltd

Significant Engineering Plastic Recycling Industry Industry Milestones

- October 2022: Indorama Ventures announced the opening of a PET Value bottle-to-bottle recycling plant in the Philippines in partnership with Coca-Cola Beverages Philippines.

- February 2022: Indorama Ventures announced the acquisition of UCY Polymers CZ s.r.o. (UCY), a Czech Republic-based PET plastic recycler. This acquisition is projected to lead to the recycling of approximately 1.12 billion additional post-consumer PET plastic bottles in the Czech Republic annually by 2025.

Future Outlook for Engineering Plastic Recycling Industry Market

The future outlook for the engineering plastic recycling industry is exceptionally bright, driven by sustained growth catalysts. Strategic opportunities lie in the development of advanced chemical recycling technologies that can process a wider array of engineering plastics, including mixed streams and contaminated materials. The increasing integration of recycled content into high-value applications, such as automotive components and electronic devices, will further expand market potential. Furthermore, collaborations between plastic producers, recyclers, and brand owners will be crucial in establishing robust and efficient circular supply chains, unlocking significant market opportunities and contributing to a more sustainable future with an estimated market value projected to reach trillions by 2033.

Engineering Plastic Recycling Industry Segmentation

-

1. Plastic Type

- 1.1. Polycarbonate

- 1.2. Polyethylene Terephthalate (PET)

- 1.3. Styrene Copolymers (ABS and SAN)

- 1.4. Polyamide

- 1.5. Other Engineering Plastics

-

2. End-user Industry

- 2.1. Packaging

- 2.2. Industrial Yarn

- 2.3. Electrical and Electronics

- 2.4. Other End-user Industries

Engineering Plastic Recycling Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Japan

- 1.4. South Korea

- 1.5. Rest of Asia Pacific

-

2. North America

- 2.1. United States

- 2.2. Canada

- 2.3. Mexico

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. France

- 3.4. Italy

- 3.5. Rest of Europe

-

4. Rest of the World

- 4.1. South America

- 4.2. Middle East and Africa

Engineering Plastic Recycling Industry Regional Market Share

Geographic Coverage of Engineering Plastic Recycling Industry

Engineering Plastic Recycling Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Plastic Type

- 5.1.1. Polycarbonate

- 5.1.2. Polyethylene Terephthalate (PET)

- 5.1.3. Styrene Copolymers (ABS and SAN)

- 5.1.4. Polyamide

- 5.1.5. Other Engineering Plastics

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Packaging

- 5.2.2. Industrial Yarn

- 5.2.3. Electrical and Electronics

- 5.2.4. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Asia Pacific

- 5.3.2. North America

- 5.3.3. Europe

- 5.3.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Plastic Type

- 6. Global Engineering Plastic Recycling Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Plastic Type

- 6.1.1. Polycarbonate

- 6.1.2. Polyethylene Terephthalate (PET)

- 6.1.3. Styrene Copolymers (ABS and SAN)

- 6.1.4. Polyamide

- 6.1.5. Other Engineering Plastics

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Packaging

- 6.2.2. Industrial Yarn

- 6.2.3. Electrical and Electronics

- 6.2.4. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Plastic Type

- 7. Asia Pacific Engineering Plastic Recycling Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Plastic Type

- 7.1.1. Polycarbonate

- 7.1.2. Polyethylene Terephthalate (PET)

- 7.1.3. Styrene Copolymers (ABS and SAN)

- 7.1.4. Polyamide

- 7.1.5. Other Engineering Plastics

- 7.2. Market Analysis, Insights and Forecast - by End-user Industry

- 7.2.1. Packaging

- 7.2.2. Industrial Yarn

- 7.2.3. Electrical and Electronics

- 7.2.4. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by Plastic Type

- 8. North America Engineering Plastic Recycling Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Plastic Type

- 8.1.1. Polycarbonate

- 8.1.2. Polyethylene Terephthalate (PET)

- 8.1.3. Styrene Copolymers (ABS and SAN)

- 8.1.4. Polyamide

- 8.1.5. Other Engineering Plastics

- 8.2. Market Analysis, Insights and Forecast - by End-user Industry

- 8.2.1. Packaging

- 8.2.2. Industrial Yarn

- 8.2.3. Electrical and Electronics

- 8.2.4. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by Plastic Type

- 9. Europe Engineering Plastic Recycling Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Plastic Type

- 9.1.1. Polycarbonate

- 9.1.2. Polyethylene Terephthalate (PET)

- 9.1.3. Styrene Copolymers (ABS and SAN)

- 9.1.4. Polyamide

- 9.1.5. Other Engineering Plastics

- 9.2. Market Analysis, Insights and Forecast - by End-user Industry

- 9.2.1. Packaging

- 9.2.2. Industrial Yarn

- 9.2.3. Electrical and Electronics

- 9.2.4. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by Plastic Type

- 10. Rest of the World Engineering Plastic Recycling Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Plastic Type

- 10.1.1. Polycarbonate

- 10.1.2. Polyethylene Terephthalate (PET)

- 10.1.3. Styrene Copolymers (ABS and SAN)

- 10.1.4. Polyamide

- 10.1.5. Other Engineering Plastics

- 10.2. Market Analysis, Insights and Forecast - by End-user Industry

- 10.2.1. Packaging

- 10.2.2. Industrial Yarn

- 10.2.3. Electrical and Electronics

- 10.2.4. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by Plastic Type

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 REPRO-PET

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Placon

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Euresi Plastics SL

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 PolyClean Technologies

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Indorama Ventures Public Company Limited

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Reliance Industries Limited

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Krones AG

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Petco

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Clean Tech UK Ltd

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 JFC Group

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.11 Far Eastern New Century Corporation (Phoenix Technologies)

- 11.1.11.1. Company Overview

- 11.1.11.2. Products

- 11.1.11.3. Company Financials

- 11.1.11.4. SWOT Analysis

- 11.1.12 TEIJIN LIMITED

- 11.1.12.1. Company Overview

- 11.1.12.2. Products

- 11.1.12.3. Company Financials

- 11.1.12.4. SWOT Analysis

- 11.1.13 UltrePET LLC

- 11.1.13.1. Company Overview

- 11.1.13.2. Products

- 11.1.13.3. Company Financials

- 11.1.13.4. SWOT Analysis

- 11.1.14 Alpek S A B de C V

- 11.1.14.1. Company Overview

- 11.1.14.2. Products

- 11.1.14.3. Company Financials

- 11.1.14.4. SWOT Analysis

- 11.1.15 EF Plastics UK Ltd

- 11.1.15.1. Company Overview

- 11.1.15.2. Products

- 11.1.15.3. Company Financials

- 11.1.15.4. SWOT Analysis

- 11.1.1 REPRO-PET

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Engineering Plastic Recycling Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global Engineering Plastic Recycling Industry Volume Breakdown (K Tons, %) by Region 2025 & 2033

- Figure 3: Asia Pacific Engineering Plastic Recycling Industry Revenue (billion), by Plastic Type 2025 & 2033

- Figure 4: Asia Pacific Engineering Plastic Recycling Industry Volume (K Tons), by Plastic Type 2025 & 2033

- Figure 5: Asia Pacific Engineering Plastic Recycling Industry Revenue Share (%), by Plastic Type 2025 & 2033

- Figure 6: Asia Pacific Engineering Plastic Recycling Industry Volume Share (%), by Plastic Type 2025 & 2033

- Figure 7: Asia Pacific Engineering Plastic Recycling Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 8: Asia Pacific Engineering Plastic Recycling Industry Volume (K Tons), by End-user Industry 2025 & 2033

- Figure 9: Asia Pacific Engineering Plastic Recycling Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 10: Asia Pacific Engineering Plastic Recycling Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 11: Asia Pacific Engineering Plastic Recycling Industry Revenue (billion), by Country 2025 & 2033

- Figure 12: Asia Pacific Engineering Plastic Recycling Industry Volume (K Tons), by Country 2025 & 2033

- Figure 13: Asia Pacific Engineering Plastic Recycling Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Engineering Plastic Recycling Industry Volume Share (%), by Country 2025 & 2033

- Figure 15: North America Engineering Plastic Recycling Industry Revenue (billion), by Plastic Type 2025 & 2033

- Figure 16: North America Engineering Plastic Recycling Industry Volume (K Tons), by Plastic Type 2025 & 2033

- Figure 17: North America Engineering Plastic Recycling Industry Revenue Share (%), by Plastic Type 2025 & 2033

- Figure 18: North America Engineering Plastic Recycling Industry Volume Share (%), by Plastic Type 2025 & 2033

- Figure 19: North America Engineering Plastic Recycling Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 20: North America Engineering Plastic Recycling Industry Volume (K Tons), by End-user Industry 2025 & 2033

- Figure 21: North America Engineering Plastic Recycling Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 22: North America Engineering Plastic Recycling Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 23: North America Engineering Plastic Recycling Industry Revenue (billion), by Country 2025 & 2033

- Figure 24: North America Engineering Plastic Recycling Industry Volume (K Tons), by Country 2025 & 2033

- Figure 25: North America Engineering Plastic Recycling Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: North America Engineering Plastic Recycling Industry Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Engineering Plastic Recycling Industry Revenue (billion), by Plastic Type 2025 & 2033

- Figure 28: Europe Engineering Plastic Recycling Industry Volume (K Tons), by Plastic Type 2025 & 2033

- Figure 29: Europe Engineering Plastic Recycling Industry Revenue Share (%), by Plastic Type 2025 & 2033

- Figure 30: Europe Engineering Plastic Recycling Industry Volume Share (%), by Plastic Type 2025 & 2033

- Figure 31: Europe Engineering Plastic Recycling Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 32: Europe Engineering Plastic Recycling Industry Volume (K Tons), by End-user Industry 2025 & 2033

- Figure 33: Europe Engineering Plastic Recycling Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 34: Europe Engineering Plastic Recycling Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 35: Europe Engineering Plastic Recycling Industry Revenue (billion), by Country 2025 & 2033

- Figure 36: Europe Engineering Plastic Recycling Industry Volume (K Tons), by Country 2025 & 2033

- Figure 37: Europe Engineering Plastic Recycling Industry Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Engineering Plastic Recycling Industry Volume Share (%), by Country 2025 & 2033

- Figure 39: Rest of the World Engineering Plastic Recycling Industry Revenue (billion), by Plastic Type 2025 & 2033

- Figure 40: Rest of the World Engineering Plastic Recycling Industry Volume (K Tons), by Plastic Type 2025 & 2033

- Figure 41: Rest of the World Engineering Plastic Recycling Industry Revenue Share (%), by Plastic Type 2025 & 2033

- Figure 42: Rest of the World Engineering Plastic Recycling Industry Volume Share (%), by Plastic Type 2025 & 2033

- Figure 43: Rest of the World Engineering Plastic Recycling Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 44: Rest of the World Engineering Plastic Recycling Industry Volume (K Tons), by End-user Industry 2025 & 2033

- Figure 45: Rest of the World Engineering Plastic Recycling Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 46: Rest of the World Engineering Plastic Recycling Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 47: Rest of the World Engineering Plastic Recycling Industry Revenue (billion), by Country 2025 & 2033

- Figure 48: Rest of the World Engineering Plastic Recycling Industry Volume (K Tons), by Country 2025 & 2033

- Figure 49: Rest of the World Engineering Plastic Recycling Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Rest of the World Engineering Plastic Recycling Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Engineering Plastic Recycling Industry Revenue billion Forecast, by Plastic Type 2020 & 2033

- Table 2: Global Engineering Plastic Recycling Industry Volume K Tons Forecast, by Plastic Type 2020 & 2033

- Table 3: Global Engineering Plastic Recycling Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 4: Global Engineering Plastic Recycling Industry Volume K Tons Forecast, by End-user Industry 2020 & 2033

- Table 5: Global Engineering Plastic Recycling Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global Engineering Plastic Recycling Industry Volume K Tons Forecast, by Region 2020 & 2033

- Table 7: Global Engineering Plastic Recycling Industry Revenue billion Forecast, by Plastic Type 2020 & 2033

- Table 8: Global Engineering Plastic Recycling Industry Volume K Tons Forecast, by Plastic Type 2020 & 2033

- Table 9: Global Engineering Plastic Recycling Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 10: Global Engineering Plastic Recycling Industry Volume K Tons Forecast, by End-user Industry 2020 & 2033

- Table 11: Global Engineering Plastic Recycling Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Global Engineering Plastic Recycling Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 13: China Engineering Plastic Recycling Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: China Engineering Plastic Recycling Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 15: India Engineering Plastic Recycling Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: India Engineering Plastic Recycling Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 17: Japan Engineering Plastic Recycling Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Japan Engineering Plastic Recycling Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 19: South Korea Engineering Plastic Recycling Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: South Korea Engineering Plastic Recycling Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 21: Rest of Asia Pacific Engineering Plastic Recycling Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Rest of Asia Pacific Engineering Plastic Recycling Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 23: Global Engineering Plastic Recycling Industry Revenue billion Forecast, by Plastic Type 2020 & 2033

- Table 24: Global Engineering Plastic Recycling Industry Volume K Tons Forecast, by Plastic Type 2020 & 2033

- Table 25: Global Engineering Plastic Recycling Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 26: Global Engineering Plastic Recycling Industry Volume K Tons Forecast, by End-user Industry 2020 & 2033

- Table 27: Global Engineering Plastic Recycling Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 28: Global Engineering Plastic Recycling Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 29: United States Engineering Plastic Recycling Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: United States Engineering Plastic Recycling Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 31: Canada Engineering Plastic Recycling Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Canada Engineering Plastic Recycling Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 33: Mexico Engineering Plastic Recycling Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Mexico Engineering Plastic Recycling Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 35: Global Engineering Plastic Recycling Industry Revenue billion Forecast, by Plastic Type 2020 & 2033

- Table 36: Global Engineering Plastic Recycling Industry Volume K Tons Forecast, by Plastic Type 2020 & 2033

- Table 37: Global Engineering Plastic Recycling Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 38: Global Engineering Plastic Recycling Industry Volume K Tons Forecast, by End-user Industry 2020 & 2033

- Table 39: Global Engineering Plastic Recycling Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 40: Global Engineering Plastic Recycling Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 41: Germany Engineering Plastic Recycling Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Germany Engineering Plastic Recycling Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 43: United Kingdom Engineering Plastic Recycling Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: United Kingdom Engineering Plastic Recycling Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 45: France Engineering Plastic Recycling Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: France Engineering Plastic Recycling Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 47: Italy Engineering Plastic Recycling Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 48: Italy Engineering Plastic Recycling Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 49: Rest of Europe Engineering Plastic Recycling Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 50: Rest of Europe Engineering Plastic Recycling Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 51: Global Engineering Plastic Recycling Industry Revenue billion Forecast, by Plastic Type 2020 & 2033

- Table 52: Global Engineering Plastic Recycling Industry Volume K Tons Forecast, by Plastic Type 2020 & 2033

- Table 53: Global Engineering Plastic Recycling Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 54: Global Engineering Plastic Recycling Industry Volume K Tons Forecast, by End-user Industry 2020 & 2033

- Table 55: Global Engineering Plastic Recycling Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 56: Global Engineering Plastic Recycling Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 57: South America Engineering Plastic Recycling Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 58: South America Engineering Plastic Recycling Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 59: Middle East and Africa Engineering Plastic Recycling Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 60: Middle East and Africa Engineering Plastic Recycling Industry Volume (K Tons) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Engineering Plastic Recycling Industry?

The projected CAGR is approximately 8%.

2. Which companies are prominent players in the Engineering Plastic Recycling Industry?

Key companies in the market include REPRO-PET, Placon, Euresi Plastics SL, PolyClean Technologies, Indorama Ventures Public Company Limited, Reliance Industries Limited, Krones AG, Petco, Clean Tech UK Ltd, JFC Group, Far Eastern New Century Corporation (Phoenix Technologies), TEIJIN LIMITED, UltrePET LLC, Alpek S A B de C V, EF Plastics UK Ltd.

3. What are the main segments of the Engineering Plastic Recycling Industry?

The market segments include Plastic Type, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 5 billion as of 2022.

5. What are some drivers contributing to market growth?

Growing Emphasis on Sustainability among Consumer and Packaging Products; Increasing Use of Recycled Polyester; Other Drivers.

6. What are the notable trends driving market growth?

Packaging Industry to Dominate the Market.

7. Are there any restraints impacting market growth?

Difficulty in Collecting and Sorting Mixed Plastic; Other Restraints.

8. Can you provide examples of recent developments in the market?

October 2022: Indorama Venturas announced the opening of a PET Value bottle-to-bottle recycling plant in the Philippines in partnership with Coca-Cola Beverages Philippines.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Engineering Plastic Recycling Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Engineering Plastic Recycling Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Engineering Plastic Recycling Industry?

To stay informed about further developments, trends, and reports in the Engineering Plastic Recycling Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence