Key Insights

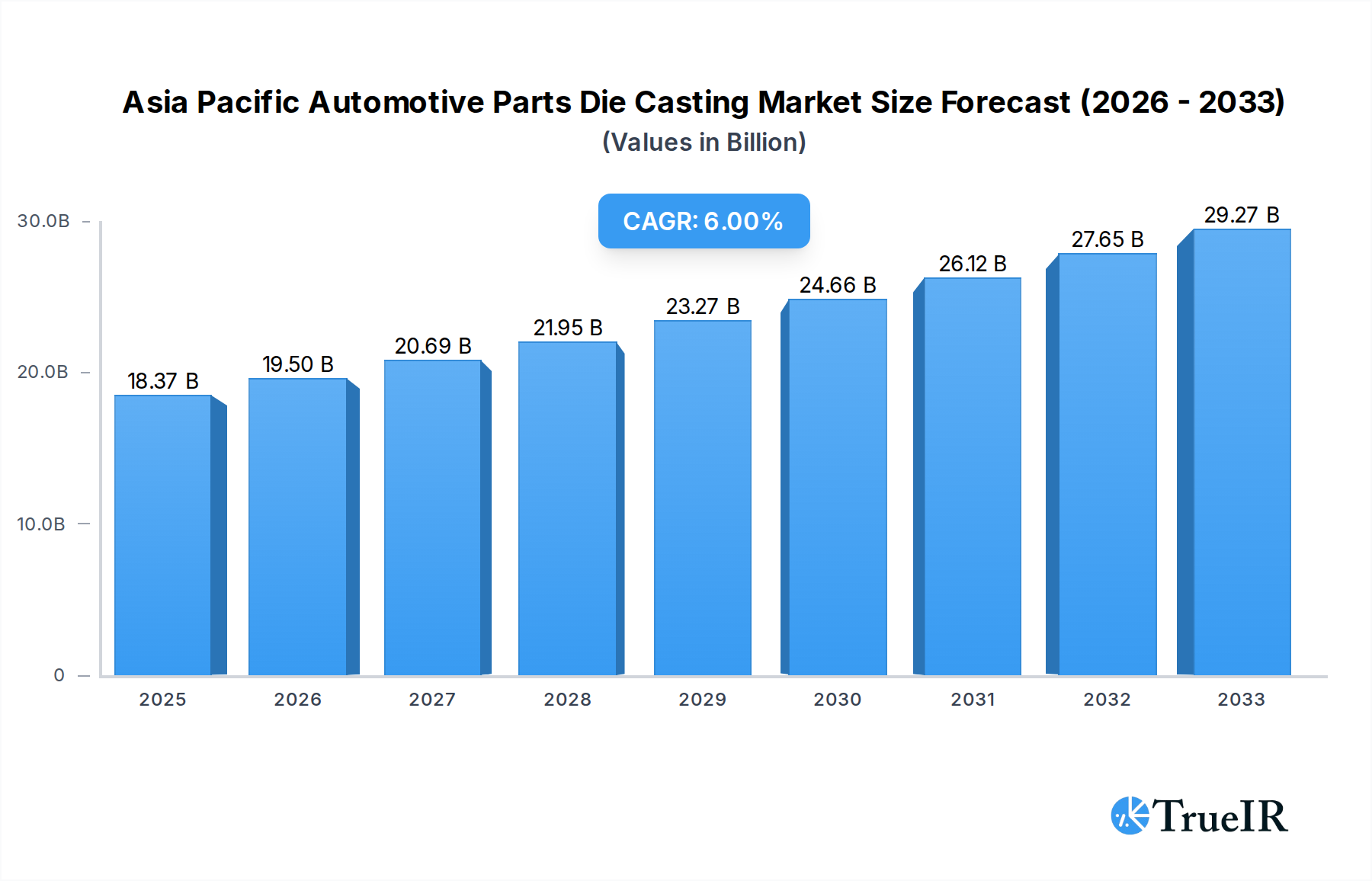

The Asia Pacific automotive parts die casting market is poised for robust growth, driven by escalating vehicle production and the increasing demand for lightweight, high-strength components. The market is projected to reach an estimated USD 18.37 billion in 2025, exhibiting a compound annual growth rate (CAGR) of 6% during the forecast period of 2025-2033. This expansion is significantly influenced by the widespread adoption of advanced die casting techniques like vacuum die casting and semi-solid die casting, which enhance component performance and reduce manufacturing complexities. Furthermore, the growing preference for aluminum, zinc, and magnesium alloys in automotive manufacturing, owing to their superior strength-to-weight ratios and recyclability, is a key enabler for market expansion. Major applications, including body assembly, engine parts, and transmission parts, are witnessing substantial investments in die-cast components to improve fuel efficiency and vehicle dynamics.

Asia Pacific Automotive Parts Die Casting Market Market Size (In Billion)

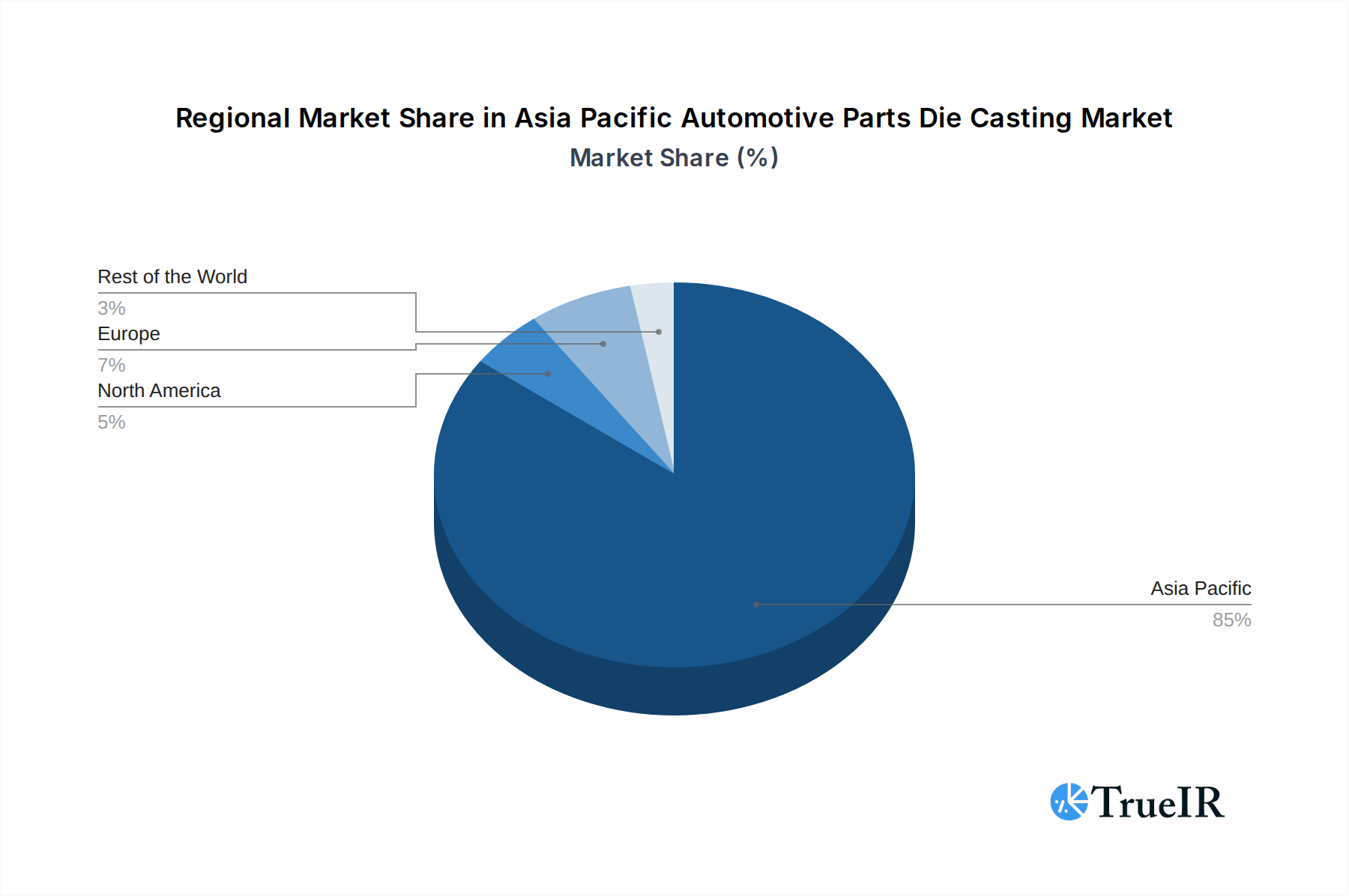

The market's dynamism is further characterized by significant regional contributions, with China, India, Japan, and South Korea leading the charge in both production and consumption. These nations are at the forefront of automotive innovation, adopting cutting-edge die casting technologies and catering to the evolving needs of global automakers. While the market benefits from strong demand drivers, it also faces certain restraints. The fluctuating raw material prices and the capital-intensive nature of advanced die casting machinery can pose challenges to smaller manufacturers. Nevertheless, the continuous innovation in production processes, coupled with the increasing focus on sustainable manufacturing practices and the expansion of electric vehicle (EV) production, are expected to propel the Asia Pacific automotive parts die casting market to new heights. Key players like SYX Die Casting, GIBBS DIE CASTING GROUP, and Endurance Technologies Ltd are strategically expanding their capacities and product portfolios to capture a larger market share.

Asia Pacific Automotive Parts Die Casting Market Company Market Share

The Asia Pacific automotive parts die casting market is poised for significant expansion, driven by increasing vehicle production, the growing demand for lightweight components, and advancements in die casting technologies. This report provides an in-depth analysis of the market's structure, trends, key players, and future outlook, offering valuable insights for stakeholders navigating this dynamic industry. The study period spans from 2019 to 2033, with a base year of 2025 and a forecast period extending from 2025 to 2033.

Asia Pacific Automotive Parts Die Casting Market Market Structure & Competitive Landscape

The Asia Pacific automotive parts die casting market exhibits a moderately concentrated structure, characterized by the presence of both large multinational corporations and regional specialized manufacturers. Key players like SYX Die Casting, GIBBS DIE CASTING GROUP, and ALUMINIUM DIE CASTING (CHINA) LTD are significant contributors, holding substantial market share through their extensive manufacturing capabilities and established supply chains. Innovation drivers are primarily centered on developing high-pressure die casting techniques for complex and integrated components, the utilization of advanced alloys (such as high-strength aluminum and magnesium alloys) for weight reduction, and the adoption of Industry 4.0 principles for enhanced automation and process efficiency. Regulatory impacts, particularly concerning environmental standards and emissions, are increasingly influencing material choices and production processes, favoring more sustainable die casting methods and recycled materials. Product substitutes, though limited in the core die casting segment, can emerge from alternative manufacturing processes like stamping or forging for certain component types, albeit often with trade-offs in complexity and integration. End-user segmentation is heavily influenced by the automotive industry's shift towards electric vehicles (EVs) and advanced driver-assistance systems (ADAS), requiring specialized die-cast parts for battery enclosures, motor housings, and sensor components. Mergers and acquisitions (M&A) trends are evident, with larger entities acquiring smaller, specialized firms to broaden their technological portfolios, expand geographical reach, and consolidate market positions. For instance, the acquisition of smaller die casting units by larger automotive component manufacturers aims to achieve vertical integration and secure a more stable supply of critical parts. The market concentration ratio for the top five players is estimated to be around 45% in 2025, with continuous efforts to enhance this through strategic alliances and capacity expansions.

Asia Pacific Automotive Parts Die Casting Market Market Trends & Opportunities

The Asia Pacific automotive parts die casting market is experiencing robust growth, projected to reach a valuation exceeding $30 billion by 2033. This expansion is fueled by a confluence of technological advancements, evolving consumer preferences, and dynamic competitive forces. A significant trend is the escalating demand for lightweight automotive components, driven by the global imperative to improve fuel efficiency and reduce emissions. Die casting, particularly using aluminum and magnesium alloys, offers an optimal solution for producing intricate, yet lightweight, parts for both internal combustion engine (ICE) vehicles and the rapidly growing electric vehicle (EV) segment. The surge in EV production in countries like China and South Korea is creating substantial opportunities for die casters specializing in components such as battery housings, electric motor casings, and structural elements. The market is also witnessing a shift towards more sophisticated die casting processes, including vacuum die casting and semi-solid die casting, which enable the production of parts with enhanced mechanical properties, reduced porosity, and improved surface finish, thereby catering to the stringent quality requirements of modern automotive applications. The adoption of automation and Industry 4.0 technologies is another key trend, with manufacturers investing in smart factories to optimize production cycles, reduce waste, and improve overall operational efficiency. This includes the implementation of advanced simulation software for mold design, robotic automation for material handling, and real-time data analytics for process monitoring and control. Consumer preferences are increasingly leaning towards vehicles with advanced safety features and higher performance, both of which necessitate precision-engineered, lightweight components that die casting excels at producing. The competitive landscape is characterized by intense rivalry, pushing companies to focus on cost optimization, technological innovation, and strategic partnerships. Opportunities lie in catering to the burgeoning aftermarket segment, which requires reliable and cost-effective replacement parts, and in developing specialized die-cast solutions for emerging mobility solutions such as autonomous vehicles and advanced drones. The compound annual growth rate (CAGR) for the Asia Pacific automotive parts die casting market is estimated to be approximately 6.2% during the forecast period. Market penetration rates for advanced die casting applications, especially in EVs, are expected to rise from around 35% in 2025 to over 55% by 2033.

Dominant Markets & Segments in Asia Pacific Automotive Parts Die Casting Market

China stands as the undisputed dominant market within the Asia Pacific automotive parts die casting landscape, contributing over 50% of the total market revenue. Its dominance is propelled by its unparalleled position as the world's largest automotive manufacturing hub, supported by a robust domestic demand for vehicles and substantial foreign direct investment. Government initiatives promoting the automotive sector, coupled with a well-established supply chain for raw materials and manufacturing expertise, further solidify China's leadership.

Production Process Type:

- Pressure Die Casting: This process holds the lion's share, accounting for approximately 85% of the market. Its widespread adoption is due to its efficiency, high production rates, and ability to produce complex shapes with excellent surface finish, making it ideal for mass-produced automotive components. Key growth drivers include its cost-effectiveness for high-volume applications and its suitability for producing parts like engine blocks, transmission housings, and body panels.

- Vacuum Die Casting: While currently holding a smaller market share (around 8%), this process is experiencing rapid growth. Its ability to reduce porosity and improve the mechanical properties of cast parts makes it increasingly vital for critical engine components and structural parts in advanced vehicles, especially EVs.

- Squeeze Die Casting: Representing about 5% of the market, squeeze die casting offers improved mechanical properties and dimensional accuracy, making it suitable for high-performance components.

- Semi-Solid Die Casting: This niche segment (around 2%) is gaining traction for producing parts requiring exceptional ductility and impact resistance, such as suspension components.

Raw Material:

- Aluminum: Dominates the raw material segment, accounting for over 70% of the market. Its lightweight nature, excellent strength-to-weight ratio, and recyclability make it the preferred choice for a vast array of automotive parts, from engine components to body structures.

- Zinc: Holds a significant share (around 20%), primarily used for smaller, intricate parts like door handles, locks, and connectors, due to its excellent fluidity and lower melting point.

- Magnesium: Though a smaller segment (around 7%), magnesium is witnessing considerable growth due to its even lighter weight than aluminum, making it increasingly attractive for powertrain components and structural parts in premium and electric vehicles.

- Others: Includes alloys like copper, accounting for a negligible percentage.

Application Type:

- Engine Parts: This remains a core application, comprising roughly 35% of the market. Die-cast components like engine blocks, cylinder heads, and oil pans are essential for vehicle performance and efficiency.

- Transmission Parts: Constituting about 30% of the market, transmission housings and other related components benefit from the precision and structural integrity offered by die casting.

- Body Assembly: This segment is experiencing rapid growth (approximately 25%), driven by the demand for lightweight structural components, chassis parts, and closures like hoods and doors, particularly in advanced vehicle architectures.

- Others: This includes components for interiors, chassis, and electrical systems, accounting for the remaining 10%.

Countries:

- China: As mentioned, China is the dominant country market.

- India: Exhibiting strong growth (around 15% market share), driven by its expanding automotive industry and increasing localization of manufacturing.

- Japan: A mature market (around 10% market share) known for its technological sophistication and high-quality production, particularly in advanced automotive applications and EVs.

- South Korea: A significant player (around 8% market share), especially in the EV segment, with major players like Hyundai and Kia driving demand for advanced die-cast components.

- Rest of Asia-Pacific: Includes countries like Thailand, Indonesia, and Malaysia, collectively holding about 12% of the market, with growing automotive production capabilities.

Asia Pacific Automotive Parts Die Casting Market Product Analysis

The Asia Pacific automotive parts die casting market is characterized by continuous product innovation focused on enhancing performance, reducing weight, and improving manufacturing efficiency. Aluminum alloy die castings, particularly high-strength variants, are increasingly prevalent for engine blocks and structural components, offering superior strength-to-weight ratios. Magnesium alloy die castings are emerging as a key area of growth for critical powertrain and chassis parts in electric vehicles, capitalizing on their extreme lightweight properties. Innovations in vacuum die casting and semi-solid die casting are enabling the production of parts with reduced porosity and improved mechanical integrity, crucial for high-stress applications like transmission housings and suspension components. The integration of advanced computational fluid dynamics (CFD) and finite element analysis (FEA) in mold design optimizes casting quality and reduces development cycles, providing a competitive advantage for manufacturers.

Key Drivers, Barriers & Challenges in Asia Pacific Automotive Parts Die Casting Market

Key Drivers: The Asia Pacific automotive parts die casting market is primarily propelled by the relentless growth of the automotive industry, particularly in emerging economies like China and India. The escalating demand for electric vehicles (EVs) is a significant catalyst, necessitating lightweight and complex components such as battery enclosures and motor housings, for which die casting is ideally suited. Furthermore, stringent global regulations aimed at reducing vehicular emissions are driving the adoption of lighter materials, making aluminum and magnesium die castings indispensable for improving fuel efficiency. Technological advancements in die casting processes, including the adoption of Industry 4.0 principles for automation and precision, enhance production efficiency and product quality, thereby boosting market competitiveness.

Barriers & Challenges: Despite the positive growth trajectory, the market faces several challenges. Fluctuations in raw material prices, especially for aluminum and magnesium, can significantly impact manufacturing costs and profit margins. The increasingly complex regulatory landscape concerning environmental compliance and waste management adds to operational overheads. Intense competition among a large number of players, both domestic and international, exerts downward pressure on pricing, challenging profitability. Moreover, the high initial capital investment required for advanced die casting machinery and automation systems can be a barrier for smaller players seeking to upgrade their capabilities. Supply chain disruptions, as witnessed in recent global events, can also lead to production delays and increased costs.

Growth Drivers in the Asia Pacific Automotive Parts Die Casting Market Market

The Asia Pacific automotive parts die casting market is experiencing accelerated growth, driven by several key factors. The burgeoning demand for electric vehicles (EVs) in the region, particularly in China, is a primary growth engine, creating substantial opportunities for die-cast components like battery enclosures, motor casings, and structural parts. The ongoing global push for improved fuel efficiency and reduced emissions is intensifying the need for lightweight automotive components, making aluminum and magnesium die castings highly sought after for various vehicle applications. Technological advancements in die casting processes, including vacuum and semi-solid die casting, are enabling the production of higher-performance, more complex parts with superior mechanical properties. The rapid expansion of the automotive manufacturing sector in countries like India and Southeast Asian nations, coupled with government support for localized production, further fuels market expansion.

Challenges Impacting Asia Pacific Automotive Parts Die Casting Market Growth

The Asia Pacific automotive parts die casting market faces several critical challenges that could impede its growth. Volatility in the prices of key raw materials like aluminum and magnesium presents a significant economic risk, impacting cost predictability and profitability for manufacturers. Increasingly stringent environmental regulations concerning waste disposal, energy consumption, and emissions necessitate costly upgrades to production facilities and processes. The highly competitive nature of the market, characterized by numerous players, can lead to price wars and reduced profit margins, especially for less differentiated products. Furthermore, global supply chain disruptions, ranging from raw material shortages to logistics bottlenecks, can lead to production delays and increased operational costs. The need for continuous technological investment to remain competitive, particularly in advanced die casting techniques and automation, also poses a financial challenge.

Key Players Shaping the Asia Pacific Automotive Parts Die Casting Market Market

- SYX Die Casting

- GIBBS DIE CASTING GROUP

- CASTWEL AUTOPARTS PVT LTD

- Sunbeam Auto Pvt Ltd

- Sandar Technologies

- Amtek Group

- ECO Die Castings

- Endurance Technologies Ltd

- ALUMINIUM DIE CASTING (CHINA) LTD

- Dynacast Inc

Significant Asia Pacific Automotive Parts Die Casting Market Industry Milestones

- 2019: Introduction of advanced aluminum alloys for improved crashworthiness in automotive body structures.

- 2020: Increased adoption of Industry 4.0 technologies, including AI-driven quality control, in die casting facilities.

- 2021: Growing trend of lightweight magnesium alloy die castings for electric vehicle powertrains.

- 2022: Expansion of vacuum die casting capabilities to meet demand for high-integrity engine components.

- 2023: Strategic partnerships formed between die casters and EV manufacturers for component development and supply.

- 2024: Rise in M&A activities as larger players acquire specialized die casting firms to broaden their product portfolios and market reach.

Future Outlook for Asia Pacific Automotive Parts Die Casting Market Market

The future outlook for the Asia Pacific automotive parts die casting market is exceptionally promising, driven by continued innovation and the evolving automotive landscape. The accelerating transition towards electric vehicles will be a paramount growth catalyst, spurring demand for specialized, lightweight components. Advancements in die casting technology, including the wider adoption of semi-solid and advanced pressure die casting techniques, will enable the production of more complex and high-performance parts. The increasing focus on sustainability will further drive the use of recycled aluminum and the development of eco-friendly casting processes. Opportunities will also emerge from the integration of die-cast components into autonomous driving systems and other advanced mobility solutions. Manufacturers focusing on technological prowess, cost-efficiency, and strategic collaborations with automotive OEMs are well-positioned to capitalize on the substantial growth potential of this market.

Asia Pacific Automotive Parts Die Casting Market Segmentation

-

1. Production Process Type

- 1.1. Pressure Die Casting

- 1.2. Vacuum Die Casting

- 1.3. Squeeze Die Casting

- 1.4. Semi-Solid Die Casting

-

2. Raw Material

- 2.1. Aluminum

- 2.2. Zinc

- 2.3. Magnesium

- 2.4. Others

-

3. Application Type

- 3.1. Body Assembly

- 3.2. Engine Parts

- 3.3. Transmission Parts

- 3.4. Others

-

4. Countries

- 4.1. China

- 4.2. India

- 4.3. Japan

- 4.4. South Korea

- 4.5. Rest of Asia-Pacific

Asia Pacific Automotive Parts Die Casting Market Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. Japan

- 1.3. South Korea

- 1.4. India

- 1.5. Australia

- 1.6. New Zealand

- 1.7. Indonesia

- 1.8. Malaysia

- 1.9. Singapore

- 1.10. Thailand

- 1.11. Vietnam

- 1.12. Philippines

Asia Pacific Automotive Parts Die Casting Market Regional Market Share

Geographic Coverage of Asia Pacific Automotive Parts Die Casting Market

Asia Pacific Automotive Parts Die Casting Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Production Process Type

- 5.1.1. Pressure Die Casting

- 5.1.2. Vacuum Die Casting

- 5.1.3. Squeeze Die Casting

- 5.1.4. Semi-Solid Die Casting

- 5.2. Market Analysis, Insights and Forecast - by Raw Material

- 5.2.1. Aluminum

- 5.2.2. Zinc

- 5.2.3. Magnesium

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Application Type

- 5.3.1. Body Assembly

- 5.3.2. Engine Parts

- 5.3.3. Transmission Parts

- 5.3.4. Others

- 5.4. Market Analysis, Insights and Forecast - by Countries

- 5.4.1. China

- 5.4.2. India

- 5.4.3. Japan

- 5.4.4. South Korea

- 5.4.5. Rest of Asia-Pacific

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Production Process Type

- 6. Asia Pacific Automotive Parts Die Casting Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Production Process Type

- 6.1.1. Pressure Die Casting

- 6.1.2. Vacuum Die Casting

- 6.1.3. Squeeze Die Casting

- 6.1.4. Semi-Solid Die Casting

- 6.2. Market Analysis, Insights and Forecast - by Raw Material

- 6.2.1. Aluminum

- 6.2.2. Zinc

- 6.2.3. Magnesium

- 6.2.4. Others

- 6.3. Market Analysis, Insights and Forecast - by Application Type

- 6.3.1. Body Assembly

- 6.3.2. Engine Parts

- 6.3.3. Transmission Parts

- 6.3.4. Others

- 6.4. Market Analysis, Insights and Forecast - by Countries

- 6.4.1. China

- 6.4.2. India

- 6.4.3. Japan

- 6.4.4. South Korea

- 6.4.5. Rest of Asia-Pacific

- 6.1. Market Analysis, Insights and Forecast - by Production Process Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 SYX Die Casting

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 GIBBS DIE CASTING GROUP

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 CASTWEL AUTOPARTS PVT LTD

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Sunbeam Auto Pvt Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Sandar Technologies

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Amtek Group

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 ECO Die Castings

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Endurance Technologies Ltd

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 ALUMINIUM DIE CASTING (CHINA) LTD

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Dynacast Inc

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 SYX Die Casting

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Asia Pacific Automotive Parts Die Casting Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Asia Pacific Automotive Parts Die Casting Market Share (%) by Company 2025

List of Tables

- Table 1: Asia Pacific Automotive Parts Die Casting Market Revenue billion Forecast, by Production Process Type 2020 & 2033

- Table 2: Asia Pacific Automotive Parts Die Casting Market Revenue billion Forecast, by Raw Material 2020 & 2033

- Table 3: Asia Pacific Automotive Parts Die Casting Market Revenue billion Forecast, by Application Type 2020 & 2033

- Table 4: Asia Pacific Automotive Parts Die Casting Market Revenue billion Forecast, by Countries 2020 & 2033

- Table 5: Asia Pacific Automotive Parts Die Casting Market Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Asia Pacific Automotive Parts Die Casting Market Revenue billion Forecast, by Production Process Type 2020 & 2033

- Table 7: Asia Pacific Automotive Parts Die Casting Market Revenue billion Forecast, by Raw Material 2020 & 2033

- Table 8: Asia Pacific Automotive Parts Die Casting Market Revenue billion Forecast, by Application Type 2020 & 2033

- Table 9: Asia Pacific Automotive Parts Die Casting Market Revenue billion Forecast, by Countries 2020 & 2033

- Table 10: Asia Pacific Automotive Parts Die Casting Market Revenue billion Forecast, by Country 2020 & 2033

- Table 11: China Asia Pacific Automotive Parts Die Casting Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Japan Asia Pacific Automotive Parts Die Casting Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: South Korea Asia Pacific Automotive Parts Die Casting Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: India Asia Pacific Automotive Parts Die Casting Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Australia Asia Pacific Automotive Parts Die Casting Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: New Zealand Asia Pacific Automotive Parts Die Casting Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Indonesia Asia Pacific Automotive Parts Die Casting Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Malaysia Asia Pacific Automotive Parts Die Casting Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Singapore Asia Pacific Automotive Parts Die Casting Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Thailand Asia Pacific Automotive Parts Die Casting Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Vietnam Asia Pacific Automotive Parts Die Casting Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Philippines Asia Pacific Automotive Parts Die Casting Market Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Asia Pacific Automotive Parts Die Casting Market?

The projected CAGR is approximately 6%.

2. Which companies are prominent players in the Asia Pacific Automotive Parts Die Casting Market?

Key companies in the market include SYX Die Casting, GIBBS DIE CASTING GROUP, CASTWEL AUTOPARTS PVT LTD, Sunbeam Auto Pvt Ltd, Sandar Technologies, Amtek Group, ECO Die Castings, Endurance Technologies Ltd, ALUMINIUM DIE CASTING (CHINA) LTD, Dynacast Inc.

3. What are the main segments of the Asia Pacific Automotive Parts Die Casting Market?

The market segments include Production Process Type, Raw Material, Application Type, Countries.

4. Can you provide details about the market size?

The market size is estimated to be USD 18.37 billion as of 2022.

5. What are some drivers contributing to market growth?

Growth of the Automotive Industry to Drive Demand in the Die Casting Market; Growing Focus Toward Fuel Efficiency of IC Engine Vehicle to Drive Demand.

6. What are the notable trends driving market growth?

Aluminium is Expected to Grow With Highest CAGR.

7. Are there any restraints impacting market growth?

High Processing Cost May Hamper Market Expansion.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Asia Pacific Automotive Parts Die Casting Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Asia Pacific Automotive Parts Die Casting Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Asia Pacific Automotive Parts Die Casting Market?

To stay informed about further developments, trends, and reports in the Asia Pacific Automotive Parts Die Casting Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence