Key Insights

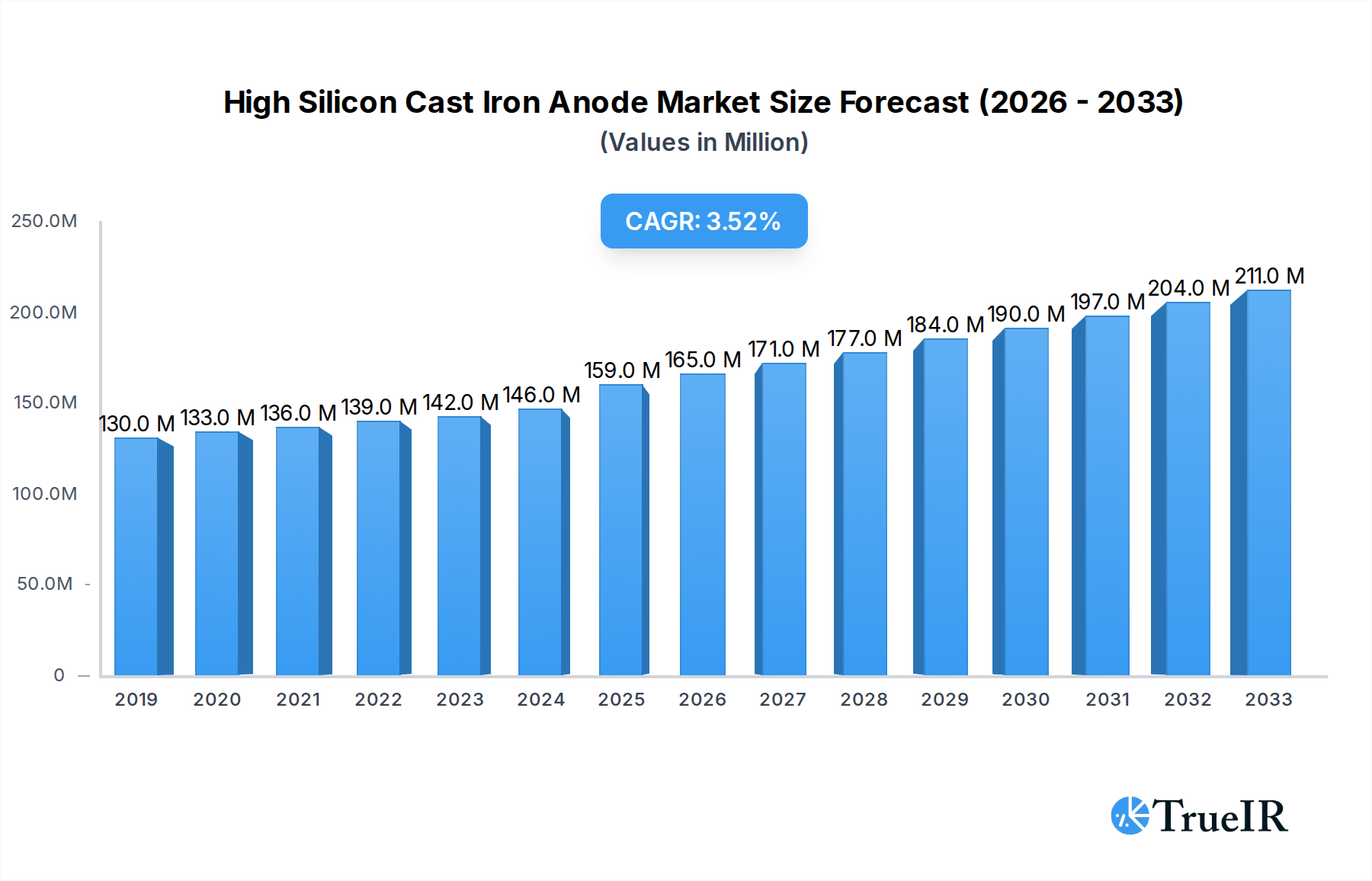

The High Silicon Cast Iron Anode market is poised for robust expansion, projected to reach a significant $159 million by 2025, driven by a steady compound annual growth rate (CAGR) of 3.9% through 2033. This growth is primarily fueled by the escalating demand for corrosion protection solutions across a multitude of industries. The chemical industry, in particular, presents a substantial opportunity due to its stringent requirements for material integrity and longevity in corrosive environments. Furthermore, the metal protection sector, encompassing infrastructure like pipelines, bridges, and offshore structures, relies heavily on these anodes to prevent costly degradation. Emerging applications, though smaller in current scale, are also contributing to the market's upward trajectory, indicating a broadening acceptance and utility of high silicon cast iron anodes. The increasing awareness of the economic benefits of proactive corrosion prevention, including reduced maintenance costs and extended asset lifespans, is a key determinant in this market's growth.

High Silicon Cast Iron Anode Market Size (In Million)

The market's expansion is further supported by technological advancements in anode design and manufacturing, leading to more efficient and durable products. The global focus on extending the lifespan of critical infrastructure and industrial assets, coupled with stricter environmental regulations that mandate the preservation of materials, are significant underlying drivers. While the market benefits from widespread adoption, certain factors could influence the pace of growth. High initial installation costs and the availability of alternative corrosion prevention methods might present challenges. However, the superior performance and longevity of high silicon cast iron anodes in demanding applications are expected to outweigh these concerns. The market is segmented by application and type, with Anode Plates and Anode Bars forming the primary product categories, catering to diverse industrial needs. Geographically, North America and Europe currently dominate, with Asia Pacific showing the most promising growth potential due to rapid industrialization and infrastructure development.

High Silicon Cast Iron Anode Company Market Share

This in-depth report provides an exhaustive analysis of the global High Silicon Cast Iron Anode market, covering historical trends, current dynamics, and future projections. Leveraging millions of data points and expert insights, this study is indispensable for stakeholders seeking to understand market structure, competitive landscape, key trends, and growth opportunities. The report spans the Study Period of 2019–2033, with a Base Year of 2025, an Estimated Year of 2025, and a Forecast Period of 2025–2033, building upon the Historical Period of 2019–2024.

High Silicon Cast Iron Anode Market Structure & Competitive Landscape

The global High Silicon Cast Iron Anode market exhibits a moderately concentrated structure, with the top 5-7 companies accounting for approximately 60% of the market share. This concentration is driven by high capital investment requirements, proprietary manufacturing technologies, and established distribution networks. Innovation is a key differentiator, with ongoing research focused on improving anode lifespan, reducing consumption rates, and enhancing electrochemical performance. Regulatory frameworks, particularly concerning environmental impact and safety standards for cathodic protection systems, play a significant role in shaping market entry and product development. Product substitutes, such as mixed metal oxide anodes and impressed current cathodic protection (ICCP) systems, present competition, especially in niche applications. End-user segmentation reveals a strong reliance on the Chemical Industry and Metal Protection sectors. Mergers and Acquisitions (M&A) activity has been moderate, with approximately 10-15 significant deals observed over the historical period, primarily aimed at expanding geographical reach and product portfolios. The market's overall health is robust, with a projected Compound Annual Growth Rate (CAGR) of around 5.5% over the forecast period.

High Silicon Cast Iron Anode Market Trends & Opportunities

The High Silicon Cast Iron Anode market is poised for significant expansion, driven by the escalating need for effective corrosion prevention across a multitude of industrial applications. The global market size is estimated to reach over $1,500 million by 2033, growing at a CAGR of approximately 5.5% from 2025. This growth is underpinned by several evolving trends and emerging opportunities.

Technological advancements are at the forefront of market development. Manufacturers are continuously innovating to enhance the durability, efficiency, and longevity of high silicon cast iron anodes. This includes developing new alloy compositions that offer superior resistance to corrosive environments, leading to reduced replacement cycles and lower operational costs for end-users. Furthermore, improvements in manufacturing processes are leading to more consistent product quality and a wider range of customizable anode shapes and sizes, catering to specific project requirements. The market is witnessing a growing demand for anodes designed for harsh and aggressive environments, such as offshore oil and gas platforms, chemical processing plants, and marine structures, where corrosion poses a severe threat to structural integrity and operational continuity.

Consumer preferences are shifting towards more sustainable and cost-effective corrosion mitigation solutions. High silicon cast iron anodes, known for their reliability and relatively long service life, align well with these preferences. Their primary application in sacrificial cathodic protection makes them an attractive choice for long-term asset protection. The increasing focus on infrastructure development and maintenance worldwide is a major catalyst for market growth. Aging infrastructure in sectors like oil and gas, water treatment, and transportation requires robust corrosion protection to ensure safety and extend asset lifespan. As governments and private entities invest heavily in maintaining and upgrading these critical assets, the demand for high silicon cast iron anodes is expected to surge.

Competitive dynamics within the market are characterized by a blend of established global players and regional specialists. Companies are increasingly focusing on strategic partnerships, collaborations, and expanding their service offerings to include complete cathodic protection system design, installation, and monitoring. This integrated approach allows them to capture a larger share of the project value chain. The drive towards digitalization and the use of advanced monitoring techniques for corrosion is also creating new opportunities. Smart anodes equipped with sensors that can transmit real-time performance data are gaining traction, enabling proactive maintenance and optimized system performance. The penetration rate of high silicon cast iron anodes in various applications is steadily increasing as their cost-effectiveness and reliability become more widely recognized. The market is expected to witness sustained growth as these trends continue to shape the demand for corrosion protection solutions globally.

Dominant Markets & Segments in High Silicon Cast Iron Anode

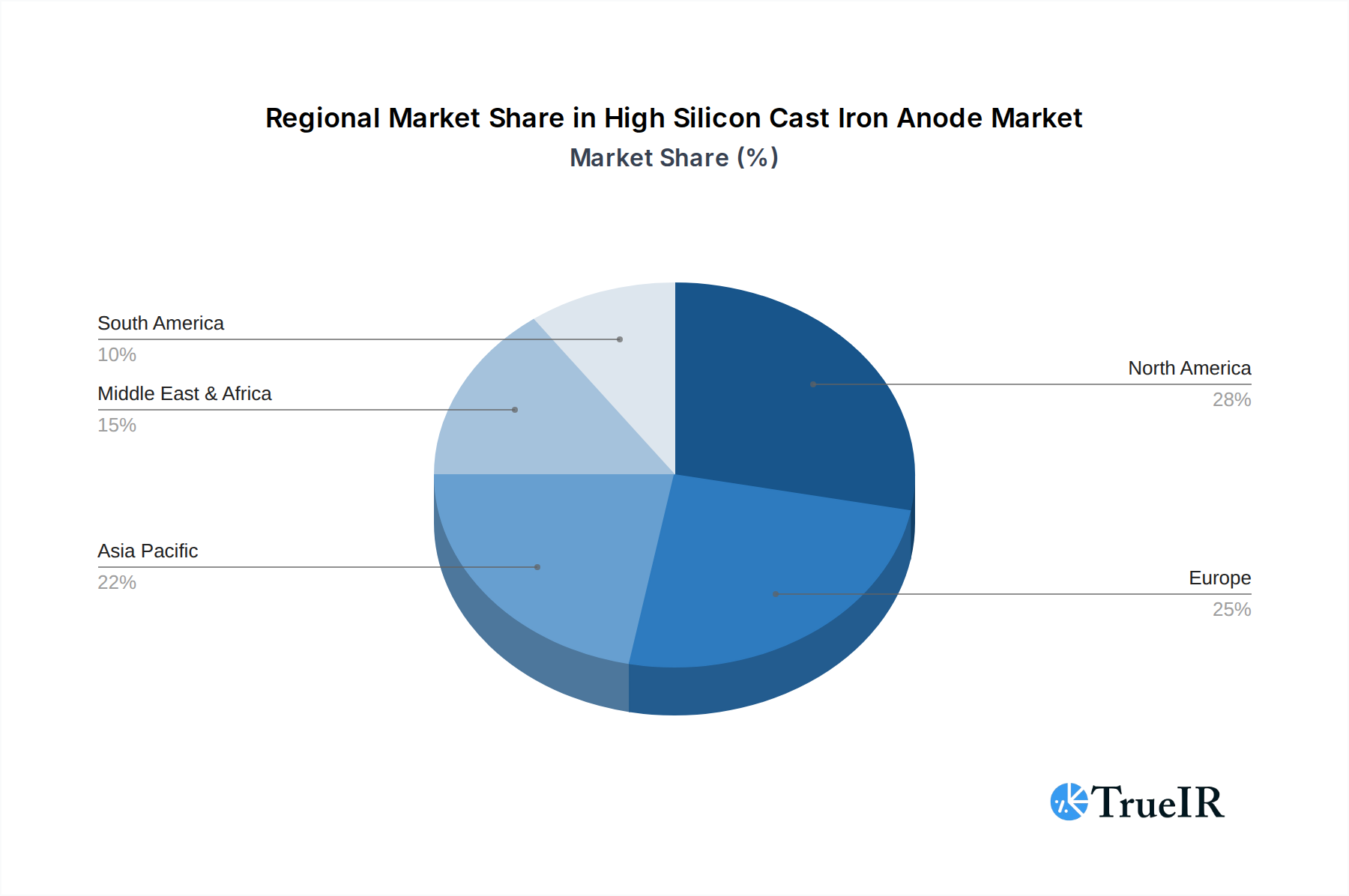

The global High Silicon Cast Iron Anode market is characterized by distinct regional dominance and strong performance within specific application and product type segments. North America currently holds the leading position, largely driven by its extensive oil and gas infrastructure, robust chemical industry, and significant investments in infrastructure maintenance and upgrades. The United States, in particular, accounts for a substantial portion of the regional market share, owing to stringent regulations on asset integrity and a proactive approach to corrosion management.

Application Segment Dominance:

- Chemical Industry: This segment is a primary growth engine. The aggressive nature of chemicals processed in this industry necessitates highly effective corrosion protection for tanks, pipelines, and processing equipment. The high silicon cast iron anodes are favored for their resistance to various chemical environments, ensuring extended equipment life and preventing costly downtime. The projected market size for this segment is estimated to exceed $600 million by 2033.

- Metal Protection: This broad category encompasses a wide array of applications including marine structures (ships, offshore platforms, ports), pipelines (oil, gas, water), bridges, and other exposed metal assets. The sheer volume of metallic infrastructure requiring protection makes this segment a cornerstone of the market. The ongoing global efforts to maintain and replace aging infrastructure directly fuel demand in this segment. Estimated market size by 2033 is projected to be over $700 million.

- Others: This segment includes niche applications such as wastewater treatment facilities, nuclear power plants, and industrial water systems. While individually smaller, the cumulative demand from these diverse sectors contributes significantly to overall market growth.

Type Segment Dominance:

- Anode Plate: Anode plates are widely utilized due to their versatility and ease of installation in various configurations. Their large surface area makes them efficient for widespread protection of structures like ship hulls, tank bottoms, and pipeline coatings. The market for anode plates is expected to reach over $900 million by 2033.

- Anode Bar: Anode bars are preferred for targeted protection in specific areas or for integration into larger cathodic protection systems. Their robust design makes them suitable for demanding applications in pipelines and bridge decks. The market for anode bars is estimated to exceed $500 million by 2033.

- Others: This category includes specialized anode shapes and custom-designed configurations for unique applications.

Key growth drivers across these dominant markets include increased infrastructure spending, stringent environmental and safety regulations mandating corrosion control, and the growing awareness of the economic benefits of proactive corrosion management. Favorable government policies promoting industrial development and the protection of critical assets further bolster market expansion.

High Silicon Cast Iron Anode Product Analysis

High silicon cast iron anodes are characterized by their superior electrochemical performance and robust resistance to corrosive environments. Their high silicon content (typically 14-16%) significantly enhances their passivation layer formation, providing excellent self-regulating properties and minimizing consumption rates. Key product innovations include advanced manufacturing techniques that ensure uniform alloy composition and improved surface finish, leading to predictable performance and extended lifespan. These anodes are ideally suited for sacrificial cathodic protection in saline and soil environments, offering a cost-effective solution for protecting steel structures in applications like buried pipelines, marine pilings, and water tanks. Their competitive advantage lies in their reliability, ease of installation, and compatibility with various electrolyte conditions, making them a preferred choice for long-term asset integrity.

Key Drivers, Barriers & Challenges in High Silicon Cast Iron Anode

Key Drivers:

- Increasing Infrastructure Development: Global investments in new infrastructure projects, particularly in energy, transportation, and water management sectors, directly drive the demand for corrosion protection solutions.

- Aging Infrastructure Maintenance: The need to extend the lifespan of existing infrastructure necessitates robust corrosion control measures, making high silicon cast iron anodes a critical component.

- Stringent Environmental Regulations: Growing concerns about environmental safety and the impact of corrosion-induced leaks or failures compel industries to adopt effective protective systems.

- Cost-Effectiveness: Compared to some advanced alloys or impressed current systems, high silicon cast iron anodes offer a more economical solution for many applications, particularly for long-term sacrificial protection.

- Technological Advancements in Manufacturing: Improved production processes lead to higher quality, more consistent, and specialized anode designs, expanding their applicability.

Barriers & Challenges:

- Availability and Cost of Raw Materials: Fluctuations in the price and availability of key raw materials like silicon and iron can impact production costs and, consequently, anode pricing.

- Competition from Alternative Technologies: Impressed Current Cathodic Protection (ICCP) systems and other advanced anode materials (e.g., MMO) offer alternatives that may be perceived as more efficient or suitable for specific, highly demanding environments, posing a competitive threat.

- Technical Expertise Requirements: Proper design, installation, and monitoring of cathodic protection systems require specialized knowledge, which can be a barrier to adoption in less technically advanced regions or smaller companies.

- Limited Application in Extremely Aggressive Environments: While versatile, in extremely aggressive or high-temperature environments, other anode types might offer superior performance, limiting the market share of high silicon cast iron anodes.

- Supply Chain Disruptions: Global supply chain vulnerabilities can affect the timely delivery of raw materials and finished products, impacting project timelines and costs.

Growth Drivers in the High Silicon Cast Iron Anode Market

The High Silicon Cast Iron Anode market's growth is propelled by a confluence of critical factors. The escalating global investments in new infrastructure, particularly in the oil and gas, chemical, and water treatment industries, represent a significant demand catalyst. Furthermore, the imperative to maintain and extend the lifespan of aging infrastructure worldwide necessitates effective corrosion control measures, making these anodes indispensable. Stringent environmental regulations and a growing emphasis on asset integrity and safety are compelling industries to adopt robust protective systems. Economically, the inherent cost-effectiveness of high silicon cast iron anodes, especially for long-term sacrificial protection, makes them a preferred choice over more expensive alternatives. Technological advancements in manufacturing are also playing a crucial role, leading to improved product quality, consistency, and the development of specialized anode designs that cater to an ever-wider range of applications.

Challenges Impacting High Silicon Cast Iron Anode Growth

Despite the robust growth potential, the High Silicon Cast Iron Anode market faces several challenges that can impede its expansion. Fluctuations in the price and availability of key raw materials, such as silicon and iron, can directly impact production costs and affect pricing strategies, potentially making them less competitive. The market is also subject to competition from alternative corrosion protection technologies, most notably Impressed Current Cathodic Protection (ICCP) systems and advanced anode materials like Mixed Metal Oxide (MMO), which can offer advantages in specific, highly demanding applications. A significant barrier can be the requirement for specialized technical expertise in the design, installation, and monitoring of cathodic protection systems, which can limit adoption in regions or by companies with less technical capacity. Moreover, while versatile, high silicon cast iron anodes might not be the optimal solution for extremely aggressive or high-temperature environments, where other anode types may offer superior performance, thereby capping their market share in certain niches. Finally, global supply chain vulnerabilities and potential disruptions can impact the timely delivery of raw materials and finished products, leading to project delays and increased costs.

Key Players Shaping the High Silicon Cast Iron Anode Market

- Corrosion Group

- Cathtect

- BAC Corrosion Control

- Cathwell

- Farwest Corrosion

- Sychem

- Cathodic Protection

- German Cathodic Protection

- Corrosion Service

- Pipeline Maintenance

- Jennings Anodes

- BSS Technologies

- Korf KB

- Tecnoseal Industry

- Matcor

- Stanford Advanced Materials

Significant High Silicon Cast Iron Anode Industry Milestones

- 2019: Increased adoption of advanced alloy formulations for enhanced anode lifespan in marine applications.

- 2020: Growth in demand for high silicon cast iron anodes for protection of offshore wind farm foundations.

- 2021: Introduction of more efficient manufacturing processes leading to reduced production costs.

- 2022: Expansion of product lines to include customized anode designs for specialized chemical processing equipment.

- 2023: Greater emphasis on sustainable manufacturing practices and material sourcing within the industry.

- 2024: Integration of IoT sensors for real-time monitoring of anode performance in pipeline applications gains traction.

Future Outlook for High Silicon Cast Iron Anode Market

The future outlook for the High Silicon Cast Iron Anode market is overwhelmingly positive, driven by sustained global demand for reliable and cost-effective corrosion protection solutions. The continuous expansion of industrial infrastructure, coupled with the critical need to preserve aging assets, will remain a primary growth catalyst. Technological innovations in anode design and manufacturing will further enhance their performance and expand their applicability across diverse environments. The increasing awareness of the economic and environmental benefits of proactive corrosion management will solidify their position in various industrial sectors. Strategic collaborations and an integrated approach to providing complete cathodic protection systems will likely define market success. The market is poised for steady growth, with opportunities arising from emerging applications and the ongoing development of smart corrosion monitoring technologies.

High Silicon Cast Iron Anode Segmentation

-

1. Application

- 1.1. Chemical Industry

- 1.2. Metal Protection

- 1.3. Others

-

2. Type

- 2.1. Anode Plate

- 2.2. Anode Bar

- 2.3. Others

High Silicon Cast Iron Anode Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

High Silicon Cast Iron Anode Regional Market Share

Geographic Coverage of High Silicon Cast Iron Anode

High Silicon Cast Iron Anode REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Chemical Industry

- 5.1.2. Metal Protection

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Anode Plate

- 5.2.2. Anode Bar

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global High Silicon Cast Iron Anode Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Chemical Industry

- 6.1.2. Metal Protection

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Anode Plate

- 6.2.2. Anode Bar

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America High Silicon Cast Iron Anode Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Chemical Industry

- 7.1.2. Metal Protection

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Anode Plate

- 7.2.2. Anode Bar

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America High Silicon Cast Iron Anode Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Chemical Industry

- 8.1.2. Metal Protection

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Anode Plate

- 8.2.2. Anode Bar

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe High Silicon Cast Iron Anode Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Chemical Industry

- 9.1.2. Metal Protection

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Anode Plate

- 9.2.2. Anode Bar

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa High Silicon Cast Iron Anode Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Chemical Industry

- 10.1.2. Metal Protection

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Anode Plate

- 10.2.2. Anode Bar

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific High Silicon Cast Iron Anode Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Chemical Industry

- 11.1.2. Metal Protection

- 11.1.3. Others

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Anode Plate

- 11.2.2. Anode Bar

- 11.2.3. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Corrosion Group

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Cathtect

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 BAC Corrosion Control

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Cathwell

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Farwest Corrosion

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Sychem

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Cathodic Protection

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 German Cathodic Protection

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Corrosion Service

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Pipeline Maintenance

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Jennings Anodes

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 BSS Technologies

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Korf KB

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Tecnoseal Industry

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Matcor

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Stanford Advanced Materials

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.1 Corrosion Group

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global High Silicon Cast Iron Anode Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America High Silicon Cast Iron Anode Revenue (million), by Application 2025 & 2033

- Figure 3: North America High Silicon Cast Iron Anode Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America High Silicon Cast Iron Anode Revenue (million), by Type 2025 & 2033

- Figure 5: North America High Silicon Cast Iron Anode Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America High Silicon Cast Iron Anode Revenue (million), by Country 2025 & 2033

- Figure 7: North America High Silicon Cast Iron Anode Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America High Silicon Cast Iron Anode Revenue (million), by Application 2025 & 2033

- Figure 9: South America High Silicon Cast Iron Anode Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America High Silicon Cast Iron Anode Revenue (million), by Type 2025 & 2033

- Figure 11: South America High Silicon Cast Iron Anode Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America High Silicon Cast Iron Anode Revenue (million), by Country 2025 & 2033

- Figure 13: South America High Silicon Cast Iron Anode Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe High Silicon Cast Iron Anode Revenue (million), by Application 2025 & 2033

- Figure 15: Europe High Silicon Cast Iron Anode Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe High Silicon Cast Iron Anode Revenue (million), by Type 2025 & 2033

- Figure 17: Europe High Silicon Cast Iron Anode Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe High Silicon Cast Iron Anode Revenue (million), by Country 2025 & 2033

- Figure 19: Europe High Silicon Cast Iron Anode Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa High Silicon Cast Iron Anode Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa High Silicon Cast Iron Anode Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa High Silicon Cast Iron Anode Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa High Silicon Cast Iron Anode Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa High Silicon Cast Iron Anode Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa High Silicon Cast Iron Anode Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific High Silicon Cast Iron Anode Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific High Silicon Cast Iron Anode Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific High Silicon Cast Iron Anode Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific High Silicon Cast Iron Anode Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific High Silicon Cast Iron Anode Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific High Silicon Cast Iron Anode Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global High Silicon Cast Iron Anode Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global High Silicon Cast Iron Anode Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global High Silicon Cast Iron Anode Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global High Silicon Cast Iron Anode Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global High Silicon Cast Iron Anode Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global High Silicon Cast Iron Anode Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States High Silicon Cast Iron Anode Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada High Silicon Cast Iron Anode Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico High Silicon Cast Iron Anode Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global High Silicon Cast Iron Anode Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global High Silicon Cast Iron Anode Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global High Silicon Cast Iron Anode Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil High Silicon Cast Iron Anode Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina High Silicon Cast Iron Anode Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America High Silicon Cast Iron Anode Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global High Silicon Cast Iron Anode Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global High Silicon Cast Iron Anode Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global High Silicon Cast Iron Anode Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom High Silicon Cast Iron Anode Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany High Silicon Cast Iron Anode Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France High Silicon Cast Iron Anode Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy High Silicon Cast Iron Anode Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain High Silicon Cast Iron Anode Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia High Silicon Cast Iron Anode Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux High Silicon Cast Iron Anode Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics High Silicon Cast Iron Anode Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe High Silicon Cast Iron Anode Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global High Silicon Cast Iron Anode Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global High Silicon Cast Iron Anode Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global High Silicon Cast Iron Anode Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey High Silicon Cast Iron Anode Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel High Silicon Cast Iron Anode Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC High Silicon Cast Iron Anode Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa High Silicon Cast Iron Anode Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa High Silicon Cast Iron Anode Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa High Silicon Cast Iron Anode Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global High Silicon Cast Iron Anode Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global High Silicon Cast Iron Anode Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global High Silicon Cast Iron Anode Revenue million Forecast, by Country 2020 & 2033

- Table 40: China High Silicon Cast Iron Anode Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India High Silicon Cast Iron Anode Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan High Silicon Cast Iron Anode Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea High Silicon Cast Iron Anode Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN High Silicon Cast Iron Anode Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania High Silicon Cast Iron Anode Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific High Silicon Cast Iron Anode Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the High Silicon Cast Iron Anode?

The projected CAGR is approximately 3.9%.

2. Which companies are prominent players in the High Silicon Cast Iron Anode?

Key companies in the market include Corrosion Group, Cathtect, BAC Corrosion Control, Cathwell, Farwest Corrosion, Sychem, Cathodic Protection, German Cathodic Protection, Corrosion Service, Pipeline Maintenance, Jennings Anodes, BSS Technologies, Korf KB, Tecnoseal Industry, Matcor, Stanford Advanced Materials.

3. What are the main segments of the High Silicon Cast Iron Anode?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 159 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4250.00, USD 6375.00, and USD 8500.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "High Silicon Cast Iron Anode," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the High Silicon Cast Iron Anode report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the High Silicon Cast Iron Anode?

To stay informed about further developments, trends, and reports in the High Silicon Cast Iron Anode, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence