Key Insights

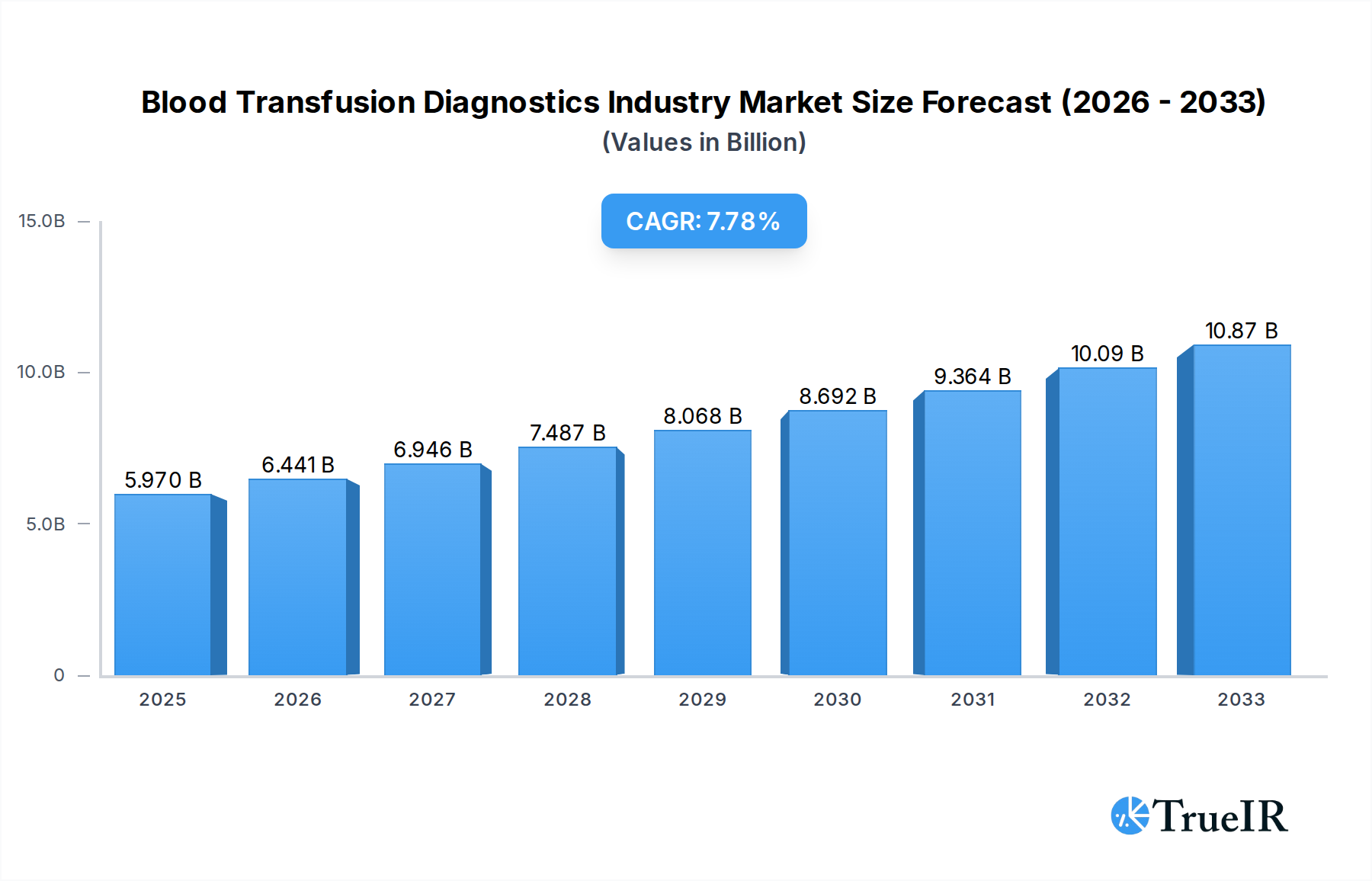

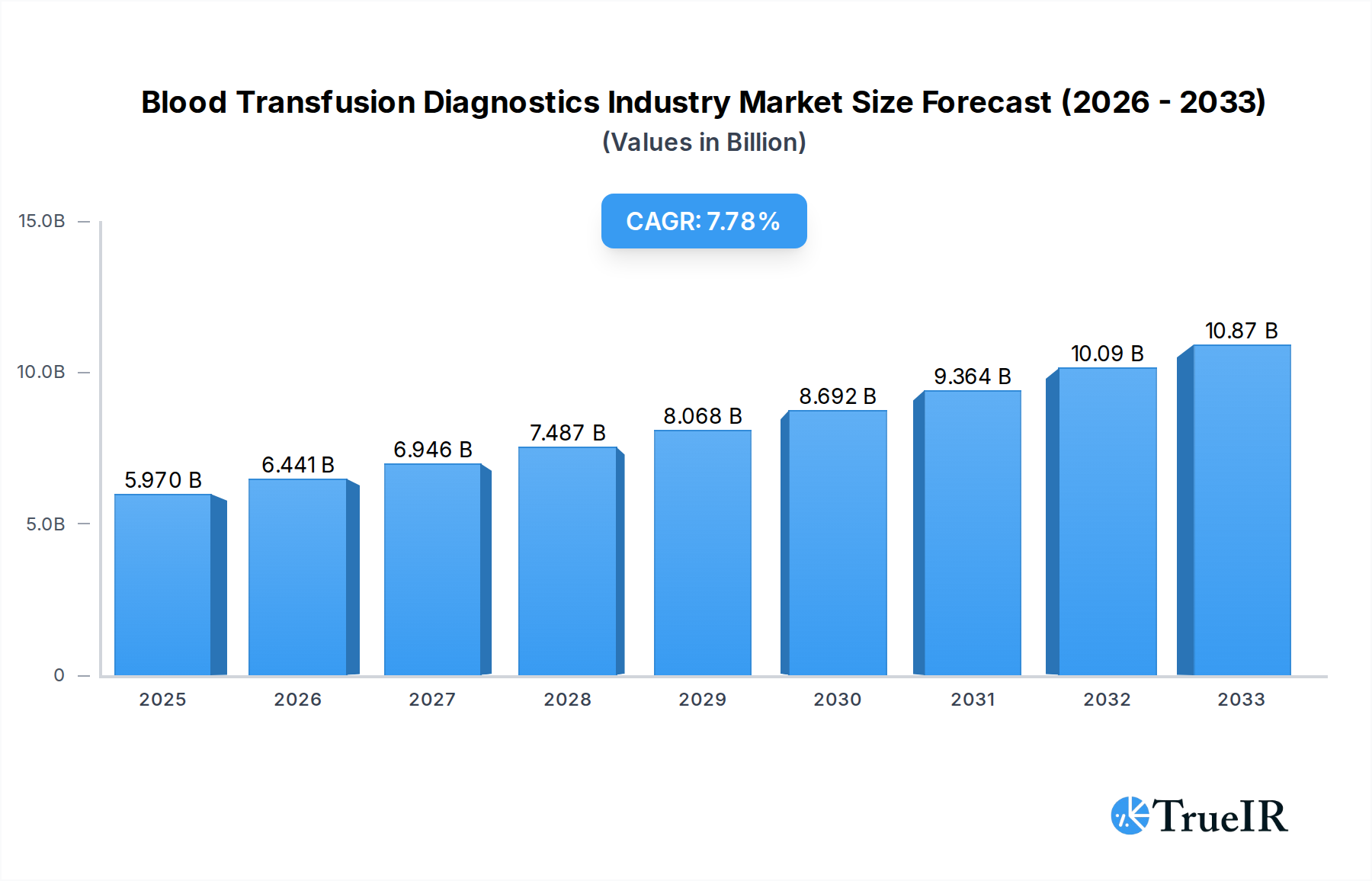

The global Blood Transfusion Diagnostics market is poised for robust expansion, projected to reach $5.97 billion in 2025 and is expected to grow at a Compound Annual Growth Rate (CAGR) of 7.89% through 2033. This significant growth is propelled by an increasing demand for safe and effective blood transfusions, driven by rising incidences of chronic diseases, surgical procedures, and organ transplantation across the globe. Advancements in diagnostic technologies, leading to improved accuracy and efficiency in detecting bloodborne pathogens and ensuring blood compatibility, are key market enablers. The increasing prevalence of infectious diseases and the growing awareness regarding transfusion-transmitted infections further underscore the critical role of sophisticated diagnostic solutions. Furthermore, government initiatives promoting blood donation and transfusion safety are contributing to market dynamics.

Blood Transfusion Diagnostics Industry Market Size (In Billion)

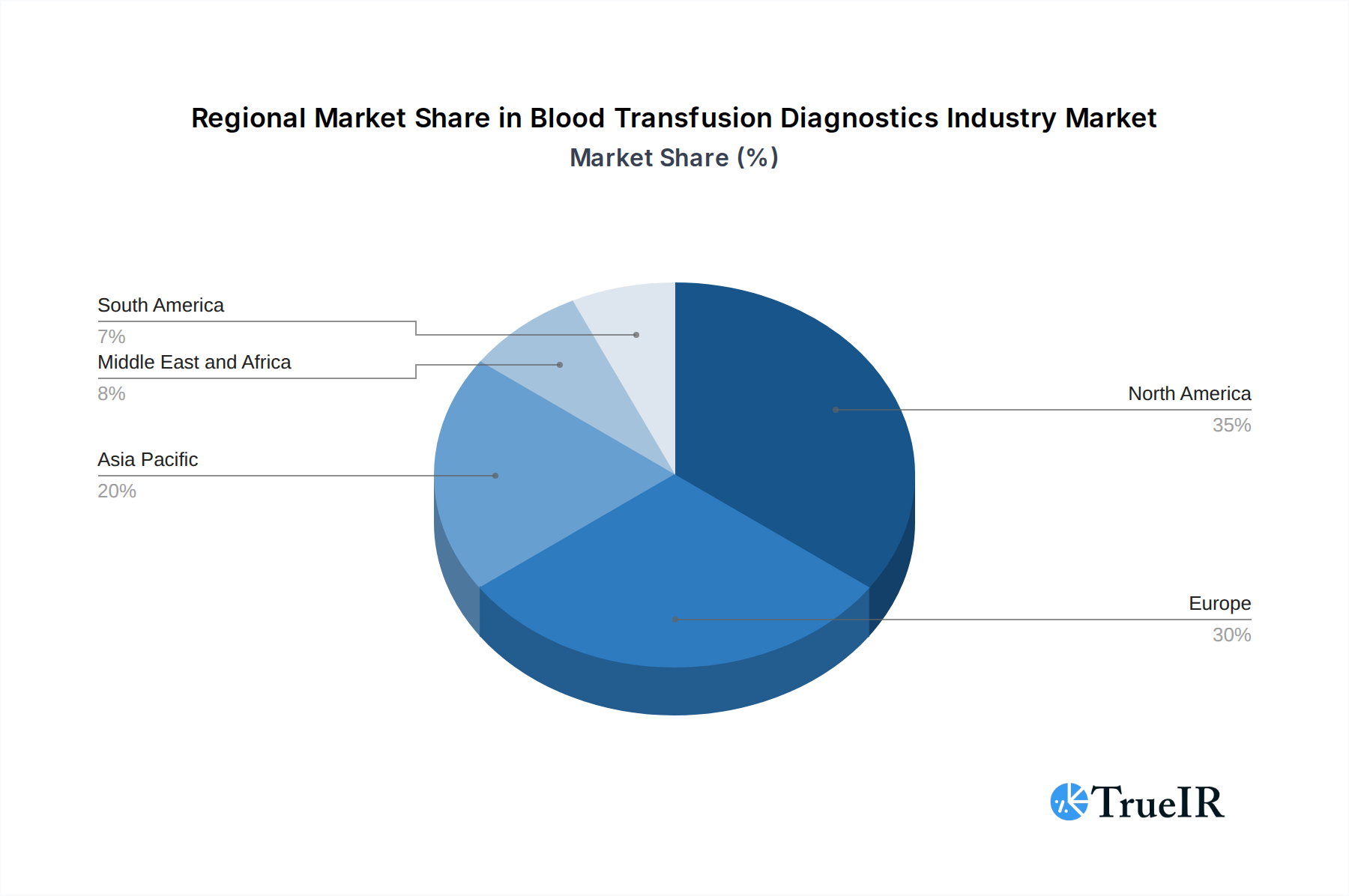

The market is segmented into Instruments and Consumables, catering to vital applications such as Blood Screening and Blood Group Typing. Hospitals, Diagnostics Laboratories, and Blood Banks represent the primary end-user segments, all prioritizing patient safety and accurate diagnostics. Geographically, North America and Europe currently dominate the market due to well-established healthcare infrastructures and high adoption rates of advanced diagnostic technologies. However, the Asia Pacific region is anticipated to witness the fastest growth, fueled by a burgeoning patient population, expanding healthcare expenditure, and increasing investments in diagnostic facilities. Key players like Abbott, Roche Diagnostics, and Bio-Rad Laboratories are instrumental in driving innovation and catering to the evolving needs of the blood transfusion diagnostics landscape.

Blood Transfusion Diagnostics Industry Company Market Share

Unlocking Critical Insights: The Blood Transfusion Diagnostics Industry Market Report (2019–2033)

This comprehensive report delves into the dynamic Blood Transfusion Diagnostics Industry, a sector vital for ensuring patient safety and optimizing healthcare outcomes. With a study period spanning from 2019 to 2033, including a base year of 2025 and a forecast period from 2025 to 2033, this analysis provides unparalleled depth into market dynamics, competitive strategies, and future trajectory. Leveraging high-volume SEO keywords such as "blood transfusion diagnostics market," "blood screening solutions," "blood group typing technology," and "in vitro diagnostics industry," this report is engineered to enhance search rankings and engage a broad spectrum of industry stakeholders, including healthcare professionals, diagnostic laboratories, blood banks, investors, and market research professionals.

The global Blood Transfusion Diagnostics Industry is projected to reach hundreds of billions by 2025, exhibiting robust growth driven by an increasing demand for safe blood transfusions, technological advancements in diagnostic tools, and a growing awareness of transfusion-transmitted infections. This report offers an in-depth analysis of market size, segmentation, regional landscapes, and the competitive forces that are shaping this critical healthcare segment.

Blood Transfusion Diagnostics Industry Market Structure & Competitive Landscape

The Blood Transfusion Diagnostics Industry is characterized by a moderately concentrated market structure, with a few dominant players holding significant market share. Key innovation drivers include the continuous pursuit of enhanced sensitivity and specificity in diagnostic assays, the development of automated and integrated platforms, and the adoption of molecular diagnostic techniques. Regulatory impacts, driven by stringent quality control standards and guidelines from bodies like the FDA and EMA, play a crucial role in shaping product development and market access. The threat of product substitutes, while present in adjacent diagnostic areas, is relatively low within core transfusion diagnostics due to specialized requirements. End-user segmentation reveals a strong reliance on hospitals and diagnostics laboratories, with blood banks also being a significant consumer segment. Merger and acquisition (M&A) trends are indicative of consolidation and strategic expansion, with an estimated tens of billions in M&A volume observed in the historical period (2019-2024). The concentration ratio among the top five players is estimated to be around XX%, highlighting the competitive intensity.

- Market Concentration: Moderately concentrated, with leading companies dominating market share.

- Innovation Drivers:

- Increased sensitivity and specificity of diagnostic tests.

- Automation and integration of diagnostic workflows.

- Adoption of molecular diagnostics.

- Point-of-care testing solutions.

- Regulatory Impacts: Strict adherence to global regulatory standards (FDA, EMA, etc.) for product approval and market entry.

- Product Substitutes: Limited within core transfusion diagnostics.

- End-User Segmentation: Hospitals, Diagnostics Laboratories, Blood Banks are key consumers.

- M&A Trends: Strategic consolidations and acquisitions to expand product portfolios and market reach.

Blood Transfusion Diagnostics Industry Market Trends & Opportunities

The Blood Transfusion Diagnostics Industry is poised for significant expansion, with the market size projected to grow from hundreds of billions in 2025 to well over trillions by 2033. This growth is fueled by a confluence of technological advancements, evolving consumer preferences towards safer and more efficient healthcare solutions, and persistent competitive dynamics that drive innovation. The Compound Annual Growth Rate (CAGR) is estimated to be robust, likely in the high single digits, as diagnostic accuracy and speed become paramount. Technological shifts are moving towards more sophisticated molecular and immunoassay-based techniques, enhancing the detection of infectious agents and optimizing pre-transfusion compatibility testing.

Consumer preferences are increasingly dictating a demand for faster turnaround times, reduced invasiveness, and greater accuracy, pushing the development of automated systems and multiplex assays. The competitive landscape is marked by intense R&D efforts, strategic partnerships, and a focus on expanding geographical reach. Opportunities abound in emerging economies, where the establishment of robust blood transfusion infrastructure is a priority, and in the development of novel diagnostic solutions for rare blood types and emerging infectious diseases. The market penetration rate of advanced diagnostic technologies, while already substantial, is expected to climb as cost-effectiveness improves and accessibility increases. Furthermore, the growing emphasis on personalized medicine and pharmacogenomics is opening new avenues for customized transfusion strategies, requiring advanced diagnostic capabilities. The increasing prevalence of chronic diseases and an aging global population also contribute to a sustained demand for blood transfusions, thereby underpinning the growth of the diagnostics sector.

Dominant Markets & Segments in Blood Transfusion Diagnostics Industry

The Blood Transfusion Diagnostics Industry is dominated by the Instruments segment in terms of market value, owing to the high cost and technological sophistication of automated analyzers and platforms used in diagnostic workflows. This dominance is further amplified by the sustained demand for capital expenditure in healthcare facilities. Within the Application category, Blood Screening commands a significant market share due to the continuous need to detect infectious diseases and ensure the safety of donated blood. The End-User segment is led by Hospitals and Diagnostics Laboratories, which represent the largest consumer base for transfusion diagnostic products and services.

Dominant Segment (Type): Instruments

- Growth Drivers: Technological advancements in automation, high throughput capabilities, and integrated analytical platforms.

- Detailed Analysis: The purchase of sophisticated laboratory instruments for blood screening and typing constitutes a major portion of market expenditure. These instruments offer efficiency, accuracy, and reduced labor costs, making them indispensable for modern healthcare facilities.

Dominant Segment (Application): Blood Screening

- Growth Drivers: Increasing prevalence of infectious diseases (e.g., HIV, Hepatitis B, Hepatitis C), stringent regulatory requirements for blood safety, and the need for early detection.

- Detailed Analysis: Comprehensive blood screening is a critical step in the transfusion process, aiming to identify known and emerging pathogens in donated blood. This segment is driven by both public health mandates and the proactive measures taken by blood banks and healthcare providers to minimize transfusion-transmitted infections.

Dominant Segment (End-User): Hospitals & Diagnostics Laboratories

- Growth Drivers: High volume of blood transfusions, presence of specialized transfusion medicine departments, and the central role of these facilities in patient care and disease diagnosis.

- Detailed Analysis: Hospitals, with their inpatient care and surgical services, are major consumers of blood products and consequently, their diagnostic tools. Similarly, dedicated diagnostic laboratories, both independent and hospital-affiliated, perform a substantial volume of blood tests, including those for transfusion compatibility and screening.

Blood Transfusion Diagnostics Industry Product Analysis

Product innovations in the Blood Transfusion Diagnostics Industry are primarily focused on enhancing the speed, accuracy, and comprehensiveness of diagnostic assays. Automated immunoassay and molecular diagnostic platforms are gaining traction, offering significant improvements in detecting a wider range of pathogens and antibodies. Competitive advantages are derived from superior assay sensitivity, rapid turnaround times, user-friendly interfaces, and robust data management capabilities. The market fit for these products is driven by the critical need for safe and effective blood transfusions, reducing the risk of transfusion-transmitted infections and improving patient outcomes.

Key Drivers, Barriers & Challenges in Blood Transfusion Diagnostics Industry

The Blood Transfusion Diagnostics Industry is propelled by several key drivers, including advancements in molecular diagnostics, increasing global demand for blood transfusions, and stringent government regulations mandating blood safety. Technological innovation in areas like multiplex assays and automation also significantly fuels market growth.

- Key Drivers:

- Technological advancements in molecular and immunoassay diagnostics.

- Growing demand for blood transfusions due to aging populations and chronic diseases.

- Stringent regulatory mandates for blood safety.

- Increased awareness of transfusion-transmitted infections.

However, the industry faces significant barriers and challenges. High development costs for new diagnostic technologies, complex regulatory approval processes, and the need for skilled personnel to operate advanced equipment are major restraints. Supply chain disruptions, particularly for specialized reagents and components, can also impact production and delivery.

- Key Barriers & Challenges:

- High R&D investment and long product development cycles.

- Stringent and evolving regulatory landscapes across different regions.

- Need for skilled workforce and specialized training.

- Supply chain vulnerabilities and logistical complexities.

- Pricing pressures and reimbursement challenges.

Growth Drivers in the Blood Transfusion Diagnostics Industry Market

Growth in the Blood Transfusion Diagnostics Industry is primarily driven by relentless technological innovation, particularly in molecular diagnostics and automation, which allows for more precise and rapid detection of bloodborne pathogens and compatibility issues. The increasing global demand for blood transfusions, fueled by aging demographics and a rising prevalence of chronic diseases requiring transfusions, directly translates into higher demand for diagnostic solutions. Furthermore, stringent government regulations and public health initiatives focused on ensuring blood safety worldwide act as powerful catalysts for market expansion, compelling healthcare providers to adopt advanced diagnostic technologies.

Challenges Impacting Blood Transfusion Diagnostics Industry Growth

Despite strong growth prospects, the Blood Transfusion Diagnostics Industry grapples with several challenges. Navigating complex and evolving regulatory frameworks across different geographical markets poses a significant hurdle, often leading to extended product approval timelines and increased compliance costs. Supply chain vulnerabilities, including the availability of raw materials and the efficient distribution of reagents and instruments, present ongoing concerns, especially in the face of global economic uncertainties. Moreover, intense competitive pressures from established players and emerging innovators necessitate continuous investment in R&D, while pricing pressures from healthcare payers can limit profit margins, impacting overall industry growth.

Key Players Shaping the Blood Transfusion Diagnostics Industry Market

- Werfen

- Bio-Rad Laboratories Inc

- QUOTIENT

- Merck KGaA

- F Hoffmann-La Roche Ltd

- Diasorin S p A

- Abbott

- Grifols S A

- Immucor Inc

- Danaher

Significant Blood Transfusion Diagnostics Industry Industry Milestones

- 2019: Introduction of advanced next-generation sequencing (NGS) based blood group genotyping systems, improving rare blood type identification.

- 2020: Increased focus on rapid molecular assays for screening emerging viral pathogens impacting blood safety globally.

- 2021: Development and adoption of AI-powered diagnostic tools to enhance data analysis and workflow efficiency in transfusion medicine.

- 2022: Strategic acquisitions and partnerships aimed at expanding product portfolios and market reach in emerging economies.

- 2023: Regulatory approvals for novel multiplex assays capable of detecting multiple transfusion-transmissible infections simultaneously, enhancing screening efficiency.

- 2024: Significant investments in point-of-care diagnostic solutions to improve turnaround times in remote or emergency settings.

Future Outlook for Blood Transfusion Diagnostics Industry Market

The future outlook for the Blood Transfusion Diagnostics Industry remains exceptionally bright, with projected continued growth driven by unmet needs in blood safety and diagnostic accuracy. Strategic opportunities lie in the development of more advanced molecular diagnostic platforms, personalized transfusion strategies, and integrated diagnostic solutions that streamline laboratory workflows. The increasing adoption of automation and artificial intelligence in diagnostics will further enhance efficiency and reduce errors. Emerging markets, with their expanding healthcare infrastructure and growing emphasis on public health, represent significant untapped potential for market expansion. The industry is poised to play an even more critical role in safeguarding global health by ensuring the safety and efficacy of blood transfusions.

Blood Transfusion Diagnostics Industry Segmentation

-

1. Type

- 1.1. Instruments

- 1.2. Consumables

-

2. Application

- 2.1. Blood Screening

- 2.2. Blood Group Typing

-

3. End-User

- 3.1. Hospitals

- 3.2. Diagnostics Laboratories

- 3.3. Blood Banks

Blood Transfusion Diagnostics Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Blood Transfusion Diagnostics Industry Regional Market Share

Geographic Coverage of Blood Transfusion Diagnostics Industry

Blood Transfusion Diagnostics Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.89% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Instruments

- 5.1.2. Consumables

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Blood Screening

- 5.2.2. Blood Group Typing

- 5.3. Market Analysis, Insights and Forecast - by End-User

- 5.3.1. Hospitals

- 5.3.2. Diagnostics Laboratories

- 5.3.3. Blood Banks

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Middle East and Africa

- 5.4.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Blood Transfusion Diagnostics Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Instruments

- 6.1.2. Consumables

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Blood Screening

- 6.2.2. Blood Group Typing

- 6.3. Market Analysis, Insights and Forecast - by End-User

- 6.3.1. Hospitals

- 6.3.2. Diagnostics Laboratories

- 6.3.3. Blood Banks

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America Blood Transfusion Diagnostics Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Instruments

- 7.1.2. Consumables

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Blood Screening

- 7.2.2. Blood Group Typing

- 7.3. Market Analysis, Insights and Forecast - by End-User

- 7.3.1. Hospitals

- 7.3.2. Diagnostics Laboratories

- 7.3.3. Blood Banks

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe Blood Transfusion Diagnostics Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Instruments

- 8.1.2. Consumables

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Blood Screening

- 8.2.2. Blood Group Typing

- 8.3. Market Analysis, Insights and Forecast - by End-User

- 8.3.1. Hospitals

- 8.3.2. Diagnostics Laboratories

- 8.3.3. Blood Banks

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Asia Pacific Blood Transfusion Diagnostics Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Instruments

- 9.1.2. Consumables

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Blood Screening

- 9.2.2. Blood Group Typing

- 9.3. Market Analysis, Insights and Forecast - by End-User

- 9.3.1. Hospitals

- 9.3.2. Diagnostics Laboratories

- 9.3.3. Blood Banks

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Middle East and Africa Blood Transfusion Diagnostics Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Instruments

- 10.1.2. Consumables

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Blood Screening

- 10.2.2. Blood Group Typing

- 10.3. Market Analysis, Insights and Forecast - by End-User

- 10.3.1. Hospitals

- 10.3.2. Diagnostics Laboratories

- 10.3.3. Blood Banks

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. South America Blood Transfusion Diagnostics Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Instruments

- 11.1.2. Consumables

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Blood Screening

- 11.2.2. Blood Group Typing

- 11.3. Market Analysis, Insights and Forecast - by End-User

- 11.3.1. Hospitals

- 11.3.2. Diagnostics Laboratories

- 11.3.3. Blood Banks

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Werfen*List Not Exhaustive

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Bio-Rad Laboratories Inc

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 QUOTIENT

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Merck KGaA

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 F Hoffmann-La Roche Ltd

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Diasorin S p A

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Abbott

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Grifols S A

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Immucor Inc

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Danaher

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Werfen*List Not Exhaustive

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Blood Transfusion Diagnostics Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Blood Transfusion Diagnostics Industry Revenue (billion), by Type 2025 & 2033

- Figure 3: North America Blood Transfusion Diagnostics Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America Blood Transfusion Diagnostics Industry Revenue (billion), by Application 2025 & 2033

- Figure 5: North America Blood Transfusion Diagnostics Industry Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Blood Transfusion Diagnostics Industry Revenue (billion), by End-User 2025 & 2033

- Figure 7: North America Blood Transfusion Diagnostics Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 8: North America Blood Transfusion Diagnostics Industry Revenue (billion), by Country 2025 & 2033

- Figure 9: North America Blood Transfusion Diagnostics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Blood Transfusion Diagnostics Industry Revenue (billion), by Type 2025 & 2033

- Figure 11: Europe Blood Transfusion Diagnostics Industry Revenue Share (%), by Type 2025 & 2033

- Figure 12: Europe Blood Transfusion Diagnostics Industry Revenue (billion), by Application 2025 & 2033

- Figure 13: Europe Blood Transfusion Diagnostics Industry Revenue Share (%), by Application 2025 & 2033

- Figure 14: Europe Blood Transfusion Diagnostics Industry Revenue (billion), by End-User 2025 & 2033

- Figure 15: Europe Blood Transfusion Diagnostics Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 16: Europe Blood Transfusion Diagnostics Industry Revenue (billion), by Country 2025 & 2033

- Figure 17: Europe Blood Transfusion Diagnostics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Blood Transfusion Diagnostics Industry Revenue (billion), by Type 2025 & 2033

- Figure 19: Asia Pacific Blood Transfusion Diagnostics Industry Revenue Share (%), by Type 2025 & 2033

- Figure 20: Asia Pacific Blood Transfusion Diagnostics Industry Revenue (billion), by Application 2025 & 2033

- Figure 21: Asia Pacific Blood Transfusion Diagnostics Industry Revenue Share (%), by Application 2025 & 2033

- Figure 22: Asia Pacific Blood Transfusion Diagnostics Industry Revenue (billion), by End-User 2025 & 2033

- Figure 23: Asia Pacific Blood Transfusion Diagnostics Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 24: Asia Pacific Blood Transfusion Diagnostics Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Asia Pacific Blood Transfusion Diagnostics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Blood Transfusion Diagnostics Industry Revenue (billion), by Type 2025 & 2033

- Figure 27: Middle East and Africa Blood Transfusion Diagnostics Industry Revenue Share (%), by Type 2025 & 2033

- Figure 28: Middle East and Africa Blood Transfusion Diagnostics Industry Revenue (billion), by Application 2025 & 2033

- Figure 29: Middle East and Africa Blood Transfusion Diagnostics Industry Revenue Share (%), by Application 2025 & 2033

- Figure 30: Middle East and Africa Blood Transfusion Diagnostics Industry Revenue (billion), by End-User 2025 & 2033

- Figure 31: Middle East and Africa Blood Transfusion Diagnostics Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 32: Middle East and Africa Blood Transfusion Diagnostics Industry Revenue (billion), by Country 2025 & 2033

- Figure 33: Middle East and Africa Blood Transfusion Diagnostics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: South America Blood Transfusion Diagnostics Industry Revenue (billion), by Type 2025 & 2033

- Figure 35: South America Blood Transfusion Diagnostics Industry Revenue Share (%), by Type 2025 & 2033

- Figure 36: South America Blood Transfusion Diagnostics Industry Revenue (billion), by Application 2025 & 2033

- Figure 37: South America Blood Transfusion Diagnostics Industry Revenue Share (%), by Application 2025 & 2033

- Figure 38: South America Blood Transfusion Diagnostics Industry Revenue (billion), by End-User 2025 & 2033

- Figure 39: South America Blood Transfusion Diagnostics Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 40: South America Blood Transfusion Diagnostics Industry Revenue (billion), by Country 2025 & 2033

- Figure 41: South America Blood Transfusion Diagnostics Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Blood Transfusion Diagnostics Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Global Blood Transfusion Diagnostics Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 3: Global Blood Transfusion Diagnostics Industry Revenue billion Forecast, by End-User 2020 & 2033

- Table 4: Global Blood Transfusion Diagnostics Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Global Blood Transfusion Diagnostics Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Blood Transfusion Diagnostics Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 7: Global Blood Transfusion Diagnostics Industry Revenue billion Forecast, by End-User 2020 & 2033

- Table 8: Global Blood Transfusion Diagnostics Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: United States Blood Transfusion Diagnostics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Canada Blood Transfusion Diagnostics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Mexico Blood Transfusion Diagnostics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Global Blood Transfusion Diagnostics Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 13: Global Blood Transfusion Diagnostics Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 14: Global Blood Transfusion Diagnostics Industry Revenue billion Forecast, by End-User 2020 & 2033

- Table 15: Global Blood Transfusion Diagnostics Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Germany Blood Transfusion Diagnostics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: United Kingdom Blood Transfusion Diagnostics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: France Blood Transfusion Diagnostics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Italy Blood Transfusion Diagnostics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Spain Blood Transfusion Diagnostics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Rest of Europe Blood Transfusion Diagnostics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Global Blood Transfusion Diagnostics Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 23: Global Blood Transfusion Diagnostics Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 24: Global Blood Transfusion Diagnostics Industry Revenue billion Forecast, by End-User 2020 & 2033

- Table 25: Global Blood Transfusion Diagnostics Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 26: China Blood Transfusion Diagnostics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Japan Blood Transfusion Diagnostics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: India Blood Transfusion Diagnostics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 29: Australia Blood Transfusion Diagnostics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: South Korea Blood Transfusion Diagnostics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 31: Rest of Asia Pacific Blood Transfusion Diagnostics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Global Blood Transfusion Diagnostics Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 33: Global Blood Transfusion Diagnostics Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 34: Global Blood Transfusion Diagnostics Industry Revenue billion Forecast, by End-User 2020 & 2033

- Table 35: Global Blood Transfusion Diagnostics Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 36: GCC Blood Transfusion Diagnostics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: South Africa Blood Transfusion Diagnostics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: Rest of Middle East and Africa Blood Transfusion Diagnostics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 39: Global Blood Transfusion Diagnostics Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 40: Global Blood Transfusion Diagnostics Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 41: Global Blood Transfusion Diagnostics Industry Revenue billion Forecast, by End-User 2020 & 2033

- Table 42: Global Blood Transfusion Diagnostics Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 43: Brazil Blood Transfusion Diagnostics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: Argentina Blood Transfusion Diagnostics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Rest of South America Blood Transfusion Diagnostics Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Blood Transfusion Diagnostics Industry?

The projected CAGR is approximately 7.89%.

2. Which companies are prominent players in the Blood Transfusion Diagnostics Industry?

Key companies in the market include Werfen*List Not Exhaustive, Bio-Rad Laboratories Inc, QUOTIENT, Merck KGaA, F Hoffmann-La Roche Ltd, Diasorin S p A, Abbott, Grifols S A, Immucor Inc, Danaher.

3. What are the main segments of the Blood Transfusion Diagnostics Industry?

The market segments include Type, Application, End-User.

4. Can you provide details about the market size?

The market size is estimated to be USD 5.97 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Number of Blood Related Disorders; Technological Advancement in the Blood Testing Kits and Assays.

6. What are the notable trends driving market growth?

Reagents & Kits Segment is Anticipated to Hold a Significant Share Over the Forecast Period.

7. Are there any restraints impacting market growth?

Certain Adverse Reaction Associated with the Procedure.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Blood Transfusion Diagnostics Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Blood Transfusion Diagnostics Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Blood Transfusion Diagnostics Industry?

To stay informed about further developments, trends, and reports in the Blood Transfusion Diagnostics Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence