Key Insights

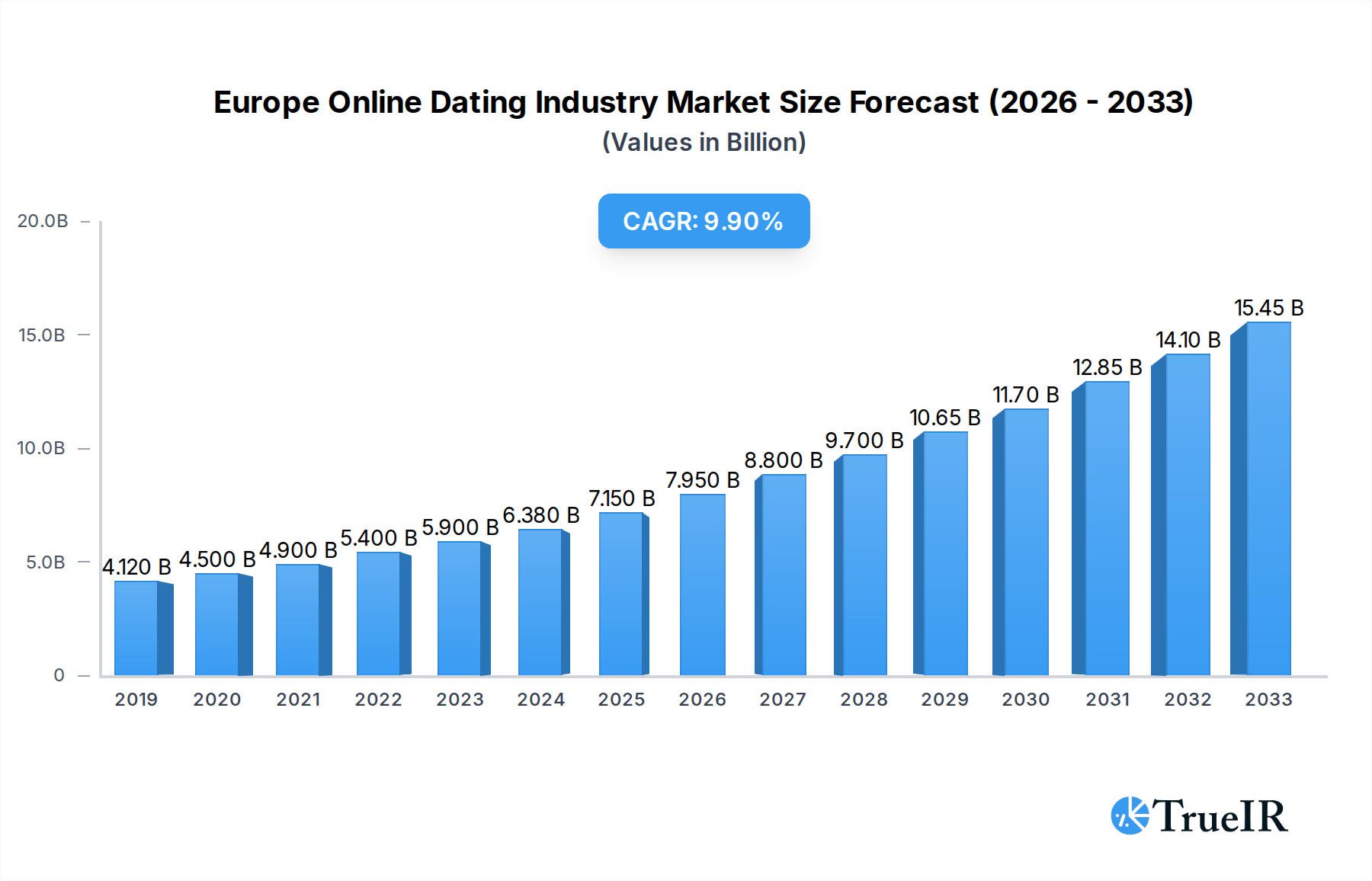

The European Online Dating industry is experiencing robust growth, projected to reach a substantial USD 7.15 billion in 2024, driven by increasing digital penetration and evolving societal attitudes towards online relationships. The market is anticipated to expand at a compound annual growth rate (CAGR) of 10.64% from 2025 to 2033, underscoring its dynamic nature and strong potential. A key driver for this expansion is the increasing comfort and acceptance of online platforms for finding romantic partners, particularly among younger demographics who are digital natives. Furthermore, advancements in technology, including AI-powered matchmaking algorithms, the integration of video dating features, and a growing emphasis on niche dating experiences catering to specific interests or demographics, are significantly fueling user engagement and acquisition. The shift towards subscription-based models and premium features within both paying and non-paying segments also contributes to revenue generation and market value. The competitive landscape is dynamic, with established players continuously innovating to capture market share.

Europe Online Dating Industry Market Size (In Billion)

The online dating market in Europe is characterized by a growing segmentation, with both non-paying and paying online dating services experiencing distinct growth trajectories. While free platforms offer broad accessibility, the paid segment is increasingly valued for its perceived higher commitment and more serious user base, leading to premium features and subscription models. Major companies like Bumble, Match Group Inc. (encompassing brands such as Tinder and Meetic), and eHarmony are actively shaping the market through strategic investments in technology and user experience. Emerging platforms and niche services are also carving out significant spaces by addressing specific user needs. Geographically, the United Kingdom, Germany, and France are leading the market, benefiting from large, tech-savvy populations and a high propensity for digital service adoption. However, other regions like Italy, Spain, and the Netherlands are rapidly catching up, indicating a widespread embrace of online dating across the continent. This sustained growth, coupled with continuous innovation, positions the European online dating market for significant and sustained expansion.

Europe Online Dating Industry Company Market Share

The Europe Online Dating Industry is characterized by a dynamic and evolving market structure, driven by increasing digital adoption and shifting consumer preferences. Market concentration is moderately high, with a few dominant players like Match Group Inc. and Bumble Inc. controlling a significant share. However, innovation remains a key driver, with new apps and features constantly emerging to cater to diverse user needs, from niche dating to casual connections. Regulatory impacts are growing, particularly concerning data privacy and security, influencing how companies operate and gather user information. Product substitutes, such as social networking platforms with dating functionalities and traditional matchmaking services, present a competitive landscape, though dedicated online dating platforms maintain their stronghold. End-user segmentation is increasingly granular, encompassing various age groups, interests, and relationship goals. Mergers and acquisitions (M&A) are a significant trend, as established players actively acquire promising startups to expand their market reach and diversify their offerings. For instance, Bumble Inc.'s acquisition of Fruitz in February 2022 highlights this strategic consolidation. Concentration ratios are estimated to be in the range of 60-70% for the top three players, with M&A volumes projected to reach several hundred million Euros annually. The competitive landscape is expected to remain intense, fostering continuous innovation and strategic partnerships.

Europe Online Dating Industry Market Trends & Opportunities

The Europe Online Dating Industry is poised for substantial growth, projected to expand from an estimated $XX billion in 2025 to $XX billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately XX% during the forecast period of 2025-2033. This robust expansion is fueled by a confluence of accelerating technological shifts, evolving consumer preferences, and dynamic competitive forces. The increasing penetration of smartphones and widespread internet access across the continent are fundamental enablers, making online dating services more accessible to a larger demographic. A significant trend is the growing adoption of AI-powered matchmaking algorithms, which enhance user experience by providing more personalized and compatible matches, leading to higher engagement and retention rates. Video dating features and virtual date functionalities have also gained traction, particularly in the wake of recent global events, offering a safer and more convenient way for users to connect before meeting in person.

Consumer preferences are shifting towards more authentic and meaningful connections, leading to the rise of niche dating apps catering to specific interests, lifestyles, or cultural backgrounds. This trend presents a significant opportunity for specialized platforms to capture market share from broader-spectrum apps. Furthermore, the increasing acceptance of online dating across all age groups, including older demographics, is a key growth catalyst. The Paying Online Dating segment is expected to witness accelerated growth as users become more willing to invest in premium features that promise higher success rates and enhanced user experiences. Conversely, the Non-paying online dating segment will continue to attract a large user base, serving as a crucial funnel for premium subscriptions.

The competitive dynamics are intensifying, with established giants like Match Group Inc. and Bumble Inc. constantly innovating and acquiring smaller players to maintain their dominance. Startups are focusing on differentiation through unique features, community building, and targeted marketing strategies. The influence of social media platforms incorporating dating features also adds another layer of complexity to the competitive landscape, pushing traditional dating apps to enhance their social integration and user engagement strategies. Market penetration rates are projected to climb steadily, reaching an estimated XX% of the adult population in key European markets by 2033. The industry's ability to adapt to evolving privacy regulations and ethical considerations will also be crucial for sustained growth and maintaining user trust.

Dominant Markets & Segments in Europe Online Dating Industry

The Europe Online Dating Industry is not a monolithic entity but rather a diverse landscape shaped by regional specificities and distinct user segments. Within the overarching market, the Paying Online Dating segment is anticipated to be a dominant force, driven by a growing consumer willingness to invest in services that promise enhanced compatibility, advanced features, and a higher probability of finding a suitable partner. Users are increasingly recognizing the value proposition of paid services, which often offer more sophisticated search filters, unlimited messaging, and profile visibility boosts, contributing to a more efficient and curated dating experience. This segment is expected to grow at a faster CAGR than its non-paying counterpart, reflecting a maturing market where users prioritize quality over free access.

Conversely, the Non-paying online dating segment will continue to serve as the foundational layer of the industry, attracting a vast user base who are either exploring their options, seeking casual connections, or have budget constraints. These platforms act as crucial entry points, often converting free users to paid subscribers as their dating journey progresses and their commitment deepens. The sheer volume of users in the non-paying segment ensures its continued relevance and contribution to the overall market size.

Geographically, Western European countries such as the United Kingdom, Germany, France, and Spain are projected to remain dominant markets due to their large, digitally connected populations, high disposable incomes, and a more open societal attitude towards online dating. Infrastructure plays a pivotal role, with widespread internet penetration and robust mobile network coverage facilitating seamless access to dating applications. Supportive policies related to digital services and consumer protection also contribute to market maturity. The increasing adoption of smartphones, particularly among younger demographics, and the normalization of online dating as a primary means of forming relationships further bolster these regions' dominance.

Key growth drivers within these dominant markets include:

- High Disposable Incomes: Enabling greater spending on premium dating services.

- Technological Infrastructure: Widespread internet and mobile connectivity.

- Societal Acceptance: A more open and progressive attitude towards online dating.

- Younger Demographics: High smartphone adoption and digital native users actively seeking partners online.

- Urbanization: Concentration of populations in urban centers, leading to a larger pool of potential matches.

The continued expansion of these dominant markets, coupled with the inherent growth potential within both paying and non-paying segments, will shape the future trajectory of the Europe Online Dating Industry.

Europe Online Dating Industry Product Analysis

The Europe Online Dating Industry is witnessing a surge in product innovation, with companies focusing on enhancing user experience through advanced technological features and tailored functionalities. AI-powered matchmaking algorithms are becoming increasingly sophisticated, analyzing user behavior, preferences, and compatibility factors to deliver more accurate and personalized match suggestions. The integration of video dating, live streaming, and augmented reality (AR) elements is transforming the way users interact, making virtual connections more engaging and authentic. Competitive advantages are being carved out through features that prioritize user safety, such as robust verification processes and in-app reporting tools, as well as those that foster genuine connections, like icebreaker prompts and shared interest matching. The ability to cater to niche demographics and specific relationship goals, such as serious long-term relationships versus casual dating, also provides a distinct market advantage. Product differentiation is increasingly achieved through unique user interfaces, gamified elements, and community-building functionalities that encourage sustained engagement.

Key Drivers, Barriers & Challenges in Europe Online Dating Industry

Key Drivers:

The Europe Online Dating Industry is propelled by several key drivers. Technological advancements, particularly the proliferation of smartphones and high-speed internet, have made online dating universally accessible. Shifting societal norms have normalized online dating as a legitimate and often preferred method for finding romantic partners. Economic factors, including increasing disposable incomes, allow more individuals to invest in premium dating services. Demographic shifts, such as a rising number of single households and later marriages, further fuel demand. The convenience and efficiency offered by online platforms, compared to traditional methods, are also significant drivers.

Barriers & Challenges:

Despite robust growth, the industry faces significant challenges. Data privacy concerns and regulatory hurdles, particularly the General Data Protection Regulation (GDPR), impose strict requirements on data handling, increasing compliance costs and operational complexity. Intense competition from a saturated market and new entrants necessitates continuous innovation and significant marketing investment. User safety and trust remain paramount challenges, with issues like catfishing and online harassment requiring ongoing vigilance and robust security measures. Achieving genuine user engagement and retention in a highly competitive digital space is also a constant battle. Supply chain issues are less directly relevant to the digital nature of the industry, but reliance on third-party cloud services could be a minor consideration.

Growth Drivers in the Europe Online Dating Industry Market

Several powerful growth drivers are propelling the Europe Online Dating Industry forward. Ubiquitous smartphone penetration and widespread internet access are foundational, enabling seamless access for a vast population. Evolving societal attitudes towards online dating have demystified and normalized its use across all age groups, fostering greater adoption. Technological innovations, such as AI-driven matchmaking, video calling, and enhanced profile customization, significantly improve user experience and engagement. Economic prosperity and increasing disposable incomes in key European markets allow for greater investment in premium dating features and subscriptions. Furthermore, shifting demographic trends, including delayed marriages and an increasing preference for personalized relationship seeking, create sustained demand for online dating solutions.

Challenges Impacting Europe Online Dating Industry Growth

The Europe Online Dating Industry encounters several challenges that can impact its growth trajectory. Stringent data privacy regulations, notably GDPR, impose significant compliance burdens and can limit data utilization for personalized marketing and algorithm development. Intense market saturation and fierce competition from both established players and emerging niche applications demand continuous innovation and substantial marketing expenditure to capture and retain user attention. Maintaining user trust and ensuring safety remain critical, with ongoing efforts required to combat fake profiles, harassment, and other online malicious activities, which can deter new users and lead to churn. The cyclical nature of dating and potential user fatigue with existing platforms present a constant challenge in maintaining sustained user engagement.

Key Players Shaping the Europe Online Dating Industry Market

- Bumble Inc.

- Match Group Inc.

- eHarmony

- Hinge Inc.

- PLENTYOFFISH

- LOVOO GmbH

- Meetic

- Badoo

- Tinder

- happn

- Ok Cupid

Significant Europe Online Dating Industry Industry Milestones

- February 2022: Bumble Inc. announced the acquisition of Fruitz, a rapidly growing dating app popular among Gen Z consumers, underscoring the strategic importance of acquiring innovative and youth-focused platforms to drive market expansion and cater to evolving user demographics.

Future Outlook for Europe Online Dating Industry Market

The future outlook for the Europe Online Dating Industry is exceptionally promising, driven by continuous technological innovation and a deepening societal acceptance of digital matchmaking. Strategic opportunities lie in further leveraging AI for hyper-personalized user experiences, enhancing safety features through advanced verification and moderation, and expanding into underserved niche markets. The integration of augmented reality for more immersive virtual dates and the development of community-centric platforms that foster genuine connections are expected to be key growth catalysts. As digital penetration deepens and consumer trust solidifies, the market potential for online dating services across Europe remains substantial, with continued growth anticipated in both established and emerging markets, further solidifying its role in modern courtship.

Europe Online Dating Industry Segmentation

-

1. Type

- 1.1. Non- paying online dating

- 1.2. Paying Online Dating

Europe Online Dating Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Online Dating Industry Regional Market Share

Geographic Coverage of Europe Online Dating Industry

Europe Online Dating Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.64% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Non- paying online dating

- 5.1.2. Paying Online Dating

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Europe Online Dating Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Non- paying online dating

- 6.1.2. Paying Online Dating

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Bumble

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Match Group Inc

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 eHarmony

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Hinge Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 PLENTYOFFISH

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 LOVOO GmbH

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Meetic

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Badoo

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Tinder

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 happn

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Ok Cupid*List Not Exhaustive

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.1 Bumble

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe Online Dating Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Europe Online Dating Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Online Dating Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Europe Online Dating Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Europe Online Dating Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 4: Europe Online Dating Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 5: United Kingdom Europe Online Dating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 6: Germany Europe Online Dating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 7: France Europe Online Dating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Italy Europe Online Dating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Spain Europe Online Dating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Netherlands Europe Online Dating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Belgium Europe Online Dating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Sweden Europe Online Dating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Norway Europe Online Dating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Poland Europe Online Dating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Denmark Europe Online Dating Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Online Dating Industry?

The projected CAGR is approximately 10.64%.

2. Which companies are prominent players in the Europe Online Dating Industry?

Key companies in the market include Bumble, Match Group Inc, eHarmony, Hinge Inc, PLENTYOFFISH, LOVOO GmbH, Meetic, Badoo, Tinder, happn, Ok Cupid*List Not Exhaustive.

3. What are the main segments of the Europe Online Dating Industry?

The market segments include Type .

4. Can you provide details about the market size?

The market size is estimated to be USD 6.38 billion as of 2022.

5. What are some drivers contributing to market growth?

Continuous Innovation in Service Offerings; Growing Penetration of Smartphones and Mobile Devices.

6. What are the notable trends driving market growth?

Non Paying Online Dating to Show Significant Growth.

7. Are there any restraints impacting market growth?

Rising fake accounts is set to create hurdles for the Online Dating Services Market..

8. Can you provide examples of recent developments in the market?

February 2022 - Bumble Inc announced the acquisition of Fruitz, one of Europe's fastest-growing dating apps. The dating app is popular with Gen Z, a growing segment of online dating consumers. Such acquisitions by the major players in the region are promoting the growth of inline dating app services.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Online Dating Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Online Dating Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Online Dating Industry?

To stay informed about further developments, trends, and reports in the Europe Online Dating Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence