Key Insights

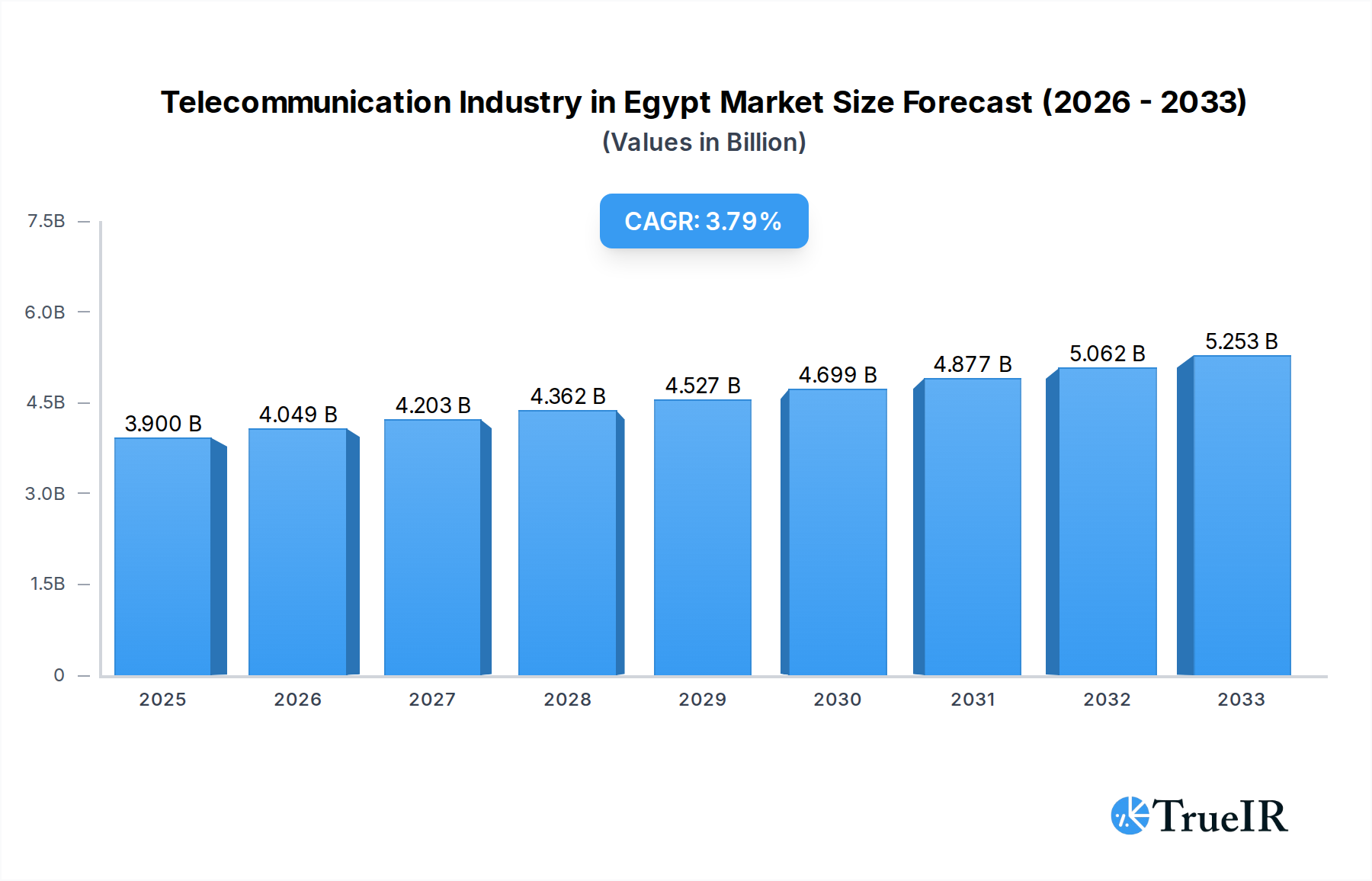

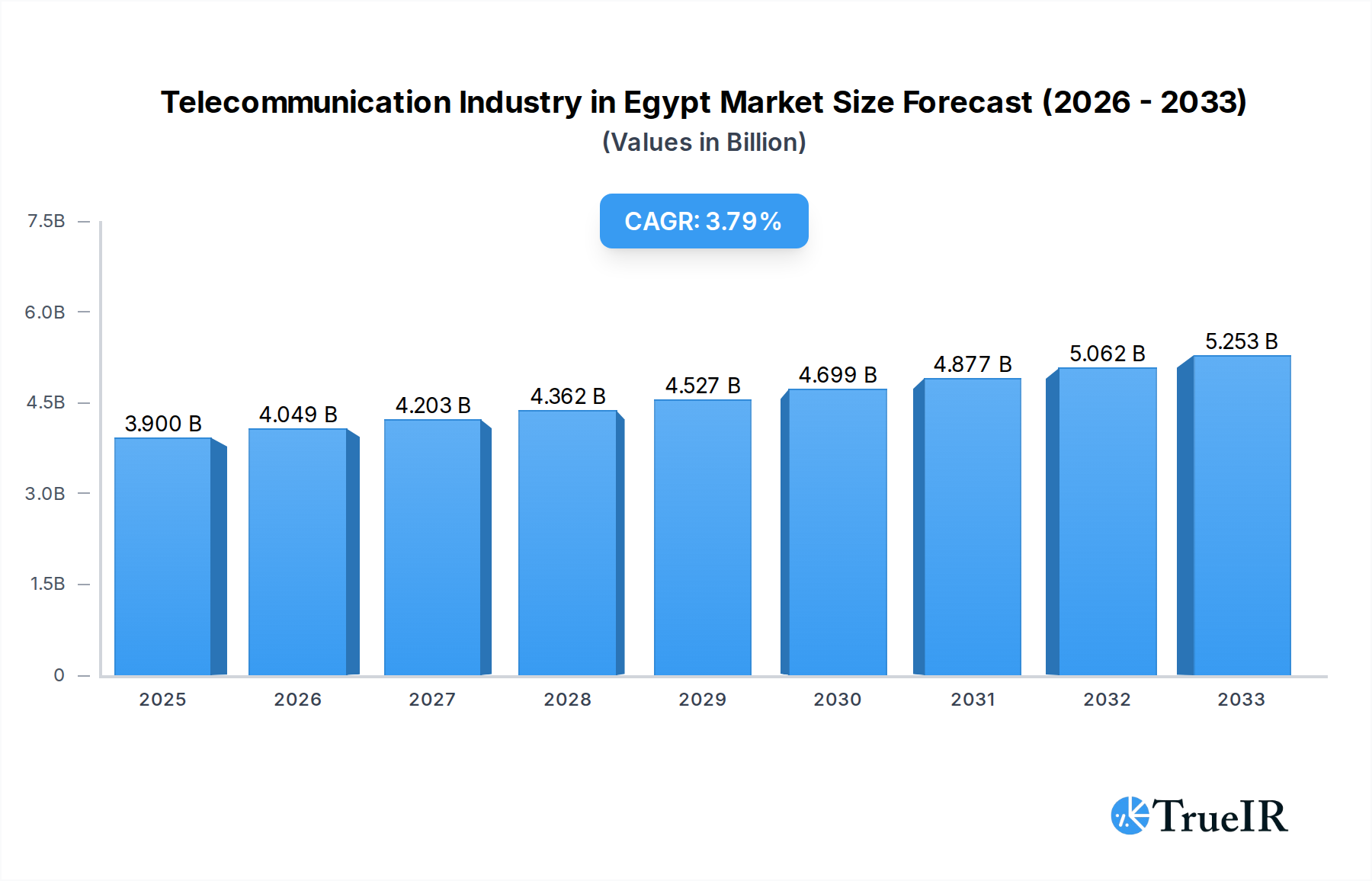

The Egyptian telecommunications market is poised for robust growth, projected to reach approximately USD 3.9 billion in 2025 with a Compound Annual Growth Rate (CAGR) of 3.85% between 2025 and 2033. This expansion is significantly driven by the increasing demand for high-speed data services, the proliferation of Over-The-Top (OTT) and PayTV offerings, and the continuous evolution of voice services, encompassing both wired and wireless solutions. The government's commitment to digital transformation initiatives, including the expansion of 5G networks and fiber optic infrastructure, is further bolstering market penetration and service adoption. This surge is also fueled by a growing young, digitally-native population and the increasing adoption of smartphones and IoT devices, creating a fertile ground for innovative telecommunication solutions. The competitive landscape features key players like Etisalat Egypt, Vodafone, and Telecom Egypt, all vying to capture market share through service diversification and strategic partnerships.

Telecommunication Industry in Egypt Market Size (In Billion)

Despite the positive outlook, certain factors could temper the market's trajectory. The substantial capital expenditure required for infrastructure upgrades, particularly for advanced technologies like 5G, presents a significant financial hurdle. Furthermore, intense price competition among service providers, driven by the need to attract and retain subscribers in an increasingly saturated market, can impact profitability. Regulatory complexities and the need for continuous adaptation to evolving technological landscapes also pose challenges. However, the inherent demand for enhanced connectivity, driven by remote work trends, online education, and the burgeoning digital economy, is expected to outweigh these restraints. The market's segmentation into Voice Services (Wired, Wireless), Data, and OTT and PayTV Services highlights the diverse avenues for revenue generation and consumer engagement within the Egyptian telecommunication ecosystem.

Telecommunication Industry in Egypt Company Market Share

Here's a comprehensive, SEO-optimized report description for the Telecommunication Industry in Egypt, designed for immediate use without further modification.

Report Title: Egypt Telecommunication Market: Growth, Trends, and Future Outlook 2025-2033

Report Description: Dive deep into the dynamic Egyptian telecommunication market with our in-depth report, covering the period from 2019 to 2033, with a base and estimated year of 2025. This report provides unparalleled insights into market structure, trends, opportunities, and key players shaping Egypt's digital landscape. Featuring high-volume keywords like "Egypt telecom market," "telecommunication services Egypt," "5G Egypt," "mobile operators Egypt," and "digital transformation Egypt," this analysis is crucial for stakeholders seeking to understand and capitalize on the nation's robust growth in voice services, data, OTT, and PayTV. We meticulously examine market concentration, regulatory impacts, and the competitive environment featuring Etisalat Egypt, Mobilink, Orange, Vodafone, Telecom Egypt, OSN, AT&T, CallZ Telecom, Global Telecom, and Ericsson. Uncover evolving consumer preferences, technological shifts, and the significant impact of industry developments, including the Ericsson collaboration with Orange Egypt for 2600MHz deployment, Telecom Egypt's national roaming agreement with Orange Egypt, and Nokia's support for Orange Egypt's 5G ambitions. This report is an indispensable resource for strategic planning and investment in the burgeoning Egyptian telecommunication sector.

Telecommunication Industry in Egypt Market Structure & Competitive Landscape

The Egyptian telecommunication market is characterized by a moderate to high level of concentration, primarily dominated by a few major mobile network operators and a significant state-owned incumbent. Innovation drivers are largely propelled by the demand for higher bandwidth, faster data speeds, and the increasing adoption of digital services, including Over-the-Top (OTT) platforms and advanced PayTV offerings. Regulatory impacts are substantial, with government policies dictating spectrum allocation, licensing, and consumer protection measures, significantly influencing market entry and competition. Product substitutes, particularly in the voice services segment, are increasingly being replaced by Over-the-Top (OTT) communication applications. The end-user segmentation is broad, encompassing individual consumers, small and medium-sized enterprises (SMEs), and large corporations, each with distinct service requirements. Merger and Acquisition (M&A) trends, while not as frequent as in more mature markets, are driven by the pursuit of scale, network expansion, and diversification into emerging digital services. The Herfindahl-Hirschman Index (HHI) for market concentration is estimated to be around 0.25, indicating an oligopolistic structure. M&A volumes have been relatively modest, with an estimated XX billion USD over the historical period, often focused on tactical acquisitions to strengthen service portfolios or expand geographical reach.

Telecommunication Industry in Egypt Market Trends & Opportunities

The Egyptian telecommunication market is poised for significant expansion, driven by a rapidly growing, young, and increasingly connected population, alongside a government-driven digital transformation agenda. The market size for telecommunication services in Egypt is projected to reach an estimated $XX billion by 2025 and is forecast to grow at a Compound Annual Growth Rate (CAGR) of approximately XX% from 2025 to 2033, reaching an estimated $XX billion by 2033. This robust growth is underpinned by several key trends. A primary trend is the relentless demand for mobile data services, fueled by the proliferation of smartphones and the increasing consumption of data-intensive applications like video streaming, social media, and online gaming. The penetration rate of mobile subscriptions, already high, is expected to continue its upward trajectory, with a focus on multiple SIM usage and the adoption of higher-tier data plans.

Technological shifts are central to this market's evolution. The ongoing rollout and expansion of 4G networks have significantly improved data speeds and reliability, laying the groundwork for the eventual widespread adoption of 5G technology. Industry developments highlight this progression, with Ericsson working with Orange Egypt to supply antennas for 2600MHz deployment, enhancing network capabilities and reducing operational costs. Furthermore, Nokia's collaboration with Orange Egypt to modernize its SDM solution signifies a proactive approach to subscriber growth and readiness for future 5G services.

Consumer preferences are also evolving. There is a discernible shift towards digital-first engagement, with consumers increasingly preferring online channels for service subscriptions, customer support, and content consumption. The burgeoning Over-The-Top (OTT) and PayTV segments are direct beneficiaries of this trend, offering a richer and more personalized entertainment experience compared to traditional broadcast media. OSN is a key player in this segment, catering to a growing demand for premium content.

Competitive dynamics are intense, with established players like Vodafone Egypt, Etisalat Egypt, Telecom Egypt, and Orange Egypt continuously innovating to attract and retain subscribers. Strategic partnerships, such as the five-year national roaming agreement between Telecom Egypt and Orange Egypt, underscore the collaborative efforts to enhance service coverage and quality nationwide. These collaborations are vital for ensuring seamless connectivity and high-quality voice and data mobile network coverage for customers across the country.

Opportunities abound in areas such as fixed broadband expansion, particularly in underserved urban and peri-urban areas, and the development of specialized enterprise solutions for sectors like finance, healthcare, and education, leveraging the growing digital infrastructure. The government's push for digital transformation also presents significant opportunities for telecommunication providers to partner in developing smart city initiatives, e-governance platforms, and IoT solutions. The continued investment in infrastructure by players like Mobilink (now a part of Orascom Telecom Holding, which also operates under the Orange brand in some regions) and Global Telecom signifies a commitment to meeting the ever-increasing demand for connectivity.

Dominant Markets & Segments in Telecommunication Industry in Egypt

The dominant segment within the Egyptian telecommunication industry is unequivocally Data and mobile services, driven by widespread smartphone adoption and an ever-increasing appetite for internet-based activities. This segment has surpassed traditional Voice Services(Wired, Wireless) in terms of revenue generation and growth potential. The increasing affordability of smartphones and data packages, coupled with the expansion of 4G network coverage across major urban and semi-urban areas, has made mobile internet access a necessity rather than a luxury for a significant portion of the Egyptian population.

Key Growth Drivers for Data and Mobile Services:

- Infrastructure Investment: Continuous network upgrades and expansions by operators like Vodafone Egypt, Etisalat Egypt, Orange Egypt, and Telecom Egypt to enhance data speeds and capacity are crucial. The ongoing deployment of 2600MHz spectrum by operators, facilitated by partnerships like the one between Ericsson and Orange Egypt, directly bolsters mobile data performance.

- Digital Transformation Initiatives: Government initiatives aimed at digitalizing various sectors, including e-governance, e-learning, and digital payments, necessitate robust data connectivity, thereby driving demand.

- Content Consumption: The surge in demand for streaming services, social media, online gaming, and video conferencing fuels the need for higher data allowances and faster internet speeds.

- Smartphone Penetration: The increasing affordability and availability of smartphones across various price points continue to expand the user base for mobile data services.

- Favorable Demographics: Egypt's large, young, and tech-savvy population represents a significant consumer base eager to adopt new digital services and applications.

While Data and mobile services dominate, OTT and PayTV Services are experiencing rapid growth, presenting a significant opportunity. This growth is attributed to changing consumer entertainment preferences, the desire for on-demand content, and the increasing availability of diverse and high-quality content from providers like OSN. The convergence of telecommunication and media is evident, with operators often bundling data plans with streaming subscriptions or offering their own content platforms. The ability of Orange Egypt to leverage its modernized SDM solution, as supported by Nokia, to support subscriber growth and future 5G launches will further enable the delivery of immersive OTT experiences.

Voice Services (Wired and Wireless), though less dynamic in terms of growth compared to data, remains a foundational element of the telecommunication ecosystem. Wireless voice services continue to be a primary mode of communication, with operators like Mobilink and Telecom Egypt maintaining substantial subscriber bases. Wired voice services, primarily through fixed-line telephony, are gradually being complemented and, in some instances, replaced by Voice over IP (VoIP) and Over-The-Top (OTT) voice solutions. However, for enterprise and critical communication needs, wired voice infrastructure continues to hold relevance. The national roaming agreement between Telecom Egypt and Orange Egypt ensures enhanced voice call quality and coverage, benefiting all subscribers across these traditional segments.

The market's dominance by Data and mobile services is a testament to the evolving digital landscape in Egypt, where connectivity fuels economic activity, social interaction, and entertainment. This shift underscores the strategic importance for telecommunication companies to prioritize their investments and service offerings in these high-growth areas.

Telecommunication Industry in Egypt Product Analysis

The Egyptian telecommunication market is characterized by a robust and evolving product portfolio. Innovations are primarily focused on enhancing data speeds, network reliability, and the diversity of digital services offered. Key product advancements include the widespread deployment of 4G LTE technology, enabling significantly faster mobile broadband experiences. The upcoming introduction of 5G services, supported by infrastructure upgrades and partnerships like those involving Ericsson and Nokia with Orange Egypt, promises ultra-low latency and massive connectivity, opening doors for new applications in IoT and advanced mobile broadband. Beyond core network services, the market sees significant product innovation in bundled service offerings, encompassing mobile data, voice, fixed broadband, and digital content subscriptions from players like OSN. Competitive advantages are built upon network superiority, attractive pricing strategies, and the unique value propositions of integrated digital service ecosystems.

Key Drivers, Barriers & Challenges in Telecommunication Industry in Egypt

Key Drivers:

- Young & Growing Population: A large, digitally-native youth demographic fuels demand for mobile data, social media, and entertainment services.

- Government Digitalization Push: National strategies to digitize public services and foster economic growth necessitate enhanced telecommunication infrastructure and services.

- Increasing Smartphone Penetration: The affordability and accessibility of smartphones drive data consumption and adoption of digital applications.

- Technological Advancements: Continuous deployment of 4G and the anticipation of 5G enhance service capabilities and user experience.

- Foreign Direct Investment: Continued investment in infrastructure and technology by global and local players stimulates market growth.

Key Barriers & Challenges:

- Infrastructure Investment Costs: The substantial capital required for network expansion, upgrades, and the rollout of new technologies like 5G presents a significant financial challenge.

- Regulatory Hurdles & Spectrum Allocation: Navigating complex regulatory frameworks, including spectrum availability and pricing, can impede rapid deployment and innovation.

- Competition & Price Wars: Intense competition among major operators can lead to price wars, impacting profitability and the ability to reinvest in infrastructure.

- Cybersecurity Threats: The increasing reliance on digital services necessitates robust cybersecurity measures to protect sensitive data and critical infrastructure.

- Digital Divide: Ensuring equitable access to telecommunication services across all regions, particularly rural and underserved areas, remains a persistent challenge.

Growth Drivers in the Telecommunication Industry in Egypt Market

Several key factors are propelling the growth of Egypt's telecommunication sector. The nation's young and rapidly growing population is a primary driver, exhibiting a strong appetite for mobile data, social media, and digital content. Complementing this demographic advantage is the government's strategic emphasis on digital transformation, which is creating an environment conducive to infrastructure development and the adoption of advanced technologies. Significant investments in network upgrades, particularly the expansion of 4G and the preparations for 5G deployment by major players like Vodafone Egypt and Etisalat Egypt, are enhancing service capabilities and creating new revenue streams. Furthermore, the increasing affordability of smartphones is broadening the reach of mobile services, enabling more Egyptians to participate in the digital economy. Economic stability and foreign direct investment also play a crucial role, providing the financial impetus for large-scale infrastructure projects.

Challenges Impacting Telecommunication Industry in Egypt Growth

Despite the promising growth trajectory, the telecommunication industry in Egypt faces several significant challenges. The substantial capital expenditure required for building and upgrading network infrastructure, especially for the deployment of advanced technologies like 5G, remains a considerable financial hurdle. Regulatory complexities, including spectrum allocation policies and licensing procedures, can sometimes create delays and add to operational costs. Intense market competition among key players such as Orange Egypt, Telecom Egypt, and Vodafone Egypt can lead to price erosion, impacting profitability and the capacity for future investment. Supply chain disruptions, particularly for specialized equipment and components, can also affect the pace of network expansion and maintenance. Moreover, ensuring equitable access to high-quality telecommunication services across all geographical regions, bridging the digital divide between urban and rural areas, continues to be a persistent operational and social challenge.

Key Players Shaping the Telecommunication Industry in Egypt Market

- OSN

- Etisalat Egypt

- Mobilink

- AT&T

- Orange

- CallZ Telecom

- Vodafone

- Telecom Egypt

- Global Telecom

- Ericsson

- Nokia

Significant Telecommunication Industry in Egypt Industry Milestones

- June 2022: Ericsson is working with Orange Egypt to supply antennas for 2600MHz deployment, significantly improving Orange Egypt's network capabilities and reducing operational site expenses.

- August 2022: Telecom Egypt signed a five-year agreement with Orange Egypt for a national roaming service, enhancing nationwide high-quality voice and data mobile network coverage for both companies' customers.

- August 2022: Nokia is working with Orange Egypt to modernize its existing Nokia SDM solution, preparing it to support subscriber growth over the next five years and facilitating Orange Egypt's planned launch of 5G services.

Future Outlook for Telecommunication Industry in Egypt Market

The future outlook for the Egyptian telecommunication industry is exceptionally bright, driven by a confluence of factors including a young, growing population, robust government support for digital transformation, and continuous technological advancements. The projected growth in mobile data consumption, the imminent rollout of 5G services, and the expanding digital services ecosystem, encompassing OTT and PayTV, will serve as major growth catalysts. Strategic investments in infrastructure by key players like Vodafone Egypt, Etisalat Egypt, Orange Egypt, and Telecom Egypt, coupled with the potential for new service innovations in areas like IoT and enterprise solutions, promise to significantly boost market penetration and revenue. Opportunities will emerge from smart city initiatives, e-commerce expansion, and the further digitalization of various economic sectors. The market is well-positioned to become a regional hub for digital innovation and connectivity, offering substantial strategic opportunities for stakeholders.

Telecommunication Industry in Egypt Segmentation

-

1. Services

-

1.1. Voice Services

- 1.1.1. Wired

- 1.1.2. Wireless

- 1.2. Data and

- 1.3. OTT and PayTV Services

-

1.1. Voice Services

Telecommunication Industry in Egypt Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

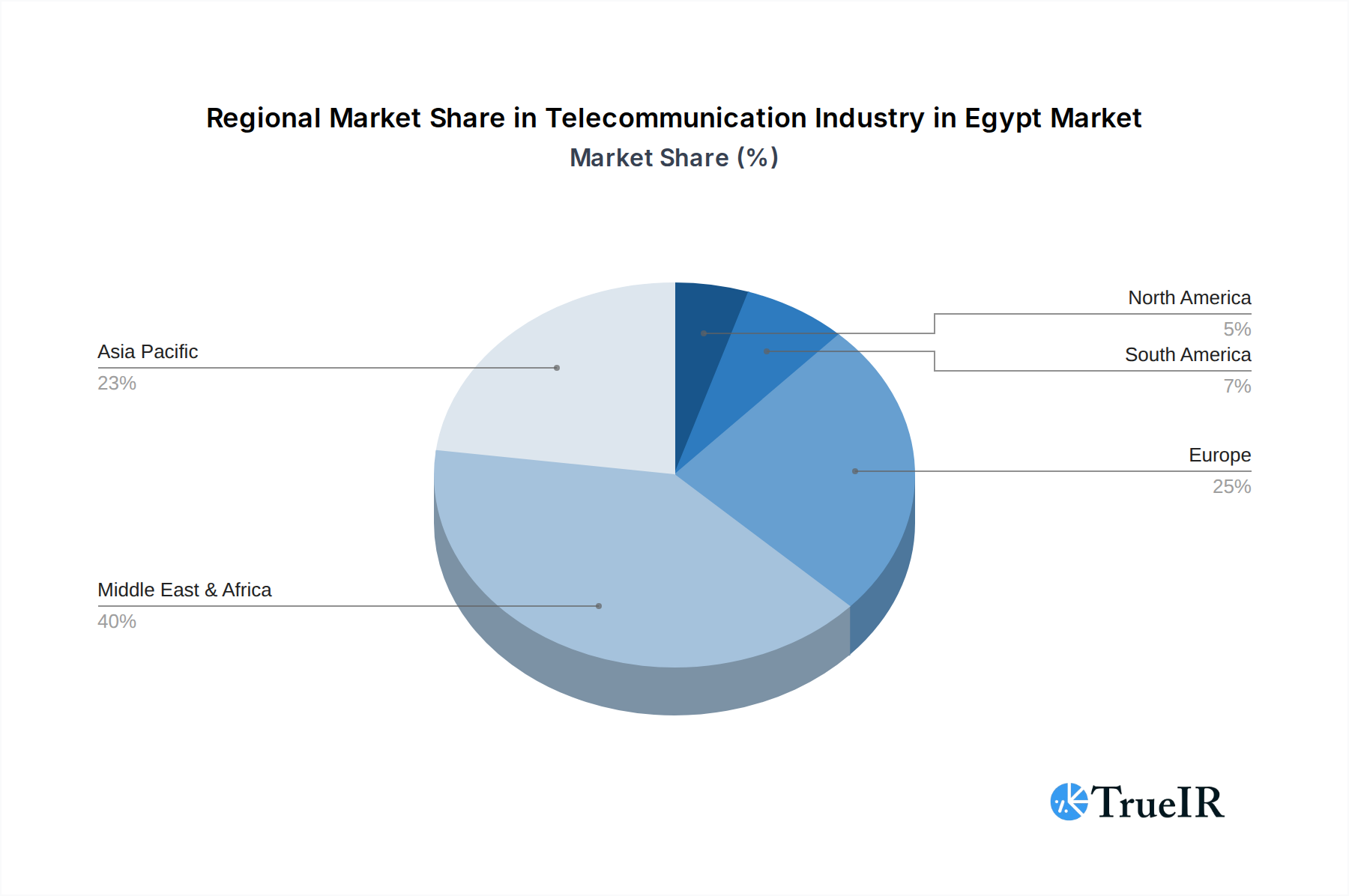

Telecommunication Industry in Egypt Regional Market Share

Geographic Coverage of Telecommunication Industry in Egypt

Telecommunication Industry in Egypt REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.85% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Services

- 5.1.1. Voice Services

- 5.1.1.1. Wired

- 5.1.1.2. Wireless

- 5.1.2. Data and

- 5.1.3. OTT and PayTV Services

- 5.1.1. Voice Services

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. South America

- 5.2.3. Europe

- 5.2.4. Middle East & Africa

- 5.2.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Services

- 6. Global Telecommunication Industry in Egypt Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Services

- 6.1.1. Voice Services

- 6.1.1.1. Wired

- 6.1.1.2. Wireless

- 6.1.2. Data and

- 6.1.3. OTT and PayTV Services

- 6.1.1. Voice Services

- 6.1. Market Analysis, Insights and Forecast - by Services

- 7. North America Telecommunication Industry in Egypt Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Services

- 7.1.1. Voice Services

- 7.1.1.1. Wired

- 7.1.1.2. Wireless

- 7.1.2. Data and

- 7.1.3. OTT and PayTV Services

- 7.1.1. Voice Services

- 7.1. Market Analysis, Insights and Forecast - by Services

- 8. South America Telecommunication Industry in Egypt Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Services

- 8.1.1. Voice Services

- 8.1.1.1. Wired

- 8.1.1.2. Wireless

- 8.1.2. Data and

- 8.1.3. OTT and PayTV Services

- 8.1.1. Voice Services

- 8.1. Market Analysis, Insights and Forecast - by Services

- 9. Europe Telecommunication Industry in Egypt Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Services

- 9.1.1. Voice Services

- 9.1.1.1. Wired

- 9.1.1.2. Wireless

- 9.1.2. Data and

- 9.1.3. OTT and PayTV Services

- 9.1.1. Voice Services

- 9.1. Market Analysis, Insights and Forecast - by Services

- 10. Middle East & Africa Telecommunication Industry in Egypt Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Services

- 10.1.1. Voice Services

- 10.1.1.1. Wired

- 10.1.1.2. Wireless

- 10.1.2. Data and

- 10.1.3. OTT and PayTV Services

- 10.1.1. Voice Services

- 10.1. Market Analysis, Insights and Forecast - by Services

- 11. Asia Pacific Telecommunication Industry in Egypt Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Services

- 11.1.1. Voice Services

- 11.1.1.1. Wired

- 11.1.1.2. Wireless

- 11.1.2. Data and

- 11.1.3. OTT and PayTV Services

- 11.1.1. Voice Services

- 11.1. Market Analysis, Insights and Forecast - by Services

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 OSN

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Etisalat Egypt

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Mobilink

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 AT&T

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Orange

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 CallZ Telecom*List Not Exhaustive

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Vodafone

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Telecom Egypt

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Global Telecom

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Ericsson

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 OSN

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Telecommunication Industry in Egypt Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Telecommunication Industry in Egypt Revenue (billion), by Services 2025 & 2033

- Figure 3: North America Telecommunication Industry in Egypt Revenue Share (%), by Services 2025 & 2033

- Figure 4: North America Telecommunication Industry in Egypt Revenue (billion), by Country 2025 & 2033

- Figure 5: North America Telecommunication Industry in Egypt Revenue Share (%), by Country 2025 & 2033

- Figure 6: South America Telecommunication Industry in Egypt Revenue (billion), by Services 2025 & 2033

- Figure 7: South America Telecommunication Industry in Egypt Revenue Share (%), by Services 2025 & 2033

- Figure 8: South America Telecommunication Industry in Egypt Revenue (billion), by Country 2025 & 2033

- Figure 9: South America Telecommunication Industry in Egypt Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Telecommunication Industry in Egypt Revenue (billion), by Services 2025 & 2033

- Figure 11: Europe Telecommunication Industry in Egypt Revenue Share (%), by Services 2025 & 2033

- Figure 12: Europe Telecommunication Industry in Egypt Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe Telecommunication Industry in Egypt Revenue Share (%), by Country 2025 & 2033

- Figure 14: Middle East & Africa Telecommunication Industry in Egypt Revenue (billion), by Services 2025 & 2033

- Figure 15: Middle East & Africa Telecommunication Industry in Egypt Revenue Share (%), by Services 2025 & 2033

- Figure 16: Middle East & Africa Telecommunication Industry in Egypt Revenue (billion), by Country 2025 & 2033

- Figure 17: Middle East & Africa Telecommunication Industry in Egypt Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Telecommunication Industry in Egypt Revenue (billion), by Services 2025 & 2033

- Figure 19: Asia Pacific Telecommunication Industry in Egypt Revenue Share (%), by Services 2025 & 2033

- Figure 20: Asia Pacific Telecommunication Industry in Egypt Revenue (billion), by Country 2025 & 2033

- Figure 21: Asia Pacific Telecommunication Industry in Egypt Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Telecommunication Industry in Egypt Revenue billion Forecast, by Services 2020 & 2033

- Table 2: Global Telecommunication Industry in Egypt Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Global Telecommunication Industry in Egypt Revenue billion Forecast, by Services 2020 & 2033

- Table 4: Global Telecommunication Industry in Egypt Revenue billion Forecast, by Country 2020 & 2033

- Table 5: United States Telecommunication Industry in Egypt Revenue (billion) Forecast, by Application 2020 & 2033

- Table 6: Canada Telecommunication Industry in Egypt Revenue (billion) Forecast, by Application 2020 & 2033

- Table 7: Mexico Telecommunication Industry in Egypt Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Global Telecommunication Industry in Egypt Revenue billion Forecast, by Services 2020 & 2033

- Table 9: Global Telecommunication Industry in Egypt Revenue billion Forecast, by Country 2020 & 2033

- Table 10: Brazil Telecommunication Industry in Egypt Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Argentina Telecommunication Industry in Egypt Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Rest of South America Telecommunication Industry in Egypt Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Global Telecommunication Industry in Egypt Revenue billion Forecast, by Services 2020 & 2033

- Table 14: Global Telecommunication Industry in Egypt Revenue billion Forecast, by Country 2020 & 2033

- Table 15: United Kingdom Telecommunication Industry in Egypt Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Germany Telecommunication Industry in Egypt Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: France Telecommunication Industry in Egypt Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Italy Telecommunication Industry in Egypt Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Spain Telecommunication Industry in Egypt Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Russia Telecommunication Industry in Egypt Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Benelux Telecommunication Industry in Egypt Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Nordics Telecommunication Industry in Egypt Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Rest of Europe Telecommunication Industry in Egypt Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Global Telecommunication Industry in Egypt Revenue billion Forecast, by Services 2020 & 2033

- Table 25: Global Telecommunication Industry in Egypt Revenue billion Forecast, by Country 2020 & 2033

- Table 26: Turkey Telecommunication Industry in Egypt Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Israel Telecommunication Industry in Egypt Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: GCC Telecommunication Industry in Egypt Revenue (billion) Forecast, by Application 2020 & 2033

- Table 29: North Africa Telecommunication Industry in Egypt Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: South Africa Telecommunication Industry in Egypt Revenue (billion) Forecast, by Application 2020 & 2033

- Table 31: Rest of Middle East & Africa Telecommunication Industry in Egypt Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Global Telecommunication Industry in Egypt Revenue billion Forecast, by Services 2020 & 2033

- Table 33: Global Telecommunication Industry in Egypt Revenue billion Forecast, by Country 2020 & 2033

- Table 34: China Telecommunication Industry in Egypt Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: India Telecommunication Industry in Egypt Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Japan Telecommunication Industry in Egypt Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: South Korea Telecommunication Industry in Egypt Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: ASEAN Telecommunication Industry in Egypt Revenue (billion) Forecast, by Application 2020 & 2033

- Table 39: Oceania Telecommunication Industry in Egypt Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Rest of Asia Pacific Telecommunication Industry in Egypt Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Telecommunication Industry in Egypt?

The projected CAGR is approximately 3.85%.

2. Which companies are prominent players in the Telecommunication Industry in Egypt?

Key companies in the market include OSN, Etisalat Egypt, Mobilink, AT&T, Orange, CallZ Telecom*List Not Exhaustive, Vodafone, Telecom Egypt, Global Telecom, Ericsson.

3. What are the main segments of the Telecommunication Industry in Egypt?

The market segments include Services.

4. Can you provide details about the market size?

The market size is estimated to be USD 3.9 billion as of 2022.

5. What are some drivers contributing to market growth?

Rising demand for 5G; Growth of IoT usage in Telecom.

6. What are the notable trends driving market growth?

Rising demand for Fixed Broadband Services.

7. Are there any restraints impacting market growth?

High Costs And Limited Commercialization.

8. Can you provide examples of recent developments in the market?

June 2022: Ericsson is working with Orange Egypt to supply antennas for 2600MHz deployment. Orange Egypt improved its network capabilities through this collaboration and significantly reduced operational site expenses.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Telecommunication Industry in Egypt," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Telecommunication Industry in Egypt report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Telecommunication Industry in Egypt?

To stay informed about further developments, trends, and reports in the Telecommunication Industry in Egypt, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence