Key Insights

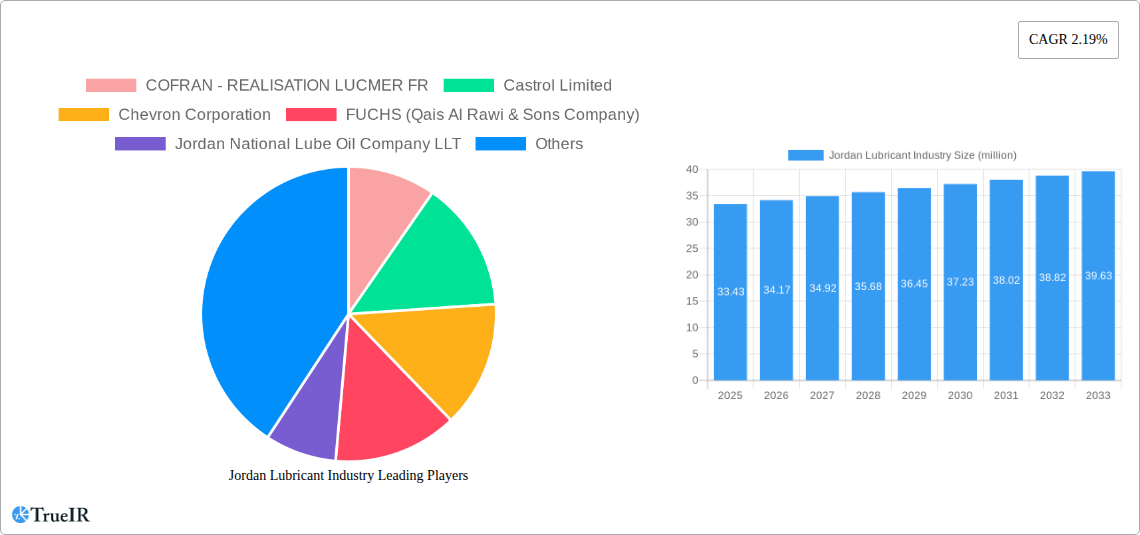

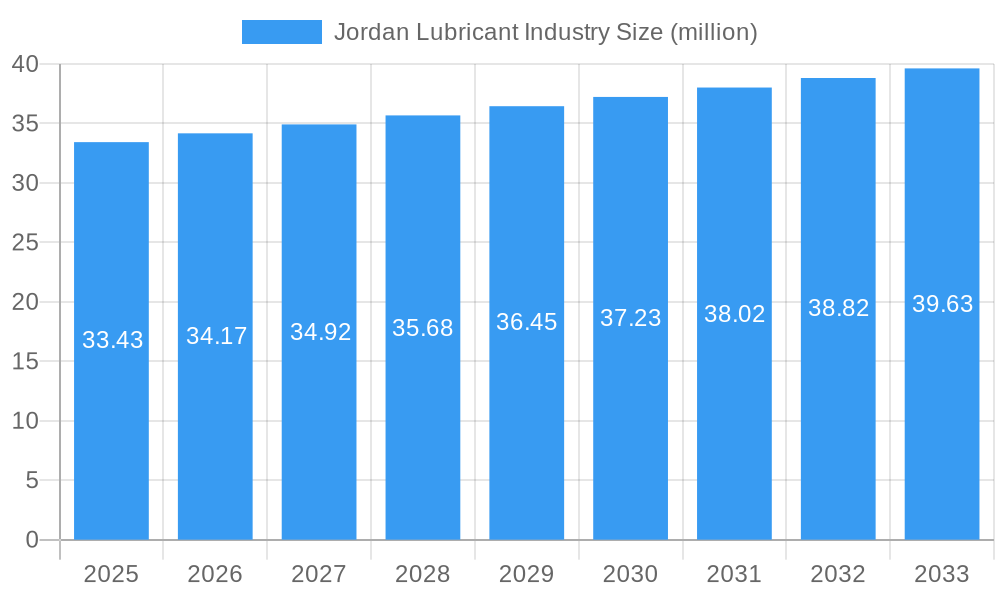

The Jordan Lubricant Industry is poised for steady growth, projected to reach a market size of USD 33.43 million in 2025, with a Compound Annual Growth Rate (CAGR) of 2.19% expected throughout the forecast period (2025-2033). This growth is underpinned by robust demand from key sectors such as Automotive and Transportation, which consistently requires a significant volume of engine oils, transmission fluids, and greases. The increasing vehicle parc, coupled with the aging vehicle population in Jordan, necessitates regular maintenance and replacement of lubricants, serving as a primary market driver. Furthermore, the Heavy Equipment sector, driven by ongoing infrastructure development and construction projects, also contributes substantially to lubricant consumption, particularly for specialized industrial oils and hydraulic fluids. Power Generation, while a smaller segment, also presents a consistent demand for high-performance lubricants.

Jordan Lubricant Industry Market Size (In Million)

The market's expansion is further fueled by technological advancements leading to the development of higher-performance, longer-lasting lubricants, and increasing awareness among consumers and industries regarding the importance of using quality lubricants for optimal equipment performance and longevity. However, the industry faces certain restraints, including fluctuating raw material prices, which can impact profit margins and lead to price volatility. Additionally, the availability of counterfeit lubricants poses a challenge to genuine market players. Despite these hurdles, strategic product development, an emphasis on premium and specialized lubricant offerings, and efficient supply chain management by key players like Shell Plc, Chevron Corporation, and TotalEnergies are expected to navigate these challenges and ensure a sustained upward trajectory for the Jordan Lubricant Industry.

Jordan Lubricant Industry Company Market Share

Jordan Lubricant Industry Market Structure & Competitive Landscape

The Jordan lubricant industry exhibits a moderately concentrated market structure, with a few major international players dominating a significant share of the market, alongside a growing number of local manufacturers. The concentration ratio is estimated to be in the range of 60-70%, indicating a substantial presence of the top 5-7 companies. Innovation drivers are primarily focused on developing high-performance, eco-friendly lubricants that meet stringent international standards and cater to the evolving needs of advanced machinery and automotive technologies. Regulatory impacts, particularly those related to environmental protection and fuel efficiency, are increasingly shaping product development and market entry strategies. Product substitutes, such as synthetic lubricants and alternative lubrication technologies, are gaining traction, challenging the dominance of traditional mineral-based oils.

End-user segmentation is diverse, with the automotive and transportation sector being the largest consumer, followed by heavy equipment and power generation. Mergers and acquisitions (M&A) trends are less pronounced in the domestic market, with most activity involving international companies acquiring stakes or forming strategic alliances to expand their reach. The volume of M&A deals in the historical period (2019-2024) is estimated to be around $20-30 million, primarily driven by consolidation and portfolio expansion strategies of global lubricant giants.

- Market Concentration: Moderately concentrated, with top players holding a significant market share.

- Innovation Drivers: Eco-friendly formulations, enhanced performance, adherence to international standards.

- Regulatory Impacts: Environmental regulations, fuel efficiency mandates.

- Product Substitutes: Synthetic lubricants, alternative lubrication technologies.

- End-user Segmentation: Automotive & Transportation, Heavy Equipment, Power Generation.

- M&A Trends: Limited domestic M&A, strategic alliances with international players.

Jordan Lubricant Industry Market Trends & Opportunities

The Jordan lubricant industry is poised for steady growth, driven by robust demand from its key end-user sectors and an increasing focus on technological advancements and sustainable practices. The market size is projected to expand significantly, with a Compound Annual Growth Rate (CAGR) estimated at approximately 5.5% for the forecast period of 2025–2033. This growth trajectory is underpinned by several converging trends. Firstly, the expanding automotive fleet, including both passenger vehicles and commercial transport, necessitates a consistent supply of high-quality engine oils and transmission fluids. The government’s initiatives to modernize transportation infrastructure and encourage private vehicle ownership further bolster this demand.

Secondly, the burgeoning construction and infrastructure development projects across Jordan are a major impetus for the heavy equipment sector, directly translating into increased consumption of industrial lubricants, hydraulic fluids, and gear oils. As these machines operate under demanding conditions, the need for specialized, high-performance lubricants that ensure longevity and efficiency becomes paramount. The power generation sector, while perhaps a smaller segment, also contributes to market growth. With ongoing investments in power infrastructure to meet rising energy demands, the requirement for reliable industrial oils for turbines and generators remains a consistent factor.

Technological shifts are another critical trend. The industry is witnessing a growing preference for synthetic and semi-synthetic lubricants, which offer superior performance characteristics, extended drain intervals, and improved fuel efficiency compared to traditional mineral oils. This shift is driven by both end-user demand for cost savings and performance optimization, as well as by environmental considerations and the push for reduced emissions. Lubricant manufacturers are actively investing in research and development to formulate products that meet advanced OEM specifications and address the unique operating conditions prevalent in Jordan, such as high temperatures and dusty environments.

Consumer preferences are also evolving. Beyond just price, end-users are increasingly prioritizing product quality, brand reputation, and the availability of technical support. This has led to a greater emphasis on value-added services and customer engagement from lubricant providers. Competitive dynamics are intensifying, with both multinational corporations and local players vying for market share. Opportunities exist for companies that can offer innovative products, responsive customer service, and a strong distribution network across the country. The increasing adoption of digitalization in business operations presents opportunities for enhanced supply chain management and direct-to-consumer sales channels, though traditional distribution remains vital. The market penetration rate for advanced lubricant technologies is still developing, presenting a significant opportunity for early adopters and innovators. The overall market is estimated to reach approximately $1.2 billion by the end of the forecast period.

Dominant Markets & Segments in Jordan Lubricant Industry

The Jordan lubricant industry is characterized by dominant segments driven by robust economic activity and infrastructure development. The Automotive and Transportation end-user industry stands out as the largest and most influential market segment, accounting for an estimated 45% of the total market value. This dominance is fueled by a substantial and growing vehicle parc, encompassing passenger cars, commercial trucks, buses, and motorcycles. Jordan's strategic location as a regional logistics hub further amplifies the demand for high-performance engine oils, transmission fluids, and greases to maintain the efficiency and longevity of this vast fleet. Government policies aimed at modernizing public transportation and encouraging fleet upgrades also contribute to sustained demand.

Within product types, Engine Oil represents the leading segment, directly correlating with the high volume of vehicles in operation. The demand for various grades of engine oil, from conventional mineral oils to advanced synthetic formulations, is consistently strong. The trend towards more fuel-efficient and emissions-compliant vehicles is driving the adoption of specialized engine oils that meet stringent OEM specifications.

The Heavy Equipment end-user industry is the second-largest market segment, comprising approximately 30% of the market share. This segment is primarily driven by ongoing infrastructure development, construction projects, and the mining sector. The operation of excavators, bulldozers, cranes, and other heavy machinery under challenging environmental conditions necessitates the use of robust and high-performance transmission and hydraulic fluids, gear oils, and specialized greases. The forecast period is expected to see continued investment in infrastructure, further solidifying the importance of this segment.

Transmission and Hydraulic Fluid as a product type is intrinsically linked to the performance of both automotive and heavy equipment sectors, experiencing significant demand due to its critical role in power transmission and operational efficiency.

The Power Generation end-user industry, though a smaller segment (around 15%), plays a crucial role. Investments in power plants, including thermal and renewable energy facilities, require specialized industrial oils for turbines, generators, and auxiliary equipment. While the growth in this segment might be more moderate compared to automotive or heavy equipment, the high-value nature of these specialized lubricants ensures its continued significance.

General Industrial Oil and Gear Oil are essential across a wide spectrum of manufacturing and industrial operations, catering to the remaining market share. The growth of Jordan's industrial base, though nascent, offers potential for expansion in these segments. The rise of specialized manufacturing facilities and processing plants will likely increase the demand for tailored industrial lubricants.

Grease is a vital product across all end-user industries, essential for lubricating moving parts and reducing friction in various applications, from automotive components to industrial machinery. Its demand is therefore a function of the overall industrial and automotive activity.

- Dominant End-user Industry: Automotive and Transportation

- Key Growth Drivers: Growing vehicle parc, modernization of public transport, logistics hub status, favorable government policies.

- Market Dominance Analysis: Sustained demand for engine oils and transmission fluids due to high vehicle usage and fleet expansion.

- Leading Product Type: Engine Oil

- Key Growth Drivers: Increasing adoption of fuel-efficient and emissions-compliant vehicles, demand for synthetic and semi-synthetic formulations.

- Market Dominance Analysis: Directly tied to the automotive sector's needs, with a growing emphasis on advanced product specifications.

- Second Dominant End-user Industry: Heavy Equipment

- Key Growth Drivers: Infrastructure development, construction projects, mining activities, need for durable and high-performance fluids.

- Market Dominance Analysis: High consumption of hydraulic fluids, gear oils, and specialized greases due to demanding operational environments.

- Significant Product Type: Transmission and Hydraulic Fluid

- Key Growth Drivers: Essential for both automotive and heavy equipment operational efficiency and longevity.

- Market Dominance Analysis: Crucial for power transfer and smooth operation of machinery.

- Other Significant End-user Industry: Power Generation

- Key Growth Drivers: Investments in power infrastructure, need for specialized industrial oils for turbines and generators.

- Market Dominance Analysis: Consistent demand for high-value industrial lubricants.

- Other Important Product Types: General Industrial Oil, Gear Oil, Grease

- Key Growth Drivers: Growth of manufacturing sector, diverse industrial applications.

- Market Dominance Analysis: Supporting a broad range of industrial and mechanical operations.

Jordan Lubricant Industry Product Analysis

The Jordan lubricant industry is witnessing a surge in product innovation focused on enhanced performance, extended equipment life, and environmental sustainability. Manufacturers are increasingly developing synthetic and semi-synthetic lubricants that offer superior thermal stability, oxidation resistance, and wear protection compared to conventional mineral oils. These advanced formulations are crucial for meeting the stringent specifications of modern automotive engines and heavy-duty industrial machinery. Applications span from high-performance engine oils designed for fuel efficiency and reduced emissions in passenger vehicles to specialized hydraulic fluids that maintain optimal performance in extreme temperatures and pressures for construction equipment. The competitive advantage lies in offering products that not only meet but exceed OEM requirements, providing tangible benefits like reduced maintenance costs and improved operational reliability for end-users.

Key Drivers, Barriers & Challenges in Jordan Lubricant Industry

Key Drivers: The Jordan lubricant industry is propelled by several significant drivers. Technologically, the increasing adoption of advanced engine designs and heavy machinery that necessitate higher-performance lubricants is a primary catalyst. Economically, robust growth in the automotive and transportation sectors, coupled with ongoing infrastructure development projects, fuels consistent demand. Policy-driven factors, such as government initiatives promoting industrial growth and potentially stricter emission standards in the future, also encourage the use of more efficient and environmentally friendly lubricants.

Key Barriers & Challenges: Despite the positive drivers, the industry faces notable challenges. Supply chain complexities, including the reliance on imported raw materials and finished products, can lead to price volatility and potential disruptions, impacting the overall cost of production and availability. Regulatory hurdles, though aimed at ensuring quality and safety, can also add to compliance costs for manufacturers and distributors. Competitive pressures are intense, with both global brands and local players vying for market share, leading to price sensitivity among some consumer segments. Economic fluctuations, such as currency depreciation, can also impact the affordability of imported lubricants.

Growth Drivers in the Jordan Lubricant Industry Market

Key growth drivers for the Jordan lubricant industry are multifaceted. Technologically, the demand for high-performance synthetic and semi-synthetic lubricants, driven by advancements in engine technology and industrial machinery, is a significant factor. Economically, the expanding automotive fleet, coupled with substantial investments in infrastructure and construction, directly translates to increased consumption of lubricants across various segments. Regulatory factors, such as an increasing focus on environmental sustainability and potential future mandates for lower emissions, are encouraging the adoption of more eco-friendly and efficient lubricant formulations. Furthermore, the strategic importance of Jordan as a regional trade hub supports the growth of the transportation and logistics sectors, indirectly boosting lubricant demand.

Challenges Impacting Jordan Lubricant Industry Growth

Challenges impacting Jordan Lubricant Industry growth include significant supply chain vulnerabilities, primarily stemming from the reliance on imported base oils and additives, which can lead to price fluctuations and availability issues. Regulatory complexities, while essential for quality control, can impose substantial compliance costs and lengthy approval processes for new product introductions. Intense competitive pressures from both established multinational corporations and agile local players can lead to price wars and thin profit margins, particularly in the retail segment. Furthermore, the fluctuating global oil prices directly influence the cost of raw materials, impacting the overall pricing strategy and profitability of lubricant manufacturers and distributors in Jordan. Economic instability and currency depreciation can also affect the affordability of premium lubricant products for a segment of the market.

Key Players Shaping the Jordan Lubricant Industry Market

- COFRAN - REALISATION LUCMER FR

- Castrol Limited

- Chevron Corporation

- FUCHS (Qais Al Rawi & Sons Company)

- Jordan National Lube Oil Company LLT

- Jordan Petroleum Refinery Company Limited - JoPetrol

- Lubrilog

- Morris Lubricants

- Scope Lubricants

- Shell Plc

- TotalEnergie

Significant Jordan Lubricant Industry Industry Milestones

The recent developments pertaining to the major players in the market are being covered in the complete study.

Future Outlook for Jordan Lubricant Industry Market

The future outlook for the Jordan lubricant industry is cautiously optimistic, with growth catalysts expected to drive sustained expansion. The increasing adoption of advanced lubricant technologies, such as synthetics and environmentally friendly formulations, will be a key growth driver, aligning with global trends and evolving consumer preferences. Strategic opportunities lie in catering to the burgeoning automotive and heavy equipment sectors, which are expected to see continued demand due to ongoing infrastructure development and a growing vehicle parc. Furthermore, the potential for increased local manufacturing and blending capabilities could enhance supply chain resilience and offer competitive advantages. The market also presents opportunities for companies that can effectively leverage digital channels for sales and customer engagement, alongside traditional distribution networks, to capture a wider market share. The overall market potential remains significant, supported by the country's economic development and its role as a regional commercial hub.

Jordan Lubricant Industry Segmentation

-

1. Product Type

- 1.1. Engine Oil

- 1.2. Transmission and Hydraulic Fluid

- 1.3. General Industrial Oil

- 1.4. Gear Oil

- 1.5. Grease

- 1.6. Other Product Types

-

2. End-user Industry

- 2.1. Power Generation

- 2.2. Automotive and Transportation

- 2.3. Heavy Equipment

- 2.4. Other End-user Industries

Jordan Lubricant Industry Segmentation By Geography

- 1. Jordan

Jordan Lubricant Industry Regional Market Share

Geographic Coverage of Jordan Lubricant Industry

Jordan Lubricant Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.19% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Engine Oil

- 5.1.2. Transmission and Hydraulic Fluid

- 5.1.3. General Industrial Oil

- 5.1.4. Gear Oil

- 5.1.5. Grease

- 5.1.6. Other Product Types

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Power Generation

- 5.2.2. Automotive and Transportation

- 5.2.3. Heavy Equipment

- 5.2.4. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Jordan

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Jordan Lubricant Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Engine Oil

- 6.1.2. Transmission and Hydraulic Fluid

- 6.1.3. General Industrial Oil

- 6.1.4. Gear Oil

- 6.1.5. Grease

- 6.1.6. Other Product Types

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Power Generation

- 6.2.2. Automotive and Transportation

- 6.2.3. Heavy Equipment

- 6.2.4. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 COFRAN - REALISATION LUCMER FR

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Castrol Limited

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Chevron Corporation

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 FUCHS (Qais Al Rawi & Sons Company)

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Jordan National Lube Oil Company LLT

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Jordan Petroleum Refinery Company Limited - JoPetrol

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Lubrilog

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Morris Lubricants

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Scope Lubricants

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Shell Plc

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 TotalEnergie

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.1 COFRAN - REALISATION LUCMER FR

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Jordan Lubricant Industry Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: Jordan Lubricant Industry Share (%) by Company 2025

List of Tables

- Table 1: Jordan Lubricant Industry Revenue million Forecast, by Product Type 2020 & 2033

- Table 2: Jordan Lubricant Industry Revenue million Forecast, by End-user Industry 2020 & 2033

- Table 3: Jordan Lubricant Industry Revenue million Forecast, by Region 2020 & 2033

- Table 4: Jordan Lubricant Industry Revenue million Forecast, by Product Type 2020 & 2033

- Table 5: Jordan Lubricant Industry Revenue million Forecast, by End-user Industry 2020 & 2033

- Table 6: Jordan Lubricant Industry Revenue million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Jordan Lubricant Industry?

The projected CAGR is approximately 2.19%.

2. Which companies are prominent players in the Jordan Lubricant Industry?

Key companies in the market include COFRAN - REALISATION LUCMER FR, Castrol Limited, Chevron Corporation, FUCHS (Qais Al Rawi & Sons Company), Jordan National Lube Oil Company LLT, Jordan Petroleum Refinery Company Limited - JoPetrol, Lubrilog, Morris Lubricants, Scope Lubricants, Shell Plc, TotalEnergie.

3. What are the main segments of the Jordan Lubricant Industry?

The market segments include Product Type, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 33.43 million as of 2022.

5. What are some drivers contributing to market growth?

Surging Vehicle Population to Drive the Demand for Lubricants; Robust Growth of Investments in the Power Generation Sector; Other Drivers.

6. What are the notable trends driving market growth?

Engine Oil is Expected to Dominate the Market.

7. Are there any restraints impacting market growth?

Surging Vehicle Population to Drive the Demand for Lubricants; Robust Growth of Investments in the Power Generation Sector; Other Drivers.

8. Can you provide examples of recent developments in the market?

The recent developments pertaining to the major players in the market are being covered in the complete study.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Jordan Lubricant Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Jordan Lubricant Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Jordan Lubricant Industry?

To stay informed about further developments, trends, and reports in the Jordan Lubricant Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence