Key Insights for TCP and RTP Pipe Market

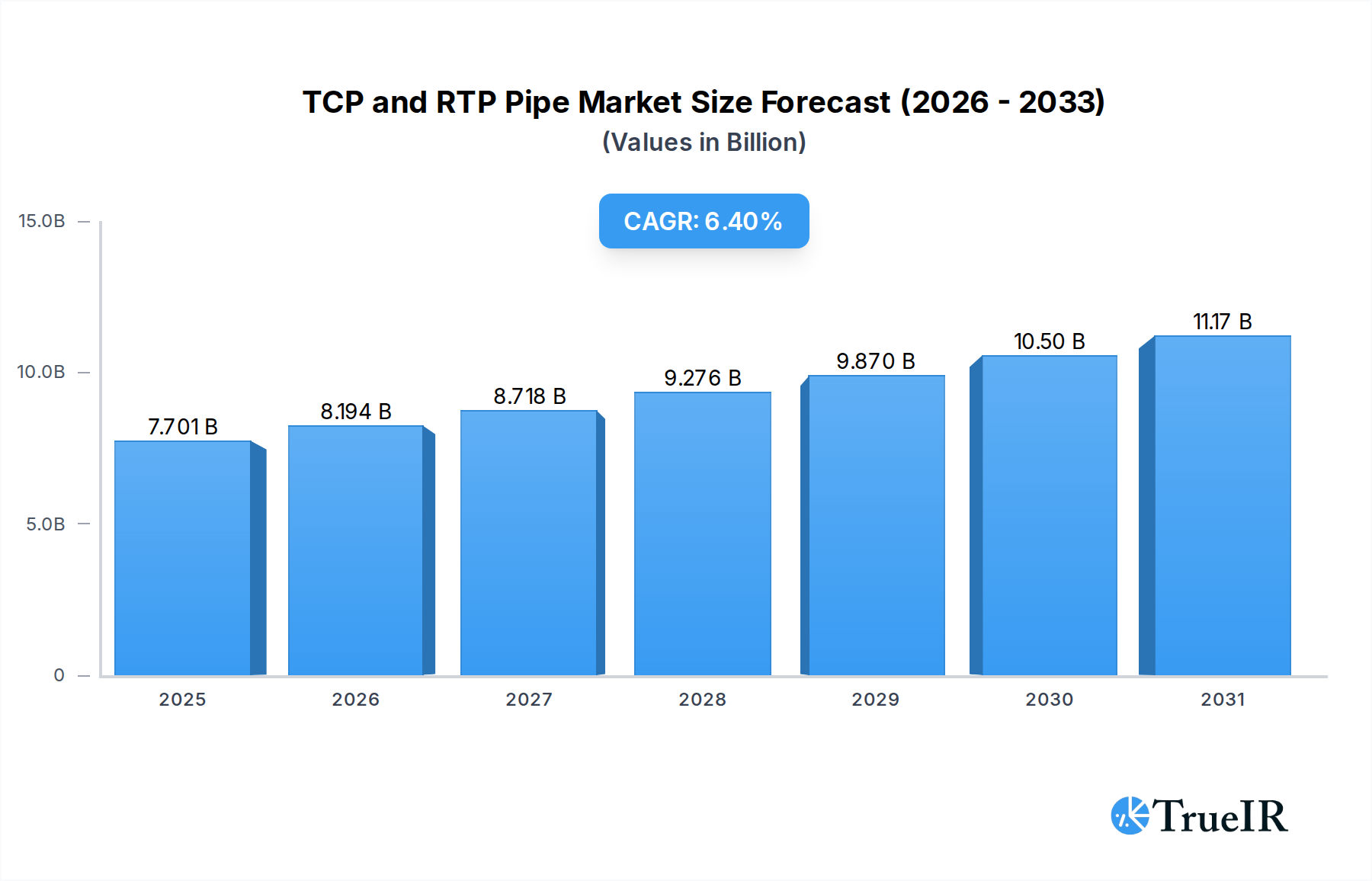

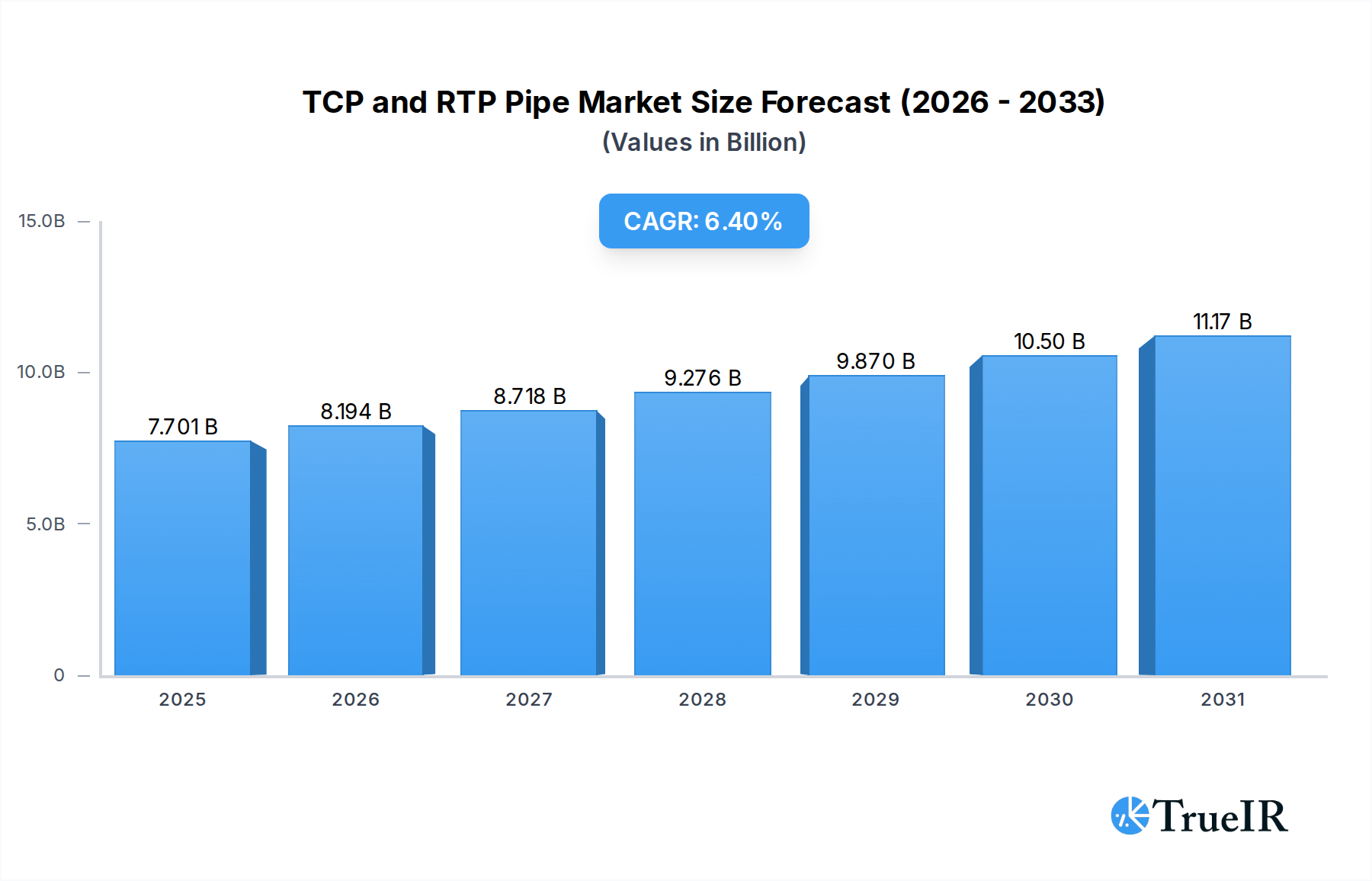

The Global TCP and RTP Pipe Market, valued at an estimated $7237.5 million in 2024, is poised for substantial expansion, projected to reach approximately $12762.6 million by 2033, exhibiting a robust Compound Annual Growth Rate (CAGR) of 6.4% over the forecast period. This significant growth trajectory is primarily propelled by the inherent advantages of Thermoplastic Composite Pipes (TCP) and Reinforced Thermoplastic Pipes (RTP) over traditional metallic piping solutions. These include superior corrosion resistance, lighter weight, enhanced flexibility, and reduced installation costs, making them highly attractive for critical infrastructure applications.

TCP and RTP Pipe Market Size (In Billion)

Key demand drivers encompass the burgeoning need for efficient and durable pipeline infrastructure in the oil and gas sector, where TCP and RTP are increasingly deployed for flowlines, gathering lines, and injection lines, as well as the escalating global demand for reliable water and wastewater transport systems. The inherent material properties, such as those derived from Polyethylene (HDPE), Polyamide (PA12), and Polyetheretherketone (PEEK), enable these pipes to withstand harsh operating environments, including corrosive fluids, high pressures, and extreme temperatures. Furthermore, the push for sustainable infrastructure and stringent environmental regulations concerning pipeline integrity and leak prevention are accelerating the adoption of these advanced piping solutions. The integration of high-strength fibers like aramid, polyester, or carbon fiber further enhances the performance envelope, contributing to the growth of the Advanced Pipe Systems Market. Geographically, while established markets in North America and Europe continue to drive innovation and replacement demand, the Asia Pacific region is emerging as a significant growth hub due to rapid industrialization and infrastructure development. The broader demand for robust solutions in the Specialty Chemicals Market also underpins advancements in polymer composites crucial for TCP and RTP manufacturing. This market’s outlook remains positive, driven by continuous technological advancements in materials science and fabrication techniques, coupled with increasing recognition of their long-term economic and operational benefits across diverse industrial applications."

TCP and RTP Pipe Company Market Share

- "

Reinforced Thermoplastic Pipe Segment Dominance in TCP and RTP Pipe Market

Within the broader TCP and RTP Pipe Market, the Reinforced Thermoplastic Pipe Market segment currently holds a substantial revenue share and is anticipated to maintain its prominence due to a confluence of technological and economic factors. RTPs, characterized by a thermoplastic liner, a reinforcement layer (typically helical windings of high-strength fibers like aramid or polyester embedded in a thermoplastic matrix), and a thermoplastic outer jacket, offer a compelling balance of performance, flexibility, and cost-effectiveness. Their primary advantage lies in their superior resistance to corrosion and scaling, which significantly reduces maintenance costs and extends operational lifespans compared to conventional steel pipes, particularly in corrosive fluid transport within the Oil and Gas Pipeline Market. The ease of deployment, often involving reel-lay or coiling techniques, allows for faster installation times and lower associated logistical costs, making them highly attractive for challenging terrains and offshore applications.

While the Thermoplastic Composite Pipe Market, encompassing fully bonded or unbonded composite structures, offers even higher performance envelopes, especially for ultra-deepwater and high-pressure/high-temperature applications, RTPs currently benefit from a broader application scope and a more mature manufacturing base for a wider range of standard pressures and diameters. Key players such as Strohm, TechnipFMC plc, and Magma Global Ltd. are significant contributors to both segments, continually innovating to expand the capabilities of RTPs. The increasing demand from the Water & Wastewater Infrastructure Market for durable, non-corroding pipes further bolsters the RTP segment, where flexibility and chemical resistance are critical for municipal and industrial water management. Growth in this segment is also fueled by ongoing material science advancements, particularly in the development of more robust and chemically inert thermoplastic liners and higher-strength reinforcing fibers, further enhancing the operational capabilities and market reach of RTP solutions. The versatility of RTPs across diverse applications, from high-pressure oil and gas flowlines to less demanding industrial fluid transport, ensures its continued leadership within the TCP and RTP Pipe Market."

- "

Key Market Drivers & Constraints in TCP and RTP Pipe Market

Several intrinsic factors are rigorously driving the expansion of the TCP and RTP Pipe Market, while a few constraints temper its growth. A primary driver is the unparalleled Corrosion Resistance offered by these pipes. Traditional metallic pipelines are highly susceptible to corrosion, especially in aggressive environments such as those found in the Oil and Gas Pipeline Market and certain chemical processing industries. The global cost of corrosion, estimated by NACE International to be in excess of $2.5 trillion annually, highlights the economic imperative for corrosion-resistant alternatives. TCP and RTP significantly mitigate this issue, extending pipeline lifespans and dramatically reducing maintenance and replacement costs, often by more than 50% over a 20-year period compared to steel.

Another significant driver is Operational Efficiency and Reduced Installation Costs. TCP and RTP are considerably lighter and more flexible than their metallic counterparts. For instance, an RTP can be up to 70% lighter than a steel pipe of equivalent diameter and pressure rating. This characteristic allows for long pipe sections to be spooled onto reels, facilitating rapid installation (e.g., pipeline projects reporting up to 40% faster deployment) with fewer jointing requirements, particularly in offshore and difficult-to-access onshore locations. This efficiency directly translates into lower project CAPEX and OPEX.

Conversely, a key constraint for the TCP and RTP Pipe Market is the Initial Capital Expenditure. While lifecycle costs are typically lower, the upfront cost of advanced thermoplastic and composite materials and the specialized manufacturing processes can make TCP and RTP solutions more expensive than traditional alternatives for certain applications, especially in regions with mature steel pipe supply chains. Additionally, Limited Standardization and Market Penetration in specific, highly regulated sectors or for ultra-large diameter applications poses a challenge. Although standards bodies like API and ISO are developing more comprehensive specifications, the slower adoption rate in conservative industries, coupled with a lack of familiarity among some engineering firms, can restrict market growth. This is gradually being overcome as the benefits become more widely recognized, particularly for specialized applications within the Water & Wastewater Infrastructure Market."

- "

Competitive Ecosystem of TCP and RTP Pipe Market

The competitive landscape of the TCP and RTP Pipe Market is characterized by a mix of established industrial conglomerates and specialized manufacturers, all vying for market share through product innovation, strategic partnerships, and regional expansion. Key players are increasingly focusing on developing application-specific solutions and expanding their manufacturing capabilities to cater to diverse end-use industries.

- Strohm: A leading global provider of TCP solutions, particularly for the oil & gas and renewables sectors, renowned for its extensive track record in challenging deepwater and ultra-deepwater projects.

- TechnipFMC plc: A major player in subsea technologies, offering integrated solutions that include advanced flexible and rigid pipes, contributing significantly to offshore oil and gas infrastructure.

- NOV.: A diversified provider of equipment and components for the oil and gas industry, with a focus on advanced pipe technologies and solutions for various demanding applications.

- Baker Hughes Company: An energy technology company providing a broad portfolio of solutions across the energy value chain, including specialized pipe systems for upstream and midstream operations.

- Prysmian: A world leader in energy and telecom cable systems, with offerings that extend into specialized piping solutions, leveraging its expertise in material science and large-scale manufacturing.

- Wienerberger AG: Primarily known for ceramic building materials, the company also engages in specific piping solutions, particularly in the broader infrastructure sector within its regional markets.

- Georg Fischer Ltd.: A global industrial company with a strong presence in piping systems, offering a wide range of thermoplastic solutions for water, gas, and industrial applications.

- Flexpipe: A specialist in high-density polyethylene (HDPE) composite pipe systems for oil and gas, known for its spoolable and corrosion-resistant products.

- Advanced Drainage Systems. : A leading manufacturer of stormwater and wastewater management solutions, including corrugated plastic pipe, serving municipal and infrastructure needs.

- Chevron Phillips Chemical Company LLC.: A major producer of olefins and polyolefins, providing critical raw materials like polyethylene for pipe manufacturing, thus indirectly influencing the market.

- Uponor Corporation: A prominent international provider of solutions for plumbing, indoor climate, and infrastructure, with a focus on sustainable and efficient pipe systems.

- Magma Global Ltd.: Specializes in the development and manufacture of high-performance composite pipes, particularly for demanding subsea applications in the energy industry.

- PES.TEC: Focuses on advanced polymer engineering and provides bespoke thermoplastic and composite solutions for various industrial applications.

- FlexSteel USA, LLC.: A key provider of spoolable, high-pressure composite line pipe systems, primarily serving the oil and gas industry with cost-effective and durable solutions.

- Simtech: Offers a range of thermoplastic piping products and services, catering to industrial applications requiring chemical resistance and reliability.

- Future Pipe Industries: A global leader in composite pipe systems, offering a wide range of products for oil & gas, water, industrial, and infrastructure applications.

- SoluForce B.V.: A pioneer and leading manufacturer of high-pressure Reinforced Thermoplastic Pipe (RTP) systems, with a strong focus on the oil and gas, hydrogen, and water markets."

- "

Recent Developments & Milestones in TCP and RTP Pipe Market

- Q4 2024: Strohm announced a strategic partnership with a major European energy company to pilot the use of large-diameter TCP for offshore hydrogen transport, signaling a significant step towards future energy infrastructure applications within the TCP and RTP Pipe Market.

- Q3 2024: FlexSteel USA, LLC. unveiled a new generation of its spoolable composite line pipe, designed for enhanced pressure ratings and improved chemical resistance, specifically targeting challenging sour gas applications in North America.

- Q2 2025: Magma Global Ltd. reported successful qualification of its m-pipe® for ultra-deepwater applications up to 3,000 meters (9,842 feet) in the Gulf of Mexico, further solidifying its position in the high-performance subsea segment.

- Q1 2025: Future Pipe Industries expanded its manufacturing capabilities in Saudi Arabia, increasing production capacity for large-diameter RTP and composite pipes to meet the growing demand from regional infrastructure and industrial projects, including those in the Polyethylene Pipe Market.

- Q4 2023: TechnipFMC plc completed the installation of a complex flexible pipe system for a deepwater project off the coast of Brazil, showcasing the versatility and reliability of advanced flexible and composite solutions in demanding offshore environments.

- Q3 2025: Advanced Drainage Systems. announced new product lines incorporating recycled content into their thermoplastic pipe offerings, aligning with global sustainability goals and expanding their eco-friendly footprint in municipal and agricultural water management."

- "

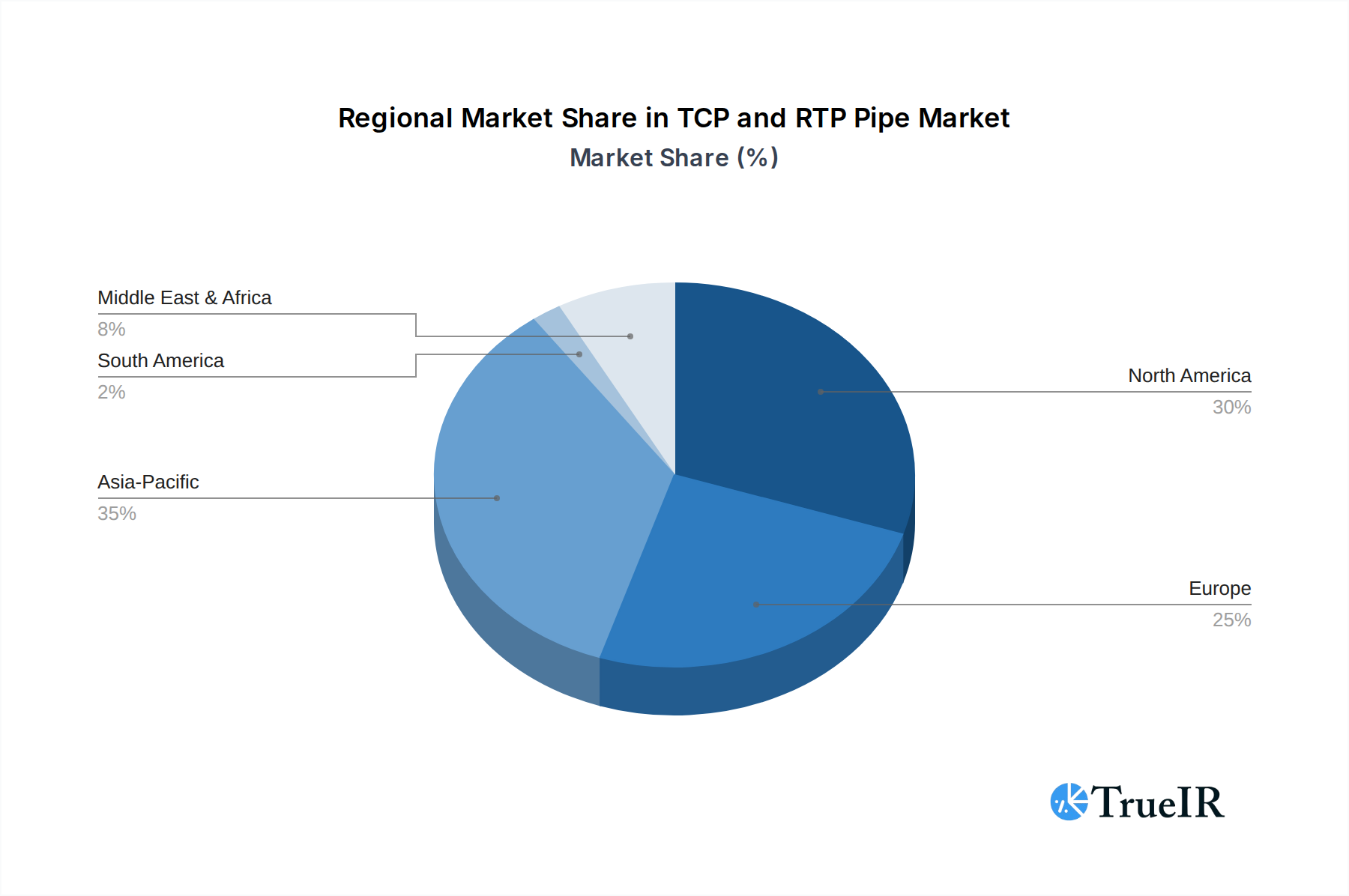

Regional Market Breakdown for TCP and RTP Pipe Market

The TCP and RTP Pipe Market exhibits distinct dynamics across key geographical regions, driven by varying infrastructure needs, regulatory environments, and industrial growth trajectories. Asia Pacific is anticipated to be the fastest-growing region, driven by rapid industrialization, urbanization, and significant investments in oil and gas infrastructure, water treatment plants, and mining operations, particularly in economies such as China, India, and ASEAN nations. The region's substantial demand for new infrastructure, coupled with the need for durable and cost-effective piping solutions, makes it a high-potential market. Major projects across the Oil and Gas Pipeline Market and the Water & Wastewater Infrastructure Market are significant demand drivers.

North America holds a substantial revenue share, representing a mature yet evolving market. The demand here is largely propelled by the replacement of aging infrastructure, expansion of shale oil and gas production, and stringent regulations demanding leak-proof and corrosion-resistant piping. The focus on reducing operational costs and environmental impact fuels the adoption of TCP and RTP, with key investments in the refurbishment of existing pipelines and new midstream projects. The United States and Canada are leading this trend, leveraging advanced material solutions, including those employing Carbon Fiber Composites Market technologies.

Europe presents a stable market with moderate growth, characterized by a strong emphasis on sustainability, energy transition, and the modernization of existing pipeline networks. The region is seeing increasing application of TCP and RTP in hydrogen transport infrastructure and CO2 capture, utilization, and storage (CCUS) projects, aligning with its decarbonization goals. Countries like Germany, the UK, and Norway are at the forefront of adopting these advanced solutions for both traditional and new energy carriers.

The Middle East & Africa region is a critical market, particularly for the oil and gas sector. The harsh operating environments, including high temperatures and corrosive fluids, make TCP and RTP highly attractive for new exploration, production, and transportation projects. Significant investments in expanding oil and gas fields, coupled with infrastructure development in countries within the GCC, are primary drivers for market growth, positioning this region for considerable expansion due to its extensive resource base and ongoing large-scale projects."

- "

TCP and RTP Pipe Regional Market Share

Regulatory & Policy Landscape Shaping TCP and RTP Pipe Market

The TCP and RTP Pipe Market operates within a complex web of regulatory frameworks, industry standards, and government policies that significantly influence product development, market acceptance, and deployment. International standards organizations, such as the International Organization for Standardization (ISO) and the American Petroleum Institute (API), play a crucial role in establishing performance benchmarks and safety specifications. For instance, API 17J (Specification for Unbonded Flexible Pipe) and API 15S (Qualification of Spoolable Reinforced Thermoplastic Linepipe) are critical for products used in the Oil and Gas Pipeline Market, ensuring material integrity and operational safety in high-pressure and corrosive environments. Similarly, ISO 14692 (Petroleum and natural gas industries — Glass-reinforced plastics (GRP) piping systems) provides a foundation that is often adapted for other fiber-reinforced polymer pipes.

National and regional regulations, such as those from the U.S. Department of Transportation (DOT) for pipeline safety, and various directives within the European Union, impose stringent requirements on pipeline construction, operation, and maintenance. Recent policy shifts towards reducing carbon emissions and enhancing environmental protection are also impacting the market. For example, policies supporting hydrogen infrastructure development are creating new opportunities for TCP and RTP, as these pipes are well-suited for transporting hydrogen due to their non-corrosive nature and chemical compatibility. Furthermore, regulations promoting the use of sustainable materials and minimizing environmental impact during pipeline installation and decommissioning are increasingly favoring the lightweight and often recyclable aspects of thermoplastic materials. Adherence to these evolving standards and regulations is not only a compliance necessity but also a competitive differentiator within the TCP and RTP Pipe Market, driving continuous innovation in material science and pipe design to meet ever-higher safety and environmental performance criteria."

- "

Export, Trade Flow & Tariff Impact on TCP and RTP Pipe Market

The global TCP and RTP Pipe Market is characterized by significant international trade flows, driven by specialized manufacturing capabilities and regional demand discrepancies. Major exporting nations are typically those with advanced polymer processing industries and strong research and development capabilities, primarily in North America and Europe. These regions supply high-performance TCP and RTP products, often customized for specific applications in the Oil and Gas Pipeline Market, to demanding markets worldwide. Conversely, leading importing nations include developing economies in Asia Pacific, the Middle East, and Africa, which are undergoing rapid infrastructure expansion and require reliable, advanced piping solutions for their growing energy, water, and mining sectors. The trade of raw materials, such as high-density polyethylene (HDPE), polyamide (PA12), and carbon fibers, also contributes significantly to the cross-border movement, influencing production costs and competitiveness across different geographies.

Tariffs and non-tariff barriers, though not as directly prominent as in some other sectors, can influence the cross-border volume and pricing within the Industrial Piping Systems Market. For instance, general trade tensions, such as those between the U.S. and China, can lead to tariffs on certain polymer resins or manufactured composite components, indirectly increasing the cost of TCP and RTP products or raw materials for manufacturers in affected regions. Brexit has introduced new customs procedures and potential tariffs between the UK and the EU, which can affect the supply chain efficiency for European manufacturers. Furthermore, local content requirements in some emerging markets can act as non-tariff barriers, encouraging local manufacturing or partnerships rather than direct imports. These trade policies prompt companies to strategically locate manufacturing facilities closer to key demand centers, such as the expansion of plants in the Middle East and Asia, to mitigate tariff impacts, reduce logistics costs, and improve supply chain resilience, thereby influencing regional market dynamics for the TCP and RTP Pipe Market.

TCP and RTP Pipe Segmentation

-

1. Type

- 1.1. Reinforced Thermoplastic Pipe

- 1.2. Thermoplastic composite pipe

-

2. Material

- 2.1. Polyethylene (HDPE)

- 2.2. Polyamide (PA12),

- 2.3. Polyvinylidene fluoride (PVDF)

- 2.4. Polyetheretherketone (PEEK)

- 2.5. Thermoplastic tape (UD tape)

- 2.6. Aramid or polyester fiber

- 2.7. Carbon fiber

- 2.8. Other

-

3. Application Industry

- 3.1. Oil and Gas

- 3.2. Water & Wastewater

- 3.3. Mining

- 3.4. Other Industrial Uses

-

4. Diameter Size

- 4.1. Small Diameter Pipes

- 4.2. Medium Diameter Pipes

- 4.3. Large Diameter Pipes

-

5. Distribution Channel

- 5.1. Direct Sales

- 5.2. Indirect Sales

TCP and RTP Pipe Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

TCP and RTP Pipe Regional Market Share

Geographic Coverage of TCP and RTP Pipe

TCP and RTP Pipe REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Reinforced Thermoplastic Pipe

- 5.1.2. Thermoplastic composite pipe

- 5.2. Market Analysis, Insights and Forecast - by Material

- 5.2.1. Polyethylene (HDPE)

- 5.2.2. Polyamide (PA12),

- 5.2.3. Polyvinylidene fluoride (PVDF)

- 5.2.4. Polyetheretherketone (PEEK)

- 5.2.5. Thermoplastic tape (UD tape)

- 5.2.6. Aramid or polyester fiber

- 5.2.7. Carbon fiber

- 5.2.8. Other

- 5.3. Market Analysis, Insights and Forecast - by Application Industry

- 5.3.1. Oil and Gas

- 5.3.2. Water & Wastewater

- 5.3.3. Mining

- 5.3.4. Other Industrial Uses

- 5.4. Market Analysis, Insights and Forecast - by Diameter Size

- 5.4.1. Small Diameter Pipes

- 5.4.2. Medium Diameter Pipes

- 5.4.3. Large Diameter Pipes

- 5.5. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.5.1. Direct Sales

- 5.5.2. Indirect Sales

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. North America

- 5.6.2. South America

- 5.6.3. Europe

- 5.6.4. Middle East & Africa

- 5.6.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global TCP and RTP Pipe Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Reinforced Thermoplastic Pipe

- 6.1.2. Thermoplastic composite pipe

- 6.2. Market Analysis, Insights and Forecast - by Material

- 6.2.1. Polyethylene (HDPE)

- 6.2.2. Polyamide (PA12),

- 6.2.3. Polyvinylidene fluoride (PVDF)

- 6.2.4. Polyetheretherketone (PEEK)

- 6.2.5. Thermoplastic tape (UD tape)

- 6.2.6. Aramid or polyester fiber

- 6.2.7. Carbon fiber

- 6.2.8. Other

- 6.3. Market Analysis, Insights and Forecast - by Application Industry

- 6.3.1. Oil and Gas

- 6.3.2. Water & Wastewater

- 6.3.3. Mining

- 6.3.4. Other Industrial Uses

- 6.4. Market Analysis, Insights and Forecast - by Diameter Size

- 6.4.1. Small Diameter Pipes

- 6.4.2. Medium Diameter Pipes

- 6.4.3. Large Diameter Pipes

- 6.5. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.5.1. Direct Sales

- 6.5.2. Indirect Sales

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America TCP and RTP Pipe Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Reinforced Thermoplastic Pipe

- 7.1.2. Thermoplastic composite pipe

- 7.2. Market Analysis, Insights and Forecast - by Material

- 7.2.1. Polyethylene (HDPE)

- 7.2.2. Polyamide (PA12),

- 7.2.3. Polyvinylidene fluoride (PVDF)

- 7.2.4. Polyetheretherketone (PEEK)

- 7.2.5. Thermoplastic tape (UD tape)

- 7.2.6. Aramid or polyester fiber

- 7.2.7. Carbon fiber

- 7.2.8. Other

- 7.3. Market Analysis, Insights and Forecast - by Application Industry

- 7.3.1. Oil and Gas

- 7.3.2. Water & Wastewater

- 7.3.3. Mining

- 7.3.4. Other Industrial Uses

- 7.4. Market Analysis, Insights and Forecast - by Diameter Size

- 7.4.1. Small Diameter Pipes

- 7.4.2. Medium Diameter Pipes

- 7.4.3. Large Diameter Pipes

- 7.5. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.5.1. Direct Sales

- 7.5.2. Indirect Sales

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. South America TCP and RTP Pipe Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Reinforced Thermoplastic Pipe

- 8.1.2. Thermoplastic composite pipe

- 8.2. Market Analysis, Insights and Forecast - by Material

- 8.2.1. Polyethylene (HDPE)

- 8.2.2. Polyamide (PA12),

- 8.2.3. Polyvinylidene fluoride (PVDF)

- 8.2.4. Polyetheretherketone (PEEK)

- 8.2.5. Thermoplastic tape (UD tape)

- 8.2.6. Aramid or polyester fiber

- 8.2.7. Carbon fiber

- 8.2.8. Other

- 8.3. Market Analysis, Insights and Forecast - by Application Industry

- 8.3.1. Oil and Gas

- 8.3.2. Water & Wastewater

- 8.3.3. Mining

- 8.3.4. Other Industrial Uses

- 8.4. Market Analysis, Insights and Forecast - by Diameter Size

- 8.4.1. Small Diameter Pipes

- 8.4.2. Medium Diameter Pipes

- 8.4.3. Large Diameter Pipes

- 8.5. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.5.1. Direct Sales

- 8.5.2. Indirect Sales

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Europe TCP and RTP Pipe Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Reinforced Thermoplastic Pipe

- 9.1.2. Thermoplastic composite pipe

- 9.2. Market Analysis, Insights and Forecast - by Material

- 9.2.1. Polyethylene (HDPE)

- 9.2.2. Polyamide (PA12),

- 9.2.3. Polyvinylidene fluoride (PVDF)

- 9.2.4. Polyetheretherketone (PEEK)

- 9.2.5. Thermoplastic tape (UD tape)

- 9.2.6. Aramid or polyester fiber

- 9.2.7. Carbon fiber

- 9.2.8. Other

- 9.3. Market Analysis, Insights and Forecast - by Application Industry

- 9.3.1. Oil and Gas

- 9.3.2. Water & Wastewater

- 9.3.3. Mining

- 9.3.4. Other Industrial Uses

- 9.4. Market Analysis, Insights and Forecast - by Diameter Size

- 9.4.1. Small Diameter Pipes

- 9.4.2. Medium Diameter Pipes

- 9.4.3. Large Diameter Pipes

- 9.5. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.5.1. Direct Sales

- 9.5.2. Indirect Sales

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Middle East & Africa TCP and RTP Pipe Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Reinforced Thermoplastic Pipe

- 10.1.2. Thermoplastic composite pipe

- 10.2. Market Analysis, Insights and Forecast - by Material

- 10.2.1. Polyethylene (HDPE)

- 10.2.2. Polyamide (PA12),

- 10.2.3. Polyvinylidene fluoride (PVDF)

- 10.2.4. Polyetheretherketone (PEEK)

- 10.2.5. Thermoplastic tape (UD tape)

- 10.2.6. Aramid or polyester fiber

- 10.2.7. Carbon fiber

- 10.2.8. Other

- 10.3. Market Analysis, Insights and Forecast - by Application Industry

- 10.3.1. Oil and Gas

- 10.3.2. Water & Wastewater

- 10.3.3. Mining

- 10.3.4. Other Industrial Uses

- 10.4. Market Analysis, Insights and Forecast - by Diameter Size

- 10.4.1. Small Diameter Pipes

- 10.4.2. Medium Diameter Pipes

- 10.4.3. Large Diameter Pipes

- 10.5. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.5.1. Direct Sales

- 10.5.2. Indirect Sales

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Asia Pacific TCP and RTP Pipe Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Reinforced Thermoplastic Pipe

- 11.1.2. Thermoplastic composite pipe

- 11.2. Market Analysis, Insights and Forecast - by Material

- 11.2.1. Polyethylene (HDPE)

- 11.2.2. Polyamide (PA12),

- 11.2.3. Polyvinylidene fluoride (PVDF)

- 11.2.4. Polyetheretherketone (PEEK)

- 11.2.5. Thermoplastic tape (UD tape)

- 11.2.6. Aramid or polyester fiber

- 11.2.7. Carbon fiber

- 11.2.8. Other

- 11.3. Market Analysis, Insights and Forecast - by Application Industry

- 11.3.1. Oil and Gas

- 11.3.2. Water & Wastewater

- 11.3.3. Mining

- 11.3.4. Other Industrial Uses

- 11.4. Market Analysis, Insights and Forecast - by Diameter Size

- 11.4.1. Small Diameter Pipes

- 11.4.2. Medium Diameter Pipes

- 11.4.3. Large Diameter Pipes

- 11.5. Market Analysis, Insights and Forecast - by Distribution Channel

- 11.5.1. Direct Sales

- 11.5.2. Indirect Sales

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Strohm

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 TechnipFMC plc

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 NOV.

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Baker Hughes Company

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Prysmian

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Wienerberger AG

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Georg Fischer Ltd.

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Flexpipe

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Advanced Drainage Systems.

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Chevron Phillips Chemical Company LLC.

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Uponor Corporation

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Magma Global Ltd.

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 PES.TEC

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 FlexSteel USA LLC.

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Simtech

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Future Pipe Industries

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 SoluForce B.V.

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.1 Strohm

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global TCP and RTP Pipe Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America TCP and RTP Pipe Revenue (million), by Type 2025 & 2033

- Figure 3: North America TCP and RTP Pipe Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America TCP and RTP Pipe Revenue (million), by Material 2025 & 2033

- Figure 5: North America TCP and RTP Pipe Revenue Share (%), by Material 2025 & 2033

- Figure 6: North America TCP and RTP Pipe Revenue (million), by Application Industry 2025 & 2033

- Figure 7: North America TCP and RTP Pipe Revenue Share (%), by Application Industry 2025 & 2033

- Figure 8: North America TCP and RTP Pipe Revenue (million), by Diameter Size 2025 & 2033

- Figure 9: North America TCP and RTP Pipe Revenue Share (%), by Diameter Size 2025 & 2033

- Figure 10: North America TCP and RTP Pipe Revenue (million), by Distribution Channel 2025 & 2033

- Figure 11: North America TCP and RTP Pipe Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 12: North America TCP and RTP Pipe Revenue (million), by Country 2025 & 2033

- Figure 13: North America TCP and RTP Pipe Revenue Share (%), by Country 2025 & 2033

- Figure 14: South America TCP and RTP Pipe Revenue (million), by Type 2025 & 2033

- Figure 15: South America TCP and RTP Pipe Revenue Share (%), by Type 2025 & 2033

- Figure 16: South America TCP and RTP Pipe Revenue (million), by Material 2025 & 2033

- Figure 17: South America TCP and RTP Pipe Revenue Share (%), by Material 2025 & 2033

- Figure 18: South America TCP and RTP Pipe Revenue (million), by Application Industry 2025 & 2033

- Figure 19: South America TCP and RTP Pipe Revenue Share (%), by Application Industry 2025 & 2033

- Figure 20: South America TCP and RTP Pipe Revenue (million), by Diameter Size 2025 & 2033

- Figure 21: South America TCP and RTP Pipe Revenue Share (%), by Diameter Size 2025 & 2033

- Figure 22: South America TCP and RTP Pipe Revenue (million), by Distribution Channel 2025 & 2033

- Figure 23: South America TCP and RTP Pipe Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 24: South America TCP and RTP Pipe Revenue (million), by Country 2025 & 2033

- Figure 25: South America TCP and RTP Pipe Revenue Share (%), by Country 2025 & 2033

- Figure 26: Europe TCP and RTP Pipe Revenue (million), by Type 2025 & 2033

- Figure 27: Europe TCP and RTP Pipe Revenue Share (%), by Type 2025 & 2033

- Figure 28: Europe TCP and RTP Pipe Revenue (million), by Material 2025 & 2033

- Figure 29: Europe TCP and RTP Pipe Revenue Share (%), by Material 2025 & 2033

- Figure 30: Europe TCP and RTP Pipe Revenue (million), by Application Industry 2025 & 2033

- Figure 31: Europe TCP and RTP Pipe Revenue Share (%), by Application Industry 2025 & 2033

- Figure 32: Europe TCP and RTP Pipe Revenue (million), by Diameter Size 2025 & 2033

- Figure 33: Europe TCP and RTP Pipe Revenue Share (%), by Diameter Size 2025 & 2033

- Figure 34: Europe TCP and RTP Pipe Revenue (million), by Distribution Channel 2025 & 2033

- Figure 35: Europe TCP and RTP Pipe Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 36: Europe TCP and RTP Pipe Revenue (million), by Country 2025 & 2033

- Figure 37: Europe TCP and RTP Pipe Revenue Share (%), by Country 2025 & 2033

- Figure 38: Middle East & Africa TCP and RTP Pipe Revenue (million), by Type 2025 & 2033

- Figure 39: Middle East & Africa TCP and RTP Pipe Revenue Share (%), by Type 2025 & 2033

- Figure 40: Middle East & Africa TCP and RTP Pipe Revenue (million), by Material 2025 & 2033

- Figure 41: Middle East & Africa TCP and RTP Pipe Revenue Share (%), by Material 2025 & 2033

- Figure 42: Middle East & Africa TCP and RTP Pipe Revenue (million), by Application Industry 2025 & 2033

- Figure 43: Middle East & Africa TCP and RTP Pipe Revenue Share (%), by Application Industry 2025 & 2033

- Figure 44: Middle East & Africa TCP and RTP Pipe Revenue (million), by Diameter Size 2025 & 2033

- Figure 45: Middle East & Africa TCP and RTP Pipe Revenue Share (%), by Diameter Size 2025 & 2033

- Figure 46: Middle East & Africa TCP and RTP Pipe Revenue (million), by Distribution Channel 2025 & 2033

- Figure 47: Middle East & Africa TCP and RTP Pipe Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 48: Middle East & Africa TCP and RTP Pipe Revenue (million), by Country 2025 & 2033

- Figure 49: Middle East & Africa TCP and RTP Pipe Revenue Share (%), by Country 2025 & 2033

- Figure 50: Asia Pacific TCP and RTP Pipe Revenue (million), by Type 2025 & 2033

- Figure 51: Asia Pacific TCP and RTP Pipe Revenue Share (%), by Type 2025 & 2033

- Figure 52: Asia Pacific TCP and RTP Pipe Revenue (million), by Material 2025 & 2033

- Figure 53: Asia Pacific TCP and RTP Pipe Revenue Share (%), by Material 2025 & 2033

- Figure 54: Asia Pacific TCP and RTP Pipe Revenue (million), by Application Industry 2025 & 2033

- Figure 55: Asia Pacific TCP and RTP Pipe Revenue Share (%), by Application Industry 2025 & 2033

- Figure 56: Asia Pacific TCP and RTP Pipe Revenue (million), by Diameter Size 2025 & 2033

- Figure 57: Asia Pacific TCP and RTP Pipe Revenue Share (%), by Diameter Size 2025 & 2033

- Figure 58: Asia Pacific TCP and RTP Pipe Revenue (million), by Distribution Channel 2025 & 2033

- Figure 59: Asia Pacific TCP and RTP Pipe Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 60: Asia Pacific TCP and RTP Pipe Revenue (million), by Country 2025 & 2033

- Figure 61: Asia Pacific TCP and RTP Pipe Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global TCP and RTP Pipe Revenue million Forecast, by Type 2020 & 2033

- Table 2: Global TCP and RTP Pipe Revenue million Forecast, by Material 2020 & 2033

- Table 3: Global TCP and RTP Pipe Revenue million Forecast, by Application Industry 2020 & 2033

- Table 4: Global TCP and RTP Pipe Revenue million Forecast, by Diameter Size 2020 & 2033

- Table 5: Global TCP and RTP Pipe Revenue million Forecast, by Distribution Channel 2020 & 2033

- Table 6: Global TCP and RTP Pipe Revenue million Forecast, by Region 2020 & 2033

- Table 7: Global TCP and RTP Pipe Revenue million Forecast, by Type 2020 & 2033

- Table 8: Global TCP and RTP Pipe Revenue million Forecast, by Material 2020 & 2033

- Table 9: Global TCP and RTP Pipe Revenue million Forecast, by Application Industry 2020 & 2033

- Table 10: Global TCP and RTP Pipe Revenue million Forecast, by Diameter Size 2020 & 2033

- Table 11: Global TCP and RTP Pipe Revenue million Forecast, by Distribution Channel 2020 & 2033

- Table 12: Global TCP and RTP Pipe Revenue million Forecast, by Country 2020 & 2033

- Table 13: United States TCP and RTP Pipe Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Canada TCP and RTP Pipe Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Mexico TCP and RTP Pipe Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global TCP and RTP Pipe Revenue million Forecast, by Type 2020 & 2033

- Table 17: Global TCP and RTP Pipe Revenue million Forecast, by Material 2020 & 2033

- Table 18: Global TCP and RTP Pipe Revenue million Forecast, by Application Industry 2020 & 2033

- Table 19: Global TCP and RTP Pipe Revenue million Forecast, by Diameter Size 2020 & 2033

- Table 20: Global TCP and RTP Pipe Revenue million Forecast, by Distribution Channel 2020 & 2033

- Table 21: Global TCP and RTP Pipe Revenue million Forecast, by Country 2020 & 2033

- Table 22: Brazil TCP and RTP Pipe Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Argentina TCP and RTP Pipe Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Rest of South America TCP and RTP Pipe Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Global TCP and RTP Pipe Revenue million Forecast, by Type 2020 & 2033

- Table 26: Global TCP and RTP Pipe Revenue million Forecast, by Material 2020 & 2033

- Table 27: Global TCP and RTP Pipe Revenue million Forecast, by Application Industry 2020 & 2033

- Table 28: Global TCP and RTP Pipe Revenue million Forecast, by Diameter Size 2020 & 2033

- Table 29: Global TCP and RTP Pipe Revenue million Forecast, by Distribution Channel 2020 & 2033

- Table 30: Global TCP and RTP Pipe Revenue million Forecast, by Country 2020 & 2033

- Table 31: United Kingdom TCP and RTP Pipe Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Germany TCP and RTP Pipe Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: France TCP and RTP Pipe Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: Italy TCP and RTP Pipe Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: Spain TCP and RTP Pipe Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Russia TCP and RTP Pipe Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Benelux TCP and RTP Pipe Revenue (million) Forecast, by Application 2020 & 2033

- Table 38: Nordics TCP and RTP Pipe Revenue (million) Forecast, by Application 2020 & 2033

- Table 39: Rest of Europe TCP and RTP Pipe Revenue (million) Forecast, by Application 2020 & 2033

- Table 40: Global TCP and RTP Pipe Revenue million Forecast, by Type 2020 & 2033

- Table 41: Global TCP and RTP Pipe Revenue million Forecast, by Material 2020 & 2033

- Table 42: Global TCP and RTP Pipe Revenue million Forecast, by Application Industry 2020 & 2033

- Table 43: Global TCP and RTP Pipe Revenue million Forecast, by Diameter Size 2020 & 2033

- Table 44: Global TCP and RTP Pipe Revenue million Forecast, by Distribution Channel 2020 & 2033

- Table 45: Global TCP and RTP Pipe Revenue million Forecast, by Country 2020 & 2033

- Table 46: Turkey TCP and RTP Pipe Revenue (million) Forecast, by Application 2020 & 2033

- Table 47: Israel TCP and RTP Pipe Revenue (million) Forecast, by Application 2020 & 2033

- Table 48: GCC TCP and RTP Pipe Revenue (million) Forecast, by Application 2020 & 2033

- Table 49: North Africa TCP and RTP Pipe Revenue (million) Forecast, by Application 2020 & 2033

- Table 50: South Africa TCP and RTP Pipe Revenue (million) Forecast, by Application 2020 & 2033

- Table 51: Rest of Middle East & Africa TCP and RTP Pipe Revenue (million) Forecast, by Application 2020 & 2033

- Table 52: Global TCP and RTP Pipe Revenue million Forecast, by Type 2020 & 2033

- Table 53: Global TCP and RTP Pipe Revenue million Forecast, by Material 2020 & 2033

- Table 54: Global TCP and RTP Pipe Revenue million Forecast, by Application Industry 2020 & 2033

- Table 55: Global TCP and RTP Pipe Revenue million Forecast, by Diameter Size 2020 & 2033

- Table 56: Global TCP and RTP Pipe Revenue million Forecast, by Distribution Channel 2020 & 2033

- Table 57: Global TCP and RTP Pipe Revenue million Forecast, by Country 2020 & 2033

- Table 58: China TCP and RTP Pipe Revenue (million) Forecast, by Application 2020 & 2033

- Table 59: India TCP and RTP Pipe Revenue (million) Forecast, by Application 2020 & 2033

- Table 60: Japan TCP and RTP Pipe Revenue (million) Forecast, by Application 2020 & 2033

- Table 61: South Korea TCP and RTP Pipe Revenue (million) Forecast, by Application 2020 & 2033

- Table 62: ASEAN TCP and RTP Pipe Revenue (million) Forecast, by Application 2020 & 2033

- Table 63: Oceania TCP and RTP Pipe Revenue (million) Forecast, by Application 2020 & 2033

- Table 64: Rest of Asia Pacific TCP and RTP Pipe Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the TCP and RTP Pipe?

The projected CAGR is approximately 6.4%.

2. Which companies are prominent players in the TCP and RTP Pipe?

Key companies in the market include Strohm , TechnipFMC plc, NOV., Baker Hughes Company , Prysmian , Wienerberger AG, Georg Fischer Ltd., Flexpipe , Advanced Drainage Systems. , Chevron Phillips Chemical Company LLC., Uponor Corporation , Magma Global Ltd., PES.TEC , FlexSteel USA, LLC., Simtech , Future Pipe Industries , SoluForce B.V..

3. What are the main segments of the TCP and RTP Pipe?

The market segments include Type, Material , Application Industry, Diameter Size, Distribution Channel .

4. Can you provide details about the market size?

The market size is estimated to be USD 7237.5 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "TCP and RTP Pipe," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the TCP and RTP Pipe report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the TCP and RTP Pipe?

To stay informed about further developments, trends, and reports in the TCP and RTP Pipe, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence