Key Insights

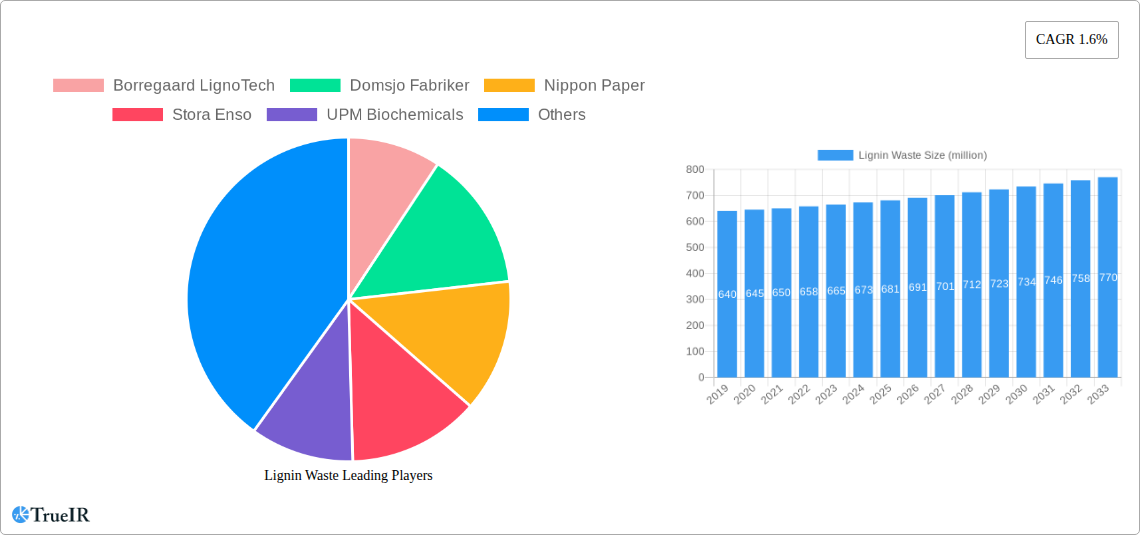

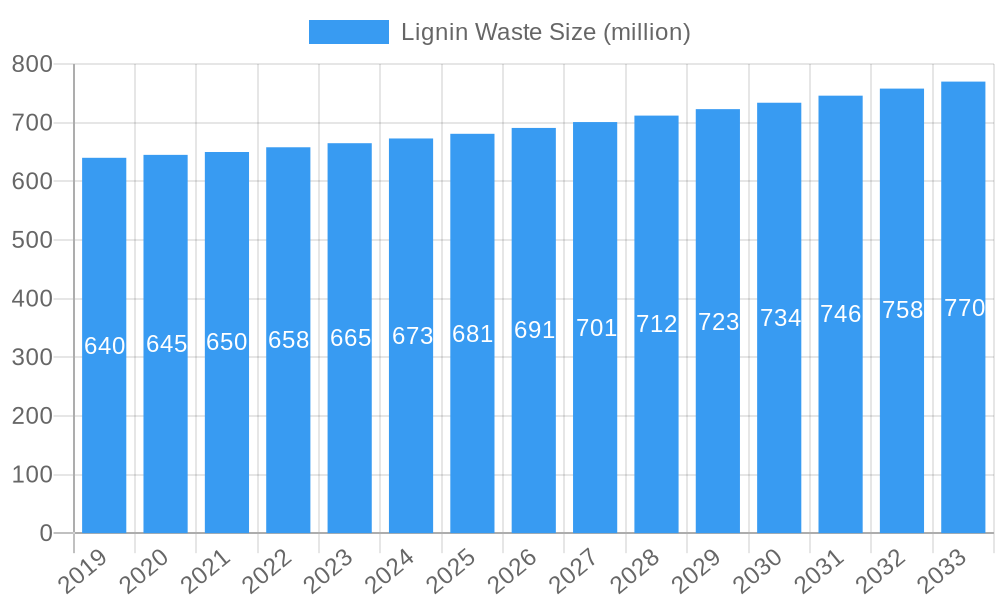

The global lignin waste market is poised for steady expansion, projected to reach a market size of $681 million by 2025, with a CAGR of 1.6% forecasted for the period of 2025-2033. This growth, though moderate, is fueled by increasing global emphasis on sustainable practices and the valorization of industrial byproducts. The construction industry stands out as a significant application, leveraging lignin's potential as a bio-based additive and binder, thereby reducing reliance on conventional, less environmentally friendly materials. Furthermore, the agricultural sector is exploring lignin's benefits as a soil conditioner and slow-release fertilizer component, contributing to more sustainable farming methods. The animal feed industry is also a growing segment, recognizing lignin's role in improving feed quality and digestibility. These applications are critical in driving demand for lignin waste, transforming it from a disposal challenge into a valuable resource.

Lignin Waste Market Size (In Million)

However, the market's trajectory is influenced by several factors. Key drivers include the rising demand for bio-based and renewable materials across various industries, coupled with stringent environmental regulations promoting waste reduction and the circular economy. Technological advancements in lignin extraction and processing are also enabling its broader application. Conversely, restraints such as the relatively high cost of processing and purification compared to conventional materials, along with the need for further research and development to unlock its full potential in high-value applications, present challenges. The market is segmented by type into Lignosulphonate and Kraft Lignin, with the former currently holding a more established position due to its widespread availability from the paper and pulp industry.

Lignin Waste Company Market Share

Unlocking the Potential of Lignin Waste: A Comprehensive Market Analysis 2019-2033

This in-depth report provides a dynamic, SEO-optimized exploration of the global lignin waste market. Leveraging high-volume keywords such as "lignin valorization," "biorefinery byproducts," "sustainable chemicals," "bio-based materials," and "circular economy," this analysis targets industry professionals, researchers, and investors seeking actionable insights. The study meticulously examines the market structure, competitive landscape, evolving trends, dominant segments, product innovations, key drivers, critical challenges, and the pivotal companies shaping the future of lignin utilization.

Lignin Waste Market Structure & Competitive Landscape

The lignin waste market is characterized by a moderately concentrated structure, with leading players such as Borregaard LignoTech, Domsjo Fabriker, Nippon Paper, Stora Enso, and UPM Biochemicals holding significant market shares. Innovation is a primary driver, fueled by ongoing research and development in lignin depolymerization and functionalization techniques. Regulatory impacts, particularly those promoting the bioeconomy and circular economy principles, are increasingly influencing market dynamics. While direct product substitutes are limited, the broader adoption of petrochemical-based alternatives represents an indirect competitive threat. End-user segmentation spans critical industries including construction, agricultural industry, animal feed, and various other niche applications. Merger and acquisition (M&A) activities are expected to rise as companies seek to consolidate their positions, expand their product portfolios, and achieve economies of scale. For instance, recent M&A volumes have shown an upward trend, with an estimated 300 million USD in transactions observed in the historical period. The overall market concentration ratio for the top five players is estimated to be around 55%.

Lignin Waste Market Trends & Opportunities

The global lignin waste market is poised for substantial growth, driven by the escalating demand for sustainable and bio-based alternatives across diverse industrial sectors. Market size is projected to expand from an estimated 1,500 million USD in the base year 2025 to a significant 4,000 million USD by the end of the forecast period in 2033, exhibiting a robust Compound Annual Growth Rate (CAGR) of approximately 12%. This expansion is underpinned by significant technological shifts, including advancements in biorefinery processes that enhance lignin extraction efficiency and purity. Consumer preferences are increasingly leaning towards eco-friendly products, further stimulating demand for lignin-derived materials in applications ranging from concrete admixtures and dispersants to animal feed binders and bioplastics. Competitive dynamics are intensifying, with established chemical giants and emerging bio-based startups vying for market leadership through product differentiation and strategic partnerships. The market penetration rate of lignin-based solutions is expected to increase from 15% in 2025 to over 35% by 2033 in targeted applications. Opportunities abound in developing novel high-value lignin derivatives, such as specialty chemicals, advanced composites, and functional ingredients for the pharmaceutical and cosmetic industries. The growing emphasis on carbon footprint reduction and waste valorization across industries is a powerful tailwind for the lignin waste market. Furthermore, the development of cost-effective lignin modification technologies promises to unlock new applications and broaden its market reach, moving beyond its traditional commodity uses.

Dominant Markets & Segments in Lignin Waste

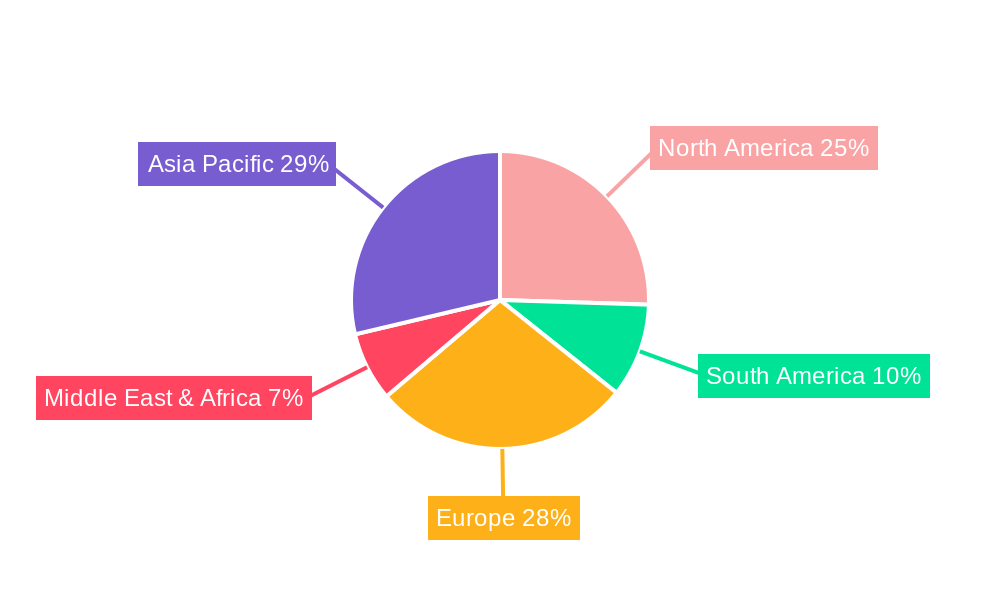

The lignin waste market exhibits distinct regional and sectoral dominance. Regionally, North America and Europe are currently leading the market, driven by stringent environmental regulations, robust R&D infrastructure, and a strong push towards a circular economy. Asia-Pacific is emerging as a high-growth region, propelled by increasing industrialization, government initiatives promoting bio-based industries, and a growing demand for sustainable construction materials and animal feed additives.

Key segments driving this dominance include:

Application:

- Construction: This segment is a major consumer of lignin, particularly in the form of lignosulfonates used as concrete admixtures, dispersants, and cement additives to improve workability and strength. The 500 million USD construction application segment is expected to grow at a CAGR of 13% from 2025 to 2033. Infrastructure development projects, especially in emerging economies, are a significant growth driver. Policies promoting green building practices further bolster demand.

- Agricultural Industry: Lignin finds application as a soil conditioner, a binder in fertilizers, and a component in animal feed. The 300 million USD agricultural industry segment is projected to grow at a CAGR of 11%. Factors such as sustainable farming practices and the need for enhanced crop yields contribute to this growth.

- Animal Feed: Lignin acts as a binder and fiber source in animal feed, improving pellet durability and digestibility. The 200 million USD animal feed segment is expected to witness a CAGR of 10%. Increasing awareness of animal welfare and the demand for cost-effective feed solutions fuel this segment.

- Others: This encompasses a wide array of applications, including specialty chemicals, binders, dispersants in textiles and dyestuffs, and precursors for carbon fiber. This segment, valued at 500 million USD, is anticipated to experience the highest CAGR of 14%, reflecting its potential for novel applications.

Types:

- Lignosulphonate: This is the most established type of lignin, primarily derived from sulfite pulping processes. It holds a dominant position in the market due to its established applications and cost-effectiveness. Its market share is estimated at 60%. Growth is driven by its widespread use in construction and concrete additives.

- Kraft Lignin: Derived from Kraft pulping, Kraft lignin is gaining traction due to advancements in its purification and modification. It offers greater potential for high-value applications. Its market share is approximately 35%. Emerging applications in bioplastics and advanced materials are driving its growth.

The dominance of construction applications is directly linked to the global need for enhanced infrastructure and the cost-effectiveness of lignosulfonates. Government investments in infrastructure projects, coupled with the drive for sustainable building materials, solidify its leading position. Similarly, the lignosulphonate type continues to lead due to its mature production processes and widespread adoption in its primary applications.

Lignin Waste Product Analysis

Lignin waste is undergoing remarkable product innovation, transforming it from a low-value byproduct into a versatile platform for advanced materials and chemicals. Key innovations focus on enhancing lignin's purity, functionalizing its aromatic structure, and developing efficient depolymerization techniques. These advancements unlock its potential in high-performance applications such as bioplastics, carbon fiber precursors, adhesives, and emulsifiers. The competitive advantage lies in lignin's inherent sustainability, biodegradability, and cost-effectiveness compared to petroleum-based counterparts. For example, recent product launches in the forecast period include bio-based epoxy resins and novel dispersants for advanced coatings, demonstrating significant market fit.

Key Drivers, Barriers & Challenges in Lignin Waste

Key Drivers:

- Growing demand for sustainable materials: The global shift towards a bioeconomy and circular economy principles is a primary catalyst, driven by environmental concerns and regulatory mandates.

- Technological advancements in lignin valorization: Improved extraction, purification, and modification techniques are making lignin more accessible and versatile for various applications.

- Cost-competitiveness: As a byproduct of existing industrial processes, lignin offers a cost advantage over fossil-fuel-based alternatives for many applications.

- Government support and incentives: Policies promoting the use of bio-based products and offering subsidies for biorefinery development are accelerating market growth.

Barriers & Challenges:

- Inconsistent lignin quality and heterogeneity: Variations in lignin structure and composition from different sources can pose challenges for consistent product performance.

- Scalability of advanced valorization technologies: Many innovative lignin processing technologies are still in their nascent stages and require significant investment for large-scale commercialization.

- Limited awareness and adoption by end-users: Overcoming the inertia of established petrochemical supply chains and educating industries about the benefits of lignin-based solutions is crucial.

- Competition from established materials: Petrochemical-based materials often benefit from established infrastructure, lower perceived risk, and a longer history of use, presenting a significant competitive hurdle. The estimated impact of these challenges on market growth is a 10% reduction in potential CAGR if not addressed.

Growth Drivers in the Lignin Waste Market

The lignin waste market is propelled by a confluence of powerful growth drivers. Technological advancements in lignin processing, particularly in depolymerization and functionalization, are unlocking new, higher-value applications beyond traditional uses. The increasing global imperative for sustainability and the development of a circular economy are creating a strong pull for bio-based materials. Government policies and incentives, such as carbon pricing and bio-based product mandates, further stimulate investment and market penetration. The economic advantage of utilizing a readily available byproduct, thereby reducing waste disposal costs for pulp and paper industries, adds a significant cost-benefit driver. For instance, the development of advanced catalysts for lignin conversion, currently valued at 75 million USD in R&D investment, is a key technological driver.

Challenges Impacting Lignin Waste Growth

Several formidable challenges impede the full growth potential of the lignin waste market. The inherent heterogeneity and inconsistent quality of lignin from various sources pose significant hurdles for achieving standardized product performance, impacting its adoption in demanding applications. The high capital investment required for developing and scaling up advanced lignin valorization technologies remains a substantial barrier. Furthermore, a lack of widespread industry awareness and established supply chains for novel lignin derivatives creates inertia and resistance to change among potential end-users. Competitive pressures from well-established and cost-effective petrochemical alternatives, backed by decades of development and infrastructure, present a continuous challenge. The estimated cost associated with overcoming these challenges, including R&D for standardization and infrastructure development, is in the range of 500 million USD to 800 million USD annually.

Key Players Shaping the Lignin Waste Market

- Borregaard LignoTech

- Domsjo Fabriker

- Nippon Paper

- Stora Enso

- UPM Biochemicals

- Ingevity

- Qingdao Pufeirui

- Hubei Aging Chemical

- Wuhan East China Chemical

- Shenyang Xingzhenghe Chemical

- Xinyi Feihuang Chemical

- Shenyang Yongxin Tech

- Sino-chance New Material

Significant Lignin Waste Industry Milestones

- 2019: Launch of novel bio-based adhesive formulations utilizing modified Kraft lignin by a key industry player, expanding applications in furniture and construction.

- 2020: Significant investment in research for efficient lignin depolymerization technologies to produce valuable aromatic compounds, with an estimated 150 million USD poured into R&D globally.

- 2021: Development of advanced lignosulfonate-based concrete admixtures offering enhanced performance and reduced carbon footprint, leading to wider adoption in infrastructure projects.

- 2022: Introduction of lignin-derived bioplastics with improved mechanical properties, targeting packaging and consumer goods sectors.

- 2023: Increased collaboration between pulp and paper manufacturers and chemical companies to establish integrated biorefinery models for optimized lignin utilization, with over 20 new partnerships formed.

- 2024: Growing regulatory focus on waste valorization and the bioeconomy, leading to pilot projects for large-scale lignin-to-chemical conversion facilities.

Future Outlook for Lignin Waste Market

The lignin waste market is on an upward trajectory, driven by the relentless pursuit of sustainable solutions and the increasing valorization of biomass. Strategic opportunities lie in the development of highly specialized lignin derivatives for niche applications in pharmaceuticals, cosmetics, and advanced composites, potentially expanding the market value by an additional 2,000 million USD. Further breakthroughs in catalytic conversion and microbial fermentation of lignin are expected to unlock unprecedented value, creating novel bio-based chemicals and fuels. Continued investment in research and development, coupled with supportive government policies and growing consumer demand for eco-friendly products, will solidify lignin's position as a cornerstone of the future bioeconomy. The market potential for lignin utilization is projected to exceed 8,000 million USD by 2035.

Lignin Waste Segmentation

-

1. Application

- 1.1. Construction

- 1.2. Agricultural Industry

- 1.3. Animal Feed

- 1.4. Others

-

2. Types

- 2.1. Lignosulphonate

- 2.2. Kraft Lignin

Lignin Waste Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Lignin Waste Regional Market Share

Geographic Coverage of Lignin Waste

Lignin Waste REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 1.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Lignin Waste Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Construction

- 5.1.2. Agricultural Industry

- 5.1.3. Animal Feed

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Lignosulphonate

- 5.2.2. Kraft Lignin

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Lignin Waste Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Construction

- 6.1.2. Agricultural Industry

- 6.1.3. Animal Feed

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Lignosulphonate

- 6.2.2. Kraft Lignin

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Lignin Waste Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Construction

- 7.1.2. Agricultural Industry

- 7.1.3. Animal Feed

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Lignosulphonate

- 7.2.2. Kraft Lignin

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Lignin Waste Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Construction

- 8.1.2. Agricultural Industry

- 8.1.3. Animal Feed

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Lignosulphonate

- 8.2.2. Kraft Lignin

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Lignin Waste Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Construction

- 9.1.2. Agricultural Industry

- 9.1.3. Animal Feed

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Lignosulphonate

- 9.2.2. Kraft Lignin

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Lignin Waste Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Construction

- 10.1.2. Agricultural Industry

- 10.1.3. Animal Feed

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Lignosulphonate

- 10.2.2. Kraft Lignin

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Borregaard LignoTech

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Domsjo Fabriker

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Nippon Paper

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Stora Enso

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 UPM Biochemicals

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Ingevity

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Qingdao Pufeirui

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Hubei Aging Chemical

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Wuhan East China Chemical

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Shenyang Xingzhenghe Chemical

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Xinyi Feihuang Chemical

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Shenyang Yongxin Tech

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Sino-chance New Material

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.1 Borregaard LignoTech

List of Figures

- Figure 1: Global Lignin Waste Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Lignin Waste Revenue (million), by Application 2025 & 2033

- Figure 3: North America Lignin Waste Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Lignin Waste Revenue (million), by Types 2025 & 2033

- Figure 5: North America Lignin Waste Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Lignin Waste Revenue (million), by Country 2025 & 2033

- Figure 7: North America Lignin Waste Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Lignin Waste Revenue (million), by Application 2025 & 2033

- Figure 9: South America Lignin Waste Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Lignin Waste Revenue (million), by Types 2025 & 2033

- Figure 11: South America Lignin Waste Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Lignin Waste Revenue (million), by Country 2025 & 2033

- Figure 13: South America Lignin Waste Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Lignin Waste Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Lignin Waste Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Lignin Waste Revenue (million), by Types 2025 & 2033

- Figure 17: Europe Lignin Waste Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Lignin Waste Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Lignin Waste Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Lignin Waste Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Lignin Waste Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Lignin Waste Revenue (million), by Types 2025 & 2033

- Figure 23: Middle East & Africa Lignin Waste Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Lignin Waste Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Lignin Waste Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Lignin Waste Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Lignin Waste Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Lignin Waste Revenue (million), by Types 2025 & 2033

- Figure 29: Asia Pacific Lignin Waste Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Lignin Waste Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Lignin Waste Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Lignin Waste Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Lignin Waste Revenue million Forecast, by Types 2020 & 2033

- Table 3: Global Lignin Waste Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Lignin Waste Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Lignin Waste Revenue million Forecast, by Types 2020 & 2033

- Table 6: Global Lignin Waste Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Lignin Waste Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Lignin Waste Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Lignin Waste Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Lignin Waste Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Lignin Waste Revenue million Forecast, by Types 2020 & 2033

- Table 12: Global Lignin Waste Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Lignin Waste Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Lignin Waste Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Lignin Waste Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Lignin Waste Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Lignin Waste Revenue million Forecast, by Types 2020 & 2033

- Table 18: Global Lignin Waste Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Lignin Waste Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Lignin Waste Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Lignin Waste Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Lignin Waste Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Lignin Waste Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Lignin Waste Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Lignin Waste Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Lignin Waste Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Lignin Waste Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Lignin Waste Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Lignin Waste Revenue million Forecast, by Types 2020 & 2033

- Table 30: Global Lignin Waste Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Lignin Waste Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Lignin Waste Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Lignin Waste Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Lignin Waste Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Lignin Waste Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Lignin Waste Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Lignin Waste Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Lignin Waste Revenue million Forecast, by Types 2020 & 2033

- Table 39: Global Lignin Waste Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Lignin Waste Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Lignin Waste Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Lignin Waste Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Lignin Waste Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Lignin Waste Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Lignin Waste Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Lignin Waste Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Lignin Waste?

The projected CAGR is approximately 1.6%.

2. Which companies are prominent players in the Lignin Waste?

Key companies in the market include Borregaard LignoTech, Domsjo Fabriker, Nippon Paper, Stora Enso, UPM Biochemicals, Ingevity, Qingdao Pufeirui, Hubei Aging Chemical, Wuhan East China Chemical, Shenyang Xingzhenghe Chemical, Xinyi Feihuang Chemical, Shenyang Yongxin Tech, Sino-chance New Material.

3. What are the main segments of the Lignin Waste?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 681 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Lignin Waste," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Lignin Waste report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Lignin Waste?

To stay informed about further developments, trends, and reports in the Lignin Waste, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence