Key Insights

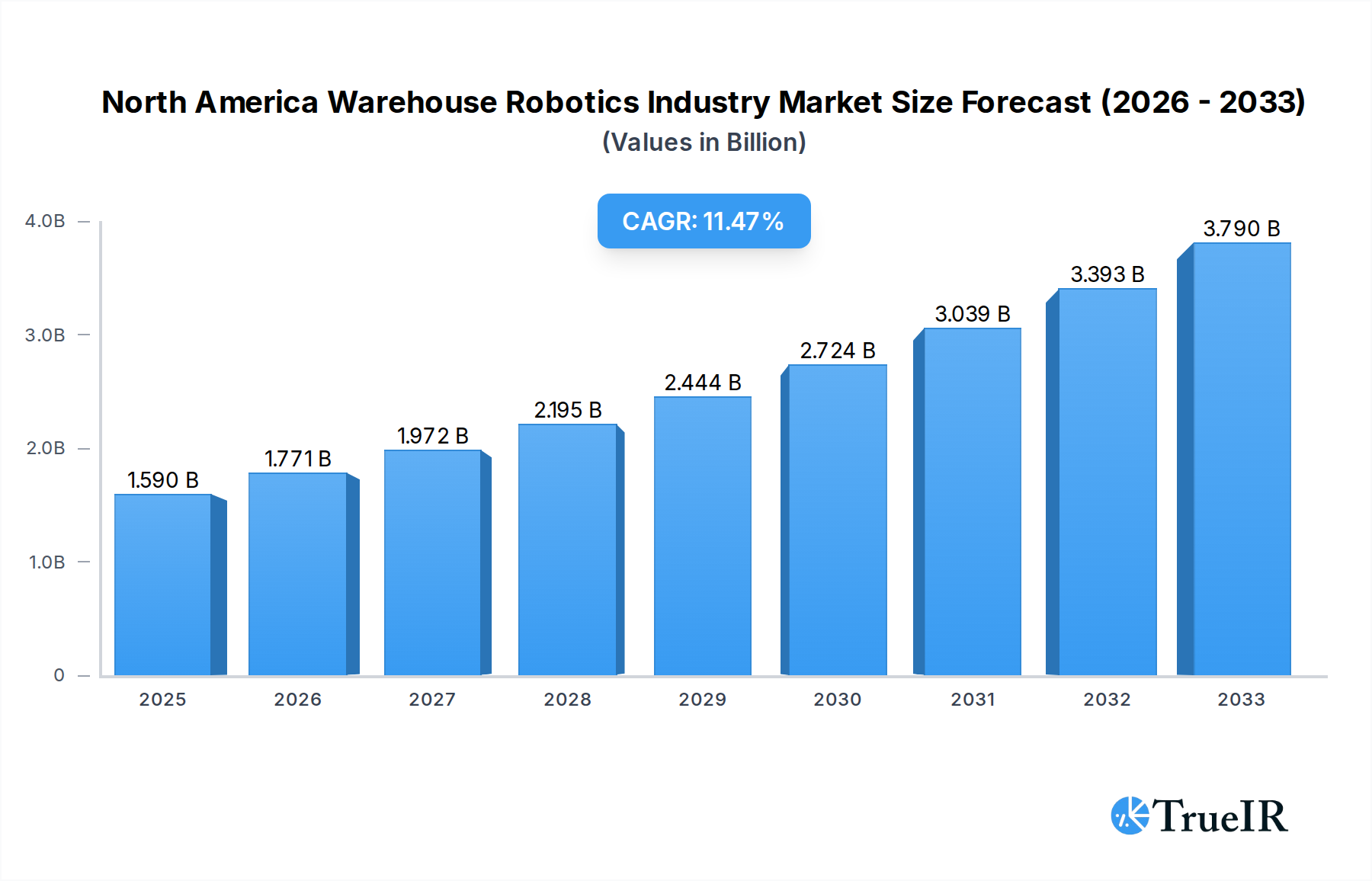

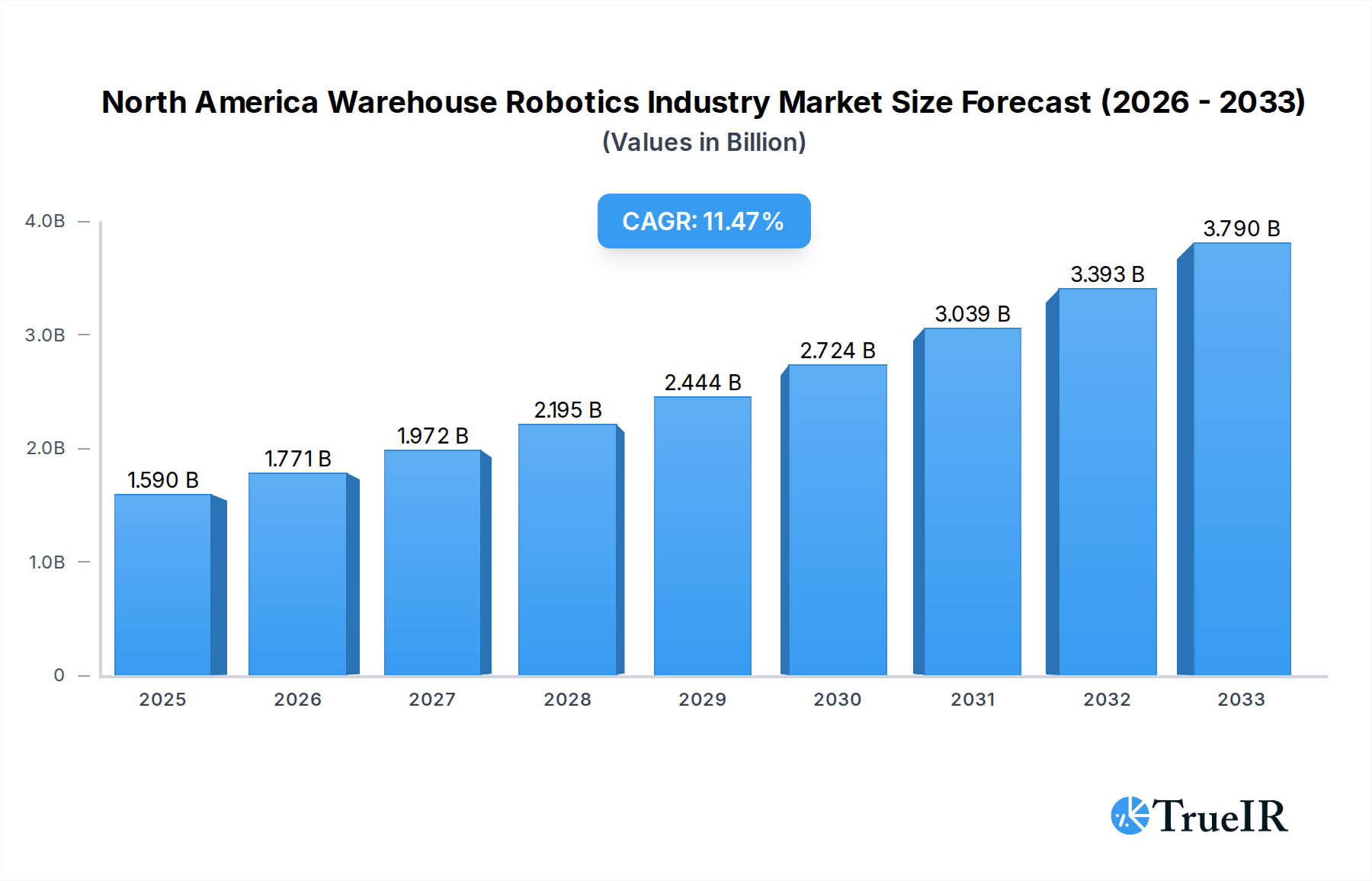

The North America warehouse robotics market is poised for substantial growth, projected to reach USD 1.59 billion in 2025 and expand at a robust Compound Annual Growth Rate (CAGR) of 11.34% through 2033. This expansion is primarily driven by the escalating demand for efficient storage, faster order fulfillment, and improved operational throughput across various industries. The increasing adoption of automation in logistics and supply chain management is a key catalyst, as businesses increasingly recognize the benefits of robotics in reducing labor costs, minimizing errors, and enhancing overall productivity. Specifically, the surge in e-commerce has amplified the need for sophisticated warehousing solutions, pushing companies to invest in advanced technologies like Automated Storage and Retrieval Systems (ASRS), mobile robots (AGVs and AMRs), and intelligent sortation systems. These technologies are crucial for handling the complexity of modern distribution centers and meeting the ever-increasing consumer expectations for rapid delivery.

North America Warehouse Robotics Industry Market Size (In Billion)

The market landscape is characterized by a diverse range of applications and end-user segments. Industrial robots, sortation systems, conveyors, palletizers, and ASRS are central to modern warehouse operations, each contributing to distinct aspects of the supply chain. Mobile robots, including Automated Guided Vehicles (AGVs) and Autonomous Mobile Robots (AMRs), are gaining significant traction due to their flexibility and ability to adapt to dynamic warehouse environments. Key end-user industries driving this growth include Food and Beverage, Automotive, Retail, and Electrical and Electronics, all of whom are seeking to optimize their logistics operations. While the market benefits from strong growth drivers, potential restraints such as the high initial investment costs for some robotic solutions and the need for skilled personnel to operate and maintain these systems will need to be strategically addressed by industry stakeholders to ensure sustained and widespread adoption.

North America Warehouse Robotics Industry Company Market Share

North America Warehouse Robotics Industry Market Structure & Competitive Landscape

The North America warehouse robotics market is characterized by a moderate to high degree of concentration, driven by significant investments from established industrial automation giants and agile innovators. Key players like Honeywell International Inc., Locus Robotics, Omron Adept Technologies, and Amazon Robotics LLC (formerly Kiva Systems) dominate significant market shares, leveraging extensive R&D budgets and established customer relationships. The innovation landscape is a vibrant ecosystem, fueled by advancements in artificial intelligence, machine learning, and sensor technology, enabling robots to perform increasingly complex tasks with greater autonomy and precision. Regulatory impacts, while nascent, are beginning to shape the market, with a growing emphasis on safety standards and data security for automated systems. Product substitutes, such as advanced manual automation and semi-automated solutions, continue to exist, but the superior efficiency and scalability of robotics are driving adoption. End-user segmentation reveals a strong demand from the Retail, Food and Beverage, and Automotive sectors, each with unique operational challenges addressed by tailored robotic solutions. Merger and acquisition (M&A) activity remains a strategic imperative for market leaders, with an estimated xx volume of transactions in the historical period (2019-2024) aimed at acquiring new technologies, expanding product portfolios, and consolidating market presence. For instance, acquisitions of smaller, specialized robotics firms by larger corporations have been prevalent, demonstrating a clear trend towards integration and comprehensive solution offerings.

North America Warehouse Robotics Industry Market Trends & Opportunities

The North America warehouse robotics market is poised for unprecedented growth, with a projected market size exceeding billions by 2033. This expansion is driven by a confluence of technological advancements, evolving consumer demands for faster fulfillment, and the persistent need for operational efficiency in the face of rising labor costs and labor shortages. The market size is estimated to reach billions in the base year 2025, with a compound annual growth rate (CAGR) of xx% projected for the forecast period (2025–2033). Technological shifts are at the forefront, with the increasing sophistication of Artificial Intelligence (AI) and Machine Learning (ML) enabling robots to adapt to dynamic warehouse environments, optimize picking routes, and collaborate seamlessly with human workers. The rise of autonomous mobile robots (AMRs) and collaborative robots (cobots) is transforming traditional warehousing paradigms, offering greater flexibility and scalability compared to fixed automation systems. Consumer preferences for rapid delivery and personalized experiences are placing immense pressure on supply chains, compelling businesses to invest in automation that can accelerate order fulfillment processes and reduce errors. This is particularly evident in the e-commerce sector, where the ability to process a high volume of orders quickly and accurately is a critical competitive differentiator. Competitive dynamics are intensifying, with both established players and emerging startups vying for market dominance. This intense competition fosters a continuous cycle of innovation, leading to the development of more intelligent, efficient, and cost-effective robotic solutions. The market penetration rate for warehouse robotics is steadily increasing, moving beyond early adopters to encompass a broader spectrum of industries and business sizes. Opportunities abound for companies that can offer integrated solutions, advanced analytics, and tailored robotic applications to address specific industry needs. The growing emphasis on sustainability is also creating opportunities for robotics solutions that can optimize energy consumption and reduce waste within warehouse operations. Furthermore, the ongoing digitalization of supply chains and the adoption of Industry 4.0 principles are creating a fertile ground for the widespread integration of robotics.

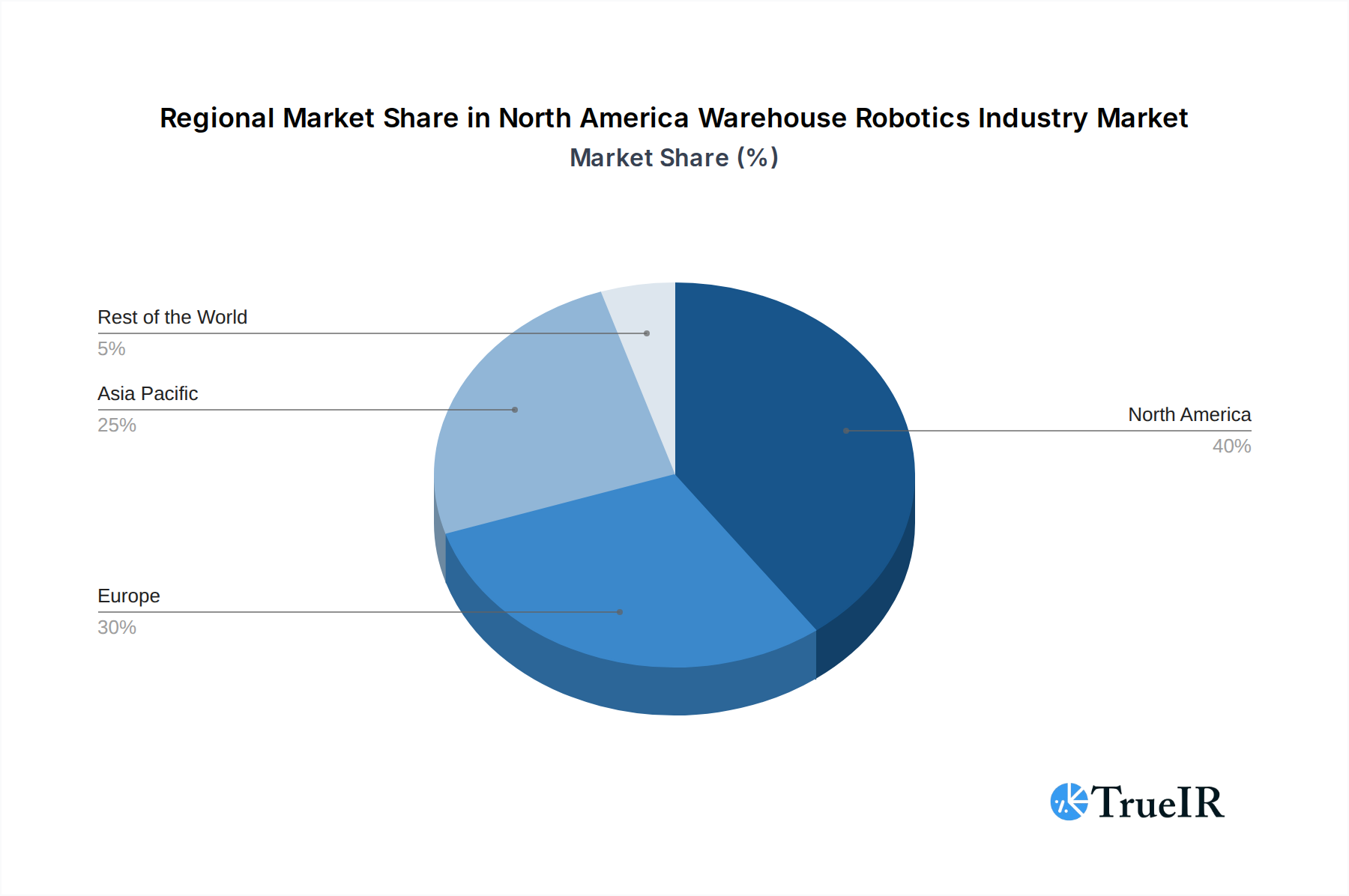

Dominant Markets & Segments in North America Warehouse Robotics Industry

The North America warehouse robotics industry exhibits distinct regional and segment-specific dominance, driven by unique market dynamics and operational requirements.

Regional Dominance:

- United States: The United States stands as the undisputed leader in the North America warehouse robotics market. Its dominance is fueled by a robust e-commerce infrastructure, a large and diverse industrial base, and significant private and public investment in automation technologies.

- Key Growth Drivers:

- Extensive E-commerce Penetration: The sheer volume of online retail in the US necessitates highly efficient fulfillment operations, driving demand for robotic solutions.

- Labor Shortages and Rising Wages: Persistent labor challenges in warehousing push companies towards automation to maintain operational continuity and cost-effectiveness.

- Technological Adoption: The US is a hub for technological innovation, readily adopting advanced robotics and AI solutions.

- Government Initiatives & Investment: While not always direct, supportive policies and significant venture capital funding foster an environment conducive to automation adoption.

- Key Growth Drivers:

- Canada: Canada represents a significant, albeit smaller, market with a growing appetite for warehouse automation, particularly in its major urban centers.

- Key Growth Drivers:

- Increasing E-commerce Growth: Similar to the US, Canada's online retail sector is expanding, creating a need for optimized logistics.

- Focus on Efficiency in Key Industries: Sectors like Food and Beverage and Retail are actively seeking efficiency gains through automation.

- Proximity to US Market: The interconnectedness of North American supply chains encourages the adoption of similar technologies.

- Key Growth Drivers:

North America Warehouse Robotics Industry Regional Market Share

Segment Dominance by Type:

- Mobile Robots (AGVs and AMRs): This segment is experiencing explosive growth, driven by its flexibility and adaptability in dynamic warehouse environments.

- Detailed Analysis: AMRs, in particular, are revolutionizing operations by navigating without fixed infrastructure, enabling seamless integration into existing workflows. They excel in tasks such as goods-to-person picking, inventory movement, and sortation. The ability to scale operations up or down by adding or removing robots makes them highly attractive to businesses with fluctuating demand.

- Automated Storage and Retrieval Systems (ASRS): ASRS systems remain crucial for high-density storage and efficient retrieval of goods, especially in large-scale distribution centers.

- Detailed Analysis: These systems are ideal for optimizing space utilization and ensuring rapid access to inventory. They are particularly prevalent in industries with large SKUs and high throughput requirements, such as e-commerce fulfillment and automotive parts distribution. The precision and speed of ASRS contribute significantly to overall warehouse efficiency.

- Industrial Robots: While traditionally associated with manufacturing, industrial robots are increasingly finding applications in warehousing for tasks like palletizing and depalletizing.

- Detailed Analysis: Their robust nature and precision make them ideal for repetitive, heavy-duty tasks. The development of collaborative industrial robots is further expanding their utility within warehouse settings, allowing for safe human-robot interaction.

- Sortation Systems & Conveyors: These are foundational elements of automated warehousing, essential for moving goods efficiently between different zones within a facility.

- Detailed Analysis: Advanced sortation systems, often integrated with robotics, are critical for high-volume order processing, enabling rapid and accurate routing of items to their destinations.

Segment Dominance by Function:

- Storage: The primary function driving the adoption of robotics, aiming to optimize space utilization and inventory management.

- Detailed Analysis: Robotics plays a pivotal role in automating both the put-away and retrieval of goods, leading to reduced labor costs and improved inventory accuracy.

- Packaging: Robotics are increasingly employed for automated packaging processes, enhancing speed and consistency.

- Detailed Analysis: This includes tasks like case packing, pallet wrapping, and kitting, where robots can perform with greater efficiency and fewer errors than manual methods.

Segment Dominance by End User:

- Retail: The e-commerce boom has made the Retail sector the largest driver of warehouse robotics adoption.

- Detailed Analysis: Retailers require rapid order fulfillment, accurate inventory management, and efficient returns processing, all areas where robotics offer significant advantages. The ability to handle a wide variety of SKUs and fluctuating demand is paramount.

- Food and Beverage: This sector demands high levels of hygiene, temperature control, and traceability, areas where automation can significantly improve operations.

- Detailed Analysis: Robotics help ensure product integrity, speed up order processing, and improve worker safety in potentially hazardous environments.

- Automotive: The automotive industry relies heavily on efficient supply chains and just-in-time delivery, making warehouse robotics crucial for managing complex parts inventory.

- Detailed Analysis: Automated systems ensure that the right parts are available at the right time for production lines, minimizing downtime and optimizing inventory levels.

North America Warehouse Robotics Industry Product Analysis

Product innovation in North America warehouse robotics is centered on enhancing autonomy, intelligence, and adaptability. Mobile robots are evolving with advanced navigation systems, sophisticated object recognition, and improved payload capacities, enabling them to handle a wider range of goods and operate in more complex environments. Collaborative robots are being designed for safer, more intuitive human-robot interaction, broadening their applicability in tasks previously performed by humans. AI-powered software platforms are a key differentiator, offering predictive analytics, real-time route optimization, and sophisticated fleet management capabilities. These advancements allow for a more dynamic and responsive warehouse operation. Competitive advantages are increasingly derived from a combination of hardware robustness, software intelligence, and seamless integration capabilities, enabling end-users to achieve significant gains in efficiency, accuracy, and scalability.

Key Drivers, Barriers & Challenges in North America Warehouse Robotics Industry

The North America warehouse robotics industry is propelled by several key drivers, including the relentless growth of e-commerce necessitating faster fulfillment, persistent labor shortages and rising labor costs, and the imperative for increased operational efficiency and accuracy. Technological advancements in AI, machine learning, and sensor technology are also critical enablers, allowing for more sophisticated and autonomous robotic solutions. Policy initiatives promoting industrial automation and smart manufacturing further bolster adoption.

However, significant barriers and challenges impede growth. High initial capital investment remains a considerable hurdle for small and medium-sized enterprises (SMEs). The complexity of integrating robotic systems with existing legacy infrastructure requires substantial planning and expertise. Cybersecurity concerns and data privacy issues are also paramount, especially with increasingly interconnected systems. Furthermore, the need for skilled personnel to operate and maintain these advanced systems presents a workforce development challenge, with a gap in trained technicians and engineers. Supply chain disruptions and component shortages can also impact the availability and cost of robotic hardware, creating production and delivery delays, estimated to have caused a xx% increase in lead times during the historical period.

Growth Drivers in the North America Warehouse Robotics Industry Market

Key growth drivers in the North America warehouse robotics market are primarily technological, economic, and driven by evolving operational demands. The exponential growth of e-commerce continues to be a paramount driver, forcing businesses to invest in automation to meet consumer expectations for rapid delivery and seamless order fulfillment. Economic factors such as persistent labor shortages and escalating wage pressures across North America are compelling companies to seek robotic solutions for increased productivity and cost containment. Furthermore, the continuous evolution of AI and machine learning is enabling robots to perform more complex tasks with greater autonomy, leading to enhanced efficiency, accuracy, and safety in warehouse operations. Policy support for advanced manufacturing and smart logistics also plays a role.

Challenges Impacting North America Warehouse Robotics Industry Growth

Challenges impacting the North America warehouse robotics industry growth include the substantial upfront capital investment required for acquiring and implementing robotic systems, which can be a significant barrier for smaller enterprises. The integration of new robotic technologies with existing legacy warehouse management systems (WMS) often presents technical complexities and requires specialized expertise. Cybersecurity threats and concerns surrounding data privacy in increasingly interconnected automated environments are also major considerations for businesses. Furthermore, a shortage of skilled labor capable of operating, maintaining, and repairing advanced robotics systems poses a persistent challenge to widespread adoption and optimal utilization, with an estimated xx% skills gap identified in the historical period.

Key Players Shaping the North America Warehouse Robotics Industry Market

- Honeywell International Inc.

- Locus Robotics

- InVia Robotics Inc.

- Omron Adept Technologies

- Amazon Robotics LLC

- Fetch Robotics Inc.

Significant North America Warehouse Robotics Industry Industry Milestones

- 2019: Increased adoption of AI in mobile robots for enhanced navigation and decision-making.

- 2020: Rise in demand for robotics in e-commerce fulfillment centers due to the global pandemic.

- 2021: Significant advancements in cobot (collaborative robot) technology, allowing for safer human-robot interaction in warehouses.

- 2022: Growing investment in Autonomous Mobile Robots (AMRs) for flexible warehouse operations.

- 2023: Emergence of robotic solutions for sustainability initiatives, focusing on energy efficiency and waste reduction.

- 2024: Continued consolidation within the industry through strategic mergers and acquisitions.

Future Outlook for North America Warehouse Robotics Industry Market

The future outlook for the North America warehouse robotics industry is exceptionally bright, driven by sustained demand for automation solutions that enhance efficiency, speed, and accuracy in logistics operations. Continued advancements in AI, machine learning, and sensor technologies will lead to the development of more intelligent, adaptable, and cost-effective robots, further lowering adoption barriers. The growing emphasis on supply chain resilience and agility, coupled with the ongoing evolution of e-commerce, will fuel significant investment in robotic automation. Strategic opportunities lie in offering integrated solutions that combine hardware, software, and advanced analytics, as well as catering to the specific needs of emerging sectors and specialized warehouse functions. The market is expected to witness further innovation in areas like swarm robotics and enhanced human-robot collaboration, promising a transformative impact on the future of warehousing.

North America Warehouse Robotics Industry Segmentation

-

1. Type

- 1.1. Industrial Robots

- 1.2. Sortation Systems

- 1.3. Conveyors

- 1.4. Palletizers

- 1.5. Automated Storage and Retrieval System (ASRS)

- 1.6. Mobile Robots (AGVs and AMRs)

-

2. Function

- 2.1. Storage

- 2.2. Plastic Bottles

- 2.3. Packaging

- 2.4. Trans-shipments

- 2.5. Other Functions

-

3. End User

- 3.1. Food and Beverage

- 3.2. Automotive

- 3.3. Retail

- 3.4. Electrical and Electronics

- 3.5. Pharmaceutical

- 3.6. Other End Users

North America Warehouse Robotics Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

North America Warehouse Robotics Industry Regional Market Share

Geographic Coverage of North America Warehouse Robotics Industry

North America Warehouse Robotics Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.34% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Industrial Robots

- 5.1.2. Sortation Systems

- 5.1.3. Conveyors

- 5.1.4. Palletizers

- 5.1.5. Automated Storage and Retrieval System (ASRS)

- 5.1.6. Mobile Robots (AGVs and AMRs)

- 5.2. Market Analysis, Insights and Forecast - by Function

- 5.2.1. Storage

- 5.2.2. Plastic Bottles

- 5.2.3. Packaging

- 5.2.4. Trans-shipments

- 5.2.5. Other Functions

- 5.3. Market Analysis, Insights and Forecast - by End User

- 5.3.1. Food and Beverage

- 5.3.2. Automotive

- 5.3.3. Retail

- 5.3.4. Electrical and Electronics

- 5.3.5. Pharmaceutical

- 5.3.6. Other End Users

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. North America Warehouse Robotics Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Industrial Robots

- 6.1.2. Sortation Systems

- 6.1.3. Conveyors

- 6.1.4. Palletizers

- 6.1.5. Automated Storage and Retrieval System (ASRS)

- 6.1.6. Mobile Robots (AGVs and AMRs)

- 6.2. Market Analysis, Insights and Forecast - by Function

- 6.2.1. Storage

- 6.2.2. Plastic Bottles

- 6.2.3. Packaging

- 6.2.4. Trans-shipments

- 6.2.5. Other Functions

- 6.3. Market Analysis, Insights and Forecast - by End User

- 6.3.1. Food and Beverage

- 6.3.2. Automotive

- 6.3.3. Retail

- 6.3.4. Electrical and Electronics

- 6.3.5. Pharmaceutical

- 6.3.6. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Honeywell International Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Locus Robotics

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 InVia Robotics Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Omron Adept Technologies

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Kiva Systems (Amazon Robotics LLC)

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Fetch Robotics Inc *List Not Exhaustive

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.1 Honeywell International Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: North America Warehouse Robotics Industry Revenue Breakdown (undefined, %) by Product 2025 & 2033

- Figure 2: North America Warehouse Robotics Industry Share (%) by Company 2025

List of Tables

- Table 1: North America Warehouse Robotics Industry Revenue undefined Forecast, by Type 2020 & 2033

- Table 2: North America Warehouse Robotics Industry Revenue undefined Forecast, by Function 2020 & 2033

- Table 3: North America Warehouse Robotics Industry Revenue undefined Forecast, by End User 2020 & 2033

- Table 4: North America Warehouse Robotics Industry Revenue undefined Forecast, by Region 2020 & 2033

- Table 5: North America Warehouse Robotics Industry Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: North America Warehouse Robotics Industry Revenue undefined Forecast, by Function 2020 & 2033

- Table 7: North America Warehouse Robotics Industry Revenue undefined Forecast, by End User 2020 & 2033

- Table 8: North America Warehouse Robotics Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 9: United States North America Warehouse Robotics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Canada North America Warehouse Robotics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 11: Mexico North America Warehouse Robotics Industry Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Warehouse Robotics Industry?

The projected CAGR is approximately 11.34%.

2. Which companies are prominent players in the North America Warehouse Robotics Industry?

Key companies in the market include Honeywell International Inc, Locus Robotics, InVia Robotics Inc, Omron Adept Technologies, Kiva Systems (Amazon Robotics LLC), Fetch Robotics Inc *List Not Exhaustive.

3. What are the main segments of the North America Warehouse Robotics Industry?

The market segments include Type, Function, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

; Increasing Number of SKUs; Growth of E-commerce in Developing Countries.

6. What are the notable trends driving market growth?

Growth of E-commerce in Developing Countries.

7. Are there any restraints impacting market growth?

; Lack of Awareness and Budget to Deploy INS in Emerging Economies.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Warehouse Robotics Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Warehouse Robotics Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Warehouse Robotics Industry?

To stay informed about further developments, trends, and reports in the North America Warehouse Robotics Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence