Key Insights

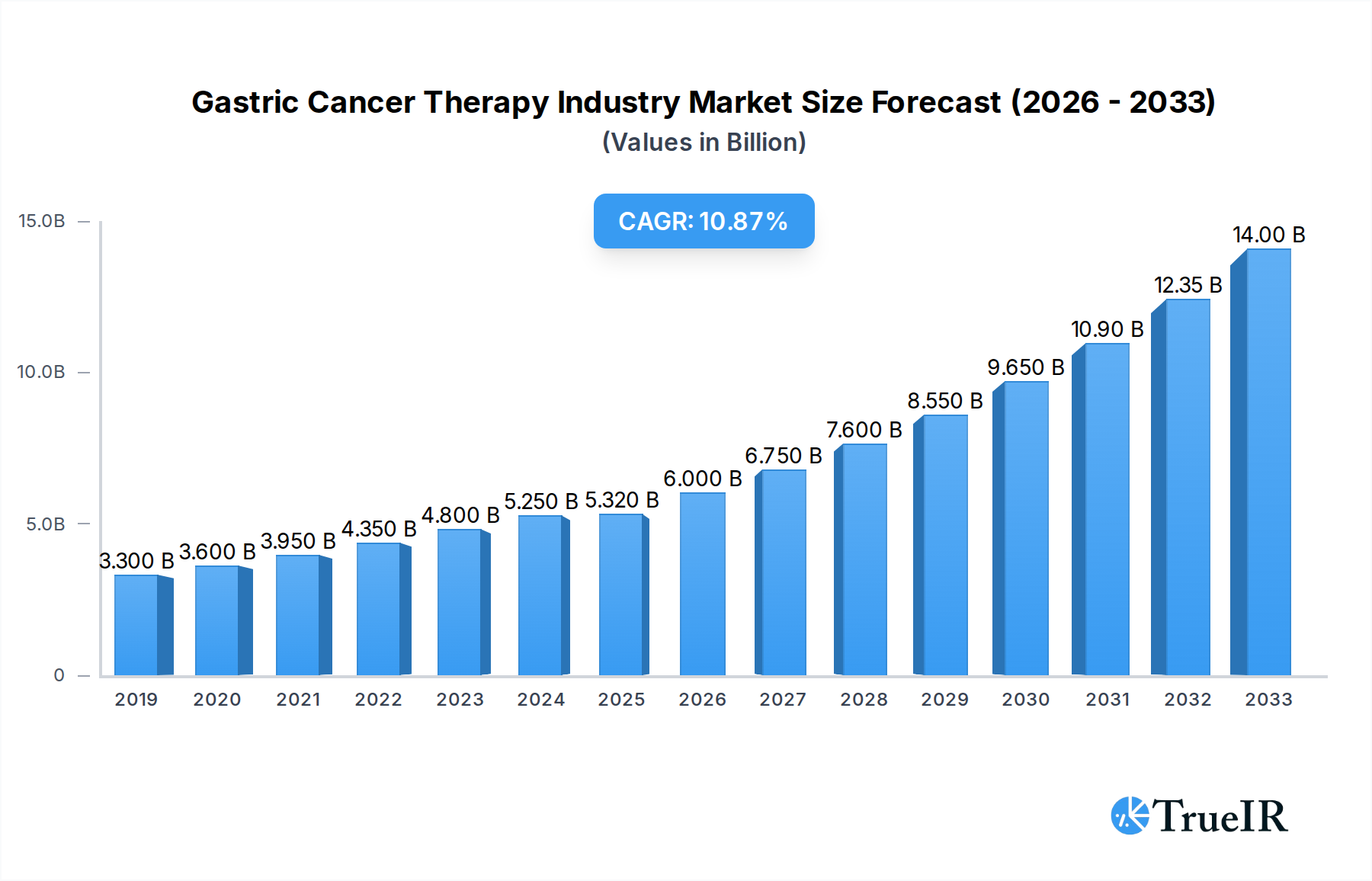

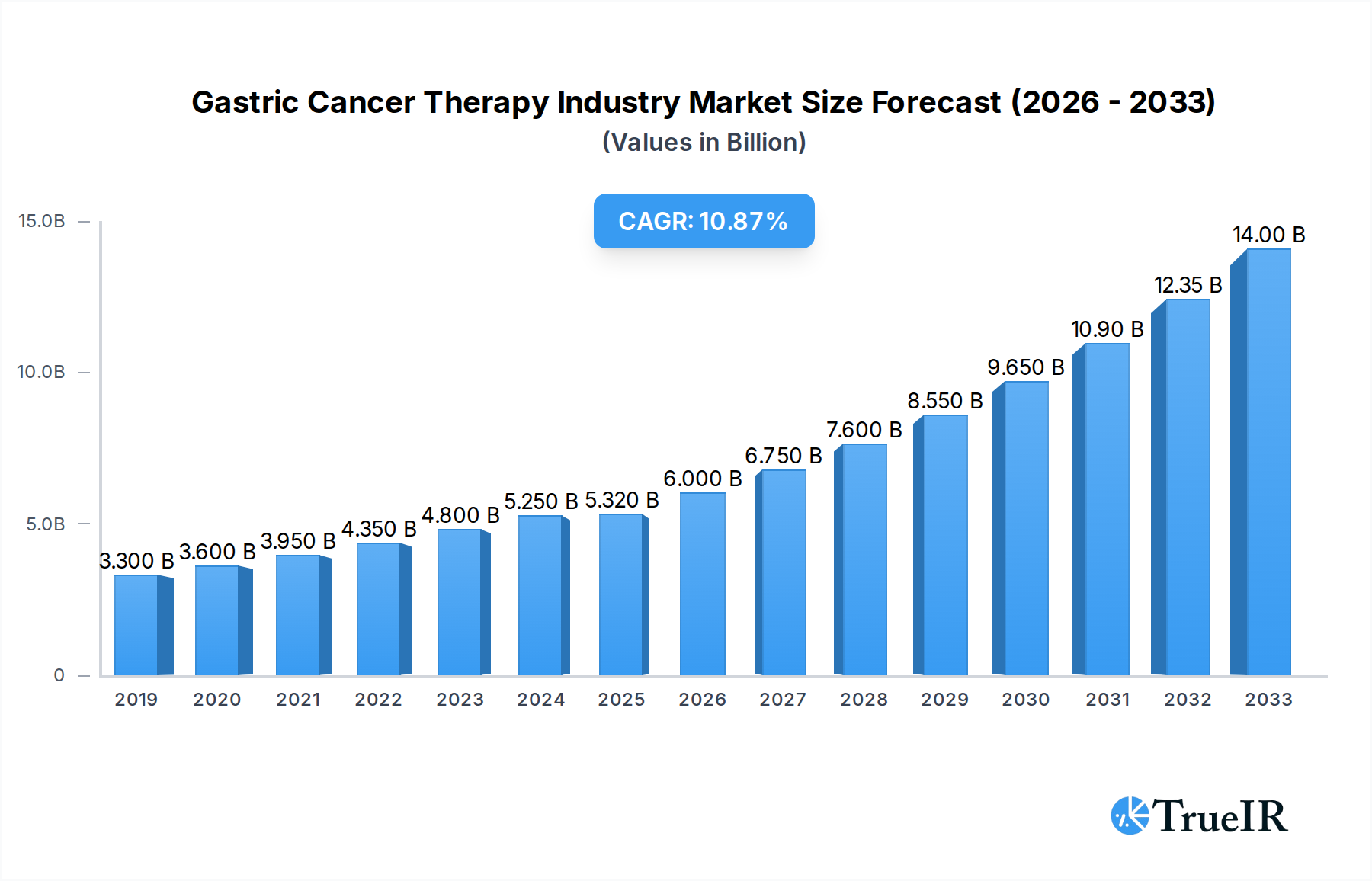

The global Gastric Cancer Therapy market is projected to experience significant expansion, reaching an estimated $5.32 million in 2025 and demonstrating a robust Compound Annual Growth Rate (CAGR) of 12.63% through 2033. This substantial growth is fueled by advancements in therapeutic approaches, including the increasing adoption of targeted therapies and immunotherapies, which offer more personalized and effective treatment options compared to traditional chemotherapy. The rising incidence of gastric cancer globally, coupled with a growing emphasis on early diagnosis and preventative measures, further contributes to market expansion. Furthermore, the development of novel drug combinations and a deeper understanding of the molecular mechanisms driving gastric cancer are paving the way for innovative treatment strategies. The market is also benefiting from improved healthcare infrastructure and increased R&D investments by leading pharmaceutical and biotechnology companies.

Gastric Cancer Therapy Industry Market Size (In Billion)

The market's trajectory is shaped by a dynamic interplay of drivers and restraints. Key drivers include the unmet medical needs in advanced gastric cancer treatment, the growing preference for minimally invasive surgical procedures performed in ambulatory surgery centers, and the expanding pipeline of novel drug candidates in clinical trials. Trends such as the integration of companion diagnostics to guide therapy selection and the increasing use of radiation therapy in multimodal treatment regimens are also propelling market growth. However, challenges such as the high cost of novel therapies, potential side effects, and the need for extensive clinical trials present restraining factors. Despite these challenges, the overall outlook for the Gastric Cancer Therapy market remains highly positive, with substantial opportunities for innovation and growth across various therapy types and end-user segments.

Gastric Cancer Therapy Industry Company Market Share

Global Gastric Cancer Therapy Industry: Market Insights, Forecasts, and Strategic Analysis (2019-2033)

This comprehensive report provides an in-depth analysis of the global gastric cancer therapy market, a critical and evolving sector within oncology. Leveraging extensive market data and high-volume keywords, this report is designed for industry stakeholders seeking to understand current dynamics, forecast future trends, and identify strategic growth opportunities. The study covers the historical period from 2019 to 2024, with a base year of 2025 and a forecast period extending to 2033. We delve into the intricate market structure, competitive landscape, emerging trends, dominant segments, product innovations, key drivers, barriers, challenges, and the strategic landscape shaped by leading players.

Gastric Cancer Therapy Industry Market Structure & Competitive Landscape

The gastric cancer therapy market exhibits a moderately concentrated structure, characterized by the presence of both established pharmaceutical giants and innovative biotechnology firms. Key innovation drivers include advancements in targeted therapies, immunotherapy development, and novel drug delivery systems. Regulatory impacts, while stringent, are crucial for ensuring patient safety and therapeutic efficacy, influencing R&D pipelines and market entry strategies. The threat of product substitutes is present but is often mitigated by the unique mechanisms of action of novel therapies. End-user segmentation primarily includes hospitals and specialty clinics, with ambulatory surgery centers playing an increasing role. Mergers and acquisitions (M&A) are significant, with an estimated 15-20 major M&A deals valued at over $500 million annually in the broader oncology therapeutics space, indicating a trend towards consolidation and portfolio expansion. The concentration ratio among the top 5 players is estimated to be around 45-55%.

Gastric Cancer Therapy Industry Market Trends & Opportunities

The global gastric cancer therapy market is poised for substantial growth, projected to reach an estimated value of over $15 billion by 2033, with a compound annual growth rate (CAGR) of approximately 7.5% during the forecast period (2025-2033). This expansion is fueled by a growing global incidence of gastric cancer, an aging population, and increasing healthcare expenditures worldwide. Technological shifts are revolutionizing treatment paradigms, with a notable rise in the adoption of targeted therapies and immunotherapies. These advanced treatments offer improved efficacy and reduced side effects compared to traditional chemotherapy, leading to enhanced patient outcomes and quality of life. Consumer preferences are increasingly leaning towards personalized medicine approaches, driving demand for diagnostic tools that can identify specific genetic mutations and biomarkers for tailored therapy selection. Competitive dynamics are intense, with companies investing heavily in R&D to develop next-generation therapies. The market penetration of advanced therapies is expected to rise from approximately 30% in the base year 2025 to over 55% by 2033. Early detection initiatives and increased awareness campaigns are also contributing to market expansion by identifying more cases at earlier, more treatable stages. The development of combination therapies, leveraging the synergistic effects of different treatment modalities, represents a significant growth opportunity. Furthermore, advancements in drug formulation and delivery mechanisms are improving therapeutic adherence and patient convenience. The increasing prevalence of Helicobacter pylori infection, a known risk factor for gastric cancer, also indirectly contributes to the long-term demand for effective treatments. Emerging markets, with their growing healthcare infrastructure and increasing access to advanced treatments, present significant untapped potential for market expansion. The ongoing research into novel biomarkers and predictive diagnostics will further refine treatment selection, leading to more efficient and effective therapeutic strategies.

Dominant Markets & Segments in Gastric Cancer Therapy Industry

The Hospitals and Specialty Clinics segment is the dominant end-user in the gastric cancer therapy industry, accounting for an estimated 70% of the market share in 2025. This dominance is attributed to the complexity of gastric cancer treatment, which often requires multidisciplinary care, advanced diagnostic capabilities, and intensive monitoring typically found in hospital settings. Key growth drivers in this segment include the continuous influx of novel therapies requiring specialized administration protocols and the presence of dedicated oncology departments and research centers.

Therapy Type Dominance:

- Immunotherapy: This segment is experiencing the most rapid growth, projected to capture over 25% of the market share by 2033. Its dominance is driven by significant clinical advancements, including the approval of checkpoint inhibitors and the development of novel immunotherapeutic agents.

- Growth Drivers: Breakthrough clinical trial results, expanding indications for approved drugs, and the potential for durable responses in a subset of patients.

- Targeted Therapy: This segment holds a substantial market share, estimated at around 30% in 2025, and is expected to grow steadily. It plays a crucial role in personalized medicine by targeting specific molecular pathways involved in cancer cell growth.

- Growth Drivers: Development of new molecularly targeted drugs, companion diagnostics for patient stratification, and increasing understanding of gastric cancer subtypes.

- Chemotherapy: While foundational, chemotherapy's market share is projected to decline gradually as newer, more effective therapies gain traction. However, it remains a critical component, often used in combination regimens.

- Growth Drivers: Continued use in first-line and adjuvant settings, development of novel chemotherapy agents with improved toxicity profiles.

- Surgery: Essential for early-stage gastric cancer and for palliation, surgery remains a cornerstone of treatment. Its market share is expected to remain stable, driven by advancements in minimally invasive surgical techniques.

- Growth Drivers: Laparoscopic and robotic surgery adoption, improved surgical outcomes and recovery times.

- Radiation Therapy: Primarily used in conjunction with other modalities, radiation therapy's market share is expected to be consistent, playing a supportive role in treatment plans.

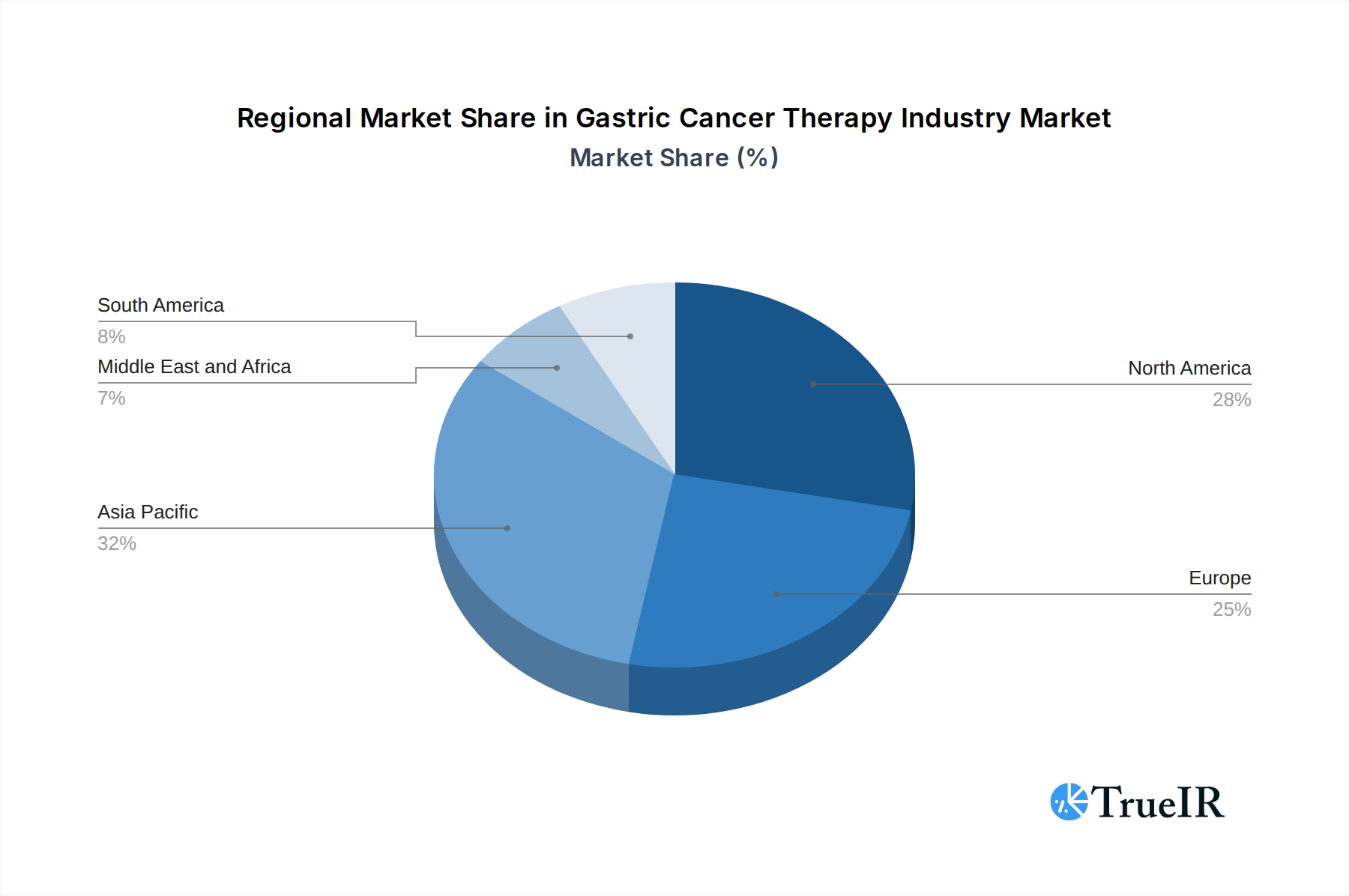

Regional Dominance:

- North America: This region is a leading market, driven by high healthcare spending, advanced research infrastructure, and early adoption of novel therapies.

- Growth Drivers: Robust clinical trial activity, strong reimbursement policies for innovative treatments, and a high prevalence of gastric cancer in specific demographics.

- Europe: A significant market with a well-established healthcare system and a focus on evidence-based medicine.

- Growth Drivers: Favorable regulatory pathways for drug approvals, active patient advocacy groups, and ongoing research initiatives.

- Asia Pacific: This region is expected to exhibit the highest growth rate due to increasing healthcare access, a rising burden of gastric cancer, and growing investments in pharmaceutical R&D and manufacturing.

- Growth Drivers: Expanding middle class, government initiatives to improve cancer care, and a large patient population.

Gastric Cancer Therapy Industry Product Analysis

Product innovation in gastric cancer therapy is characterized by the development of novel immunotherapy agents, including PD-1 inhibitors and dual-action antibodies, which have shown promising results in improving patient survival rates. Targeted therapies focusing on HER2-positive and other specific molecular aberrations are also gaining prominence, offering personalized treatment options with improved efficacy and reduced toxicity. The integration of these advanced therapies with traditional chemotherapy and surgery is creating synergistic treatment regimens, enhancing overall therapeutic outcomes.

Key Drivers, Barriers & Challenges in Gastric Cancer Therapy Industry

Key Drivers:

- Technological Advancements: Breakthroughs in immunotherapy and targeted therapy development are significantly expanding treatment options and improving patient prognoses.

- Increasing Gastric Cancer Incidence: A rising global prevalence, coupled with an aging population, is driving demand for effective therapies.

- Growing Healthcare Expenditure: Increased investment in healthcare infrastructure and treatment access, particularly in emerging economies, is a major growth catalyst.

Barriers & Challenges:

- High Cost of Novel Therapies: The exorbitant pricing of advanced treatments poses a significant barrier to access, especially in resource-limited regions.

- Regulatory Hurdles: Stringent regulatory approval processes for novel drugs can lead to lengthy development timelines and increased R&D costs.

- Complex Supply Chain Management: Ensuring the reliable and timely delivery of temperature-sensitive biological therapies globally presents logistical challenges.

- Resistance to Therapy: The development of drug resistance remains a significant challenge, necessitating ongoing research into combination therapies and alternative treatment strategies.

- Competitive Pressures: Intense competition among pharmaceutical companies drives innovation but also necessitates substantial investment in R&D and marketing.

Growth Drivers in the Gastric Cancer Therapy Industry Market

Key growth drivers in the gastric cancer therapy market are primarily propelled by significant technological advancements, most notably the rapid evolution and adoption of immunotherapies and targeted therapies. These innovations offer improved patient outcomes and are increasingly becoming the standard of care for various gastric cancer subtypes. Economically, rising global healthcare expenditures and expanding insurance coverage, particularly in emerging markets, are enhancing patient access to these advanced treatments. Policy-driven initiatives focused on early detection, cancer screening programs, and increased funding for oncology research further stimulate market growth by identifying more patients and fostering the development of innovative therapeutic solutions. The increasing global burden of gastric cancer due to factors like aging populations and lifestyle changes also underpins sustained demand for effective therapies.

Challenges Impacting Gastric Cancer Therapy Industry Growth

Regulatory complexities and stringent approval processes for novel oncology drugs remain a significant barrier, often leading to extended development timelines and substantial financial investments. Supply chain issues, particularly for biologics requiring specialized handling and cold chain logistics, pose challenges in ensuring consistent global availability of therapies. Intense competitive pressures among pharmaceutical giants and emerging biotechs necessitate continuous innovation and significant R&D spending, which can strain company resources. Furthermore, the high cost of advanced gastric cancer therapies limits accessibility for a significant portion of the global patient population, especially in low- and middle-income countries, thereby impacting market penetration and growth.

Key Players Shaping the Gastric Cancer Therapy Industry Market

- Celltrion Healthcare Co Ltd

- Astrazeneca

- Novartis AG

- Merck & Co Inc

- F Hoffmann-La Roche Ltd

- Amgen

- Eli Lilly and Company

- Otsuka Holdings Co Ltd

- GSK plc

- Imugene Limited

- Bristol-Myers Squibb Company

- Sanofi S A

- Pfizer Inc

Significant Gastric Cancer Therapy Industry Industry Milestones

- March 2023: Akeso, Inc. completed patient enrollment for its pivotal Phase III clinical trial involving cadonilimab (PD-1/CTLA-4 bi-specific antibody, AK104). This milestone brings the world's pioneering dual-immune checkpoint bi-specific antibody drug closer to market approval for a major indication, following its approval for cervical cancer treatment.

- January 2023: Eisai Co., Ltd. presented research on various gastrointestinal cancers at the 2023 American Society of Clinical Oncology (ASCO) gastrointestinal cancers symposium (#GI23) in San Francisco, California, highlighting ongoing advancements in GI cancer research and treatment.

Future Outlook for Gastric Cancer Therapy Industry Market

The future outlook for the gastric cancer therapy industry is exceptionally promising, driven by a confluence of innovation and increasing demand. Strategic opportunities lie in the further development and adoption of personalized medicine approaches, including advanced diagnostics and combination therapies. The growing emphasis on early detection and preventative measures will also contribute to a more robust market. The expansion of healthcare infrastructure and improved access to advanced treatments in emerging economies presents significant market potential, promising to broaden the reach of life-saving therapies and improve global gastric cancer survival rates.

Gastric Cancer Therapy Industry Segmentation

-

1. Therapy Type

- 1.1. Chemotherapy

- 1.2. Targeted Therapy

- 1.3. Immunotherapy

- 1.4. Radiation Therapy

- 1.5. Surgery

-

2. End-User

- 2.1. Ambulatory Surgery Centers

- 2.2. Hospitals and Specialty Clinics

- 2.3. Other End-users

Gastric Cancer Therapy Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Gastric Cancer Therapy Industry Regional Market Share

Geographic Coverage of Gastric Cancer Therapy Industry

Gastric Cancer Therapy Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.63% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Therapy Type

- 5.1.1. Chemotherapy

- 5.1.2. Targeted Therapy

- 5.1.3. Immunotherapy

- 5.1.4. Radiation Therapy

- 5.1.5. Surgery

- 5.2. Market Analysis, Insights and Forecast - by End-User

- 5.2.1. Ambulatory Surgery Centers

- 5.2.2. Hospitals and Specialty Clinics

- 5.2.3. Other End-users

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Middle East and Africa

- 5.3.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Therapy Type

- 6. Global Gastric Cancer Therapy Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Therapy Type

- 6.1.1. Chemotherapy

- 6.1.2. Targeted Therapy

- 6.1.3. Immunotherapy

- 6.1.4. Radiation Therapy

- 6.1.5. Surgery

- 6.2. Market Analysis, Insights and Forecast - by End-User

- 6.2.1. Ambulatory Surgery Centers

- 6.2.2. Hospitals and Specialty Clinics

- 6.2.3. Other End-users

- 6.1. Market Analysis, Insights and Forecast - by Therapy Type

- 7. North America Gastric Cancer Therapy Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Therapy Type

- 7.1.1. Chemotherapy

- 7.1.2. Targeted Therapy

- 7.1.3. Immunotherapy

- 7.1.4. Radiation Therapy

- 7.1.5. Surgery

- 7.2. Market Analysis, Insights and Forecast - by End-User

- 7.2.1. Ambulatory Surgery Centers

- 7.2.2. Hospitals and Specialty Clinics

- 7.2.3. Other End-users

- 7.1. Market Analysis, Insights and Forecast - by Therapy Type

- 8. Europe Gastric Cancer Therapy Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Therapy Type

- 8.1.1. Chemotherapy

- 8.1.2. Targeted Therapy

- 8.1.3. Immunotherapy

- 8.1.4. Radiation Therapy

- 8.1.5. Surgery

- 8.2. Market Analysis, Insights and Forecast - by End-User

- 8.2.1. Ambulatory Surgery Centers

- 8.2.2. Hospitals and Specialty Clinics

- 8.2.3. Other End-users

- 8.1. Market Analysis, Insights and Forecast - by Therapy Type

- 9. Asia Pacific Gastric Cancer Therapy Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Therapy Type

- 9.1.1. Chemotherapy

- 9.1.2. Targeted Therapy

- 9.1.3. Immunotherapy

- 9.1.4. Radiation Therapy

- 9.1.5. Surgery

- 9.2. Market Analysis, Insights and Forecast - by End-User

- 9.2.1. Ambulatory Surgery Centers

- 9.2.2. Hospitals and Specialty Clinics

- 9.2.3. Other End-users

- 9.1. Market Analysis, Insights and Forecast - by Therapy Type

- 10. Middle East and Africa Gastric Cancer Therapy Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Therapy Type

- 10.1.1. Chemotherapy

- 10.1.2. Targeted Therapy

- 10.1.3. Immunotherapy

- 10.1.4. Radiation Therapy

- 10.1.5. Surgery

- 10.2. Market Analysis, Insights and Forecast - by End-User

- 10.2.1. Ambulatory Surgery Centers

- 10.2.2. Hospitals and Specialty Clinics

- 10.2.3. Other End-users

- 10.1. Market Analysis, Insights and Forecast - by Therapy Type

- 11. South America Gastric Cancer Therapy Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Therapy Type

- 11.1.1. Chemotherapy

- 11.1.2. Targeted Therapy

- 11.1.3. Immunotherapy

- 11.1.4. Radiation Therapy

- 11.1.5. Surgery

- 11.2. Market Analysis, Insights and Forecast - by End-User

- 11.2.1. Ambulatory Surgery Centers

- 11.2.2. Hospitals and Specialty Clinics

- 11.2.3. Other End-users

- 11.1. Market Analysis, Insights and Forecast - by Therapy Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Celltrion Healthcare Co Ltd

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Astrazeneca

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Novartis AG

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Merck & Co Inc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 F Hoffmann-La Roche Ltd

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Amgen*List Not Exhaustive

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Eli Lilly and Company

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Otsuka Holdings Co Ltd

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 GSK plc

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Imugene Limited

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Bristol-Myers Squibb Company

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Sanofi S A

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Pfizer Inc

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.1 Celltrion Healthcare Co Ltd

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Gastric Cancer Therapy Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Gastric Cancer Therapy Industry Revenue (Million), by Therapy Type 2025 & 2033

- Figure 3: North America Gastric Cancer Therapy Industry Revenue Share (%), by Therapy Type 2025 & 2033

- Figure 4: North America Gastric Cancer Therapy Industry Revenue (Million), by End-User 2025 & 2033

- Figure 5: North America Gastric Cancer Therapy Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 6: North America Gastric Cancer Therapy Industry Revenue (Million), by Country 2025 & 2033

- Figure 7: North America Gastric Cancer Therapy Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Gastric Cancer Therapy Industry Revenue (Million), by Therapy Type 2025 & 2033

- Figure 9: Europe Gastric Cancer Therapy Industry Revenue Share (%), by Therapy Type 2025 & 2033

- Figure 10: Europe Gastric Cancer Therapy Industry Revenue (Million), by End-User 2025 & 2033

- Figure 11: Europe Gastric Cancer Therapy Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 12: Europe Gastric Cancer Therapy Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Europe Gastric Cancer Therapy Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Gastric Cancer Therapy Industry Revenue (Million), by Therapy Type 2025 & 2033

- Figure 15: Asia Pacific Gastric Cancer Therapy Industry Revenue Share (%), by Therapy Type 2025 & 2033

- Figure 16: Asia Pacific Gastric Cancer Therapy Industry Revenue (Million), by End-User 2025 & 2033

- Figure 17: Asia Pacific Gastric Cancer Therapy Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 18: Asia Pacific Gastric Cancer Therapy Industry Revenue (Million), by Country 2025 & 2033

- Figure 19: Asia Pacific Gastric Cancer Therapy Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East and Africa Gastric Cancer Therapy Industry Revenue (Million), by Therapy Type 2025 & 2033

- Figure 21: Middle East and Africa Gastric Cancer Therapy Industry Revenue Share (%), by Therapy Type 2025 & 2033

- Figure 22: Middle East and Africa Gastric Cancer Therapy Industry Revenue (Million), by End-User 2025 & 2033

- Figure 23: Middle East and Africa Gastric Cancer Therapy Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 24: Middle East and Africa Gastric Cancer Therapy Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Middle East and Africa Gastric Cancer Therapy Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Gastric Cancer Therapy Industry Revenue (Million), by Therapy Type 2025 & 2033

- Figure 27: South America Gastric Cancer Therapy Industry Revenue Share (%), by Therapy Type 2025 & 2033

- Figure 28: South America Gastric Cancer Therapy Industry Revenue (Million), by End-User 2025 & 2033

- Figure 29: South America Gastric Cancer Therapy Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 30: South America Gastric Cancer Therapy Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: South America Gastric Cancer Therapy Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Gastric Cancer Therapy Industry Revenue Million Forecast, by Therapy Type 2020 & 2033

- Table 2: Global Gastric Cancer Therapy Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 3: Global Gastric Cancer Therapy Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Gastric Cancer Therapy Industry Revenue Million Forecast, by Therapy Type 2020 & 2033

- Table 5: Global Gastric Cancer Therapy Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 6: Global Gastric Cancer Therapy Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: United States Gastric Cancer Therapy Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Canada Gastric Cancer Therapy Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Gastric Cancer Therapy Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Global Gastric Cancer Therapy Industry Revenue Million Forecast, by Therapy Type 2020 & 2033

- Table 11: Global Gastric Cancer Therapy Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 12: Global Gastric Cancer Therapy Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Germany Gastric Cancer Therapy Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: United Kingdom Gastric Cancer Therapy Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: France Gastric Cancer Therapy Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Italy Gastric Cancer Therapy Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Spain Gastric Cancer Therapy Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Rest of Europe Gastric Cancer Therapy Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Global Gastric Cancer Therapy Industry Revenue Million Forecast, by Therapy Type 2020 & 2033

- Table 20: Global Gastric Cancer Therapy Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 21: Global Gastric Cancer Therapy Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 22: China Gastric Cancer Therapy Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: Japan Gastric Cancer Therapy Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: India Gastric Cancer Therapy Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 25: Australia Gastric Cancer Therapy Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: South Korea Gastric Cancer Therapy Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Asia Pacific Gastric Cancer Therapy Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Global Gastric Cancer Therapy Industry Revenue Million Forecast, by Therapy Type 2020 & 2033

- Table 29: Global Gastric Cancer Therapy Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 30: Global Gastric Cancer Therapy Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 31: GCC Gastric Cancer Therapy Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: South Africa Gastric Cancer Therapy Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 33: Rest of Middle East and Africa Gastric Cancer Therapy Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Global Gastric Cancer Therapy Industry Revenue Million Forecast, by Therapy Type 2020 & 2033

- Table 35: Global Gastric Cancer Therapy Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 36: Global Gastric Cancer Therapy Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 37: Brazil Gastric Cancer Therapy Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: Argentina Gastric Cancer Therapy Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 39: Rest of South America Gastric Cancer Therapy Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Gastric Cancer Therapy Industry?

The projected CAGR is approximately 12.63%.

2. Which companies are prominent players in the Gastric Cancer Therapy Industry?

Key companies in the market include Celltrion Healthcare Co Ltd, Astrazeneca, Novartis AG, Merck & Co Inc, F Hoffmann-La Roche Ltd, Amgen*List Not Exhaustive, Eli Lilly and Company, Otsuka Holdings Co Ltd, GSK plc, Imugene Limited, Bristol-Myers Squibb Company, Sanofi S A, Pfizer Inc.

3. What are the main segments of the Gastric Cancer Therapy Industry?

The market segments include Therapy Type, End-User.

4. Can you provide details about the market size?

The market size is estimated to be USD 5.32 Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Burden of Gastric Cancer; Increase in Research and Development for Novel Therapies Coupled with Government Initiatives.

6. What are the notable trends driving market growth?

Targeted Segment is Expected to Hold a Significant Share of the Market Over the Forecast Period.

7. Are there any restraints impacting market growth?

High Cost of Cancer Therapy and Side Effects of Cancer Drugs.

8. Can you provide examples of recent developments in the market?

March 2023: Akeso, Inc., completed the patient enrollment for its pivotal Phase III clinical trial involving cadonilimab (PD-1/CTLA-4 bi-specific antibody, AK104), which stands as the world's pioneering dual-immune checkpoint bi-specific antibody drug to be approved and brought to market. This marks a step closer to the launch of cadonilimab for a major indication after the indication for treatment of cervical cancer has been approved.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Gastric Cancer Therapy Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Gastric Cancer Therapy Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Gastric Cancer Therapy Industry?

To stay informed about further developments, trends, and reports in the Gastric Cancer Therapy Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence