Key Insights

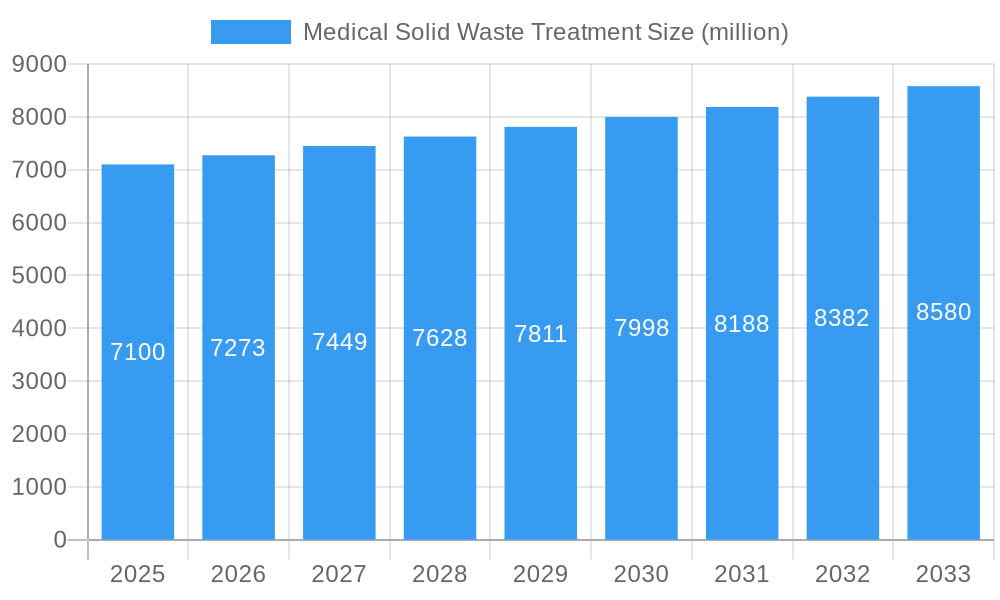

The global Medical Solid Waste Treatment market is projected to reach an estimated $7.1 billion by 2025, exhibiting a steady compound annual growth rate (CAGR) of 2.5% through 2033. This robust expansion is fueled by escalating healthcare expenditures, a growing volume of medical procedures, and an increasing global emphasis on stringent waste management protocols to mitigate the risks associated with infectious materials. The rising awareness of public health and environmental safety, particularly in the wake of global health crises, further propels the demand for effective and compliant medical waste treatment solutions. Key drivers include the growing burden of chronic diseases, an aging global population, and the expansion of healthcare infrastructure in emerging economies, all contributing to a consistent increase in the generation of medical solid waste. The market's growth is also supported by evolving regulatory frameworks and a greater adoption of advanced treatment technologies that ensure complete sterilization and safe disposal.

Medical Solid Waste Treatment Market Size (In Billion)

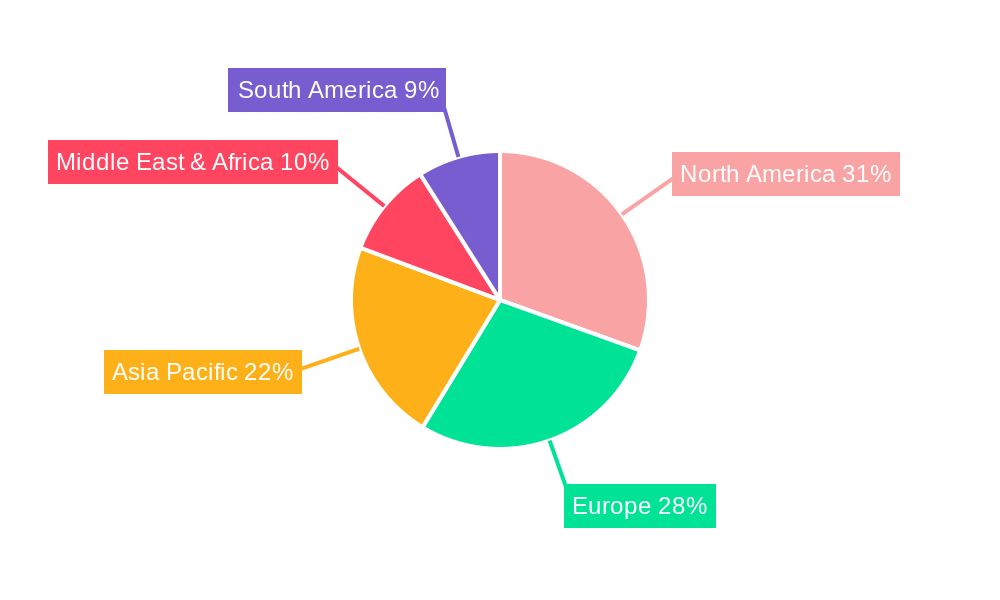

The market is segmented by application, with hospitals representing the largest share due to their high volume of waste generation, followed by diagnostic laboratories and clinics. Incineration and autoclaving remain dominant treatment types, offering proven efficacy in rendering medical waste safe. However, there is a noticeable trend towards more sustainable and environmentally friendly methods such as chemical treatment and advanced physical processes, driven by increasing concerns over emissions and the ecological impact of traditional methods. Geographically, North America and Europe currently lead the market, owing to well-established healthcare systems and stringent environmental regulations. Nevertheless, the Asia Pacific region is poised for significant growth, driven by rapid healthcare development, increasing medical tourism, and a growing awareness of the importance of medical waste management. Major companies like Stericycle, Veolia Environnement, and Waste Management are actively investing in innovative solutions and expanding their service offerings to meet the dynamic demands of this critical sector.

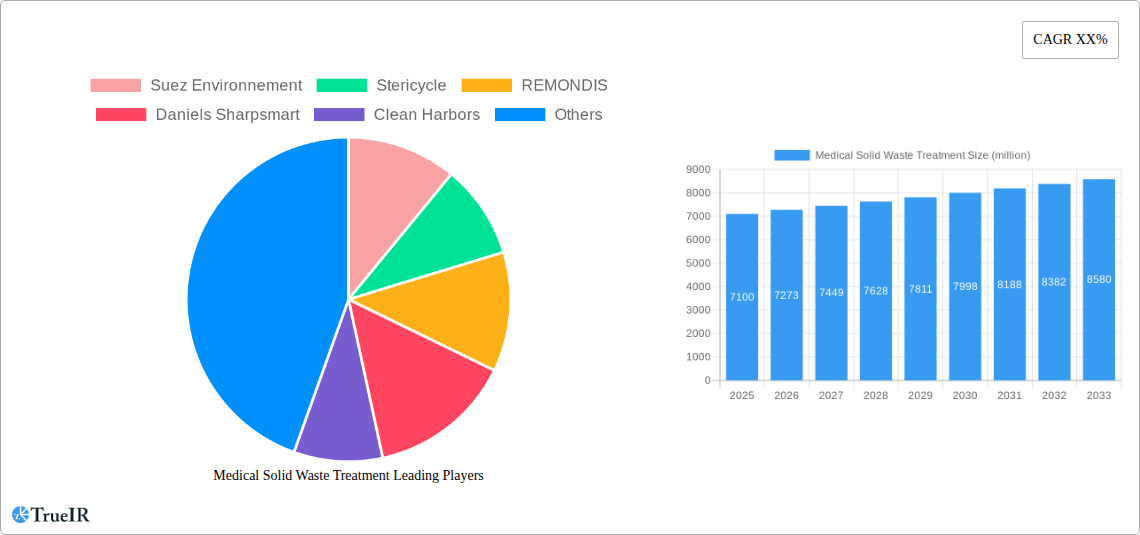

Medical Solid Waste Treatment Company Market Share

Here's a dynamic, SEO-optimized report description for the Medical Solid Waste Treatment market, designed for immediate use and incorporating your specified details.

This in-depth report provides a definitive analysis of the global Medical Solid Waste Treatment market, forecasting its trajectory from 2019 to 2033. With a base year of 2025 and a detailed forecast period spanning 2025-2033, this study offers unparalleled insights into market dynamics, emerging trends, and strategic opportunities. We meticulously examine key segments including Hospital, Clinic, Diagnostic Laboratory, Nursing Home, and Other applications, alongside dominant treatment Types such as Incineration, Autoclaving, Chemical Treatment, Mechanical/Physical Treatment, Encapsulation, Microwave Treatment, and Others. Leveraging a wealth of data from the historical period (2019-2024), this report is an indispensable resource for stakeholders seeking to navigate the evolving landscape of medical waste management.

Medical Solid Waste Treatment Market Structure & Competitive Landscape

The global Medical Solid Waste Treatment market is characterized by a moderate to high concentration, with key players investing billions in advanced disposal technologies and services. Innovation drivers are primarily fueled by stringent environmental regulations and the increasing demand for safe and sustainable healthcare waste management solutions, projected to exceed $20 billion in market value by 2025. Regulatory impacts are significant, influencing treatment methodologies and operational compliance, with governments worldwide enforcing stricter disposal protocols. Product substitutes are emerging, particularly in advanced sterilization and chemical inactivation techniques, but established methods like incineration and autoclaving continue to dominate due to their proven efficacy and cost-effectiveness. End-user segmentation reveals a strong reliance on treatment services by hospitals and diagnostic laboratories, accounting for over 70% of the market share in 2025. Mergers and acquisitions (M&A) activity remains robust, with an estimated 15-20 billion worth of deals annually in recent years, as larger entities seek to expand their service portfolios and geographic reach.

Medical Solid Waste Treatment Market Trends & Opportunities

The Medical Solid Waste Treatment market is poised for substantial growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 7.5% from 2025 to 2033. This surge is driven by an escalating global volume of infectious and hazardous medical waste, estimated to reach over 50 billion tons annually by 2025, stemming from the expanding healthcare infrastructure and an aging global population. Technological shifts are paramount, with a discernible move towards more environmentally friendly and efficient treatment methods. Autoclaving, for instance, is witnessing increased adoption due to its ability to reduce emissions compared to traditional incineration, and its market penetration is expected to rise by 15% by 2030. Chemical treatment technologies are also evolving, offering effective neutralization of hazardous components. Consumer preferences, driven by heightened public awareness of environmental sustainability and healthcare-associated infections, are pushing for transparent and verifiable waste management practices. Companies are responding by investing in digital tracking and reporting systems, enhancing traceability from point of generation to final disposal, a trend expected to capture an additional 10% market share. Competitive dynamics are intensifying, with both established giants and innovative startups vying for market dominance. Key players are focusing on integrated service offerings, encompassing collection, treatment, and disposal, creating a comprehensive waste management ecosystem. The market penetration of advanced treatment technologies is still relatively low in emerging economies, representing a significant growth opportunity for companies willing to invest in infrastructure and local partnerships. The increasing prevalence of chronic diseases and the expanding scope of medical procedures further contribute to the continuous generation of medical solid waste, ensuring a sustained demand for treatment services. Furthermore, the development of cost-effective and scalable solutions for smaller healthcare facilities and remote areas presents another avenue for market expansion. The growing emphasis on circular economy principles within the healthcare sector is also influencing the development of waste-to-energy solutions and material recovery processes, albeit in nascent stages.

Dominant Markets & Segments in Medical Solid Waste Treatment

The Hospital segment stands as the undisputed dominant market within Medical Solid Waste Treatment applications, contributing an estimated 45% of the total market revenue in 2025. This dominance is fueled by the sheer volume and complexity of waste generated in hospital settings, including sharps, infectious materials, pathological waste, and pharmaceutical waste. The Diagnostic Laboratory segment follows closely, representing approximately 25% of the market, driven by the increasing number of diagnostic tests and sample processing.

Key growth drivers for the Hospital and Diagnostic Laboratory segments include:

- Infrastructure Expansion: Continuous growth in healthcare infrastructure, particularly in emerging economies, leads to a proportional increase in medical waste generation.

- Stringent Regulatory Policies: Governments are implementing and enforcing stricter regulations on medical waste disposal, compelling healthcare facilities to adopt compliant treatment methods.

- Technological Advancements in Diagnostics: The proliferation of advanced diagnostic tools and procedures generates more specialized and potentially hazardous waste.

In terms of treatment Types, Incineration continues to hold a significant market share, estimated at 35% in 2025, due to its effectiveness in reducing the volume and infectious potential of medical waste. However, Autoclaving is experiencing robust growth, projected to reach 30% market share by 2033, driven by its environmentally friendly profile and cost-effectiveness for certain waste streams.

Key growth drivers for Autoclaving and other advanced treatment methods include:

- Environmental Concerns: Growing global concern over air pollution and greenhouse gas emissions from incineration plants is promoting the adoption of cleaner technologies.

- Cost Efficiency: For many types of medical waste, autoclaving offers a more economical solution compared to high-temperature incineration.

- Regulatory Mandates for Emission Control: Increasingly stringent emission standards for incinerators are encouraging a shift towards alternative technologies like autoclaving and chemical treatment.

The Mechanical/Physical Treatment segment, encompassing methods like shredding and compaction, is also crucial for volume reduction, especially as a pre-treatment step. While Chemical Treatment and Encapsulation serve niche but critical roles for specific hazardous waste types, Microwave Treatment represents an emerging technology with potential for future growth. The continued investment in research and development for these advanced methods, coupled with their ability to meet specific waste disposal requirements, solidifies their importance in the overall market landscape.

Medical Solid Waste Treatment Product Analysis

Innovations in Medical Solid Waste Treatment are primarily focused on enhancing efficiency, reducing environmental impact, and improving safety. Autoclaving technologies are advancing with faster cycle times and lower energy consumption, making them more accessible and cost-effective. Chemical treatment is seeing developments in more targeted and potent inactivation agents for specific pathogens. Mechanical treatment systems are becoming more integrated and automated, increasing throughput and reducing manual handling. The market fit for these products is strong, driven by evolving regulatory landscapes and the healthcare industry's increasing commitment to sustainable waste management practices. Competitive advantages are being built on reliability, compliance with international standards, and the ability to handle diverse waste streams effectively, with an estimated 3 billion annual investment in R&D by leading firms.

Key Drivers, Barriers & Challenges in Medical Solid Waste Treatment

Key Drivers: The Medical Solid Waste Treatment market is propelled by stringent government regulations mandating safe disposal, rising healthcare expenditure leading to increased waste generation, and growing environmental consciousness among healthcare providers and the public. Technological advancements in treatment methods, such as advanced autoclaving and chemical disinfection, offer more efficient and eco-friendly solutions, projected to drive market adoption by over 20%. Economic drivers include the increasing demand for specialized waste management services, creating lucrative opportunities for service providers.

Barriers & Challenges: Significant challenges include the high capital investment required for advanced treatment infrastructure, particularly in developing regions. Fluctuating fuel costs impact the operational expenses of incineration. Supply chain disruptions can affect the availability of consumables and spare parts for treatment equipment. Regulatory complexities and varying disposal standards across different jurisdictions create hurdles for companies operating globally. Competitive pressures among established players and the emergence of new market entrants also pose a challenge.

Growth Drivers in the Medical Solid Waste Treatment Market

The Medical Solid Waste Treatment market is experiencing robust growth driven by several key factors. Technological advancements, particularly in autoclaving and chemical treatment, are providing more efficient and environmentally friendly disposal options, projected to capture an additional 15% of the market share by 2030. Economic factors such as increasing healthcare spending globally, leading to higher waste generation, and the growing demand for outsourced waste management services are significant catalysts. Regulatory mandates from governmental bodies, emphasizing stringent disposal protocols and waste minimization, are compelling healthcare facilities to adopt compliant treatment solutions. The expansion of healthcare infrastructure in emerging economies further fuels this growth.

Challenges Impacting Medical Solid Waste Treatment Growth

Despite promising growth, several challenges impede the expansion of the Medical Solid Waste Treatment market. Regulatory complexities and the lack of standardized global disposal practices create compliance burdens and increase operational costs. Supply chain vulnerabilities, particularly concerning the availability of specialized equipment and chemical reagents, can disrupt service delivery. High capital investment for advanced treatment technologies remains a significant barrier, especially for smaller healthcare providers and in less developed regions, potentially limiting market penetration by an estimated 10%. Competitive pressures from established players and the need for continuous innovation to stay ahead also present ongoing challenges.

Key Players Shaping the Medical Solid Waste Treatment Market

- Suez Environnement

- Stericycle

- REMONDIS

- Daniels Sharpsmart

- Clean Harbors

- BioMedical Waste Solutions, LLC

- EcoMed Services

- Republic Services

- Sharps Compliance

- Veolia Environnement

- Waste Management

- BWS Incorporated

- GRP & Associates

- MedPro Disposal

Significant Medical Solid Waste Treatment Industry Milestones

- 2019: Increased global focus on single-use medical supplies, leading to higher volumes of medical solid waste.

- 2020: Emergence of COVID-19 pandemic, significantly increasing the demand for medical waste disposal services and highlighting the importance of robust treatment infrastructure.

- 2021: Release of updated WHO guidelines on safe management of health-care waste, influencing national regulations and driving adoption of best practices.

- 2022: Growing investment in advanced autoclaving technologies for more sustainable waste treatment.

- 2023: Increased M&A activity as larger waste management companies consolidate their market positions and expand service offerings.

- 2024: Enhanced focus on digital tracking and reporting for medical waste management, improving transparency and accountability.

Future Outlook for Medical Solid Waste Treatment Market

The future outlook for the Medical Solid Waste Treatment market is exceptionally positive, projecting sustained growth driven by increasing global healthcare expenditures and a growing emphasis on environmental sustainability. Strategic opportunities lie in the development and adoption of innovative, low-emission treatment technologies and integrated waste management solutions. The market potential is vast, particularly in emerging economies where healthcare infrastructure is expanding rapidly, and regulatory frameworks are being strengthened. Companies that can offer cost-effective, compliant, and environmentally sound waste treatment services are poised for significant success in the coming years, with an anticipated market value exceeding $35 billion by 2033.

Medical Solid Waste Treatment Segmentation

-

1. Application

- 1.1. Hospital

- 1.2. Clinic

- 1.3. Diagnostic Laboratory

- 1.4. Nursing Home

- 1.5. Other

-

2. Types

- 2.1. Incineration

- 2.2. Autoclaving

- 2.3. Chemical Treatment

- 2.4. Mechanical/Physical Treatment

- 2.5. Encapsulation

- 2.6. Microwave Treatment

- 2.7. Others

Medical Solid Waste Treatment Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Medical Solid Waste Treatment Regional Market Share

Geographic Coverage of Medical Solid Waste Treatment

Medical Solid Waste Treatment REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 13.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Medical Solid Waste Treatment Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospital

- 5.1.2. Clinic

- 5.1.3. Diagnostic Laboratory

- 5.1.4. Nursing Home

- 5.1.5. Other

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Incineration

- 5.2.2. Autoclaving

- 5.2.3. Chemical Treatment

- 5.2.4. Mechanical/Physical Treatment

- 5.2.5. Encapsulation

- 5.2.6. Microwave Treatment

- 5.2.7. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Medical Solid Waste Treatment Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hospital

- 6.1.2. Clinic

- 6.1.3. Diagnostic Laboratory

- 6.1.4. Nursing Home

- 6.1.5. Other

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Incineration

- 6.2.2. Autoclaving

- 6.2.3. Chemical Treatment

- 6.2.4. Mechanical/Physical Treatment

- 6.2.5. Encapsulation

- 6.2.6. Microwave Treatment

- 6.2.7. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Medical Solid Waste Treatment Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hospital

- 7.1.2. Clinic

- 7.1.3. Diagnostic Laboratory

- 7.1.4. Nursing Home

- 7.1.5. Other

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Incineration

- 7.2.2. Autoclaving

- 7.2.3. Chemical Treatment

- 7.2.4. Mechanical/Physical Treatment

- 7.2.5. Encapsulation

- 7.2.6. Microwave Treatment

- 7.2.7. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Medical Solid Waste Treatment Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hospital

- 8.1.2. Clinic

- 8.1.3. Diagnostic Laboratory

- 8.1.4. Nursing Home

- 8.1.5. Other

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Incineration

- 8.2.2. Autoclaving

- 8.2.3. Chemical Treatment

- 8.2.4. Mechanical/Physical Treatment

- 8.2.5. Encapsulation

- 8.2.6. Microwave Treatment

- 8.2.7. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Medical Solid Waste Treatment Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hospital

- 9.1.2. Clinic

- 9.1.3. Diagnostic Laboratory

- 9.1.4. Nursing Home

- 9.1.5. Other

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Incineration

- 9.2.2. Autoclaving

- 9.2.3. Chemical Treatment

- 9.2.4. Mechanical/Physical Treatment

- 9.2.5. Encapsulation

- 9.2.6. Microwave Treatment

- 9.2.7. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Medical Solid Waste Treatment Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hospital

- 10.1.2. Clinic

- 10.1.3. Diagnostic Laboratory

- 10.1.4. Nursing Home

- 10.1.5. Other

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Incineration

- 10.2.2. Autoclaving

- 10.2.3. Chemical Treatment

- 10.2.4. Mechanical/Physical Treatment

- 10.2.5. Encapsulation

- 10.2.6. Microwave Treatment

- 10.2.7. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Suez Environnement

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Stericycle

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 REMONDIS

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Daniels Sharpsmart

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Clean Harbors

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 BioMedical Waste Solutions

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 LLC

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 EcoMed Services

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Republic Services

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Sharps Compliance

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Veolia Environnement

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Waste Management

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 BWS Incorporated

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 GRP & Associates

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 MedPro Disposal

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.1 Suez Environnement

List of Figures

- Figure 1: Global Medical Solid Waste Treatment Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Medical Solid Waste Treatment Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Medical Solid Waste Treatment Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Medical Solid Waste Treatment Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Medical Solid Waste Treatment Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Medical Solid Waste Treatment Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Medical Solid Waste Treatment Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Medical Solid Waste Treatment Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Medical Solid Waste Treatment Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Medical Solid Waste Treatment Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Medical Solid Waste Treatment Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Medical Solid Waste Treatment Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Medical Solid Waste Treatment Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Medical Solid Waste Treatment Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Medical Solid Waste Treatment Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Medical Solid Waste Treatment Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Medical Solid Waste Treatment Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Medical Solid Waste Treatment Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Medical Solid Waste Treatment Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Medical Solid Waste Treatment Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Medical Solid Waste Treatment Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Medical Solid Waste Treatment Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Medical Solid Waste Treatment Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Medical Solid Waste Treatment Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Medical Solid Waste Treatment Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Medical Solid Waste Treatment Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Medical Solid Waste Treatment Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Medical Solid Waste Treatment Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Medical Solid Waste Treatment Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Medical Solid Waste Treatment Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Medical Solid Waste Treatment Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Medical Solid Waste Treatment Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Medical Solid Waste Treatment Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Medical Solid Waste Treatment Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Medical Solid Waste Treatment Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Medical Solid Waste Treatment Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Medical Solid Waste Treatment Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Medical Solid Waste Treatment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Medical Solid Waste Treatment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Medical Solid Waste Treatment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Medical Solid Waste Treatment Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Medical Solid Waste Treatment Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Medical Solid Waste Treatment Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Medical Solid Waste Treatment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Medical Solid Waste Treatment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Medical Solid Waste Treatment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Medical Solid Waste Treatment Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Medical Solid Waste Treatment Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Medical Solid Waste Treatment Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Medical Solid Waste Treatment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Medical Solid Waste Treatment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Medical Solid Waste Treatment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Medical Solid Waste Treatment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Medical Solid Waste Treatment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Medical Solid Waste Treatment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Medical Solid Waste Treatment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Medical Solid Waste Treatment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Medical Solid Waste Treatment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Medical Solid Waste Treatment Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Medical Solid Waste Treatment Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Medical Solid Waste Treatment Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Medical Solid Waste Treatment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Medical Solid Waste Treatment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Medical Solid Waste Treatment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Medical Solid Waste Treatment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Medical Solid Waste Treatment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Medical Solid Waste Treatment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Medical Solid Waste Treatment Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Medical Solid Waste Treatment Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Medical Solid Waste Treatment Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Medical Solid Waste Treatment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Medical Solid Waste Treatment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Medical Solid Waste Treatment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Medical Solid Waste Treatment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Medical Solid Waste Treatment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Medical Solid Waste Treatment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Medical Solid Waste Treatment Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Medical Solid Waste Treatment?

The projected CAGR is approximately 13.4%.

2. Which companies are prominent players in the Medical Solid Waste Treatment?

Key companies in the market include Suez Environnement, Stericycle, REMONDIS, Daniels Sharpsmart, Clean Harbors, BioMedical Waste Solutions, LLC, EcoMed Services, Republic Services, Sharps Compliance, Veolia Environnement, Waste Management, BWS Incorporated, GRP & Associates, MedPro Disposal.

3. What are the main segments of the Medical Solid Waste Treatment?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Medical Solid Waste Treatment," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Medical Solid Waste Treatment report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Medical Solid Waste Treatment?

To stay informed about further developments, trends, and reports in the Medical Solid Waste Treatment, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence