Key Insights

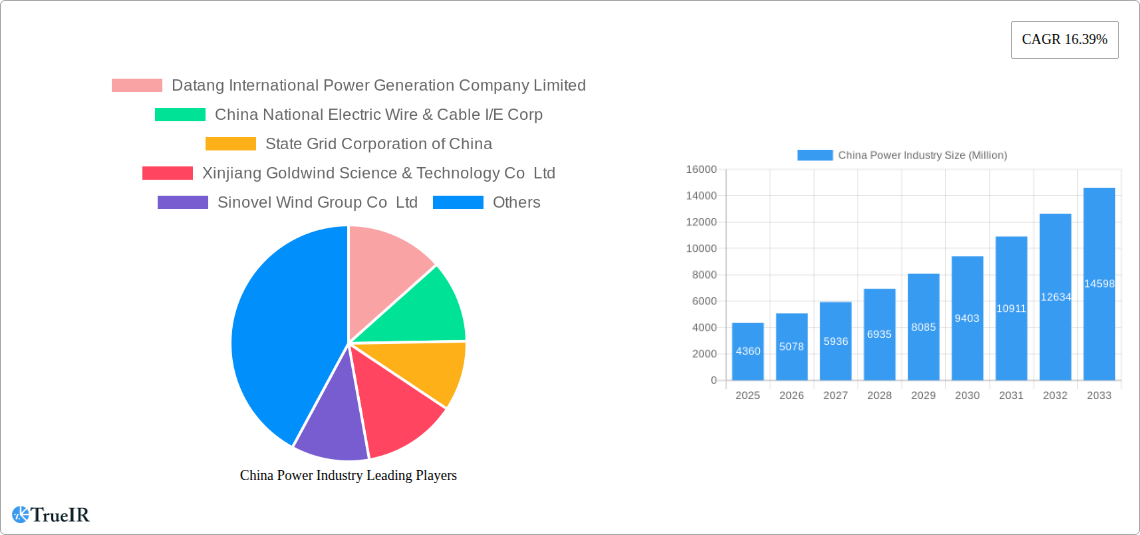

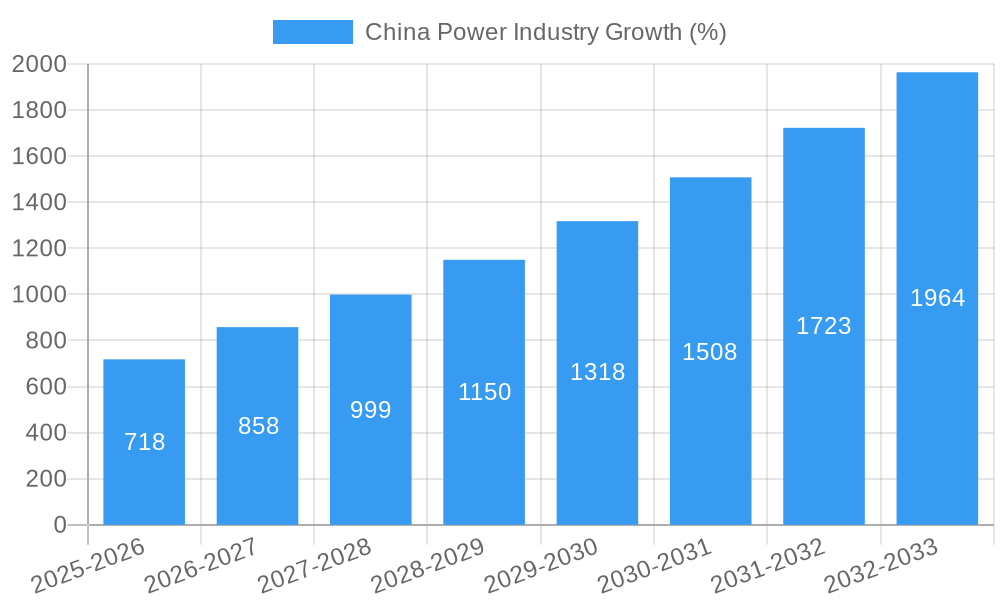

The China power industry, valued at $4.36 billion in 2025, is projected to experience robust growth, driven by increasing energy demand fueled by rapid economic expansion and urbanization. A compound annual growth rate (CAGR) of 16.39% is anticipated from 2025 to 2033, indicating a significant market expansion. Key growth drivers include the government's ambitious renewable energy targets, aimed at diversifying the energy mix and reducing reliance on thermal power. This transition is fostering significant investment in wind, solar, and hydroelectric projects, creating opportunities for companies like Xinjiang Goldwind Science & Technology Co Ltd and Sinovel Wind Group Co Ltd. Further expansion is anticipated from the modernization of existing infrastructure and the development of smart grids to enhance efficiency and reliability. However, challenges remain, including managing the integration of intermittent renewable energy sources into the grid and ensuring the sustainable development of hydroelectric projects. While the dominance of State-owned enterprises like Datang International Power Generation Company Limited and State Grid Corporation of China is evident, the market also presents opportunities for smaller players specializing in niche areas like renewable energy technology and grid management solutions.

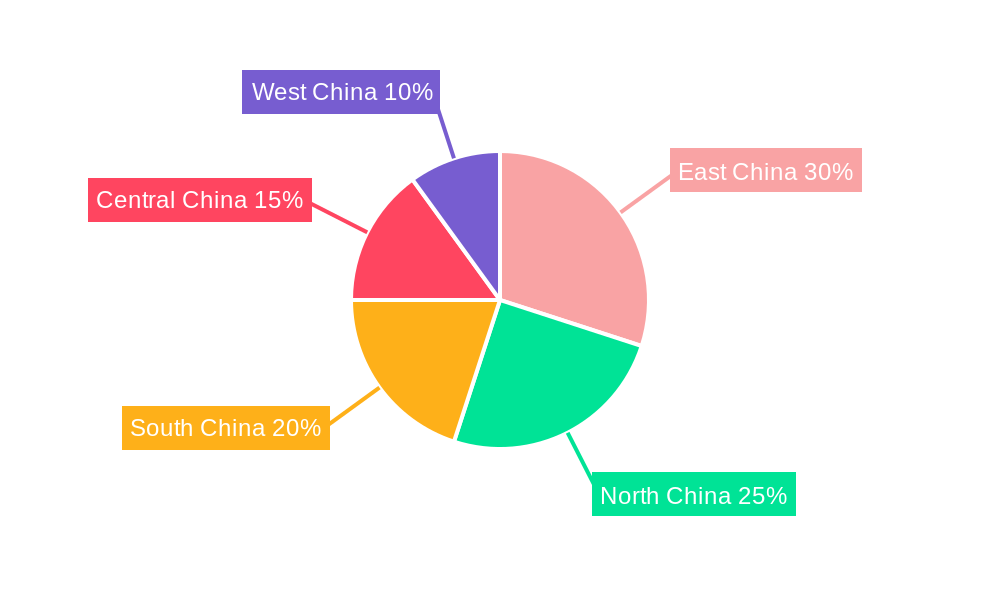

The industry's segmentation reveals a diverse landscape. While thermal power currently holds a significant share, the rapid increase in renewable energy capacity is expected to significantly alter this distribution over the forecast period. Hydroelectric power, despite its established presence, faces constraints related to environmental concerns and geographical limitations. Nuclear power's contribution remains relatively stable, balanced by ongoing safety and regulatory considerations. The "Other" category encompasses emerging technologies and distributed generation solutions, which are poised for growth alongside the overall expansion of the power sector. Regional variations within China are likely, with coastal regions potentially experiencing faster growth due to higher energy consumption. The forecast period will likely see continued consolidation within the industry, with larger players acquiring smaller companies to expand their market share and technological capabilities.

China Power Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the dynamic China power industry, offering invaluable insights for investors, industry professionals, and strategic decision-makers. With a focus on market trends, competitive landscapes, and future growth projections, this report covers the period from 2019 to 2033, with a base year of 2025 and a forecast period of 2025-2033. The report utilizes data from the historical period of 2019-2024 and projects key market indicators for the future. The total market size in 2025 is estimated at xx Million USD. The projected Compound Annual Growth Rate (CAGR) for the forecast period is xx%. This report covers key players like Datang International Power Generation Company Limited, China National Electric Wire & Cable I/E Corp, State Grid Corporation of China, Xinjiang Goldwind Science & Technology Co Ltd, Sinovel Wind Group Co Ltd, China National Electric Engineering Co Ltd, China Yangtze Power Co Ltd, Wuxi Suntech Power Co Ltd, Sinohydro Corporation, and Shandong Energy Group Co Ltd, among others.

China Power Industry Market Structure & Competitive Landscape

The Chinese power industry exhibits a complex interplay of state-owned enterprises (SOEs) and private players. Market concentration is high, with a few dominant SOEs controlling significant market share in various segments. Concentration ratios are estimated at xx% for power generation and xx% for transmission and distribution in 2025. Innovation is driven primarily by government policies promoting renewable energy and energy efficiency. Stringent environmental regulations are significantly impacting the industry, pushing for cleaner energy sources and phasing out coal-fired power plants. Product substitutes, primarily renewable energy sources, are gaining traction, driven by technological advancements and policy support. End-user segmentation is primarily divided into residential, commercial, and industrial sectors, with industrial consumers accounting for the largest share of electricity consumption. Mergers and acquisitions (M&A) activity is notable, with SOEs consolidating their position and private players seeking strategic partnerships to expand their reach. M&A volume in the power sector between 2019 and 2024 reached approximately xx Million USD, with a projected increase to xx Million USD by 2033.

China Power Industry Market Trends & Opportunities

The China power industry is undergoing a significant transformation, driven by increasing energy demand, government policies focused on energy security and environmental sustainability, and technological advancements in renewable energy. The market size is projected to grow from xx Million USD in 2025 to xx Million USD by 2033, representing a strong CAGR. Technological shifts towards renewable energy sources, such as solar and wind power, are prominent, with significant government investment and supportive policies accelerating their adoption. Consumer preferences are shifting towards cleaner and more sustainable energy solutions, contributing to the growth of renewable energy segments. Competitive dynamics are marked by intensified competition among both domestic and international players, particularly in the renewable energy sector. Market penetration rates for solar and wind power are projected to reach xx% and xx% respectively by 2033.

Dominant Markets & Segments in China Power Industry

- Thermal Power: Remains a significant segment due to established infrastructure and readily available resources. However, its dominance is declining due to environmental concerns and government policies promoting renewables.

- Hydroelectric Power: A major contributor to China's energy mix, driven by substantial hydropower resources, particularly in the southwest. Growth is constrained by environmental concerns and the limitations of geographical suitability.

- Nuclear Power: Experiencing steady growth, with ongoing investments in new nuclear power plants. Government support and advancements in nuclear technology are driving expansion.

- Renewable Power (Solar & Wind): Experiencing explosive growth, driven by strong government support, technological advancements, and decreasing costs. This segment is expected to become the dominant power generation source in the long term.

- Other Power Generation Sources: This segment includes biomass, geothermal, and other emerging technologies. It is anticipated to experience moderate growth, driven by niche applications and technological advancements.

The renewable energy segment is expected to experience the most significant growth, driven by government incentives, favorable policies, and technological breakthroughs, leading to substantial investments in solar and wind energy projects across various regions. Infrastructure development, including the expansion of transmission and distribution networks, is a major growth driver for all segments, enhancing accessibility and reliability of power supply. Strong government policies emphasizing energy security and environmental protection are fundamental to the growth of this industry.

China Power Industry Product Analysis

The Chinese power industry is witnessing significant innovation in power generation technologies, particularly in renewable energy. Advances in solar PV technology, wind turbine design, and energy storage solutions are enhancing efficiency and reducing costs. These improvements are leading to greater market penetration of renewable energy sources. The focus on smart grids and grid modernization is another key trend, improving the integration of renewable energy into the national grid and enhancing grid reliability. The market is increasingly demanding products with higher efficiency, lower emissions, and improved grid integration capabilities.

Key Drivers, Barriers & Challenges in China Power Industry

Key Drivers: Government policies promoting renewable energy, strong economic growth driving energy demand, and technological advancements in renewable energy technologies are key drivers. The ongoing expansion of the national power grid is also a major factor.

Challenges: Meeting the increasing energy demand while reducing carbon emissions poses a significant challenge. Supply chain disruptions and fluctuating commodity prices impact the cost of power generation. Integration of intermittent renewable energy sources into the grid remains a technical hurdle. Regulatory complexities and bureaucratic hurdles can delay project development and deployment.

Growth Drivers in the China Power Industry Market

Technological innovation in renewable energy, government support through subsidies and tax incentives, and increasing energy demand from industrial and residential sectors all contribute to market growth. The development of smart grids is also a major catalyst.

Challenges Impacting China Power Industry Growth

Regulatory complexities, particularly in obtaining environmental permits and land acquisition, hinder project development. Supply chain vulnerabilities and dependence on imported equipment pose risks. Competition from established players and the emergence of new entrants intensify market pressures.

Key Players Shaping the China Power Industry Market

- Datang International Power Generation Company Limited

- China National Electric Wire & Cable I/E Corp

- State Grid Corporation of China

- Xinjiang Goldwind Science & Technology Co Ltd

- Sinovel Wind Group Co Ltd

- China National Electric Engineering Co Ltd

- China Yangtze Power Co Ltd

- Wuxi Suntech Power Co Ltd

- Sinohydro Corporation

- Shandong Energy Group Co Ltd

Significant China Power Industry Industry Milestones

- February 2023: Commencement of the world's largest ultra-high-voltage energy transmission project, boosting grid connectivity and renewable energy integration.

- January 2023: China Three Gorges' announcement of a 16 GW solar, wind, and coal project, signaling a significant investment in diverse energy sources.

- March 2022: Shenzhen Energy Group's order for GE gas turbines for a new 2-GW natural gas-fired power plant, reflecting efforts towards cleaner energy sources and coal-fired power plant retirement.

Future Outlook for China Power Industry Market

The Chinese power industry is poised for continued growth, driven by ongoing investments in renewable energy, grid modernization, and energy efficiency initiatives. Strategic opportunities lie in developing smart grid technologies, exploring innovative energy storage solutions, and expanding renewable energy capacity. The market's long-term potential is substantial, fueled by the country's commitment to achieving its environmental goals and ensuring energy security.

China Power Industry Segmentation

-

1. Power Generation Source

- 1.1. Thermal

- 1.2. Hydroelectric

- 1.3. Nuclear

- 1.4. Renewable

- 1.5. Other Power Generation Sources

- 2. Power Transmission and Distribution (T&D)

China Power Industry Segmentation By Geography

- 1. China

China Power Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 16.39% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Upcoming Investments in Renewable Energy Sector4.; Growing Manufacturing Sector Increases Demand For Power

- 3.3. Market Restrains

- 3.3.1. Rising Phase Out of Coal-based Power Plants

- 3.4. Market Trends

- 3.4.1. The Renewable Energy Segment Expected to Dominate the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. China Power Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Power Generation Source

- 5.1.1. Thermal

- 5.1.2. Hydroelectric

- 5.1.3. Nuclear

- 5.1.4. Renewable

- 5.1.5. Other Power Generation Sources

- 5.2. Market Analysis, Insights and Forecast - by Power Transmission and Distribution (T&D)

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. China

- 5.1. Market Analysis, Insights and Forecast - by Power Generation Source

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 Datang International Power Generation Company Limited

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 China National Electric Wire & Cable I/E Corp

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 State Grid Corporation of China

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Xinjiang Goldwind Science & Technology Co Ltd

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Sinovel Wind Group Co Ltd

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 China National Electric Engineering Co Ltd

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 China Yangtze Power Co Ltd

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Wuxi Suntech Power Co Ltd

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Sinohydro Corporation

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Shandong energy group co Ltd *List Not Exhaustive

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 Datang International Power Generation Company Limited

List of Figures

- Figure 1: China Power Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: China Power Industry Share (%) by Company 2024

List of Tables

- Table 1: China Power Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: China Power Industry Revenue Million Forecast, by Power Generation Source 2019 & 2032

- Table 3: China Power Industry Revenue Million Forecast, by Power Transmission and Distribution (T&D) 2019 & 2032

- Table 4: China Power Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: China Power Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: China Power Industry Revenue Million Forecast, by Power Generation Source 2019 & 2032

- Table 7: China Power Industry Revenue Million Forecast, by Power Transmission and Distribution (T&D) 2019 & 2032

- Table 8: China Power Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Power Industry?

The projected CAGR is approximately 16.39%.

2. Which companies are prominent players in the China Power Industry?

Key companies in the market include Datang International Power Generation Company Limited, China National Electric Wire & Cable I/E Corp, State Grid Corporation of China, Xinjiang Goldwind Science & Technology Co Ltd, Sinovel Wind Group Co Ltd, China National Electric Engineering Co Ltd, China Yangtze Power Co Ltd, Wuxi Suntech Power Co Ltd, Sinohydro Corporation, Shandong energy group co Ltd *List Not Exhaustive.

3. What are the main segments of the China Power Industry?

The market segments include Power Generation Source, Power Transmission and Distribution (T&D).

4. Can you provide details about the market size?

The market size is estimated to be USD 4.36 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Upcoming Investments in Renewable Energy Sector4.; Growing Manufacturing Sector Increases Demand For Power.

6. What are the notable trends driving market growth?

The Renewable Energy Segment Expected to Dominate the Market.

7. Are there any restraints impacting market growth?

Rising Phase Out of Coal-based Power Plants.

8. Can you provide examples of recent developments in the market?

February 2023: China announced that it had started work on the world's biggest ultrahigh-voltage energy transmission project, which will connect Southwest China's Sichuan Province and the Xizang Autonomous Region to Central China's Hubei Province. The transmission project will carry around 40 billion KW hours of electricity, including hydroelectricity from the Jinsha River's upper stream, comparable to one-sixth of Hubei Province's annual power demand.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Power Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Power Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Power Industry?

To stay informed about further developments, trends, and reports in the China Power Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence