Key Insights

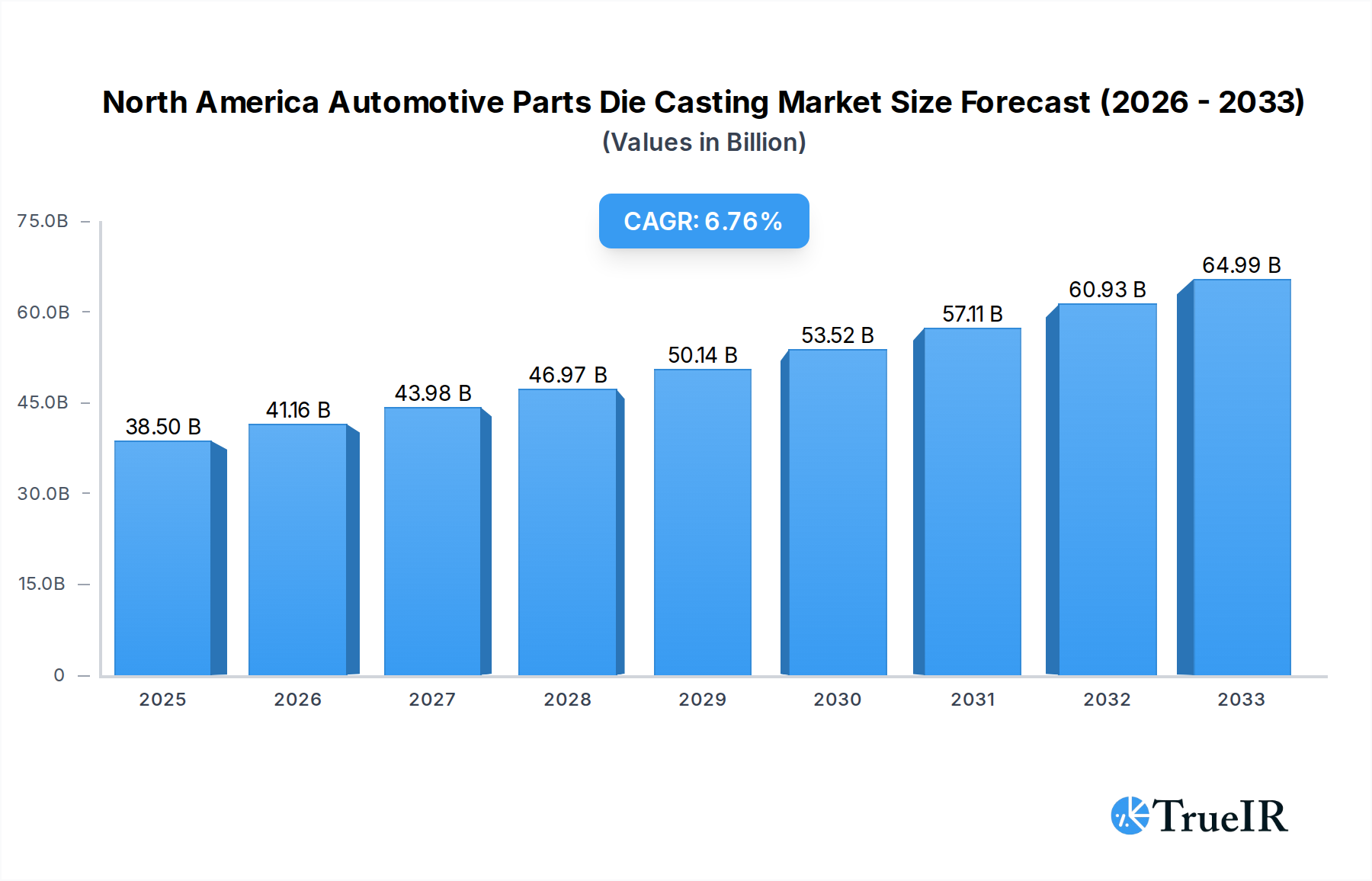

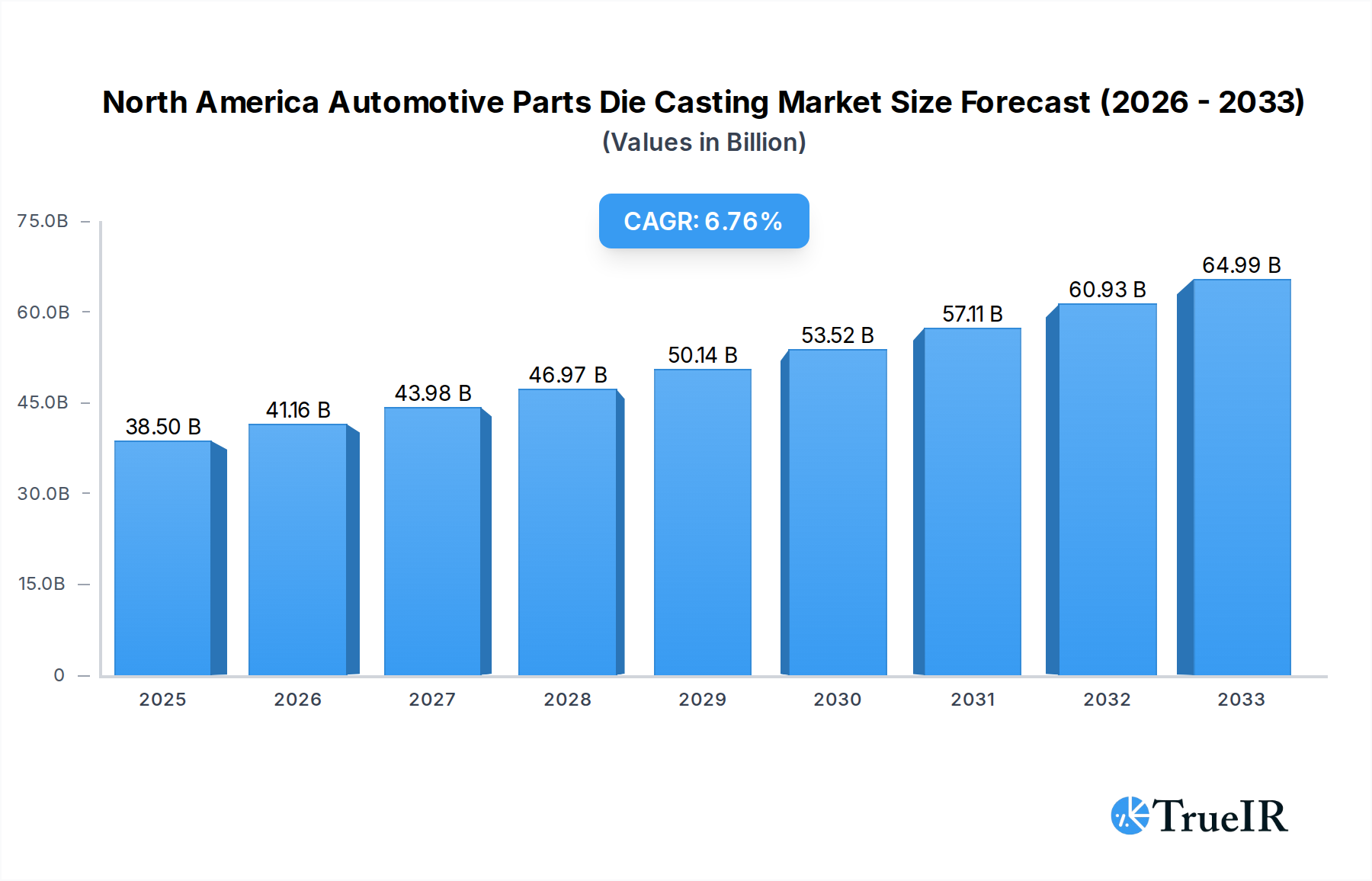

The North America automotive parts die casting market is poised for robust expansion, with an estimated market size of $38.5 billion in 2025, driven by increasing vehicle production and the growing demand for lightweight, complex automotive components. The market is projected to grow at a CAGR of 6.8% from 2025 to 2033. Key growth drivers include the shift towards electric vehicles (EVs), which necessitate specialized die-cast components for battery enclosures, electric motors, and power electronics, and the continuous need for enhanced fuel efficiency in internal combustion engine (ICE) vehicles, spurring the adoption of lighter materials like aluminum and magnesium. Advancements in die casting technologies, such as vacuum die casting and semi-solid die casting, are enabling the production of higher-performance parts with improved mechanical properties and reduced manufacturing defects, further bolstering market growth. The increasing complexity and integration of automotive systems also create opportunities for sophisticated die-cast parts in areas like engine blocks, transmission housings, and structural body components.

North America Automotive Parts Die Casting Market Market Size (In Billion)

The market's trajectory is further influenced by evolving trends in automotive manufacturing, including the adoption of Industry 4.0 principles for greater automation and efficiency in die casting operations, and a focus on sustainable manufacturing practices. While the demand for high-quality, precision-engineered automotive parts remains strong, certain restraints could impact the market's pace. Fluctuations in raw material prices, particularly for aluminum and magnesium, can affect production costs. Furthermore, stringent environmental regulations and the need for significant capital investment in advanced die casting facilities present challenges. However, the dominant application segments, including engine parts and transmission components, alongside the growing significance of body parts for lightweighting and safety, indicate a dynamic and evolving market. North America's commitment to automotive innovation and its established manufacturing base position it as a critical region for die casting advancements.

North America Automotive Parts Die Casting Market Company Market Share

Here's a comprehensive and SEO-optimized report description for the North America Automotive Parts Die Casting Market, designed for immediate use and maximum impact.

This in-depth market research report provides a thorough analysis of the North America Automotive Parts Die Casting Market, a critical sector driving innovation and efficiency in the automotive industry. Valued at an estimated $XX billion in the base year of 2025, the market is poised for significant expansion, projected to reach $XX billion by 2033, exhibiting a robust Compound Annual Growth Rate (CAGR) of XX% during the forecast period of 2025–2033. This report offers unparalleled insights into market dynamics, segmentation, competitive strategies, and future trends, making it an indispensable resource for stakeholders seeking to capitalize on emerging opportunities in this dynamic landscape.

The study meticulously covers the historical period from 2019 to 2024, providing a solid foundation for understanding past market performance and identifying key evolutionary trends. With a focus on high-volume keywords such as "automotive die casting," "North America auto parts," "aluminum die casting automotive," "zinc die casting automotive," "magnesium die casting automotive," "engine parts die casting," "transmission components die casting," and "automotive body parts die casting," this report is optimized for search engine visibility and designed to attract a wide range of industry professionals, including manufacturers, suppliers, investors, and automotive OEMs.

North America Automotive Parts Die Casting Market Market Structure & Competitive Landscape

The North America Automotive Parts Die Casting Market is characterized by a moderately concentrated structure, with key players vying for market share through continuous innovation and strategic partnerships. Several factors influence this landscape, including stringent regulatory frameworks, the persistent threat of product substitutes like advanced plastics and composite materials, and evolving end-user preferences driven by demand for lighter, more fuel-efficient vehicles. Mergers and acquisitions (M&A) have played a significant role in market consolidation, with an estimated XX M&A deals recorded during the historical period, further shaping the competitive arena. Innovation drivers are primarily centered around enhancing casting precision, improving material properties for increased durability and weight reduction, and optimizing production processes for cost-effectiveness and sustainability. Understanding the intricate interplay of these elements is crucial for navigating the competitive currents and identifying strategic advantages within the automotive die casting sector.

- Market Concentration: Moderate, with a few dominant players alongside a significant number of specialized manufacturers.

- Innovation Drivers: Lightweighting, improved mechanical properties, cost reduction, advanced automation, and sustainable manufacturing practices.

- Regulatory Impacts: Emission standards, safety regulations, and environmental mandates influence material choices and manufacturing processes.

- Product Substitutes: High-performance plastics, composite materials, and additive manufacturing present competitive alternatives.

- End-User Segmentation: Automotive OEMs are the primary end-users, with specific demands from passenger vehicles, commercial vehicles, and electric vehicles (EVs).

- M&A Trends: Strategic acquisitions aimed at expanding product portfolios, gaining technological expertise, and increasing market reach.

North America Automotive Parts Die Casting Market Market Trends & Opportunities

The North America Automotive Parts Die Casting Market is experiencing a transformative period, driven by the burgeoning demand for lightweight components, the electrification of vehicles, and advancements in casting technologies. The overall market size is projected to witness substantial growth, fueled by the automotive industry's ongoing efforts to enhance fuel efficiency and reduce emissions. Technological shifts are evident in the increasing adoption of advanced die casting techniques, such as vacuum die casting and semi-solid die casting, which offer superior surface finish, improved mechanical properties, and the ability to cast more complex geometries. Consumer preferences are increasingly leaning towards vehicles that are both performance-oriented and environmentally conscious, directly impacting the demand for lightweight aluminum and magnesium alloy components. The competitive dynamics are evolving, with established players investing heavily in research and development to stay ahead of the curve and new entrants exploring niche markets.

Opportunities abound in the growing electric vehicle (EV) segment, which requires specialized die-cast components for battery enclosures, motor housings, and thermal management systems. The ongoing transition from internal combustion engines (ICE) to EVs presents a significant growth catalyst for the North American automotive parts die casting market. Furthermore, the integration of Industry 4.0 principles, including automation, data analytics, and artificial intelligence, is revolutionizing manufacturing processes, leading to enhanced productivity, reduced waste, and improved quality control. The increasing focus on sustainable manufacturing practices and the circular economy is also opening doors for innovative solutions in material recycling and energy-efficient casting operations. The market penetration rate of advanced die casting techniques is expected to rise, as manufacturers recognize their ability to deliver higher value and meet the stringent requirements of modern automotive design.

Dominant Markets & Segments in North America Automotive Parts Die Casting Market

The North America Automotive Parts Die Casting Market exhibits distinct patterns of dominance across its various segments. Pressure Die Casting remains the dominant production process due to its high efficiency, speed, and cost-effectiveness for mass production of automotive components, particularly for high-volume parts like engine blocks and transmission housings. While other processes like vacuum die casting and semi-solid die casting are gaining traction for specialized applications requiring enhanced properties, pressure die casting will continue to lead in overall market volume.

In terms of application type, Engine Parts represent the largest and most influential segment. The intricate designs and stringent performance requirements of modern engines necessitate precise and durable die-cast components. Transmission Components also hold significant market share, as advanced transmissions demand complex, lightweight, and structurally sound parts. Body Parts are an emerging growth area, driven by the automotive industry's focus on lightweighting for improved fuel economy and EV range, with an increasing number of structural and aesthetic body panels being die-cast.

Material-wise, Aluminum alloys are the undisputed leader, owing to their excellent strength-to-weight ratio, corrosion resistance, and recyclability. The growing demand for lightweight vehicles directly boosts the consumption of aluminum die castings. Magnesium alloys are also witnessing a steady rise in demand, offering even greater weight savings than aluminum, making them ideal for specialized applications within the automotive sector. Zinc alloys, while traditionally used for smaller, intricate parts, are seeing renewed interest in certain applications due to their excellent castability and durability.

- Dominant Production Process: Pressure Die Casting, driven by its efficiency and cost-effectiveness for mass production of automotive components.

- Dominant Application Type: Engine Parts, due to the complex designs and stringent performance requirements of modern engines.

- Key Growth Drivers: Lightweighting initiatives, enhanced engine performance, and stringent emission regulations.

- Dominant Material Type: Aluminum, owing to its superior strength-to-weight ratio, corrosion resistance, and widespread recyclability.

- Key Growth Drivers: Growing demand for fuel-efficient vehicles and electric vehicles (EVs), advancements in aluminum alloy development.

North America Automotive Parts Die Casting Market Product Analysis

The North America Automotive Parts Die Casting Market is characterized by a continuous stream of product innovations focused on achieving superior performance, reduced weight, and enhanced sustainability. Manufacturers are increasingly leveraging advanced alloys, such as high-strength aluminum and lightweight magnesium, to produce components that meet the stringent demands of modern automotive engineering. Innovations in die casting technology, including the development of more precise molds and advanced process controls, enable the production of intricate geometries and parts with improved surface finish, minimizing the need for secondary machining operations. These advancements are critical for the development of lighter, more fuel-efficient vehicles and the rapidly expanding electric vehicle sector, where weight reduction is paramount for battery range optimization. The competitive advantage lies in the ability to deliver high-quality, cost-effective die-cast solutions that integrate seamlessly into complex automotive systems, driving efficiency and performance.

Key Drivers, Barriers & Challenges in North America Automotive Parts Die Casting Market

Key Drivers:

- Lightweighting Trend: The persistent drive for fuel efficiency and extended EV range fuels the demand for lightweight die-cast components made from aluminum and magnesium.

- Electric Vehicle (EV) Growth: The burgeoning EV market necessitates specialized die-cast parts for battery systems, powertrains, and thermal management, creating significant new demand.

- Technological Advancements: Continuous improvements in die casting processes, including automation and advanced simulation software, enhance precision, reduce costs, and enable complex designs.

- Cost-Effectiveness: Die casting remains a cost-effective method for high-volume production of complex metal parts compared to other manufacturing techniques.

- Regulatory Push for Emissions Reduction: Stricter emission standards incentivize the use of lighter materials and more efficient engine designs, both of which benefit from die casting.

Barriers & Challenges:

- Raw Material Price Volatility: Fluctuations in the prices of aluminum, magnesium, and zinc can significantly impact production costs and profit margins.

- Supply Chain Disruptions: Global supply chain vulnerabilities, including logistics bottlenecks and geopolitical factors, can affect the availability and cost of raw materials and finished goods.

- Intense Competition: The market is highly competitive, with both established global players and regional manufacturers vying for contracts, leading to price pressures.

- High Initial Investment: Setting up advanced die casting facilities requires substantial capital investment, posing a barrier to entry for smaller companies.

- Environmental Regulations: While driving innovation, increasingly stringent environmental regulations related to energy consumption and waste management can add to operational costs.

Growth Drivers in the North America Automotive Parts Die Casting Market Market

The North America Automotive Parts Die Casting Market is propelled by a confluence of powerful growth drivers. The relentless pursuit of vehicle lightweighting to enhance fuel economy and extend electric vehicle (EV) range is a primary catalyst, boosting demand for aluminum and magnesium die castings. The accelerating adoption of EVs across North America presents a substantial opportunity, as these vehicles require a host of specialized die-cast components for battery enclosures, motor housings, and thermal management systems. Furthermore, ongoing advancements in die casting technology, including automation, simulation software, and improved alloy formulations, are enabling the production of more complex and precise parts, driving efficiency and reducing manufacturing costs. The competitive advantage offered by die casting for mass production of intricate metal components remains a significant economic driver.

Challenges Impacting North America Automotive Parts Die Casting Market Growth

Despite robust growth prospects, the North America Automotive Parts Die Casting Market faces several significant challenges. The inherent volatility in raw material prices, particularly for aluminum and magnesium, poses a constant threat to cost management and profitability. Disruptions within the global supply chain, stemming from logistical issues and geopolitical uncertainties, can lead to material shortages and increased lead times. The market is also characterized by intense competition, with numerous players vying for automotive contracts, often leading to downward pressure on pricing. Moreover, the substantial initial capital investment required for state-of-the-art die casting facilities can act as a barrier to entry for new participants. Navigating complex and evolving environmental regulations regarding energy consumption and waste management also presents an ongoing challenge for manufacturers.

Key Players Shaping the North America Automotive Parts Die Casting Market Market

- DYNACAST

- KSM Castings

- Ryobi Die Casting

- Rheinmetall AG

- Martinrea Honsel

- GRUPO ANTOLIN-IRAUSA S A

- SAINT JEAN INDUSTRIES

- Nemak

- EMPIRE DIE CASTING COMPANY

- ALBERT HANDTMANN METALLGUSSWERK GMBH & CO KG

Significant North America Automotive Parts Die Casting Market Industry Milestones

- 2019: Introduction of advanced aluminum alloys with enhanced strength-to-weight ratios, enabling lighter vehicle components.

- 2020: Increased investment in automation and Industry 4.0 technologies for improved die casting efficiency and precision.

- 2021: Growing demand for magnesium die castings for EV battery enclosures and structural components.

- 2022: Significant M&A activity aimed at consolidating market share and expanding technological capabilities.

- 2023: Development of more sustainable die casting processes with reduced energy consumption and waste generation.

- 2024: Focus on developing die-cast solutions for next-generation EV platforms and autonomous driving systems.

Future Outlook for North America Automotive Parts Die Casting Market Market

The future outlook for the North America Automotive Parts Die Casting Market is exceptionally bright, driven by the accelerating transition towards electric vehicles and the ongoing imperative for vehicle lightweighting. Strategic opportunities lie in expanding production capabilities for specialized EV components, such as battery housings and integrated structural parts, which demand high precision and advanced material properties. The market will likely witness further integration of advanced manufacturing technologies, including AI-powered process optimization and advanced simulation tools, to enhance efficiency and product quality. Continuous innovation in aluminum and magnesium alloys, along with the exploration of new sustainable casting practices, will be crucial for maintaining a competitive edge. Stakeholders who can adapt to evolving OEM requirements, invest in cutting-edge technology, and navigate the dynamic regulatory landscape are poised for substantial growth and profitability in the coming years.

North America Automotive Parts Die Casting Market Segmentation

-

1. Production Process

- 1.1. Pressure Die Casting

- 1.2. Vaccum Die Casting

- 1.3. Squeeze Die Casting

- 1.4. Semi-Solid Die Casting

-

2. Application Type

- 2.1. Engine Parts

- 2.2. Transmission Components

- 2.3. Body Parts

- 2.4. Others

-

3. Material Type

- 3.1. Aluminum

- 3.2. Zinc

- 3.3. Magnesium

- 3.4. Others

North America Automotive Parts Die Casting Market Segmentation By Geography

- 1. United States

- 2. Canada

- 3. Rest of North America

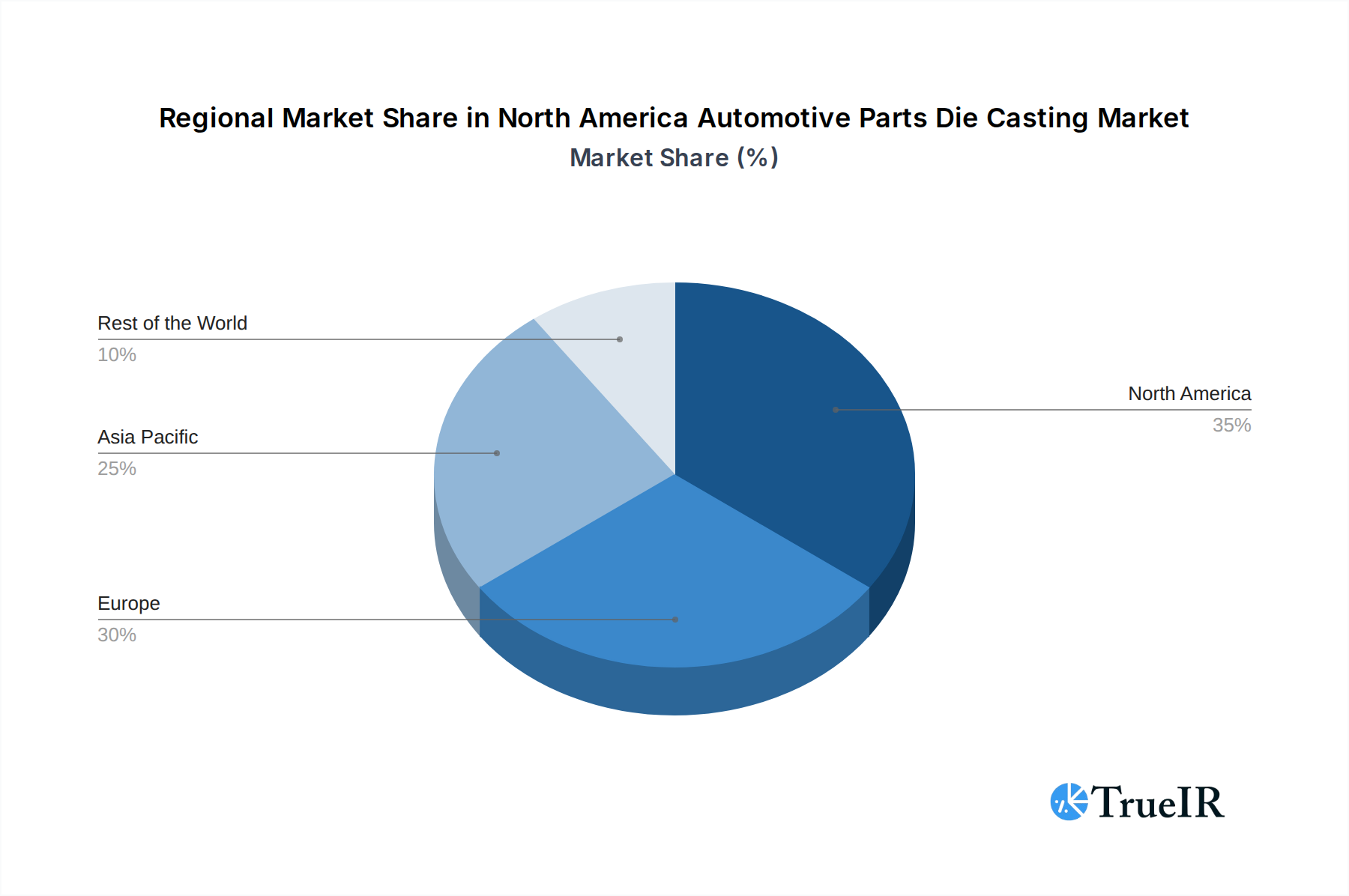

North America Automotive Parts Die Casting Market Regional Market Share

Geographic Coverage of North America Automotive Parts Die Casting Market

North America Automotive Parts Die Casting Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Production Process

- 5.1.1. Pressure Die Casting

- 5.1.2. Vaccum Die Casting

- 5.1.3. Squeeze Die Casting

- 5.1.4. Semi-Solid Die Casting

- 5.2. Market Analysis, Insights and Forecast - by Application Type

- 5.2.1. Engine Parts

- 5.2.2. Transmission Components

- 5.2.3. Body Parts

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Material Type

- 5.3.1. Aluminum

- 5.3.2. Zinc

- 5.3.3. Magnesium

- 5.3.4. Others

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. United States

- 5.4.2. Canada

- 5.4.3. Rest of North America

- 5.1. Market Analysis, Insights and Forecast - by Production Process

- 6. North America Automotive Parts Die Casting Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Production Process

- 6.1.1. Pressure Die Casting

- 6.1.2. Vaccum Die Casting

- 6.1.3. Squeeze Die Casting

- 6.1.4. Semi-Solid Die Casting

- 6.2. Market Analysis, Insights and Forecast - by Application Type

- 6.2.1. Engine Parts

- 6.2.2. Transmission Components

- 6.2.3. Body Parts

- 6.2.4. Others

- 6.3. Market Analysis, Insights and Forecast - by Material Type

- 6.3.1. Aluminum

- 6.3.2. Zinc

- 6.3.3. Magnesium

- 6.3.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Production Process

- 7. United States North America Automotive Parts Die Casting Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Production Process

- 7.1.1. Pressure Die Casting

- 7.1.2. Vaccum Die Casting

- 7.1.3. Squeeze Die Casting

- 7.1.4. Semi-Solid Die Casting

- 7.2. Market Analysis, Insights and Forecast - by Application Type

- 7.2.1. Engine Parts

- 7.2.2. Transmission Components

- 7.2.3. Body Parts

- 7.2.4. Others

- 7.3. Market Analysis, Insights and Forecast - by Material Type

- 7.3.1. Aluminum

- 7.3.2. Zinc

- 7.3.3. Magnesium

- 7.3.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Production Process

- 8. Canada North America Automotive Parts Die Casting Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Production Process

- 8.1.1. Pressure Die Casting

- 8.1.2. Vaccum Die Casting

- 8.1.3. Squeeze Die Casting

- 8.1.4. Semi-Solid Die Casting

- 8.2. Market Analysis, Insights and Forecast - by Application Type

- 8.2.1. Engine Parts

- 8.2.2. Transmission Components

- 8.2.3. Body Parts

- 8.2.4. Others

- 8.3. Market Analysis, Insights and Forecast - by Material Type

- 8.3.1. Aluminum

- 8.3.2. Zinc

- 8.3.3. Magnesium

- 8.3.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Production Process

- 9. Rest of North America North America Automotive Parts Die Casting Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Production Process

- 9.1.1. Pressure Die Casting

- 9.1.2. Vaccum Die Casting

- 9.1.3. Squeeze Die Casting

- 9.1.4. Semi-Solid Die Casting

- 9.2. Market Analysis, Insights and Forecast - by Application Type

- 9.2.1. Engine Parts

- 9.2.2. Transmission Components

- 9.2.3. Body Parts

- 9.2.4. Others

- 9.3. Market Analysis, Insights and Forecast - by Material Type

- 9.3.1. Aluminum

- 9.3.2. Zinc

- 9.3.3. Magnesium

- 9.3.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Production Process

- 10. Competitive Analysis

- 10.1. Company Profiles

- 10.1.1 DYNACAST

- 10.1.1.1. Company Overview

- 10.1.1.2. Products

- 10.1.1.3. Company Financials

- 10.1.1.4. SWOT Analysis

- 10.1.2 KSM Castings

- 10.1.2.1. Company Overview

- 10.1.2.2. Products

- 10.1.2.3. Company Financials

- 10.1.2.4. SWOT Analysis

- 10.1.3 Ryobi Die Casting

- 10.1.3.1. Company Overview

- 10.1.3.2. Products

- 10.1.3.3. Company Financials

- 10.1.3.4. SWOT Analysis

- 10.1.4 Rheinmetall AG

- 10.1.4.1. Company Overview

- 10.1.4.2. Products

- 10.1.4.3. Company Financials

- 10.1.4.4. SWOT Analysis

- 10.1.5 Martinrea Honsel

- 10.1.5.1. Company Overview

- 10.1.5.2. Products

- 10.1.5.3. Company Financials

- 10.1.5.4. SWOT Analysis

- 10.1.6 GRUPO ANTOLIN-IRAUSA S A

- 10.1.6.1. Company Overview

- 10.1.6.2. Products

- 10.1.6.3. Company Financials

- 10.1.6.4. SWOT Analysis

- 10.1.7 SAINT JEAN INDUSTRIES

- 10.1.7.1. Company Overview

- 10.1.7.2. Products

- 10.1.7.3. Company Financials

- 10.1.7.4. SWOT Analysis

- 10.1.8 Nemak

- 10.1.8.1. Company Overview

- 10.1.8.2. Products

- 10.1.8.3. Company Financials

- 10.1.8.4. SWOT Analysis

- 10.1.9 EMPIRE DIE CASTING COMPANY

- 10.1.9.1. Company Overview

- 10.1.9.2. Products

- 10.1.9.3. Company Financials

- 10.1.9.4. SWOT Analysis

- 10.1.10 ALBERT HANDTMANN METALLGUSSWERK GMBH & CO KG

- 10.1.10.1. Company Overview

- 10.1.10.2. Products

- 10.1.10.3. Company Financials

- 10.1.10.4. SWOT Analysis

- 10.1.1 DYNACAST

- 10.2. Market Entropy

- 10.2.1 Company's Key Areas Served

- 10.2.2 Recent Developments

- 10.3. Company Market Share Analysis 2025

- 10.3.1 Top 5 Companies Market Share Analysis

- 10.3.2 Top 3 Companies Market Share Analysis

- 10.4. List of Potential Customers

- 11. Research Methodology

List of Figures

- Figure 1: North America Automotive Parts Die Casting Market Revenue Breakdown (undefined, %) by Product 2025 & 2033

- Figure 2: North America Automotive Parts Die Casting Market Share (%) by Company 2025

List of Tables

- Table 1: North America Automotive Parts Die Casting Market Revenue undefined Forecast, by Production Process 2020 & 2033

- Table 2: North America Automotive Parts Die Casting Market Revenue undefined Forecast, by Application Type 2020 & 2033

- Table 3: North America Automotive Parts Die Casting Market Revenue undefined Forecast, by Material Type 2020 & 2033

- Table 4: North America Automotive Parts Die Casting Market Revenue undefined Forecast, by Region 2020 & 2033

- Table 5: North America Automotive Parts Die Casting Market Revenue undefined Forecast, by Production Process 2020 & 2033

- Table 6: North America Automotive Parts Die Casting Market Revenue undefined Forecast, by Application Type 2020 & 2033

- Table 7: North America Automotive Parts Die Casting Market Revenue undefined Forecast, by Material Type 2020 & 2033

- Table 8: North America Automotive Parts Die Casting Market Revenue undefined Forecast, by Country 2020 & 2033

- Table 9: North America Automotive Parts Die Casting Market Revenue undefined Forecast, by Production Process 2020 & 2033

- Table 10: North America Automotive Parts Die Casting Market Revenue undefined Forecast, by Application Type 2020 & 2033

- Table 11: North America Automotive Parts Die Casting Market Revenue undefined Forecast, by Material Type 2020 & 2033

- Table 12: North America Automotive Parts Die Casting Market Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: North America Automotive Parts Die Casting Market Revenue undefined Forecast, by Production Process 2020 & 2033

- Table 14: North America Automotive Parts Die Casting Market Revenue undefined Forecast, by Application Type 2020 & 2033

- Table 15: North America Automotive Parts Die Casting Market Revenue undefined Forecast, by Material Type 2020 & 2033

- Table 16: North America Automotive Parts Die Casting Market Revenue undefined Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Automotive Parts Die Casting Market?

The projected CAGR is approximately 6.8%.

2. Which companies are prominent players in the North America Automotive Parts Die Casting Market?

Key companies in the market include DYNACAST, KSM Castings, Ryobi Die Casting, Rheinmetall AG, Martinrea Honsel, GRUPO ANTOLIN-IRAUSA S A, SAINT JEAN INDUSTRIES, Nemak, EMPIRE DIE CASTING COMPANY, ALBERT HANDTMANN METALLGUSSWERK GMBH & CO KG.

3. What are the main segments of the North America Automotive Parts Die Casting Market?

The market segments include Production Process, Application Type, Material Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

Increasing Consumer Preference toward Fast Food Consumption Fosters the Growth of the Market.

6. What are the notable trends driving market growth?

Magnesium Die Casting Grows with Highest CAGR.

7. Are there any restraints impacting market growth?

Rapid Integration of Online Food Delivery Services Hampers the Growth of the Market.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Automotive Parts Die Casting Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Automotive Parts Die Casting Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Automotive Parts Die Casting Market?

To stay informed about further developments, trends, and reports in the North America Automotive Parts Die Casting Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence