Key Insights

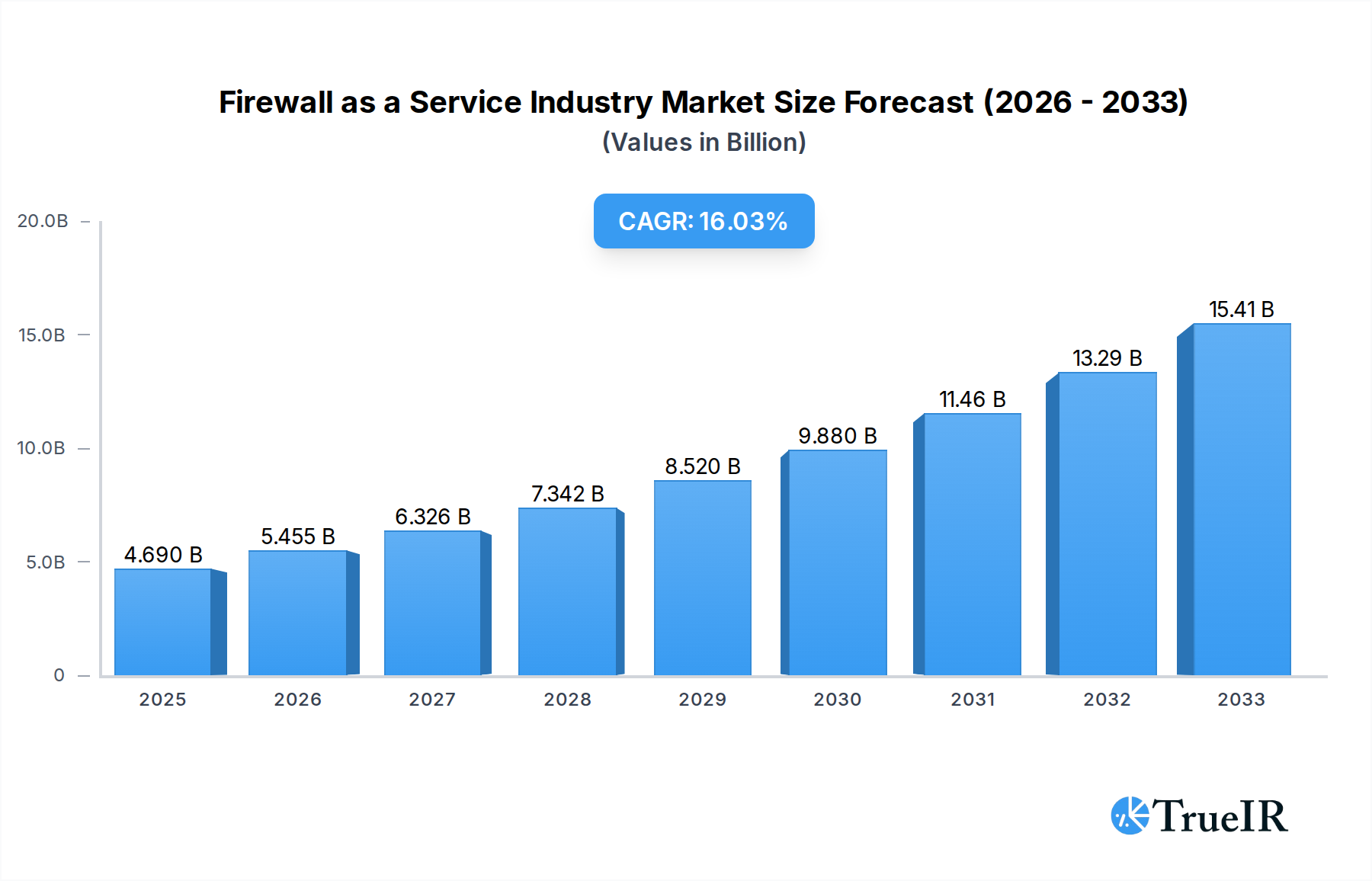

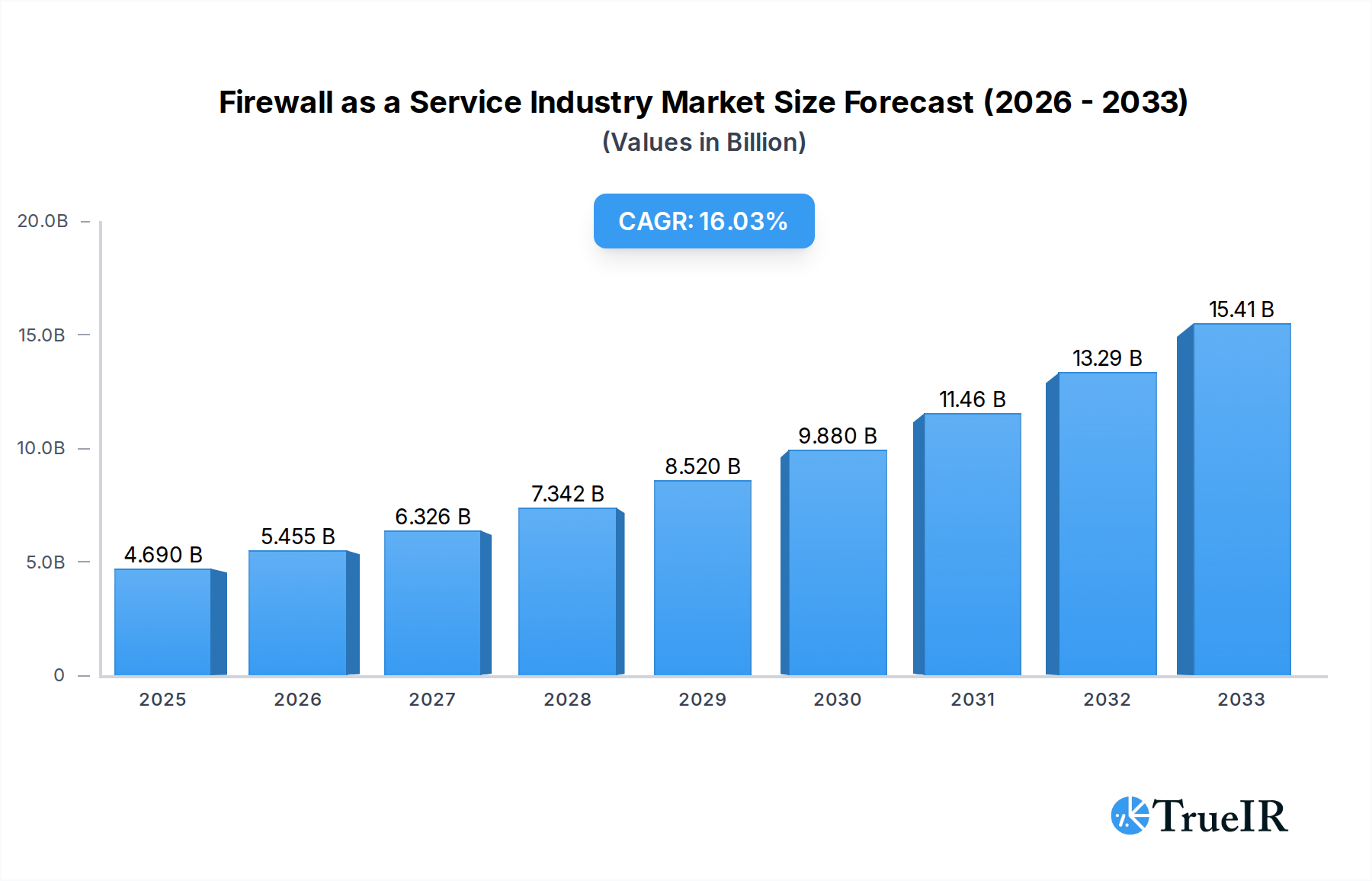

The Firewall as a Service (FWaaS) industry is experiencing robust expansion, projected to reach a market size of $4.69 billion by 2025. This significant growth is fueled by a compelling Compound Annual Growth Rate (CAGR) of 16.47%, indicating a dynamic and rapidly evolving market. The increasing adoption of cloud computing, coupled with the rising sophistication and frequency of cyber threats, are primary drivers propelling the demand for scalable, flexible, and cost-effective security solutions like FWaaS. Organizations are increasingly looking beyond traditional, hardware-based firewalls to embrace subscription-based models that offer agility and centralized management, particularly beneficial for distributed workforces and hybrid cloud environments. The shift towards robust cybersecurity postures, regulatory compliance mandates, and the inherent advantages of cloud-native security platforms are further accelerating market penetration.

Firewall as a Service Industry Market Size (In Billion)

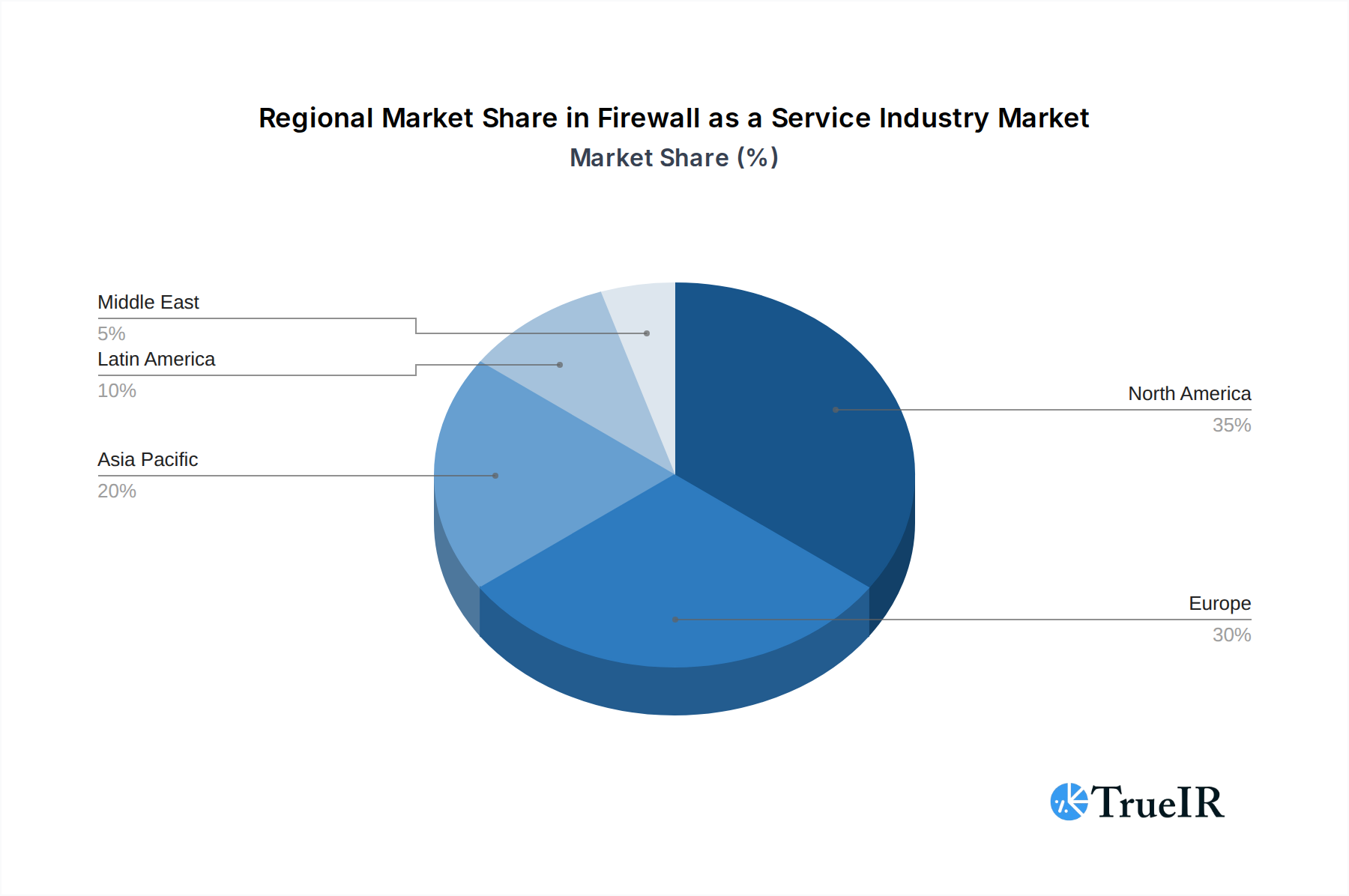

The FWaaS market is segmented across various service models, including SaaS, IaaS, and PaaS, with SaaS models likely dominating due to their ease of deployment and management. Deployment models range from private, public, and hybrid clouds, catering to diverse enterprise needs and risk appetites. User types, encompassing both Large Enterprises and Small and Medium-sized Enterprises (SMEs), are contributing to this growth, with SMEs finding FWaaS an accessible and powerful security solution. Key industry verticals like BFSI, IT & Telecom, Healthcare, and Retail are at the forefront of FWaaS adoption due to the sensitive nature of data they handle and stringent compliance requirements. Geographically, North America and Europe are expected to lead the market, followed by the rapidly growing Asia Pacific region. Emerging trends also point towards the integration of advanced threat intelligence, AI-driven security analytics, and zero-trust security architectures within FWaaS offerings, solidifying its position as a cornerstone of modern network security.

Firewall as a Service Industry Company Market Share

Firewall as a Service Industry: Comprehensive Market Analysis and Future Projections (2019–2033)

This in-depth report provides a definitive analysis of the global Firewall as a Service (FWaaS) industry, offering strategic insights and actionable intelligence for stakeholders. Covering the historical period from 2019 to 2024, with a base year of 2025 and an extensive forecast period extending to 2033, this study leverages high-volume keywords to enhance SEO visibility and engage a broad industry audience. We dissect market structure, trends, dominant segments, product innovations, key drivers, barriers, and the competitive landscape, painting a clear picture of the FWaaS market's trajectory. The estimated market size for 2025 is predicted to reach $XX Million.

Firewall as a Service Industry Market Structure & Competitive Landscape

The Firewall as a Service (FWaaS) industry is characterized by a dynamic and evolving competitive landscape, marked by a moderate to high degree of market concentration driven by significant players and ongoing technological advancements. Innovation is a primary driver, with companies continuously investing in R&D to develop advanced security features, cloud-native solutions, and integrated platform offerings. Regulatory impacts, particularly evolving data privacy laws and cybersecurity mandates, are increasingly shaping market entry and operational strategies, pushing for robust compliance mechanisms within FWaaS solutions. Product substitutes, while present in traditional on-premise firewalls, are becoming less viable as organizations prioritize scalability, flexibility, and cost-efficiency offered by cloud-based FWaaS.

End-user segmentation is diverse, ranging from large enterprises with complex security needs to small and medium-sized enterprises (SMEs) seeking simplified, cost-effective security solutions. Mergers and acquisitions (M&A) activity is a notable trend, with larger players acquiring smaller innovative firms to expand their product portfolios, customer base, and geographical reach. For instance, the past few years have seen several strategic acquisitions aimed at bolstering cloud security and SASE capabilities. The concentration ratio for the top five players is estimated to be around XX%, reflecting the influence of established vendors. M&A volumes are projected to continue at an average of XX per year over the forecast period, indicating ongoing consolidation and strategic realignment.

Firewall as a Service Industry Market Trends & Opportunities

The Firewall as a Service (FWaaS) market is poised for substantial growth, driven by an escalating demand for robust cybersecurity solutions in an increasingly interconnected and threat-laden digital landscape. The projected market size for FWaaS is expected to experience a Compound Annual Growth Rate (CAGR) of XX% from 2025 to 2033, reaching an estimated $XX Million by the end of the forecast period. This expansion is fueled by a fundamental shift in how businesses approach network security, moving away from traditional hardware-centric models to more agile, scalable, and cost-effective cloud-based services.

Technological shifts are at the forefront of this growth. The rise of Secure Access Service Edge (SASE) frameworks, which converge networking and security functions into a unified cloud-delivered service, is a major catalyst. FWaaS is a core component of SASE, offering granular access control, threat prevention, and secure connectivity for distributed workforces. The increasing adoption of Software-Defined Wide Area Networking (SD-WAN) further complements FWaaS, enabling seamless integration and centralized management of network security policies across multiple locations. Furthermore, advancements in artificial intelligence (AI) and machine learning (ML) are being integrated into FWaaS solutions to provide predictive threat intelligence, automated incident response, and enhanced detection capabilities for sophisticated cyberattacks.

Consumer preferences are also evolving. Businesses are increasingly prioritizing ease of deployment, management, and scalability, benefits inherent in cloud-based FWaaS. The operational expenditure (OpEx) model, where organizations pay a subscription fee rather than making large capital expenditures (CapEx) on hardware, is highly attractive, especially for SMEs and rapidly growing enterprises. The growing prevalence of remote and hybrid work models necessitates perimeter-less security, making FWaaS an indispensable tool for securing access for a geographically dispersed workforce. The market penetration rate for FWaaS is currently estimated at XX% and is expected to surge to over XX% by 2033.

Competitive dynamics are intensifying, with both established cybersecurity vendors and new cloud-native security providers vying for market share. Strategic partnerships and alliances are becoming crucial for expanding service offerings and reach. For instance, collaborations between FWaaS providers and cloud infrastructure giants like AWS and Azure are enabling seamless integration and enhanced security for cloud deployments. The ongoing innovation in threat detection, including zero-trust architecture implementations and advanced endpoint protection, presents significant opportunities for FWaaS providers to differentiate themselves and capture market share. The growing awareness of the financial and reputational damage caused by cyberattacks is further accelerating the adoption of comprehensive FWaaS solutions, creating a fertile ground for innovation and growth within the industry.

Dominant Markets & Segments in Firewall as a Service Industry

The Firewall as a Service (FWaaS) market exhibits distinct patterns of dominance across various segments, driven by specific industry needs, technological adoption rates, and regulatory environments.

Service Model Dominance:

- SaaS (Software as a Service): This is the most dominant service model within the FWaaS industry. Its inherent cloud-native architecture, subscription-based pricing, and ease of scalability align perfectly with the demands of modern businesses. Organizations of all sizes are increasingly opting for SaaS-based FWaaS for its agility and reduced management overhead. The market share for SaaS FWaaS is estimated to be around XX%.

- Key Growth Drivers: User-friendly interfaces, rapid deployment capabilities, continuous updates and feature enhancements, and predictable subscription costs.

- IaaS (Infrastructure as a Service): While less dominant than SaaS, IaaS plays a crucial role, particularly for organizations that require greater control over their underlying infrastructure while still leveraging cloud security benefits. This model allows businesses to deploy FWaaS solutions on their own cloud instances, offering customization and integration flexibility.

- Key Growth Drivers: Requirement for specific configurations, integration with existing IaaS environments, and advanced customization needs.

- PaaS (Platform as a Service): PaaS is emerging as a niche but significant segment, offering developers and IT professionals a platform to build and deploy secure applications with integrated FWaaS capabilities. This model is gaining traction in environments focused on application development and continuous integration/continuous deployment (CI/CD).

- Key Growth Drivers: Facilitating secure application development, enabling DevOps practices, and offering tailored security for specific platforms.

Deployment Model Dominance:

- Public Cloud: The public cloud deployment model is experiencing rapid adoption due to its cost-effectiveness, scalability, and accessibility. Major cloud providers offer integrated FWaaS solutions, making it a preferred choice for many organizations looking to leverage the benefits of cloud computing. The public cloud segment is projected to account for XX% of the market.

- Key Growth Drivers: Cost savings, elastic scalability, broad availability of services from major cloud providers (AWS, Azure, GCP).

- Hybrid Cloud: The hybrid cloud deployment model is also highly significant, catering to organizations that require a mix of on-premise and cloud-based security. This model allows for flexibility in data handling and regulatory compliance, while still benefiting from cloud-based FWaaS for distributed environments.

- Key Growth Drivers: Compliance with data residency laws, integration with existing on-premise infrastructure, and a phased approach to cloud migration.

- Private Cloud: While less prevalent than public or hybrid models, private cloud deployments remain critical for highly regulated industries or organizations with extremely sensitive data requiring maximum control and isolation.

- Key Growth Drivers: Enhanced data security and privacy, strict regulatory compliance requirements, and tailored security policies.

User Type Dominance:

- Large Enterprises: These organizations, with their expansive networks, complex IT infrastructures, and high-value data, are major consumers of FWaaS. Their need for advanced threat protection, centralized management, and compliance with stringent regulations makes them prime candidates for comprehensive FWaaS solutions. Large enterprises are expected to contribute XX% to the market revenue.

- Key Growth Drivers: Sophisticated threat landscapes, compliance mandates, scalability for distributed operations, and need for robust security analytics.

- SMEs (Small and Medium-sized Enterprises): SMEs are increasingly adopting FWaaS due to its cost-effectiveness, ease of deployment, and the ability to access enterprise-grade security without significant upfront investment. The growing threat of cyberattacks targeting smaller businesses is driving this segment's growth. SMEs represent a rapidly expanding segment, estimated at XX% of the market.

- Key Growth Drivers: Budget-friendly security solutions, simplified management, protection against increasing cyber threats, and access to advanced security features without dedicated IT security staff.

Industry Vertical Dominance:

- IT & Telecom: This sector is a leading adopter of FWaaS, driven by its inherently digital infrastructure, the constant need to protect vast amounts of data, and the rapid evolution of network technologies. The demand for secure connectivity and protection against sophisticated cyber threats is paramount. This vertical accounts for an estimated XX% market share.

- Key Growth Drivers: High volume of data traffic, critical infrastructure protection, rapid adoption of cloud technologies, and stringent security requirements for service delivery.

- BFSI (Banking, Financial Services, and Insurance): The BFSI sector is a high-priority segment for FWaaS due to the extreme sensitivity of financial data and the stringent regulatory requirements governing the industry. Protecting against financial fraud, data breaches, and ensuring compliance are critical. The BFSI sector is estimated to contribute XX% to the market.

- Key Growth Drivers: Regulatory compliance (e.g., PCI DSS, GDPR), protection against sophisticated financial fraud, safeguarding sensitive customer data, and maintaining customer trust.

- Healthcare: With the increasing digitization of patient records and the growing threat of ransomware attacks targeting healthcare systems, the healthcare industry is a significant and growing adopter of FWaaS. Ensuring patient data privacy and the availability of critical systems are paramount. This vertical is projected to hold XX% of the market share.

- Key Growth Drivers: Protecting sensitive patient health information (PHI), ensuring continuity of care, compliance with HIPAA, and mitigating risks from ransomware attacks.

- Retail: The retail industry's reliance on e-commerce and digital transactions makes it vulnerable to cyber threats. FWaaS plays a crucial role in protecting customer data, securing payment gateways, and preventing online fraud.

- Key Growth Drivers: Securing online transactions, protecting customer data, preventing e-commerce fraud, and ensuring compliance with data privacy regulations.

- Aerospace & Defence: This vertical demands the highest levels of security due to the sensitive nature of its operations and intellectual property. FWaaS solutions are essential for protecting critical infrastructure, research data, and secure communication channels.

- Key Growth Drivers: Protecting highly sensitive data and intellectual property, securing critical infrastructure, ensuring national security, and maintaining secure communication.

- Other Industry Verticals: A diverse range of other industries, including manufacturing, government, education, and energy, are also increasingly adopting FWaaS to enhance their cybersecurity posture. The generalized need for data protection, regulatory compliance, and secure remote access is driving adoption across these segments.

Firewall as a Service Industry Product Analysis

The Firewall as a Service (FWaaS) industry is witnessing a rapid evolution in product offerings, driven by technological advancements and the increasing sophistication of cyber threats. Key innovations include the integration of AI and machine learning for predictive threat detection and automated response, as well as the development of unified security platforms that consolidate multiple security functions into a single, cloud-delivered service. Products are increasingly optimized for cloud-native environments and distributed workforces, offering features such as zero-trust network access, advanced web filtering, and secure granular policy enforcement. Competitive advantages are being carved out through superior threat intelligence, ease of management, scalability, and seamless integration with other security and networking solutions. The focus is on providing comprehensive, agile, and intelligent security that adapts to the dynamic threat landscape.

Key Drivers, Barriers & Challenges in Firewall as a Service Industry

Key Drivers:

The Firewall as a Service (FWaaS) market is propelled by several key factors. The escalating sophistication and frequency of cyberattacks worldwide represent a primary driver, forcing organizations to seek robust, cloud-delivered security solutions. The widespread adoption of remote and hybrid work models has created an urgent need for secure access and perimeter-less security, a core offering of FWaaS. Furthermore, the growing emphasis on digital transformation and cloud migration necessitates scalable and flexible security infrastructure that FWaaS provides. Favorable economic factors, such as the shift from CapEx to OpEx and the cost-effectiveness of subscription-based services, are also significant drivers, particularly for SMEs. Policy-driven factors, including stringent data privacy regulations (e.g., GDPR, CCPA) and national cybersecurity mandates, compel organizations to adopt advanced security measures like FWaaS to ensure compliance.

Barriers & Challenges:

Despite its growth, the FWaaS market faces several barriers and challenges. Regulatory complexities and varying compliance requirements across different geographies can create hurdles for global deployment and adoption. Supply chain issues, while more prominent in hardware-centric security, can still indirectly impact the availability of underlying cloud infrastructure components necessary for FWaaS. Competitive pressures from established network security vendors and emerging cloud security specialists are intense, requiring continuous innovation and differentiation. Moreover, concerns regarding data privacy and security within cloud environments, coupled with potential vendor lock-in, can also act as restraints for some organizations. The perceived complexity of integrating new cloud-based security solutions into existing IT infrastructures can also be a challenge for some IT departments.

Growth Drivers in the Firewall as a Service Industry Market

The Firewall as a Service (FWaaS) market is experiencing robust growth driven by a confluence of technological, economic, and policy factors. Technologically, the rise of advanced threat landscapes, including sophisticated malware and ransomware, necessitates continuous security evolution that cloud-native FWaaS offers. The increasing adoption of cloud computing and the proliferation of remote workforces are fundamental drivers, demanding flexible, scalable, and accessible security solutions. Economically, the shift towards subscription-based models (OpEx) over capital expenditures (CapEx) makes advanced security more attainable for businesses of all sizes. Policy-wise, stringent data privacy regulations and increasing cybersecurity mandates from governments worldwide are pushing organizations to invest in comprehensive security measures like FWaaS to ensure compliance and protect sensitive data.

Challenges Impacting Firewall as a Service Industry Growth

The growth of the Firewall as a Service (FWaaS) industry is not without its obstacles. Regulatory complexities and the need to navigate diverse compliance landscapes across different regions pose significant challenges for vendors aiming for global reach. While less direct than for hardware, supply chain vulnerabilities in the broader cloud infrastructure ecosystem can indirectly impact service availability. Intense competitive pressures from both established players and agile startups demand constant innovation and strategic market positioning. Furthermore, inherent concerns regarding data privacy within cloud environments and the potential for vendor lock-in can create hesitations for some enterprises. Overcoming these challenges requires clear communication of security benefits, robust compliance frameworks, and a commitment to open integration.

Key Players Shaping the Firewall as a Service Industry Market

- Check Point Software Technologies Inc

- Barracuda Networks Inc

- Cato Networks

- Fortinet Inc

- Vocus Communications

- IntraSystems

- Cisco Systems Inc

- Microsoft Corporation

- Juniper Networks Inc

- Zscaler Inc

- Sprout Technologies Ltd

- Forcepoint

- WatchGuard Technologies

Significant Firewall as a Service Industry Industry Milestones

- February 2023: WatchGuard Technologies introduced the Firebox T25/T25-W, T45/T45-POE/T45-W-POE, and T85-POE tabletop firewall appliances. These new firewalls, powered by WatchGuard's Unified Security Platform architecture that offers advanced security and easy management via WatchGuard Cloud, are designed to offer the remote and distributed business environments required for better protection against network security threats.

- March 2022: Palo Alto Networks partnered with Amazon Web Services (AWS) to introduce the new Palo Alto Networks Cloud NGFW for AWS. This managed Next-Generation Firewall (NGFW) service aims to simplify securing AWS deployments, allowing businesses to innovate more quickly while maintaining high security. Palo Alto Networks is a 10-time market leader in network firewalls, and this new solution is expected to enhance its portfolio of cloud security offerings.

- February 2022: Juniper Networks unveiled Juniper Secure Edge, the newest component of its Secure Access Service Edge (SASE) design. This solution enables businesses to secure workforces regardless of their location. Juniper Secure Edge provides Firewall-as-a-Service (FWaaS) as a single-stack software architecture managed by Security Director Cloud. As a pioneer in secure, AI-powered networks, Juniper Networks is expected to leverage its expertise in this area to offer an innovative and secure solution for businesses seeking to protect their remote workforces.

Future Outlook for Firewall as a Service Industry Market

The future outlook for the Firewall as a Service (FWaaS) market is exceptionally promising, projecting sustained growth and innovation. The continuous evolution of cyber threats, coupled with the permanent shift towards hybrid and remote work models, will fuel the demand for flexible, scalable, and intelligent security solutions. The increasing integration of AI and machine learning will lead to more proactive threat detection and automated response capabilities. Furthermore, the ongoing expansion of SASE frameworks will solidify FWaaS as a core component of modern network security architecture. Strategic opportunities lie in offering comprehensive security platforms that seamlessly integrate with other cloud services, providing end-to-end protection and simplifying security management for organizations of all sizes. Market potential is significant as businesses across all verticals prioritize robust cybersecurity to navigate an increasingly complex digital landscape.

Firewall as a Service Industry Segmentation

-

1. Service Model

- 1.1. SaaS

- 1.2. IaaS

- 1.3. PaaS

-

2. Deployment Model

- 2.1. Private

- 2.2. Public

- 2.3. Hybrid

-

3. User Type

- 3.1. Large Enterprises

- 3.2. SMEs

-

4. Industry Vertical

- 4.1. BFSI

- 4.2. IT & Telecom

- 4.3. Healthcare

- 4.4. Retail

- 4.5. Aerospace & Defence

- 4.6. Other Industry Verticals

Firewall as a Service Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. United Kingdom

- 2.2. Germany

- 2.3. France

- 2.4. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. Australia

- 3.4. Rest of Asia Pacific

-

4. Latin America

- 4.1. Mexico

- 4.2. Brazil

- 4.3. Rest of Latin America

- 5. Middle East

Firewall as a Service Industry Regional Market Share

Geographic Coverage of Firewall as a Service Industry

Firewall as a Service Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 16.47% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Service Model

- 5.1.1. SaaS

- 5.1.2. IaaS

- 5.1.3. PaaS

- 5.2. Market Analysis, Insights and Forecast - by Deployment Model

- 5.2.1. Private

- 5.2.2. Public

- 5.2.3. Hybrid

- 5.3. Market Analysis, Insights and Forecast - by User Type

- 5.3.1. Large Enterprises

- 5.3.2. SMEs

- 5.4. Market Analysis, Insights and Forecast - by Industry Vertical

- 5.4.1. BFSI

- 5.4.2. IT & Telecom

- 5.4.3. Healthcare

- 5.4.4. Retail

- 5.4.5. Aerospace & Defence

- 5.4.6. Other Industry Verticals

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. North America

- 5.5.2. Europe

- 5.5.3. Asia Pacific

- 5.5.4. Latin America

- 5.5.5. Middle East

- 5.1. Market Analysis, Insights and Forecast - by Service Model

- 6. Global Firewall as a Service Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Service Model

- 6.1.1. SaaS

- 6.1.2. IaaS

- 6.1.3. PaaS

- 6.2. Market Analysis, Insights and Forecast - by Deployment Model

- 6.2.1. Private

- 6.2.2. Public

- 6.2.3. Hybrid

- 6.3. Market Analysis, Insights and Forecast - by User Type

- 6.3.1. Large Enterprises

- 6.3.2. SMEs

- 6.4. Market Analysis, Insights and Forecast - by Industry Vertical

- 6.4.1. BFSI

- 6.4.2. IT & Telecom

- 6.4.3. Healthcare

- 6.4.4. Retail

- 6.4.5. Aerospace & Defence

- 6.4.6. Other Industry Verticals

- 6.1. Market Analysis, Insights and Forecast - by Service Model

- 7. North America Firewall as a Service Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Service Model

- 7.1.1. SaaS

- 7.1.2. IaaS

- 7.1.3. PaaS

- 7.2. Market Analysis, Insights and Forecast - by Deployment Model

- 7.2.1. Private

- 7.2.2. Public

- 7.2.3. Hybrid

- 7.3. Market Analysis, Insights and Forecast - by User Type

- 7.3.1. Large Enterprises

- 7.3.2. SMEs

- 7.4. Market Analysis, Insights and Forecast - by Industry Vertical

- 7.4.1. BFSI

- 7.4.2. IT & Telecom

- 7.4.3. Healthcare

- 7.4.4. Retail

- 7.4.5. Aerospace & Defence

- 7.4.6. Other Industry Verticals

- 7.1. Market Analysis, Insights and Forecast - by Service Model

- 8. Europe Firewall as a Service Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Service Model

- 8.1.1. SaaS

- 8.1.2. IaaS

- 8.1.3. PaaS

- 8.2. Market Analysis, Insights and Forecast - by Deployment Model

- 8.2.1. Private

- 8.2.2. Public

- 8.2.3. Hybrid

- 8.3. Market Analysis, Insights and Forecast - by User Type

- 8.3.1. Large Enterprises

- 8.3.2. SMEs

- 8.4. Market Analysis, Insights and Forecast - by Industry Vertical

- 8.4.1. BFSI

- 8.4.2. IT & Telecom

- 8.4.3. Healthcare

- 8.4.4. Retail

- 8.4.5. Aerospace & Defence

- 8.4.6. Other Industry Verticals

- 8.1. Market Analysis, Insights and Forecast - by Service Model

- 9. Asia Pacific Firewall as a Service Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Service Model

- 9.1.1. SaaS

- 9.1.2. IaaS

- 9.1.3. PaaS

- 9.2. Market Analysis, Insights and Forecast - by Deployment Model

- 9.2.1. Private

- 9.2.2. Public

- 9.2.3. Hybrid

- 9.3. Market Analysis, Insights and Forecast - by User Type

- 9.3.1. Large Enterprises

- 9.3.2. SMEs

- 9.4. Market Analysis, Insights and Forecast - by Industry Vertical

- 9.4.1. BFSI

- 9.4.2. IT & Telecom

- 9.4.3. Healthcare

- 9.4.4. Retail

- 9.4.5. Aerospace & Defence

- 9.4.6. Other Industry Verticals

- 9.1. Market Analysis, Insights and Forecast - by Service Model

- 10. Latin America Firewall as a Service Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Service Model

- 10.1.1. SaaS

- 10.1.2. IaaS

- 10.1.3. PaaS

- 10.2. Market Analysis, Insights and Forecast - by Deployment Model

- 10.2.1. Private

- 10.2.2. Public

- 10.2.3. Hybrid

- 10.3. Market Analysis, Insights and Forecast - by User Type

- 10.3.1. Large Enterprises

- 10.3.2. SMEs

- 10.4. Market Analysis, Insights and Forecast - by Industry Vertical

- 10.4.1. BFSI

- 10.4.2. IT & Telecom

- 10.4.3. Healthcare

- 10.4.4. Retail

- 10.4.5. Aerospace & Defence

- 10.4.6. Other Industry Verticals

- 10.1. Market Analysis, Insights and Forecast - by Service Model

- 11. Middle East Firewall as a Service Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Service Model

- 11.1.1. SaaS

- 11.1.2. IaaS

- 11.1.3. PaaS

- 11.2. Market Analysis, Insights and Forecast - by Deployment Model

- 11.2.1. Private

- 11.2.2. Public

- 11.2.3. Hybrid

- 11.3. Market Analysis, Insights and Forecast - by User Type

- 11.3.1. Large Enterprises

- 11.3.2. SMEs

- 11.4. Market Analysis, Insights and Forecast - by Industry Vertical

- 11.4.1. BFSI

- 11.4.2. IT & Telecom

- 11.4.3. Healthcare

- 11.4.4. Retail

- 11.4.5. Aerospace & Defence

- 11.4.6. Other Industry Verticals

- 11.1. Market Analysis, Insights and Forecast - by Service Model

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Check Point Software Technologies Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Barracuda Networks Inc

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Cato Networks

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Fortinet Inc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Vocus Communications

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 IntraSystems

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Cisco Systems Inc

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Microsoft Corporation

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Juniper Networks Inc

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Zscaler Inc

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Sprout Technologies Ltd

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Forcepoint

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 Check Point Software Technologies Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Firewall as a Service Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Firewall as a Service Industry Revenue (Million), by Service Model 2025 & 2033

- Figure 3: North America Firewall as a Service Industry Revenue Share (%), by Service Model 2025 & 2033

- Figure 4: North America Firewall as a Service Industry Revenue (Million), by Deployment Model 2025 & 2033

- Figure 5: North America Firewall as a Service Industry Revenue Share (%), by Deployment Model 2025 & 2033

- Figure 6: North America Firewall as a Service Industry Revenue (Million), by User Type 2025 & 2033

- Figure 7: North America Firewall as a Service Industry Revenue Share (%), by User Type 2025 & 2033

- Figure 8: North America Firewall as a Service Industry Revenue (Million), by Industry Vertical 2025 & 2033

- Figure 9: North America Firewall as a Service Industry Revenue Share (%), by Industry Vertical 2025 & 2033

- Figure 10: North America Firewall as a Service Industry Revenue (Million), by Country 2025 & 2033

- Figure 11: North America Firewall as a Service Industry Revenue Share (%), by Country 2025 & 2033

- Figure 12: Europe Firewall as a Service Industry Revenue (Million), by Service Model 2025 & 2033

- Figure 13: Europe Firewall as a Service Industry Revenue Share (%), by Service Model 2025 & 2033

- Figure 14: Europe Firewall as a Service Industry Revenue (Million), by Deployment Model 2025 & 2033

- Figure 15: Europe Firewall as a Service Industry Revenue Share (%), by Deployment Model 2025 & 2033

- Figure 16: Europe Firewall as a Service Industry Revenue (Million), by User Type 2025 & 2033

- Figure 17: Europe Firewall as a Service Industry Revenue Share (%), by User Type 2025 & 2033

- Figure 18: Europe Firewall as a Service Industry Revenue (Million), by Industry Vertical 2025 & 2033

- Figure 19: Europe Firewall as a Service Industry Revenue Share (%), by Industry Vertical 2025 & 2033

- Figure 20: Europe Firewall as a Service Industry Revenue (Million), by Country 2025 & 2033

- Figure 21: Europe Firewall as a Service Industry Revenue Share (%), by Country 2025 & 2033

- Figure 22: Asia Pacific Firewall as a Service Industry Revenue (Million), by Service Model 2025 & 2033

- Figure 23: Asia Pacific Firewall as a Service Industry Revenue Share (%), by Service Model 2025 & 2033

- Figure 24: Asia Pacific Firewall as a Service Industry Revenue (Million), by Deployment Model 2025 & 2033

- Figure 25: Asia Pacific Firewall as a Service Industry Revenue Share (%), by Deployment Model 2025 & 2033

- Figure 26: Asia Pacific Firewall as a Service Industry Revenue (Million), by User Type 2025 & 2033

- Figure 27: Asia Pacific Firewall as a Service Industry Revenue Share (%), by User Type 2025 & 2033

- Figure 28: Asia Pacific Firewall as a Service Industry Revenue (Million), by Industry Vertical 2025 & 2033

- Figure 29: Asia Pacific Firewall as a Service Industry Revenue Share (%), by Industry Vertical 2025 & 2033

- Figure 30: Asia Pacific Firewall as a Service Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: Asia Pacific Firewall as a Service Industry Revenue Share (%), by Country 2025 & 2033

- Figure 32: Latin America Firewall as a Service Industry Revenue (Million), by Service Model 2025 & 2033

- Figure 33: Latin America Firewall as a Service Industry Revenue Share (%), by Service Model 2025 & 2033

- Figure 34: Latin America Firewall as a Service Industry Revenue (Million), by Deployment Model 2025 & 2033

- Figure 35: Latin America Firewall as a Service Industry Revenue Share (%), by Deployment Model 2025 & 2033

- Figure 36: Latin America Firewall as a Service Industry Revenue (Million), by User Type 2025 & 2033

- Figure 37: Latin America Firewall as a Service Industry Revenue Share (%), by User Type 2025 & 2033

- Figure 38: Latin America Firewall as a Service Industry Revenue (Million), by Industry Vertical 2025 & 2033

- Figure 39: Latin America Firewall as a Service Industry Revenue Share (%), by Industry Vertical 2025 & 2033

- Figure 40: Latin America Firewall as a Service Industry Revenue (Million), by Country 2025 & 2033

- Figure 41: Latin America Firewall as a Service Industry Revenue Share (%), by Country 2025 & 2033

- Figure 42: Middle East Firewall as a Service Industry Revenue (Million), by Service Model 2025 & 2033

- Figure 43: Middle East Firewall as a Service Industry Revenue Share (%), by Service Model 2025 & 2033

- Figure 44: Middle East Firewall as a Service Industry Revenue (Million), by Deployment Model 2025 & 2033

- Figure 45: Middle East Firewall as a Service Industry Revenue Share (%), by Deployment Model 2025 & 2033

- Figure 46: Middle East Firewall as a Service Industry Revenue (Million), by User Type 2025 & 2033

- Figure 47: Middle East Firewall as a Service Industry Revenue Share (%), by User Type 2025 & 2033

- Figure 48: Middle East Firewall as a Service Industry Revenue (Million), by Industry Vertical 2025 & 2033

- Figure 49: Middle East Firewall as a Service Industry Revenue Share (%), by Industry Vertical 2025 & 2033

- Figure 50: Middle East Firewall as a Service Industry Revenue (Million), by Country 2025 & 2033

- Figure 51: Middle East Firewall as a Service Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Firewall as a Service Industry Revenue Million Forecast, by Service Model 2020 & 2033

- Table 2: Global Firewall as a Service Industry Revenue Million Forecast, by Deployment Model 2020 & 2033

- Table 3: Global Firewall as a Service Industry Revenue Million Forecast, by User Type 2020 & 2033

- Table 4: Global Firewall as a Service Industry Revenue Million Forecast, by Industry Vertical 2020 & 2033

- Table 5: Global Firewall as a Service Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Global Firewall as a Service Industry Revenue Million Forecast, by Service Model 2020 & 2033

- Table 7: Global Firewall as a Service Industry Revenue Million Forecast, by Deployment Model 2020 & 2033

- Table 8: Global Firewall as a Service Industry Revenue Million Forecast, by User Type 2020 & 2033

- Table 9: Global Firewall as a Service Industry Revenue Million Forecast, by Industry Vertical 2020 & 2033

- Table 10: Global Firewall as a Service Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 11: United States Firewall as a Service Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Canada Firewall as a Service Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Global Firewall as a Service Industry Revenue Million Forecast, by Service Model 2020 & 2033

- Table 14: Global Firewall as a Service Industry Revenue Million Forecast, by Deployment Model 2020 & 2033

- Table 15: Global Firewall as a Service Industry Revenue Million Forecast, by User Type 2020 & 2033

- Table 16: Global Firewall as a Service Industry Revenue Million Forecast, by Industry Vertical 2020 & 2033

- Table 17: Global Firewall as a Service Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 18: United Kingdom Firewall as a Service Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Germany Firewall as a Service Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: France Firewall as a Service Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: Rest of Europe Firewall as a Service Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Global Firewall as a Service Industry Revenue Million Forecast, by Service Model 2020 & 2033

- Table 23: Global Firewall as a Service Industry Revenue Million Forecast, by Deployment Model 2020 & 2033

- Table 24: Global Firewall as a Service Industry Revenue Million Forecast, by User Type 2020 & 2033

- Table 25: Global Firewall as a Service Industry Revenue Million Forecast, by Industry Vertical 2020 & 2033

- Table 26: Global Firewall as a Service Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 27: China Firewall as a Service Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Japan Firewall as a Service Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 29: Australia Firewall as a Service Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Rest of Asia Pacific Firewall as a Service Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 31: Global Firewall as a Service Industry Revenue Million Forecast, by Service Model 2020 & 2033

- Table 32: Global Firewall as a Service Industry Revenue Million Forecast, by Deployment Model 2020 & 2033

- Table 33: Global Firewall as a Service Industry Revenue Million Forecast, by User Type 2020 & 2033

- Table 34: Global Firewall as a Service Industry Revenue Million Forecast, by Industry Vertical 2020 & 2033

- Table 35: Global Firewall as a Service Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 36: Mexico Firewall as a Service Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 37: Brazil Firewall as a Service Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: Rest of Latin America Firewall as a Service Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 39: Global Firewall as a Service Industry Revenue Million Forecast, by Service Model 2020 & 2033

- Table 40: Global Firewall as a Service Industry Revenue Million Forecast, by Deployment Model 2020 & 2033

- Table 41: Global Firewall as a Service Industry Revenue Million Forecast, by User Type 2020 & 2033

- Table 42: Global Firewall as a Service Industry Revenue Million Forecast, by Industry Vertical 2020 & 2033

- Table 43: Global Firewall as a Service Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Firewall as a Service Industry?

The projected CAGR is approximately 16.47%.

2. Which companies are prominent players in the Firewall as a Service Industry?

Key companies in the market include Check Point Software Technologies Inc, Barracuda Networks Inc, Cato Networks, Fortinet Inc, Vocus Communications, IntraSystems, Cisco Systems Inc, Microsoft Corporation, Juniper Networks Inc, Zscaler Inc , Sprout Technologies Ltd, Forcepoint.

3. What are the main segments of the Firewall as a Service Industry?

The market segments include Service Model, Deployment Model, User Type, Industry Vertical.

4. Can you provide details about the market size?

The market size is estimated to be USD 4.69 Million as of 2022.

5. What are some drivers contributing to market growth?

Enormous Growth in Cloud Based Applications; Surge in Data Breaches on Public Cloud Environment; Everchanging Firewall Protocols for Business Organisations.

6. What are the notable trends driving market growth?

Public Cloud Deployment Model is Expected to Hold Significant Market Share.

7. Are there any restraints impacting market growth?

Complexity in Integrating Hosted Firewalls with On-premise Firewalls.

8. Can you provide examples of recent developments in the market?

February 2023, WatchGuard Technologies introduced the Firebox T25/T25-W, T45/T45-POE/T45-W-POE, and T85-POE tabletop firewall appliances. These new firewalls, powered by WatchGuard's Unified Security Platform architecture that offers advanced security and easy management via WatchGuard Cloud, are designed to offer the remote and distributed business environments required for better protection against network security threats.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Firewall as a Service Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Firewall as a Service Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Firewall as a Service Industry?

To stay informed about further developments, trends, and reports in the Firewall as a Service Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence