Key Insights

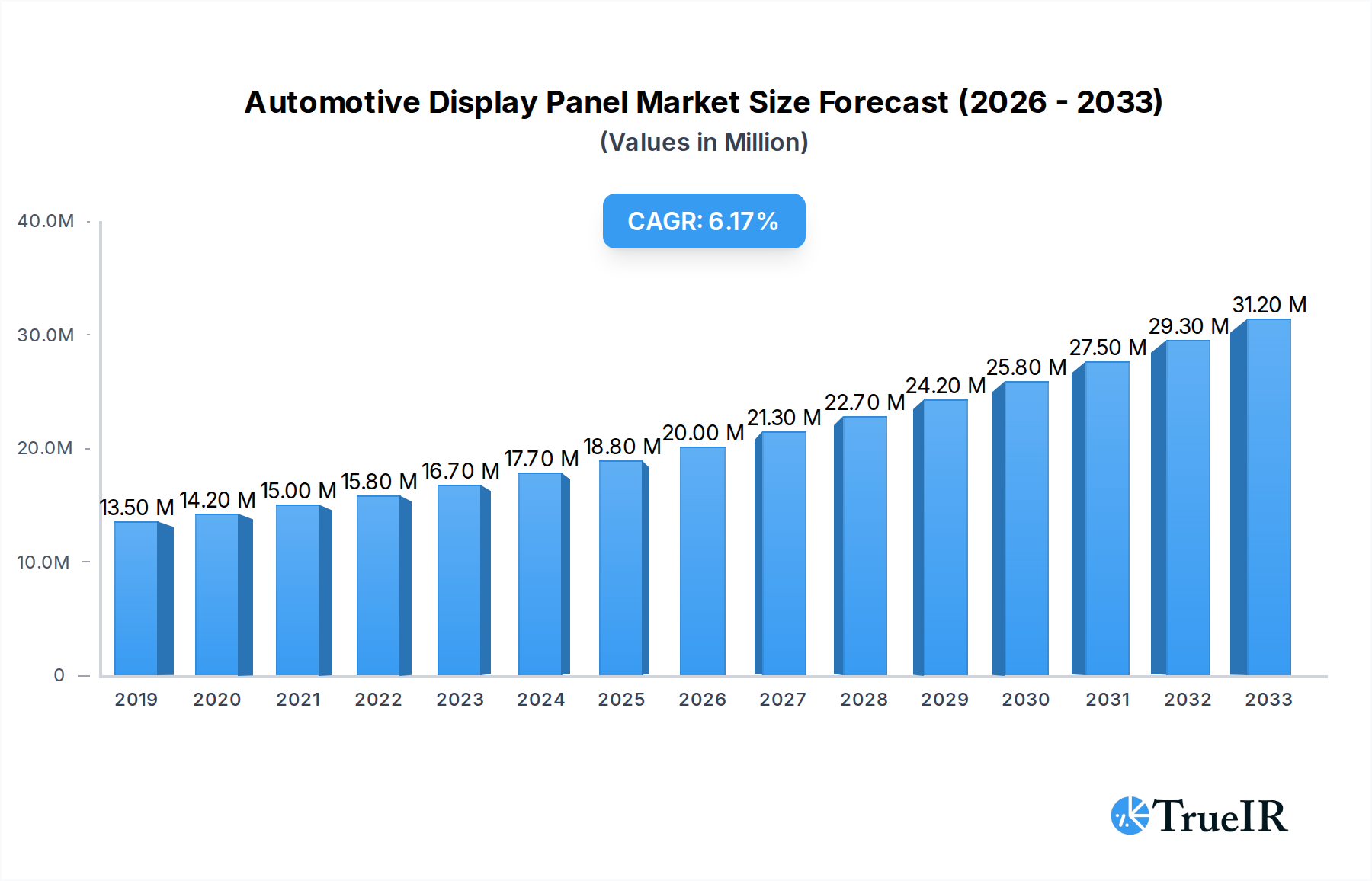

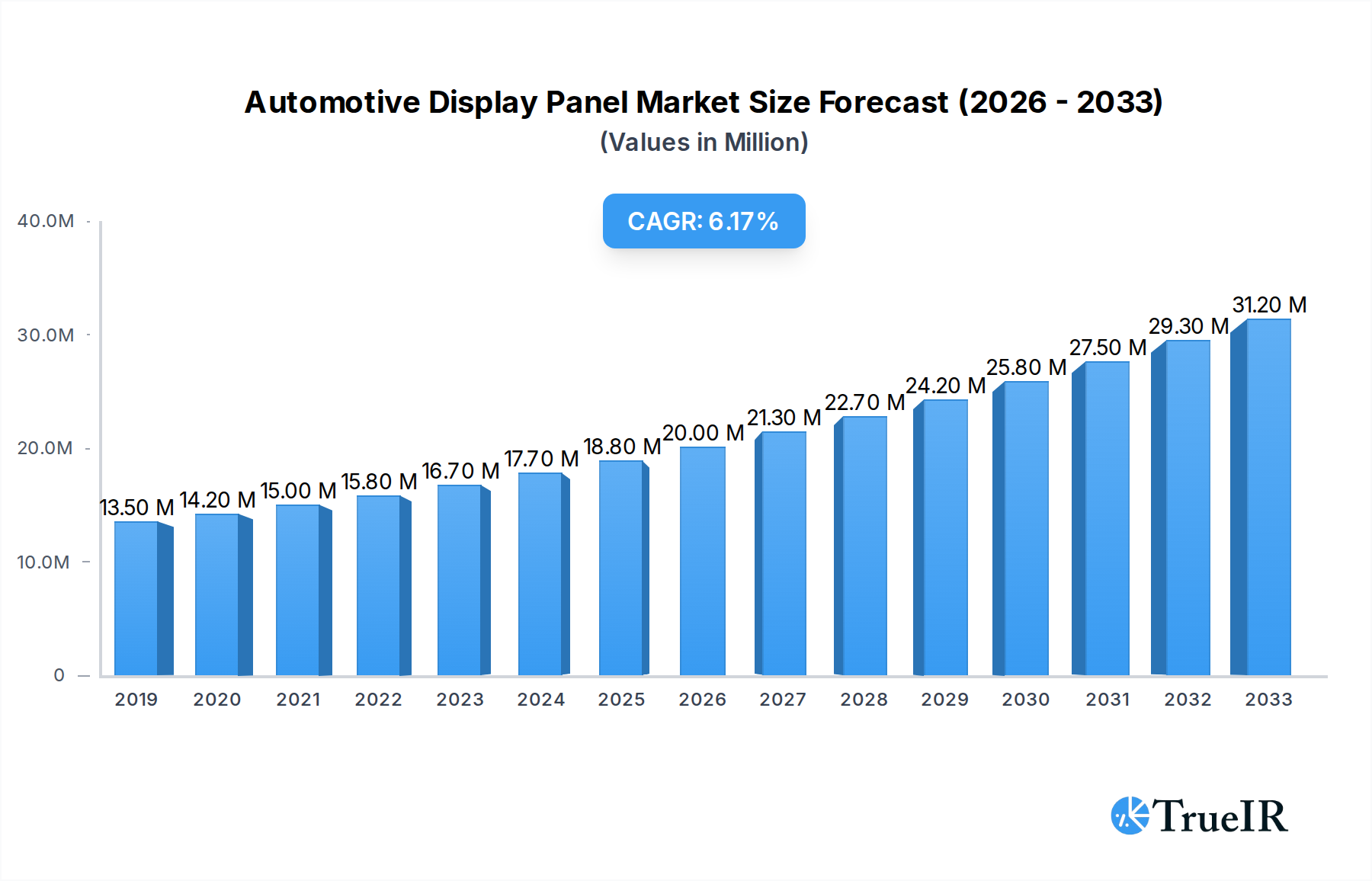

The automotive display panel market is poised for substantial growth, projected to reach an estimated $20.75 million by 2025, driven by an impressive compound annual growth rate (CAGR) of 6.80% through 2033. This expansion is primarily fueled by the escalating demand for advanced in-car infotainment systems, sophisticated instrument clusters, and the increasing integration of heads-up displays (HUDs) in vehicles across all segments. The continuous evolution of vehicle interiors, moving towards a more digital and interactive experience, is a significant tailwind for this market. Furthermore, the burgeoning trend of autonomous driving necessitates more complex and informative displays to convey critical data to both drivers and passengers. The growing adoption of electric vehicles (EVs), which often feature larger and more advanced digital displays for battery management and connectivity features, also contributes to market acceleration. Emerging technologies like micro-LED and advancements in OLED are expected to further enhance display quality, functionality, and energy efficiency, thereby stimulating market adoption and innovation.

Automotive Display Panel Market Market Size (In Million)

Key segments driving this growth include display consoles/clusters, encompassing instrument clusters, center stacks, and heads-up displays, as well as the underlying display panel technologies. AMOLED and Oxide LCD technologies are gaining prominence due to their superior contrast ratios, vibrant colors, and flexibility, making them ideal for modern automotive aesthetics and functionality. While the market is experiencing robust growth, certain challenges such as the high cost of advanced display technologies and the need for stringent durability and safety certifications within the automotive industry present moderate restraints. However, the strategic focus of leading automotive display manufacturers and tier-1 suppliers, including LG Display, Samsung Display, BOE, and Continental, on research and development for next-generation displays, coupled with strategic partnerships, will continue to propel the market forward. Regional analysis indicates Asia as a dominant market due to the strong presence of automotive manufacturing hubs and increasing consumer demand for premium in-car technologies.

Automotive Display Panel Market Company Market Share

This comprehensive report provides an in-depth analysis of the Automotive Display Panel Market, a rapidly evolving sector driven by advancements in in-vehicle infotainment and safety systems. Spanning from 2019 to 2033, with a Base Year of 2025, this study meticulously details historical trends, current market dynamics, and future projections for the Forecast Period of 2025–2033. Our expert analysis covers critical market segments, technological innovations, and the competitive landscape, offering valuable insights for stakeholders in the automotive and electronics industries. The global market is projected to reach an estimated value of USD XXX Billion in 2025, with a projected Compound Annual Growth Rate (CAGR) of XX% during the forecast period.

Automotive Display Panel Market Market Structure & Competitive Landscape

The automotive display panel market is characterized by a moderately concentrated structure, with a few key players dominating a significant portion of the market share. Innovation is a primary driver, fueled by the escalating demand for sophisticated in-vehicle infotainment and advanced driver-assistance systems (ADAS). Regulatory frameworks, though evolving, are increasingly focusing on safety standards and energy efficiency, indirectly shaping product development. Product substitutes, such as simpler integrated control panels, exist but are rapidly losing ground to the superior user experience offered by advanced display technologies. The end-user segmentation is primarily driven by vehicle type, with luxury and premium segments adopting cutting-edge displays at a faster rate. Mergers and Acquisitions (M&A) have been a strategic tool for market consolidation and technological enhancement, with approximately XX significant M&A deals recorded between 2019 and 2024, involving key players aiming to expand their technological portfolios and market reach. For instance, the acquisition of BHTC by AUO signifies a strategic move to strengthen upstream integration and direct collaboration with automakers, impacting market dynamics.

- Market Concentration: Moderately concentrated with a few dominant global manufacturers.

- Innovation Drivers: Demand for advanced infotainment, ADAS integration, augmented reality displays, and enhanced user experience.

- Regulatory Impacts: Stringent safety standards, emission regulations, and evolving data privacy laws influencing display integration and functionality.

- Product Substitutes: Traditional button-based controls, basic integrated displays.

- End-User Segmentation: Luxury vehicles, premium vehicles, mass-market vehicles, commercial vehicles.

- M&A Trends: Strategic acquisitions for technology acquisition, market penetration, and supply chain control.

Automotive Display Panel Market Market Trends & Opportunities

The automotive display panel market is witnessing an unprecedented surge, driven by a confluence of technological advancements, evolving consumer expectations, and the relentless pursuit of enhanced in-vehicle experiences. The market size is expanding at an impressive rate, projected to reach USD XXX Billion by 2025, with a robust CAGR of XX% anticipated between 2025 and 2033. This growth is fundamentally underpinned by the rapid integration of advanced display technologies into vehicle interiors, transforming them into sophisticated, connected, and personalized environments. The shift from conventional analog dashboards to sophisticated digital instrument clusters is a primary catalyst, offering drivers richer information, customizable interfaces, and improved readability. Furthermore, the escalating adoption of large-format center stack displays, designed to manage infotainment, navigation, climate control, and vehicle settings, is reshaping the automotive interior design paradigm.

The emergence and rapid maturation of OLED and Mini-LED display technologies are pivotal to this market expansion. AMOLED displays, in particular, are gaining significant traction due to their superior contrast ratios, vibrant colors, faster response times, and energy efficiency, making them ideal for high-definition graphics and dynamic content. LTPS LCD technology also continues to play a crucial role, offering a cost-effective yet high-performance solution for a wide range of applications. The growing demand for Heads-Up Displays (HUDs), which project critical driving information directly onto the windshield, is another significant trend, enhancing driver focus and safety by minimizing the need to divert attention from the road. This trend is further bolstered by advancements in augmented reality HUDs, capable of overlaying navigation directions and hazard warnings onto the real-world view.

Consumer preferences are increasingly leaning towards larger, more immersive, and intuitive display interfaces. This demand is creating substantial opportunities for display manufacturers to collaborate more closely with automotive OEMs. The trend towards electric vehicles (EVs) and autonomous driving (AD) further amplifies the importance of displays, as these vehicles often require more sophisticated interfaces for managing charging, range, and advanced driving functionalities. The opportunity lies in developing integrated display solutions that not only enhance user experience but also contribute to vehicle efficiency and safety. For instance, the development of smart displays that can dynamically adjust content based on driving conditions or driver attention levels presents a significant future growth avenue. The competitive landscape is dynamic, with established players continuously innovating and new entrants vying for market share, particularly from Asia. Strategic partnerships and vertical integration, as exemplified by AUO’s acquisition of BHTC, are becoming crucial for staying ahead in this competitive environment.

Dominant Markets & Segments in Automotive Display Panel Market

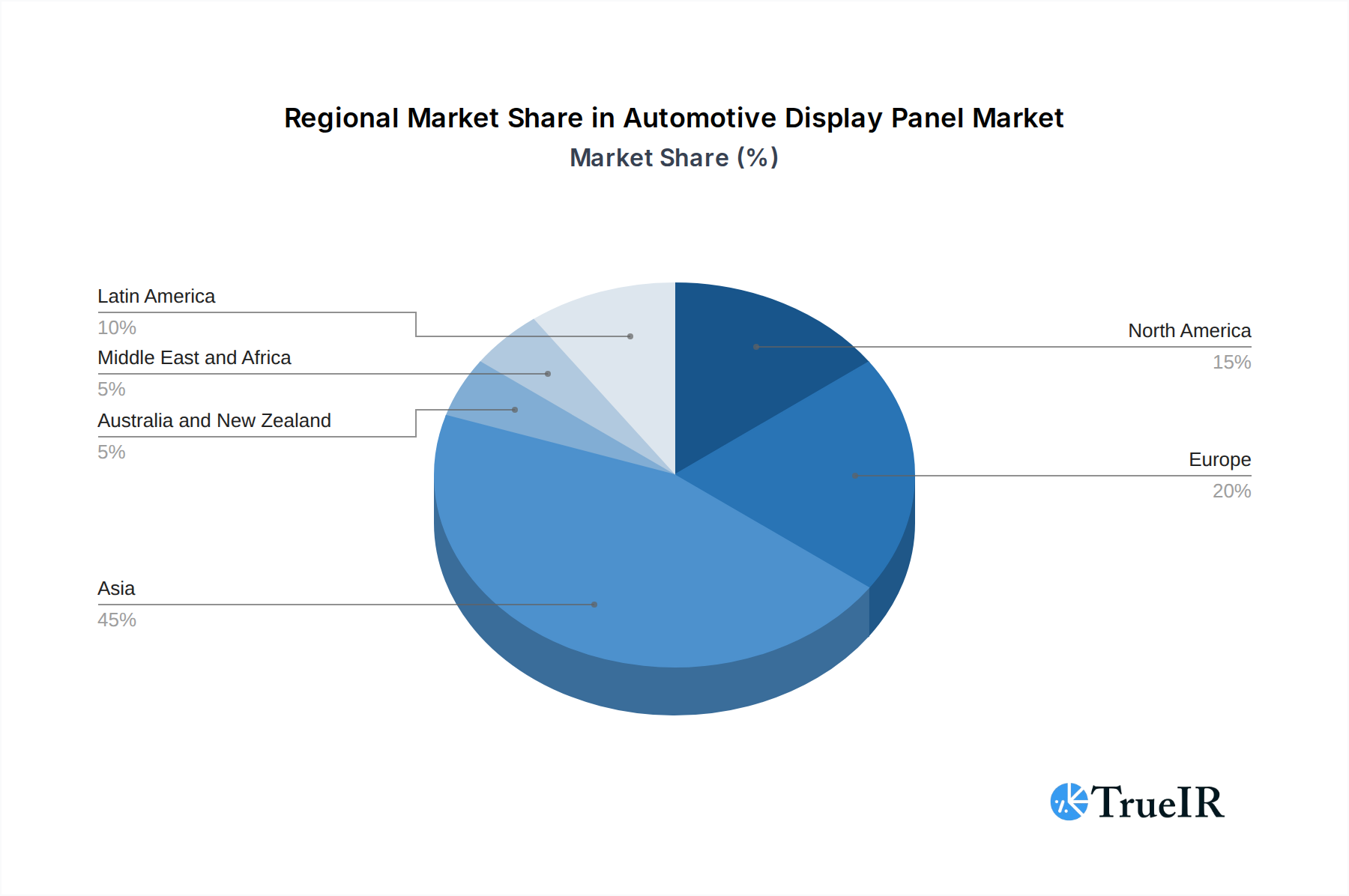

The global automotive display panel market exhibits distinct regional dominance and segment leadership, driven by varying factors of economic development, technological adoption rates, and automotive industry maturity. Asia Pacific stands out as the dominant region, propelled by its robust automotive manufacturing base, significant technological innovation hubs, and a burgeoning demand for advanced vehicle features. Countries like China, South Korea, and Japan are at the forefront of this dominance, benefiting from substantial investments in research and development, large domestic automotive markets, and government support for the electronics industry. The sheer volume of vehicle production and the rapid adoption of cutting-edge technologies by both established and emerging automotive brands in this region contribute significantly to market growth.

Within the Display Panel: By Technology segment, AMOLED technology is emerging as a key growth driver and is projected to witness the fastest expansion. Its superior visual quality, flexibility, and energy efficiency make it highly sought after for premium applications, including large-format displays and curved screens. While a-Si LCD and LTPS LCD technologies continue to hold a significant market share due to their cost-effectiveness and established manufacturing processes, the trend is undeniably towards advanced display solutions. Oxide LCD technology is also gaining prominence for its improved performance characteristics over traditional a-Si LCD, particularly in terms of power consumption and refresh rates.

In terms of Display Console/Cluster: By Application, the Instrument Cluster segment remains a cornerstone of the market, with a steady transition from analog to digital and increasingly sophisticated digital clusters. However, the Center Stack display segment is experiencing explosive growth. These large, central displays are becoming the primary interface for a multitude of vehicle functions, including infotainment, navigation, climate control, and connectivity services. The increasing complexity of in-vehicle infotainment systems and the consumer demand for seamless integration of personal devices are fueling this expansion.

The Heads-Up Display (HUD) segment, while currently smaller in market share, represents a significant growth opportunity. Advancements in augmented reality HUDs are poised to revolutionize driver information delivery, projecting critical data directly into the driver's line of sight, thereby enhancing safety and reducing distraction. This technology is becoming a key differentiator, particularly in luxury and premium vehicles. The "Other Applications" category encompasses a range of emerging uses, including rear-seat entertainment displays, digital side-view mirrors, and advanced dashboard elements, all contributing to the overall market's dynamic growth.

- Dominant Region: Asia Pacific, driven by China, South Korea, and Japan.

- Key Growth Drivers: Extensive automotive manufacturing, strong R&D capabilities, supportive government policies, high consumer adoption of advanced technologies.

- Leading Display Technology: AMOLED, with significant growth expected due to its superior visual performance and efficiency.

- Growth Drivers: Demand for high-resolution, vibrant, and energy-efficient displays; increasing adoption in premium vehicle segments.

- Leading Application: Center Stack displays, evolving into sophisticated infotainment and control hubs.

- Growth Drivers: Integration of advanced infotainment systems, connectivity features, and touch-screen functionalities; consumer preference for large, intuitive interfaces.

- Emerging Application: Heads-Up Displays (HUDs), particularly Augmented Reality HUDs, poised for substantial growth.

- Growth Drivers: Enhanced driver safety, reduced distraction, integration of navigation and ADAS information.

Automotive Display Panel Market Product Analysis

The automotive display panel market is defined by continuous product innovation focused on enhancing visual clarity, user experience, and functional integration. Key product advancements include the development of flexible and curved AMOLED displays that enable novel interior designs and immersive viewing experiences. Furthermore, significant progress has been made in display technologies such as Mini-LED and Micro-LED, promising superior brightness, contrast, and longevity. The integration of advanced touch technologies, haptic feedback, and anti-glare coatings are becoming standard features, improving usability and reducing reflections. Competitive advantages are derived from offering high resolution, wide color gamuts, fast response times, and robust durability to withstand the demanding automotive environment.

Key Drivers, Barriers & Challenges in Automotive Display Panel Market

The automotive display panel market is propelled by several key drivers. The escalating demand for sophisticated in-vehicle infotainment systems and advanced driver-assistance systems (ADAS) is a primary growth engine. Technological advancements, such as the integration of AI and augmented reality into displays, are creating new opportunities. Furthermore, government regulations promoting enhanced safety features and the growing trend of vehicle electrification, which necessitates new interface designs, are significant drivers. The increasing consumer preference for premium and connected vehicle experiences also fuels market expansion.

However, the market faces notable barriers and challenges. The high cost of advanced display technologies, particularly AMOLED and Mini-LED, can be a restraint, especially for mass-market vehicles. Supply chain disruptions and the reliance on specialized components can impact production volumes and timelines. Stringent automotive qualification processes and long development cycles also pose challenges. Intense competition among manufacturers, coupled with the need for continuous innovation, puts pressure on profit margins. Furthermore, cybersecurity concerns related to connected displays and data privacy present regulatory and technical hurdles.

Growth Drivers in the Automotive Display Panel Market Market

The automotive display panel market is experiencing robust growth driven by several interconnected factors. The insatiable consumer appetite for advanced in-vehicle infotainment and seamless connectivity is a fundamental driver, pushing OEMs to integrate larger, higher-resolution, and more interactive displays. The rapid evolution of Advanced Driver-Assistance Systems (ADAS) and the nascent stages of autonomous driving necessitate sophisticated visual feedback mechanisms, making advanced display panels crucial for conveying complex information to the driver. Furthermore, the automotive industry's transition towards electrification is indirectly fueling display demand, as electric vehicles often feature redesigned interiors and require intuitive interfaces for managing battery status, charging, and energy efficiency. Regulatory pushes towards enhanced safety features, such as the mandated inclusion of certain driver monitoring systems, are also spurring the adoption of advanced display technologies.

Challenges Impacting Automotive Display Panel Market Growth

Despite the strong growth trajectory, the automotive display panel market faces several significant challenges that could impede its progress. The sheer cost associated with cutting-edge display technologies like AMOLED and Micro-LED remains a considerable barrier for widespread adoption, particularly in mid-range and economy vehicles. The complex and often lengthy automotive qualification and certification processes for new display components can lead to extended development timelines and increased R&D expenditure. Supply chain vulnerabilities, including the availability of critical raw materials and semiconductor shortages, continue to pose risks to consistent production and timely delivery. Furthermore, the intense competitive landscape necessitates continuous innovation, which can be costly and puts pressure on profit margins for manufacturers. Ensuring robust cybersecurity for increasingly connected in-vehicle display systems and addressing evolving data privacy regulations are also critical challenges that require ongoing attention and investment.

Key Players Shaping the Automotive Display Panel Market Market

- LG Display

- Samsung Display

- BOE

- Tianma

- Japan Display

- Innolux Corporation

- AUO

- Sharp Corporation

- Century

- Continental

- Nippon Seiki

- Denso

- Visteon

- Marelli

- Bosch

- Yazaki

- Faurecia

- Desay SV

- Foryou General Electronic

Significant Automotive Display Panel Market Industry Milestones

- November 2023: Hyundai Mobis Co. developed an innovative premium display for vehicles as automakers increasingly demand high-end products for in-vehicle infotainment and entertainment systems. The quantum dot and local dimming display are characterized by the large size of the screen, high definition, and slim design, using a fusion of innovative technologies targeting luxury vehicles.

- October 2023: AUO announced that it aimed to work directly with automakers toward upstream production, seeking to grasp development trends better for in-vehicle displays to compete against Chinese rivals. The company also announced the acquisition of a 100% stake in German auto parts manufacturer BHTC, which supplies Audi and other automakers.

Future Outlook for Automotive Display Panel Market Market

The future outlook for the automotive display panel market remains exceptionally bright, driven by sustained innovation and an ever-increasing demand for advanced in-vehicle technologies. The proliferation of electric vehicles and the gradual introduction of autonomous driving features will further necessitate sophisticated and intuitive display interfaces, creating a fertile ground for growth. Strategic collaborations between display manufacturers and automotive OEMs will become even more critical, fostering co-creation and faster integration of new technologies. The market is poised to witness significant advancements in display integration, with a trend towards larger, more immersive, and potentially even holographic displays. The focus on user experience, safety, and personalized in-car environments will continue to be the primary catalysts, ensuring a dynamic and expanding market for automotive display panels for years to come.

Automotive Display Panel Market Segmentation

-

1. Display Panel

-

1.1. By Technology

- 1.1.1. a-Si LCD

- 1.1.2. Oxide LCD

- 1.1.3. LTPS LCD

- 1.1.4. AMOLED

-

1.1. By Technology

-

2. Display Console/Cluster

-

2.1. By Application

- 2.1.1. Instrument Cluster

- 2.1.2. Center Stack

- 2.1.3. Heads-up Display

- 2.1.4. Other Applications

-

2.1. By Application

Automotive Display Panel Market Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia

- 4. Australia and New Zealand

- 5. Middle East and Africa

- 6. Latin America

Automotive Display Panel Market Regional Market Share

Geographic Coverage of Automotive Display Panel Market

Automotive Display Panel Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.80% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Display Panel

- 5.1.1. By Technology

- 5.1.1.1. a-Si LCD

- 5.1.1.2. Oxide LCD

- 5.1.1.3. LTPS LCD

- 5.1.1.4. AMOLED

- 5.1.1. By Technology

- 5.2. Market Analysis, Insights and Forecast - by Display Console/Cluster

- 5.2.1. By Application

- 5.2.1.1. Instrument Cluster

- 5.2.1.2. Center Stack

- 5.2.1.3. Heads-up Display

- 5.2.1.4. Other Applications

- 5.2.1. By Application

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia

- 5.3.4. Australia and New Zealand

- 5.3.5. Middle East and Africa

- 5.3.6. Latin America

- 5.1. Market Analysis, Insights and Forecast - by Display Panel

- 6. Global Automotive Display Panel Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Display Panel

- 6.1.1. By Technology

- 6.1.1.1. a-Si LCD

- 6.1.1.2. Oxide LCD

- 6.1.1.3. LTPS LCD

- 6.1.1.4. AMOLED

- 6.1.1. By Technology

- 6.2. Market Analysis, Insights and Forecast - by Display Console/Cluster

- 6.2.1. By Application

- 6.2.1.1. Instrument Cluster

- 6.2.1.2. Center Stack

- 6.2.1.3. Heads-up Display

- 6.2.1.4. Other Applications

- 6.2.1. By Application

- 6.1. Market Analysis, Insights and Forecast - by Display Panel

- 7. North America Automotive Display Panel Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Display Panel

- 7.1.1. By Technology

- 7.1.1.1. a-Si LCD

- 7.1.1.2. Oxide LCD

- 7.1.1.3. LTPS LCD

- 7.1.1.4. AMOLED

- 7.1.1. By Technology

- 7.2. Market Analysis, Insights and Forecast - by Display Console/Cluster

- 7.2.1. By Application

- 7.2.1.1. Instrument Cluster

- 7.2.1.2. Center Stack

- 7.2.1.3. Heads-up Display

- 7.2.1.4. Other Applications

- 7.2.1. By Application

- 7.1. Market Analysis, Insights and Forecast - by Display Panel

- 8. Europe Automotive Display Panel Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Display Panel

- 8.1.1. By Technology

- 8.1.1.1. a-Si LCD

- 8.1.1.2. Oxide LCD

- 8.1.1.3. LTPS LCD

- 8.1.1.4. AMOLED

- 8.1.1. By Technology

- 8.2. Market Analysis, Insights and Forecast - by Display Console/Cluster

- 8.2.1. By Application

- 8.2.1.1. Instrument Cluster

- 8.2.1.2. Center Stack

- 8.2.1.3. Heads-up Display

- 8.2.1.4. Other Applications

- 8.2.1. By Application

- 8.1. Market Analysis, Insights and Forecast - by Display Panel

- 9. Asia Automotive Display Panel Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Display Panel

- 9.1.1. By Technology

- 9.1.1.1. a-Si LCD

- 9.1.1.2. Oxide LCD

- 9.1.1.3. LTPS LCD

- 9.1.1.4. AMOLED

- 9.1.1. By Technology

- 9.2. Market Analysis, Insights and Forecast - by Display Console/Cluster

- 9.2.1. By Application

- 9.2.1.1. Instrument Cluster

- 9.2.1.2. Center Stack

- 9.2.1.3. Heads-up Display

- 9.2.1.4. Other Applications

- 9.2.1. By Application

- 9.1. Market Analysis, Insights and Forecast - by Display Panel

- 10. Australia and New Zealand Automotive Display Panel Market Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Display Panel

- 10.1.1. By Technology

- 10.1.1.1. a-Si LCD

- 10.1.1.2. Oxide LCD

- 10.1.1.3. LTPS LCD

- 10.1.1.4. AMOLED

- 10.1.1. By Technology

- 10.2. Market Analysis, Insights and Forecast - by Display Console/Cluster

- 10.2.1. By Application

- 10.2.1.1. Instrument Cluster

- 10.2.1.2. Center Stack

- 10.2.1.3. Heads-up Display

- 10.2.1.4. Other Applications

- 10.2.1. By Application

- 10.1. Market Analysis, Insights and Forecast - by Display Panel

- 11. Middle East and Africa Automotive Display Panel Market Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Display Panel

- 11.1.1. By Technology

- 11.1.1.1. a-Si LCD

- 11.1.1.2. Oxide LCD

- 11.1.1.3. LTPS LCD

- 11.1.1.4. AMOLED

- 11.1.1. By Technology

- 11.2. Market Analysis, Insights and Forecast - by Display Console/Cluster

- 11.2.1. By Application

- 11.2.1.1. Instrument Cluster

- 11.2.1.2. Center Stack

- 11.2.1.3. Heads-up Display

- 11.2.1.4. Other Applications

- 11.2.1. By Application

- 11.1. Market Analysis, Insights and Forecast - by Display Panel

- 12. Latin America Automotive Display Panel Market Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Display Panel

- 12.1.1. By Technology

- 12.1.1.1. a-Si LCD

- 12.1.1.2. Oxide LCD

- 12.1.1.3. LTPS LCD

- 12.1.1.4. AMOLED

- 12.1.1. By Technology

- 12.2. Market Analysis, Insights and Forecast - by Display Console/Cluster

- 12.2.1. By Application

- 12.2.1.1. Instrument Cluster

- 12.2.1.2. Center Stack

- 12.2.1.3. Heads-up Display

- 12.2.1.4. Other Applications

- 12.2.1. By Application

- 12.1. Market Analysis, Insights and Forecast - by Display Panel

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 LG Display

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Samsung Display

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 BOE

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 Tianma

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 Japan Display

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 Innolux Corporation

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 AUO

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 Sharp Corporation

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 Century

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 Continental

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.11 Nippon Seiki

- 13.1.11.1. Company Overview

- 13.1.11.2. Products

- 13.1.11.3. Company Financials

- 13.1.11.4. SWOT Analysis

- 13.1.12 Denso

- 13.1.12.1. Company Overview

- 13.1.12.2. Products

- 13.1.12.3. Company Financials

- 13.1.12.4. SWOT Analysis

- 13.1.13 Visteon

- 13.1.13.1. Company Overview

- 13.1.13.2. Products

- 13.1.13.3. Company Financials

- 13.1.13.4. SWOT Analysis

- 13.1.14 Marelli

- 13.1.14.1. Company Overview

- 13.1.14.2. Products

- 13.1.14.3. Company Financials

- 13.1.14.4. SWOT Analysis

- 13.1.15 Bosch

- 13.1.15.1. Company Overview

- 13.1.15.2. Products

- 13.1.15.3. Company Financials

- 13.1.15.4. SWOT Analysis

- 13.1.16 Yazaki

- 13.1.16.1. Company Overview

- 13.1.16.2. Products

- 13.1.16.3. Company Financials

- 13.1.16.4. SWOT Analysis

- 13.1.17 Faurecia

- 13.1.17.1. Company Overview

- 13.1.17.2. Products

- 13.1.17.3. Company Financials

- 13.1.17.4. SWOT Analysis

- 13.1.18 Desay SV

- 13.1.18.1. Company Overview

- 13.1.18.2. Products

- 13.1.18.3. Company Financials

- 13.1.18.4. SWOT Analysis

- 13.1.19 Foryou General Electronic

- 13.1.19.1. Company Overview

- 13.1.19.2. Products

- 13.1.19.3. Company Financials

- 13.1.19.4. SWOT Analysis

- 13.1.1 LG Display

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Global Automotive Display Panel Market Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Global Automotive Display Panel Market Volume Breakdown (Billion, %) by Region 2025 & 2033

- Figure 3: North America Automotive Display Panel Market Revenue (Million), by Display Panel 2025 & 2033

- Figure 4: North America Automotive Display Panel Market Volume (Billion), by Display Panel 2025 & 2033

- Figure 5: North America Automotive Display Panel Market Revenue Share (%), by Display Panel 2025 & 2033

- Figure 6: North America Automotive Display Panel Market Volume Share (%), by Display Panel 2025 & 2033

- Figure 7: North America Automotive Display Panel Market Revenue (Million), by Display Console/Cluster 2025 & 2033

- Figure 8: North America Automotive Display Panel Market Volume (Billion), by Display Console/Cluster 2025 & 2033

- Figure 9: North America Automotive Display Panel Market Revenue Share (%), by Display Console/Cluster 2025 & 2033

- Figure 10: North America Automotive Display Panel Market Volume Share (%), by Display Console/Cluster 2025 & 2033

- Figure 11: North America Automotive Display Panel Market Revenue (Million), by Country 2025 & 2033

- Figure 12: North America Automotive Display Panel Market Volume (Billion), by Country 2025 & 2033

- Figure 13: North America Automotive Display Panel Market Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Automotive Display Panel Market Volume Share (%), by Country 2025 & 2033

- Figure 15: Europe Automotive Display Panel Market Revenue (Million), by Display Panel 2025 & 2033

- Figure 16: Europe Automotive Display Panel Market Volume (Billion), by Display Panel 2025 & 2033

- Figure 17: Europe Automotive Display Panel Market Revenue Share (%), by Display Panel 2025 & 2033

- Figure 18: Europe Automotive Display Panel Market Volume Share (%), by Display Panel 2025 & 2033

- Figure 19: Europe Automotive Display Panel Market Revenue (Million), by Display Console/Cluster 2025 & 2033

- Figure 20: Europe Automotive Display Panel Market Volume (Billion), by Display Console/Cluster 2025 & 2033

- Figure 21: Europe Automotive Display Panel Market Revenue Share (%), by Display Console/Cluster 2025 & 2033

- Figure 22: Europe Automotive Display Panel Market Volume Share (%), by Display Console/Cluster 2025 & 2033

- Figure 23: Europe Automotive Display Panel Market Revenue (Million), by Country 2025 & 2033

- Figure 24: Europe Automotive Display Panel Market Volume (Billion), by Country 2025 & 2033

- Figure 25: Europe Automotive Display Panel Market Revenue Share (%), by Country 2025 & 2033

- Figure 26: Europe Automotive Display Panel Market Volume Share (%), by Country 2025 & 2033

- Figure 27: Asia Automotive Display Panel Market Revenue (Million), by Display Panel 2025 & 2033

- Figure 28: Asia Automotive Display Panel Market Volume (Billion), by Display Panel 2025 & 2033

- Figure 29: Asia Automotive Display Panel Market Revenue Share (%), by Display Panel 2025 & 2033

- Figure 30: Asia Automotive Display Panel Market Volume Share (%), by Display Panel 2025 & 2033

- Figure 31: Asia Automotive Display Panel Market Revenue (Million), by Display Console/Cluster 2025 & 2033

- Figure 32: Asia Automotive Display Panel Market Volume (Billion), by Display Console/Cluster 2025 & 2033

- Figure 33: Asia Automotive Display Panel Market Revenue Share (%), by Display Console/Cluster 2025 & 2033

- Figure 34: Asia Automotive Display Panel Market Volume Share (%), by Display Console/Cluster 2025 & 2033

- Figure 35: Asia Automotive Display Panel Market Revenue (Million), by Country 2025 & 2033

- Figure 36: Asia Automotive Display Panel Market Volume (Billion), by Country 2025 & 2033

- Figure 37: Asia Automotive Display Panel Market Revenue Share (%), by Country 2025 & 2033

- Figure 38: Asia Automotive Display Panel Market Volume Share (%), by Country 2025 & 2033

- Figure 39: Australia and New Zealand Automotive Display Panel Market Revenue (Million), by Display Panel 2025 & 2033

- Figure 40: Australia and New Zealand Automotive Display Panel Market Volume (Billion), by Display Panel 2025 & 2033

- Figure 41: Australia and New Zealand Automotive Display Panel Market Revenue Share (%), by Display Panel 2025 & 2033

- Figure 42: Australia and New Zealand Automotive Display Panel Market Volume Share (%), by Display Panel 2025 & 2033

- Figure 43: Australia and New Zealand Automotive Display Panel Market Revenue (Million), by Display Console/Cluster 2025 & 2033

- Figure 44: Australia and New Zealand Automotive Display Panel Market Volume (Billion), by Display Console/Cluster 2025 & 2033

- Figure 45: Australia and New Zealand Automotive Display Panel Market Revenue Share (%), by Display Console/Cluster 2025 & 2033

- Figure 46: Australia and New Zealand Automotive Display Panel Market Volume Share (%), by Display Console/Cluster 2025 & 2033

- Figure 47: Australia and New Zealand Automotive Display Panel Market Revenue (Million), by Country 2025 & 2033

- Figure 48: Australia and New Zealand Automotive Display Panel Market Volume (Billion), by Country 2025 & 2033

- Figure 49: Australia and New Zealand Automotive Display Panel Market Revenue Share (%), by Country 2025 & 2033

- Figure 50: Australia and New Zealand Automotive Display Panel Market Volume Share (%), by Country 2025 & 2033

- Figure 51: Middle East and Africa Automotive Display Panel Market Revenue (Million), by Display Panel 2025 & 2033

- Figure 52: Middle East and Africa Automotive Display Panel Market Volume (Billion), by Display Panel 2025 & 2033

- Figure 53: Middle East and Africa Automotive Display Panel Market Revenue Share (%), by Display Panel 2025 & 2033

- Figure 54: Middle East and Africa Automotive Display Panel Market Volume Share (%), by Display Panel 2025 & 2033

- Figure 55: Middle East and Africa Automotive Display Panel Market Revenue (Million), by Display Console/Cluster 2025 & 2033

- Figure 56: Middle East and Africa Automotive Display Panel Market Volume (Billion), by Display Console/Cluster 2025 & 2033

- Figure 57: Middle East and Africa Automotive Display Panel Market Revenue Share (%), by Display Console/Cluster 2025 & 2033

- Figure 58: Middle East and Africa Automotive Display Panel Market Volume Share (%), by Display Console/Cluster 2025 & 2033

- Figure 59: Middle East and Africa Automotive Display Panel Market Revenue (Million), by Country 2025 & 2033

- Figure 60: Middle East and Africa Automotive Display Panel Market Volume (Billion), by Country 2025 & 2033

- Figure 61: Middle East and Africa Automotive Display Panel Market Revenue Share (%), by Country 2025 & 2033

- Figure 62: Middle East and Africa Automotive Display Panel Market Volume Share (%), by Country 2025 & 2033

- Figure 63: Latin America Automotive Display Panel Market Revenue (Million), by Display Panel 2025 & 2033

- Figure 64: Latin America Automotive Display Panel Market Volume (Billion), by Display Panel 2025 & 2033

- Figure 65: Latin America Automotive Display Panel Market Revenue Share (%), by Display Panel 2025 & 2033

- Figure 66: Latin America Automotive Display Panel Market Volume Share (%), by Display Panel 2025 & 2033

- Figure 67: Latin America Automotive Display Panel Market Revenue (Million), by Display Console/Cluster 2025 & 2033

- Figure 68: Latin America Automotive Display Panel Market Volume (Billion), by Display Console/Cluster 2025 & 2033

- Figure 69: Latin America Automotive Display Panel Market Revenue Share (%), by Display Console/Cluster 2025 & 2033

- Figure 70: Latin America Automotive Display Panel Market Volume Share (%), by Display Console/Cluster 2025 & 2033

- Figure 71: Latin America Automotive Display Panel Market Revenue (Million), by Country 2025 & 2033

- Figure 72: Latin America Automotive Display Panel Market Volume (Billion), by Country 2025 & 2033

- Figure 73: Latin America Automotive Display Panel Market Revenue Share (%), by Country 2025 & 2033

- Figure 74: Latin America Automotive Display Panel Market Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automotive Display Panel Market Revenue Million Forecast, by Display Panel 2020 & 2033

- Table 2: Global Automotive Display Panel Market Volume Billion Forecast, by Display Panel 2020 & 2033

- Table 3: Global Automotive Display Panel Market Revenue Million Forecast, by Display Console/Cluster 2020 & 2033

- Table 4: Global Automotive Display Panel Market Volume Billion Forecast, by Display Console/Cluster 2020 & 2033

- Table 5: Global Automotive Display Panel Market Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Global Automotive Display Panel Market Volume Billion Forecast, by Region 2020 & 2033

- Table 7: Global Automotive Display Panel Market Revenue Million Forecast, by Display Panel 2020 & 2033

- Table 8: Global Automotive Display Panel Market Volume Billion Forecast, by Display Panel 2020 & 2033

- Table 9: Global Automotive Display Panel Market Revenue Million Forecast, by Display Console/Cluster 2020 & 2033

- Table 10: Global Automotive Display Panel Market Volume Billion Forecast, by Display Console/Cluster 2020 & 2033

- Table 11: Global Automotive Display Panel Market Revenue Million Forecast, by Country 2020 & 2033

- Table 12: Global Automotive Display Panel Market Volume Billion Forecast, by Country 2020 & 2033

- Table 13: Global Automotive Display Panel Market Revenue Million Forecast, by Display Panel 2020 & 2033

- Table 14: Global Automotive Display Panel Market Volume Billion Forecast, by Display Panel 2020 & 2033

- Table 15: Global Automotive Display Panel Market Revenue Million Forecast, by Display Console/Cluster 2020 & 2033

- Table 16: Global Automotive Display Panel Market Volume Billion Forecast, by Display Console/Cluster 2020 & 2033

- Table 17: Global Automotive Display Panel Market Revenue Million Forecast, by Country 2020 & 2033

- Table 18: Global Automotive Display Panel Market Volume Billion Forecast, by Country 2020 & 2033

- Table 19: Global Automotive Display Panel Market Revenue Million Forecast, by Display Panel 2020 & 2033

- Table 20: Global Automotive Display Panel Market Volume Billion Forecast, by Display Panel 2020 & 2033

- Table 21: Global Automotive Display Panel Market Revenue Million Forecast, by Display Console/Cluster 2020 & 2033

- Table 22: Global Automotive Display Panel Market Volume Billion Forecast, by Display Console/Cluster 2020 & 2033

- Table 23: Global Automotive Display Panel Market Revenue Million Forecast, by Country 2020 & 2033

- Table 24: Global Automotive Display Panel Market Volume Billion Forecast, by Country 2020 & 2033

- Table 25: Global Automotive Display Panel Market Revenue Million Forecast, by Display Panel 2020 & 2033

- Table 26: Global Automotive Display Panel Market Volume Billion Forecast, by Display Panel 2020 & 2033

- Table 27: Global Automotive Display Panel Market Revenue Million Forecast, by Display Console/Cluster 2020 & 2033

- Table 28: Global Automotive Display Panel Market Volume Billion Forecast, by Display Console/Cluster 2020 & 2033

- Table 29: Global Automotive Display Panel Market Revenue Million Forecast, by Country 2020 & 2033

- Table 30: Global Automotive Display Panel Market Volume Billion Forecast, by Country 2020 & 2033

- Table 31: Global Automotive Display Panel Market Revenue Million Forecast, by Display Panel 2020 & 2033

- Table 32: Global Automotive Display Panel Market Volume Billion Forecast, by Display Panel 2020 & 2033

- Table 33: Global Automotive Display Panel Market Revenue Million Forecast, by Display Console/Cluster 2020 & 2033

- Table 34: Global Automotive Display Panel Market Volume Billion Forecast, by Display Console/Cluster 2020 & 2033

- Table 35: Global Automotive Display Panel Market Revenue Million Forecast, by Country 2020 & 2033

- Table 36: Global Automotive Display Panel Market Volume Billion Forecast, by Country 2020 & 2033

- Table 37: Global Automotive Display Panel Market Revenue Million Forecast, by Display Panel 2020 & 2033

- Table 38: Global Automotive Display Panel Market Volume Billion Forecast, by Display Panel 2020 & 2033

- Table 39: Global Automotive Display Panel Market Revenue Million Forecast, by Display Console/Cluster 2020 & 2033

- Table 40: Global Automotive Display Panel Market Volume Billion Forecast, by Display Console/Cluster 2020 & 2033

- Table 41: Global Automotive Display Panel Market Revenue Million Forecast, by Country 2020 & 2033

- Table 42: Global Automotive Display Panel Market Volume Billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Display Panel Market?

The projected CAGR is approximately 6.80%.

2. Which companies are prominent players in the Automotive Display Panel Market?

Key companies in the market include LG Display, Samsung Display, BOE, Tianma, Japan Display, Innolux Corporation, AUO, Sharp Corporation, Century, Continental, Nippon Seiki, Denso, Visteon, Marelli, Bosch, Yazaki, Faurecia, Desay SV, Foryou General Electronic.

3. What are the main segments of the Automotive Display Panel Market?

The market segments include Display Panel, Display Console/Cluster.

4. Can you provide details about the market size?

The market size is estimated to be USD 20.75 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand for Connected Cars; Stringent Government Regulations to Reduce Car Accidents; Increasing Focus to Provide AR Experience.

6. What are the notable trends driving market growth?

The Heads-up Display Segment is Anticipated to Hold a Significant Market Share.

7. Are there any restraints impacting market growth?

Increasing Demand for Connected Cars; Stringent Government Regulations to Reduce Car Accidents; Increasing Focus to Provide AR Experience.

8. Can you provide examples of recent developments in the market?

November 2023: Hyundai Mobis Co. developed an innovative premium display for vehicles as automakers increasingly demand high-end products for in-vehicle infotainment and entertainment systems. The quantum dot and local dimming display are characterized by the large size of the screen, high definition, and slim design, using a fusion of innovative technologies targeting luxury vehicles.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Display Panel Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Display Panel Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Display Panel Market?

To stay informed about further developments, trends, and reports in the Automotive Display Panel Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence