Key Insights

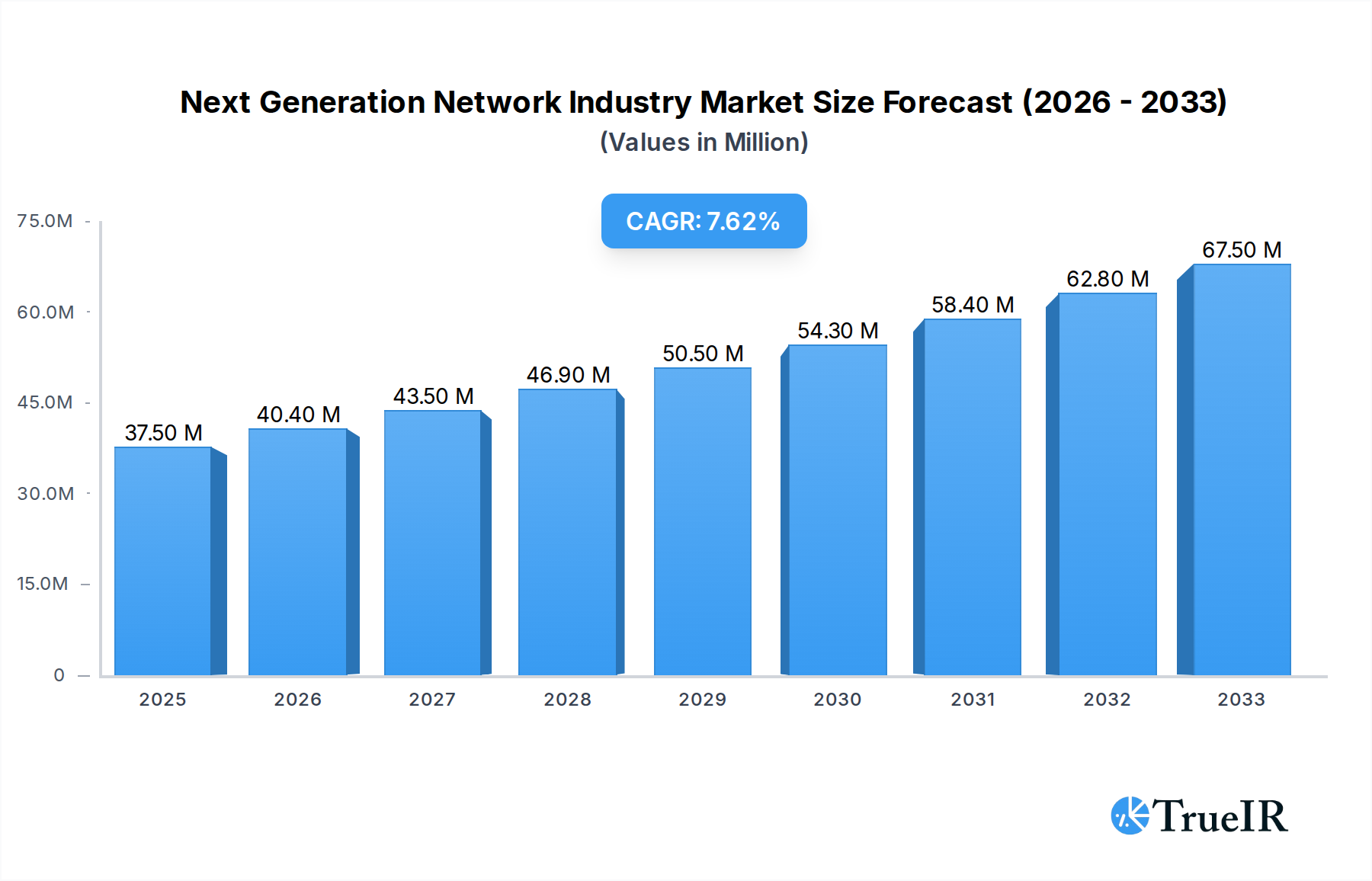

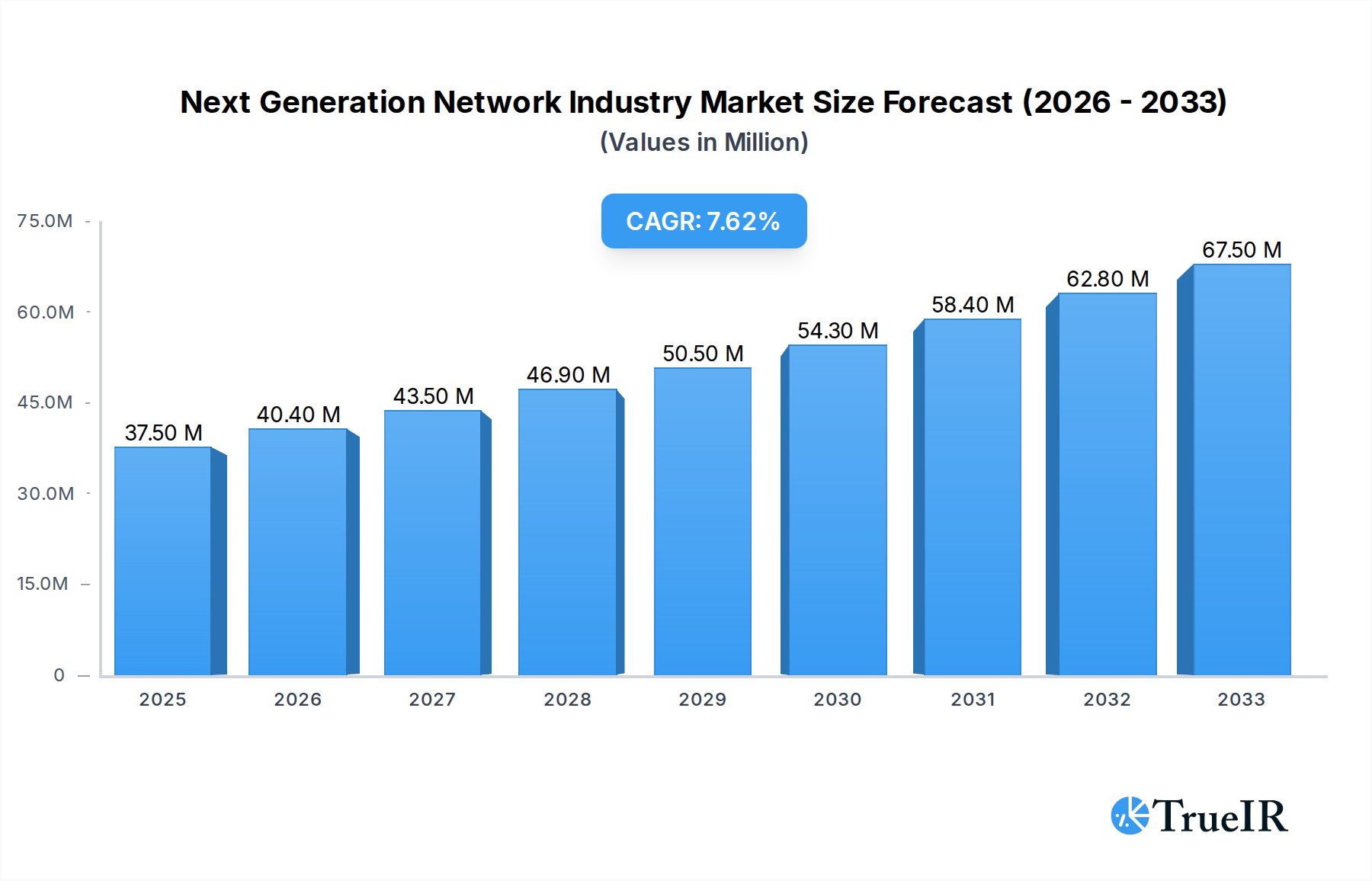

The global Next Generation Network (NGN) market is poised for robust expansion, projecting a market size of 30.55 million units and a Compound Annual Growth Rate (CAGR) of 7.70% from 2019 to 2033. This significant growth is propelled by a confluence of factors, primarily the escalating demand for high-speed, reliable, and scalable network infrastructures across diverse industries. Key drivers include the widespread adoption of 5G technology, the proliferation of the Internet of Things (IoT) devices, and the increasing need for enhanced communication services driven by remote work, online education, and immersive digital experiences. The market's trajectory is further bolstered by ongoing advancements in network virtualization, software-defined networking (SDN), and network function virtualization (NFV), which are crucial enablers for flexible and efficient network management. These technological shifts are instrumental in transforming legacy networks into dynamic and agile platforms capable of supporting the ever-growing data traffic and diverse service requirements of the digital age.

Next Generation Network Industry Market Size (In Million)

The NGN market is segmented by offering, with hardware, software, and services all playing critical roles in the ecosystem. Telecom and Internet Service Providers (ISPs) represent the dominant end-user segment, investing heavily in upgrading their infrastructure to meet evolving customer demands. Government initiatives aimed at digital transformation and smart city development also contribute significantly to market growth, alongside adoption by "Other End-users" such as enterprises and research institutions. However, the market is not without its challenges. High initial investment costs for NGN deployment, coupled with complex integration processes and evolving cybersecurity threats, present considerable restraints. Nonetheless, the compelling advantages of NGNs in terms of improved performance, cost-efficiency, and enhanced user experience are expected to outweigh these obstacles, driving sustained innovation and adoption across the globe.

Next Generation Network Industry Company Market Share

Next Generation Network Industry Market Structure & Competitive Landscape

The next-generation network industry is characterized by a highly concentrated market, with a significant portion of market share held by a few dominant players, including IBM Corporation, Samsung Electronics Co Ltd, Cisco Systems Inc, Juniper Networks Inc, Telefonaktiebolaget LM Ericsso, NEC Corporation, Huawei Technologies Co Ltd, ZTE Corporation, Nokia Corporation, and Ciena Corporation. Innovation drivers are paramount, fueled by the relentless pursuit of higher bandwidth, lower latency, and enhanced connectivity. Key technological advancements in 5G, Wi-Fi 7, and AI-powered network management are reshaping the competitive landscape. Regulatory impacts, while sometimes creating hurdles, also foster opportunities for standardization and fair competition, especially concerning spectrum allocation and data privacy. Product substitutes are emerging, particularly in areas like private LTE/5G networks that offer alternatives to traditional fixed broadband for enterprises. End-user segmentation reveals a strong reliance on Telecom and Internet Service Providers, with growing adoption by Government entities and a diverse range of Other End-users seeking advanced connectivity solutions. Mergers and acquisitions (M&A) trends indicate a strategic consolidation to gain market access, acquire new technologies, and achieve economies of scale. Over the historical period (2019-2024), M&A activities have seen an average of approximately 25 significant transactions annually, with a combined deal value exceeding $50 Billion. The Herfindahl-Hirschman Index (HHI) for the core network equipment segment is estimated to be around 2,500, indicating a highly concentrated market.

Next Generation Network Industry Market Trends & Opportunities

The next-generation network industry is poised for exponential growth, driven by a projected market size expansion to over $700 Billion by 2033. The CAGR for the forecast period (2025–2033) is estimated at a robust 18.5%. This growth is underpinned by a confluence of technological shifts, fundamentally altering how data is transmitted and consumed. The widespread deployment of 5G technology continues to be a primary catalyst, enabling new use cases such as enhanced mobile broadband, ultra-reliable low-latency communications, and massive machine-type communications. Simultaneously, the evolution towards Wi-Fi 7 is set to revolutionize indoor wireless connectivity, offering multi-gigabit speeds and improved capacity, as evidenced by Charter Communications' collaboration with Qualcomm Technologies for next-generation Wi-Fi routers. Consumer preferences are increasingly dictating the demand for seamless, high-performance connectivity, impacting everything from streaming services and online gaming to the burgeoning metaverse and augmented reality applications. This necessitates networks that can handle immense data volumes and deliver near-instantaneous response times.

Competitive dynamics are intensifying, with established players investing heavily in R&D to maintain their edge and new entrants seeking to disrupt the market with innovative solutions. The shift towards software-defined networking (SDN) and network function virtualization (NFV) is enabling greater flexibility, agility, and cost-efficiency in network operations. Furthermore, the integration of artificial intelligence (AI) and machine learning (ML) is optimizing network performance, predictive maintenance, and security. Edge computing is another significant trend, pushing processing power closer to the data source, which is crucial for latency-sensitive applications. The ongoing digital transformation across industries, including manufacturing, healthcare, and transportation, is creating substantial demand for reliable and advanced networking infrastructure. The adoption of private 5G networks by enterprises for enhanced operational control and efficiency presents a significant opportunity. The increasing focus on open and interoperable network architectures, exemplified by Schneider Electric's collaboration with Intel and Red Hat on a Distributed Control Node (DCN) software framework, is also fostering innovation and reducing vendor lock-in. This trend is particularly relevant for industrial automation, where real-time control and data processing are critical. The market penetration rate for advanced networking technologies, while varying by region and segment, is steadily increasing, indicating a broad societal and economic reliance on next-generation connectivity.

Dominant Markets & Segments in Next Generation Network Industry

The next-generation network industry's dominance is clearly established within the Telecom and Internet Service Providers end-user segment. This segment is the primary adopter and deployer of advanced network infrastructure, investing heavily in 5G, fiber optic expansion, and next-generation core network technologies. Key growth drivers within this segment include the escalating demand for high-speed broadband, the need to support an ever-increasing number of connected devices (IoT), and the delivery of new revenue-generating services like private enterprise networks and enhanced mobile broadband. Policies promoting digital inclusion and the expansion of high-speed internet access across both urban and rural areas further bolster this segment's dominance.

Within the Offering breakdown, Hardware continues to be a foundational segment, encompassing essential components like routers, switches, base stations, and fiber optic cables. However, the Software segment is witnessing explosive growth, driven by the increasing sophistication of network management, orchestration, and security solutions. Software-defined networking (SDN) and network function virtualization (NFV) are pivotal, allowing for greater agility and automation. The Services segment, including network integration, managed services, and consulting, is also experiencing substantial expansion as organizations increasingly rely on external expertise to design, deploy, and maintain complex next-generation networks.

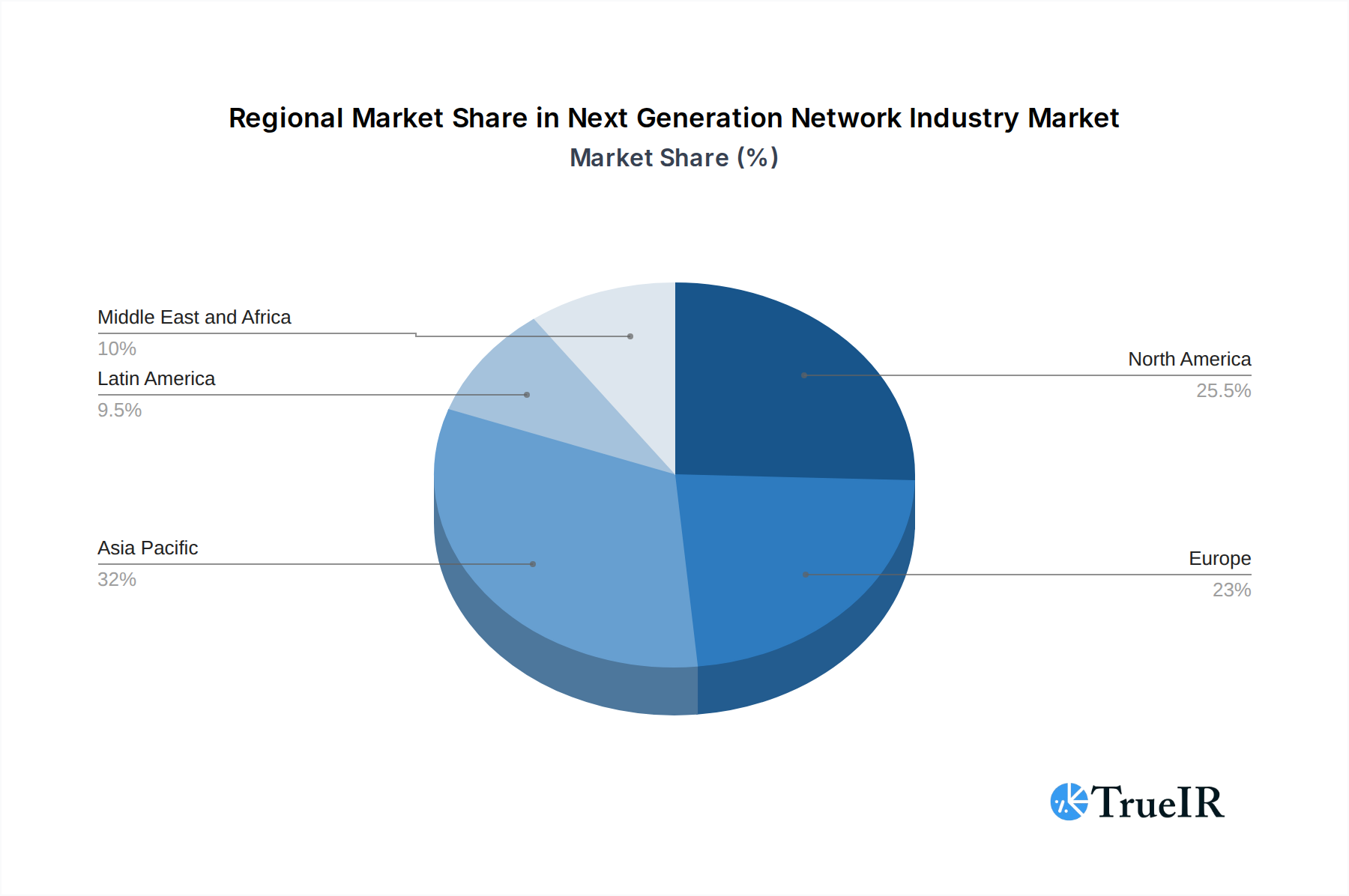

Geographically, North America and Asia Pacific are identified as dominant markets. North America benefits from significant private sector investment, robust regulatory support for broadband expansion, and a high concentration of technological innovation. The United States, in particular, is a leader in 5G deployment and fiber build-out. Asia Pacific, led by countries like China and South Korea, is characterized by rapid infrastructure development, a massive consumer base driving demand, and strong government initiatives supporting digital transformation and 5G adoption. The sheer scale of population and the aggressive rollout of advanced network technologies in these regions underscore their leading positions. The Government segment, while smaller in overall market value compared to Telecom and Internet Service Providers, is a critical influencer, driving demand for secure and resilient networks for defense, public safety, and smart city initiatives.

Next Generation Network Industry Product Analysis

Next-generation network products are characterized by cutting-edge technological advancements aimed at delivering unprecedented speed, capacity, and intelligence. Innovations in 5G NR (New Radio) and Wi-Fi 7 are at the forefront, enabling multi-gigabit per second speeds and ultra-low latency for a seamless, immersive user experience. The integration of AI and machine learning into network hardware and software is a key competitive advantage, facilitating automated network management, predictive maintenance, and enhanced cybersecurity. Examples include distributed control nodes for industrial automation and advanced Wi-Fi routers capable of supporting high-bandwidth applications. These products are designed for optimal performance in diverse environments, from dense urban areas to critical industrial settings, ensuring reliability and scalability.

Key Drivers, Barriers & Challenges in Next Generation Network Industry

Key Drivers:

- Technological Advancements: The continuous evolution of 5G, Wi-Fi 7, AI, and edge computing is a primary propeller, enabling new applications and services.

- Increasing Data Demand: The exponential growth in data consumption from video streaming, IoT devices, and cloud services necessitates higher bandwidth and lower latency.

- Digital Transformation Initiatives: Government and enterprise-led digital transformation efforts across various sectors are creating substantial demand for advanced network infrastructure.

- Economic Growth & Investment: Significant investments from both public and private sectors in network upgrades and expansions are fueling market growth.

Barriers & Challenges:

- High Infrastructure Deployment Costs: The capital expenditure required for deploying next-generation networks, particularly 5G and fiber, remains a significant barrier.

- Regulatory Hurdles and Spectrum Allocation: Navigating complex regulatory frameworks and securing sufficient spectrum licenses can be time-consuming and costly.

- Cybersecurity Threats: The expanded attack surface of next-generation networks presents complex cybersecurity challenges, requiring robust and evolving security solutions.

- Skilled Workforce Shortage: A lack of adequately trained professionals to design, deploy, and manage these advanced networks poses a restraint on rapid expansion.

- Supply Chain Disruptions: Global supply chain vulnerabilities can impact the availability and cost of critical network components, estimated to cause potential project delays of up to 15% in affected periods.

Growth Drivers in the Next Generation Network Industry Market

The growth drivers in the next-generation network industry market are multifaceted, primarily propelled by rapid technological advancements such as the widespread adoption of 5G technology, the emergence of Wi-Fi 7, and the integration of Artificial Intelligence (AI) in network management. The increasing demand for enhanced mobile broadband, ultra-reliable low-latency communications (URLLC), and massive machine-type communications (mMTC) from consumers and enterprises alike is a significant economic factor. Government initiatives promoting digital transformation, smart city development, and universal broadband access are also crucial regulatory drivers. Furthermore, the growing prevalence of the Internet of Things (IoT) across various industries, from manufacturing to healthcare, necessitates the deployment of robust and high-performance networks.

Challenges Impacting Next Generation Network Industry Growth

Challenges impacting next-generation network industry growth include the substantial capital investment required for infrastructure deployment, estimated at over $1 Million per square mile for comprehensive 5G coverage in certain regions. Regulatory complexities and the time-consuming process of spectrum allocation can also create significant delays. Supply chain issues, as seen with semiconductor shortages, can lead to increased costs and longer lead times for critical network equipment, potentially impacting project timelines by 10-20%. Moreover, the escalating cybersecurity threats associated with a more interconnected landscape demand continuous investment in robust security measures. Intense competitive pressures among established players and emerging startups also necessitate constant innovation and aggressive pricing strategies.

Key Players Shaping the Next Generation Network Industry Market

- IBM Corporation

- Samsung Electronics Co Ltd

- Cisco Systems Inc

- Juniper Networks Inc

- Telefonaktiebolaget LM Ericsso

- NEC Corporation

- Huawei Technologies Co Ltd

- ZTE Corporation

- Nokia Corporation

- Ciena Corporation

Significant Next Generation Network Industry Industry Milestones

- February 2024: Schneider Electric, in collaboration with Intel and Red Hat, released a Distributed Control Node (DCN) software framework. This expansion of their EcoStruxure Automation Expert allows industrial companies to adopt a software-defined, plug-and-produce solution, enhancing operations, quality, and cost optimization.

- September 2023: Charter Communications Inc. partnered with Qualcomm Technologies Inc. to deliver next-generation advanced Wi-Fi routers featuring Wi-Fi 7 and 10 Gbps capabilities. This initiative aims to enhance the converged connectivity experience for residential and SMB customers, supporting immersive VR and multi-gig wireless connectivity.

Future Outlook for Next Generation Network Industry Market

The future outlook for the next-generation network industry market is exceptionally bright, driven by sustained demand for ubiquitous, high-speed, and low-latency connectivity. Strategic opportunities lie in the continued expansion of 5G and the adoption of 6G technologies, the proliferation of edge computing solutions for real-time data processing, and the increasing integration of AI for intelligent network management. The growing adoption of private networks by enterprises and the advancement of applications like the metaverse and autonomous systems will further fuel market growth, projecting a market value exceeding $900 Billion by 2033. The industry's capacity to innovate and adapt to evolving technological landscapes and user demands will be critical in realizing its full potential.

Next Generation Network Industry Segmentation

-

1. Offering

- 1.1. Hardware

- 1.2. Software

- 1.3. Services

-

2. End User

- 2.1. Telecom and Internet Service Providers

- 2.2. Government

- 2.3. Other End-users

Next Generation Network Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East and Africa

Next Generation Network Industry Regional Market Share

Geographic Coverage of Next Generation Network Industry

Next Generation Network Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.70% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Offering

- 5.1.1. Hardware

- 5.1.2. Software

- 5.1.3. Services

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Telecom and Internet Service Providers

- 5.2.2. Government

- 5.2.3. Other End-users

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Latin America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Offering

- 6. Global Next Generation Network Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Offering

- 6.1.1. Hardware

- 6.1.2. Software

- 6.1.3. Services

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Telecom and Internet Service Providers

- 6.2.2. Government

- 6.2.3. Other End-users

- 6.1. Market Analysis, Insights and Forecast - by Offering

- 7. North America Next Generation Network Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Offering

- 7.1.1. Hardware

- 7.1.2. Software

- 7.1.3. Services

- 7.2. Market Analysis, Insights and Forecast - by End User

- 7.2.1. Telecom and Internet Service Providers

- 7.2.2. Government

- 7.2.3. Other End-users

- 7.1. Market Analysis, Insights and Forecast - by Offering

- 8. Europe Next Generation Network Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Offering

- 8.1.1. Hardware

- 8.1.2. Software

- 8.1.3. Services

- 8.2. Market Analysis, Insights and Forecast - by End User

- 8.2.1. Telecom and Internet Service Providers

- 8.2.2. Government

- 8.2.3. Other End-users

- 8.1. Market Analysis, Insights and Forecast - by Offering

- 9. Asia Pacific Next Generation Network Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Offering

- 9.1.1. Hardware

- 9.1.2. Software

- 9.1.3. Services

- 9.2. Market Analysis, Insights and Forecast - by End User

- 9.2.1. Telecom and Internet Service Providers

- 9.2.2. Government

- 9.2.3. Other End-users

- 9.1. Market Analysis, Insights and Forecast - by Offering

- 10. Latin America Next Generation Network Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Offering

- 10.1.1. Hardware

- 10.1.2. Software

- 10.1.3. Services

- 10.2. Market Analysis, Insights and Forecast - by End User

- 10.2.1. Telecom and Internet Service Providers

- 10.2.2. Government

- 10.2.3. Other End-users

- 10.1. Market Analysis, Insights and Forecast - by Offering

- 11. Middle East and Africa Next Generation Network Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Offering

- 11.1.1. Hardware

- 11.1.2. Software

- 11.1.3. Services

- 11.2. Market Analysis, Insights and Forecast - by End User

- 11.2.1. Telecom and Internet Service Providers

- 11.2.2. Government

- 11.2.3. Other End-users

- 11.1. Market Analysis, Insights and Forecast - by Offering

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 IBM Corporation

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Samsung Electronics Co Ltd

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Cisco Systems Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Juniper Networks Inc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Telefonaktiebolaget LM Ericsso

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 NEC Corporation

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Huawei Technologies Co Ltd

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 ZTE Corporation

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Nokia Corporation

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Ciena Corporation

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 IBM Corporation

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Next Generation Network Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Next Generation Network Industry Revenue (Million), by Offering 2025 & 2033

- Figure 3: North America Next Generation Network Industry Revenue Share (%), by Offering 2025 & 2033

- Figure 4: North America Next Generation Network Industry Revenue (Million), by End User 2025 & 2033

- Figure 5: North America Next Generation Network Industry Revenue Share (%), by End User 2025 & 2033

- Figure 6: North America Next Generation Network Industry Revenue (Million), by Country 2025 & 2033

- Figure 7: North America Next Generation Network Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Next Generation Network Industry Revenue (Million), by Offering 2025 & 2033

- Figure 9: Europe Next Generation Network Industry Revenue Share (%), by Offering 2025 & 2033

- Figure 10: Europe Next Generation Network Industry Revenue (Million), by End User 2025 & 2033

- Figure 11: Europe Next Generation Network Industry Revenue Share (%), by End User 2025 & 2033

- Figure 12: Europe Next Generation Network Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Europe Next Generation Network Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Next Generation Network Industry Revenue (Million), by Offering 2025 & 2033

- Figure 15: Asia Pacific Next Generation Network Industry Revenue Share (%), by Offering 2025 & 2033

- Figure 16: Asia Pacific Next Generation Network Industry Revenue (Million), by End User 2025 & 2033

- Figure 17: Asia Pacific Next Generation Network Industry Revenue Share (%), by End User 2025 & 2033

- Figure 18: Asia Pacific Next Generation Network Industry Revenue (Million), by Country 2025 & 2033

- Figure 19: Asia Pacific Next Generation Network Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Latin America Next Generation Network Industry Revenue (Million), by Offering 2025 & 2033

- Figure 21: Latin America Next Generation Network Industry Revenue Share (%), by Offering 2025 & 2033

- Figure 22: Latin America Next Generation Network Industry Revenue (Million), by End User 2025 & 2033

- Figure 23: Latin America Next Generation Network Industry Revenue Share (%), by End User 2025 & 2033

- Figure 24: Latin America Next Generation Network Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Latin America Next Generation Network Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Next Generation Network Industry Revenue (Million), by Offering 2025 & 2033

- Figure 27: Middle East and Africa Next Generation Network Industry Revenue Share (%), by Offering 2025 & 2033

- Figure 28: Middle East and Africa Next Generation Network Industry Revenue (Million), by End User 2025 & 2033

- Figure 29: Middle East and Africa Next Generation Network Industry Revenue Share (%), by End User 2025 & 2033

- Figure 30: Middle East and Africa Next Generation Network Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: Middle East and Africa Next Generation Network Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Next Generation Network Industry Revenue Million Forecast, by Offering 2020 & 2033

- Table 2: Global Next Generation Network Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 3: Global Next Generation Network Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Next Generation Network Industry Revenue Million Forecast, by Offering 2020 & 2033

- Table 5: Global Next Generation Network Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 6: Global Next Generation Network Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: Global Next Generation Network Industry Revenue Million Forecast, by Offering 2020 & 2033

- Table 8: Global Next Generation Network Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 9: Global Next Generation Network Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 10: Global Next Generation Network Industry Revenue Million Forecast, by Offering 2020 & 2033

- Table 11: Global Next Generation Network Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 12: Global Next Generation Network Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Global Next Generation Network Industry Revenue Million Forecast, by Offering 2020 & 2033

- Table 14: Global Next Generation Network Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 15: Global Next Generation Network Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Global Next Generation Network Industry Revenue Million Forecast, by Offering 2020 & 2033

- Table 17: Global Next Generation Network Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 18: Global Next Generation Network Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Next Generation Network Industry?

The projected CAGR is approximately 7.70%.

2. Which companies are prominent players in the Next Generation Network Industry?

Key companies in the market include IBM Corporation, Samsung Electronics Co Ltd, Cisco Systems Inc, Juniper Networks Inc, Telefonaktiebolaget LM Ericsso, NEC Corporation, Huawei Technologies Co Ltd, ZTE Corporation, Nokia Corporation, Ciena Corporation.

3. What are the main segments of the Next Generation Network Industry?

The market segments include Offering, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 30.55 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand for High-Speed Services.

6. What are the notable trends driving market growth?

Hardware Offering Holds Significant Market Share.

7. Are there any restraints impacting market growth?

High Costs Related to the Infrastructure.

8. Can you provide examples of recent developments in the market?

February 2024 - Schneider Electric, delivering next-generation, open automation infrastructure in collaboration with the technology companies Intel and Red Hat, released a Distributed Control Node (DCN) software framework. An expansion of Schneider Electric's EcoStruxure Automation Expert, this new framework allows industrial companies to move to a software-defined, plug-and-produce solution, enabling them to augment their operations, ensure quality, minimize complexity, and optimize costs.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Next Generation Network Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Next Generation Network Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Next Generation Network Industry?

To stay informed about further developments, trends, and reports in the Next Generation Network Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence