Key Insights

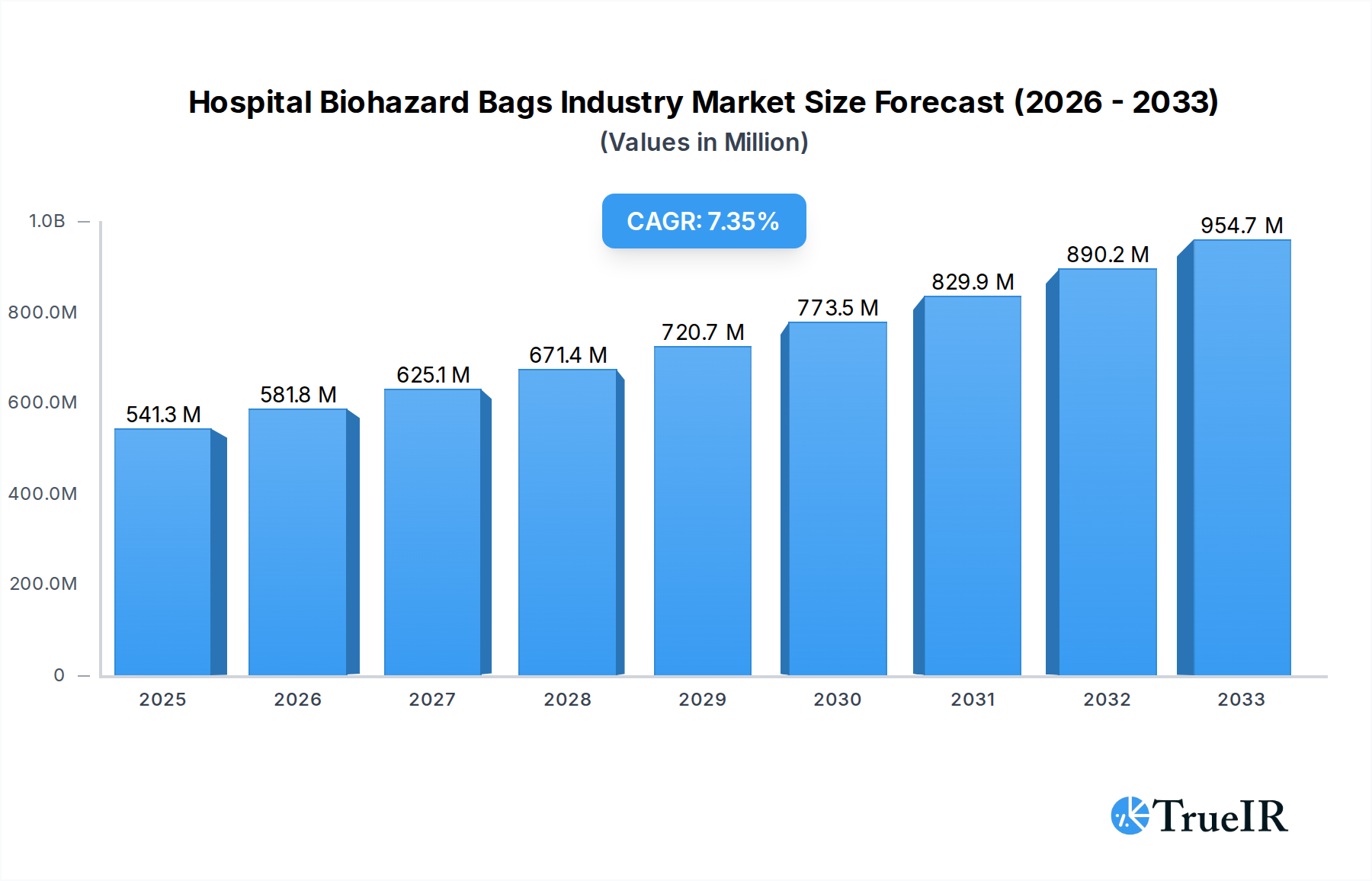

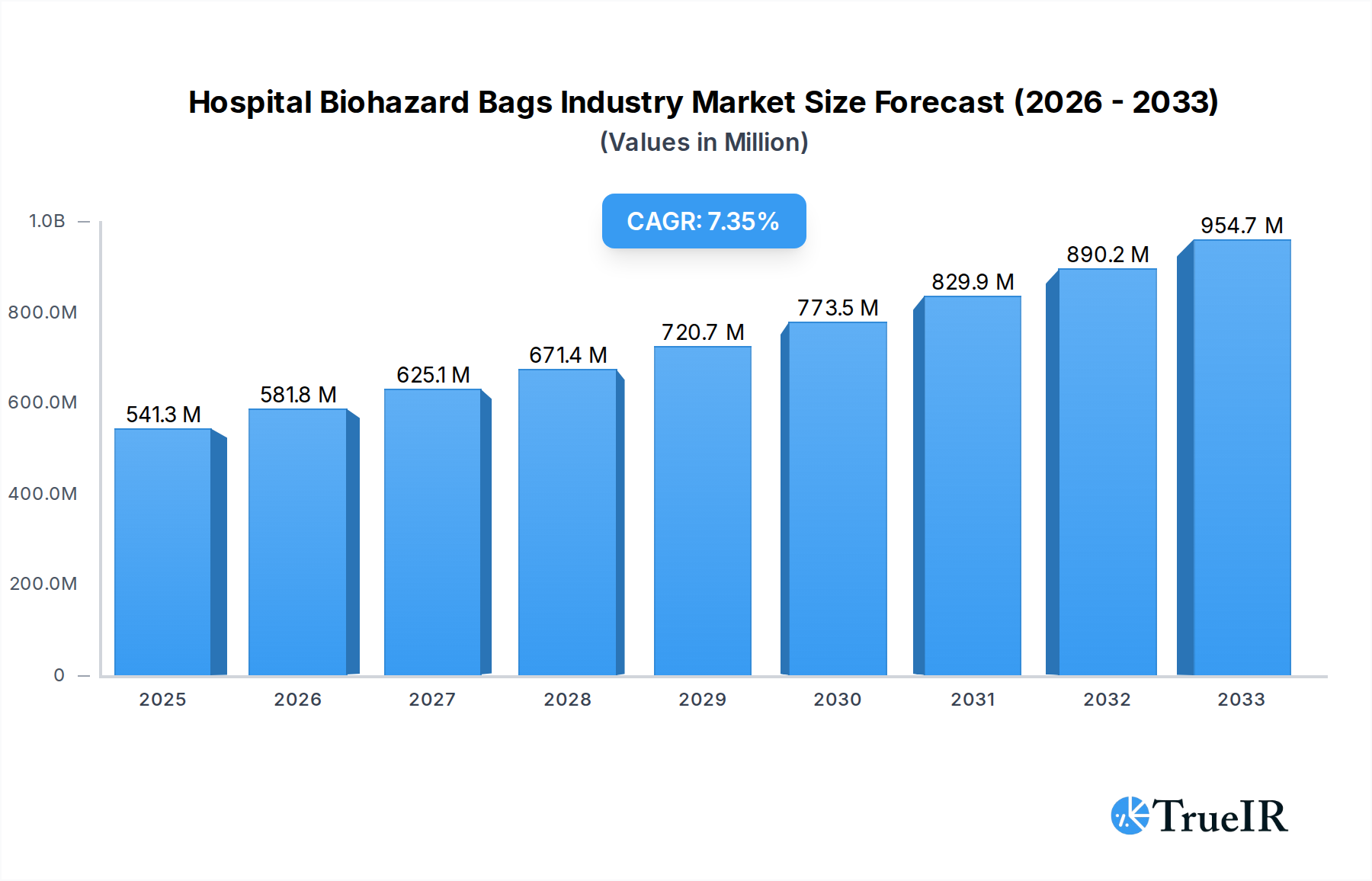

The global Hospital Biohazard Bags market is poised for substantial growth, projected to reach $541.28 million by 2025, demonstrating a robust Compound Annual Growth Rate (CAGR) of 7.6% through 2033. This upward trajectory is largely fueled by escalating healthcare expenditures worldwide, a growing emphasis on infection control protocols within medical facilities, and the increasing volume of infectious waste generated by hospitals and diagnostic laboratories. The surge in awareness regarding proper biohazardous waste disposal, coupled with stringent regulatory frameworks aimed at preventing the spread of infections, further propels market expansion. Advancements in material science, leading to the development of more durable and puncture-resistant biohazard bags, are also key drivers, enhancing safety and compliance.

Hospital Biohazard Bags Industry Market Size (In Million)

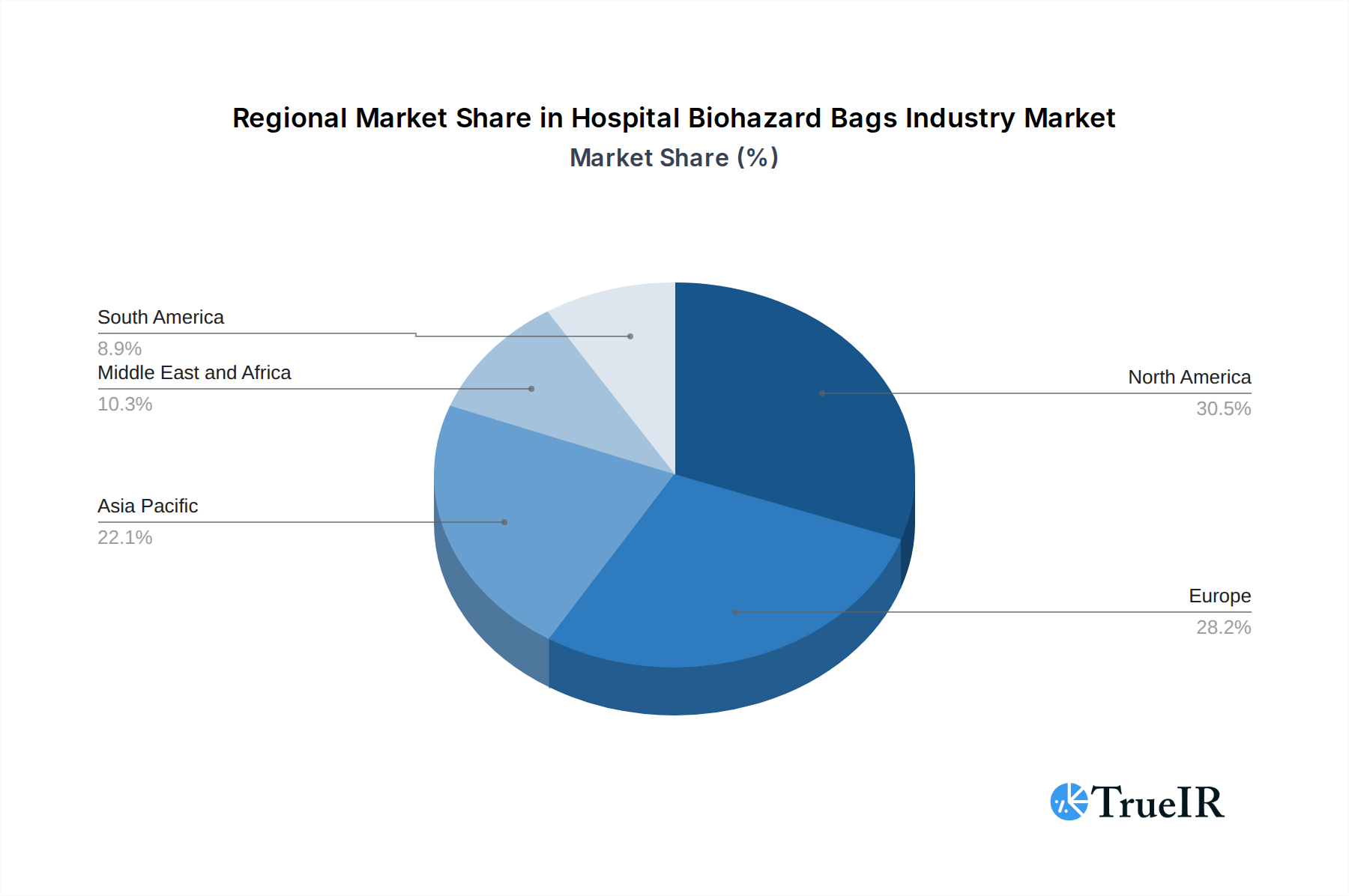

The market segmentation reveals significant opportunities across various product materials and applications. LDPE, HDPE, and Polypropylene are expected to dominate product material segments due to their cost-effectiveness and essential barrier properties. In terms of applications, the management of infectious waste and the containment of healthcare waste represent the largest segments, reflecting the core function of these bags. Hospitals and diagnostic laboratories are identified as the primary end-users, underscoring their critical role in generating and managing biohazardous materials. Geographically, North America and Europe are anticipated to maintain their leading positions, driven by well-established healthcare infrastructures and high standards for waste management. However, the Asia Pacific region is expected to exhibit the fastest growth, propelled by rapid healthcare development, increasing adoption of advanced medical practices, and a growing patient base.

Hospital Biohazard Bags Industry Company Market Share

This in-depth report provides a dynamic and SEO-optimized analysis of the global Hospital Biohazard Bags market. Leveraging high-volume keywords such as "biohazard bags," "medical waste disposal," "healthcare safety products," and "infection control solutions," this research meticulously details market dynamics, trends, opportunities, and competitive landscapes. Our study covers the historical period from 2019 to 2024, with a base year of 2025 and a comprehensive forecast extending to 2033.

The Hospital Biohazard Bags industry is a critical component of healthcare infrastructure, ensuring safe containment and disposal of infectious materials. This report aims to equip stakeholders, including manufacturers, suppliers, healthcare providers, and investors, with actionable intelligence to navigate this vital sector. The analysis encompasses a detailed examination of product materials, application segments, end-user demographics, and significant industry developments.

Hospital Biohazard Bags Industry Market Structure & Competitive Landscape

The Hospital Biohazard Bags market exhibits a moderately consolidated structure, characterized by the presence of both large multinational corporations and a significant number of regional players. Innovation drivers are primarily focused on enhanced durability, puncture resistance, leak-proof sealing, and advanced color-coding systems for improved waste segregation. Regulatory frameworks play a pivotal role, with stringent guidelines governing the safe handling and disposal of biohazardous materials influencing product development and market entry. Product substitutes, while limited for specialized biohazard applications, include general-purpose waste bags and reusable containment systems, though these do not offer the same level of safety and compliance. End-user segmentation reveals a strong reliance on hospitals, which constitute the largest consumer base, followed by diagnostic laboratories and other healthcare facilities. Mergers and acquisitions (M&A) trends, while not extensively dominant, indicate strategic consolidations aimed at expanding market reach, technological capabilities, and product portfolios. For instance, the past few years have seen strategic acquisitions aimed at bolstering supply chains and integrating advanced manufacturing technologies, contributing to a concentration ratio in the range of 35-45% among the top five players in specific regional markets.

Hospital Biohazard Bags Industry Market Trends & Opportunities

The Hospital Biohazard Bags industry is poised for robust growth, driven by an increasing global emphasis on infection control and public health. The market size is projected to witness a Compound Annual Growth Rate (CAGR) of approximately 6.5% from 2025 to 2033, expanding from an estimated market value of over $500 million in the base year to potentially exceed $850 million by the end of the forecast period. Technological shifts are increasingly favoring the development of biohazard bags with enhanced barrier properties, such as improved puncture resistance and superior sealing technologies, to prevent leaks and cross-contamination. Consumer preferences are evolving towards eco-friendlier options, prompting manufacturers to explore biodegradable and compostable materials, albeit with careful consideration for their efficacy in containing hazardous waste. Competitive dynamics are intensifying, with players focusing on product differentiation through specialized features, certifications, and competitive pricing strategies. The growing prevalence of infectious diseases, coupled with expanding healthcare infrastructure in emerging economies, presents significant market penetration opportunities. Furthermore, the increasing adoption of stringent waste management protocols by governments worldwide acts as a powerful catalyst for market expansion. The demand for specialized biohazard bags for specific waste streams, such as chemotherapy waste and radioactive materials, is also on the rise, opening niche market opportunities. The integration of smart technologies, such as RFID tagging for enhanced tracking and inventory management of biohazardous waste, is an emerging trend that could redefine product offerings and operational efficiencies for end-users.

Dominant Markets & Segments in Hospital Biohazard Bags Industry

The Hospital Biohazard Bags industry is dominated by regions with well-established healthcare systems and stringent waste management regulations. North America and Europe currently hold significant market share, driven by high healthcare expenditure, advanced medical facilities, and strong public health initiatives. However, the Asia Pacific region is emerging as a rapidly growing market, fueled by a burgeoning healthcare sector, increasing awareness of infectious disease control, and government investments in medical infrastructure.

- Dominant Region: North America, followed closely by Europe.

- Dominant Country: The United States leads in market consumption due to its extensive healthcare network and robust regulatory framework.

Key Segment Analysis:

Product Material:

- LDPE (Low-Density Polyethylene): Holds the largest market share due to its flexibility, tear resistance, and cost-effectiveness, making it suitable for a wide range of applications. Its widespread use is driven by its proven reliability in containing various types of medical waste.

- HDPE (High-Density Polyethylene): Offers superior strength and rigidity, making it ideal for heavier waste or where a more robust barrier is required.

- Polypropylene: Increasingly gaining traction due to its excellent chemical resistance and high-temperature stability, particularly for specialized applications.

- Cellophane: Though a smaller segment, it is utilized in specific niche applications where biodegradability and transparency are paramount, subject to regulatory compliance for hazardous waste containment.

Application:

- Healthcare Waste: This is the most dominant application segment, encompassing general medical waste, contaminated materials, and sharps. The sheer volume of healthcare waste generated globally ensures continuous demand.

- Infections: Specifically refers to the containment of materials contaminated by highly infectious agents, requiring specialized bags with enhanced barrier properties and clear labeling.

- Chemical & Pharmaceutical: Utilized for the safe disposal of chemical and pharmaceutical waste generated in research laboratories and manufacturing facilities.

- Other Applications: Includes waste from veterinary clinics, research institutions, and industrial settings dealing with hazardous substances.

End User:

- Hospitals: Represent the largest end-user segment, accounting for a significant portion of the global demand due to the high volume of biohazardous waste generated from patient care, surgeries, and laboratories.

- Diagnostic Laboratories: These facilities generate substantial amounts of infectious and chemical waste, making them crucial consumers of biohazard bags.

- Other End Users: This includes clinics, long-term care facilities, research institutions, blood banks, and emergency medical services.

Growth drivers across these segments include the increasing number of surgical procedures, the rising incidence of hospital-acquired infections, and the expanding network of diagnostic testing facilities, particularly in developing nations. Government initiatives promoting safe medical waste management and the enforcement of environmental regulations further bolster the demand for compliant biohazard bags.

Hospital Biohazard Bags Industry Product Analysis

Product innovations in the Hospital Biohazard Bags industry are continuously enhancing safety and efficiency. Key advancements include the development of multi-layer construction for superior puncture and tear resistance, integrated tamper-evident seals for enhanced security, and specialized antimicrobial coatings to inhibit microbial growth within the bag. Applications span the safe containment of infectious materials from patient care, sharps disposal, chemotherapy waste, and radioactive substances, each requiring specific certifications and material properties. Competitive advantages are derived from compliance with international standards (e.g., ASTM, ISO), robust leak-proof performance, user-friendly features like reinforced handles, and clear, standardized hazard symbol printing, ensuring effective communication of risks.

Key Drivers, Barriers & Challenges in Hospital Biohazard Bags Industry

Key Drivers: The Hospital Biohazard Bags industry is propelled by a confluence of factors. Technologically, advancements in polymer science are yielding more durable, puncture-resistant, and leak-proof bag materials, enhancing safety. Economically, the growing global healthcare expenditure and the expansion of healthcare infrastructure, particularly in emerging economies, are significantly increasing demand. Policy-driven factors, such as increasingly stringent government regulations on medical waste disposal and a growing global awareness of infection control protocols, are paramount. For instance, government mandates for the segregation and safe disposal of infectious waste directly stimulate the market for specialized biohazard bags. The increasing prevalence of infectious diseases also acts as a persistent driver.

Barriers & Challenges: Despite robust growth, the Hospital Biohazard Bags industry faces several challenges. Supply chain disruptions, particularly in raw material sourcing and logistics, can impact production and delivery timelines. Regulatory hurdles, while driving demand, can also present barriers to entry for new manufacturers, requiring significant investment in compliance and certifications. Competitive pressures, especially from low-cost manufacturers in certain regions, can affect profit margins. The cost of specialized, high-performance biohazard bags can also be a restraint for smaller healthcare facilities with limited budgets. Furthermore, the development and adoption of truly sustainable biohazard bag options that meet stringent safety requirements remain a complex challenge, balancing environmental concerns with critical containment needs.

Growth Drivers in the Hospital Biohazard Bags Industry Market

Key growth drivers in the Hospital Biohazard Bags industry are multifaceted. Technological advancements in material science are leading to the development of stronger, more puncture-resistant, and leak-proof biohazard bags, enhancing safety and reliability. The increasing global expenditure on healthcare, coupled with the expansion of healthcare infrastructure, especially in emerging economies, directly translates to higher demand for medical consumables, including biohazard bags. Regulatory mandates from governments worldwide, emphasizing stringent medical waste disposal protocols and infection control, are significant growth catalysts. For example, regulations requiring specific color-coding and labeling for different types of biohazardous waste spur demand for compliant products. The rising global incidence of infectious diseases and pandemics further amplifies the need for effective containment and disposal solutions, creating consistent market demand.

Challenges Impacting Hospital Biohazard Bags Industry Growth

The Hospital Biohazard Bags industry faces several significant challenges. Regulatory complexities, including evolving standards and the need for extensive product testing and certification, can create barriers to entry and slow down product development cycles. Supply chain vulnerabilities, ranging from raw material price volatility to logistical bottlenecks, can impact production costs and delivery timelines, especially in a globalized market. Intense competitive pressures, particularly from manufacturers in regions with lower production costs, can lead to price wars and erode profit margins. The development of truly biodegradable and compostable biohazard bags that meet the stringent safety and containment requirements for hazardous medical waste remains a significant technical and economic challenge, as current eco-friendly alternatives may not always offer the required level of protection.

Key Players Shaping the Hospital Biohazard Bags Industry Market

- Transcendia Inc

- Merck KGaA

- Bionics Scientific Technologies Pvt Ltd

- Harbour Group (SP Bel-Art)

- Desco Medical India

- Welpack Industries Pvt Ltd

- TUFPAK INC

- International Plastics Inc

- Champion Plastics

- Inteplast Group Corporation (Minigrip LLC)

- Thermo Fisher Scientific

Significant Hospital Biohazard Bags Industry Industry Milestones

- April 2022: The West Bengal Bench of the Authority for Advance Ruling (AAR) announced in April 2022 that services offered to the State Government for collecting and disposing of bio-medical waste are exempt from GST. This ruling provides significant financial relief to entities involved in bio-medical waste management, potentially encouraging greater investment and efficiency in waste disposal services, indirectly boosting the demand for compliant biohazard bags.

- January 2022: The South Delhi Municipal Corporation (SDMC) established helpline numbers for collecting biomedical waste from the residences of Covid-19 patients. This initiative highlights a crucial adaptation in waste management during public health crises, emphasizing the need for accessible and efficient collection of infectious waste from non-traditional sources, underscoring the vital role of reliable biohazard containment solutions in diverse settings.

Future Outlook for Hospital Biohazard Bags Industry Market

The future outlook for the Hospital Biohazard Bags industry is exceptionally promising, driven by sustained global demand for effective healthcare waste management. Strategic opportunities lie in the development and commercialization of advanced biodegradable and compostable biohazard bags that meet stringent safety standards, addressing growing environmental concerns. The expanding healthcare infrastructure in emerging markets presents significant growth potential, requiring a substantial increase in the supply of essential safety products. Furthermore, the integration of smart technologies for enhanced tracking and inventory management of biohazardous waste offers a pathway for value-added product differentiation and improved operational efficiency for end-users. Continued investment in research and development to create superior barrier properties and user-friendly designs will be crucial for market leadership.

Hospital Biohazard Bags Industry Segmentation

-

1. Product Material

- 1.1. LDPE

- 1.2. HDPE

- 1.3. Cellophane

- 1.4. Polypropylene

-

2. Application

- 2.1. Infections

- 2.2. Healthcare Waste

- 2.3. Chemical & Pharmaceutical

- 2.4. Other Applications

-

3. End User

- 3.1. Hospitals

- 3.2. Diagnostic Laboratories

- 3.3. Other End Users

Hospital Biohazard Bags Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Hospital Biohazard Bags Industry Regional Market Share

Geographic Coverage of Hospital Biohazard Bags Industry

Hospital Biohazard Bags Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Material

- 5.1.1. LDPE

- 5.1.2. HDPE

- 5.1.3. Cellophane

- 5.1.4. Polypropylene

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Infections

- 5.2.2. Healthcare Waste

- 5.2.3. Chemical & Pharmaceutical

- 5.2.4. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by End User

- 5.3.1. Hospitals

- 5.3.2. Diagnostic Laboratories

- 5.3.3. Other End Users

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Middle East and Africa

- 5.4.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Product Material

- 6. Global Hospital Biohazard Bags Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Material

- 6.1.1. LDPE

- 6.1.2. HDPE

- 6.1.3. Cellophane

- 6.1.4. Polypropylene

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Infections

- 6.2.2. Healthcare Waste

- 6.2.3. Chemical & Pharmaceutical

- 6.2.4. Other Applications

- 6.3. Market Analysis, Insights and Forecast - by End User

- 6.3.1. Hospitals

- 6.3.2. Diagnostic Laboratories

- 6.3.3. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Product Material

- 7. North America Hospital Biohazard Bags Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product Material

- 7.1.1. LDPE

- 7.1.2. HDPE

- 7.1.3. Cellophane

- 7.1.4. Polypropylene

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Infections

- 7.2.2. Healthcare Waste

- 7.2.3. Chemical & Pharmaceutical

- 7.2.4. Other Applications

- 7.3. Market Analysis, Insights and Forecast - by End User

- 7.3.1. Hospitals

- 7.3.2. Diagnostic Laboratories

- 7.3.3. Other End Users

- 7.1. Market Analysis, Insights and Forecast - by Product Material

- 8. Europe Hospital Biohazard Bags Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product Material

- 8.1.1. LDPE

- 8.1.2. HDPE

- 8.1.3. Cellophane

- 8.1.4. Polypropylene

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Infections

- 8.2.2. Healthcare Waste

- 8.2.3. Chemical & Pharmaceutical

- 8.2.4. Other Applications

- 8.3. Market Analysis, Insights and Forecast - by End User

- 8.3.1. Hospitals

- 8.3.2. Diagnostic Laboratories

- 8.3.3. Other End Users

- 8.1. Market Analysis, Insights and Forecast - by Product Material

- 9. Asia Pacific Hospital Biohazard Bags Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product Material

- 9.1.1. LDPE

- 9.1.2. HDPE

- 9.1.3. Cellophane

- 9.1.4. Polypropylene

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Infections

- 9.2.2. Healthcare Waste

- 9.2.3. Chemical & Pharmaceutical

- 9.2.4. Other Applications

- 9.3. Market Analysis, Insights and Forecast - by End User

- 9.3.1. Hospitals

- 9.3.2. Diagnostic Laboratories

- 9.3.3. Other End Users

- 9.1. Market Analysis, Insights and Forecast - by Product Material

- 10. Middle East and Africa Hospital Biohazard Bags Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product Material

- 10.1.1. LDPE

- 10.1.2. HDPE

- 10.1.3. Cellophane

- 10.1.4. Polypropylene

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Infections

- 10.2.2. Healthcare Waste

- 10.2.3. Chemical & Pharmaceutical

- 10.2.4. Other Applications

- 10.3. Market Analysis, Insights and Forecast - by End User

- 10.3.1. Hospitals

- 10.3.2. Diagnostic Laboratories

- 10.3.3. Other End Users

- 10.1. Market Analysis, Insights and Forecast - by Product Material

- 11. South America Hospital Biohazard Bags Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product Material

- 11.1.1. LDPE

- 11.1.2. HDPE

- 11.1.3. Cellophane

- 11.1.4. Polypropylene

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Infections

- 11.2.2. Healthcare Waste

- 11.2.3. Chemical & Pharmaceutical

- 11.2.4. Other Applications

- 11.3. Market Analysis, Insights and Forecast - by End User

- 11.3.1. Hospitals

- 11.3.2. Diagnostic Laboratories

- 11.3.3. Other End Users

- 11.1. Market Analysis, Insights and Forecast - by Product Material

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Transcendia Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Merck KGaA

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Bionics Scientific Technologies Pvt Ltd

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Harbour Group (SP Bel-Art)

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Desco Medical India*List Not Exhaustive

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Welpack Industries Pvt Ltd

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 TUFPAK INC

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 International Plastics Inc

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Champion Plastics

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Inteplast Group Corporation (Minigrip LLC)

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Thermo Fisher Scientific

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.1 Transcendia Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Hospital Biohazard Bags Industry Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Hospital Biohazard Bags Industry Revenue (million), by Product Material 2025 & 2033

- Figure 3: North America Hospital Biohazard Bags Industry Revenue Share (%), by Product Material 2025 & 2033

- Figure 4: North America Hospital Biohazard Bags Industry Revenue (million), by Application 2025 & 2033

- Figure 5: North America Hospital Biohazard Bags Industry Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Hospital Biohazard Bags Industry Revenue (million), by End User 2025 & 2033

- Figure 7: North America Hospital Biohazard Bags Industry Revenue Share (%), by End User 2025 & 2033

- Figure 8: North America Hospital Biohazard Bags Industry Revenue (million), by Country 2025 & 2033

- Figure 9: North America Hospital Biohazard Bags Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Hospital Biohazard Bags Industry Revenue (million), by Product Material 2025 & 2033

- Figure 11: Europe Hospital Biohazard Bags Industry Revenue Share (%), by Product Material 2025 & 2033

- Figure 12: Europe Hospital Biohazard Bags Industry Revenue (million), by Application 2025 & 2033

- Figure 13: Europe Hospital Biohazard Bags Industry Revenue Share (%), by Application 2025 & 2033

- Figure 14: Europe Hospital Biohazard Bags Industry Revenue (million), by End User 2025 & 2033

- Figure 15: Europe Hospital Biohazard Bags Industry Revenue Share (%), by End User 2025 & 2033

- Figure 16: Europe Hospital Biohazard Bags Industry Revenue (million), by Country 2025 & 2033

- Figure 17: Europe Hospital Biohazard Bags Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Hospital Biohazard Bags Industry Revenue (million), by Product Material 2025 & 2033

- Figure 19: Asia Pacific Hospital Biohazard Bags Industry Revenue Share (%), by Product Material 2025 & 2033

- Figure 20: Asia Pacific Hospital Biohazard Bags Industry Revenue (million), by Application 2025 & 2033

- Figure 21: Asia Pacific Hospital Biohazard Bags Industry Revenue Share (%), by Application 2025 & 2033

- Figure 22: Asia Pacific Hospital Biohazard Bags Industry Revenue (million), by End User 2025 & 2033

- Figure 23: Asia Pacific Hospital Biohazard Bags Industry Revenue Share (%), by End User 2025 & 2033

- Figure 24: Asia Pacific Hospital Biohazard Bags Industry Revenue (million), by Country 2025 & 2033

- Figure 25: Asia Pacific Hospital Biohazard Bags Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Hospital Biohazard Bags Industry Revenue (million), by Product Material 2025 & 2033

- Figure 27: Middle East and Africa Hospital Biohazard Bags Industry Revenue Share (%), by Product Material 2025 & 2033

- Figure 28: Middle East and Africa Hospital Biohazard Bags Industry Revenue (million), by Application 2025 & 2033

- Figure 29: Middle East and Africa Hospital Biohazard Bags Industry Revenue Share (%), by Application 2025 & 2033

- Figure 30: Middle East and Africa Hospital Biohazard Bags Industry Revenue (million), by End User 2025 & 2033

- Figure 31: Middle East and Africa Hospital Biohazard Bags Industry Revenue Share (%), by End User 2025 & 2033

- Figure 32: Middle East and Africa Hospital Biohazard Bags Industry Revenue (million), by Country 2025 & 2033

- Figure 33: Middle East and Africa Hospital Biohazard Bags Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: South America Hospital Biohazard Bags Industry Revenue (million), by Product Material 2025 & 2033

- Figure 35: South America Hospital Biohazard Bags Industry Revenue Share (%), by Product Material 2025 & 2033

- Figure 36: South America Hospital Biohazard Bags Industry Revenue (million), by Application 2025 & 2033

- Figure 37: South America Hospital Biohazard Bags Industry Revenue Share (%), by Application 2025 & 2033

- Figure 38: South America Hospital Biohazard Bags Industry Revenue (million), by End User 2025 & 2033

- Figure 39: South America Hospital Biohazard Bags Industry Revenue Share (%), by End User 2025 & 2033

- Figure 40: South America Hospital Biohazard Bags Industry Revenue (million), by Country 2025 & 2033

- Figure 41: South America Hospital Biohazard Bags Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Hospital Biohazard Bags Industry Revenue million Forecast, by Product Material 2020 & 2033

- Table 2: Global Hospital Biohazard Bags Industry Revenue million Forecast, by Application 2020 & 2033

- Table 3: Global Hospital Biohazard Bags Industry Revenue million Forecast, by End User 2020 & 2033

- Table 4: Global Hospital Biohazard Bags Industry Revenue million Forecast, by Region 2020 & 2033

- Table 5: Global Hospital Biohazard Bags Industry Revenue million Forecast, by Product Material 2020 & 2033

- Table 6: Global Hospital Biohazard Bags Industry Revenue million Forecast, by Application 2020 & 2033

- Table 7: Global Hospital Biohazard Bags Industry Revenue million Forecast, by End User 2020 & 2033

- Table 8: Global Hospital Biohazard Bags Industry Revenue million Forecast, by Country 2020 & 2033

- Table 9: United States Hospital Biohazard Bags Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Canada Hospital Biohazard Bags Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 11: Mexico Hospital Biohazard Bags Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 12: Global Hospital Biohazard Bags Industry Revenue million Forecast, by Product Material 2020 & 2033

- Table 13: Global Hospital Biohazard Bags Industry Revenue million Forecast, by Application 2020 & 2033

- Table 14: Global Hospital Biohazard Bags Industry Revenue million Forecast, by End User 2020 & 2033

- Table 15: Global Hospital Biohazard Bags Industry Revenue million Forecast, by Country 2020 & 2033

- Table 16: Germany Hospital Biohazard Bags Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 17: United Kingdom Hospital Biohazard Bags Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 18: France Hospital Biohazard Bags Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 19: Italy Hospital Biohazard Bags Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Spain Hospital Biohazard Bags Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: Rest of Europe Hospital Biohazard Bags Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Global Hospital Biohazard Bags Industry Revenue million Forecast, by Product Material 2020 & 2033

- Table 23: Global Hospital Biohazard Bags Industry Revenue million Forecast, by Application 2020 & 2033

- Table 24: Global Hospital Biohazard Bags Industry Revenue million Forecast, by End User 2020 & 2033

- Table 25: Global Hospital Biohazard Bags Industry Revenue million Forecast, by Country 2020 & 2033

- Table 26: China Hospital Biohazard Bags Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Japan Hospital Biohazard Bags Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: India Hospital Biohazard Bags Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 29: Australia Hospital Biohazard Bags Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 30: South Korea Hospital Biohazard Bags Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 31: Rest of Asia Pacific Hospital Biohazard Bags Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Global Hospital Biohazard Bags Industry Revenue million Forecast, by Product Material 2020 & 2033

- Table 33: Global Hospital Biohazard Bags Industry Revenue million Forecast, by Application 2020 & 2033

- Table 34: Global Hospital Biohazard Bags Industry Revenue million Forecast, by End User 2020 & 2033

- Table 35: Global Hospital Biohazard Bags Industry Revenue million Forecast, by Country 2020 & 2033

- Table 36: GCC Hospital Biohazard Bags Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: South Africa Hospital Biohazard Bags Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 38: Rest of Middle East and Africa Hospital Biohazard Bags Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 39: Global Hospital Biohazard Bags Industry Revenue million Forecast, by Product Material 2020 & 2033

- Table 40: Global Hospital Biohazard Bags Industry Revenue million Forecast, by Application 2020 & 2033

- Table 41: Global Hospital Biohazard Bags Industry Revenue million Forecast, by End User 2020 & 2033

- Table 42: Global Hospital Biohazard Bags Industry Revenue million Forecast, by Country 2020 & 2033

- Table 43: Brazil Hospital Biohazard Bags Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: Argentina Hospital Biohazard Bags Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Rest of South America Hospital Biohazard Bags Industry Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Hospital Biohazard Bags Industry?

The projected CAGR is approximately 7.6%.

2. Which companies are prominent players in the Hospital Biohazard Bags Industry?

Key companies in the market include Transcendia Inc, Merck KGaA, Bionics Scientific Technologies Pvt Ltd, Harbour Group (SP Bel-Art), Desco Medical India*List Not Exhaustive, Welpack Industries Pvt Ltd, TUFPAK INC, International Plastics Inc, Champion Plastics, Inteplast Group Corporation (Minigrip LLC), Thermo Fisher Scientific.

3. What are the main segments of the Hospital Biohazard Bags Industry?

The market segments include Product Material, Application, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 541.28 million as of 2022.

5. What are some drivers contributing to market growth?

Increased Flow of Samples in Diagnostic Labs; Growing Number of Hospital Beds in Developing Countries.

6. What are the notable trends driving market growth?

Hospital Segment is Expected to Hold Significant Market Share Over the Forecast Period.

7. Are there any restraints impacting market growth?

Presence of Alternatives.

8. Can you provide examples of recent developments in the market?

April 2022: The West Bengal Bench of the Authority for Advance Ruling (AAR) announced in April 2022 that services offered to the State Government for collecting and disposing of bio-medical waste are exempt from GST.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Hospital Biohazard Bags Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Hospital Biohazard Bags Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Hospital Biohazard Bags Industry?

To stay informed about further developments, trends, and reports in the Hospital Biohazard Bags Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence