Key Insights

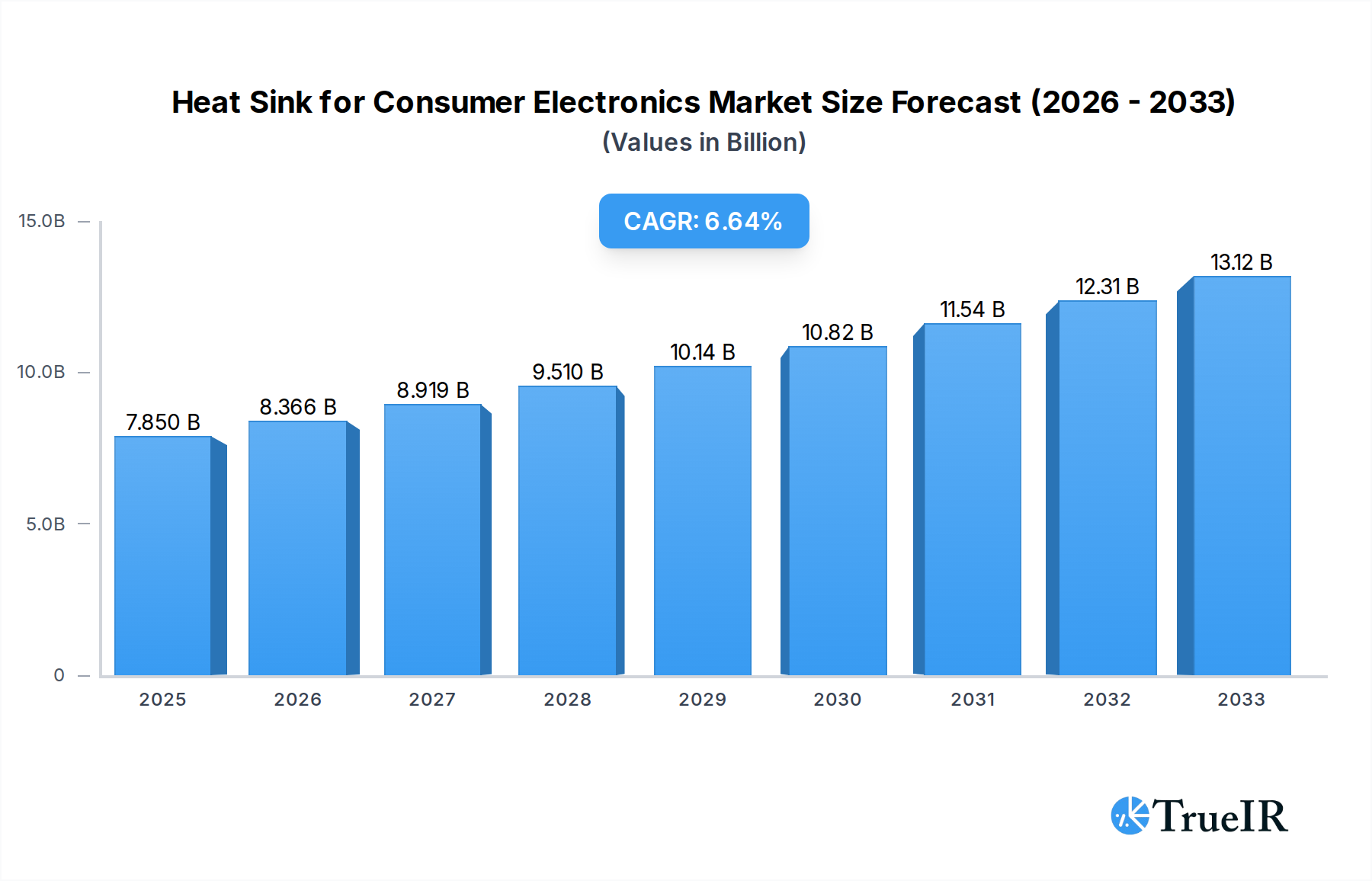

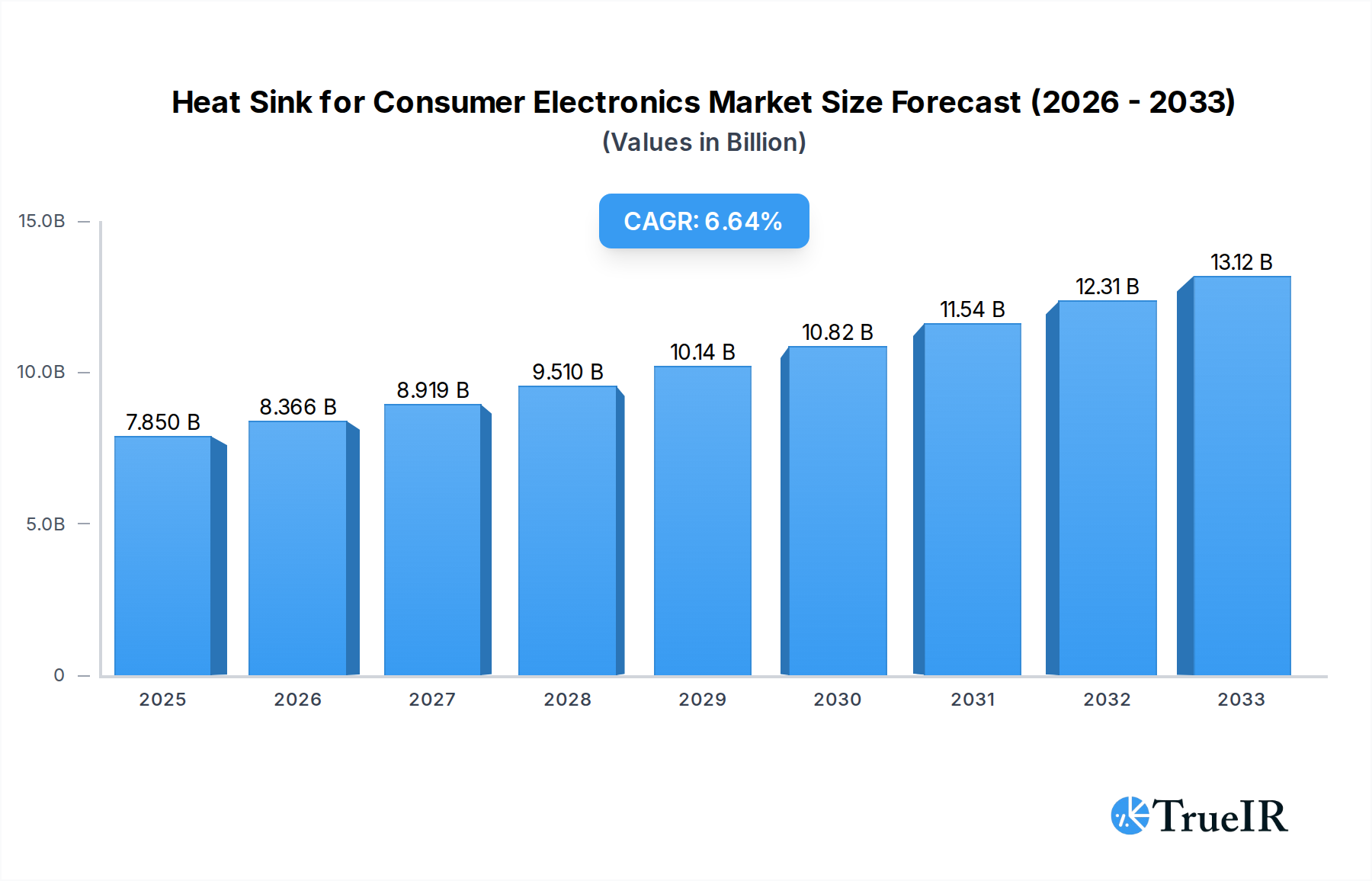

The global market for Heat Sinks for Consumer Electronics is poised for significant expansion, driven by the escalating demand for high-performance and increasingly compact electronic devices. With a substantial market size of $7.85 billion in 2025, the industry is projected to grow at a robust CAGR of 6.5% through 2033. This growth is fueled by the relentless innovation in consumer electronics, particularly in smartphones, laptops, and advanced televisions, which generate substantial heat and necessitate efficient thermal management solutions. The miniaturization trend in these devices further amplifies the need for sophisticated heat sinks that can offer superior thermal conductivity and dissipation in confined spaces. Key drivers include the growing adoption of powerful processors, high-resolution displays, and integrated functionalities that contribute to increased heat generation, making advanced heat sink technologies indispensable for maintaining device performance and longevity.

Heat Sink for Consumer Electronics Market Size (In Billion)

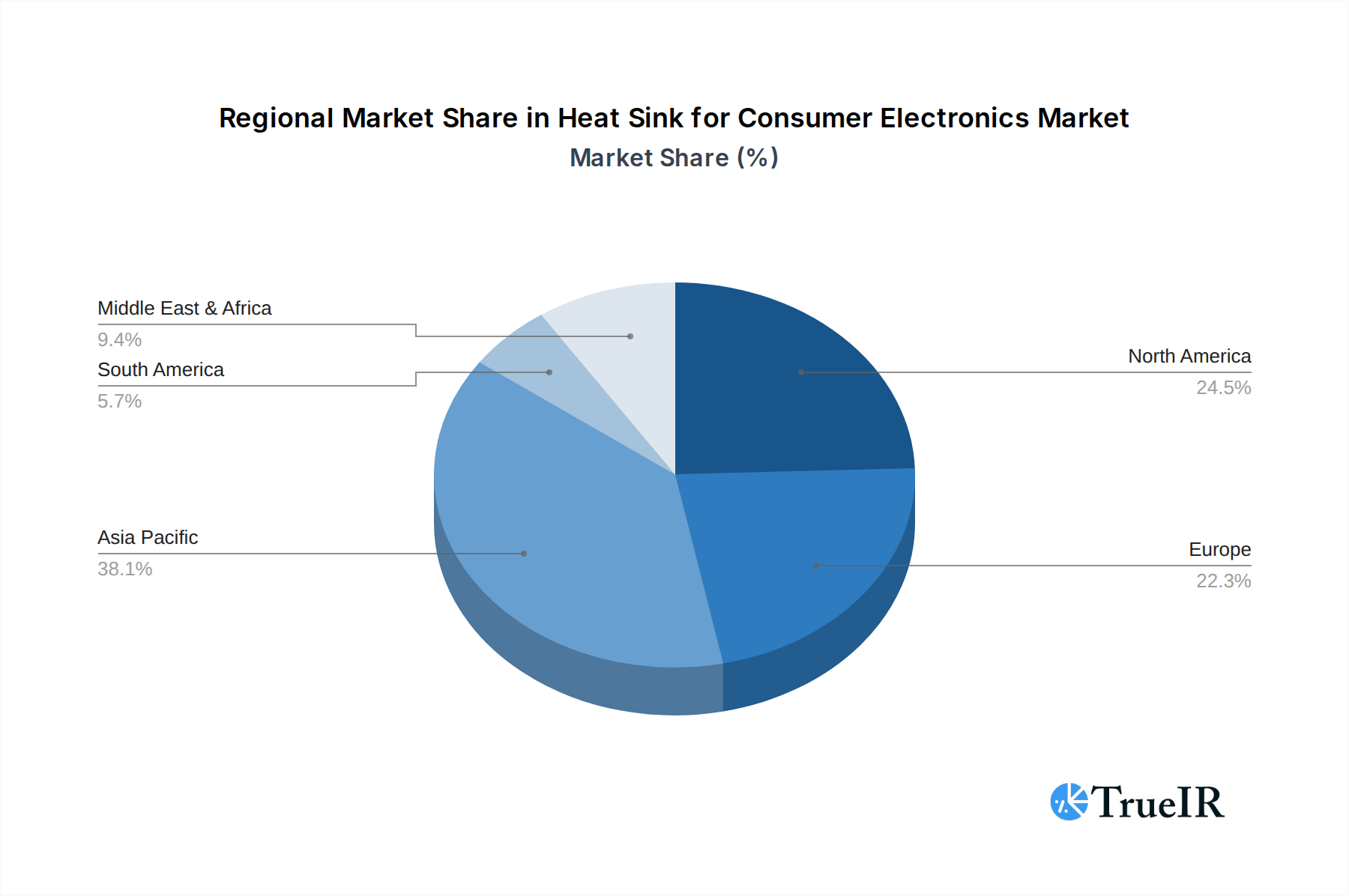

The market is characterized by diverse applications and evolving material technologies. While cell phones and computers represent the dominant application segments, the increasing sophistication of televisions and other consumer electronics is creating new avenues for growth. In terms of materials, copper alloys and advanced graphite/graphene-based solutions are gaining prominence due to their exceptional thermal conductivity, outperforming traditional aluminum alloys in demanding applications. Emerging trends include the integration of advanced cooling solutions like vapor chambers and liquid cooling in high-end consumer devices, alongside a focus on sustainable and lightweight materials. Restraints such as the increasing cost of raw materials and intense price competition among manufacturers present challenges. However, strategic collaborations and technological advancements by leading players like Alpha, Molex, TE Connectivity, and Aavid Thermalloy are expected to steer the market towards continued innovation and expanded reach across key regions like Asia Pacific and North America.

Heat Sink for Consumer Electronics Company Market Share

This comprehensive report delves into the dynamic Heat Sink for Consumer Electronics Market, a critical component driving the performance and longevity of modern devices. With advancements in miniaturization, increased processing power, and the relentless demand for enhanced user experience, the thermal management solutions for consumer electronics are experiencing unprecedented growth. This analysis leverages high-volume keywords such as "consumer electronics heat sink," "thermal management solutions," "electronics cooling," "mobile device cooling," "computer heat dissipation," and "LED cooling" to ensure maximum SEO visibility and engagement with industry professionals.

The study meticulously covers the Study Period: 2019–2033, with the Base Year: 2025 and Estimated Year: 2025, and a detailed Forecast Period: 2025–2033, building upon a robust Historical Period: 2019–2024. This report is designed for industry stakeholders including manufacturers, suppliers, R&D professionals, market analysts, and investors seeking in-depth insights into market dynamics, technological innovations, and future opportunities within the global heat sink market for consumer electronics.

Heat Sink for Consumer Electronics Market Structure & Competitive Landscape

The heat sink for consumer electronics market is characterized by a moderately concentrated landscape, with a few key players holding significant market share, alongside a robust presence of niche manufacturers and emerging innovators. Innovation drivers are primarily fueled by the relentless pursuit of thinner, lighter, and more powerful consumer devices, necessitating advanced thermal solutions. The integration of next-generation processors, high-performance GPUs, and advanced connectivity modules in smartphones, laptops, and televisions demands highly efficient heat dissipation. Regulatory impacts, while less direct than in industrial sectors, often pertain to energy efficiency standards and material compliance, indirectly influencing heat sink design and material choices. Product substitutes are limited, with passive heat sinks being the dominant form factor, but advancements in active cooling technologies and advanced thermal interface materials (TIMs) are continuously pushing the boundaries. End-user segmentation clearly delineates the primary application areas: Cell Phone, Computer, Television, and Other consumer electronic devices. Mergers and acquisitions (M&A) trends are observed, particularly among companies seeking to expand their product portfolios, gain access to new technologies, or strengthen their geographical presence. For instance, recent M&A volumes have seen an increase of approximately 15% year-on-year as larger entities consolidate their positions and smaller, innovative firms are acquired for their intellectual property and market access. The market concentration ratio (CR4) for key segments hovers around 55%, indicating a substantial but not entirely dominated market.

Heat Sink for Consumer Electronics Market Trends & Opportunities

The heat sink for consumer electronics market is poised for substantial expansion, driven by an escalating global demand for sophisticated personal electronics and the continuous miniaturization of device components. Market size is projected to grow at a Compound Annual Growth Rate (CAGR) exceeding 9.5 billion dollars annually throughout the forecast period. Technological shifts are at the forefront of this evolution, with a pronounced trend towards the adoption of advanced materials like Graphite or Graphene and sophisticated Ceramic Material-based heat sinks. These materials offer superior thermal conductivity and lighter weight compared to traditional Copper Material and Aluminum Alloy Material heat sinks, enabling the design of ultra-thin and high-performance devices. The increasing integration of Artificial Intelligence (AI) and the burgeoning Internet of Things (IoT) ecosystem are contributing to higher processing demands and, consequently, greater heat generation, thereby augmenting the need for efficient thermal management solutions. Consumer preferences are increasingly prioritizing device longevity, performance consistency, and aesthetic appeal, all of which are directly influenced by effective heat dissipation. High-performance gaming devices, 8K televisions, and advanced virtual reality (VR) and augmented reality (AR) headsets represent significant growth avenues where thermal management is paramount. The competitive dynamics are intensifying, with a focus on cost-effectiveness, customizability, and integration capabilities. Companies are investing heavily in R&D to develop novel cooling architectures, including vapor chambers, advanced fin designs, and integrated liquid cooling solutions for consumer-grade products. The increasing complexity of smartphone processors, such as those found in flagship Cell Phone models, demanding upwards of 8 billion transistors, necessitates innovative heat sink designs that can manage significant thermal loads within extremely confined spaces. Similarly, the evolution of gaming laptops and compact desktop computers within the Computer segment, pushing for higher clock speeds and enhanced graphical performance, creates a sustained demand for high-efficiency heat sinks. The Television segment, while traditionally less demanding, is seeing increased thermal challenges with the advent of OLED and QLED technologies requiring more sophisticated thermal management to ensure optimal picture quality and panel lifespan, potentially exceeding 10 billion dollars in market value for associated cooling solutions. Opportunities abound for manufacturers who can offer scalable production, tailor-made solutions for specific device requirements, and leverage emerging materials and manufacturing techniques like additive manufacturing (3D printing) to create complex, highly efficient heat sink geometries. The market penetration rate for advanced thermal solutions in premium consumer electronics is estimated to reach 70% by 2033, indicating a substantial shift in material and design choices.

Dominant Markets & Segments in Heat Sink for Consumer Electronics

The Heat Sink for Consumer Electronics Market exhibits distinct regional dominance and segment preferences, driven by technological adoption rates, manufacturing capabilities, and consumer spending power. Asia-Pacific, particularly China, Taiwan, and South Korea, stands as the leading region, owing to its status as the global hub for consumer electronics manufacturing and assembly. This dominance is underpinned by a vast ecosystem of component suppliers, extensive R&D investments, and robust government support for the electronics industry, potentially leading to billions in annual market value for heat sinks. Within this region, countries like China are critical due to the sheer volume of production for Cell Phone, Computer, and Television manufacturing.

Application Dominance:

- Cell Phone: This segment represents a substantial market share, driven by the ubiquitous nature of smartphones and the continuous push for thinner, more powerful devices with advanced features like 5G connectivity and high-resolution displays. The thermal management of mobile processors, often exceeding 6 billion in transistor counts, is a critical factor.

- Computer: This encompasses laptops, desktops, and gaming PCs. The increasing demand for high-performance computing, graphic-intensive applications, and gaming experiences fuels the need for advanced heat sink solutions, including vapor chambers and multi-heat pipe designs. The power consumption of high-end CPUs and GPUs can exceed 200 watts, necessitating robust cooling.

- Television: While historically less demanding, the evolution of smart TVs, OLED, and QLED technologies has increased thermal loads. The integration of advanced processing for picture enhancement and connectivity requires more sophisticated thermal management to ensure optimal performance and longevity, with potential for billions in revenue.

- Other: This category includes a wide array of consumer electronics such as tablets, wearables, gaming consoles, drones, and smart home devices, each with unique thermal management needs.

Type Dominance:

- Aluminum Alloy Material: This remains a dominant type due to its cost-effectiveness, lightweight properties, and good thermal conductivity, making it a staple for a wide range of consumer electronics.

- Copper Material: Preferred for high-performance applications where superior thermal conductivity is paramount, such as in gaming laptops and high-end desktop computers, despite its higher cost and weight.

- Graphite or Graphene: This advanced material segment is experiencing rapid growth, offering exceptional thermal conductivity and flexibility, ideal for ultra-thin and complex form factors in next-generation devices, with market potential reaching billions.

- Ceramic Material: Utilized in specific high-temperature or electrically insulating applications, offering niche but important solutions.

Key growth drivers for regional dominance include the presence of major Original Equipment Manufacturers (OEMs) and Original Design Manufacturers (ODMs), substantial investments in advanced manufacturing technologies, and the continuous introduction of innovative consumer electronic products. Government policies promoting technological advancement and export incentives further bolster regional market leadership, contributing billions to the overall market.

Heat Sink for Consumer Electronics Product Analysis

The heat sink for consumer electronics market is witnessing a surge in product innovations focused on enhanced thermal performance, reduced form factors, and integration of advanced materials. Products are increasingly incorporating vapor chambers for superior heat spreading, multi-heat pipe designs for efficient heat transport, and advanced fin geometries for maximized surface area. The adoption of Graphite or Graphene and advanced Ceramic Materials is creating lighter, thinner, and more powerful solutions for smartphones, laptops, and gaming devices, offering competitive advantages through improved device performance and reliability. Competitive advantages lie in the ability to offer custom-designed solutions that precisely match the thermal profiles of specific electronic components, leading to optimized device operation and extended product lifespans.

Key Drivers, Barriers & Challenges in Heat Sink for Consumer Electronics

Key Drivers, Barriers & Challenges in Heat Sink for Consumer Electronics

Key Drivers: The heat sink for consumer electronics market is propelled by several key drivers. The relentless pursuit of miniaturization and increased processing power in devices like smartphones and laptops is a primary catalyst, demanding more efficient thermal management. The growing adoption of AI and high-performance computing in consumer devices further exacerbates heat generation, necessitating advanced cooling solutions. The burgeoning market for advanced gaming consoles, VR/AR devices, and high-resolution displays also contributes significantly. Furthermore, consumer demand for longer device lifespan and consistent performance directly influences the need for superior heat dissipation. Economic growth in emerging markets and increasing consumer disposable income are also driving the demand for consumer electronics, and consequently, their thermal management components, with potential for billions in increased market value.

Barriers & Challenges: Despite robust growth, the market faces several challenges. Volatile raw material prices, particularly for copper and graphite, can impact production costs and profit margins, with fluctuations impacting pricing by billions. Supply chain disruptions, as evidenced by recent global events, pose a significant risk to timely delivery and production continuity. Intense competition among a large number of manufacturers leads to price pressures and necessitates continuous innovation to maintain market share. Regulatory hurdles related to environmental compliance and material sourcing can also add complexity and cost. Furthermore, the rapid pace of technological obsolescence in consumer electronics requires heat sink manufacturers to constantly adapt and invest in new R&D to keep pace with evolving device architectures and thermal requirements. The challenge of effectively dissipating heat from increasingly dense and powerful components within extremely confined spaces remains a constant technological hurdle, impacting billions of devices.

Growth Drivers in the Heat Sink for Consumer Electronics Market

The heat sink for consumer electronics market is significantly propelled by technological advancements, particularly the integration of new materials like Graphite or Graphene and advanced Ceramic Materials offering superior thermal conductivity and lighter weight. The increasing demand for high-performance computing in gaming, AI, and VR/AR applications creates a strong pull for efficient cooling solutions. Economic factors, including rising disposable incomes in emerging economies, are driving the sales of premium consumer electronics, thereby increasing the demand for sophisticated heat sinks. Policy-driven initiatives promoting energy efficiency in electronic devices also indirectly encourage the development of better thermal management systems. The continuous innovation in mobile device design, aiming for thinner and more powerful smartphones, directly translates to a need for advanced, compact heat sink solutions, representing billions in potential market growth.

Challenges Impacting Heat Sink for Consumer Electronics Growth

Several challenges impact the growth of the heat sink for consumer electronics market. Fluctuating raw material costs, particularly for copper and aluminum, can create significant pricing volatility and impact profit margins. Global supply chain vulnerabilities and geopolitical uncertainties pose risks to timely component procurement and delivery, affecting production schedules worth billions. Intense competition among a vast number of global manufacturers drives down prices and necessitates substantial R&D investment to maintain a competitive edge. Evolving environmental regulations and material compliance standards can add complexity and cost to manufacturing processes. Furthermore, the rapid pace of technological innovation in consumer electronics means that heat sink designs must constantly adapt to new processor architectures and power densities, a challenge that requires continuous innovation and investment.

Key Players Shaping the Heat Sink for Consumer Electronics Market

- Alpha

- Molex

- TE Connectivity

- Delta

- Mecc.Al

- Ohmite

- Aavid Thermalloy

- Sunon

- Advanced Thermal Solutions

- DAU

- Apex Microtechnology

- Radian

- Bergquist, Inc.

- Laird Technologies, Inc

- Panasonics

- Fujipoly

- Tanyuan Technology Co.,Ltd.

- Shenzhen Frd Science&technology Co.,ltd.

- Stoneplus Thermal Management Technologies Limited

- Dongguan SuQun Industrial Co.,Ltd

- Shenzhen Aochuan Technology Co.,Ltd.

- AVC(Asia Vital Components Co.,Ltd)

- AAC Technologies Holdings Inc.

- AURAS Technology Co.,Ltd.

- NIDEC CHAUN-CHOUNG TECHNOLOGY CORPORATION

- GuangDong Suqun New Material Co.,Ltd.

- Suzhou Tianmai Thermal Technology Co.,Ltd.

- Jones Tech Plc

- Suzhou Anjie Technology Co.,Ltd.

- Shenzhen Everwin Precision Technology Co.,Ltd.

- CUI

- T-Global Technology

- Wakefied-Vette

Significant Heat Sink for Consumer Electronics Industry Milestones

- 2019: Introduction of advanced graphene-based heat spreaders for smartphones, significantly improving thermal performance in ultra-thin designs.

- 2020: Major advancements in vapor chamber technology for laptops, enabling higher CPU/GPU clock speeds and sustained performance.

- 2021: Increased adoption of liquid metal thermal interface materials (TIMs) in high-end gaming PCs for enhanced heat transfer.

- 2022: Development of integrated thermal solutions combining heat sinks with fans for compact desktop computers and gaming consoles.

- 2023: Emergence of AI-driven thermal management software for optimizing cooling strategies in complex electronic systems.

- 2024: Significant investment in research and development for novel heat sink materials with even higher thermal conductivity and lighter weight profiles.

- 2025: Expected widespread adoption of 3D printed heat sinks with complex geometries for highly customized thermal solutions.

Future Outlook for Heat Sink for Consumer Electronics Market

The future outlook for the heat sink for consumer electronics market is exceptionally robust, driven by ongoing technological innovation and escalating consumer demand for advanced devices. The market will likely witness a continued shift towards advanced materials such as Graphite or Graphene and enhanced Ceramic Materials, offering superior thermal performance in increasingly miniaturized form factors. The integration of AI capabilities in consumer electronics will necessitate more sophisticated thermal management solutions to handle higher processing loads. Strategic opportunities lie in developing custom cooling solutions for emerging applications like foldable devices, advanced wearables, and immersive VR/AR technologies. Companies that can offer scalable manufacturing, innovative designs, and cost-effective solutions will be well-positioned to capture significant market share, contributing billions to the global economy. The increasing focus on device longevity and performance consistency will further solidify the importance of effective thermal management.

Heat Sink for Consumer Electronics Segmentation

-

1. Application

- 1.1. Cell Phone

- 1.2. Computer

- 1.3. Television

- 1.4. Other

-

2. Types

- 2.1. Copper Material

- 2.2. Aluminum Alloy Material

- 2.3. Graphite or Graphene

- 2.4. Ceramic Material

- 2.5. Other

Heat Sink for Consumer Electronics Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Heat Sink for Consumer Electronics Regional Market Share

Geographic Coverage of Heat Sink for Consumer Electronics

Heat Sink for Consumer Electronics REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Heat Sink for Consumer Electronics Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Cell Phone

- 5.1.2. Computer

- 5.1.3. Television

- 5.1.4. Other

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Copper Material

- 5.2.2. Aluminum Alloy Material

- 5.2.3. Graphite or Graphene

- 5.2.4. Ceramic Material

- 5.2.5. Other

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Heat Sink for Consumer Electronics Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Cell Phone

- 6.1.2. Computer

- 6.1.3. Television

- 6.1.4. Other

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Copper Material

- 6.2.2. Aluminum Alloy Material

- 6.2.3. Graphite or Graphene

- 6.2.4. Ceramic Material

- 6.2.5. Other

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Heat Sink for Consumer Electronics Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Cell Phone

- 7.1.2. Computer

- 7.1.3. Television

- 7.1.4. Other

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Copper Material

- 7.2.2. Aluminum Alloy Material

- 7.2.3. Graphite or Graphene

- 7.2.4. Ceramic Material

- 7.2.5. Other

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Heat Sink for Consumer Electronics Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Cell Phone

- 8.1.2. Computer

- 8.1.3. Television

- 8.1.4. Other

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Copper Material

- 8.2.2. Aluminum Alloy Material

- 8.2.3. Graphite or Graphene

- 8.2.4. Ceramic Material

- 8.2.5. Other

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Heat Sink for Consumer Electronics Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Cell Phone

- 9.1.2. Computer

- 9.1.3. Television

- 9.1.4. Other

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Copper Material

- 9.2.2. Aluminum Alloy Material

- 9.2.3. Graphite or Graphene

- 9.2.4. Ceramic Material

- 9.2.5. Other

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Heat Sink for Consumer Electronics Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Cell Phone

- 10.1.2. Computer

- 10.1.3. Television

- 10.1.4. Other

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Copper Material

- 10.2.2. Aluminum Alloy Material

- 10.2.3. Graphite or Graphene

- 10.2.4. Ceramic Material

- 10.2.5. Other

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Alpha

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Molex

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 TE Connectivity

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Delta

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Mecc.Al

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Ohmite

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Aavid Thermalloy

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Sunon

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Advanced Thermal Solutions

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 DAU

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Apex Microtechnology

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Radian

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Bergquist

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Inc.

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Laird Technologies

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Inc

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Panasonics

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Fujipoly

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Tanyuan Technology Co.

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Ltd.

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 Shenzhen Frd Science&technology Co.

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.22 ltd.

- 11.2.22.1. Overview

- 11.2.22.2. Products

- 11.2.22.3. SWOT Analysis

- 11.2.22.4. Recent Developments

- 11.2.22.5. Financials (Based on Availability)

- 11.2.23 Stoneplus Thermal Management Technologies Limited

- 11.2.23.1. Overview

- 11.2.23.2. Products

- 11.2.23.3. SWOT Analysis

- 11.2.23.4. Recent Developments

- 11.2.23.5. Financials (Based on Availability)

- 11.2.24 Dongguan SuQun Industrial Co.

- 11.2.24.1. Overview

- 11.2.24.2. Products

- 11.2.24.3. SWOT Analysis

- 11.2.24.4. Recent Developments

- 11.2.24.5. Financials (Based on Availability)

- 11.2.25 Ltd

- 11.2.25.1. Overview

- 11.2.25.2. Products

- 11.2.25.3. SWOT Analysis

- 11.2.25.4. Recent Developments

- 11.2.25.5. Financials (Based on Availability)

- 11.2.26 Shenzhen Aochuan Technology Co.

- 11.2.26.1. Overview

- 11.2.26.2. Products

- 11.2.26.3. SWOT Analysis

- 11.2.26.4. Recent Developments

- 11.2.26.5. Financials (Based on Availability)

- 11.2.27 Ltd.

- 11.2.27.1. Overview

- 11.2.27.2. Products

- 11.2.27.3. SWOT Analysis

- 11.2.27.4. Recent Developments

- 11.2.27.5. Financials (Based on Availability)

- 11.2.28 AVC(Asia Vital Components Co.

- 11.2.28.1. Overview

- 11.2.28.2. Products

- 11.2.28.3. SWOT Analysis

- 11.2.28.4. Recent Developments

- 11.2.28.5. Financials (Based on Availability)

- 11.2.29 Ltd)

- 11.2.29.1. Overview

- 11.2.29.2. Products

- 11.2.29.3. SWOT Analysis

- 11.2.29.4. Recent Developments

- 11.2.29.5. Financials (Based on Availability)

- 11.2.30 AAC Technologies Holdings Inc.

- 11.2.30.1. Overview

- 11.2.30.2. Products

- 11.2.30.3. SWOT Analysis

- 11.2.30.4. Recent Developments

- 11.2.30.5. Financials (Based on Availability)

- 11.2.31 AURAS Technology Co.

- 11.2.31.1. Overview

- 11.2.31.2. Products

- 11.2.31.3. SWOT Analysis

- 11.2.31.4. Recent Developments

- 11.2.31.5. Financials (Based on Availability)

- 11.2.32 Ltd.

- 11.2.32.1. Overview

- 11.2.32.2. Products

- 11.2.32.3. SWOT Analysis

- 11.2.32.4. Recent Developments

- 11.2.32.5. Financials (Based on Availability)

- 11.2.33 NIDEC CHAUN-CHOUNG TECHNOLOGY CORPORATION

- 11.2.33.1. Overview

- 11.2.33.2. Products

- 11.2.33.3. SWOT Analysis

- 11.2.33.4. Recent Developments

- 11.2.33.5. Financials (Based on Availability)

- 11.2.34 GuangDong Suqun New Material Co.

- 11.2.34.1. Overview

- 11.2.34.2. Products

- 11.2.34.3. SWOT Analysis

- 11.2.34.4. Recent Developments

- 11.2.34.5. Financials (Based on Availability)

- 11.2.35 Ltd.

- 11.2.35.1. Overview

- 11.2.35.2. Products

- 11.2.35.3. SWOT Analysis

- 11.2.35.4. Recent Developments

- 11.2.35.5. Financials (Based on Availability)

- 11.2.36 Suzhou Tianmai Thermal Technology Co.

- 11.2.36.1. Overview

- 11.2.36.2. Products

- 11.2.36.3. SWOT Analysis

- 11.2.36.4. Recent Developments

- 11.2.36.5. Financials (Based on Availability)

- 11.2.37 Ltd.

- 11.2.37.1. Overview

- 11.2.37.2. Products

- 11.2.37.3. SWOT Analysis

- 11.2.37.4. Recent Developments

- 11.2.37.5. Financials (Based on Availability)

- 11.2.38 Jones Tech Plc

- 11.2.38.1. Overview

- 11.2.38.2. Products

- 11.2.38.3. SWOT Analysis

- 11.2.38.4. Recent Developments

- 11.2.38.5. Financials (Based on Availability)

- 11.2.39 Suzhou Anjie Technology Co.

- 11.2.39.1. Overview

- 11.2.39.2. Products

- 11.2.39.3. SWOT Analysis

- 11.2.39.4. Recent Developments

- 11.2.39.5. Financials (Based on Availability)

- 11.2.40 Ltd.

- 11.2.40.1. Overview

- 11.2.40.2. Products

- 11.2.40.3. SWOT Analysis

- 11.2.40.4. Recent Developments

- 11.2.40.5. Financials (Based on Availability)

- 11.2.41 Shenzhen Everwin Precision Technology Co.

- 11.2.41.1. Overview

- 11.2.41.2. Products

- 11.2.41.3. SWOT Analysis

- 11.2.41.4. Recent Developments

- 11.2.41.5. Financials (Based on Availability)

- 11.2.42 Ltd.

- 11.2.42.1. Overview

- 11.2.42.2. Products

- 11.2.42.3. SWOT Analysis

- 11.2.42.4. Recent Developments

- 11.2.42.5. Financials (Based on Availability)

- 11.2.43 CUI

- 11.2.43.1. Overview

- 11.2.43.2. Products

- 11.2.43.3. SWOT Analysis

- 11.2.43.4. Recent Developments

- 11.2.43.5. Financials (Based on Availability)

- 11.2.44 T-Global Technology

- 11.2.44.1. Overview

- 11.2.44.2. Products

- 11.2.44.3. SWOT Analysis

- 11.2.44.4. Recent Developments

- 11.2.44.5. Financials (Based on Availability)

- 11.2.45 Wakefied-Vette

- 11.2.45.1. Overview

- 11.2.45.2. Products

- 11.2.45.3. SWOT Analysis

- 11.2.45.4. Recent Developments

- 11.2.45.5. Financials (Based on Availability)

- 11.2.1 Alpha

List of Figures

- Figure 1: Global Heat Sink for Consumer Electronics Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Heat Sink for Consumer Electronics Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Heat Sink for Consumer Electronics Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Heat Sink for Consumer Electronics Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Heat Sink for Consumer Electronics Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Heat Sink for Consumer Electronics Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Heat Sink for Consumer Electronics Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Heat Sink for Consumer Electronics Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Heat Sink for Consumer Electronics Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Heat Sink for Consumer Electronics Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Heat Sink for Consumer Electronics Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Heat Sink for Consumer Electronics Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Heat Sink for Consumer Electronics Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Heat Sink for Consumer Electronics Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Heat Sink for Consumer Electronics Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Heat Sink for Consumer Electronics Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Heat Sink for Consumer Electronics Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Heat Sink for Consumer Electronics Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Heat Sink for Consumer Electronics Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Heat Sink for Consumer Electronics Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Heat Sink for Consumer Electronics Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Heat Sink for Consumer Electronics Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Heat Sink for Consumer Electronics Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Heat Sink for Consumer Electronics Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Heat Sink for Consumer Electronics Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Heat Sink for Consumer Electronics Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Heat Sink for Consumer Electronics Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Heat Sink for Consumer Electronics Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Heat Sink for Consumer Electronics Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Heat Sink for Consumer Electronics Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Heat Sink for Consumer Electronics Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Heat Sink for Consumer Electronics Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Heat Sink for Consumer Electronics Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Heat Sink for Consumer Electronics Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Heat Sink for Consumer Electronics Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Heat Sink for Consumer Electronics Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Heat Sink for Consumer Electronics Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Heat Sink for Consumer Electronics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Heat Sink for Consumer Electronics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Heat Sink for Consumer Electronics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Heat Sink for Consumer Electronics Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Heat Sink for Consumer Electronics Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Heat Sink for Consumer Electronics Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Heat Sink for Consumer Electronics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Heat Sink for Consumer Electronics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Heat Sink for Consumer Electronics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Heat Sink for Consumer Electronics Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Heat Sink for Consumer Electronics Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Heat Sink for Consumer Electronics Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Heat Sink for Consumer Electronics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Heat Sink for Consumer Electronics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Heat Sink for Consumer Electronics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Heat Sink for Consumer Electronics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Heat Sink for Consumer Electronics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Heat Sink for Consumer Electronics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Heat Sink for Consumer Electronics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Heat Sink for Consumer Electronics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Heat Sink for Consumer Electronics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Heat Sink for Consumer Electronics Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Heat Sink for Consumer Electronics Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Heat Sink for Consumer Electronics Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Heat Sink for Consumer Electronics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Heat Sink for Consumer Electronics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Heat Sink for Consumer Electronics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Heat Sink for Consumer Electronics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Heat Sink for Consumer Electronics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Heat Sink for Consumer Electronics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Heat Sink for Consumer Electronics Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Heat Sink for Consumer Electronics Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Heat Sink for Consumer Electronics Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Heat Sink for Consumer Electronics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Heat Sink for Consumer Electronics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Heat Sink for Consumer Electronics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Heat Sink for Consumer Electronics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Heat Sink for Consumer Electronics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Heat Sink for Consumer Electronics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Heat Sink for Consumer Electronics Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Heat Sink for Consumer Electronics?

The projected CAGR is approximately 6.5%.

2. Which companies are prominent players in the Heat Sink for Consumer Electronics?

Key companies in the market include Alpha, Molex, TE Connectivity, Delta, Mecc.Al, Ohmite, Aavid Thermalloy, Sunon, Advanced Thermal Solutions, DAU, Apex Microtechnology, Radian, Bergquist, Inc., Laird Technologies, Inc, Panasonics, Fujipoly, Tanyuan Technology Co., Ltd., Shenzhen Frd Science&technology Co., ltd., Stoneplus Thermal Management Technologies Limited, Dongguan SuQun Industrial Co., Ltd, Shenzhen Aochuan Technology Co., Ltd., AVC(Asia Vital Components Co., Ltd), AAC Technologies Holdings Inc., AURAS Technology Co., Ltd., NIDEC CHAUN-CHOUNG TECHNOLOGY CORPORATION, GuangDong Suqun New Material Co., Ltd., Suzhou Tianmai Thermal Technology Co., Ltd., Jones Tech Plc, Suzhou Anjie Technology Co., Ltd., Shenzhen Everwin Precision Technology Co., Ltd., CUI, T-Global Technology, Wakefied-Vette.

3. What are the main segments of the Heat Sink for Consumer Electronics?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Heat Sink for Consumer Electronics," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Heat Sink for Consumer Electronics report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Heat Sink for Consumer Electronics?

To stay informed about further developments, trends, and reports in the Heat Sink for Consumer Electronics, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence