Key Insights

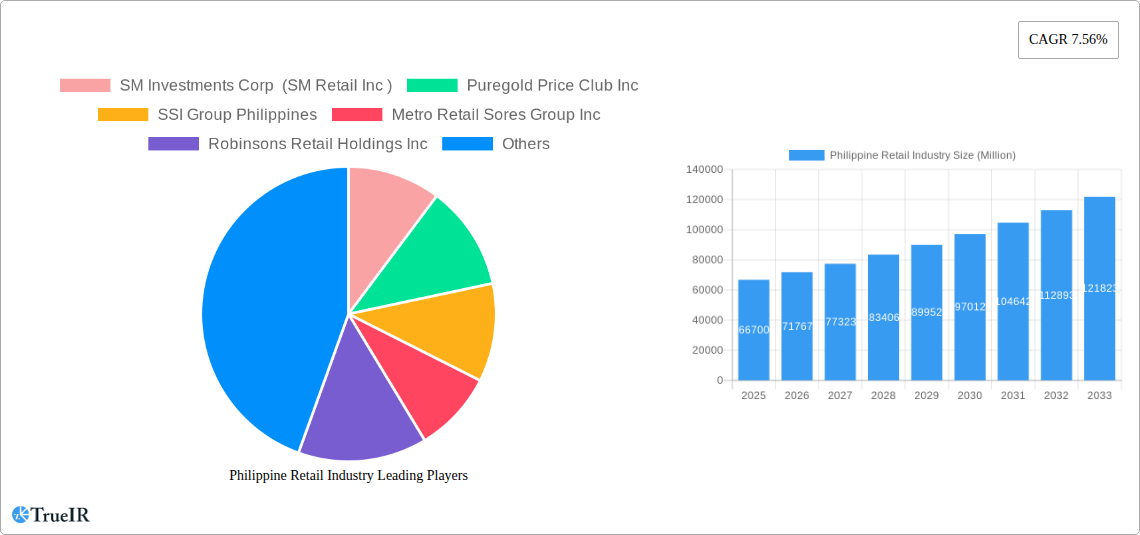

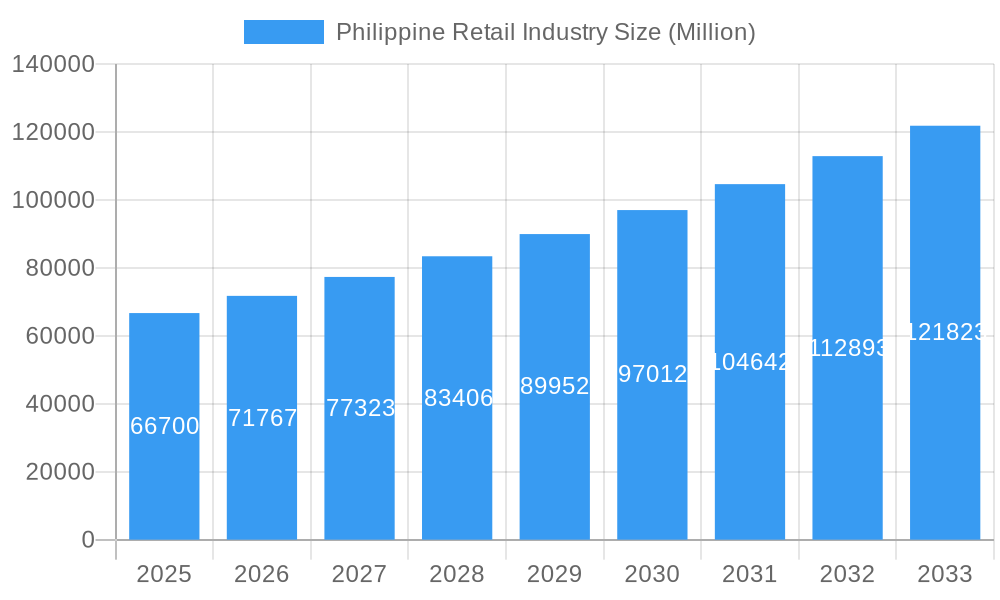

The Philippine retail industry, valued at $66.70 billion in 2025, is projected to experience robust growth, exhibiting a Compound Annual Growth Rate (CAGR) of 7.56% from 2025 to 2033. This expansion is fueled by several key drivers. A burgeoning middle class with increasing disposable income is a significant factor, driving demand for a wider range of goods and services. The rise of e-commerce and digital payments further accelerates market growth, providing convenient access to retail offerings across the archipelago. Furthermore, strategic investments in modern retail infrastructure, particularly in expanding urban areas and emerging provinces, are creating new opportunities for retailers to reach broader consumer bases. Increased foreign direct investment also plays a role, bringing in expertise and capital to enhance the retail landscape. However, challenges remain. Inflationary pressures and potential economic volatility could impact consumer spending, while intense competition among established players and emerging e-commerce businesses necessitates strategic adaptability.

Philippine Retail Industry Market Size (In Billion)

The competitive landscape is dominated by a mix of large, established players such as SM Investments Corp, Puregold Price Club Inc, and Robinsons Retail Holdings Inc, alongside smaller, specialized retailers and a growing number of e-commerce platforms. These businesses are actively innovating to cater to evolving consumer preferences, embracing omnichannel strategies that integrate online and offline experiences. The industry segmentation reveals a diverse range of formats, encompassing hypermarkets, supermarkets, convenience stores, specialty retail, and e-commerce. Future growth will likely see continued consolidation among players, further expansion into underserved markets, and a heightened focus on enhancing customer experience through loyalty programs, personalized offerings, and improved supply chain efficiency. Analyzing regional performance will be crucial to understanding market dynamics and optimizing investment strategies across various regions within the Philippines.

Philippine Retail Industry Company Market Share

This comprehensive report provides an in-depth analysis of the dynamic Philippine retail industry, offering valuable insights for investors, businesses, and industry professionals. Covering the period 2019-2033, with a base year of 2025 and a forecast period of 2025-2033, this report leverages extensive market research to deliver actionable intelligence. Discover key trends, challenges, and opportunities within the Philippine retail sector, including detailed profiles of major players like SM Investments Corp, Puregold Price Club Inc., and Robinsons Retail Holdings Inc. This report is your essential guide to navigating the complexities and unlocking the potential of this rapidly evolving market. The report uses Millions (M) for all values.

Philippine Retail Industry Market Structure & Competitive Landscape

The Philippine retail industry is characterized by a moderately concentrated market structure. Major players like SM Investments Corp (SM Retail Inc) and Puregold Price Club Inc. command significant market share, although a substantial number of smaller businesses and regional players also contribute to the overall landscape. The concentration ratio (CR4) for the grocery sector, for example, is estimated at 45% in 2025, indicating moderate dominance by the top four players.

Innovation in the Philippine retail landscape is driven by several factors: the rising adoption of e-commerce, the growing preference for omnichannel experiences, and the increasing demand for personalized shopping experiences. The industry is significantly impacted by government regulations relating to consumer protection, taxation, and foreign investment. Product substitutes, such as online marketplaces and direct-to-consumer brands, pose a competitive threat, especially to traditional brick-and-mortar retailers. The end-user segmentation is diverse, encompassing various socio-economic groups with distinct purchasing patterns.

Mergers and acquisitions (M&A) activity has been relatively robust in recent years, particularly involving smaller players consolidating to improve their scale and competitiveness. The total value of M&A deals in the retail sector during 2019-2024 is estimated at xx Million.

- Market Concentration: CR4 estimated at 45% in 2025 (Grocery Sector).

- Innovation Drivers: E-commerce, omnichannel strategies, personalization.

- Regulatory Impacts: Consumer protection laws, tax policies, foreign investment regulations.

- M&A Trends: Increasing consolidation among smaller players, total M&A deal value (2019-2024): xx Million.

Philippine Retail Industry Market Trends & Opportunities

The Philippine retail market exhibits robust growth, driven by a burgeoning middle class, rising disposable incomes, and expanding urbanization. The market size is projected to reach xx Million in 2025, exhibiting a Compound Annual Growth Rate (CAGR) of xx% during 2025-2033. Technological advancements, such as mobile commerce and the integration of artificial intelligence (AI) and big data analytics, are transforming the industry. Consumer preferences are shifting towards convenience, personalized experiences, and value-for-money offerings. Competitive dynamics are intensifying, with both established players and new entrants vying for market share. The market penetration rate of e-commerce is steadily increasing and is projected to reach xx% by 2033. Growth opportunities abound in the areas of e-commerce, specialized retail formats (such as health and wellness), and omnichannel strategies.

Dominant Markets & Segments in Philippine Retail Industry

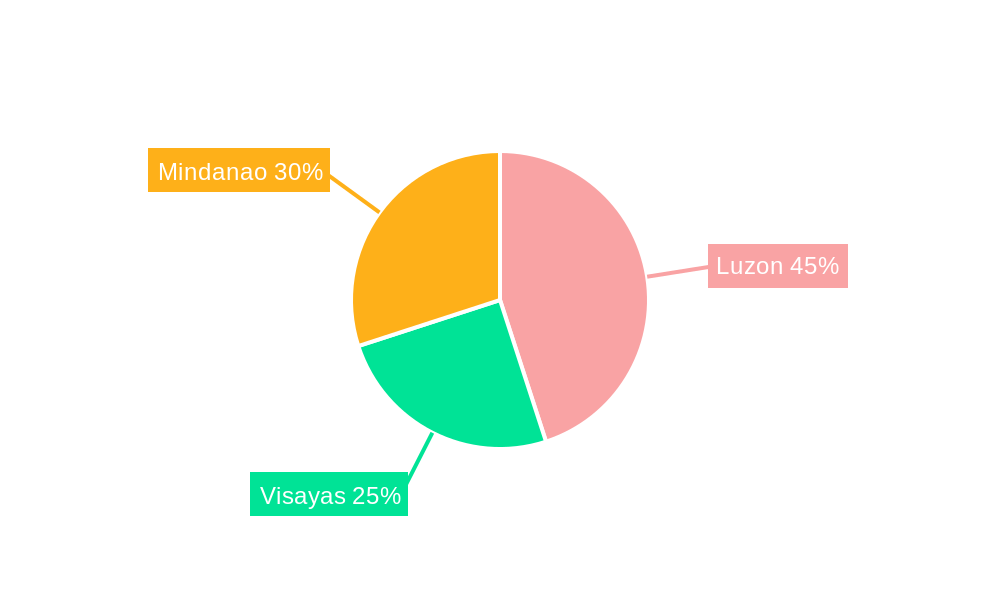

The National Capital Region (NCR) remains the dominant market, accounting for xx% of total retail sales in 2025. However, significant growth is also observed in key provincial cities driven by rising incomes and infrastructural improvements.

- Key Growth Drivers in NCR: High population density, high disposable incomes, robust infrastructure.

- Key Growth Drivers in Provincial Cities: Rising incomes, improved infrastructure (e.g., roads, transportation), government initiatives to stimulate regional economic growth.

The grocery sector remains the largest segment, followed by apparel and footwear, and health and beauty. The healthcare retail segment shows particularly strong growth, driven by a growing health-conscious population and rising healthcare expenditures.

Philippine Retail Industry Product Analysis

Technological advancements are driving product innovation in the Philippine retail industry. We are seeing increased use of digital technologies in areas such as inventory management, customer relationship management (CRM), and personalized marketing. The adoption of omnichannel strategies integrates online and offline channels, improving customer experience and convenience. The market is witnessing growing demand for products that cater to the needs of specific consumer segments and lifestyle trends such as health and wellness, sustainable products, and convenience food.

Key Drivers, Barriers & Challenges in Philippine Retail Industry

Key Drivers:

- Rising disposable incomes and a growing middle class.

- Increased urbanization and population growth.

- Technological advancements facilitating e-commerce and omnichannel operations.

- Government initiatives to improve infrastructure and stimulate economic growth.

Challenges:

- Supply chain disruptions, leading to increased costs and delays. This is reflected in a xx% increase in logistics costs between 2019 and 2024.

- Intense competition from both established players and new entrants.

- Regulatory complexities and bureaucratic hurdles.

- Economic uncertainty and fluctuations in consumer spending.

Growth Drivers in the Philippine Retail Industry Market

The growth of the Philippine retail market is fuelled by several factors: a burgeoning middle class, increasing urbanization, and the rising adoption of digital technologies. Government initiatives promoting infrastructure development and easing foreign investment regulations further support this growth. These factors together create a favorable environment for both domestic and international retail players.

Challenges Impacting Philippine Retail Industry Growth

Significant challenges exist, including intense competition, supply chain vulnerabilities (with logistics costs increasing by xx% from 2019 to 2024), and regulatory hurdles. Economic uncertainty and fluctuating consumer confidence add to the complexity of the market.

Key Players Shaping the Philippine Retail Industry Market

- SM Investments Corp (SM Retail Inc) [link to SM Investments Corp global website if available]

- Puregold Price Club Inc [link to Puregold Price Club Inc global website if available]

- SSI Group Philippines [link to SSI Group Philippines global website if available]

- Metro Retail Stores Group Inc [link to Metro Retail Stores Group Inc global website if available]

- Robinsons Retail Holdings Inc [link to Robinsons Retail Holdings Inc global website if available]

- Rustan Supercenters Inc [link to Rustan Supercenters Inc global website if available]

- Alfamart [link to Alfamart global website if available]

- 7-Eleven [link to 7-Eleven global website if available]

- Golden ABC Inc [link to Golden ABC Inc global website if available]

- Mercury Drug Corp [link to Mercury Drug Corp global website if available]

- List Not Exhaustive

Significant Philippine Retail Industry Milestones

- January 2024: Robinsons Retail partners with DFI Retail to launch Meadows, a premium brand offering food, beverages, home essentials, and beauty products.

- February 2024: Rose Pharmacy opens its 400th store, showcasing products from Guardian (DFI Retail).

Future Outlook for Philippine Retail Industry Market

The Philippine retail industry is poised for continued growth, driven by sustained economic expansion, rising consumer spending, and the ongoing adoption of digital technologies. Strategic opportunities exist for retailers to leverage omnichannel strategies, focus on personalization, and cater to the evolving needs of diverse consumer segments. The market's dynamism and potential for innovation guarantee a vibrant and competitive future.

Philippine Retail Industry Segmentation

-

1. Products

- 1.1. Food and Beverage

- 1.2. Personal and Household Care

- 1.3. Apparel

- 1.4. Footwear and Accessories

- 1.5. Furniture

- 1.6. Toys and Hobbies

- 1.7. Electronic and Household Appliances

- 1.8. Other Products

-

2. Distribution Channel

- 2.1. Supermarkets/Hypermarkets

- 2.2. Convenience Stores

- 2.3. Department Stores

- 2.4. Specialty Stores

- 2.5. Online

- 2.6. Other Distribution Channels

Philippine Retail Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Philippine Retail Industry Regional Market Share

Geographic Coverage of Philippine Retail Industry

Philippine Retail Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.56% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Products

- 5.1.1. Food and Beverage

- 5.1.2. Personal and Household Care

- 5.1.3. Apparel

- 5.1.4. Footwear and Accessories

- 5.1.5. Furniture

- 5.1.6. Toys and Hobbies

- 5.1.7. Electronic and Household Appliances

- 5.1.8. Other Products

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Supermarkets/Hypermarkets

- 5.2.2. Convenience Stores

- 5.2.3. Department Stores

- 5.2.4. Specialty Stores

- 5.2.5. Online

- 5.2.6. Other Distribution Channels

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Products

- 6. Global Philippine Retail Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Products

- 6.1.1. Food and Beverage

- 6.1.2. Personal and Household Care

- 6.1.3. Apparel

- 6.1.4. Footwear and Accessories

- 6.1.5. Furniture

- 6.1.6. Toys and Hobbies

- 6.1.7. Electronic and Household Appliances

- 6.1.8. Other Products

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Supermarkets/Hypermarkets

- 6.2.2. Convenience Stores

- 6.2.3. Department Stores

- 6.2.4. Specialty Stores

- 6.2.5. Online

- 6.2.6. Other Distribution Channels

- 6.1. Market Analysis, Insights and Forecast - by Products

- 7. North America Philippine Retail Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Products

- 7.1.1. Food and Beverage

- 7.1.2. Personal and Household Care

- 7.1.3. Apparel

- 7.1.4. Footwear and Accessories

- 7.1.5. Furniture

- 7.1.6. Toys and Hobbies

- 7.1.7. Electronic and Household Appliances

- 7.1.8. Other Products

- 7.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.2.1. Supermarkets/Hypermarkets

- 7.2.2. Convenience Stores

- 7.2.3. Department Stores

- 7.2.4. Specialty Stores

- 7.2.5. Online

- 7.2.6. Other Distribution Channels

- 7.1. Market Analysis, Insights and Forecast - by Products

- 8. South America Philippine Retail Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Products

- 8.1.1. Food and Beverage

- 8.1.2. Personal and Household Care

- 8.1.3. Apparel

- 8.1.4. Footwear and Accessories

- 8.1.5. Furniture

- 8.1.6. Toys and Hobbies

- 8.1.7. Electronic and Household Appliances

- 8.1.8. Other Products

- 8.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.2.1. Supermarkets/Hypermarkets

- 8.2.2. Convenience Stores

- 8.2.3. Department Stores

- 8.2.4. Specialty Stores

- 8.2.5. Online

- 8.2.6. Other Distribution Channels

- 8.1. Market Analysis, Insights and Forecast - by Products

- 9. Europe Philippine Retail Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Products

- 9.1.1. Food and Beverage

- 9.1.2. Personal and Household Care

- 9.1.3. Apparel

- 9.1.4. Footwear and Accessories

- 9.1.5. Furniture

- 9.1.6. Toys and Hobbies

- 9.1.7. Electronic and Household Appliances

- 9.1.8. Other Products

- 9.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.2.1. Supermarkets/Hypermarkets

- 9.2.2. Convenience Stores

- 9.2.3. Department Stores

- 9.2.4. Specialty Stores

- 9.2.5. Online

- 9.2.6. Other Distribution Channels

- 9.1. Market Analysis, Insights and Forecast - by Products

- 10. Middle East & Africa Philippine Retail Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Products

- 10.1.1. Food and Beverage

- 10.1.2. Personal and Household Care

- 10.1.3. Apparel

- 10.1.4. Footwear and Accessories

- 10.1.5. Furniture

- 10.1.6. Toys and Hobbies

- 10.1.7. Electronic and Household Appliances

- 10.1.8. Other Products

- 10.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.2.1. Supermarkets/Hypermarkets

- 10.2.2. Convenience Stores

- 10.2.3. Department Stores

- 10.2.4. Specialty Stores

- 10.2.5. Online

- 10.2.6. Other Distribution Channels

- 10.1. Market Analysis, Insights and Forecast - by Products

- 11. Asia Pacific Philippine Retail Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Products

- 11.1.1. Food and Beverage

- 11.1.2. Personal and Household Care

- 11.1.3. Apparel

- 11.1.4. Footwear and Accessories

- 11.1.5. Furniture

- 11.1.6. Toys and Hobbies

- 11.1.7. Electronic and Household Appliances

- 11.1.8. Other Products

- 11.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 11.2.1. Supermarkets/Hypermarkets

- 11.2.2. Convenience Stores

- 11.2.3. Department Stores

- 11.2.4. Specialty Stores

- 11.2.5. Online

- 11.2.6. Other Distribution Channels

- 11.1. Market Analysis, Insights and Forecast - by Products

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 SM Investments Corp (SM Retail Inc )

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Puregold Price Club Inc

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 SSI Group Philippines

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Metro Retail Sores Group Inc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Robinsons Retail Holdings Inc

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Rustan Supercenters Inc

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Alfamart

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 7-Eleven

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Golden ABC Inc

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Mercury Drug Corp **List Not Exhaustive

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 SM Investments Corp (SM Retail Inc )

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Philippine Retail Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Global Philippine Retail Industry Volume Breakdown (Billion, %) by Region 2025 & 2033

- Figure 3: North America Philippine Retail Industry Revenue (Million), by Products 2025 & 2033

- Figure 4: North America Philippine Retail Industry Volume (Billion), by Products 2025 & 2033

- Figure 5: North America Philippine Retail Industry Revenue Share (%), by Products 2025 & 2033

- Figure 6: North America Philippine Retail Industry Volume Share (%), by Products 2025 & 2033

- Figure 7: North America Philippine Retail Industry Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 8: North America Philippine Retail Industry Volume (Billion), by Distribution Channel 2025 & 2033

- Figure 9: North America Philippine Retail Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 10: North America Philippine Retail Industry Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 11: North America Philippine Retail Industry Revenue (Million), by Country 2025 & 2033

- Figure 12: North America Philippine Retail Industry Volume (Billion), by Country 2025 & 2033

- Figure 13: North America Philippine Retail Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Philippine Retail Industry Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Philippine Retail Industry Revenue (Million), by Products 2025 & 2033

- Figure 16: South America Philippine Retail Industry Volume (Billion), by Products 2025 & 2033

- Figure 17: South America Philippine Retail Industry Revenue Share (%), by Products 2025 & 2033

- Figure 18: South America Philippine Retail Industry Volume Share (%), by Products 2025 & 2033

- Figure 19: South America Philippine Retail Industry Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 20: South America Philippine Retail Industry Volume (Billion), by Distribution Channel 2025 & 2033

- Figure 21: South America Philippine Retail Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 22: South America Philippine Retail Industry Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 23: South America Philippine Retail Industry Revenue (Million), by Country 2025 & 2033

- Figure 24: South America Philippine Retail Industry Volume (Billion), by Country 2025 & 2033

- Figure 25: South America Philippine Retail Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Philippine Retail Industry Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Philippine Retail Industry Revenue (Million), by Products 2025 & 2033

- Figure 28: Europe Philippine Retail Industry Volume (Billion), by Products 2025 & 2033

- Figure 29: Europe Philippine Retail Industry Revenue Share (%), by Products 2025 & 2033

- Figure 30: Europe Philippine Retail Industry Volume Share (%), by Products 2025 & 2033

- Figure 31: Europe Philippine Retail Industry Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 32: Europe Philippine Retail Industry Volume (Billion), by Distribution Channel 2025 & 2033

- Figure 33: Europe Philippine Retail Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 34: Europe Philippine Retail Industry Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 35: Europe Philippine Retail Industry Revenue (Million), by Country 2025 & 2033

- Figure 36: Europe Philippine Retail Industry Volume (Billion), by Country 2025 & 2033

- Figure 37: Europe Philippine Retail Industry Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Philippine Retail Industry Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Philippine Retail Industry Revenue (Million), by Products 2025 & 2033

- Figure 40: Middle East & Africa Philippine Retail Industry Volume (Billion), by Products 2025 & 2033

- Figure 41: Middle East & Africa Philippine Retail Industry Revenue Share (%), by Products 2025 & 2033

- Figure 42: Middle East & Africa Philippine Retail Industry Volume Share (%), by Products 2025 & 2033

- Figure 43: Middle East & Africa Philippine Retail Industry Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 44: Middle East & Africa Philippine Retail Industry Volume (Billion), by Distribution Channel 2025 & 2033

- Figure 45: Middle East & Africa Philippine Retail Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 46: Middle East & Africa Philippine Retail Industry Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 47: Middle East & Africa Philippine Retail Industry Revenue (Million), by Country 2025 & 2033

- Figure 48: Middle East & Africa Philippine Retail Industry Volume (Billion), by Country 2025 & 2033

- Figure 49: Middle East & Africa Philippine Retail Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Philippine Retail Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Philippine Retail Industry Revenue (Million), by Products 2025 & 2033

- Figure 52: Asia Pacific Philippine Retail Industry Volume (Billion), by Products 2025 & 2033

- Figure 53: Asia Pacific Philippine Retail Industry Revenue Share (%), by Products 2025 & 2033

- Figure 54: Asia Pacific Philippine Retail Industry Volume Share (%), by Products 2025 & 2033

- Figure 55: Asia Pacific Philippine Retail Industry Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 56: Asia Pacific Philippine Retail Industry Volume (Billion), by Distribution Channel 2025 & 2033

- Figure 57: Asia Pacific Philippine Retail Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 58: Asia Pacific Philippine Retail Industry Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 59: Asia Pacific Philippine Retail Industry Revenue (Million), by Country 2025 & 2033

- Figure 60: Asia Pacific Philippine Retail Industry Volume (Billion), by Country 2025 & 2033

- Figure 61: Asia Pacific Philippine Retail Industry Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Philippine Retail Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Philippine Retail Industry Revenue Million Forecast, by Products 2020 & 2033

- Table 2: Global Philippine Retail Industry Volume Billion Forecast, by Products 2020 & 2033

- Table 3: Global Philippine Retail Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 4: Global Philippine Retail Industry Volume Billion Forecast, by Distribution Channel 2020 & 2033

- Table 5: Global Philippine Retail Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Global Philippine Retail Industry Volume Billion Forecast, by Region 2020 & 2033

- Table 7: Global Philippine Retail Industry Revenue Million Forecast, by Products 2020 & 2033

- Table 8: Global Philippine Retail Industry Volume Billion Forecast, by Products 2020 & 2033

- Table 9: Global Philippine Retail Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 10: Global Philippine Retail Industry Volume Billion Forecast, by Distribution Channel 2020 & 2033

- Table 11: Global Philippine Retail Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: Global Philippine Retail Industry Volume Billion Forecast, by Country 2020 & 2033

- Table 13: United States Philippine Retail Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: United States Philippine Retail Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 15: Canada Philippine Retail Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Canada Philippine Retail Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 17: Mexico Philippine Retail Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Mexico Philippine Retail Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 19: Global Philippine Retail Industry Revenue Million Forecast, by Products 2020 & 2033

- Table 20: Global Philippine Retail Industry Volume Billion Forecast, by Products 2020 & 2033

- Table 21: Global Philippine Retail Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 22: Global Philippine Retail Industry Volume Billion Forecast, by Distribution Channel 2020 & 2033

- Table 23: Global Philippine Retail Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 24: Global Philippine Retail Industry Volume Billion Forecast, by Country 2020 & 2033

- Table 25: Brazil Philippine Retail Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Brazil Philippine Retail Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 27: Argentina Philippine Retail Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Argentina Philippine Retail Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Philippine Retail Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Philippine Retail Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 31: Global Philippine Retail Industry Revenue Million Forecast, by Products 2020 & 2033

- Table 32: Global Philippine Retail Industry Volume Billion Forecast, by Products 2020 & 2033

- Table 33: Global Philippine Retail Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 34: Global Philippine Retail Industry Volume Billion Forecast, by Distribution Channel 2020 & 2033

- Table 35: Global Philippine Retail Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 36: Global Philippine Retail Industry Volume Billion Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Philippine Retail Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Philippine Retail Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 39: Germany Philippine Retail Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 40: Germany Philippine Retail Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 41: France Philippine Retail Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: France Philippine Retail Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 43: Italy Philippine Retail Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 44: Italy Philippine Retail Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 45: Spain Philippine Retail Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 46: Spain Philippine Retail Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 47: Russia Philippine Retail Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 48: Russia Philippine Retail Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 49: Benelux Philippine Retail Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 50: Benelux Philippine Retail Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 51: Nordics Philippine Retail Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 52: Nordics Philippine Retail Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Philippine Retail Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Philippine Retail Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 55: Global Philippine Retail Industry Revenue Million Forecast, by Products 2020 & 2033

- Table 56: Global Philippine Retail Industry Volume Billion Forecast, by Products 2020 & 2033

- Table 57: Global Philippine Retail Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 58: Global Philippine Retail Industry Volume Billion Forecast, by Distribution Channel 2020 & 2033

- Table 59: Global Philippine Retail Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 60: Global Philippine Retail Industry Volume Billion Forecast, by Country 2020 & 2033

- Table 61: Turkey Philippine Retail Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 62: Turkey Philippine Retail Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 63: Israel Philippine Retail Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 64: Israel Philippine Retail Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 65: GCC Philippine Retail Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 66: GCC Philippine Retail Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 67: North Africa Philippine Retail Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 68: North Africa Philippine Retail Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 69: South Africa Philippine Retail Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 70: South Africa Philippine Retail Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Philippine Retail Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Philippine Retail Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 73: Global Philippine Retail Industry Revenue Million Forecast, by Products 2020 & 2033

- Table 74: Global Philippine Retail Industry Volume Billion Forecast, by Products 2020 & 2033

- Table 75: Global Philippine Retail Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 76: Global Philippine Retail Industry Volume Billion Forecast, by Distribution Channel 2020 & 2033

- Table 77: Global Philippine Retail Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 78: Global Philippine Retail Industry Volume Billion Forecast, by Country 2020 & 2033

- Table 79: China Philippine Retail Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 80: China Philippine Retail Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 81: India Philippine Retail Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 82: India Philippine Retail Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 83: Japan Philippine Retail Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 84: Japan Philippine Retail Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 85: South Korea Philippine Retail Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 86: South Korea Philippine Retail Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Philippine Retail Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Philippine Retail Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 89: Oceania Philippine Retail Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 90: Oceania Philippine Retail Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Philippine Retail Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Philippine Retail Industry Volume (Billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Philippine Retail Industry?

The projected CAGR is approximately 7.56%.

2. Which companies are prominent players in the Philippine Retail Industry?

Key companies in the market include SM Investments Corp (SM Retail Inc ), Puregold Price Club Inc, SSI Group Philippines, Metro Retail Sores Group Inc, Robinsons Retail Holdings Inc, Rustan Supercenters Inc, Alfamart, 7-Eleven, Golden ABC Inc, Mercury Drug Corp **List Not Exhaustive.

3. What are the main segments of the Philippine Retail Industry?

The market segments include Products, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 66.70 Million as of 2022.

5. What are some drivers contributing to market growth?

The Rising Demand for Packaged and Ready to Eat Food is Driving the Market; Increase in the Demand for Branded Goods Categories such as Apparel. Cosmetics. Footwear. Watches. Beverages. and Food.

6. What are the notable trends driving market growth?

The Philippines' Food and Beverage Sector: A Key Pillar of the Nation's Economy.

7. Are there any restraints impacting market growth?

The Rising Demand for Packaged and Ready to Eat Food is Driving the Market; Increase in the Demand for Branded Goods Categories such as Apparel. Cosmetics. Footwear. Watches. Beverages. and Food.

8. Can you provide examples of recent developments in the market?

February 2024: Rose Pharmacy, a prominent player in the Philippine healthcare retail sector, marked a significant milestone on January 29, 2024, with the inauguration of its 400th store. Strategically located at Nustar Resort and Casino in Cebu City, this new outlet stands as a comprehensive destination for health and wellness needs. Beyond offering a diverse range of medicines, Rose Pharmacy's newest store showcases an array of products from Guardian, a leading Southeast Asian health and wellness brand. Notably, Guardian is under the ownership of DFI Retail and enjoys exclusive distribution through Rose Pharmacy in the Philippines.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Philippine Retail Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Philippine Retail Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Philippine Retail Industry?

To stay informed about further developments, trends, and reports in the Philippine Retail Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence