Key Insights

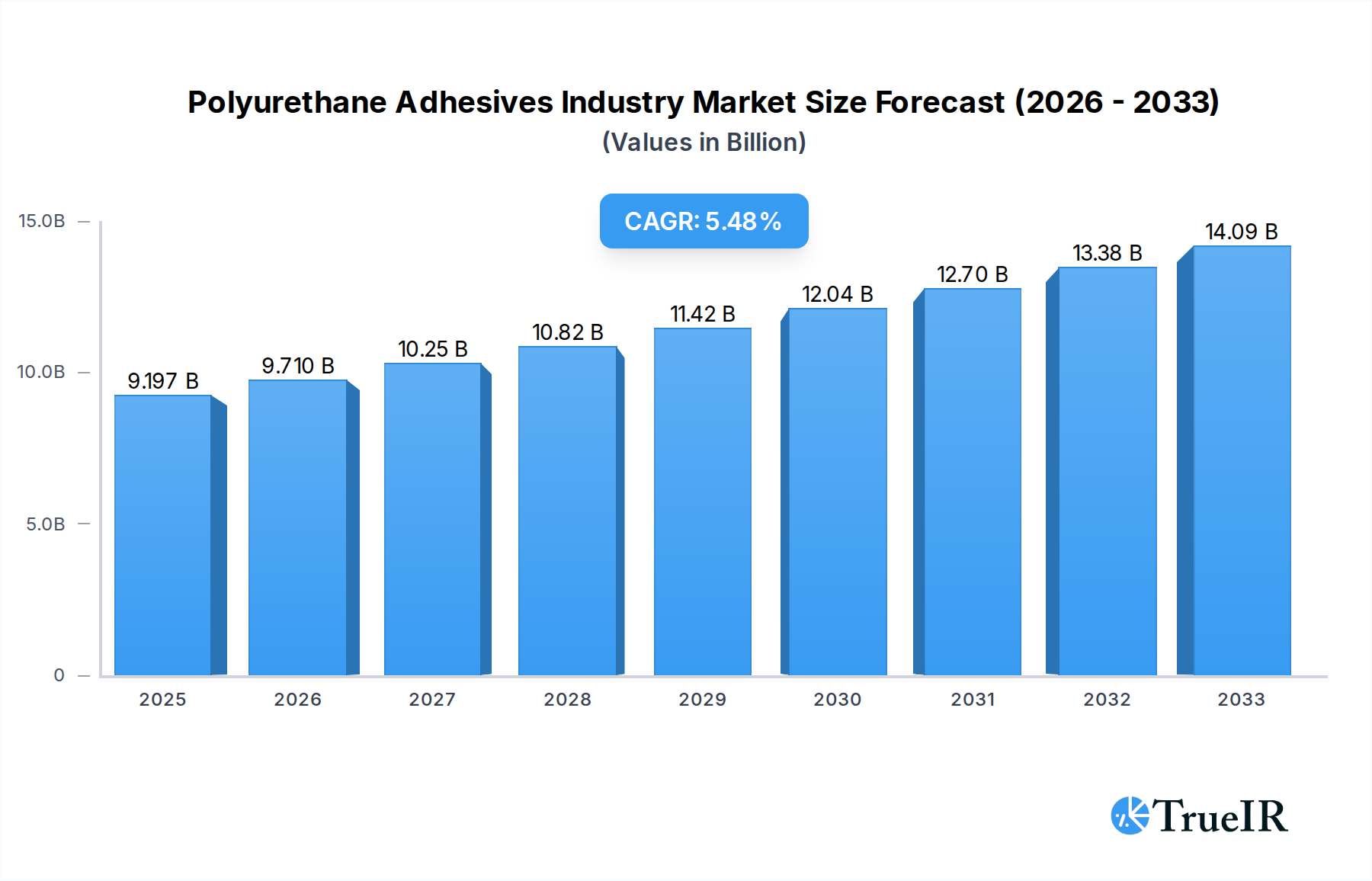

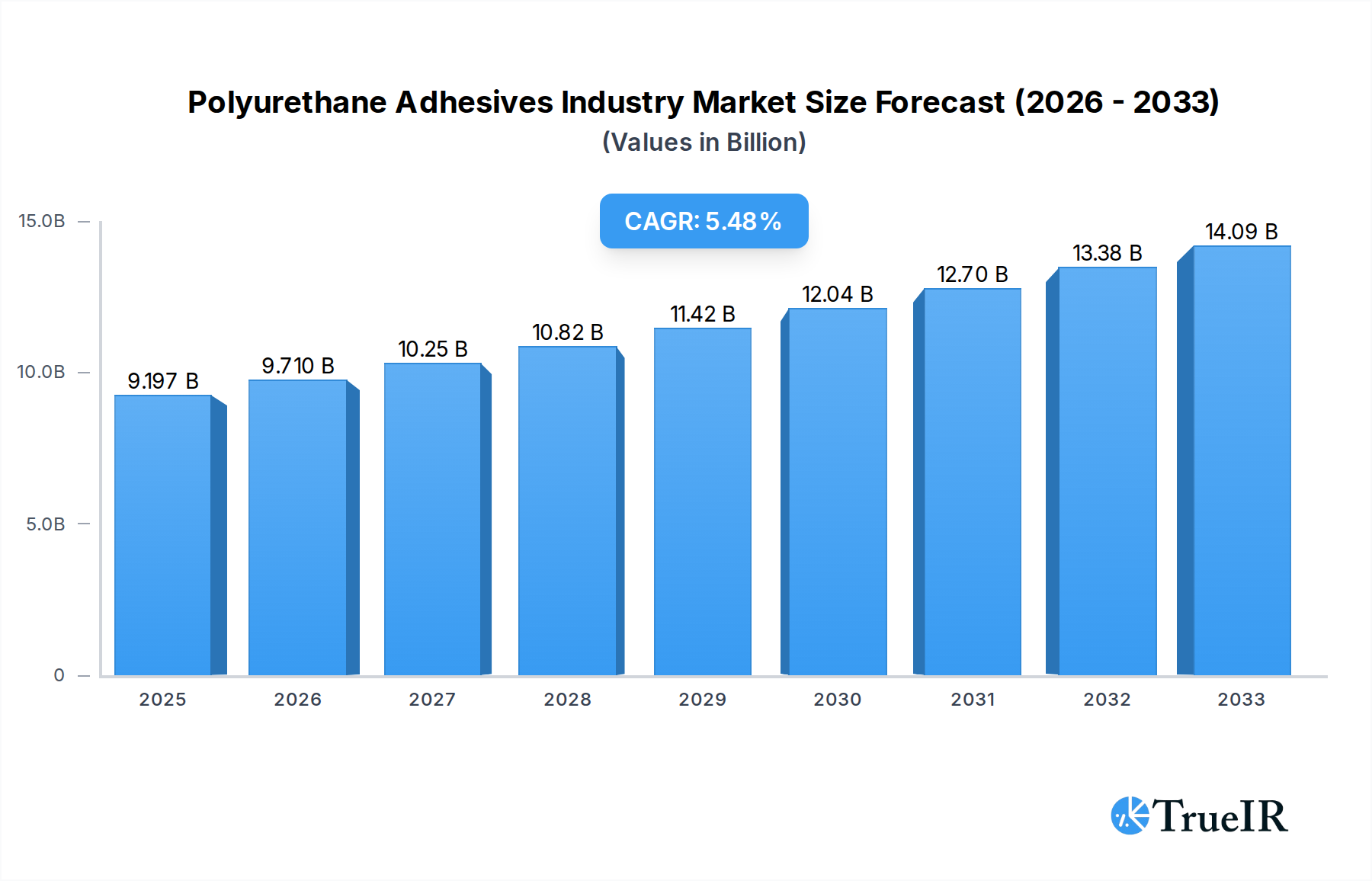

The global Polyurethane Adhesives market is poised for robust expansion, projected to reach an impressive $9196.6 million in 2025. This growth is underpinned by a steady Compound Annual Growth Rate (CAGR) of 5.62% from 2019 to 2033. The demand is significantly driven by escalating requirements from key end-user industries such as automotive and aerospace, where the need for lightweight, durable, and high-performance bonding solutions is paramount. The building and construction sector also presents substantial opportunities, with polyurethane adhesives being increasingly favored for their excellent sealing, insulating, and structural bonding properties in modern construction techniques. Furthermore, the packaging industry's continuous evolution towards sustainable and efficient packaging solutions is creating new avenues for growth, particularly for flexible and robust adhesive applications. Emerging economies, especially in the Asia Pacific region, are expected to be significant contributors to this market expansion due to rapid industrialization and increased infrastructure development.

Polyurethane Adhesives Industry Market Size (In Billion)

The market landscape is characterized by technological advancements and evolving consumer preferences, pushing manufacturers towards innovative solutions. The growing emphasis on eco-friendly and low-VOC (Volatile Organic Compound) adhesives is steering the industry towards water-borne and UV-cured technologies, offering sustainable alternatives to traditional solvent-borne systems. While the inherent strength and versatility of polyurethane adhesives present significant growth drivers, certain restraints such as fluctuating raw material prices and intense competition among established players could pose challenges. However, strategic partnerships, mergers, and acquisitions among key companies like Henkel AG & Co KGaA, Pidilite Industries Ltd, and 3M are expected to shape the competitive dynamics and drive market consolidation. The ongoing R&D efforts focused on enhancing adhesive properties like flexibility, temperature resistance, and cure speed will further solidify the market's upward trajectory.

Polyurethane Adhesives Industry Company Market Share

Polyurethane Adhesives Industry Market Insights: Global Analysis, Trends, and Forecast (2019–2033)

Report Description:

This comprehensive polyurethane adhesives market report provides an in-depth analysis of the global polyurethane adhesive industry, covering market size, growth drivers, segmentation, competitive landscape, and future outlook. Utilizing a robust research methodology, this report offers critical insights for stakeholders seeking to understand the dynamics of the polyurethane adhesive market. The study period spans from 2019 to 2033, with the base year and estimated year set at 2025, and a detailed forecast period from 2025 to 2033, encompassing historical data from 2019 to 2024. The report leverages high-volume keywords such as polyurethane adhesives market size, polyurethane adhesive industry growth, automotive adhesives market, construction adhesives market, and packaging adhesives market, to enhance SEO visibility and reach a broad industry audience. With an estimated market value projected to reach hundreds of millions, this report is an indispensable resource for understanding the evolving polyurethane adhesive applications, polyurethane adhesive technology, and the strategic moves of key players in this vibrant sector.

Polyurethane Adhesives Industry Market Structure & Competitive Landscape

The global polyurethane adhesives market is characterized by a moderately concentrated structure, with a few dominant players holding a significant market share, alongside a growing number of regional and specialized manufacturers. Innovation drivers are primarily focused on enhancing adhesive performance, such as improved bond strength, faster curing times, and greater flexibility, alongside the development of environmentally friendly polyurethane adhesives with low VOC content and increased recyclability. Regulatory impacts, particularly concerning environmental and health standards, are increasingly influencing product development and manufacturing processes, pushing for sustainable solutions. Product substitutes, while present in some niche applications, are generally unable to match the unique combination of properties offered by polyurethanes, including their versatility and durability.

End-user segmentation is critical, with the automotive adhesives market, building and construction adhesives market, and packaging adhesives market representing the largest segments by volume and value. The competitive landscape is dynamic, marked by strategic alliances, mergers, and acquisitions (M&A) as companies seek to expand their product portfolios, geographical reach, and technological capabilities. The volume of M&A activities in the polyurethane adhesive market has been substantial, with companies investing hundreds of millions to consolidate their positions and gain a competitive edge. Key competitive factors include product quality, cost-effectiveness, technical support, and the ability to offer customized solutions to diverse end-user industries. The pursuit of advanced formulations and sustainable alternatives remains a central theme in the competitive strategies of leading companies.

Polyurethane Adhesives Industry Market Trends & Opportunities

The global polyurethane adhesives market is experiencing robust growth, propelled by a multitude of interconnected trends and emerging opportunities. The market size is projected to expand significantly, driven by an estimated Compound Annual Growth Rate (CAGR) in the high single digits throughout the forecast period. This expansion is fueled by the increasing demand for high-performance bonding solutions across diverse end-user industries. Technological shifts are a major catalyst, with advancements in reactive polyurethane adhesives and hot melt polyurethane adhesives offering enhanced application flexibility and improved product performance. The shift towards water-borne and solvent-free formulations underscores a growing consumer preference for sustainable adhesives and products with lower environmental impact, opening new avenues for innovation and market penetration.

Consumer preferences are increasingly leaning towards lighter, more durable, and environmentally conscious products, directly influencing the demand for sophisticated bonding solutions like polyurethanes. In the automotive industry, for instance, the drive towards lightweighting and improved fuel efficiency necessitates advanced adhesives for structural bonding and assembly, creating substantial market opportunities. Similarly, the construction sector relies heavily on polyurethane adhesives for insulation, sealing, and structural integrity, especially with the growing focus on energy-efficient buildings. The packaging industry's need for stronger, more versatile, and recyclable packaging materials further contributes to market growth.

Competitive dynamics are intensifying, with established players investing heavily in research and development to introduce next-generation adhesives. Strategic partnerships and acquisitions are becoming more common as companies aim to broaden their technological expertise and market access. Opportunities abound for manufacturers who can develop specialized polyurethane adhesives tailored to specific application requirements, such as those in the aerospace, electronics, or medical device sectors. The increasing adoption of UV cured polyurethane adhesives in specialized applications also presents a growing niche. Furthermore, the growing disposable income and urbanization in developing economies are expected to spur demand for construction and automotive products, consequently boosting the polyurethane adhesives market in these regions. The development of bio-based polyurethane adhesives is another significant emerging opportunity, aligning with global sustainability initiatives and consumer demand for eco-friendly alternatives, potentially unlocking market penetration rates in new segments.

Dominant Markets & Segments in Polyurethane Adhesives Industry

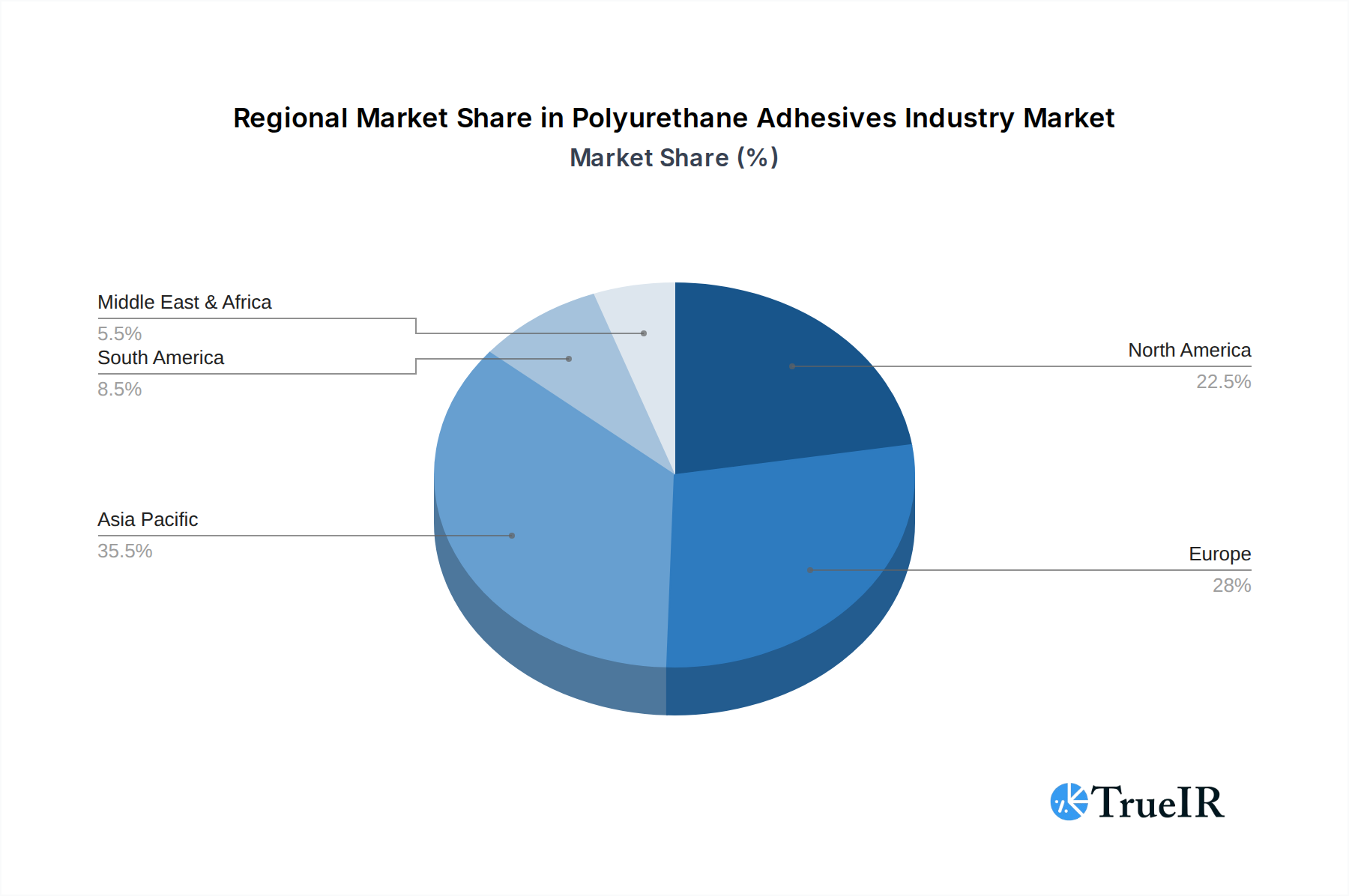

The polyurethane adhesives industry exhibits distinct patterns of dominance across geographical regions and end-user industries, driven by a confluence of economic, technological, and infrastructural factors. In terms of regional dominance, Asia Pacific is emerging as a leading market, fueled by rapid industrialization, significant investments in infrastructure development, and a burgeoning manufacturing sector, particularly in countries like China and India. The building and construction sector is a paramount segment, accounting for a substantial share of the global polyurethane adhesives market. This dominance is attributed to the increasing demand for durable, weather-resistant, and energy-efficient building materials, coupled with large-scale infrastructure projects. Government policies promoting sustainable construction practices and urban development further bolster this segment.

The automotive industry represents another pivotal segment, driven by the global demand for vehicles and the evolving needs of automotive manufacturers. Polyurethane adhesives are integral to lightweighting initiatives, structural bonding, interior trim assembly, and windshield bonding, contributing to improved fuel efficiency and enhanced safety. The increasing production of electric vehicles also presents new applications for specialized polyurethane adhesives. The packaging industry is also a significant driver, with a growing demand for high-strength, flexible, and food-grade adhesives for laminating, sealing, and labeling applications. The rise of e-commerce and the need for robust and protective packaging further amplify this segment's importance.

From a technology perspective, reactive polyurethane adhesives and hot melt polyurethane adhesives are currently the dominant technologies due to their versatility, high performance, and wide range of applications. Reactive adhesives offer superior bond strength and durability for demanding structural applications, while hot melt adhesives provide fast setting times and ease of use in high-volume production environments. However, there is a notable and increasing trend towards water-borne polyurethane adhesives and UV cured polyurethane adhesives. Water-borne adhesives are gaining traction due to their environmentally friendly nature, offering low VOC emissions and reduced health risks. UV cured adhesives are favored for applications requiring rapid curing and precise application, such as in electronics and medical devices. The growth of the footwear and leather industry, especially in emerging economies, also contributes to the demand for polyurethane adhesives for bonding various materials. The aerospace and healthcare sectors, while smaller in volume, represent high-value segments where specialized, high-performance polyurethane adhesives are crucial for critical applications.

Polyurethane Adhesives Industry Product Analysis

The polyurethane adhesives market is distinguished by a continuous stream of product innovations aimed at enhancing performance, sustainability, and application efficiency. Key product advancements include the development of high-strength reactive polyurethane adhesives with rapid curing capabilities for demanding automotive and construction applications, as well as flexible polyurethane adhesives that offer excellent vibration and impact resistance. The industry is also witnessing significant innovation in sustainable polyurethane adhesive formulations, including water-borne and bio-based options, designed to meet stringent environmental regulations and evolving consumer preferences. These products offer competitive advantages by providing reduced VOC emissions, improved recyclability, and a safer working environment. The versatility of polyurethane chemistry allows for tailored solutions, addressing specific needs in sectors like packaging, woodworking, and electronics, further solidifying their market position.

Key Drivers, Barriers & Challenges in Polyurethane Adhesives Industry

The polyurethane adhesives industry is propelled by several key drivers, including the escalating demand from the automotive sector for lightweighting and structural integrity, and the robust growth in the building and construction industry, driven by infrastructure development and urban expansion. Technological advancements, leading to improved adhesive performance and sustainability, are also significant growth catalysts. Economic growth in emerging markets, coupled with favorable government policies supporting industrial manufacturing and construction, further fuels market expansion.

However, the industry faces notable barriers and challenges. The fluctuating raw material prices, particularly for isocyanates and polyols, can impact profitability and pricing strategies. Stringent environmental regulations concerning VOC emissions and chemical safety can necessitate significant investment in R&D and process modifications. Intense competitive pressure from alternative adhesive technologies and established players can also pose a challenge, particularly in price-sensitive segments. Supply chain disruptions, as witnessed globally, can affect the availability and cost of raw materials, impacting production schedules and lead times. Furthermore, the specialized nature of some polyurethane adhesive applications requires significant technical expertise for implementation, which can be a barrier to adoption for smaller enterprises.

Growth Drivers in the Polyurethane Adhesives Industry Market

The polyurethane adhesives market is experiencing significant growth, driven by several interconnected factors. Technologically, innovations in formulations are yielding adhesives with superior bond strength, flexibility, and faster curing times, catering to increasingly demanding applications. Economically, global economic recovery and expansion, particularly in developing nations, are fueling demand in key end-user industries such as construction and automotive manufacturing. Favorable government policies promoting infrastructure development, sustainable building practices, and automotive manufacturing incentives also play a crucial role. The increasing emphasis on lightweighting in the automotive sector to improve fuel efficiency and the growing trend towards prefabrication and modular construction in building and construction are major growth catalysts. The expanding packaging industry, driven by e-commerce and consumer goods, further contributes to the robust demand for reliable and versatile adhesive solutions.

Challenges Impacting Polyurethane Adhesives Industry Growth

The growth of the polyurethane adhesives industry faces several significant challenges. Regulatory complexities and evolving environmental standards, particularly concerning the use of certain chemicals and VOC emissions, necessitate continuous investment in research and development for compliant formulations. Supply chain issues, including the availability and price volatility of key raw materials like isocyanates and polyols, can significantly impact production costs and delivery timelines. Competitive pressures from alternative adhesive technologies and the presence of numerous market players lead to price sensitivity in certain segments. The need for specialized application equipment and technical expertise for certain high-performance polyurethane adhesives can also act as a barrier to wider adoption, especially for smaller end-users. Furthermore, the global economic uncertainties and geopolitical events can lead to fluctuations in demand from key end-user industries.

Key Players Shaping the Polyurethane Adhesives Industry Market

- Henkel AG & Co KGaA

- Pidilite Industries Ltd

- 3M

- Kangda New Materials (Group) Co Ltd

- Beijing Comens New Materials Co Ltd

- Hubei Huitian New Materials Co Ltd

- NANPAO RESINS CHEMICAL GROUP

- Arkema Group

- Huntsman International LLC

- Dow

- H B Fuller Company

- Soudal Holding N V

- MAPEI S p A

- Sika AG

- Jowat SE

Significant Polyurethane Adhesives Industry Industry Milestones

- July 2022: Mapei started the construction of its third manufacturing facility in Kosi, Mathura, to cater to the demand generated from Northern India, indicating expansion and increased production capacity to meet regional market needs.

- May 2022: Henkel introduced new products, such as Loctite Liofol LA 7818 RE / 6231 RE and Loctite Liofol LA 7102 RE / 6902 RE, to promote recyclability in the packaging industry, highlighting a strategic focus on sustainable solutions and innovation in the packaging adhesives sector.

- February 2022: Arkema Group completed the acquisition of Ashland's Performance Adhesives business. Ashland is a world leader in high-performance adhesives in the United States, demonstrating a significant consolidation move within the industry and an expansion of Arkema's product portfolio and market presence in high-performance adhesives.

Future Outlook for Polyurethane Adhesives Industry Market

The future outlook for the polyurethane adhesives market is exceptionally promising, driven by sustained innovation and increasing demand across diverse sectors. Strategic opportunities lie in the development of advanced, high-performance adhesives that cater to the evolving needs of the automotive industry, particularly with the rise of electric vehicles and the continuous pursuit of lightweighting. The growing global emphasis on sustainable construction practices will continue to fuel demand for eco-friendly polyurethane adhesives, including water-borne and low-VOC formulations. Furthermore, the expansion of e-commerce and the increasing demand for robust and protective packaging solutions present significant growth potential for the packaging adhesives segment. Investments in research and development for bio-based and recyclable polyurethane adhesives are expected to open new market avenues and enhance market penetration. The market's trajectory indicates continued growth, with an estimated market value poised to reach hundreds of millions by the end of the forecast period, driven by technological advancements and expanding application areas.

Polyurethane Adhesives Industry Segmentation

-

1. End User Industry

- 1.1. Aerospace

- 1.2. Automotive

- 1.3. Building and Construction

- 1.4. Footwear and Leather

- 1.5. Healthcare

- 1.6. Packaging

- 1.7. Woodworking and Joinery

- 1.8. Other End-user Industries

-

2. Technology

- 2.1. Hot Melt

- 2.2. Reactive

- 2.3. Solvent-borne

- 2.4. UV Cured Adhesives

- 2.5. Water-borne

Polyurethane Adhesives Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Polyurethane Adhesives Industry Regional Market Share

Geographic Coverage of Polyurethane Adhesives Industry

Polyurethane Adhesives Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.62% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by End User Industry

- 5.1.1. Aerospace

- 5.1.2. Automotive

- 5.1.3. Building and Construction

- 5.1.4. Footwear and Leather

- 5.1.5. Healthcare

- 5.1.6. Packaging

- 5.1.7. Woodworking and Joinery

- 5.1.8. Other End-user Industries

- 5.2. Market Analysis, Insights and Forecast - by Technology

- 5.2.1. Hot Melt

- 5.2.2. Reactive

- 5.2.3. Solvent-borne

- 5.2.4. UV Cured Adhesives

- 5.2.5. Water-borne

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by End User Industry

- 6. Global Polyurethane Adhesives Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by End User Industry

- 6.1.1. Aerospace

- 6.1.2. Automotive

- 6.1.3. Building and Construction

- 6.1.4. Footwear and Leather

- 6.1.5. Healthcare

- 6.1.6. Packaging

- 6.1.7. Woodworking and Joinery

- 6.1.8. Other End-user Industries

- 6.2. Market Analysis, Insights and Forecast - by Technology

- 6.2.1. Hot Melt

- 6.2.2. Reactive

- 6.2.3. Solvent-borne

- 6.2.4. UV Cured Adhesives

- 6.2.5. Water-borne

- 6.1. Market Analysis, Insights and Forecast - by End User Industry

- 7. North America Polyurethane Adhesives Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by End User Industry

- 7.1.1. Aerospace

- 7.1.2. Automotive

- 7.1.3. Building and Construction

- 7.1.4. Footwear and Leather

- 7.1.5. Healthcare

- 7.1.6. Packaging

- 7.1.7. Woodworking and Joinery

- 7.1.8. Other End-user Industries

- 7.2. Market Analysis, Insights and Forecast - by Technology

- 7.2.1. Hot Melt

- 7.2.2. Reactive

- 7.2.3. Solvent-borne

- 7.2.4. UV Cured Adhesives

- 7.2.5. Water-borne

- 7.1. Market Analysis, Insights and Forecast - by End User Industry

- 8. South America Polyurethane Adhesives Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by End User Industry

- 8.1.1. Aerospace

- 8.1.2. Automotive

- 8.1.3. Building and Construction

- 8.1.4. Footwear and Leather

- 8.1.5. Healthcare

- 8.1.6. Packaging

- 8.1.7. Woodworking and Joinery

- 8.1.8. Other End-user Industries

- 8.2. Market Analysis, Insights and Forecast - by Technology

- 8.2.1. Hot Melt

- 8.2.2. Reactive

- 8.2.3. Solvent-borne

- 8.2.4. UV Cured Adhesives

- 8.2.5. Water-borne

- 8.1. Market Analysis, Insights and Forecast - by End User Industry

- 9. Europe Polyurethane Adhesives Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by End User Industry

- 9.1.1. Aerospace

- 9.1.2. Automotive

- 9.1.3. Building and Construction

- 9.1.4. Footwear and Leather

- 9.1.5. Healthcare

- 9.1.6. Packaging

- 9.1.7. Woodworking and Joinery

- 9.1.8. Other End-user Industries

- 9.2. Market Analysis, Insights and Forecast - by Technology

- 9.2.1. Hot Melt

- 9.2.2. Reactive

- 9.2.3. Solvent-borne

- 9.2.4. UV Cured Adhesives

- 9.2.5. Water-borne

- 9.1. Market Analysis, Insights and Forecast - by End User Industry

- 10. Middle East & Africa Polyurethane Adhesives Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by End User Industry

- 10.1.1. Aerospace

- 10.1.2. Automotive

- 10.1.3. Building and Construction

- 10.1.4. Footwear and Leather

- 10.1.5. Healthcare

- 10.1.6. Packaging

- 10.1.7. Woodworking and Joinery

- 10.1.8. Other End-user Industries

- 10.2. Market Analysis, Insights and Forecast - by Technology

- 10.2.1. Hot Melt

- 10.2.2. Reactive

- 10.2.3. Solvent-borne

- 10.2.4. UV Cured Adhesives

- 10.2.5. Water-borne

- 10.1. Market Analysis, Insights and Forecast - by End User Industry

- 11. Asia Pacific Polyurethane Adhesives Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by End User Industry

- 11.1.1. Aerospace

- 11.1.2. Automotive

- 11.1.3. Building and Construction

- 11.1.4. Footwear and Leather

- 11.1.5. Healthcare

- 11.1.6. Packaging

- 11.1.7. Woodworking and Joinery

- 11.1.8. Other End-user Industries

- 11.2. Market Analysis, Insights and Forecast - by Technology

- 11.2.1. Hot Melt

- 11.2.2. Reactive

- 11.2.3. Solvent-borne

- 11.2.4. UV Cured Adhesives

- 11.2.5. Water-borne

- 11.1. Market Analysis, Insights and Forecast - by End User Industry

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Henkel AG & Co KGaA

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Pidilite Industries Ltd

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 3M

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Kangda New Materials (Group) Co Ltd

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Beijing Comens New Materials Co Ltd

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Hubei Huitian New Materials Co Ltd

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 NANPAO RESINS CHEMICAL GROUP

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Arkema Group

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Huntsman International LLC

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Dow

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 H B Fuller Company

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Soudal Holding N V

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 MAPEI S p A

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Sika AG

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Jowat SE

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.1 Henkel AG & Co KGaA

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Polyurethane Adhesives Industry Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Polyurethane Adhesives Industry Revenue (million), by End User Industry 2025 & 2033

- Figure 3: North America Polyurethane Adhesives Industry Revenue Share (%), by End User Industry 2025 & 2033

- Figure 4: North America Polyurethane Adhesives Industry Revenue (million), by Technology 2025 & 2033

- Figure 5: North America Polyurethane Adhesives Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 6: North America Polyurethane Adhesives Industry Revenue (million), by Country 2025 & 2033

- Figure 7: North America Polyurethane Adhesives Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Polyurethane Adhesives Industry Revenue (million), by End User Industry 2025 & 2033

- Figure 9: South America Polyurethane Adhesives Industry Revenue Share (%), by End User Industry 2025 & 2033

- Figure 10: South America Polyurethane Adhesives Industry Revenue (million), by Technology 2025 & 2033

- Figure 11: South America Polyurethane Adhesives Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 12: South America Polyurethane Adhesives Industry Revenue (million), by Country 2025 & 2033

- Figure 13: South America Polyurethane Adhesives Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Polyurethane Adhesives Industry Revenue (million), by End User Industry 2025 & 2033

- Figure 15: Europe Polyurethane Adhesives Industry Revenue Share (%), by End User Industry 2025 & 2033

- Figure 16: Europe Polyurethane Adhesives Industry Revenue (million), by Technology 2025 & 2033

- Figure 17: Europe Polyurethane Adhesives Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 18: Europe Polyurethane Adhesives Industry Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Polyurethane Adhesives Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Polyurethane Adhesives Industry Revenue (million), by End User Industry 2025 & 2033

- Figure 21: Middle East & Africa Polyurethane Adhesives Industry Revenue Share (%), by End User Industry 2025 & 2033

- Figure 22: Middle East & Africa Polyurethane Adhesives Industry Revenue (million), by Technology 2025 & 2033

- Figure 23: Middle East & Africa Polyurethane Adhesives Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 24: Middle East & Africa Polyurethane Adhesives Industry Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Polyurethane Adhesives Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Polyurethane Adhesives Industry Revenue (million), by End User Industry 2025 & 2033

- Figure 27: Asia Pacific Polyurethane Adhesives Industry Revenue Share (%), by End User Industry 2025 & 2033

- Figure 28: Asia Pacific Polyurethane Adhesives Industry Revenue (million), by Technology 2025 & 2033

- Figure 29: Asia Pacific Polyurethane Adhesives Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 30: Asia Pacific Polyurethane Adhesives Industry Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Polyurethane Adhesives Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Polyurethane Adhesives Industry Revenue million Forecast, by End User Industry 2020 & 2033

- Table 2: Global Polyurethane Adhesives Industry Revenue million Forecast, by Technology 2020 & 2033

- Table 3: Global Polyurethane Adhesives Industry Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Polyurethane Adhesives Industry Revenue million Forecast, by End User Industry 2020 & 2033

- Table 5: Global Polyurethane Adhesives Industry Revenue million Forecast, by Technology 2020 & 2033

- Table 6: Global Polyurethane Adhesives Industry Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Polyurethane Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Polyurethane Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Polyurethane Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Polyurethane Adhesives Industry Revenue million Forecast, by End User Industry 2020 & 2033

- Table 11: Global Polyurethane Adhesives Industry Revenue million Forecast, by Technology 2020 & 2033

- Table 12: Global Polyurethane Adhesives Industry Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Polyurethane Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Polyurethane Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Polyurethane Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Polyurethane Adhesives Industry Revenue million Forecast, by End User Industry 2020 & 2033

- Table 17: Global Polyurethane Adhesives Industry Revenue million Forecast, by Technology 2020 & 2033

- Table 18: Global Polyurethane Adhesives Industry Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Polyurethane Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Polyurethane Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Polyurethane Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Polyurethane Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Polyurethane Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Polyurethane Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Polyurethane Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Polyurethane Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Polyurethane Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Polyurethane Adhesives Industry Revenue million Forecast, by End User Industry 2020 & 2033

- Table 29: Global Polyurethane Adhesives Industry Revenue million Forecast, by Technology 2020 & 2033

- Table 30: Global Polyurethane Adhesives Industry Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Polyurethane Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Polyurethane Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Polyurethane Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Polyurethane Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Polyurethane Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Polyurethane Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Polyurethane Adhesives Industry Revenue million Forecast, by End User Industry 2020 & 2033

- Table 38: Global Polyurethane Adhesives Industry Revenue million Forecast, by Technology 2020 & 2033

- Table 39: Global Polyurethane Adhesives Industry Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Polyurethane Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Polyurethane Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Polyurethane Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Polyurethane Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Polyurethane Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Polyurethane Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Polyurethane Adhesives Industry Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Polyurethane Adhesives Industry?

The projected CAGR is approximately 5.62%.

2. Which companies are prominent players in the Polyurethane Adhesives Industry?

Key companies in the market include Henkel AG & Co KGaA, Pidilite Industries Ltd, 3M, Kangda New Materials (Group) Co Ltd, Beijing Comens New Materials Co Ltd, Hubei Huitian New Materials Co Ltd, NANPAO RESINS CHEMICAL GROUP, Arkema Group, Huntsman International LLC, Dow, H B Fuller Company, Soudal Holding N V, MAPEI S p A, Sika AG, Jowat SE.

3. What are the main segments of the Polyurethane Adhesives Industry?

The market segments include End User Industry, Technology.

4. Can you provide details about the market size?

The market size is estimated to be USD 9196.6 million as of 2022.

5. What are some drivers contributing to market growth?

Rising Demand from the Construction Industry in Saudi Arabia; Other Drivers.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

; Impact of COVID-19 Pandemic on Global Economy.

8. Can you provide examples of recent developments in the market?

July 2022: Mapei started the construction of its third manufacturing facility in Kosi, Mathura, to cater to the demand generated from Northern India.May 2022: Henkel introduced new products, such as Loctite Liofol LA 7818 RE / 6231 RE and Loctite Liofol LA 7102 RE / 6902 RE, to promote recyclability in the packaging industry.February 2022: Arkema Group completed the acquisition of Ashland's Performance Adhesives business. Ashland is a world leader in high-performance adhesives in the United States.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Polyurethane Adhesives Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Polyurethane Adhesives Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Polyurethane Adhesives Industry?

To stay informed about further developments, trends, and reports in the Polyurethane Adhesives Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence