Key Insights

The global Risk Assurance market is poised for significant expansion, projected to reach USD 5072 million by 2033, driven by a robust CAGR of 10.2%. This dynamic growth is fueled by an increasing awareness among businesses and governments regarding the imperative of proactive risk identification and mitigation. The escalating complexity of regulatory landscapes, coupled with the ever-present threat of cyberattacks and operational disruptions, compels organizations to invest heavily in comprehensive risk assurance services. Key drivers include the need for enhanced corporate governance, greater transparency in financial reporting, and the imperative to safeguard sensitive data. Furthermore, the digital transformation across industries, while offering immense opportunities, also introduces new and intricate risk profiles, necessitating sophisticated assurance solutions. The market is segmented by application into Enterprise, Government and Public Departments, and Others, with a substantial portion of demand originating from the enterprise sector seeking to fortify its operations against potential threats.

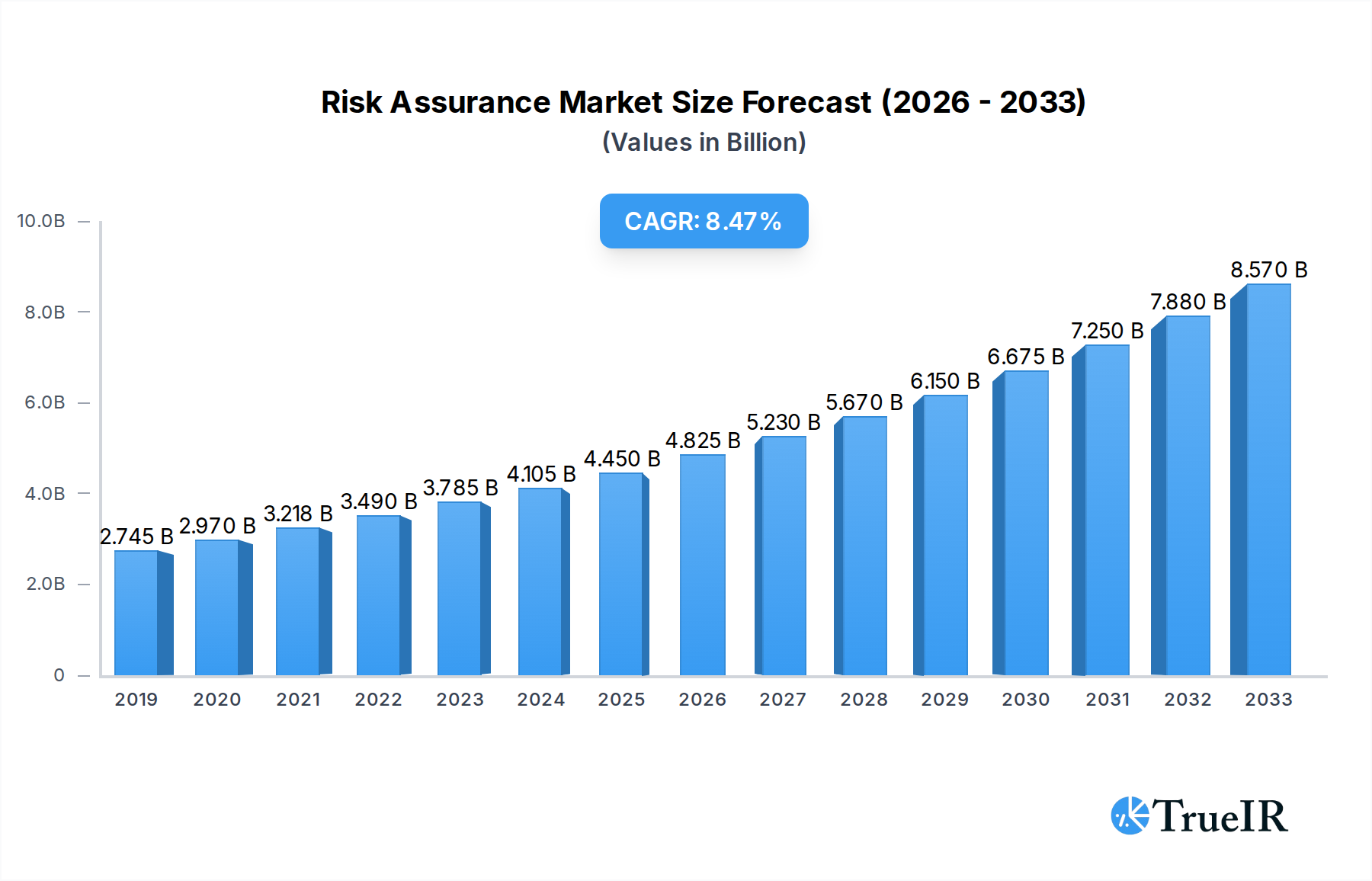

Risk Assurance Market Size (In Billion)

The burgeoning demand for Risk Assurance is further amplified by emerging trends such as the integration of advanced technologies like Artificial Intelligence (AI) and Machine Learning (ML) into risk management frameworks. These technologies enable more accurate predictive analytics, real-time monitoring, and automated risk assessments, thereby enhancing the effectiveness of assurance processes. The focus on IT and Cyber Security within the Risk Assurance services is particularly pronounced, reflecting the critical need to protect digital assets and maintain business continuity in an increasingly interconnected world. While the market experiences robust growth, certain restraints, such as the shortage of skilled risk assurance professionals and the cost of implementing advanced risk management technologies, may pose challenges. However, the overarching benefits of robust risk assurance in fostering trust, ensuring compliance, and enabling sustainable business growth are expected to outweigh these limitations, propelling the market forward.

Risk Assurance Company Market Share

Dynamic and SEO-Optimized Risk Assurance Report: Unveiling Market Dynamics and Future Trajectories (2019–2033)

This comprehensive Risk Assurance market report provides an in-depth analysis of the global landscape from 2019 to 2033, with a base and estimated year of 2025 and a forecast period spanning 2025–2033. Leveraging high-volume keywords and structured for maximum clarity, this report is essential for industry stakeholders seeking to understand market concentration, innovation drivers, regulatory impacts, dominant segments, and future growth opportunities.

Risk Assurance Market Structure & Competitive Landscape

The Risk Assurance market exhibits a moderately concentrated structure, with a significant presence of Big Four firms (PwC, KPMG, EY, Deloitte) alongside a growing number of specialized players. Innovation is primarily driven by the increasing complexity of regulatory environments and the escalating sophistication of cyber threats. Regulatory impacts are profound, with evolving compliance mandates (e.g., GDPR, CCPA) shaping service offerings and demanding continuous adaptation. Product substitutes, while present in niche areas, are largely outpaced by the integrated nature of comprehensive risk assurance solutions. End-user segmentation reveals a strong demand from Enterprise clients, followed by Government and Public Departments, and a growing "Others" category encompassing non-profits and emerging sectors. Mergers and acquisitions (M&A) remain a key trend, with an estimated volume of over 50 significant transactions between 2019 and 2024, aimed at consolidating market share, expanding service portfolios, and acquiring niche expertise. For instance, the acquisition of IT security firms by larger consultancies has been a recurring theme, reinforcing the integration of IT and Cyber Security services. The market is characterized by continuous investment in talent and technology, with an estimated 15% year-on-year growth in R&D spending by leading firms in the last two years. Concentration ratios for the top 5 players in developed markets hover around 70%, indicating a substantial but not insurmountable market dominance.

Risk Assurance Market Trends & Opportunities

The global Risk Assurance market is experiencing robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 12.5% over the forecast period (2025–2033). This expansion is fueled by an escalating awareness among organizations of all sizes regarding the multifaceted risks they face, ranging from financial and operational vulnerabilities to cyber threats and regulatory non-compliance. The market size is estimated to reach over $200 million by 2033, a significant leap from the historical figures. Technological shifts are a primary catalyst, with the increasing adoption of Artificial Intelligence (AI), Machine Learning (ML), and Big Data analytics revolutionizing how risk is assessed, monitored, and managed. These technologies enable more proactive identification of potential issues, predictive risk modeling, and automated compliance checks, thereby enhancing efficiency and accuracy. Consumer preferences are evolving towards integrated, end-to-end risk solutions that encompass not just identification but also mitigation and remediation strategies. Companies are seeking partners who can offer strategic insights and practical implementation support. Competitive dynamics are intensifying, with established players continuously innovating their service portfolios to address emerging risks, such as climate-related disclosures and ESG (Environmental, Social, and Governance) compliance. New entrants and specialized firms are carving out niches by focusing on specific industries or technological competencies. The market penetration rate for advanced risk assurance solutions is steadily increasing, driven by a growing understanding of the ROI associated with robust risk management frameworks. The continuous rise in cyber-attacks, with estimated annual losses in the tens of millions for affected enterprises, further underscores the critical need for comprehensive IT and Cyber Security assurance. The digital transformation across industries, from Enterprise applications to Government and Public Departments, necessitates a parallel transformation in risk management strategies, creating a consistent demand for specialized expertise. The market is also seeing a growing emphasis on proactive risk identification rather than reactive responses, with organizations investing millions in predictive analytics tools.

Dominant Markets & Segments in Risk Assurance

The Enterprise segment is the dominant force within the Risk Assurance market, driven by a confluence of factors including the sheer scale of their operations, the complexity of their business models, and the significant financial and reputational stakes involved in risk management. These organizations are investing billions annually in comprehensive risk assurance programs to safeguard their assets, maintain regulatory compliance, and ensure business continuity. Key growth drivers in this segment include the need for robust internal controls, effective fraud prevention, and assurance over financial reporting. The increasing adoption of digital technologies and the expansion into global markets further amplify the need for sophisticated risk assessment and management.

Application:

- Enterprise: Constitutes the largest share of the market, driven by complex regulatory landscapes, operational risks, and the need for strong governance. Investment in this segment is estimated to exceed $150 million annually.

- Government and Public Departments: A significant and growing segment, propelled by increased public scrutiny, the need for accountability, and the management of large-scale public projects. Compliance with procurement regulations and data security are key drivers, with governmental spending in this area projected to reach over $50 million annually.

- Others: This segment, encompassing non-profits, educational institutions, and smaller businesses, is demonstrating substantial growth due to rising awareness of risk and the availability of more accessible assurance solutions.

Types:

- Risk Analysis and Management: This foundational service continues to be a core offering, with organizations investing millions to understand and mitigate inherent and residual risks across their operations.

- Internal Audit: Integral to corporate governance, internal audit services are in high demand, with an estimated annual market value of over $70 million, focusing on operational efficiency, compliance, and financial integrity.

- IT and Cyber Security: This segment is experiencing explosive growth, driven by the escalating sophistication and frequency of cyber threats. Global spending on IT and Cyber Security assurance is projected to surpass $90 million annually, reflecting the critical need to protect sensitive data and critical infrastructure.

- Others: Includes specialized areas like regulatory compliance assurance, ESG assurance, and fraud investigation, all witnessing steady growth.

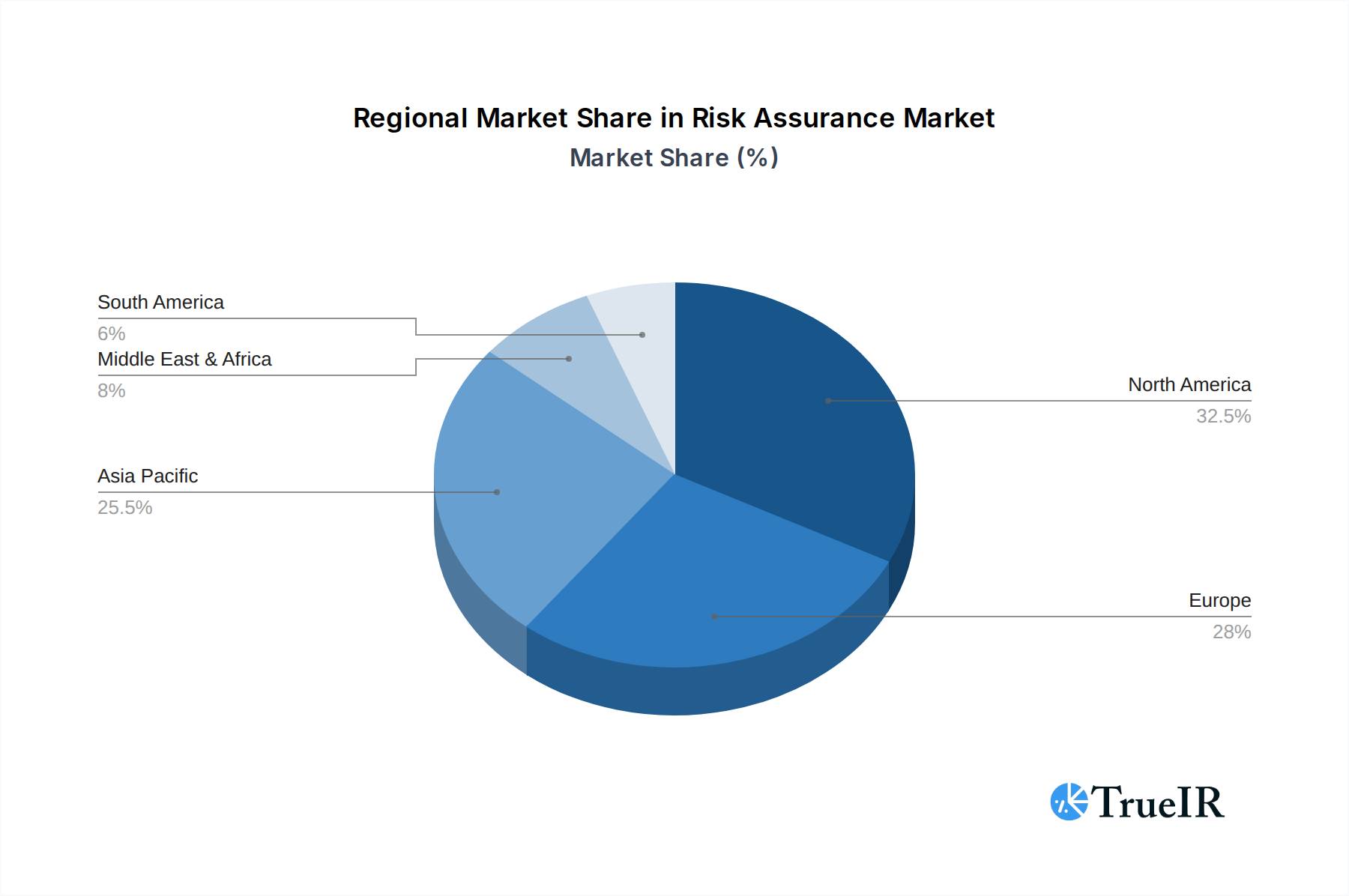

The dominant region for Risk Assurance services is North America, followed closely by Europe, due to their mature economies, stringent regulatory frameworks, and high adoption rates of advanced technologies. Asia-Pacific is emerging as a significant growth market, fueled by rapid industrialization and increasing regulatory oversight.

Risk Assurance Product Analysis

Risk assurance products are increasingly sophisticated, offering clients advanced technological solutions for risk identification, assessment, and mitigation. Innovations are heavily focused on leveraging AI and machine learning for predictive analytics, enabling organizations to anticipate potential issues before they materialize. Competitive advantages are derived from integrated platforms that combine financial, operational, and cyber risk management capabilities, providing a holistic view of an organization's risk posture. The application of these products spans across diverse industries, enhancing compliance, improving operational efficiency, and strengthening strategic decision-making. For instance, automated compliance modules are reducing manual efforts by millions of hours annually.

Key Drivers, Barriers & Challenges in Risk Assurance

Key Drivers, Barriers & Challenges in Risk Assurance The Risk Assurance market is propelled by several key drivers. Technological advancements, particularly in AI and Big Data analytics, enable more sophisticated risk assessment and predictive capabilities. Evolving regulatory landscapes, such as stricter data privacy laws and ESG reporting requirements, mandate robust assurance frameworks. Economic growth and globalization increase operational complexity, necessitating proactive risk management. Increasing awareness of reputational risk and cyber threats also fuels demand. For example, the growing sophistication of ransomware attacks, with estimated recovery costs in the tens of millions for affected businesses, directly drives investment in cyber risk assurance.

Growth Drivers in the Risk Assurance Market

Growth in the Risk Assurance market is primarily fueled by technological innovation, particularly the integration of AI and Big Data for predictive analytics and enhanced risk identification. The expanding scope of regulatory compliance, including evolving data privacy laws and ESG reporting mandates, necessitates comprehensive assurance services. Economic growth and increasing global interconnectedness lead to more complex operational environments, thereby increasing the demand for sophisticated risk management. Furthermore, the heightened awareness of cyber threats and the associated financial and reputational damage incentivizes businesses to invest in specialized IT and Cyber Security assurance.

Challenges Impacting Risk Assurance Growth

Several challenges can impact Risk Assurance growth. Regulatory complexities and the constant evolution of compliance requirements create a dynamic and demanding environment for service providers. Supply chain disruptions can indirectly affect client ability to invest in assurance services. Intense competitive pressures among established firms and emerging players can lead to price sensitivity. The scarcity of specialized talent with expertise in areas like advanced analytics and cyber security also poses a restraint. For instance, the estimated global shortage of cybersecurity professionals could impede the growth of IT and Cyber Security assurance services.

Key Players Shaping the Risk Assurance Market

- PwC

- KPMG

- EY

- Deloitte

- Azets UK

- RSM UK Group

- BPM

- Johnston Carmichael

- BDO

- Nexia

- Haysmacintyre

- Scrutton Bland

- Aspida Group

- HoganTaylor LLP

- ITSEC

- In.Corp Global

- SUBEX

- A&A Associate

- Moore Global

- Jersey Finance

- Bishop Fleming

- The Shard

- Kreston

- Mazars

Significant Risk Assurance Industry Milestones

- 2019: Increased focus on GDPR compliance post-implementation, leading to a surge in data privacy assurance services.

- 2020: The COVID-19 pandemic accelerated the adoption of remote auditing techniques and heightened focus on business continuity and supply chain resilience.

- 2021: Growing regulatory pressure around ESG reporting led to the development of specialized ESG assurance services, with significant investment in new methodologies.

- 2022: Rise in sophisticated cyber-attacks prompted substantial investment in advanced IT and cyber security assurance solutions by enterprises globally.

- 2023: Emergence of AI-driven risk assessment tools began to transform the market, offering predictive capabilities and enhancing audit efficiency.

- 2024: Increased M&A activity as larger firms sought to acquire niche expertise in areas like cloud security and data analytics.

Future Outlook for Risk Assurance Market

The future outlook for the Risk Assurance market is exceptionally positive, driven by persistent technological advancements and an ever-evolving risk landscape. Strategic opportunities lie in the continued integration of AI and ML to provide more predictive and proactive assurance solutions. The growing demand for ESG assurance and the increasing regulatory focus on climate-related risks present significant growth avenues. Expansion into emerging markets and the development of tailored services for specific industry verticals will further fuel market penetration. The increasing digitization across all sectors, from enterprise applications to government services, will continuously necessitate robust risk management frameworks, ensuring sustained demand for risk assurance professionals and solutions.

Risk Assurance Segmentation

-

1. Application

- 1.1. Enterprise

- 1.2. Government and Public Departments

- 1.3. Others

-

2. Types

- 2.1. Risk Analysis and Management

- 2.2. Internal Audit

- 2.3. IT and Cyber Security

- 2.4. Others

Risk Assurance Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Risk Assurance Regional Market Share

Geographic Coverage of Risk Assurance

Risk Assurance REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Risk Assurance Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Enterprise

- 5.1.2. Government and Public Departments

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Risk Analysis and Management

- 5.2.2. Internal Audit

- 5.2.3. IT and Cyber Security

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Risk Assurance Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Enterprise

- 6.1.2. Government and Public Departments

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Risk Analysis and Management

- 6.2.2. Internal Audit

- 6.2.3. IT and Cyber Security

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Risk Assurance Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Enterprise

- 7.1.2. Government and Public Departments

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Risk Analysis and Management

- 7.2.2. Internal Audit

- 7.2.3. IT and Cyber Security

- 7.2.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Risk Assurance Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Enterprise

- 8.1.2. Government and Public Departments

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Risk Analysis and Management

- 8.2.2. Internal Audit

- 8.2.3. IT and Cyber Security

- 8.2.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Risk Assurance Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Enterprise

- 9.1.2. Government and Public Departments

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Risk Analysis and Management

- 9.2.2. Internal Audit

- 9.2.3. IT and Cyber Security

- 9.2.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Risk Assurance Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Enterprise

- 10.1.2. Government and Public Departments

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Risk Analysis and Management

- 10.2.2. Internal Audit

- 10.2.3. IT and Cyber Security

- 10.2.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 PwC

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 KPMG

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 EY

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Deloitte

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Azets UK

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 RSM UK Group

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 BPM

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Johnston Carmichael

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 BDO

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Nexia

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Haysmacintyre

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Scrutton Bland

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Aspida Group

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 HoganTaylor LLP

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 ITSEC

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 In.Corp Global

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 SUBEX

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 A&A Associate

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Moore Global

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Jersey Finance

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 Bishop Fleming

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.22 The Shard

- 11.2.22.1. Overview

- 11.2.22.2. Products

- 11.2.22.3. SWOT Analysis

- 11.2.22.4. Recent Developments

- 11.2.22.5. Financials (Based on Availability)

- 11.2.23 Kreston

- 11.2.23.1. Overview

- 11.2.23.2. Products

- 11.2.23.3. SWOT Analysis

- 11.2.23.4. Recent Developments

- 11.2.23.5. Financials (Based on Availability)

- 11.2.24 Mazars

- 11.2.24.1. Overview

- 11.2.24.2. Products

- 11.2.24.3. SWOT Analysis

- 11.2.24.4. Recent Developments

- 11.2.24.5. Financials (Based on Availability)

- 11.2.1 PwC

List of Figures

- Figure 1: Global Risk Assurance Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Risk Assurance Revenue (million), by Application 2025 & 2033

- Figure 3: North America Risk Assurance Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Risk Assurance Revenue (million), by Types 2025 & 2033

- Figure 5: North America Risk Assurance Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Risk Assurance Revenue (million), by Country 2025 & 2033

- Figure 7: North America Risk Assurance Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Risk Assurance Revenue (million), by Application 2025 & 2033

- Figure 9: South America Risk Assurance Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Risk Assurance Revenue (million), by Types 2025 & 2033

- Figure 11: South America Risk Assurance Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Risk Assurance Revenue (million), by Country 2025 & 2033

- Figure 13: South America Risk Assurance Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Risk Assurance Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Risk Assurance Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Risk Assurance Revenue (million), by Types 2025 & 2033

- Figure 17: Europe Risk Assurance Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Risk Assurance Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Risk Assurance Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Risk Assurance Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Risk Assurance Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Risk Assurance Revenue (million), by Types 2025 & 2033

- Figure 23: Middle East & Africa Risk Assurance Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Risk Assurance Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Risk Assurance Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Risk Assurance Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Risk Assurance Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Risk Assurance Revenue (million), by Types 2025 & 2033

- Figure 29: Asia Pacific Risk Assurance Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Risk Assurance Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Risk Assurance Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Risk Assurance Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Risk Assurance Revenue million Forecast, by Types 2020 & 2033

- Table 3: Global Risk Assurance Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Risk Assurance Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Risk Assurance Revenue million Forecast, by Types 2020 & 2033

- Table 6: Global Risk Assurance Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Risk Assurance Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Risk Assurance Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Risk Assurance Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Risk Assurance Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Risk Assurance Revenue million Forecast, by Types 2020 & 2033

- Table 12: Global Risk Assurance Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Risk Assurance Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Risk Assurance Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Risk Assurance Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Risk Assurance Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Risk Assurance Revenue million Forecast, by Types 2020 & 2033

- Table 18: Global Risk Assurance Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Risk Assurance Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Risk Assurance Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Risk Assurance Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Risk Assurance Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Risk Assurance Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Risk Assurance Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Risk Assurance Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Risk Assurance Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Risk Assurance Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Risk Assurance Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Risk Assurance Revenue million Forecast, by Types 2020 & 2033

- Table 30: Global Risk Assurance Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Risk Assurance Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Risk Assurance Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Risk Assurance Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Risk Assurance Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Risk Assurance Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Risk Assurance Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Risk Assurance Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Risk Assurance Revenue million Forecast, by Types 2020 & 2033

- Table 39: Global Risk Assurance Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Risk Assurance Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Risk Assurance Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Risk Assurance Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Risk Assurance Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Risk Assurance Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Risk Assurance Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Risk Assurance Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Risk Assurance?

The projected CAGR is approximately 10.2%.

2. Which companies are prominent players in the Risk Assurance?

Key companies in the market include PwC, KPMG, EY, Deloitte, Azets UK, RSM UK Group, BPM, Johnston Carmichael, BDO, Nexia, Haysmacintyre, Scrutton Bland, Aspida Group, HoganTaylor LLP, ITSEC, In.Corp Global, SUBEX, A&A Associate, Moore Global, Jersey Finance, Bishop Fleming, The Shard, Kreston, Mazars.

3. What are the main segments of the Risk Assurance?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 5072 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Risk Assurance," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Risk Assurance report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Risk Assurance?

To stay informed about further developments, trends, and reports in the Risk Assurance, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence