Key Insights

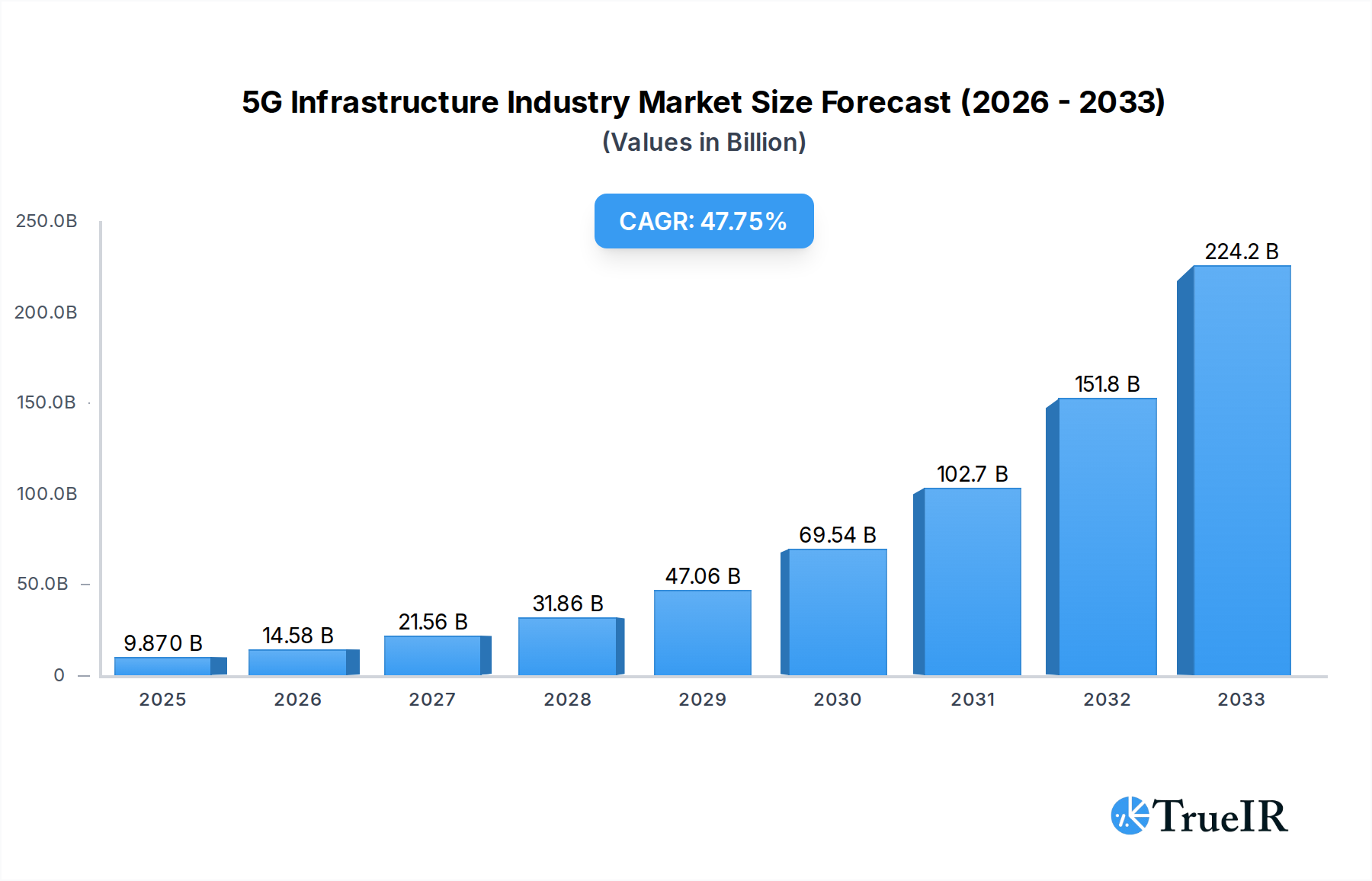

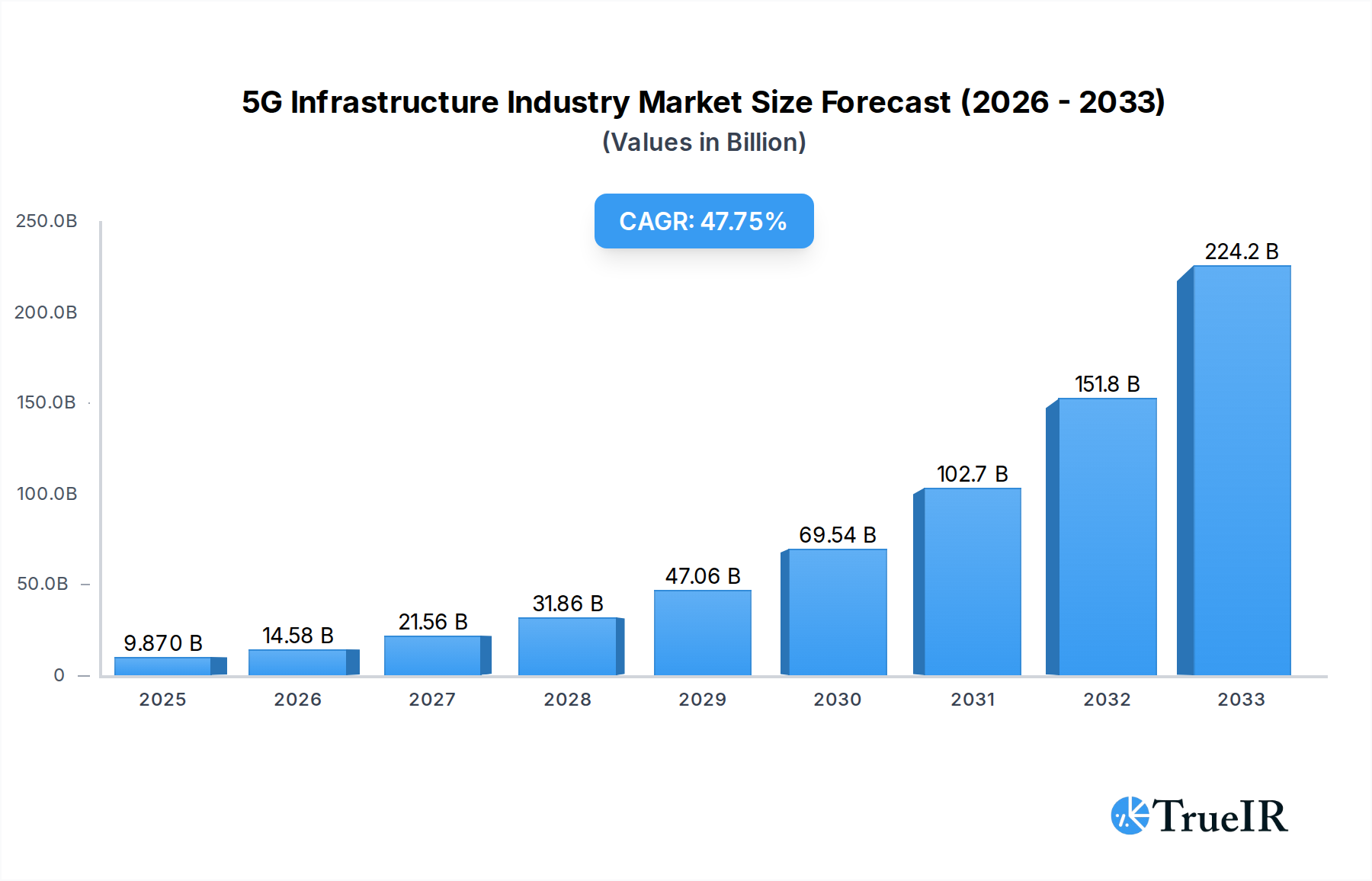

The 5G infrastructure market is poised for explosive growth, projected to reach an impressive USD 9.87 Billion by 2025. This remarkable expansion is driven by an unprecedented Compound Annual Growth Rate (CAGR) of 47.51%, indicating a rapidly accelerating adoption and deployment of 5G technologies globally. Key drivers fueling this surge include the insatiable demand for enhanced mobile broadband, mission-critical communication services, and the burgeoning Internet of Things (IoT) ecosystem. The ongoing evolution of 5G Radio Access Networks (RAN), the strategic importance of 5G Core Networks for advanced services, and the critical role of robust Transport Networks in facilitating high-speed data transfer are central to this market's trajectory. The study period, spanning from 2019 to 2033, with a base year of 2025 and a forecast period of 2025-2033, underscores a sustained and significant upward trend in investment and development within this sector. The competitive landscape is dynamic, featuring major players like Ericsson, Samsung, Huawei, Nokia, and Qualcomm, alongside innovative companies such as Mavenir and Qucell, all vying to capture market share in this high-stakes arena.

5G Infrastructure Industry Market Size (In Billion)

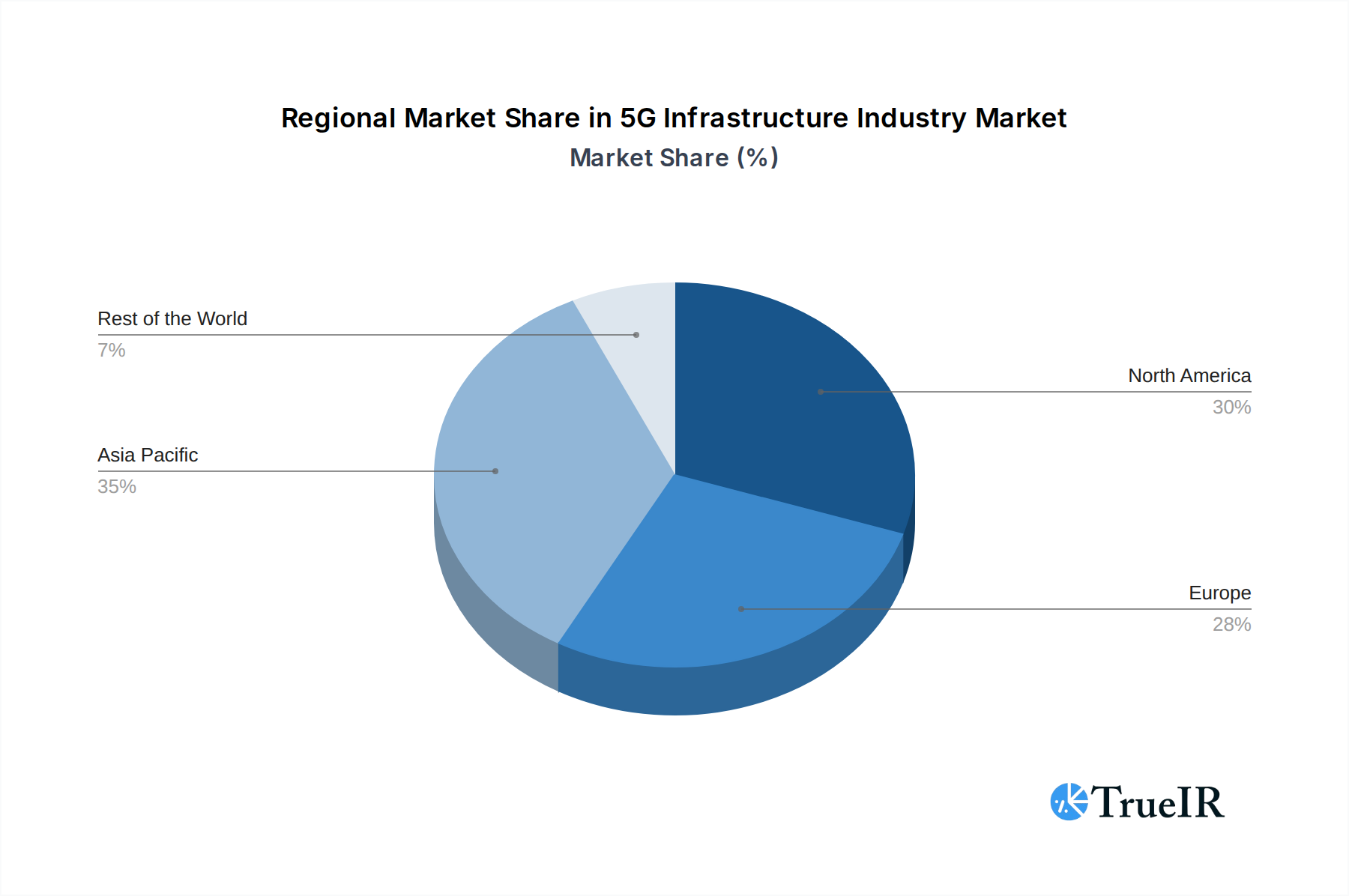

The 5G infrastructure market is characterized by significant regional variations and emerging trends. North America, particularly the United States and Canada, is expected to lead in early adoption and deployment, driven by proactive government initiatives and substantial private investment. Europe, with key markets like Germany, the UK, France, and Italy, also presents a strong growth potential, fueled by widespread 5G spectrum auctions and a growing appetite for enhanced connectivity. The Asia Pacific region, notably China, Japan, and South Korea, is a pivotal hub for 5G innovation and deployment, often setting global benchmarks. Restraints, such as the high cost of infrastructure deployment and spectrum allocation challenges, are being actively addressed through technological advancements and supportive regulatory frameworks. Emerging trends include the increasing focus on open RAN architectures, network virtualization, and edge computing, which are set to further revolutionize the 5G landscape and unlock new revenue streams for service providers and enterprises alike.

5G Infrastructure Industry Company Market Share

This in-depth report provides an unparalleled analysis of the dynamic 5G infrastructure industry, a critical enabler of the digital revolution. Delving into market structures, evolving trends, dominant segments, and key players, this study offers crucial insights for stakeholders navigating this rapidly expanding global market. We meticulously examine the 5G network deployment, 5G core network, and 5G radio access network (RAN) markets, projecting significant growth throughout the 2025–2033 forecast period, with the base year 2025. This report leverages high-volume keywords like 5G infrastructure market size, 5G deployment strategy, private 5G networks, and telecom infrastructure investment to enhance SEO visibility and engage a broad industry audience. Our study period spans from 2019–2033, encompassing historical analysis from 2019–2024.

5G Infrastructure Industry Market Structure & Competitive Landscape

The 5G infrastructure industry exhibits a moderately concentrated market structure, with a few dominant players holding significant market share, alongside a growing ecosystem of specialized vendors. Innovation is the primary driver, fueled by continuous research and development in areas like Open RAN, cloud-native architectures, and edge computing. Regulatory impacts, such as spectrum allocation policies and network security mandates, are shaping deployment strategies and market access. Product substitutes, primarily advanced 4G LTE solutions, are gradually being phased out as 5G capabilities become more compelling for enterprise and consumer applications. End-user segmentation reveals strong demand from telecommunications operators, followed by enterprise verticals like manufacturing, healthcare, and logistics seeking private 5G solutions. Mergers and acquisitions (M&A) trends are significant, with major telecommunications equipment manufacturers consolidating to enhance their portfolio and expand their global reach. For instance, M&A volumes are projected to reach an estimated 100 Million in deal value during the forecast period, reflecting strategic consolidations aimed at capturing greater market share in the 5G RAN and 5G core network segments. Concentration ratios for the top five players in the 5G infrastructure market are estimated to be around 65% in 2025.

5G Infrastructure Industry Market Trends & Opportunities

The 5G infrastructure market is poised for substantial growth, with an estimated Compound Annual Growth Rate (CAGR) of 15.8% from 2025–2033. This surge is driven by the escalating demand for higher bandwidth, lower latency, and massive connectivity to support a burgeoning array of applications, including enhanced mobile broadband (eMBB), ultra-reliable low-latency communications (URLLC), and massive machine-type communications (mMTC). Technological shifts are paramount, with the transition towards cloud-native 5G core networks and the increasing adoption of Open RAN architectures transforming the traditional vendor landscape. These advancements facilitate greater flexibility, scalability, and cost-efficiency in 5G network deployment. Consumer preferences are evolving, with a growing anticipation for immersive experiences like augmented reality (AR), virtual reality (VR), and advanced gaming, all heavily reliant on robust 5G connectivity. The competitive dynamics are intensifying, characterized by strategic partnerships, joint ventures, and a fierce race to develop and deploy cutting-edge telecom infrastructure. The market penetration rate for 5G infrastructure is expected to climb from 30% in 2025 to over 70% by 2033, presenting vast opportunities for innovative solutions and services. The global 5G infrastructure market size is projected to reach an impressive 500,000 Million by 2033.

Dominant Markets & Segments in 5G Infrastructure Industry

The 5G infrastructure industry is witnessing significant regional and segment-specific growth. North America and Asia-Pacific are emerging as dominant markets, driven by aggressive 5G spectrum auctions, substantial government investments in digital infrastructure, and a high adoption rate of advanced mobile technologies. Key growth drivers in these regions include robust policy frameworks supporting 5G deployment, a strong existing telecommunications infrastructure base, and a burgeoning demand for enhanced mobile broadband and enterprise solutions.

- 5G Radio Access Networks (RAN): This segment currently holds the largest market share and is expected to continue its dominance due to the foundational nature of RAN in establishing 5G connectivity. Growth is fueled by the ongoing rollout of 5G base stations and the increasing adoption of virtualized RAN (vRAN) and Open RAN solutions, promising greater vendor diversity and cost savings. The 5G RAN market is projected to be valued at 300,000 Million by 2033.

- 5G Core Networks: The transition to cloud-native 5G core networks is a significant trend, offering enhanced agility, scalability, and the ability to support a wider range of services. This segment is experiencing rapid growth as operators modernize their network architectures to unlock the full potential of 5G. The 5G core network market is estimated to reach 150,000 Million by 2033.

- Transport Networks: As 5G networks become denser and transmit significantly more data, the demand for high-capacity and low-latency transport networks is escalating. This includes fiber optic backhaul and fronthaul solutions crucial for connecting RAN elements to the core network. The 5G transport network market is forecasted to grow substantially, reaching 50,000 Million by 2033.

5G Infrastructure Industry Product Analysis

Product innovations in the 5G infrastructure sector are centered on enhancing network performance, flexibility, and cost-effectiveness. Key advancements include the development of next-generation 5G RAN components, such as higher frequency spectrum radios and intelligent antenna systems, designed to deliver superior speed and coverage. The evolution of cloud-native 5G core network solutions, leveraging containerization and microservices, enables greater agility and faster service deployment. Competitive advantages are increasingly derived from open and disaggregated architectures, such as Open RAN, which promote interoperability and reduce vendor lock-in, fostering innovation and customization for diverse enterprise needs.

Key Drivers, Barriers & Challenges in 5G Infrastructure Industry

Key Drivers: The primary forces propelling the 5G infrastructure market include the insatiable demand for enhanced mobile broadband (eMBB) to support high-definition streaming and gaming, the burgeoning need for ultra-reliable low-latency communications (URLLC) for industrial automation and autonomous systems, and the expansion of massive machine-type communications (mMTC) for the Internet of Things (IoT). Government initiatives and favorable regulatory policies, such as spectrum allocation and investment incentives, are also significant drivers.

Barriers & Challenges: Key challenges impacting growth include the substantial capital expenditure required for widespread 5G network deployment, estimated to be in the hundreds of billions of dollars globally. Supply chain disruptions and geopolitical tensions can also affect the availability and cost of critical components. Regulatory hurdles, including spectrum availability and licensing processes, can cause deployment delays. Furthermore, cybersecurity concerns and the need for robust network security measures present ongoing challenges. The competitive pressure among established players and emerging vendors also necessitates continuous innovation and cost optimization.

Growth Drivers in the 5G Infrastructure Industry Market

The growth of the 5G infrastructure industry is propelled by several key factors. Technologically, the pursuit of higher data speeds, lower latency, and increased connection density is driving innovation in radio access, core network architectures, and transport solutions. Economically, the immense potential for new revenue streams from enterprise services, including private 5G networks for industrial automation, smart cities, and enhanced connectivity for various sectors, fuels investment. Regulatory support, such as timely spectrum allocation and favorable policies for 5G deployment, significantly accelerates market adoption and infrastructure build-out. The increasing digitalization across industries is a major catalyst for 5G adoption.

Challenges Impacting 5G Infrastructure Industry Growth

Several challenges are impacting the growth trajectory of the 5G infrastructure industry. Regulatory complexities and inconsistencies across different regions can create deployment hurdles and delays. Supply chain issues, exacerbated by global events, can lead to component shortages and increased costs, impacting deployment timelines and profitability. Intense competitive pressures from both established players and new entrants necessitate significant R&D investment and aggressive pricing strategies. The substantial capital investment required for 5G network build-out remains a significant barrier for some operators, and concerns surrounding network security and data privacy require continuous attention and robust solutions.

Key Players Shaping the 5G Infrastructure Industry Market

- Mavenir Systems Inc

- Telefonaktiebolaget LM Ericsson

- Samsung Electronics Co Ltd

- Qucell Networks Co Ltd

- Cisco Systems Inc

- Hewlett Packard Enterprise Development LP

- CommScope Holding Company Inc

- Qualcomm Technologies Inc

- NEC Corporation

- Huawei Technologies Co Ltd

- ZTE Corporation

- Oracle Corporation

- Nokia Corporation

- Airspan Networks Inc

Significant 5G Infrastructure Industry Industry Milestones

- February 2023: Cisco and NTT Ltd. announced plans to cooperate to drive Private 5G adoption across the Automotive, Logistics, Healthcare, Retail, and Public sectors. This collaboration aims to accelerate edge connectivity through NTT's Managed Private 5G solution, combined with Intel hardware, enabling seamless integration into existing infrastructure.

- February 2023: Viettel and Qualcomm Technologies, Inc. announced a crucial milestone in their joint effort to deliver state-of-the-art 5G infrastructure globally. They completed the first versions of Viettel's 5G Distributed Unit (DU) and Radio Unit (RU) based on the Qualcomm® X100 5G RAN Accelerator Card and Qualcomm QRU100 5G RAN Platform, respectively, building on their May 2022 announcement.

Future Outlook for 5G Infrastructure Industry Market

The future outlook for the 5G infrastructure industry is exceptionally promising, driven by accelerating enterprise adoption of private 5G networks and the continued expansion of public 5G networks globally. Strategic opportunities lie in the development of specialized 5G solutions for emerging use cases such as industrial IoT, autonomous vehicles, and enhanced metaverse experiences. The ongoing evolution towards 6G technologies will also spur further innovation and investment in the underlying infrastructure. Market potential is immense, as 5G continues to evolve from a connectivity solution to a platform for unprecedented innovation across all sectors.

5G Infrastructure Industry Segmentation

-

1. Communication Infrastructure

- 1.1. 5G Radio Access Networks

- 1.2. 5G Core Networks

- 1.3. Transport Networks

5G Infrastructure Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. United Kingdom

- 2.2. Germany

- 2.3. France

- 2.4. Italy

- 2.5. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. South Korea

- 3.4. Rest of Asia Pacific

- 4. Rest of the World

5G Infrastructure Industry Regional Market Share

Geographic Coverage of 5G Infrastructure Industry

5G Infrastructure Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 47.51% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Communication Infrastructure

- 5.1.1. 5G Radio Access Networks

- 5.1.2. 5G Core Networks

- 5.1.3. Transport Networks

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. Europe

- 5.2.3. Asia Pacific

- 5.2.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Communication Infrastructure

- 6. Global 5G Infrastructure Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Communication Infrastructure

- 6.1.1. 5G Radio Access Networks

- 6.1.2. 5G Core Networks

- 6.1.3. Transport Networks

- 6.1. Market Analysis, Insights and Forecast - by Communication Infrastructure

- 7. North America 5G Infrastructure Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Communication Infrastructure

- 7.1.1. 5G Radio Access Networks

- 7.1.2. 5G Core Networks

- 7.1.3. Transport Networks

- 7.1. Market Analysis, Insights and Forecast - by Communication Infrastructure

- 8. Europe 5G Infrastructure Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Communication Infrastructure

- 8.1.1. 5G Radio Access Networks

- 8.1.2. 5G Core Networks

- 8.1.3. Transport Networks

- 8.1. Market Analysis, Insights and Forecast - by Communication Infrastructure

- 9. Asia Pacific 5G Infrastructure Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Communication Infrastructure

- 9.1.1. 5G Radio Access Networks

- 9.1.2. 5G Core Networks

- 9.1.3. Transport Networks

- 9.1. Market Analysis, Insights and Forecast - by Communication Infrastructure

- 10. Rest of the World 5G Infrastructure Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Communication Infrastructure

- 10.1.1. 5G Radio Access Networks

- 10.1.2. 5G Core Networks

- 10.1.3. Transport Networks

- 10.1. Market Analysis, Insights and Forecast - by Communication Infrastructure

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Mavenir Systems Inc

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Telefonaktiebolaget LM Ericsson

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Samsung Electronics Co Ltd

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Qucell Networks Co Ltd

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Cisco Systems Inc

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Hewlett Packard Enterprise Development LP

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 CommScope Holding Company Inc

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Qualcomm Technologies Inc

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 NEC Corporation

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Huawei Technologies Co Ltd

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.11 ZTE Corporation

- 11.1.11.1. Company Overview

- 11.1.11.2. Products

- 11.1.11.3. Company Financials

- 11.1.11.4. SWOT Analysis

- 11.1.12 Oracle Corporation

- 11.1.12.1. Company Overview

- 11.1.12.2. Products

- 11.1.12.3. Company Financials

- 11.1.12.4. SWOT Analysis

- 11.1.13 Nokia Corporation

- 11.1.13.1. Company Overview

- 11.1.13.2. Products

- 11.1.13.3. Company Financials

- 11.1.13.4. SWOT Analysis

- 11.1.14 Airspan Networks Inc

- 11.1.14.1. Company Overview

- 11.1.14.2. Products

- 11.1.14.3. Company Financials

- 11.1.14.4. SWOT Analysis

- 11.1.1 Mavenir Systems Inc

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global 5G Infrastructure Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America 5G Infrastructure Industry Revenue (Million), by Communication Infrastructure 2025 & 2033

- Figure 3: North America 5G Infrastructure Industry Revenue Share (%), by Communication Infrastructure 2025 & 2033

- Figure 4: North America 5G Infrastructure Industry Revenue (Million), by Country 2025 & 2033

- Figure 5: North America 5G Infrastructure Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: Europe 5G Infrastructure Industry Revenue (Million), by Communication Infrastructure 2025 & 2033

- Figure 7: Europe 5G Infrastructure Industry Revenue Share (%), by Communication Infrastructure 2025 & 2033

- Figure 8: Europe 5G Infrastructure Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: Europe 5G Infrastructure Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Asia Pacific 5G Infrastructure Industry Revenue (Million), by Communication Infrastructure 2025 & 2033

- Figure 11: Asia Pacific 5G Infrastructure Industry Revenue Share (%), by Communication Infrastructure 2025 & 2033

- Figure 12: Asia Pacific 5G Infrastructure Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Asia Pacific 5G Infrastructure Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Rest of the World 5G Infrastructure Industry Revenue (Million), by Communication Infrastructure 2025 & 2033

- Figure 15: Rest of the World 5G Infrastructure Industry Revenue Share (%), by Communication Infrastructure 2025 & 2033

- Figure 16: Rest of the World 5G Infrastructure Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Rest of the World 5G Infrastructure Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global 5G Infrastructure Industry Revenue Million Forecast, by Communication Infrastructure 2020 & 2033

- Table 2: Global 5G Infrastructure Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 3: Global 5G Infrastructure Industry Revenue Million Forecast, by Communication Infrastructure 2020 & 2033

- Table 4: Global 5G Infrastructure Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 5: United States 5G Infrastructure Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 6: Canada 5G Infrastructure Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 7: Global 5G Infrastructure Industry Revenue Million Forecast, by Communication Infrastructure 2020 & 2033

- Table 8: Global 5G Infrastructure Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: United Kingdom 5G Infrastructure Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Germany 5G Infrastructure Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: France 5G Infrastructure Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Italy 5G Infrastructure Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Rest of Europe 5G Infrastructure Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Global 5G Infrastructure Industry Revenue Million Forecast, by Communication Infrastructure 2020 & 2033

- Table 15: Global 5G Infrastructure Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: China 5G Infrastructure Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Japan 5G Infrastructure Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: South Korea 5G Infrastructure Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Rest of Asia Pacific 5G Infrastructure Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Global 5G Infrastructure Industry Revenue Million Forecast, by Communication Infrastructure 2020 & 2033

- Table 21: Global 5G Infrastructure Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the 5G Infrastructure Industry?

The projected CAGR is approximately 47.51%.

2. Which companies are prominent players in the 5G Infrastructure Industry?

Key companies in the market include Mavenir Systems Inc, Telefonaktiebolaget LM Ericsson, Samsung Electronics Co Ltd, Qucell Networks Co Ltd, Cisco Systems Inc, Hewlett Packard Enterprise Development LP, CommScope Holding Company Inc , Qualcomm Technologies Inc, NEC Corporation, Huawei Technologies Co Ltd, ZTE Corporation, Oracle Corporation, Nokia Corporation, Airspan Networks Inc.

3. What are the main segments of the 5G Infrastructure Industry?

The market segments include Communication Infrastructure.

4. Can you provide details about the market size?

The market size is estimated to be USD 9.87 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Machine-to-Machine/IoT Connections Due to Involvement of Various Devices; Increase in Demand for Mobile Data Services.

6. What are the notable trends driving market growth?

5G Radio Access Networks Expected to Hold Major Market Share.

7. Are there any restraints impacting market growth?

High Initial Capital Expenditure due to Deployment of Network Architecture Model and Spectrum Challenges.

8. Can you provide examples of recent developments in the market?

February 2023 - Cisco, one of the global players in technology, and NTT Ltd., an IT infrastructure and services company, announced plans to cooperate to drive Private 5G adoption across the Automotive, Logistics, Healthcare, Retail, and Public sectors. NTT and Cisco plan to co-innovate and jointly bring to market the technology and managed services that will enable business customers to deploy Private 5G successfully and achieve better company outcomes. The companies plan to accelerate edge connectivity through NTT's first-to-market, Managed Private 5G solution, combined with Intel hardware, so that Cisco and NTT customers will be able to seamlessly integrate private 5G into their pre-existing LAN/WAN/Cloud infrastructure.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "5G Infrastructure Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the 5G Infrastructure Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the 5G Infrastructure Industry?

To stay informed about further developments, trends, and reports in the 5G Infrastructure Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence