Key Insights

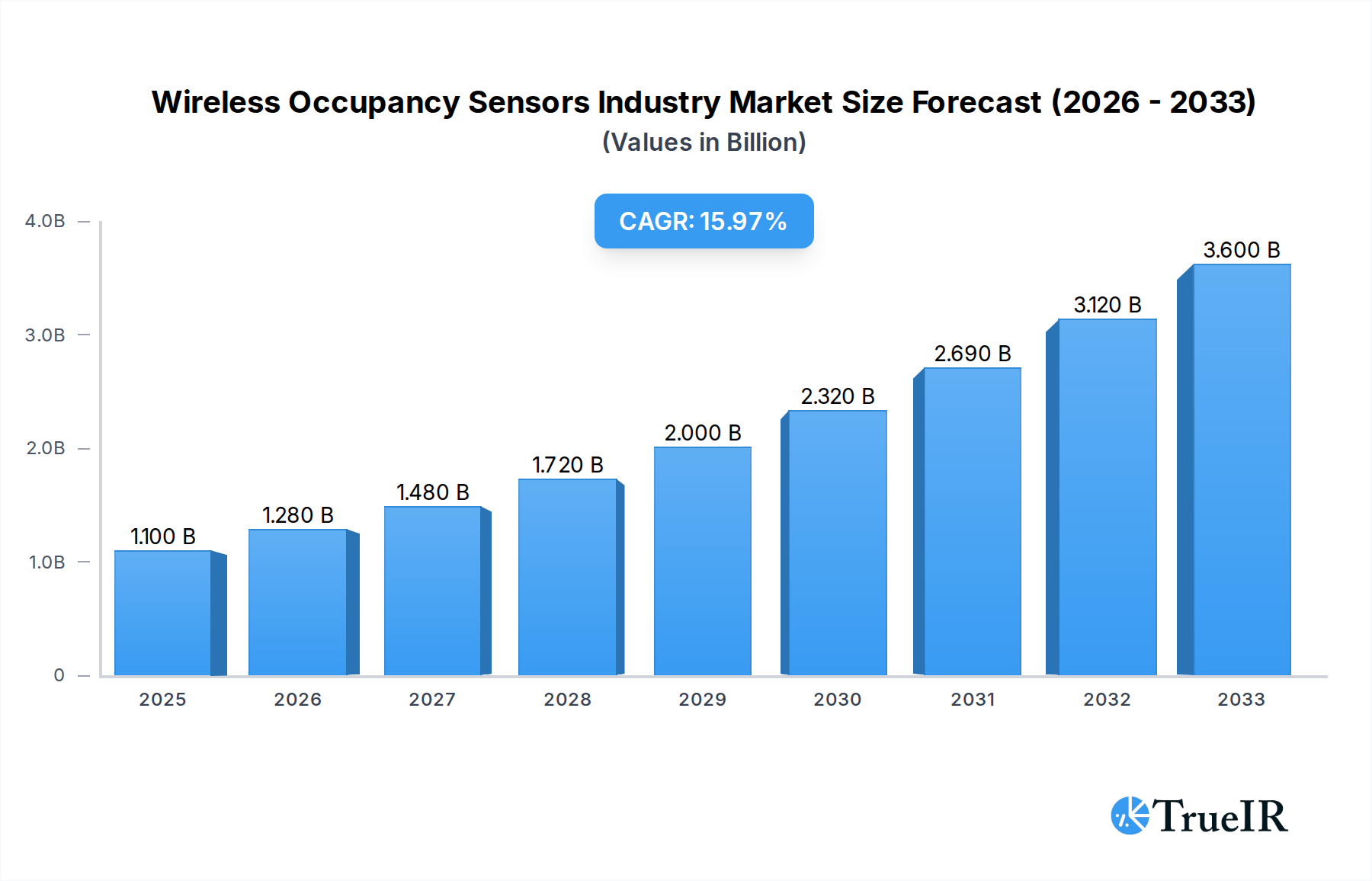

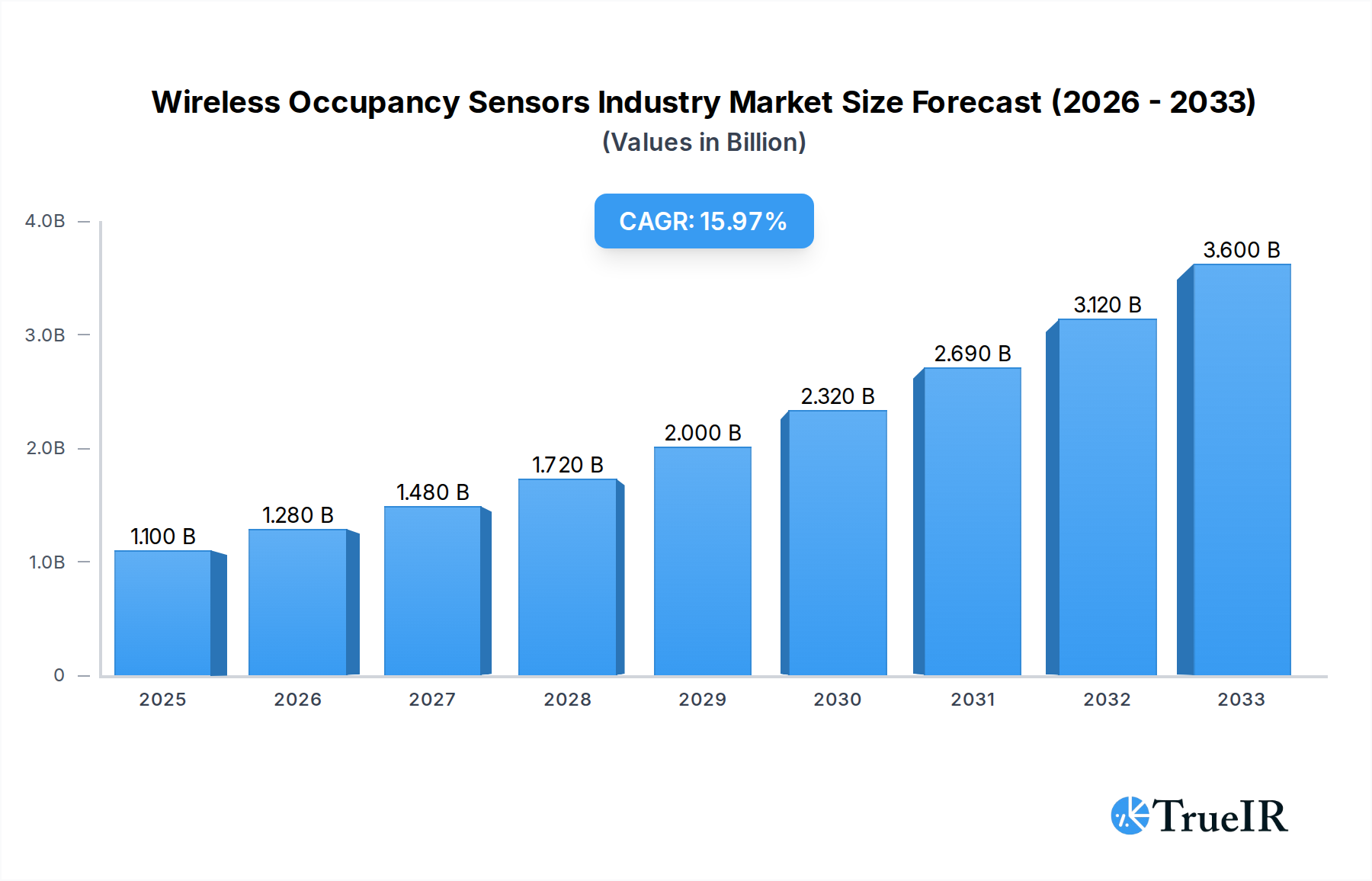

The global Wireless Occupancy Sensors market is poised for significant expansion, projected to reach USD 1.1 billion in 2025 and surge to an impressive USD 3.0 billion by 2033, driven by a remarkable Compound Annual Growth Rate (CAGR) of 15.9% during the forecast period of 2025-2033. This robust growth is underpinned by several key factors. The increasing demand for energy efficiency and cost savings in buildings is a primary catalyst, as occupancy sensors optimize lighting and HVAC systems, thereby reducing energy consumption. Furthermore, the growing adoption of smart home and building automation technologies fuels the market, with wireless sensors offering seamless integration and enhanced control. The expansion of the Internet of Things (IoT) ecosystem and advancements in sensor technology, including improved accuracy and longer battery life, also contribute to market momentum. The versatility of wireless occupancy sensors across various applications such as lighting control, HVAC management, and security surveillance, coupled with their deployment in diverse building types like residential, commercial, and industrial facilities, further solidifies their market penetration.

Wireless Occupancy Sensors Industry Market Size (In Billion)

The market dynamics are further shaped by evolving trends and strategic initiatives by key players. The increasing focus on sustainable building practices and stringent government regulations mandating energy conservation are creating a favorable environment for wireless occupancy sensors. Innovations in sensor technology, such as the integration of artificial intelligence for more sophisticated occupancy detection and behavioral analysis, are expected to drive future growth. The expansion of smart cities initiatives and the increasing demand for intelligent building management systems will also be significant growth drivers. While the market exhibits strong growth potential, certain restraints like the initial cost of implementation for some advanced systems and potential concerns regarding wireless network security might pose challenges. However, the overall outlook remains highly positive, with continuous technological advancements and increasing awareness of the benefits of occupancy sensing technology expected to overcome these hurdles. The competitive landscape features prominent companies investing in research and development to enhance product offerings and expand their global reach.

Wireless Occupancy Sensors Industry Company Market Share

This in-depth market research report provides a comprehensive analysis of the global Wireless Occupancy Sensors Industry. Covering the historical period from 2019 to 2024 and a robust forecast period extending to 2033, with a base and estimated year of 2025, this report is an essential resource for stakeholders seeking to understand market dynamics, identify growth opportunities, and navigate competitive landscapes. The study leverages high-volume keywords to ensure optimal SEO performance, driving visibility and engagement within the industry.

Wireless Occupancy Sensors Industry Market Structure & Competitive Landscape

The Wireless Occupancy Sensors Industry exhibits a moderately concentrated market structure, with a blend of established multinational corporations and emerging players vying for market share. Innovation remains a critical driver, fueled by the increasing demand for smart building technologies, energy efficiency solutions, and enhanced security. Regulatory impacts, particularly concerning energy conservation mandates and data privacy, are shaping product development and market access. While direct substitutes for occupancy sensing are limited, integrated smart building systems and manual control methods represent indirect competition. The end-user segmentation is diverse, spanning residential, commercial, and industrial sectors, each with unique adoption drivers. Mergers and acquisitions (M&A) have been a consistent feature of the landscape, with an estimated volume of XX billion USD in M&A deals observed over the historical period, driven by the pursuit of technological synergies, market expansion, and consolidated product portfolios. Concentration ratios are estimated to be around XX% for the top 5 players.

Wireless Occupancy Sensors Industry Market Trends & Opportunities

The global Wireless Occupancy Sensors Industry is poised for significant expansion, driven by an escalating imperative for energy efficiency and smart building integration. The market size is projected to reach an impressive value of over $XX billion by 2033, with a compound annual growth rate (CAGR) of approximately XX% from the base year of 2025. Technological advancements, including the proliferation of the Internet of Things (IoT), enhanced sensor accuracy, and improved wireless communication protocols (e.g., Bluetooth Low Energy, Zigbee), are fundamentally reshaping product offerings and functionality. Consumer preferences are increasingly leaning towards automated and intelligent environments, where occupancy sensors play a pivotal role in optimizing lighting, HVAC, and security systems, thereby enhancing comfort and reducing operational costs. This shift is propelled by growing environmental awareness and the desire for sustainable living and working spaces. Competitive dynamics are characterized by intense product innovation, strategic partnerships, and a focus on delivering integrated solutions. Companies are investing heavily in research and development to create more sophisticated sensors capable of distinguishing between different occupancy patterns, integrating with advanced analytics, and offering seamless interoperability with other smart home and building devices. The market penetration rate for wireless occupancy sensors, particularly in new constructions and major renovations, is expected to accelerate rapidly, surpassing XX% in commercial buildings by 2030. Opportunities lie in catering to the growing demand for intelligent facility management, predictive maintenance, and personalized user experiences within buildings. The development of AI-powered occupancy analytics, enabling dynamic space utilization and energy management, presents a significant future growth avenue. Furthermore, the increasing adoption of these sensors in niche applications such as healthcare facilities for patient monitoring and in industrial settings for safety and efficiency optimization, underscores the expanding scope of the market. The ongoing digital transformation of various industries is a strong tailwind for the wireless occupancy sensors market, as businesses seek to leverage data for operational improvements and cost savings.

Dominant Markets & Segments in Wireless Occupancy Sensors Industry

The Commercial Buildings segment is a dominant force within the Wireless Occupancy Sensors Industry, driven by substantial investments in smart building infrastructure and stringent energy efficiency regulations. The Lighting Control application within this segment holds the largest market share, directly benefiting from the need to reduce electricity consumption and comply with building codes. Key growth drivers include government incentives for green building certifications like LEED and BREEAM, as well as the growing demand for enhanced occupant comfort and productivity. For instance, the widespread adoption of LED lighting, which pairs seamlessly with occupancy sensors for optimal energy savings, has significantly boosted this market.

Within the Commercial Buildings sector, the Lighting Control application is projected to maintain its leadership position throughout the forecast period, accounting for an estimated XX% of the total market revenue. This dominance is further amplified by the increasing adoption of advanced features such as daylight harvesting and task tuning, which are facilitated by intelligent occupancy sensing. The installation of wireless occupancy sensors in office spaces, retail environments, and educational institutions is a primary focus for market growth, as these applications offer significant potential for energy cost reduction.

The Residential Buildings segment is experiencing robust growth, propelled by the increasing consumer awareness of energy savings and the rising popularity of smart home ecosystems. The integration of wireless occupancy sensors into smart home hubs and platforms is a key trend, enabling automated control of lighting, heating, and cooling based on occupancy. Government initiatives promoting energy-efficient housing and the desire for convenience and comfort are further fueling this expansion.

The HVAC application, while currently trailing lighting control, is exhibiting a rapid growth trajectory. This is attributed to the significant energy savings achievable by optimizing heating and cooling systems based on actual occupancy, rather than fixed schedules. The ability of advanced wireless occupancy sensors to detect the presence and even count of individuals allows for more granular and precise control of HVAC systems, leading to substantial reductions in energy consumption and operational costs.

The Industrial end-user industry is emerging as a crucial growth segment, driven by the demand for enhanced safety, operational efficiency, and energy management in manufacturing plants and warehouses. Wireless occupancy sensors are being deployed to monitor worker presence in hazardous zones, optimize material flow, and reduce energy waste in large industrial spaces. The Aerospace & Defence sector, though a smaller segment, is showing increasing interest in occupancy sensing for secure facility management and optimized energy usage in sensitive areas.

The Healthcare sector presents significant opportunities, with occupancy sensors being utilized for patient room monitoring, staff presence detection, and optimizing energy consumption in hospitals and clinics. The growing emphasis on patient safety and operational efficiency in healthcare facilities is a key driver for adoption.

The Consumer Electronics segment, while not a direct end-user of the sensors themselves, influences the market through the demand for integrated smart home devices and platforms that incorporate occupancy sensing technology. The Other End-user Industries, including hospitality, government, and educational institutions, also contribute to the diversified demand for wireless occupancy sensors.

Wireless Occupancy Sensors Industry Product Analysis

Product innovation in the Wireless Occupancy Sensors Industry centers on enhancing accuracy, expanding connectivity, and integrating advanced intelligence. Technologies like passive infrared (PIR), ultrasonic, and dual-tech sensors are continuously refined for superior detection capabilities, reducing false triggers and improving energy savings. The integration of AI and machine learning algorithms allows sensors to learn occupancy patterns, predict usage, and provide actionable insights for building management. The competitive advantage lies in seamless integration with smart building platforms, offering a unified control experience and robust data analytics for optimized facility operations. Market-fit is driven by evolving demands for energy efficiency, occupant comfort, and enhanced security.

Key Drivers, Barriers & Challenges in Wireless Occupancy Sensors Industry

Key Drivers:

- Energy Efficiency Mandates: Government regulations and corporate sustainability goals are compelling adoption for reduced energy consumption.

- Smart Building Growth: The expansion of the Internet of Things (IoT) and smart building technologies creates a natural demand for occupancy sensing.

- Cost Savings: Optimized lighting and HVAC control lead to significant operational cost reductions.

- Technological Advancements: Improved sensor accuracy, wireless connectivity, and AI integration enhance functionality.

- Occupant Comfort & Productivity: Automated environments improve user experience and well-being.

Barriers & Challenges:

- Initial Installation Cost: The upfront investment for sensor deployment can be a barrier for some organizations.

- Integration Complexity: Ensuring seamless compatibility with existing building management systems can be challenging.

- Data Privacy Concerns: The collection of occupancy data raises privacy issues that need to be addressed through robust security protocols.

- Competition from Traditional Systems: Existing manual control systems and older technologies present a competitive inertia.

- Lack of Awareness: In some sectors, a lack of awareness regarding the benefits of wireless occupancy sensors can hinder adoption. Supply chain disruptions can also impact availability and pricing, with potential impacts on market growth estimated at xx% during periods of significant volatility.

Growth Drivers in the Wireless Occupancy Sensors Industry Market

The Wireless Occupancy Sensors Industry is propelled by a confluence of technological, economic, and regulatory factors. The relentless pursuit of energy efficiency, driven by global sustainability initiatives and rising energy costs, is a primary economic and regulatory driver. For instance, government incentives for green building certifications and stricter energy performance standards for buildings directly encourage the adoption of occupancy sensing solutions. Technologically, the maturation of IoT infrastructure, coupled with advancements in wireless communication protocols like BLE and Zigbee, makes deployment more feasible and cost-effective. The increasing demand for smart home automation and intelligent building management systems, which rely on real-time occupancy data for optimal control, further fuels growth.

Challenges Impacting Wireless Occupancy Sensors Industry Growth

Despite significant growth potential, the Wireless Occupancy Sensors Industry faces several challenges. The initial capital expenditure associated with deploying wireless sensor networks can be a deterrent, particularly for small and medium-sized enterprises or in older building retrofits where the return on investment may take longer to materialize. Integrating these sensors seamlessly with diverse and often legacy Building Management Systems (BMS) presents a technical hurdle, requiring expertise and potentially custom solutions. Furthermore, concerns surrounding data privacy and security, as occupancy data can reveal sensitive information about building usage patterns, necessitate robust encryption and compliance with data protection regulations. Competitive pressures from established players and the ongoing development of alternative sensing technologies also present a dynamic market environment. Supply chain vulnerabilities, as witnessed in recent global events, can also lead to component shortages and price fluctuations, impacting project timelines and profitability.

Key Players Shaping the Wireless Occupancy Sensors Industry Market

- Hubbell Incorporated

- Honeywell International Inc

- Legrand SA

- Leviton Manufacturing Co Inc

- Lutron Electronics Co Inc

- Eaton Corporation PLC

- Johnson Controls Inc

- Koninklijke Philips NV

- Schneider Electric

- Acuity Brands Inc

- General Electric Company

Significant Wireless Occupancy Sensors Industry Industry Milestones

- 2019: Increased adoption of Bluetooth Low Energy (BLE) in occupancy sensors, enabling lower power consumption and easier integration with smart devices.

- 2020: Growing demand for occupancy sensors in healthcare facilities for enhanced patient monitoring and resource management during the global pandemic.

- 2021: Advancements in dual-tech sensors combining PIR and ultrasonic technologies for improved accuracy and reduced false alarms.

- 2022: Introduction of AI-powered occupancy analytics platforms for advanced building performance optimization and space utilization insights.

- 2023: Escalating focus on cybersecurity for wireless occupancy sensor networks to address growing data privacy concerns.

- 2024: Enhanced integration of occupancy sensors with HVAC systems for significant energy savings and improved thermal comfort.

Future Outlook for Wireless Occupancy Sensors Industry Market

The future outlook for the Wireless Occupancy Sensors Industry is exceptionally bright, driven by the sustained demand for smart, energy-efficient, and automated buildings. Continued technological advancements, particularly in AI and machine learning, will lead to more intelligent and predictive sensing capabilities. The expansion of smart city initiatives and the increasing adoption of the Internet of Things will create new avenues for growth. Strategic collaborations between sensor manufacturers, smart building platform providers, and energy management companies will be crucial for delivering comprehensive solutions. Opportunities exist in developing highly specialized sensors for niche applications and in catering to the growing demand for retrofitting existing buildings with advanced occupancy sensing technology. The market is expected to witness further consolidation and innovation as companies strive to capture a larger share of this rapidly evolving sector.

Wireless Occupancy Sensors Industry Segmentation

-

1. Application

- 1.1. Lighting Control

- 1.2. HVAC

- 1.3. Security Surveillance

-

2. Building Type

- 2.1. Residential Buildings

- 2.2. Commercial Buildings

-

3. End-user Industry

- 3.1. Industrial

- 3.2. Aerospace & Defence

- 3.3. Healthcare

- 3.4. Consumer Electronics

- 3.5. Other End-user Industries

Wireless Occupancy Sensors Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. United Kingdom

- 2.2. France

- 2.3. Germany

- 2.4. Russia

- 2.5. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Rest of Asia Pacific

-

4. Latin America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Maxico

- 4.4. Rest of Latin America

- 5. Middle East

-

6. Saudi Arabia

- 6.1. United Arab Emirates

- 6.2. South Africa

- 6.3. Rest of Middle East

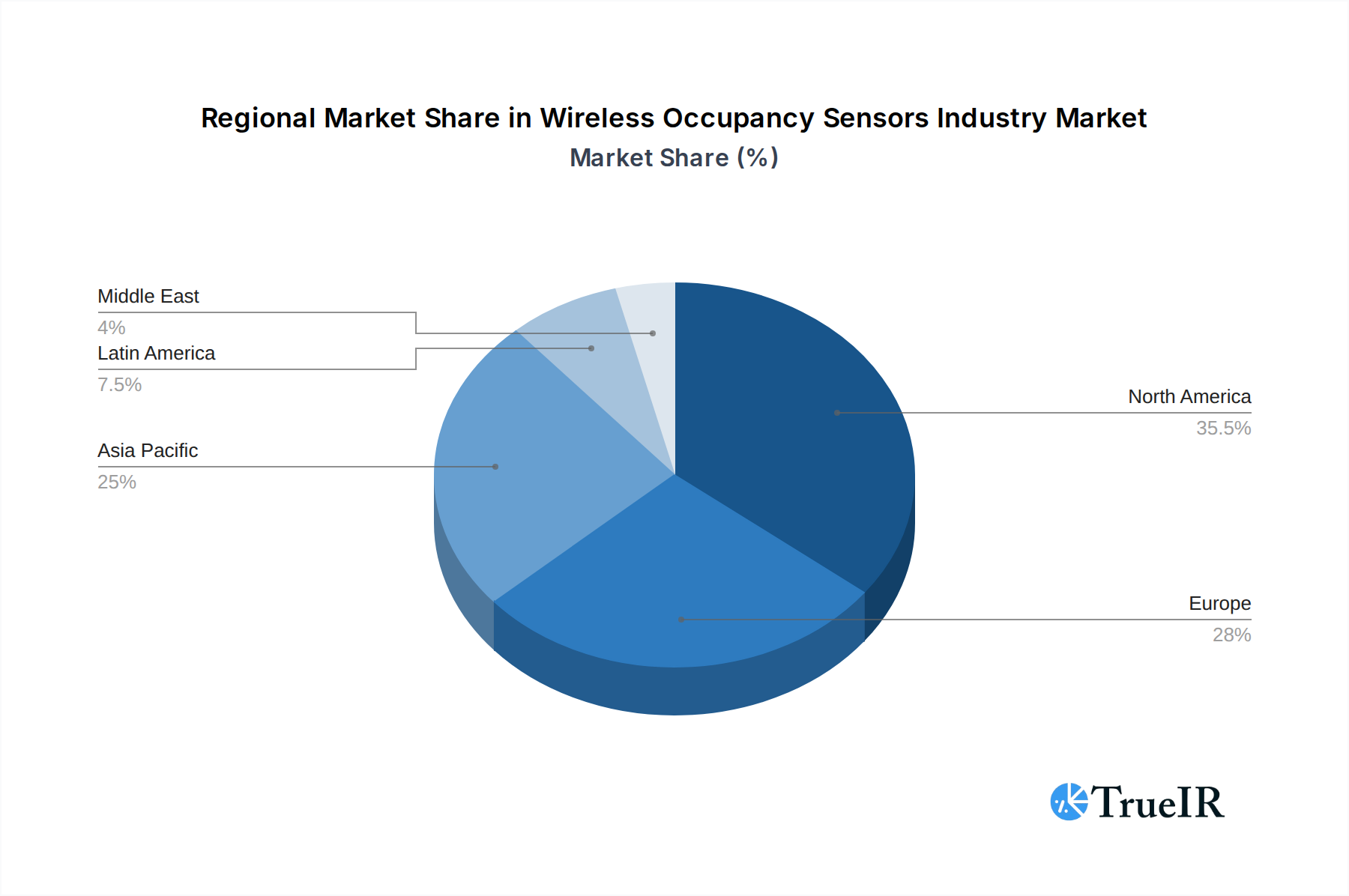

Wireless Occupancy Sensors Industry Regional Market Share

Geographic Coverage of Wireless Occupancy Sensors Industry

Wireless Occupancy Sensors Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 15.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Lighting Control

- 5.1.2. HVAC

- 5.1.3. Security Surveillance

- 5.2. Market Analysis, Insights and Forecast - by Building Type

- 5.2.1. Residential Buildings

- 5.2.2. Commercial Buildings

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. Industrial

- 5.3.2. Aerospace & Defence

- 5.3.3. Healthcare

- 5.3.4. Consumer Electronics

- 5.3.5. Other End-user Industries

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Latin America

- 5.4.5. Middle East

- 5.4.6. Saudi Arabia

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Wireless Occupancy Sensors Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Lighting Control

- 6.1.2. HVAC

- 6.1.3. Security Surveillance

- 6.2. Market Analysis, Insights and Forecast - by Building Type

- 6.2.1. Residential Buildings

- 6.2.2. Commercial Buildings

- 6.3. Market Analysis, Insights and Forecast - by End-user Industry

- 6.3.1. Industrial

- 6.3.2. Aerospace & Defence

- 6.3.3. Healthcare

- 6.3.4. Consumer Electronics

- 6.3.5. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Wireless Occupancy Sensors Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Lighting Control

- 7.1.2. HVAC

- 7.1.3. Security Surveillance

- 7.2. Market Analysis, Insights and Forecast - by Building Type

- 7.2.1. Residential Buildings

- 7.2.2. Commercial Buildings

- 7.3. Market Analysis, Insights and Forecast - by End-user Industry

- 7.3.1. Industrial

- 7.3.2. Aerospace & Defence

- 7.3.3. Healthcare

- 7.3.4. Consumer Electronics

- 7.3.5. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Wireless Occupancy Sensors Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Lighting Control

- 8.1.2. HVAC

- 8.1.3. Security Surveillance

- 8.2. Market Analysis, Insights and Forecast - by Building Type

- 8.2.1. Residential Buildings

- 8.2.2. Commercial Buildings

- 8.3. Market Analysis, Insights and Forecast - by End-user Industry

- 8.3.1. Industrial

- 8.3.2. Aerospace & Defence

- 8.3.3. Healthcare

- 8.3.4. Consumer Electronics

- 8.3.5. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Asia Pacific Wireless Occupancy Sensors Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Lighting Control

- 9.1.2. HVAC

- 9.1.3. Security Surveillance

- 9.2. Market Analysis, Insights and Forecast - by Building Type

- 9.2.1. Residential Buildings

- 9.2.2. Commercial Buildings

- 9.3. Market Analysis, Insights and Forecast - by End-user Industry

- 9.3.1. Industrial

- 9.3.2. Aerospace & Defence

- 9.3.3. Healthcare

- 9.3.4. Consumer Electronics

- 9.3.5. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Latin America Wireless Occupancy Sensors Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Lighting Control

- 10.1.2. HVAC

- 10.1.3. Security Surveillance

- 10.2. Market Analysis, Insights and Forecast - by Building Type

- 10.2.1. Residential Buildings

- 10.2.2. Commercial Buildings

- 10.3. Market Analysis, Insights and Forecast - by End-user Industry

- 10.3.1. Industrial

- 10.3.2. Aerospace & Defence

- 10.3.3. Healthcare

- 10.3.4. Consumer Electronics

- 10.3.5. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Middle East Wireless Occupancy Sensors Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Lighting Control

- 11.1.2. HVAC

- 11.1.3. Security Surveillance

- 11.2. Market Analysis, Insights and Forecast - by Building Type

- 11.2.1. Residential Buildings

- 11.2.2. Commercial Buildings

- 11.3. Market Analysis, Insights and Forecast - by End-user Industry

- 11.3.1. Industrial

- 11.3.2. Aerospace & Defence

- 11.3.3. Healthcare

- 11.3.4. Consumer Electronics

- 11.3.5. Other End-user Industries

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Saudi Arabia Wireless Occupancy Sensors Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Application

- 12.1.1. Lighting Control

- 12.1.2. HVAC

- 12.1.3. Security Surveillance

- 12.2. Market Analysis, Insights and Forecast - by Building Type

- 12.2.1. Residential Buildings

- 12.2.2. Commercial Buildings

- 12.3. Market Analysis, Insights and Forecast - by End-user Industry

- 12.3.1. Industrial

- 12.3.2. Aerospace & Defence

- 12.3.3. Healthcare

- 12.3.4. Consumer Electronics

- 12.3.5. Other End-user Industries

- 12.1. Market Analysis, Insights and Forecast - by Application

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 Hubbell Incorporated*List Not Exhaustive

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Honeywell International Inc

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Legrand SA

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 Leviton Manufacturing Co Inc

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 Lutron Electronics Co Inc

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 Eaton Corporation PLC

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 Johnson Controls Inc

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 Koninklijke Philips NV

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 Schneider Electric

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 Acuity Brands Inc

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.11 General Electric Company

- 13.1.11.1. Company Overview

- 13.1.11.2. Products

- 13.1.11.3. Company Financials

- 13.1.11.4. SWOT Analysis

- 13.1.1 Hubbell Incorporated*List Not Exhaustive

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Global Wireless Occupancy Sensors Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Wireless Occupancy Sensors Industry Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Wireless Occupancy Sensors Industry Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Wireless Occupancy Sensors Industry Revenue (billion), by Building Type 2025 & 2033

- Figure 5: North America Wireless Occupancy Sensors Industry Revenue Share (%), by Building Type 2025 & 2033

- Figure 6: North America Wireless Occupancy Sensors Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 7: North America Wireless Occupancy Sensors Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 8: North America Wireless Occupancy Sensors Industry Revenue (billion), by Country 2025 & 2033

- Figure 9: North America Wireless Occupancy Sensors Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Wireless Occupancy Sensors Industry Revenue (billion), by Application 2025 & 2033

- Figure 11: Europe Wireless Occupancy Sensors Industry Revenue Share (%), by Application 2025 & 2033

- Figure 12: Europe Wireless Occupancy Sensors Industry Revenue (billion), by Building Type 2025 & 2033

- Figure 13: Europe Wireless Occupancy Sensors Industry Revenue Share (%), by Building Type 2025 & 2033

- Figure 14: Europe Wireless Occupancy Sensors Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 15: Europe Wireless Occupancy Sensors Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 16: Europe Wireless Occupancy Sensors Industry Revenue (billion), by Country 2025 & 2033

- Figure 17: Europe Wireless Occupancy Sensors Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Wireless Occupancy Sensors Industry Revenue (billion), by Application 2025 & 2033

- Figure 19: Asia Pacific Wireless Occupancy Sensors Industry Revenue Share (%), by Application 2025 & 2033

- Figure 20: Asia Pacific Wireless Occupancy Sensors Industry Revenue (billion), by Building Type 2025 & 2033

- Figure 21: Asia Pacific Wireless Occupancy Sensors Industry Revenue Share (%), by Building Type 2025 & 2033

- Figure 22: Asia Pacific Wireless Occupancy Sensors Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 23: Asia Pacific Wireless Occupancy Sensors Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 24: Asia Pacific Wireless Occupancy Sensors Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Asia Pacific Wireless Occupancy Sensors Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Latin America Wireless Occupancy Sensors Industry Revenue (billion), by Application 2025 & 2033

- Figure 27: Latin America Wireless Occupancy Sensors Industry Revenue Share (%), by Application 2025 & 2033

- Figure 28: Latin America Wireless Occupancy Sensors Industry Revenue (billion), by Building Type 2025 & 2033

- Figure 29: Latin America Wireless Occupancy Sensors Industry Revenue Share (%), by Building Type 2025 & 2033

- Figure 30: Latin America Wireless Occupancy Sensors Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 31: Latin America Wireless Occupancy Sensors Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 32: Latin America Wireless Occupancy Sensors Industry Revenue (billion), by Country 2025 & 2033

- Figure 33: Latin America Wireless Occupancy Sensors Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Middle East Wireless Occupancy Sensors Industry Revenue (billion), by Application 2025 & 2033

- Figure 35: Middle East Wireless Occupancy Sensors Industry Revenue Share (%), by Application 2025 & 2033

- Figure 36: Middle East Wireless Occupancy Sensors Industry Revenue (billion), by Building Type 2025 & 2033

- Figure 37: Middle East Wireless Occupancy Sensors Industry Revenue Share (%), by Building Type 2025 & 2033

- Figure 38: Middle East Wireless Occupancy Sensors Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 39: Middle East Wireless Occupancy Sensors Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 40: Middle East Wireless Occupancy Sensors Industry Revenue (billion), by Country 2025 & 2033

- Figure 41: Middle East Wireless Occupancy Sensors Industry Revenue Share (%), by Country 2025 & 2033

- Figure 42: Saudi Arabia Wireless Occupancy Sensors Industry Revenue (billion), by Application 2025 & 2033

- Figure 43: Saudi Arabia Wireless Occupancy Sensors Industry Revenue Share (%), by Application 2025 & 2033

- Figure 44: Saudi Arabia Wireless Occupancy Sensors Industry Revenue (billion), by Building Type 2025 & 2033

- Figure 45: Saudi Arabia Wireless Occupancy Sensors Industry Revenue Share (%), by Building Type 2025 & 2033

- Figure 46: Saudi Arabia Wireless Occupancy Sensors Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 47: Saudi Arabia Wireless Occupancy Sensors Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 48: Saudi Arabia Wireless Occupancy Sensors Industry Revenue (billion), by Country 2025 & 2033

- Figure 49: Saudi Arabia Wireless Occupancy Sensors Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Wireless Occupancy Sensors Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Wireless Occupancy Sensors Industry Revenue billion Forecast, by Building Type 2020 & 2033

- Table 3: Global Wireless Occupancy Sensors Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 4: Global Wireless Occupancy Sensors Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Global Wireless Occupancy Sensors Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 6: Global Wireless Occupancy Sensors Industry Revenue billion Forecast, by Building Type 2020 & 2033

- Table 7: Global Wireless Occupancy Sensors Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 8: Global Wireless Occupancy Sensors Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: United States Wireless Occupancy Sensors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Canada Wireless Occupancy Sensors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Global Wireless Occupancy Sensors Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 12: Global Wireless Occupancy Sensors Industry Revenue billion Forecast, by Building Type 2020 & 2033

- Table 13: Global Wireless Occupancy Sensors Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 14: Global Wireless Occupancy Sensors Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 15: United Kingdom Wireless Occupancy Sensors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: France Wireless Occupancy Sensors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Germany Wireless Occupancy Sensors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Russia Wireless Occupancy Sensors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Rest of Europe Wireless Occupancy Sensors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Global Wireless Occupancy Sensors Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 21: Global Wireless Occupancy Sensors Industry Revenue billion Forecast, by Building Type 2020 & 2033

- Table 22: Global Wireless Occupancy Sensors Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 23: Global Wireless Occupancy Sensors Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 24: China Wireless Occupancy Sensors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Japan Wireless Occupancy Sensors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: India Wireless Occupancy Sensors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Asia Pacific Wireless Occupancy Sensors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Wireless Occupancy Sensors Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Wireless Occupancy Sensors Industry Revenue billion Forecast, by Building Type 2020 & 2033

- Table 30: Global Wireless Occupancy Sensors Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 31: Global Wireless Occupancy Sensors Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 32: Brazil Wireless Occupancy Sensors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: Argentina Wireless Occupancy Sensors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Maxico Wireless Occupancy Sensors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: Rest of Latin America Wireless Occupancy Sensors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Global Wireless Occupancy Sensors Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 37: Global Wireless Occupancy Sensors Industry Revenue billion Forecast, by Building Type 2020 & 2033

- Table 38: Global Wireless Occupancy Sensors Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 39: Global Wireless Occupancy Sensors Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 40: Global Wireless Occupancy Sensors Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 41: Global Wireless Occupancy Sensors Industry Revenue billion Forecast, by Building Type 2020 & 2033

- Table 42: Global Wireless Occupancy Sensors Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 43: Global Wireless Occupancy Sensors Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 44: United Arab Emirates Wireless Occupancy Sensors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: South Africa Wireless Occupancy Sensors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Middle East Wireless Occupancy Sensors Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Wireless Occupancy Sensors Industry?

The projected CAGR is approximately 15.9%.

2. Which companies are prominent players in the Wireless Occupancy Sensors Industry?

Key companies in the market include Hubbell Incorporated*List Not Exhaustive, Honeywell International Inc, Legrand SA, Leviton Manufacturing Co Inc, Lutron Electronics Co Inc, Eaton Corporation PLC, Johnson Controls Inc, Koninklijke Philips NV, Schneider Electric, Acuity Brands Inc, General Electric Company.

3. What are the main segments of the Wireless Occupancy Sensors Industry?

The market segments include Application, Building Type, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.1 billion as of 2022.

5. What are some drivers contributing to market growth?

; Growing Demand for Green Energy; Growing Demmand for Easily Installable and Interoperable devices.

6. What are the notable trends driving market growth?

Smart City Initiatives to Stimulate the Growth of Wireless Occupancy Sensor Market.

7. Are there any restraints impacting market growth?

; False Triggering of Switches.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Wireless Occupancy Sensors Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Wireless Occupancy Sensors Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Wireless Occupancy Sensors Industry?

To stay informed about further developments, trends, and reports in the Wireless Occupancy Sensors Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence