Key Insights

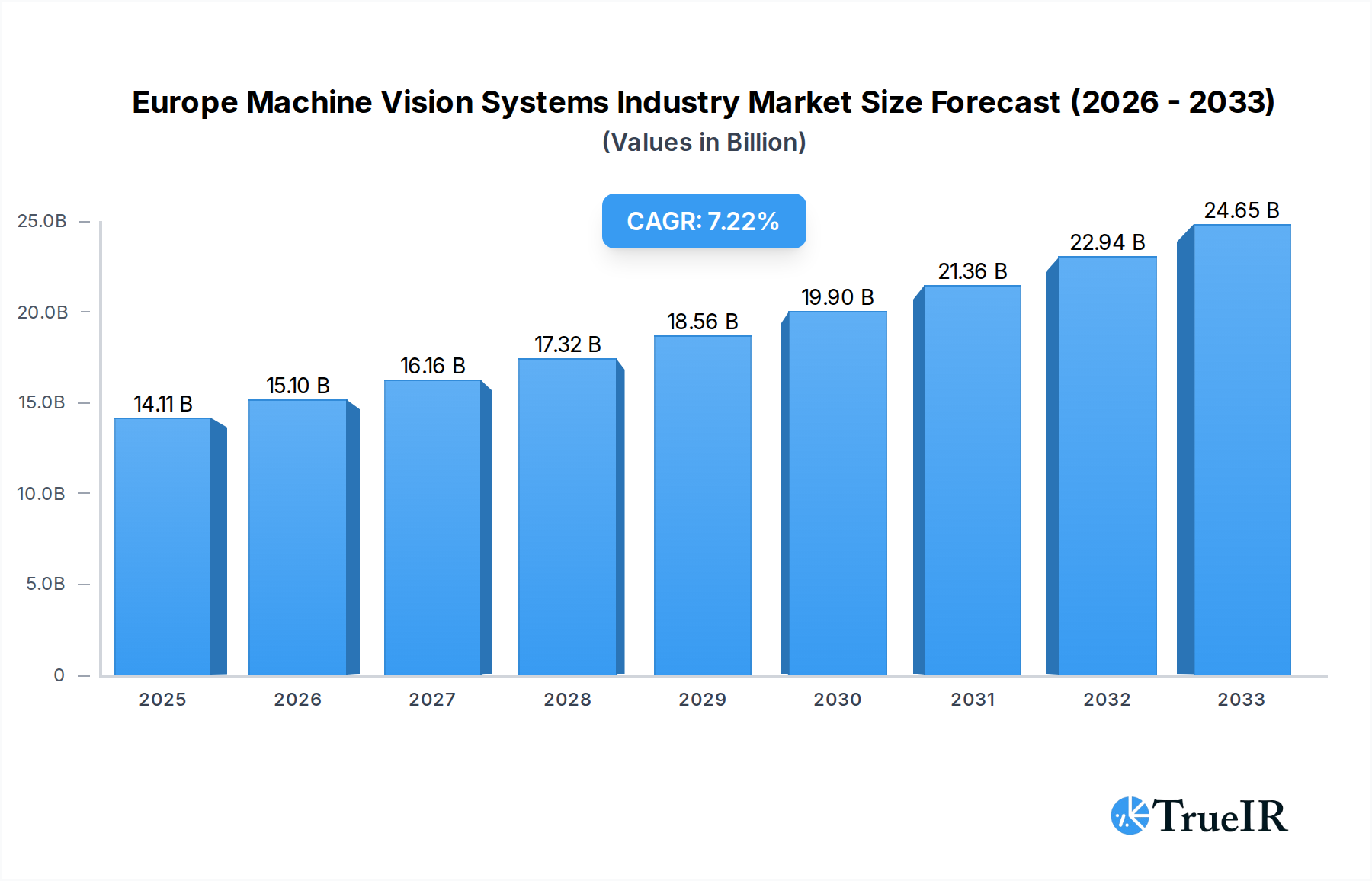

The European Machine Vision Systems market is poised for significant expansion, projected to reach an estimated $14.11 billion in 2025. This robust growth is underpinned by a compelling Compound Annual Growth Rate (CAGR) of 7% anticipated over the forecast period of 2025-2033. Several key drivers are fueling this upward trajectory, including the escalating demand for automation across diverse end-user industries and the relentless pursuit of enhanced quality control and operational efficiency. The automotive sector, with its intricate manufacturing processes and stringent quality demands, continues to be a dominant force, alongside the rapidly evolving electronics and semiconductors industry, which necessitates high-precision inspection capabilities. Furthermore, the burgeoning growth in food and beverage, healthcare and pharmaceutical, and logistics and retail sectors, driven by consumer preferences for consistent quality and efficient supply chains, is also contributing significantly to market expansion. The increasing adoption of sophisticated hardware components like advanced vision systems, high-resolution cameras, and specialized optics and illumination systems, coupled with the development of intelligent software solutions, is enabling more complex and accurate inspection tasks, further bolstering market performance.

Europe Machine Vision Systems Industry Market Size (In Billion)

The competitive landscape is characterized by a strong presence of established players like Keyence Corporation, Cognex Corporation, and Omron Corporation, who are continuously innovating and expanding their product portfolios. The market is segmented across various hardware components, including vision systems, cameras, optics, illumination systems, and frame grabbers, alongside software solutions. Product-wise, both PC-based and smart camera-based systems are witnessing considerable adoption, catering to different application needs and budget constraints. Geographically, while the provided data focuses on Europe, it highlights key markets such as the United Kingdom, Germany, France, and Italy, which are expected to remain pivotal in driving regional demand. Emerging trends like the integration of artificial intelligence (AI) and deep learning within machine vision systems are set to unlock new levels of performance in defect detection, object recognition, and process optimization, promising to further accelerate market penetration and technological advancements. Despite these positive indicators, challenges such as the initial high investment costs for sophisticated systems and the need for skilled personnel to operate and maintain them, may present some restraints to the otherwise dynamic growth trajectory.

Europe Machine Vision Systems Industry Company Market Share

This in-depth report provides a strategic overview of the Europe Machine Vision Systems Industry, analyzing its market structure, competitive landscape, key trends, and future outlook. Covering the historical period of 2019–2024, the base year of 2025, and a robust forecast period from 2025–2033, this research offers unparalleled insights into a market projected to reach billions in value. Leveraging high-volume SEO keywords, this report is designed to engage industry professionals, investors, and strategists seeking to understand and capitalize on the burgeoning opportunities within the European machine vision sector.

Europe Machine Vision Systems Industry Market Structure & Competitive Landscape

The Europe Machine Vision Systems Industry is characterized by a moderately concentrated market structure, with a blend of established global players and innovative regional specialists. Key players like Keyence Corporation, Cognex Corporation, and Omron Corporation hold significant market share, driven by their extensive product portfolios, advanced technological capabilities, and strong distribution networks. Innovation remains a primary driver, fueled by continuous advancements in artificial intelligence, deep learning, and sensor technology, enabling more sophisticated defect detection and quality control. Regulatory impacts, particularly concerning data privacy and industrial automation standards, are becoming increasingly influential, shaping product development and market access. Product substitutes, while present in the form of manual inspection or less advanced automation solutions, are rapidly losing ground to the superior efficiency and accuracy offered by machine vision. End-user segmentation reveals a diverse adoption landscape, with strong demand from sectors like Automotive and Electronics and Semiconductors. Mergers and acquisitions (M&A) activity is a notable trend, with larger entities acquiring smaller, technology-focused companies to expand their capabilities and market reach. For instance, the period has seen an estimated 15-20 significant M&A deals annually, with transaction values often reaching hundreds of millions. This consolidation aims to create comprehensive solution providers capable of addressing complex industrial challenges. The competitive intensity is high, with companies constantly vying for market leadership through product differentiation, strategic partnerships, and aggressive market penetration strategies.

Europe Machine Vision Systems Industry Market Trends & Opportunities

The Europe Machine Vision Systems Industry is experiencing a period of accelerated growth and transformation, with market size projected to surpass several hundred billion Euros by 2033. This expansion is underpinned by a confluence of technological advancements, evolving consumer preferences for higher quality products, and a relentless drive for operational efficiency across various industries. The Compound Annual Growth Rate (CAGR) for the forecast period is robust, estimated at 15-20%, signaling substantial market penetration and adoption.

Technological shifts are a paramount trend. The integration of Artificial Intelligence (AI) and Machine Learning (ML) into machine vision systems is revolutionizing capabilities. AI-powered defect detection, for example, allows for the identification of subtle flaws previously undetectable by traditional methods, even without extensive training data. This has opened up new avenues for quality control in highly sensitive sectors like pharmaceuticals and food and beverage. Furthermore, the increasing prevalence of smart cameras, offering integrated processing power, is simplifying system deployment and reducing costs for small and medium-sized enterprises (SMEs). The miniaturization and enhanced resolution of cameras, coupled with advancements in optics and illumination systems, are enabling more precise and faster inspections, even in challenging environments.

Consumer preferences are indirectly influencing the machine vision market. As consumers demand higher quality, safer, and more consistent products, manufacturers are compelled to adopt advanced inspection and quality assurance technologies like machine vision. This is particularly evident in the automotive sector, where stringent safety standards and the increasing complexity of vehicle components necessitate sophisticated inspection processes. Similarly, in the healthcare and pharmaceutical industries, the need for absolute product integrity and regulatory compliance drives the demand for high-precision vision systems.

Competitive dynamics are intensifying. While established players continue to innovate and expand their offerings, new entrants, particularly those specializing in niche AI applications or advanced software solutions, are gaining traction. Strategic collaborations between hardware manufacturers, software developers, and system integrators are becoming more common, fostering the development of end-to-end solutions. The push towards Industry 4.0 and smart factories is a significant opportunity, with machine vision systems playing a central role in data acquisition, process optimization, and automation. The growing adoption of robotics, which often relies on machine vision for guidance and object recognition, further amplifies this opportunity. The increasing focus on sustainability and traceability also presents opportunities, as machine vision can be used to monitor production processes, reduce waste, and ensure compliance with environmental regulations. The market penetration rate for advanced machine vision solutions is expected to grow significantly, moving from an estimated 45% in 2025 to over 70% by 2033 in key industrial sectors.

Dominant Markets & Segments in Europe Machine Vision Systems Industry

The dominance within the Europe Machine Vision Systems Industry is multifaceted, with key regions, countries, and specific segments exhibiting exceptional growth and market penetration. Geographically, Germany stands out as a leading market, driven by its robust automotive and electronics manufacturing sectors, coupled with a strong emphasis on industrial automation and research & development. The United Kingdom and France also represent significant markets, with growing adoption in diverse end-user industries.

From a component perspective, Hardware continues to be the dominant segment, accounting for an estimated 70-75% of the total market value. Within hardware, Vision Systems themselves, which encompass integrated hardware and software solutions, command a substantial share. Cameras are a critical and rapidly evolving sub-segment, with advancements in resolution, speed, and specialized sensor technologies driving demand. Optics and Illumination Systems are also crucial, enabling the capture of high-quality images for accurate analysis. The Frame Grabber segment, while mature, remains essential for high-speed data acquisition in demanding applications. The Software segment is experiencing the fastest growth, with an estimated CAGR of 18-22%, fueled by the increasing sophistication of AI/ML algorithms, image processing libraries, and user-friendly development platforms.

In terms of product type, PC-based vision systems, offering flexibility and powerful processing capabilities, continue to hold a significant market share, particularly in complex applications. However, Smart Camera-based systems are rapidly gaining ground due to their ease of integration, lower cost, and suitability for embedded applications and decentralized processing.

The End-User Industry landscape reveals diverse adoption patterns. The Automotive industry remains a primary driver, utilizing machine vision for quality inspection of components, assembly verification, and robot guidance. The Electronics and Semiconductors sector is another major consumer, employing vision systems for precise placement, defect detection, and testing of intricate components. The Food and Beverage industry is witnessing significant growth, driven by the need for enhanced food safety, quality control, and packaging inspection. The Healthcare and Pharmaceutical industry, while having a smaller current market share, is exhibiting the highest growth potential due to stringent regulatory requirements and the demand for sterile, defect-free products. The Logistic and Retail sector is also increasingly adopting machine vision for automated sorting, package identification, and inventory management.

Key growth drivers for these dominant segments include:

- Infrastructure Development: Investments in smart manufacturing facilities and Industry 4.0 initiatives across Europe.

- Government Policies and Initiatives: Support for automation, digitalization, and advanced manufacturing technologies through grants and funding programs.

- Technological Advancements: Continuous innovation in AI, deep learning, sensor technology, and processing power, making vision systems more capable and cost-effective.

- Increasing Labor Costs and Shortages: The need to automate repetitive and labor-intensive tasks to maintain competitiveness.

- Stringent Quality and Safety Regulations: Mandates for higher product quality and safety in sectors like automotive, healthcare, and food production.

- Growing Demand for Traceability and Data Analytics: Machine vision systems provide crucial data for process optimization and supply chain visibility.

Europe Machine Vision Systems Industry Product Analysis

Product innovations in the Europe Machine Vision Systems Industry are primarily centered on enhancing accuracy, speed, and ease of use. The integration of artificial intelligence and deep learning algorithms is leading to systems capable of sophisticated defect detection, anomaly identification, and predictive maintenance, often without extensive prior training data. For instance, the development of AI-powered defect detection that simulates human sensibility is a significant advancement. Applications are expanding beyond traditional quality control to encompass robot guidance, automated assembly verification, and complex measurement tasks. Competitive advantages are being gained through solutions offering higher resolution, faster processing speeds, broader spectral imaging capabilities, and robust integration with existing industrial automation platforms. The market fit is improving with the development of more compact, cost-effective, and user-friendly smart camera systems suitable for a wider range of SMEs and specialized applications, thereby democratizing access to advanced vision technology.

Key Drivers, Barriers & Challenges in Europe Machine Vision Systems Industry

The Europe Machine Vision Systems Industry is propelled by significant drivers. Technological Advancements, particularly in AI, deep learning, and sensor technology, enable more sophisticated and accurate inspection capabilities. The Increasing Demand for Quality and Consistency across industries, driven by consumer expectations and regulatory mandates, is a primary catalyst. Automation and Industry 4.0 Initiatives are fueling the adoption of machine vision as a core component of smart factories. Labor Shortages and Rising Labor Costs further incentivize automation. Policy-driven factors, such as government support for digitalization and advanced manufacturing, also play a crucial role.

However, the industry faces substantial barriers and challenges. High Initial Investment Costs can be a restraint for some SMEs, despite decreasing system prices. Complexity of Integration and Technical Expertise Requirements necessitate skilled personnel, posing a challenge for smaller companies. Data Security and Privacy Concerns, especially with the increasing collection of sensitive production data, require robust solutions. Supply Chain Disruptions, as witnessed in recent years, can impact the availability of critical components. Regulatory Hurdles, although often driving adoption, can also add complexity in terms of compliance for specific applications. Competitive pressures from both established players and emerging technology providers can also pose challenges.

Growth Drivers in the Europe Machine Vision Systems Industry Market

The Europe Machine Vision Systems Industry is experiencing robust growth driven by several key factors. Technological innovation, especially in artificial intelligence and deep learning, is continuously enhancing the capabilities of vision systems, enabling more complex and precise applications. The widespread adoption of Industry 4.0 and smart manufacturing initiatives across European nations positions machine vision as a fundamental technology for data-driven optimization and automation. Increasingly stringent quality and safety standards in sectors like automotive, healthcare, and food & beverage necessitate higher levels of inspection accuracy and reliability. Furthermore, the ongoing global trend towards automation to address labor shortages and rising labor costs is a significant economic driver. Government support and funding for digitalization and advanced manufacturing within the EU and individual member states also contribute to market expansion, encouraging greater investment in these technologies.

Challenges Impacting Europe Machine Vision Systems Industry Growth

Despite the strong growth trajectory, several challenges impact the Europe Machine Vision Systems Industry. The high initial investment required for sophisticated systems can be a significant barrier for small and medium-sized enterprises (SMEs), limiting their adoption. A shortage of skilled personnel with the expertise to implement, operate, and maintain advanced machine vision systems can hinder widespread deployment. The increasing complexity of cybersecurity threats poses a risk to the sensitive production data collected by these systems, demanding robust security measures. Supply chain volatility and component shortages, as experienced in recent years, can disrupt production and delay project timelines. Additionally, navigating diverse regulatory landscapes across different European countries can add complexity and cost for manufacturers aiming for pan-European market reach.

Key Players Shaping the Europe Machine Vision Systems Industry Market

- Keyence Corporation

- IDS Imaging Development Systems GmbH

- National Instruments Corporation

- Cognex Corporation

- Omron Corporation

- Uss Vision Inc

- Perceptron Inc

- Teledyne DALSA

- Datalogic SpA

- Basler AG

Significant Europe Machine Vision Systems Industry Industry Milestones

- September 2020: Omron introduced a new FH Series Vision system, which includes the industry's first defect detection AI technology, which detects defects without learning samples. The artificial intelligence technology, which attempts to simulate sensibility and skilled inspector techniques, reliably detects previously complex defects, automating human vision-based visual inspection.

Future Outlook for Europe Machine Vision Systems Industry Market

The future outlook for the Europe Machine Vision Systems Industry is exceptionally bright, with continued strong growth anticipated. Key growth catalysts include the further maturation and integration of AI and deep learning, leading to more autonomous and intelligent vision systems capable of complex decision-making. The increasing adoption of robotic automation, which heavily relies on machine vision for guidance and interaction, will significantly drive demand. Expansion into emerging end-user industries and novel applications, such as smart agriculture and advanced packaging solutions, presents substantial market potential. The drive towards greater sustainability and circular economy principles will also foster the use of machine vision for process optimization, waste reduction, and enhanced traceability. Strategic opportunities lie in developing comprehensive, end-to-end solutions that address specific industry pain points and in fostering partnerships that accelerate innovation and market penetration, particularly for SMEs looking to leverage these advanced technologies.

Europe Machine Vision Systems Industry Segmentation

-

1. Component

-

1.1. Hardware

- 1.1.1. Vision Systems

- 1.1.2. Cameras

- 1.1.3. Optics and Illumination Systems

- 1.1.4. Frame Grabber

- 1.1.5. Other Types of Hardware

- 1.2. Software

-

1.1. Hardware

-

2. Product

- 2.1. PC-based

- 2.2. Smart Camera-based

-

3. End-User Industry

- 3.1. Food and Beverage

- 3.2. Healthcare and Pharmaceutical

- 3.3. Logistic and Retail

- 3.4. Automotive

- 3.5. Electronics and Semiconductors

- 3.6. Other End-user Industries

Europe Machine Vision Systems Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Machine Vision Systems Industry Regional Market Share

Geographic Coverage of Europe Machine Vision Systems Industry

Europe Machine Vision Systems Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Component

- 5.1.1. Hardware

- 5.1.1.1. Vision Systems

- 5.1.1.2. Cameras

- 5.1.1.3. Optics and Illumination Systems

- 5.1.1.4. Frame Grabber

- 5.1.1.5. Other Types of Hardware

- 5.1.2. Software

- 5.1.1. Hardware

- 5.2. Market Analysis, Insights and Forecast - by Product

- 5.2.1. PC-based

- 5.2.2. Smart Camera-based

- 5.3. Market Analysis, Insights and Forecast - by End-User Industry

- 5.3.1. Food and Beverage

- 5.3.2. Healthcare and Pharmaceutical

- 5.3.3. Logistic and Retail

- 5.3.4. Automotive

- 5.3.5. Electronics and Semiconductors

- 5.3.6. Other End-user Industries

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Component

- 6. Europe Machine Vision Systems Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Component

- 6.1.1. Hardware

- 6.1.1.1. Vision Systems

- 6.1.1.2. Cameras

- 6.1.1.3. Optics and Illumination Systems

- 6.1.1.4. Frame Grabber

- 6.1.1.5. Other Types of Hardware

- 6.1.2. Software

- 6.1.1. Hardware

- 6.2. Market Analysis, Insights and Forecast - by Product

- 6.2.1. PC-based

- 6.2.2. Smart Camera-based

- 6.3. Market Analysis, Insights and Forecast - by End-User Industry

- 6.3.1. Food and Beverage

- 6.3.2. Healthcare and Pharmaceutical

- 6.3.3. Logistic and Retail

- 6.3.4. Automotive

- 6.3.5. Electronics and Semiconductors

- 6.3.6. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Component

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Keyence Corporation

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 IDS Imaging Development Systems GmbH

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 National Instruments Corporation

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Cognex Corporation

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Omron Corporation

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Uss Vision Inc

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Perceptron Inc

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Teledyne DALSA

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Datalogic SpA

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Basler AG

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Keyence Corporation

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe Machine Vision Systems Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Europe Machine Vision Systems Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Machine Vision Systems Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 2: Europe Machine Vision Systems Industry Volume K Unit Forecast, by Component 2020 & 2033

- Table 3: Europe Machine Vision Systems Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 4: Europe Machine Vision Systems Industry Volume K Unit Forecast, by Product 2020 & 2033

- Table 5: Europe Machine Vision Systems Industry Revenue billion Forecast, by End-User Industry 2020 & 2033

- Table 6: Europe Machine Vision Systems Industry Volume K Unit Forecast, by End-User Industry 2020 & 2033

- Table 7: Europe Machine Vision Systems Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 8: Europe Machine Vision Systems Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 9: Europe Machine Vision Systems Industry Revenue billion Forecast, by Component 2020 & 2033

- Table 10: Europe Machine Vision Systems Industry Volume K Unit Forecast, by Component 2020 & 2033

- Table 11: Europe Machine Vision Systems Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 12: Europe Machine Vision Systems Industry Volume K Unit Forecast, by Product 2020 & 2033

- Table 13: Europe Machine Vision Systems Industry Revenue billion Forecast, by End-User Industry 2020 & 2033

- Table 14: Europe Machine Vision Systems Industry Volume K Unit Forecast, by End-User Industry 2020 & 2033

- Table 15: Europe Machine Vision Systems Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Europe Machine Vision Systems Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 17: United Kingdom Europe Machine Vision Systems Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: United Kingdom Europe Machine Vision Systems Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 19: Germany Europe Machine Vision Systems Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Europe Machine Vision Systems Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 21: France Europe Machine Vision Systems Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: France Europe Machine Vision Systems Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 23: Italy Europe Machine Vision Systems Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Italy Europe Machine Vision Systems Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 25: Spain Europe Machine Vision Systems Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Spain Europe Machine Vision Systems Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 27: Netherlands Europe Machine Vision Systems Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Netherlands Europe Machine Vision Systems Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 29: Belgium Europe Machine Vision Systems Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Belgium Europe Machine Vision Systems Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 31: Sweden Europe Machine Vision Systems Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Sweden Europe Machine Vision Systems Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 33: Norway Europe Machine Vision Systems Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Norway Europe Machine Vision Systems Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 35: Poland Europe Machine Vision Systems Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Poland Europe Machine Vision Systems Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 37: Denmark Europe Machine Vision Systems Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: Denmark Europe Machine Vision Systems Industry Volume (K Unit) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Machine Vision Systems Industry?

The projected CAGR is approximately 7%.

2. Which companies are prominent players in the Europe Machine Vision Systems Industry?

Key companies in the market include Keyence Corporation, IDS Imaging Development Systems GmbH, National Instruments Corporation, Cognex Corporation, Omron Corporation, Uss Vision Inc, Perceptron Inc, Teledyne DALSA, Datalogic SpA, Basler AG.

3. What are the main segments of the Europe Machine Vision Systems Industry?

The market segments include Component, Product, End-User Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 14.11 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Need for Quality Inspection and Automation; Rising Demand for Accurate Defect Detection.

6. What are the notable trends driving market growth?

Automotive Industry to Witness Significant Growth.

7. Are there any restraints impacting market growth?

Scarcity of Flexible Machine Vision Solutions.

8. Can you provide examples of recent developments in the market?

September 2020 - Omron introduced a new FH Series Vision system, which includes the industry's first defect detection AI technology, which detects defects without learning samples. The artificial intelligence technology, which attempts to simulate sensibility and skilled inspector techniques, reliably detects previously complex defects, automating human vision-based visual inspection.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Machine Vision Systems Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Machine Vision Systems Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Machine Vision Systems Industry?

To stay informed about further developments, trends, and reports in the Europe Machine Vision Systems Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence