Key Insights

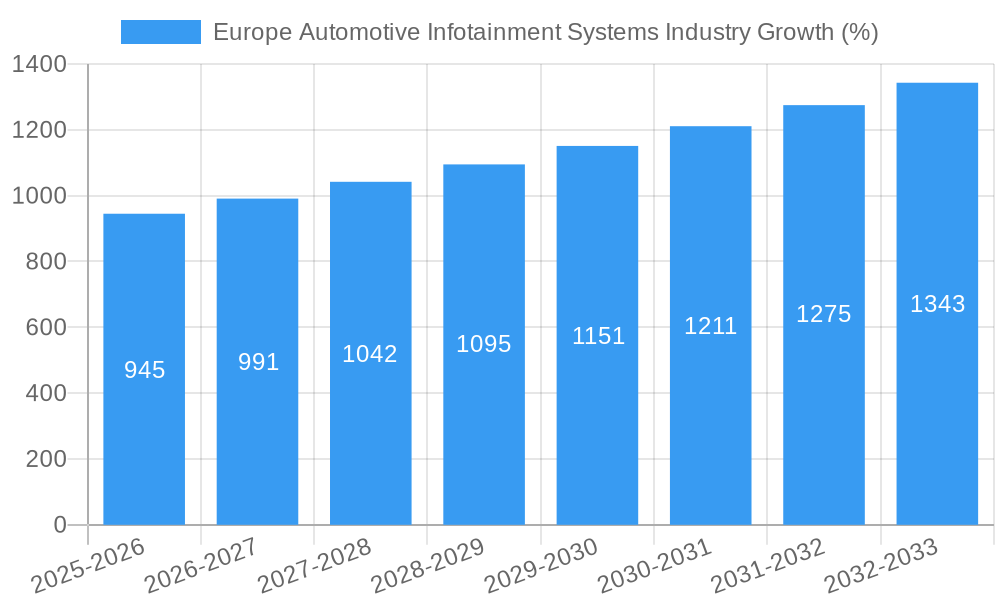

The European automotive infotainment systems market is experiencing robust growth, driven by increasing vehicle production, rising consumer demand for advanced in-car connectivity features, and the integration of sophisticated infotainment systems in both passenger cars and commercial vehicles. The market's Compound Annual Growth Rate (CAGR) of 6.07% from 2019 to 2024 indicates a healthy trajectory, projected to continue into the forecast period (2025-2033). Key growth drivers include the rising adoption of smartphones and the demand for seamless integration with vehicle systems, the increasing popularity of connected car services like navigation, entertainment streaming, and safety applications, and the technological advancements in areas such as artificial intelligence and voice recognition. The market segmentation reveals a strong preference for in-dash infotainment systems, reflecting consumer prioritization of integrated and user-friendly interfaces. Germany, the United Kingdom, and France represent the largest national markets within Europe, benefiting from higher vehicle ownership rates and technological advancement. However, the market also faces certain restraints including high initial investment costs for advanced systems and concerns about data privacy and security related to connected car technologies. Nevertheless, ongoing innovation and a focus on affordability are expected to mitigate these challenges, driving further market expansion.

The European automotive infotainment systems market is segmented by vehicle type (passenger cars and commercial vehicles), installation type (in-dash and rear seat infotainment), and country (Germany, UK, France, Italy, and Rest of Europe). The passenger car segment currently dominates due to higher vehicle sales volume, but the commercial vehicle segment is poised for significant growth as fleet operators adopt advanced telematics and communication systems for improved efficiency and safety. In terms of installation type, in-dash systems are the leading choice, reflecting a preference for integrated, user-friendly interfaces. Within the geographical segmentation, Germany, UK, and France remain the leading markets, driven by strong vehicle sales and consumer adoption of premium features. However, opportunities exist across all European countries as consumer preferences shift towards enhanced connectivity and infotainment options in vehicles. The competitive landscape is characterized by several established players, such as Alpine Electronics, Denso, Visteon, and Harman, alongside emerging companies specializing in innovative technologies. The market is likely to see continued consolidation as companies strategically invest in research and development to maintain their competitive edge.

Europe Automotive Infotainment Systems Industry: 2019-2033 Market Report

This comprehensive report provides a detailed analysis of the Europe Automotive Infotainment Systems market, offering invaluable insights for industry stakeholders, investors, and strategists. Covering the period 2019-2033, with a focus on 2025, this study unveils market dynamics, competitive landscapes, and future growth trajectories. The report leverages extensive data analysis and expert insights to forecast a robust market expansion, driven by technological advancements and evolving consumer preferences. Download now to gain a competitive edge.

Europe Automotive Infotainment Systems Industry Market Structure & Competitive Landscape

The European automotive infotainment systems market exhibits a moderately concentrated structure, with several key players dominating the landscape. Leading companies such as Alpine Electronics Inc, Denso Corporation, Visteon Corporation, Aisin Corporation, Harman International, Continental AG, BorgWarner Inc, JVCKENWOOD Corporation, Robert Bosch GmbH, Pioneer Corporation, and Panasonic Corporation, compete fiercely based on product innovation, technological capabilities, and distribution networks.

Market Concentration: The Herfindahl-Hirschman Index (HHI) for the market is estimated at xx, indicating a moderately concentrated market. Further analysis of market share and concentration ratios will be provided in the full report.

Innovation Drivers: The relentless push for enhanced driver experience, integration of advanced driver-assistance systems (ADAS), and the increasing demand for seamless connectivity are key innovation drivers. This has led to the development of sophisticated infotainment systems incorporating features like augmented reality head-up displays, AI-powered voice assistants, and advanced driver monitoring systems.

Regulatory Impacts: Stringent regulations related to data privacy, cybersecurity, and driver distraction are influencing the design and functionalities of infotainment systems, particularly impacting features like in-car internet connectivity and video streaming.

Product Substitutes: While infotainment systems are becoming increasingly integrated into vehicles, potential substitutes include smartphone-based infotainment solutions and aftermarket accessories that offer comparable features at a potentially lower cost. However, factory-integrated systems provide better safety and seamless vehicle integration, which is a critical factor for OEMs.

End-User Segmentation: The market is segmented by vehicle type (passenger cars and commercial vehicles), installation type (in-dash and rear-seat infotainment), and geography (Germany, UK, France, Italy, and Rest of Europe). Analysis of segment-wise demand and growth potential are detailed in the report.

M&A Trends: The industry has witnessed a significant number of mergers and acquisitions (M&A) in recent years, driven by the need for expansion, technological integration, and improved market position. The estimated volume of M&A deals in the sector between 2019 and 2024 is valued at approximately xx Million. These activities have had an impact on market consolidation, increasing both market concentration and the overall value of the industry. Specific details about significant deals will be included in the report.

Europe Automotive Infotainment Systems Industry Market Trends & Opportunities

The European automotive infotainment systems market is experiencing significant growth, driven by a confluence of factors. The market size is projected to reach xx Million by 2025, exhibiting a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033). This substantial growth is fueled by increasing vehicle production, rising consumer demand for enhanced connectivity features, the increasing adoption of advanced technologies in vehicles, and the penetration of electric vehicles.

The market is witnessing a rapid shift towards cloud-based infotainment systems, enabling over-the-air software updates and personalized user experiences. This is changing consumer preferences significantly, leading to greater demand for connected features and customized infotainment solutions. The increasing adoption of AI and machine learning algorithms are also transforming infotainment systems, providing better user interfaces and voice control capabilities. The market penetration of advanced driver-assistance systems and autonomous driving functionalities are also contributing significantly to the rising demand. The industry is also witnessing increased competition, leading to a focus on developing cost-effective and high-quality infotainment systems.

Dominant Markets & Segments in Europe Automotive Infotainment Systems Industry

The German market dominates the European automotive infotainment systems market, followed by the UK and France. This dominance stems from factors such as high vehicle production, strong automotive OEM presence, and high consumer spending power.

Key Growth Drivers:

- Strong Automotive Industry: Germany and the UK boast established automotive manufacturing bases, leading to high demand for infotainment systems.

- High Consumer Spending: The relatively high disposable income in these markets fuels demand for premium features in vehicles, including advanced infotainment systems.

- Government Support for Automotive Innovation: Certain countries have initiated governmental policies to promote the development and adoption of advanced automotive technologies.

- Well Developed Infrastructure: A strong infrastructure enables faster deployment and utilization of connected infotainment services.

Market Segmentation:

- Vehicle Type: The passenger car segment accounts for the majority of the market share, driven by the high demand for infotainment features in personal vehicles. Commercial vehicle segment shows a steady growth, albeit at a slower pace.

- Installation Type: The in-dash infotainment segment holds the largest market share but the rear seat infotainment is showing robust growth due to increasing passenger comfort demand.

- Country-wise Analysis: This report will provide a detailed analysis of each country including specific market trends, growth drivers, and challenges.

Europe Automotive Infotainment Systems Industry Product Analysis

The European automotive infotainment market showcases a diverse range of products, from basic audio systems to highly integrated and sophisticated systems incorporating advanced features like augmented reality, gesture control, and voice recognition. Innovations focus on improved user interfaces, enhanced connectivity, and greater integration with other vehicle systems. Key competitive advantages are derived from features that streamline driver experience, offer seamless connectivity, and incorporate the latest technological advancements, catering to diverse needs and budget requirements.

Key Drivers, Barriers & Challenges in Europe Automotive Infotainment Systems Industry

Key Drivers:

The market is propelled by factors such as the growing demand for connected car technologies, rising adoption of electric and autonomous vehicles (which necessitate sophisticated infotainment systems), and the introduction of novel features such as advanced driver-assistance systems and augmented reality overlays. Government regulations driving safety and security are also acting as key drivers.

Key Challenges and Restraints:

Supply chain disruptions, particularly related to semiconductor shortages, have hampered production and increased costs. Regulatory complexities around data privacy and cybersecurity present significant hurdles for manufacturers. Intense competition, price pressures and the rising cost of development also present hurdles. This is expected to impact the market by roughly xx Million over the forecast period.

Growth Drivers in the Europe Automotive Infotainment Systems Industry Market

Technological advancements, particularly in areas like AI, 5G connectivity, and augmented reality are major drivers. Rising consumer demand for enhanced in-car entertainment and connectivity features and an increasing focus on safety and driver assistance systems are also important drivers. Government regulations promoting vehicle electrification and automated driving are further boosting market growth.

Challenges Impacting Europe Automotive Infotainment Systems Industry Growth

Significant challenges include maintaining robust supply chains, dealing with the complexity of regulations governing data privacy and cybersecurity, and managing escalating development costs. Intense competition from both established and emerging players adds to the challenges faced by existing market players.

Key Players Shaping the Europe Automotive Infotainment Systems Industry Market

- Alpine Electronics Inc

- Denso Corporation

- Visteon Corporation

- Aisin Corporation

- Harman International

- Continental AG

- BorgWarner Inc

- JVCKENWOOD Corporation

- Robert Bosch GmbH

- Pioneer Corporation

- Panasonic Corporation

Significant Europe Automotive Infotainment Systems Industry Industry Milestones

- August 2022: Continental AG launched its innovative Switchable Privacy Display technology.

- February 2022: HARMAN announced Ready Together and Software Enabled Branded Audio innovations.

- January 2022: Robert Bosch GmbH developed a high-performance infotainment domain computing system.

Future Outlook for Europe Automotive Infotainment Systems Industry Market

The future of the European automotive infotainment systems market is exceptionally promising. Continued technological innovation, rising demand for connected car features, increasing vehicle production, and supportive government policies will ensure strong growth during the forecast period. Strategic partnerships, acquisitions, and a focus on developing cost-effective solutions while maintaining high quality will be critical for success in this dynamic and competitive market. The market is set for significant expansion, driven by the convergence of technology and consumer demands, offering substantial opportunities for players across the value chain.

Europe Automotive Infotainment Systems Industry Segmentation

-

1. Installation Type

- 1.1. In-Dash Infotainment

- 1.2. Rear Seat Infotainment

-

2. Vehicle Type

- 2.1. Passenger Cars

- 2.2. Commercial Vehicles

Europe Automotive Infotainment Systems Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Automotive Infotainment Systems Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 6.07% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Growing Demand For ADAS features in Vehicles

- 3.3. Market Restrains

- 3.3.1. High Up-Front Cost And Maintenance Cost

- 3.4. Market Trends

- 3.4.1. In-Dash Infotainment is Dominating the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Europe Automotive Infotainment Systems Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Installation Type

- 5.1.1. In-Dash Infotainment

- 5.1.2. Rear Seat Infotainment

- 5.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.2.1. Passenger Cars

- 5.2.2. Commercial Vehicles

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Installation Type

- 6. Germany Europe Automotive Infotainment Systems Industry Analysis, Insights and Forecast, 2019-2031

- 7. France Europe Automotive Infotainment Systems Industry Analysis, Insights and Forecast, 2019-2031

- 8. Italy Europe Automotive Infotainment Systems Industry Analysis, Insights and Forecast, 2019-2031

- 9. United Kingdom Europe Automotive Infotainment Systems Industry Analysis, Insights and Forecast, 2019-2031

- 10. Netherlands Europe Automotive Infotainment Systems Industry Analysis, Insights and Forecast, 2019-2031

- 11. Sweden Europe Automotive Infotainment Systems Industry Analysis, Insights and Forecast, 2019-2031

- 12. Rest of Europe Europe Automotive Infotainment Systems Industry Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 Alpine Electronics Inc

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 Denso Corporation

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 Visteon Corporatio

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 Aisin Corporation

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 Harman International

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 Continental AG

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 BorgWarner Inc

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 JVCKENWOOD Corporation

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.9 Robert Bosch GmbH

- 13.2.9.1. Overview

- 13.2.9.2. Products

- 13.2.9.3. SWOT Analysis

- 13.2.9.4. Recent Developments

- 13.2.9.5. Financials (Based on Availability)

- 13.2.10 Pioneer Corporation

- 13.2.10.1. Overview

- 13.2.10.2. Products

- 13.2.10.3. SWOT Analysis

- 13.2.10.4. Recent Developments

- 13.2.10.5. Financials (Based on Availability)

- 13.2.11 Panasonic Corporation

- 13.2.11.1. Overview

- 13.2.11.2. Products

- 13.2.11.3. SWOT Analysis

- 13.2.11.4. Recent Developments

- 13.2.11.5. Financials (Based on Availability)

- 13.2.1 Alpine Electronics Inc

List of Figures

- Figure 1: Europe Automotive Infotainment Systems Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Europe Automotive Infotainment Systems Industry Share (%) by Company 2024

List of Tables

- Table 1: Europe Automotive Infotainment Systems Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Europe Automotive Infotainment Systems Industry Revenue Million Forecast, by Installation Type 2019 & 2032

- Table 3: Europe Automotive Infotainment Systems Industry Revenue Million Forecast, by Vehicle Type 2019 & 2032

- Table 4: Europe Automotive Infotainment Systems Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Europe Automotive Infotainment Systems Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: Germany Europe Automotive Infotainment Systems Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: France Europe Automotive Infotainment Systems Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Italy Europe Automotive Infotainment Systems Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: United Kingdom Europe Automotive Infotainment Systems Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Netherlands Europe Automotive Infotainment Systems Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Sweden Europe Automotive Infotainment Systems Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Rest of Europe Europe Automotive Infotainment Systems Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Europe Automotive Infotainment Systems Industry Revenue Million Forecast, by Installation Type 2019 & 2032

- Table 14: Europe Automotive Infotainment Systems Industry Revenue Million Forecast, by Vehicle Type 2019 & 2032

- Table 15: Europe Automotive Infotainment Systems Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 16: United Kingdom Europe Automotive Infotainment Systems Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: Germany Europe Automotive Infotainment Systems Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: France Europe Automotive Infotainment Systems Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Italy Europe Automotive Infotainment Systems Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Spain Europe Automotive Infotainment Systems Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Netherlands Europe Automotive Infotainment Systems Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Belgium Europe Automotive Infotainment Systems Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Sweden Europe Automotive Infotainment Systems Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Norway Europe Automotive Infotainment Systems Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 25: Poland Europe Automotive Infotainment Systems Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Denmark Europe Automotive Infotainment Systems Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Automotive Infotainment Systems Industry?

The projected CAGR is approximately 6.07%.

2. Which companies are prominent players in the Europe Automotive Infotainment Systems Industry?

Key companies in the market include Alpine Electronics Inc, Denso Corporation, Visteon Corporatio, Aisin Corporation, Harman International, Continental AG, BorgWarner Inc, JVCKENWOOD Corporation, Robert Bosch GmbH, Pioneer Corporation, Panasonic Corporation.

3. What are the main segments of the Europe Automotive Infotainment Systems Industry?

The market segments include Installation Type, Vehicle Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Demand For ADAS features in Vehicles.

6. What are the notable trends driving market growth?

In-Dash Infotainment is Dominating the Market.

7. Are there any restraints impacting market growth?

High Up-Front Cost And Maintenance Cost.

8. Can you provide examples of recent developments in the market?

In August2022, Continental announced the creation of a innovative display that allows vehicle information to be dynamically displayed in either a private or public mode.The so-called Switchable Privacy Display, a new display technology, lets front passengers use the infotainment system or multimedia content like videos without distracting the driver from the road.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Automotive Infotainment Systems Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Automotive Infotainment Systems Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Automotive Infotainment Systems Industry?

To stay informed about further developments, trends, and reports in the Europe Automotive Infotainment Systems Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence