Key Insights

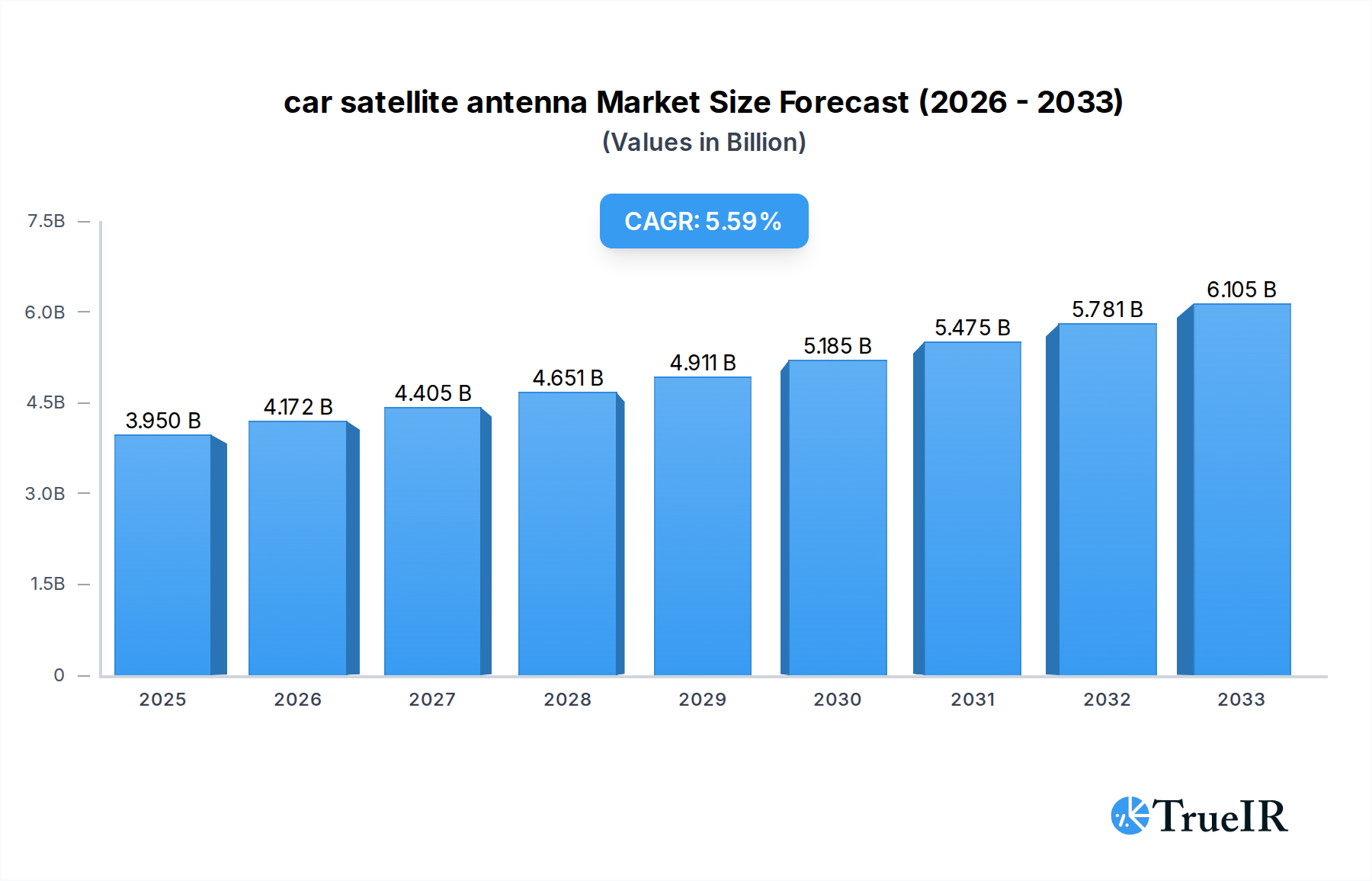

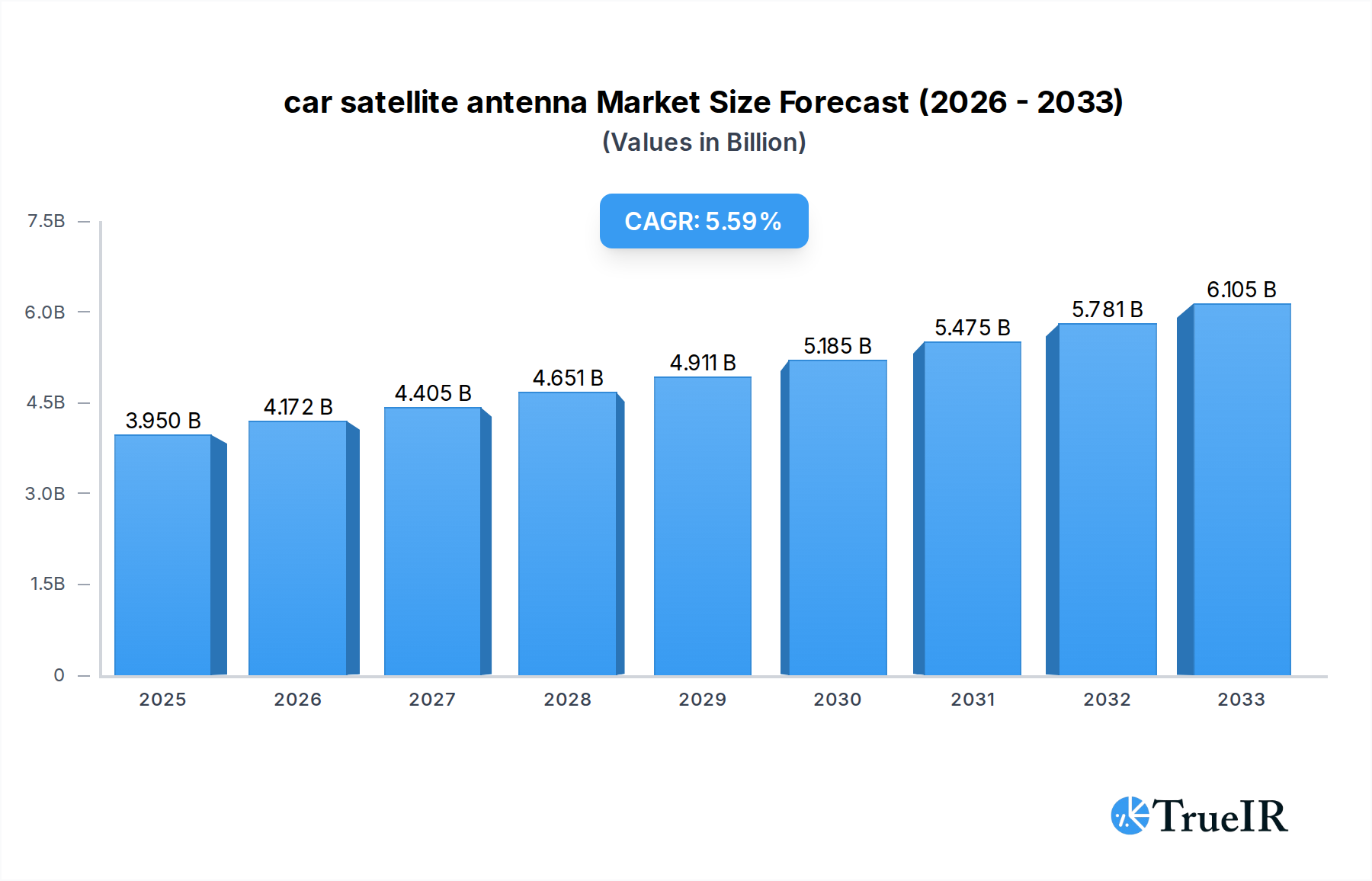

The automotive satellite antenna market is poised for significant expansion, projected to reach an estimated $3.95 billion in 2025. This robust growth is underpinned by a compelling Compound Annual Growth Rate (CAGR) of 5.56% from 2019 to 2033, indicating a sustained upward trajectory. The primary catalyst for this expansion is the increasing integration of advanced connectivity features in vehicles, driven by evolving consumer demand for seamless infotainment, navigation, and telematics services. Passenger vehicles are emerging as a dominant application segment, fueled by the widespread adoption of sophisticated GPS and SDARS (Satellite Digital Audio Radio Service) antennas. These antennas are becoming indispensable for in-car entertainment systems, real-time traffic updates, and emergency communication, directly contributing to the market's buoyancy.

car satellite antenna Market Size (In Billion)

The market is characterized by several key trends and drivers that will shape its future landscape. The growing prevalence of connected car technologies, including autonomous driving features and enhanced safety systems, necessitates reliable and high-performance satellite communication capabilities. Furthermore, the increasing demand for premium audio experiences through satellite radio is a significant market stimulant. While the market exhibits strong growth potential, certain restraints need to be considered. These include the ongoing development and adoption of alternative communication technologies like 5G, which could potentially offer competing solutions for certain in-vehicle connectivity needs. However, the specialized nature and established infrastructure of satellite communication for specific applications, such as broadcast radio and robust navigation, are expected to maintain its relevance and drive continued market penetration. Key players like Molex, Harada, and Yokowa are actively investing in innovation to meet the escalating demand for miniaturized, efficient, and cost-effective satellite antenna solutions.

car satellite antenna Company Market Share

car satellite antenna Market Structure & Competitive Landscape

The global car satellite antenna market exhibits a moderately consolidated structure, with a few dominant players holding significant market share, estimated to be around 65% of the total market value. Key players like Molex, Harada, and Yokowa are at the forefront, driving innovation and influencing market trends. The competitive landscape is shaped by a continuous influx of new technologies, particularly in signal reception and miniaturization, alongside stringent regulatory requirements for automotive safety and connectivity. Product substitutes, while limited in direct functionality, include integrated antenna solutions and alternative positioning technologies that may impact dedicated satellite antenna demand in niche applications. End-user segmentation reveals a strong preference for Passenger Vehicles, accounting for approximately 75% of the market revenue. Mergers and acquisitions (M&A) remain a strategic tool for market expansion and technology acquisition, with an estimated 30 M&A deals recorded between 2021 and 2024, involving a total transaction value of over $1 billion.

- Market Concentration: Moderate, with top 3 players holding ~65% market share.

- Innovation Drivers: Miniaturization, enhanced signal reception, integration capabilities.

- Regulatory Impacts: Automotive safety standards, emissions regulations, connectivity mandates.

- Product Substitutes: Integrated antenna solutions, alternative navigation technologies.

- End-User Segmentation: Passenger Vehicles (dominant), Commercial Vehicles.

- M&A Trends: Active, with significant transaction volumes and strategic acquisitions for technology integration.

car satellite antenna Market Trends & Opportunities

The car satellite antenna market is poised for substantial growth, projected to reach a valuation exceeding $10 billion by 2033. This expansion is driven by a Compound Annual Growth Rate (CAGR) of approximately 8.5% from the base year of 2025. The increasing penetration of advanced in-car infotainment systems, navigation technologies, and connected car services is a primary catalyst. Consumers are increasingly demanding seamless connectivity for GPS navigation, real-time traffic updates, satellite radio (SDARS), and emerging telematics applications. Technological advancements are central to this growth trajectory. The development of smaller, more efficient, and multi-functional antennas that can integrate GPS, cellular, Wi-Fi, and SDARS capabilities is a key trend. Furthermore, the shift towards electric vehicles (EVs) presents a unique opportunity, as EVs often require optimized antenna placement and integration due to battery placement and unique structural designs. This trend is expected to accelerate adoption of advanced antenna solutions.

The demand for robust and reliable satellite communication is also being fueled by the evolution of autonomous driving systems. While not directly responsible for autonomous functions, satellite antennas play a crucial role in providing accurate location data and communication redundancy for vehicle-to-everything (V2X) communication, which is foundational for the safe operation of self-driving vehicles. The global rollout of 5G infrastructure also indirectly benefits the car satellite antenna market by enhancing the overall connected car ecosystem, creating a synergistic demand for various connectivity components, including satellite antennas.

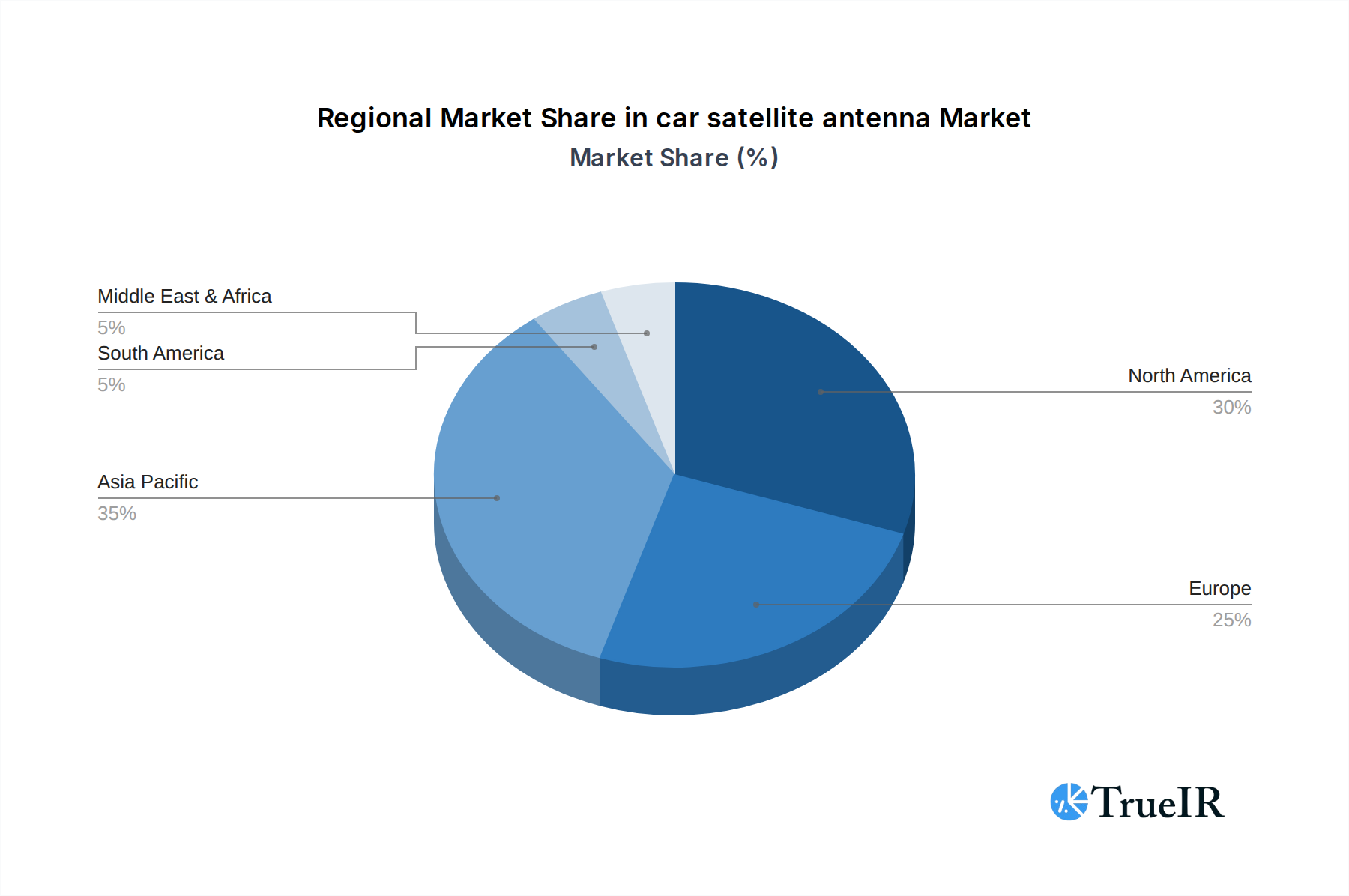

Consumer preferences are evolving towards aesthetically pleasing, low-profile antennas that blend seamlessly with vehicle design. This is pushing manufacturers to invest in research and development for aesthetically superior and aerodynamically optimized solutions. The increasing regulatory focus on vehicle safety and data privacy also necessitates reliable and secure communication channels, further bolstering the demand for high-performance satellite antennas. Regions with strong automotive manufacturing bases and high adoption rates of advanced vehicle features are expected to lead this growth. For instance, North America and Europe are currently leading markets due to their established automotive industries and early adoption of connected car technologies. Asia Pacific is anticipated to emerge as a high-growth region, driven by the rapidly expanding automotive sector in countries like China and India, and increasing disposable incomes leading to a higher demand for feature-rich vehicles.

The competitive dynamics are characterized by intense R&D investments, strategic partnerships between antenna manufacturers and automotive OEMs, and a growing emphasis on providing end-to-end connectivity solutions. Companies are focusing on developing antennas that offer superior performance in challenging environments, such as urban canyons and dense foliage, to ensure uninterrupted signal reception. The market penetration rate for GPS antennas is already high, exceeding 90% in new passenger vehicles, while the penetration for integrated GPS and SDARS antennas is steadily growing, projected to reach over 70% in the forecast period. This sustained growth in demand, coupled with ongoing technological advancements and evolving consumer needs, paints a very positive outlook for the car satellite antenna market in the coming years. The total market size is expected to grow from approximately $6 billion in 2025 to over $10 billion by 2033.

Dominant Markets & Segments in car satellite antenna

The car satellite antenna market is characterized by the clear dominance of the Passenger Vehicle segment, which commands an estimated 75% of the global market share. This segment's stronghold is attributed to the ubiquitous integration of navigation, infotainment, and increasingly, safety features in personal transportation. The rising global automotive production, particularly in emerging economies, directly fuels the demand for car satellite antennas. Infrastructure development, such as the expansion of road networks and the increasing density of smart cities, further necessitates reliable GPS and navigation capabilities, driving adoption within passenger vehicles. Policies promoting connected car technologies and vehicle safety initiatives also act as significant growth catalysts.

Within the types of car satellite antennas, the GPS Antenna segment currently holds the largest market share, estimated at around 55%. Its widespread use in navigation systems and location-based services makes it indispensable. However, the GPS and SDARS Antenna segment is exhibiting a more rapid growth trajectory. This is driven by the increasing consumer demand for integrated solutions that offer both precise positioning and enhanced entertainment options through satellite digital audio broadcasting. As automotive manufacturers strive to simplify vehicle architectures and reduce costs, the demand for integrated antenna modules is expected to rise, contributing to the accelerated growth of this segment.

Geographically, North America and Europe have historically been dominant markets for car satellite antennas. This dominance is sustained by mature automotive industries, high per capita income leading to greater adoption of premium vehicle features, and well-established regulatory frameworks supporting advanced automotive technologies. For instance, the United States, with its vast road network and high passenger vehicle ownership, represents a significant market for GPS-enabled devices. Germany, a leading automotive manufacturing hub, consistently drives demand for advanced antenna solutions.

However, the Asia Pacific region is rapidly emerging as a key growth engine. The burgeoning automotive production in countries like China, India, and South Korea, coupled with increasing government initiatives to promote smart transportation and connected vehicles, is significantly expanding the market for car satellite antennas in this region. China, in particular, is a massive market for both passenger and commercial vehicles, and its rapid technological advancements in the automotive sector are making it a crucial battleground for antenna manufacturers. The increasing disposable income and a growing middle class in these nations are leading to a higher demand for feature-rich vehicles, thereby boosting the adoption of satellite antenna technologies.

- Dominant Application Segment: Passenger Vehicle (approx. 75% market share).

- Key Growth Drivers: Rising global automotive production, demand for in-car infotainment and navigation, smart city initiatives, supportive government policies.

- Dominant Antenna Type Segment (Current): GPS Antenna (approx. 55% market share).

- Fastest Growing Antenna Type Segment: GPS and SDARS Antenna.

- Key Growth Drivers: Consumer preference for integrated solutions, cost reduction initiatives by OEMs, increasing adoption of satellite radio.

- Dominant Regions (Historical & Current): North America, Europe.

- Key Growth Drivers: Mature automotive industries, high disposable incomes, advanced technological adoption, stringent safety regulations.

- High Growth Potential Region: Asia Pacific.

- Key Growth Drivers: Rapidly expanding automotive sector, government support for smart transportation, increasing middle-class consumer base.

car satellite antenna Product Analysis

Car satellite antennas are undergoing rapid innovation, focusing on enhanced performance, miniaturization, and multi-functionality. Key advancements include the development of active antennas with integrated amplifiers for improved signal reception, particularly in challenging environments. Manufacturers are also focusing on aerodynamic designs and robust materials to withstand extreme weather conditions and vehicle vibrations. The integration of multiple antenna functions, such as GPS, SDARS, cellular, and Wi-Fi, into a single compact unit is a significant trend, offering cost and space savings for automotive manufacturers. These advancements are driven by the increasing complexity of in-car electronics and the demand for seamless connectivity. Competitive advantages lie in superior signal integrity, smaller form factors, lower power consumption, and ease of integration into diverse vehicle platforms.

Key Drivers, Barriers & Challenges in car satellite antenna

Key Drivers: The car satellite antenna market is propelled by several key drivers. The relentless advancement of connected car technologies, including GPS navigation, telematics, and V2X communication, is a primary growth catalyst. Increasing consumer demand for in-car entertainment and information services, such as satellite radio (SDARS), further fuels adoption. Government mandates and regulations promoting vehicle safety and connectivity also play a crucial role. Furthermore, the ongoing transition to electric vehicles (EVs) necessitates optimized antenna solutions due to their unique design considerations.

Barriers & Challenges: Despite strong growth prospects, the market faces several challenges. Intense price competition among manufacturers and the increasing commoditization of basic GPS antennas can put pressure on profit margins, estimated at 15% for standard GPS antennas. Supply chain disruptions, as witnessed in recent years, can impact production timelines and costs. Evolving regulatory landscapes in different regions require continuous adaptation and compliance, adding to development expenses. Moreover, the development of more sophisticated antenna technologies demands significant R&D investment, creating a barrier for smaller players. The threat of integration of multiple functionalities into single electronic modules by Tier-1 suppliers could also pose a long-term challenge to dedicated antenna suppliers.

Growth Drivers in the car satellite antenna Market

The car satellite antenna market's growth is significantly driven by the continuous expansion of the connected car ecosystem. The increasing sophistication of in-car infotainment systems, coupled with the growing adoption of advanced navigation and real-time traffic information services, directly boosts the demand for reliable satellite antennas. Furthermore, government initiatives worldwide promoting vehicle safety and the implementation of V2X communication protocols are creating a strong pull for robust positioning and communication solutions. The burgeoning electric vehicle (EV) market also presents a unique growth opportunity, as EVs often require specialized antenna designs for optimal integration and performance, driving innovation in this sector. The projected market size for connected car services is expected to exceed $500 billion by 2030, indirectly benefiting the antenna market.

Challenges Impacting car satellite antenna Growth

Several challenges are impacting the growth trajectory of the car satellite antenna market. The intense competition among numerous manufacturers leads to significant price pressures, particularly for standard GPS antennas, with average selling prices declining by approximately 5% annually in the historical period. Supply chain vulnerabilities, including the availability of critical raw materials and electronic components, can disrupt production and increase lead times, impacting revenue streams. Evolving and sometimes fragmented global regulatory frameworks for automotive electronics require continuous investment in research and development to ensure compliance, adding to operational costs. Moreover, the increasing consolidation of automotive electronics suppliers, who may offer integrated solutions, poses a competitive threat to specialized antenna manufacturers.

Key Players Shaping the car satellite antenna Market

- Molex

- Harada

- Yokowa

- Kathrein

- Northeast Industries

- Hirschmann

- ASK Industries

- Fiamm

- Suzhong Antenna Group

- Inzi Controls

- Shenglu

Significant car satellite antenna Industry Milestones

- 2019: Launch of multi-band GPS antennas offering enhanced accuracy in urban environments.

- 2020: Development of compact, shark-fin style antennas integrating GPS, cellular, and Wi-Fi capabilities.

- 2021: Increased focus on antenna miniaturization for integration into vehicle dashboards and pillars.

- 2022: Introduction of antennas with improved resistance to electromagnetic interference (EMI) for electric vehicles.

- 2023: Advancements in active antenna technology with integrated low-noise amplifiers (LNAs) for superior signal gain.

- 2024: Growing trend towards integration of 5G connectivity antennas alongside traditional satellite antennas.

Future Outlook for car satellite antenna Market

The future outlook for the car satellite antenna market is exceptionally robust, driven by the relentless evolution of connected car technologies and autonomous driving systems. The projected market size of over $10 billion by 2033 signifies substantial growth potential. Key opportunities lie in the development of highly integrated, multi-functional antennas that cater to the increasing demand for seamless connectivity in vehicles. The growing adoption of 5G and the increasing complexity of vehicle sensor suites will further necessitate advanced antenna solutions for both positioning and communication. Strategic partnerships between antenna manufacturers and automotive OEMs, along with continuous innovation in miniaturization and performance, will be critical for capturing market share and capitalizing on the expanding connected car landscape.

car satellite antenna Segmentation

-

1. Application

- 1.1. Passenger Vehicle

- 1.2. Commercial Vehicle

-

2. Types

- 2.1. GPS Antenna

- 2.2. GPS and SDARS Antenna

car satellite antenna Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

car satellite antenna Regional Market Share

Geographic Coverage of car satellite antenna

car satellite antenna REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.56% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global car satellite antenna Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Passenger Vehicle

- 5.1.2. Commercial Vehicle

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. GPS Antenna

- 5.2.2. GPS and SDARS Antenna

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America car satellite antenna Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Passenger Vehicle

- 6.1.2. Commercial Vehicle

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. GPS Antenna

- 6.2.2. GPS and SDARS Antenna

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America car satellite antenna Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Passenger Vehicle

- 7.1.2. Commercial Vehicle

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. GPS Antenna

- 7.2.2. GPS and SDARS Antenna

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe car satellite antenna Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Passenger Vehicle

- 8.1.2. Commercial Vehicle

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. GPS Antenna

- 8.2.2. GPS and SDARS Antenna

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa car satellite antenna Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Passenger Vehicle

- 9.1.2. Commercial Vehicle

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. GPS Antenna

- 9.2.2. GPS and SDARS Antenna

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific car satellite antenna Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Passenger Vehicle

- 10.1.2. Commercial Vehicle

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. GPS Antenna

- 10.2.2. GPS and SDARS Antenna

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Molex

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Harada

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Yokowa

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Kathrein

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Northeast Industries

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Hirschmann

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 ASK Industries

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Fiamm

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Suzhong Antenna Group

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Inzi Controls

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Shenglu

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.1 Molex

List of Figures

- Figure 1: Global car satellite antenna Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America car satellite antenna Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America car satellite antenna Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America car satellite antenna Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America car satellite antenna Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America car satellite antenna Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America car satellite antenna Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America car satellite antenna Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America car satellite antenna Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America car satellite antenna Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America car satellite antenna Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America car satellite antenna Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America car satellite antenna Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe car satellite antenna Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe car satellite antenna Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe car satellite antenna Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe car satellite antenna Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe car satellite antenna Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe car satellite antenna Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa car satellite antenna Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa car satellite antenna Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa car satellite antenna Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa car satellite antenna Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa car satellite antenna Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa car satellite antenna Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific car satellite antenna Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific car satellite antenna Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific car satellite antenna Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific car satellite antenna Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific car satellite antenna Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific car satellite antenna Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global car satellite antenna Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global car satellite antenna Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global car satellite antenna Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global car satellite antenna Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global car satellite antenna Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global car satellite antenna Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States car satellite antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada car satellite antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico car satellite antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global car satellite antenna Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global car satellite antenna Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global car satellite antenna Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil car satellite antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina car satellite antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America car satellite antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global car satellite antenna Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global car satellite antenna Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global car satellite antenna Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom car satellite antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany car satellite antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France car satellite antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy car satellite antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain car satellite antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia car satellite antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux car satellite antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics car satellite antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe car satellite antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global car satellite antenna Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global car satellite antenna Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global car satellite antenna Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey car satellite antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel car satellite antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC car satellite antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa car satellite antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa car satellite antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa car satellite antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global car satellite antenna Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global car satellite antenna Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global car satellite antenna Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China car satellite antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India car satellite antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan car satellite antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea car satellite antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN car satellite antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania car satellite antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific car satellite antenna Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the car satellite antenna?

The projected CAGR is approximately 5.56%.

2. Which companies are prominent players in the car satellite antenna?

Key companies in the market include Molex, Harada, Yokowa, Kathrein, Northeast Industries, Hirschmann, ASK Industries, Fiamm, Suzhong Antenna Group, Inzi Controls, Shenglu.

3. What are the main segments of the car satellite antenna?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4350.00, USD 6525.00, and USD 8700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "car satellite antenna," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the car satellite antenna report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the car satellite antenna?

To stay informed about further developments, trends, and reports in the car satellite antenna, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence