Key Insights

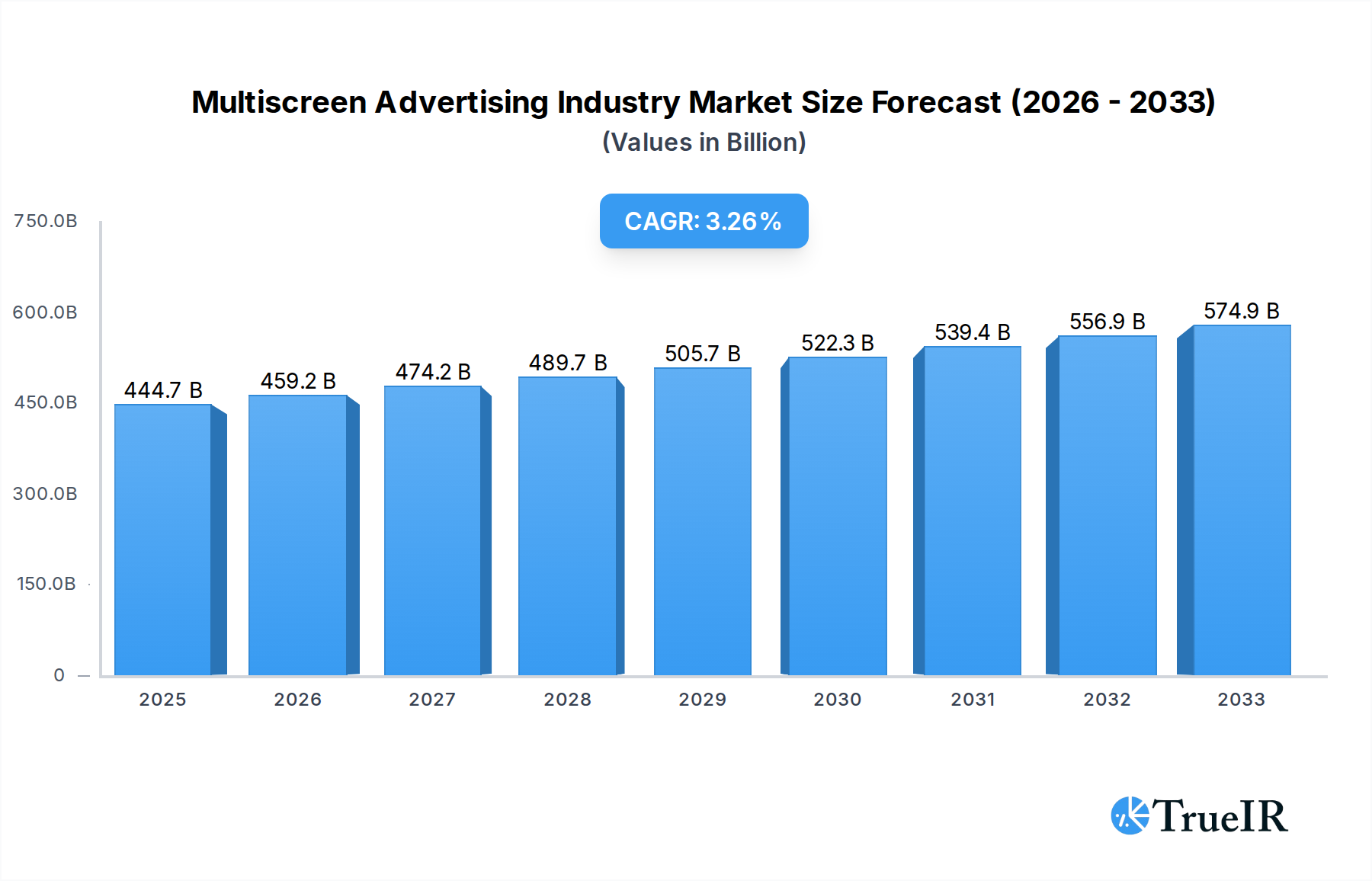

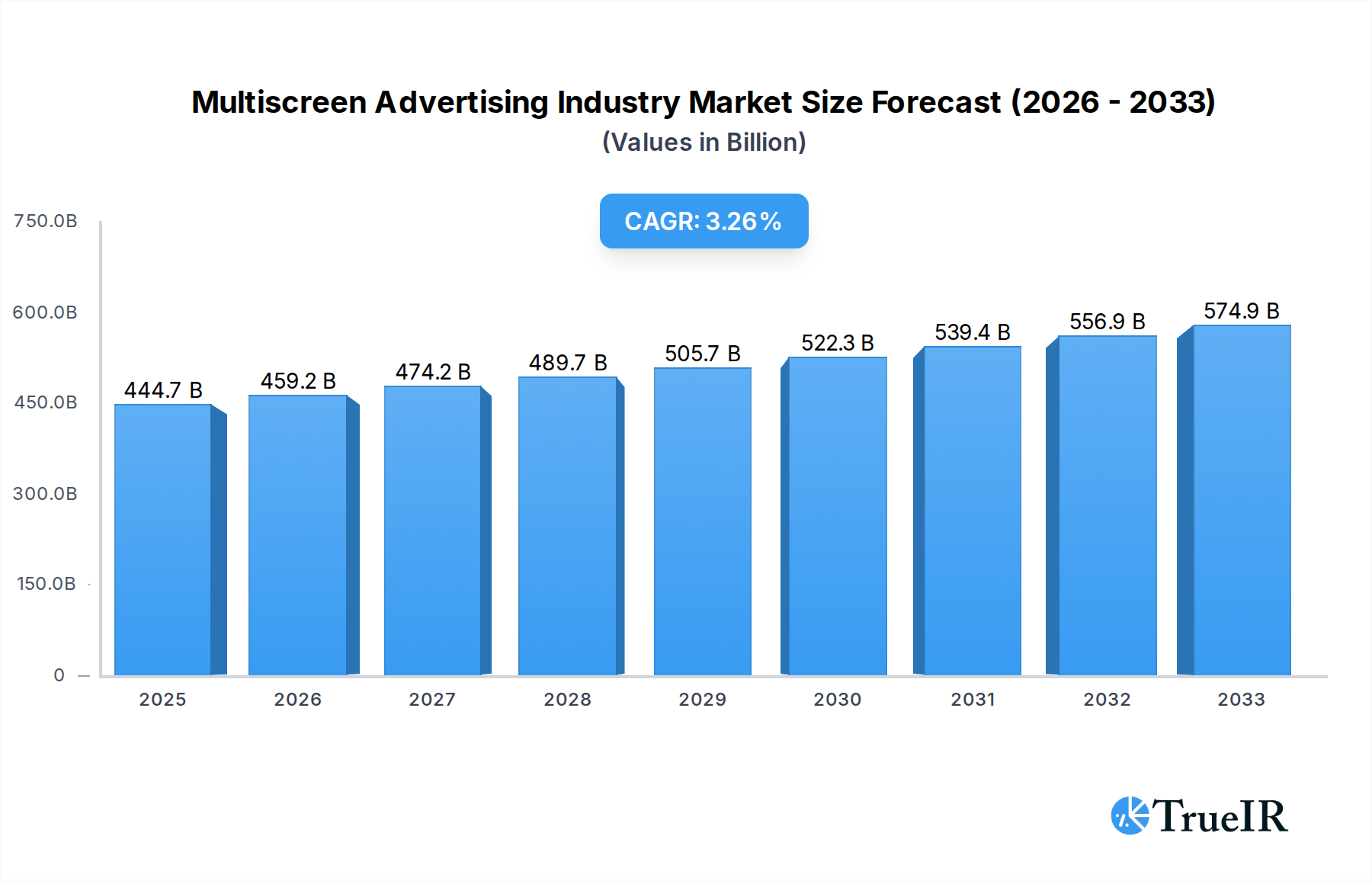

The Multiscreen Advertising Industry is poised for robust growth, projecting a market size of $444.7 billion in 2025, with an anticipated Compound Annual Growth Rate (CAGR) of 3.8% throughout the forecast period of 2025-2033. This significant expansion is primarily driven by the escalating adoption of diverse digital devices and the increasing consumer engagement across multiple screens. The shift in advertising spend towards digital platforms, coupled with the ability of multiscreen advertising to offer personalized and targeted campaigns, is a key catalyst. Advancements in programmatic advertising and the growing sophistication of data analytics enable advertisers to reach specific audiences with greater precision, optimizing ad spend and improving return on investment. Furthermore, the rise of connected TV (CTV) advertising, which bridges the gap between traditional television and digital video, is a major contributor to this market's dynamism. The integration of AI and machine learning in ad delivery and optimization is also expected to fuel innovation and efficiency.

Multiscreen Advertising Industry Market Size (In Billion)

The industry landscape is characterized by a dynamic interplay of trends and challenges. Key trends include the burgeoning demand for interactive and dynamic ad formats that foster higher engagement, and the increasing reliance on mobile devices as primary content consumption platforms. Gaming consoles are also emerging as a significant advertising touchpoint. While the market is expanding, certain restraints, such as increasing ad fatigue among consumers and the complexities of cross-platform measurement and attribution, need to be addressed. However, the persistent innovation in ad technologies and the continuous evolution of consumer viewing habits are expected to outweigh these challenges. Leading companies like Verizon Wireless, Orange SA, Netflix Inc., Vodafone Group PLC, Alphabet Inc., NTT DoCoMo Inc., Microsoft Corporation, Roku Inc., Sky Mobile, and AT&T Inc. are actively shaping the market through strategic investments in technology and content, aiming to capture a larger share of this rapidly evolving advertising ecosystem.

Multiscreen Advertising Industry Company Market Share

Multiscreen Advertising Industry: Market Intelligence & Future Projections (2019–2033)

This comprehensive report delves into the dynamic Multiscreen Advertising Industry, offering in-depth analysis of market structure, trends, opportunities, dominant segments, and future outlook. With a study period spanning from 2019 to 2033, this report provides critical insights for stakeholders seeking to navigate this rapidly evolving landscape. Our base year is 2025, with an estimated year also at 2025, and a robust forecast period extending from 2025 to 2033, building upon the historical period of 2019–2024. We project the global multiscreen advertising market to reach a colossal $1,500 billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of 15%.

Multiscreen Advertising Industry Market Structure & Competitive Landscape

The multiscreen advertising market is characterized by a moderately concentrated structure, driven by significant innovation and increasing regulatory oversight. Key innovation drivers include the rapid adoption of programmatic advertising technologies, the proliferation of connected devices, and advancements in data analytics for hyper-targeted campaigns. Regulatory impacts are becoming more pronounced, with privacy-centric legislation like GDPR and CCPA influencing data collection and ad personalization strategies, potentially affecting advertising spend. Product substitutes, such as traditional linear TV advertising and pure-play digital ad networks, are increasingly being integrated or challenged by multiscreen solutions. End-user segmentation is diverse, encompassing advertisers, agencies, publishers, and technology providers, each with distinct needs and engagement models. Mergers and acquisitions (M&A) are a significant trend, with an estimated 250+ M&A deals valued at over $100 billion occurring during the historical period, driven by the pursuit of market consolidation, technological synergy, and expanded reach. Key players are actively acquiring smaller ad-tech firms to bolster their capabilities in areas like AI-driven ad optimization and cross-device tracking.

Multiscreen Advertising Industry Market Trends & Opportunities

The multiscreen advertising market is poised for exponential growth, driven by a confluence of technological advancements, evolving consumer behaviors, and a burgeoning digital economy. The global market size, projected to exceed $1,500 billion by 2033, is experiencing a significant CAGR of 15%. This surge is fueled by the increasing penetration of high-speed internet and the widespread ownership of multiple internet-connected devices, creating a ubiquitous advertising environment. Technological shifts, such as the rise of AI-powered ad buying platforms, the maturation of addressable TV, and the integration of augmented reality (AR) and virtual reality (VR) into advertising experiences, are transforming how brands connect with consumers. Consumer preferences are increasingly leaning towards personalized and non-intrusive advertising. Viewers expect relevant content delivered seamlessly across their chosen devices, leading to a demand for dynamic and interactive ad formats that offer a more engaging experience. The competitive dynamics are intensifying, with established media giants and agile tech companies vying for market share. Opportunities abound for companies that can offer robust cross-device attribution, enhance user privacy compliance, and develop innovative ad formats that capture audience attention in an increasingly fragmented media landscape. The growth in connected TV (CTV) advertising, alone, is expected to contribute over $100 billion to the market by 2030, underscoring its significance. Furthermore, the increasing reliance on mobile advertising, projected to capture over 60% of the digital ad spend by 2028, presents a substantial growth avenue. The adoption of programmatic advertising, which currently accounts for over 80% of digital ad spend, continues to streamline ad buying and selling processes, creating efficiency and scalability. The integration of influencer marketing with multiscreen strategies also offers a promising avenue for engagement, with projections indicating a market value of over $50 billion by 2027. The demand for data-driven insights and analytics to optimize ad campaigns across multiple screens is also a major trend, creating opportunities for specialized analytics providers. The evolving landscape of gaming consoles as advertising platforms, with an estimated 500 million active users worldwide, opens up new frontiers for immersive advertising experiences. The development of unified identity solutions to overcome cookie deprecation challenges is another critical trend, with significant investment flowing into this area. The shift from broad-reach campaigns to hyper-personalized, contextually relevant advertising across all screens represents a fundamental change in advertiser strategy. The growth in over-the-top (OTT) advertising is another key trend, as consumers increasingly cut the cord from traditional cable services. The potential for interactive advertising, allowing viewers to directly engage with ads, is also a significant opportunity for enhancing campaign effectiveness. The expansion of emerging markets, particularly in Asia-Pacific and Latin America, is expected to contribute significantly to the overall growth of the multiscreen advertising market.

Dominant Markets & Segments in Multiscreen Advertising Industry

The Multiscreen Advertising Industry exhibits robust growth across several key segments, with the Mobile/Tablet platform currently dominating, projected to account for over 50% of the total market share by 2025, valued at approximately $750 billion. This dominance is propelled by the ubiquitous nature of smartphones and tablets, coupled with the high engagement rates these devices command. Infrastructure development, including widespread 5G network deployment and improved mobile internet penetration, significantly bolsters this segment's growth. Supportive government policies promoting digital adoption and e-commerce further fuel mobile advertising spend.

- Mobile/Tablet:

- Key Growth Drivers: High smartphone penetration globally, increasing mobile internet usage, surge in mobile commerce, and the effectiveness of location-based advertising.

- Detailed Analysis: Mobile devices have become the primary touchpoint for content consumption for a significant portion of the global population. Advertisers are leveraging this by investing heavily in mobile-first strategies, including in-app advertising, mobile web banners, and video ads optimized for smaller screens. The ability to target users based on their location, app usage, and browsing history makes mobile advertising exceptionally effective and attractive to advertisers.

The Television platform, particularly Connected TV (CTV), is emerging as a strong contender, expected to capture 25% of the market by 2025, valued at around $375 billion. This growth is attributed to the increasing adoption of smart TVs and streaming devices, offering advertisers the reach of television with the targeting capabilities of digital advertising.

- Television (CTV):

- Key Growth Drivers: Rise of Smart TVs and streaming devices (e.g., Roku, Amazon Fire TV), increasing cord-cutting trends, and the ability to deliver addressable advertising to households.

- Detailed Analysis: CTV offers a premium viewing experience with larger screens and higher engagement. Advertisers are shifting budgets from traditional linear TV to CTV to reach specific demographics and households with personalized ads. The development of advanced ad formats for CTV, such as shoppable ads and interactive overlays, is further enhancing its appeal.

In terms of Type of Content, Dynamic advertising, which allows for real-time personalization and adaptation of ad creatives, is gaining significant traction, projected to constitute 40% of the market by 2025, valued at $600 billion.

- Dynamic Content:

- Key Growth Drivers: AI and machine learning advancements enabling real-time creative optimization, growing demand for personalized user experiences, and improved data integration capabilities.

- Detailed Analysis: Dynamic advertising leverages data to tailor ad messages and visuals to individual users or audience segments. This personalization leads to higher engagement rates, improved conversion rates, and a more efficient allocation of advertising budgets. The ability to test and iterate on ad creatives in real-time provides a significant competitive advantage.

Desktop/Laptop advertising continues to be a significant segment, holding an estimated 20% market share by 2025, valued at $300 billion. While its growth rate might be slower compared to mobile, its established infrastructure and high-value audience make it indispensable for many campaigns.

- Desktop/Laptop:

- Key Growth Drivers: Continued importance for professional and in-depth content consumption, effective for lead generation and complex product/service promotion, and strong programmatic ad buying capabilities.

- Detailed Analysis: Desktops and laptops remain crucial for tasks requiring larger screens and more processing power, such as detailed research, online learning, and complex work-related activities. Advertisers utilize these platforms for campaigns requiring more information delivery and higher conversion rates, particularly in B2B sectors.

Interactive content, while currently a smaller segment at approximately 5% market share (valued at $75 billion in 2025), holds immense future potential as technology advances and consumer willingness to engage with ads increases.

- Interactive Content:

- Key Growth Drivers: Growing consumer desire for engaging and participatory experiences, advancements in AR/VR, and the development of gamified advertising.

- Detailed Analysis: Interactive ads move beyond passive viewing, inviting users to click, swipe, play, or even manipulate the ad itself. This level of engagement fosters deeper brand recall and can significantly impact consumer decision-making. As AR and VR technologies become more accessible, interactive multiscreen advertising is expected to see substantial growth.

Gaming Consoles represent an emerging platform, estimated to hold a 0.5% market share (valued at $7.5 billion in 2025), but with a rapidly expanding user base and innovative advertising opportunities.

- Gaming Consoles:

- Key Growth Drivers: Growing adoption of gaming consoles as entertainment hubs, increasing integration of advertising within game environments, and potential for immersive brand experiences.

- Detailed Analysis: The massive and engaged audience on gaming consoles presents a unique advertising opportunity. Advertisers can explore in-game billboards, branded virtual items, playable ad units, and sponsored content within gaming ecosystems, reaching a highly targeted and interactive demographic.

Multiscreen Advertising Industry Product Analysis

The multiscreen advertising industry is defined by continuous product innovation, focusing on enhancing ad delivery, targeting accuracy, and user engagement across diverse devices. Key product innovations include AI-powered programmatic platforms that optimize ad spend in real-time, advanced cross-device tracking solutions to ensure campaign continuity, and the development of interactive ad formats such as playable ads and AR filters. These advancements offer significant competitive advantages by improving return on ad spend (ROAS), enabling hyper-personalization, and creating more memorable brand experiences. The seamless integration of data from various touchpoints is crucial for delivering relevant ads, maximizing market fit.

Key Drivers, Barriers & Challenges in Multiscreen Advertising Industry

Key Drivers: The multiscreen advertising market is propelled by several key forces. The pervasive adoption of smartphones and connected devices fuels the demand for cross-platform advertising solutions. Technological advancements, particularly in AI and machine learning, enable sophisticated audience segmentation and ad personalization, enhancing campaign effectiveness. The increasing shift of consumer attention to digital platforms, including streaming services and social media, drives advertising budgets towards multiscreen strategies. Furthermore, the development of programmatic advertising technologies streamlines ad buying and selling, increasing efficiency and scalability. The burgeoning e-commerce sector also necessitates integrated advertising approaches across devices to guide consumers through the purchase funnel.

Barriers & Challenges: Despite its growth, the multiscreen advertising industry faces significant challenges. Regulatory complexities, especially concerning data privacy (e.g., GDPR, CCPA), impose stringent limitations on data collection and usage, impacting personalization capabilities. Supply chain issues, particularly in the ad-tech ecosystem, can lead to inefficiencies and transparency concerns. Competitive pressures from a fragmented market with numerous players can make differentiation challenging and drive down ad prices. Cross-device attribution remains a persistent hurdle, making it difficult for advertisers to accurately measure the true impact of their campaigns across different screens. Cookie deprecation by major browsers presents a substantial challenge to third-party tracking and targeting. The ongoing fight against ad fraud, which costs the industry billions annually, erodes advertiser trust and campaign efficacy. Maintaining consumer privacy while delivering personalized ads requires a delicate balance, and missteps can lead to significant backlash. The fragmentation of inventory across numerous platforms and devices makes campaign management complex and resource-intensive.

Growth Drivers in the Multiscreen Advertising Industry Market

The growth of the multiscreen advertising market is primarily driven by the exponential increase in internet-connected devices globally, making it easier for consumers to access content across various screens. Technological advancements in areas like Artificial Intelligence (AI), Machine Learning (ML), and data analytics are enabling more sophisticated audience targeting, ad personalization, and campaign optimization. The widespread adoption of high-speed internet infrastructure, including 5G, facilitates the seamless delivery of rich media and video content across all devices. Furthermore, the growing trend of cord-cutting and the rise of over-the-top (OTT) streaming services are shifting advertising budgets towards digital and multiscreen solutions. Economic factors, such as increased advertiser spending on performance-based marketing, also contribute significantly to market expansion.

Challenges Impacting Multiscreen Advertising Industry Growth

The multiscreen advertising industry faces several significant challenges that can impede its growth trajectory. Increasing regulatory scrutiny around data privacy and consumer protection, exemplified by regulations like GDPR and CCPA, imposes limitations on data collection and usage, affecting personalization strategies. Ad fraud remains a pervasive issue, leading to wasted ad spend and eroding advertiser trust in the digital ecosystem, with estimated annual losses in the tens of billions. Fragmented user identity across multiple devices makes accurate cross-device attribution and targeting a complex endeavor. The deprecation of third-party cookies by major browsers presents a substantial obstacle to traditional tracking and targeting methods, necessitating the development of alternative solutions. Intense competition among a vast number of ad-tech providers and publishers can lead to pricing pressures and challenges in differentiating offerings.

Key Players Shaping the Multiscreen Advertising Industry Market

- Verizon Wireless

- Orange SA

- Netflix Inc

- Vodafone Group PLC

- Alphabet Inc

- NTT DoCoMo Inc

- Microsoft Corporation

- Roku Inc

- Sky Mobile

- AT&T Inc

Significant Multiscreen Advertising Industry Industry Milestones

- 2019: Widespread adoption of programmatic advertising on mobile devices, reaching over 60% of mobile ad spend.

- 2020: Significant surge in Connected TV (CTV) advertising investment due to increased streaming consumption during global events.

- 2021: Introduction of advanced AI-powered real-time bidding (RTB) platforms, optimizing ad delivery and pricing across screens.

- 2022: Growing emphasis on privacy-centric advertising solutions following stricter data privacy regulations and browser changes.

- 2023: Major advancements in cross-device identification technologies to address the challenges of user tracking.

- 2024: Increased integration of Augmented Reality (AR) and Virtual Reality (VR) into multiscreen advertising campaigns, creating immersive brand experiences.

Future Outlook for Multiscreen Advertising Industry Market

The future outlook for the Multiscreen Advertising Industry is exceptionally promising, driven by continuous technological innovation and evolving consumer behaviors. The projected growth trajectory indicates a market that will exceed $1,500 billion by 2033. Key growth catalysts include the ongoing expansion of 5G networks, enabling richer and more interactive ad experiences across all devices. The maturation of AI and machine learning will further enhance personalization and targeting capabilities, leading to more effective campaigns. The increasing adoption of CTV and gaming consoles as advertising platforms presents new avenues for reaching engaged audiences. Strategic opportunities lie in developing robust privacy-compliant advertising solutions, enhancing cross-device measurement capabilities, and pioneering innovative ad formats that capture user attention. The market potential is vast, with a significant focus on data integration, audience intelligence, and delivering measurable business outcomes for advertisers.

Multiscreen Advertising Industry Segmentation

-

1. Type of Content

- 1.1. Static

- 1.2. Dynamic

- 1.3. Interactive

-

2. Platform

- 2.1. Television

- 2.2. Desktop/Laptop

- 2.3. Mobile/Tablet

- 2.4. Gaming Consoles

- 2.5. Other Platforms

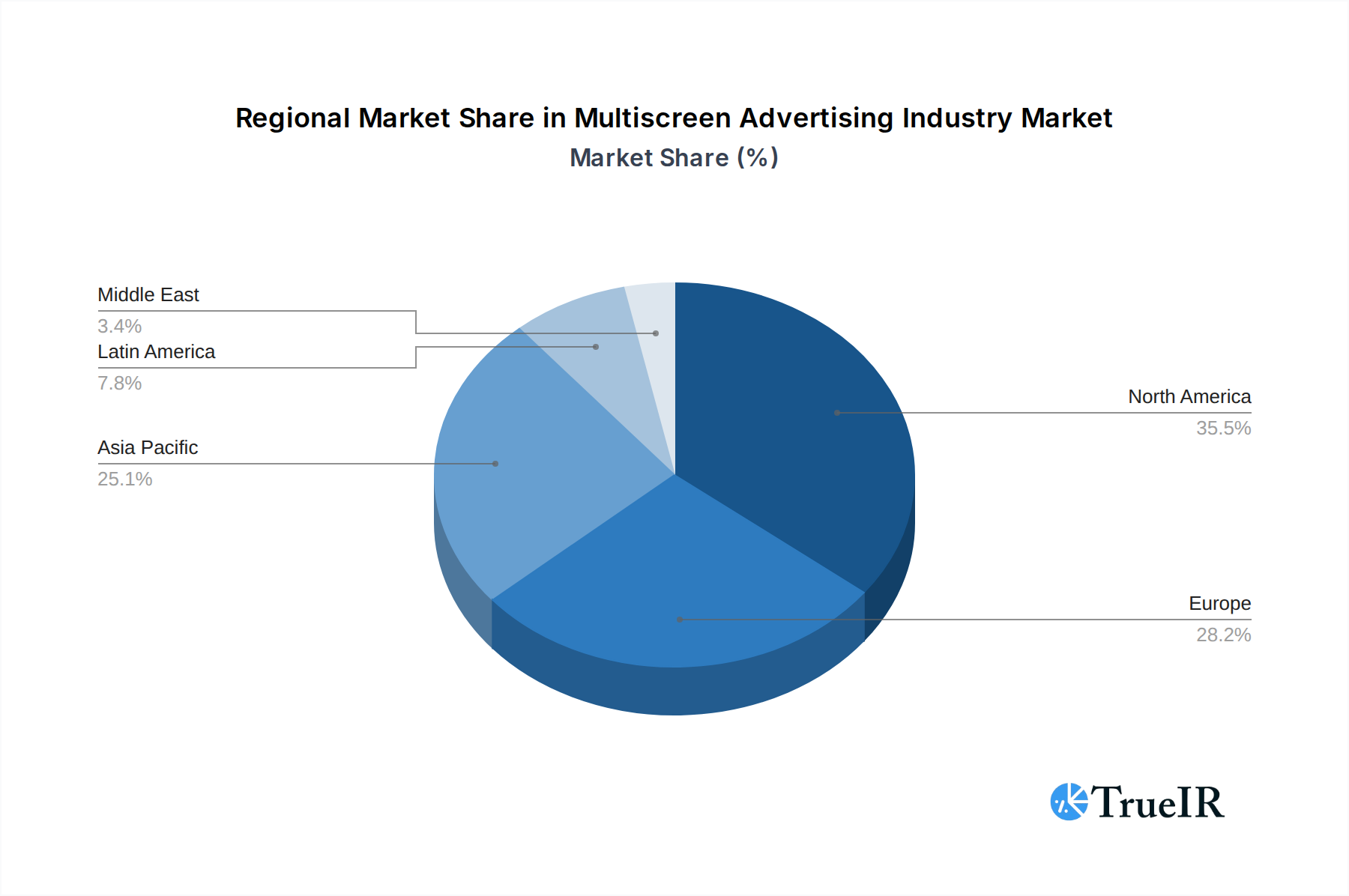

Multiscreen Advertising Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East

Multiscreen Advertising Industry Regional Market Share

Geographic Coverage of Multiscreen Advertising Industry

Multiscreen Advertising Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type of Content

- 5.1.1. Static

- 5.1.2. Dynamic

- 5.1.3. Interactive

- 5.2. Market Analysis, Insights and Forecast - by Platform

- 5.2.1. Television

- 5.2.2. Desktop/Laptop

- 5.2.3. Mobile/Tablet

- 5.2.4. Gaming Consoles

- 5.2.5. Other Platforms

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Latin America

- 5.3.5. Middle East

- 5.1. Market Analysis, Insights and Forecast - by Type of Content

- 6. Global Multiscreen Advertising Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type of Content

- 6.1.1. Static

- 6.1.2. Dynamic

- 6.1.3. Interactive

- 6.2. Market Analysis, Insights and Forecast - by Platform

- 6.2.1. Television

- 6.2.2. Desktop/Laptop

- 6.2.3. Mobile/Tablet

- 6.2.4. Gaming Consoles

- 6.2.5. Other Platforms

- 6.1. Market Analysis, Insights and Forecast - by Type of Content

- 7. North America Multiscreen Advertising Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type of Content

- 7.1.1. Static

- 7.1.2. Dynamic

- 7.1.3. Interactive

- 7.2. Market Analysis, Insights and Forecast - by Platform

- 7.2.1. Television

- 7.2.2. Desktop/Laptop

- 7.2.3. Mobile/Tablet

- 7.2.4. Gaming Consoles

- 7.2.5. Other Platforms

- 7.1. Market Analysis, Insights and Forecast - by Type of Content

- 8. Europe Multiscreen Advertising Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type of Content

- 8.1.1. Static

- 8.1.2. Dynamic

- 8.1.3. Interactive

- 8.2. Market Analysis, Insights and Forecast - by Platform

- 8.2.1. Television

- 8.2.2. Desktop/Laptop

- 8.2.3. Mobile/Tablet

- 8.2.4. Gaming Consoles

- 8.2.5. Other Platforms

- 8.1. Market Analysis, Insights and Forecast - by Type of Content

- 9. Asia Pacific Multiscreen Advertising Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type of Content

- 9.1.1. Static

- 9.1.2. Dynamic

- 9.1.3. Interactive

- 9.2. Market Analysis, Insights and Forecast - by Platform

- 9.2.1. Television

- 9.2.2. Desktop/Laptop

- 9.2.3. Mobile/Tablet

- 9.2.4. Gaming Consoles

- 9.2.5. Other Platforms

- 9.1. Market Analysis, Insights and Forecast - by Type of Content

- 10. Latin America Multiscreen Advertising Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type of Content

- 10.1.1. Static

- 10.1.2. Dynamic

- 10.1.3. Interactive

- 10.2. Market Analysis, Insights and Forecast - by Platform

- 10.2.1. Television

- 10.2.2. Desktop/Laptop

- 10.2.3. Mobile/Tablet

- 10.2.4. Gaming Consoles

- 10.2.5. Other Platforms

- 10.1. Market Analysis, Insights and Forecast - by Type of Content

- 11. Middle East Multiscreen Advertising Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type of Content

- 11.1.1. Static

- 11.1.2. Dynamic

- 11.1.3. Interactive

- 11.2. Market Analysis, Insights and Forecast - by Platform

- 11.2.1. Television

- 11.2.2. Desktop/Laptop

- 11.2.3. Mobile/Tablet

- 11.2.4. Gaming Consoles

- 11.2.5. Other Platforms

- 11.1. Market Analysis, Insights and Forecast - by Type of Content

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Verizon Wireless

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Orange SA

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Netflix Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Vodafone Group PLC*List Not Exhaustive

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Alphabet Inc

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 NTT DoCoMo Inc

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Microsoft Corporation

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Roku Inc

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Sky Mobile

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 AT&T Inc

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Verizon Wireless

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Multiscreen Advertising Industry Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Multiscreen Advertising Industry Revenue (undefined), by Type of Content 2025 & 2033

- Figure 3: North America Multiscreen Advertising Industry Revenue Share (%), by Type of Content 2025 & 2033

- Figure 4: North America Multiscreen Advertising Industry Revenue (undefined), by Platform 2025 & 2033

- Figure 5: North America Multiscreen Advertising Industry Revenue Share (%), by Platform 2025 & 2033

- Figure 6: North America Multiscreen Advertising Industry Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Multiscreen Advertising Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Multiscreen Advertising Industry Revenue (undefined), by Type of Content 2025 & 2033

- Figure 9: Europe Multiscreen Advertising Industry Revenue Share (%), by Type of Content 2025 & 2033

- Figure 10: Europe Multiscreen Advertising Industry Revenue (undefined), by Platform 2025 & 2033

- Figure 11: Europe Multiscreen Advertising Industry Revenue Share (%), by Platform 2025 & 2033

- Figure 12: Europe Multiscreen Advertising Industry Revenue (undefined), by Country 2025 & 2033

- Figure 13: Europe Multiscreen Advertising Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Multiscreen Advertising Industry Revenue (undefined), by Type of Content 2025 & 2033

- Figure 15: Asia Pacific Multiscreen Advertising Industry Revenue Share (%), by Type of Content 2025 & 2033

- Figure 16: Asia Pacific Multiscreen Advertising Industry Revenue (undefined), by Platform 2025 & 2033

- Figure 17: Asia Pacific Multiscreen Advertising Industry Revenue Share (%), by Platform 2025 & 2033

- Figure 18: Asia Pacific Multiscreen Advertising Industry Revenue (undefined), by Country 2025 & 2033

- Figure 19: Asia Pacific Multiscreen Advertising Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Latin America Multiscreen Advertising Industry Revenue (undefined), by Type of Content 2025 & 2033

- Figure 21: Latin America Multiscreen Advertising Industry Revenue Share (%), by Type of Content 2025 & 2033

- Figure 22: Latin America Multiscreen Advertising Industry Revenue (undefined), by Platform 2025 & 2033

- Figure 23: Latin America Multiscreen Advertising Industry Revenue Share (%), by Platform 2025 & 2033

- Figure 24: Latin America Multiscreen Advertising Industry Revenue (undefined), by Country 2025 & 2033

- Figure 25: Latin America Multiscreen Advertising Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East Multiscreen Advertising Industry Revenue (undefined), by Type of Content 2025 & 2033

- Figure 27: Middle East Multiscreen Advertising Industry Revenue Share (%), by Type of Content 2025 & 2033

- Figure 28: Middle East Multiscreen Advertising Industry Revenue (undefined), by Platform 2025 & 2033

- Figure 29: Middle East Multiscreen Advertising Industry Revenue Share (%), by Platform 2025 & 2033

- Figure 30: Middle East Multiscreen Advertising Industry Revenue (undefined), by Country 2025 & 2033

- Figure 31: Middle East Multiscreen Advertising Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Multiscreen Advertising Industry Revenue undefined Forecast, by Type of Content 2020 & 2033

- Table 2: Global Multiscreen Advertising Industry Revenue undefined Forecast, by Platform 2020 & 2033

- Table 3: Global Multiscreen Advertising Industry Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Multiscreen Advertising Industry Revenue undefined Forecast, by Type of Content 2020 & 2033

- Table 5: Global Multiscreen Advertising Industry Revenue undefined Forecast, by Platform 2020 & 2033

- Table 6: Global Multiscreen Advertising Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: Global Multiscreen Advertising Industry Revenue undefined Forecast, by Type of Content 2020 & 2033

- Table 8: Global Multiscreen Advertising Industry Revenue undefined Forecast, by Platform 2020 & 2033

- Table 9: Global Multiscreen Advertising Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 10: Global Multiscreen Advertising Industry Revenue undefined Forecast, by Type of Content 2020 & 2033

- Table 11: Global Multiscreen Advertising Industry Revenue undefined Forecast, by Platform 2020 & 2033

- Table 12: Global Multiscreen Advertising Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Global Multiscreen Advertising Industry Revenue undefined Forecast, by Type of Content 2020 & 2033

- Table 14: Global Multiscreen Advertising Industry Revenue undefined Forecast, by Platform 2020 & 2033

- Table 15: Global Multiscreen Advertising Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 16: Global Multiscreen Advertising Industry Revenue undefined Forecast, by Type of Content 2020 & 2033

- Table 17: Global Multiscreen Advertising Industry Revenue undefined Forecast, by Platform 2020 & 2033

- Table 18: Global Multiscreen Advertising Industry Revenue undefined Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Multiscreen Advertising Industry?

The projected CAGR is approximately 3.8%.

2. Which companies are prominent players in the Multiscreen Advertising Industry?

Key companies in the market include Verizon Wireless, Orange SA, Netflix Inc, Vodafone Group PLC*List Not Exhaustive, Alphabet Inc, NTT DoCoMo Inc, Microsoft Corporation, Roku Inc, Sky Mobile, AT&T Inc.

3. What are the main segments of the Multiscreen Advertising Industry?

The market segments include Type of Content, Platform.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

; Shifting Trends Towards Mobile Media Consumption; Ability to Target Relevant or Personalized Ads.

6. What are the notable trends driving market growth?

Mobile/Tablet Segment to Hold Significant Market Share.

7. Are there any restraints impacting market growth?

; Intrusive Nature of Ads on User Experience; Rising Adoption of Ad-blockers on Devices.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Multiscreen Advertising Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Multiscreen Advertising Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Multiscreen Advertising Industry?

To stay informed about further developments, trends, and reports in the Multiscreen Advertising Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence