Key Insights

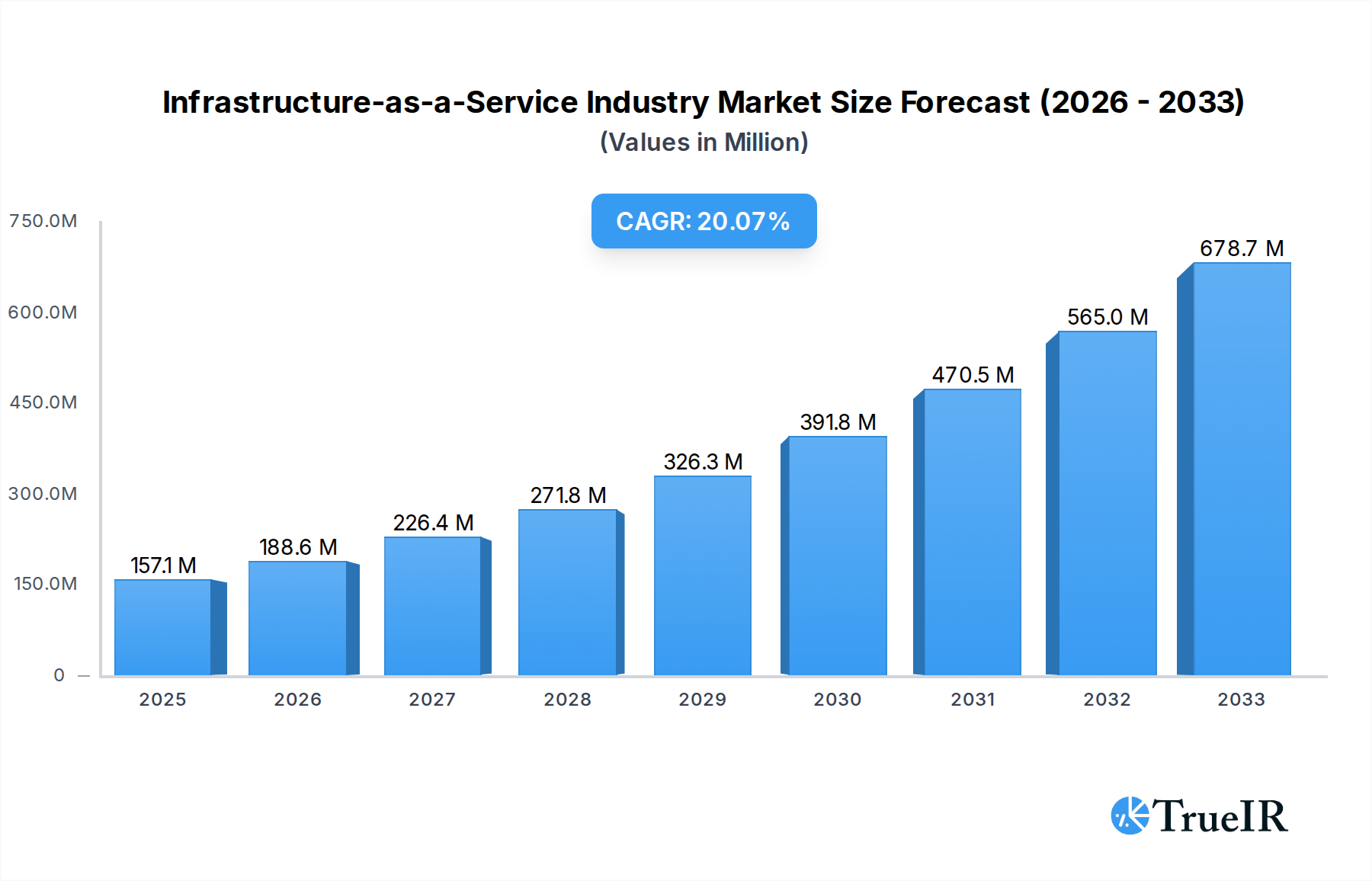

The Infrastructure-as-a-Service (IaaS) market is experiencing robust expansion, projected to reach $157.12 million by 2025. This growth is fueled by a CAGR of 20.01%, indicating a significant upward trajectory over the forecast period. The widespread adoption of cloud computing by enterprises across diverse sectors is a primary driver. Businesses are increasingly leveraging IaaS for its scalability, cost-efficiency, and flexibility, allowing them to reduce capital expenditure on physical infrastructure and focus on core competencies. The digital transformation initiatives, coupled with the growing demand for robust IT infrastructure to support Big Data analytics, AI, and IoT deployments, are further accelerating market penetration. The shift towards hybrid and multi-cloud strategies also plays a crucial role, as organizations seek to optimize workloads and enhance resilience by distributing them across various cloud environments.

Infrastructure-as-a-Service Industry Market Size (In Million)

The IaaS market is segmented across multiple deployment modes, including Public Cloud, Private Cloud, and Hybrid Cloud, with Public Cloud likely dominating due to its accessibility and cost advantages for a broad range of users. Key services offered within IaaS encompass Managed Hosting, Disaster Recovery as a Service (DRaaS), Communication as a Service (CaaS), Database as a Service (DBaaS), and Storage as a Service (SaaS), each catering to specific business needs. The BFSI, IT & Telecom, and Healthcare sectors are anticipated to be major end-users, driven by their substantial data processing requirements and stringent security needs. As the digital landscape continues to evolve, the demand for flexible, secure, and on-demand IT infrastructure will solidify IaaS as a cornerstone of modern enterprise operations. Leading companies such as Amazon Web Services, Microsoft Azure, and Google Cloud are at the forefront, continuously innovating and expanding their service portfolios to capture market share.

Infrastructure-as-a-Service Industry Company Market Share

Unlock the future of cloud computing with this in-depth report on the Infrastructure-as-a-Service (IaaS) market. Spanning from 2019 to 2033, with a base and estimated year of 2025, this comprehensive analysis delves into market dynamics, key players, and emerging opportunities within the rapidly evolving IaaS landscape. Leveraging high-volume keywords such as "cloud computing," "virtualization," "data centers," "managed hosting," and "hybrid cloud," this report is meticulously crafted for optimal SEO performance and maximum reader engagement. Discover critical insights into deployment modes, service offerings, and end-user industry adoption, alongside detailed analyses of market trends, competitive strategies, and future growth catalysts.

Infrastructure-as-a-Service Industry Market Structure & Competitive Landscape

The global Infrastructure-as-a-Service (IaaS) market exhibits a moderately concentrated structure, driven by significant capital investment requirements and the dominance of a few major players. Innovation is a key differentiator, with companies continuously enhancing their offerings in areas like scalability, security, and specialized services. Regulatory impacts, while present, are largely centered on data privacy and compliance, pushing providers towards robust security frameworks. Product substitutes are limited, primarily revolving around on-premises infrastructure, which is increasingly being outpaced by the agility and cost-effectiveness of IaaS. End-user segmentation reveals diverse adoption patterns across industries, with IT & Telecom and BFSI leading the charge. Mergers and acquisitions (M&A) are strategic moves to consolidate market share, acquire new technologies, and expand service portfolios, contributing to an average of 10-15 M&A deals annually within the broader cloud infrastructure space. Concentration ratios, particularly among the top three providers, exceed 60%, underscoring the significant market share held by industry giants.

Infrastructure-as-a-Service Industry Market Trends & Opportunities

The Infrastructure-as-a-Service (IaaS) market is experiencing robust growth, projected to achieve a Compound Annual Growth Rate (CAGR) of approximately 18% during the forecast period (2025–2033). This expansion is fueled by a paradigm shift towards digital transformation, where businesses of all sizes are increasingly reliant on scalable, on-demand computing resources. Technological shifts, including advancements in AI, machine learning, and the Internet of Things (IoT), are creating a higher demand for the flexible and powerful infrastructure that IaaS providers offer. Consumer preferences are leaning towards cost optimization, operational efficiency, and enhanced agility, all of which are core tenets of the IaaS model. The competitive dynamics are intensifying, with providers differentiating themselves through specialized services, improved security offerings, and seamless integration capabilities. Market penetration rates continue to climb, as more organizations recognize the strategic advantage of outsourcing their IT infrastructure management. Opportunities abound in the development of niche IaaS solutions, catering to specific industry needs, and in the expansion of hybrid and multi-cloud strategies, which offer enhanced flexibility and resilience. The market size is estimated to reach over $300 Billion by 2025, with significant potential for further growth as emerging economies adopt cloud technologies.

Dominant Markets & Segments in Infrastructure-as-a-Service Industry

The Public Cloud segment is currently the dominant deployment mode within the Infrastructure-as-a-Service (IaaS) market, driven by its inherent scalability, cost-effectiveness, and broad accessibility for businesses of all sizes. Within the service offerings, Managed Hosting remains a cornerstone, providing businesses with comprehensive control over their infrastructure with the added benefit of provider management. The IT & Telecom sector consistently emerges as a leading end-user industry, due to its continuous need for robust, scalable, and secure digital infrastructure to support its vast array of services and applications. Following closely are the BFSI and Healthcare industries, where data security, compliance, and high availability are paramount.

Deployment Mode Dominance:

- Public Cloud: Characterized by widespread adoption due to its pay-as-you-go model, rapid scalability, and minimal upfront investment, making it highly attractive for startups and large enterprises alike.

- Hybrid Cloud: Growing in popularity as organizations seek to balance the benefits of public cloud agility with the security and control of private cloud environments, enabling optimized workload placement.

- Private Cloud: Remains crucial for organizations with stringent regulatory requirements or unique performance needs, offering dedicated resources and enhanced data sovereignty.

Leading Service Segments:

- Managed Hosting: Continues to be a foundational service, offering a balanced approach to control and convenience for businesses.

- Storage as a Service (SaaS): Experiencing significant growth driven by the explosion of data, from big data analytics to digital media storage needs.

- Disaster Recovery as a Service (DRaaS): Increasingly vital for business continuity, with growing demand for robust and reliable backup and recovery solutions.

Key End-User Industry Growth Drivers:

- IT & Telecom: Continuous demand for high-performance computing, network virtualization, and agile development environments.

- BFSI: Stringent security and compliance mandates, the need for scalable transaction processing, and the rise of fintech solutions.

- Healthcare: Growing adoption of electronic health records (EHRs), telemedicine, and the need for secure, compliant data storage and processing.

- Retail: E-commerce expansion, inventory management, supply chain optimization, and personalized customer experiences powered by cloud infrastructure.

- Media & Entertainment: Demand for high-capacity storage and processing for content creation, streaming, and distribution.

Infrastructure-as-a-Service Industry Product Analysis

Product innovations in the Infrastructure-as-a-Service (IaaS) market are heavily focused on enhancing performance, security, and cost-efficiency. Providers are increasingly offering specialized compute and storage options, including GPU-accelerated instances for AI/ML workloads and high-performance NVMe storage for demanding applications. Advancements in containerization technologies and serverless computing are further blurring the lines of traditional infrastructure, offering greater abstraction and agility. Key competitive advantages lie in the ease of integration with existing IT ecosystems, robust security features like advanced threat detection and encryption, and flexible pricing models that cater to diverse usage patterns. The market fit is exceptionally strong for businesses seeking to reduce capital expenditure on hardware, accelerate time-to-market for new applications, and gain the agility to respond to dynamic business demands.

Key Drivers, Barriers & Challenges in Infrastructure-as-a-Service Industry

Key drivers propelling the Infrastructure-as-a-Service (IaaS) market include the relentless pursuit of digital transformation across industries, the economic advantages of pay-as-you-go models, and the inherent scalability and flexibility offered by cloud infrastructure. Technological advancements in virtualization, networking, and automation are continuously enhancing IaaS capabilities, making them more attractive to a wider range of businesses. Government initiatives promoting cloud adoption and digital governance also play a significant role.

However, several barriers and challenges impact growth. Security concerns and data privacy regulations remain significant hurdles, requiring providers to invest heavily in robust security measures and compliance frameworks. The complexity of managing multi-cloud environments and the potential for vendor lock-in also present challenges for some organizations. Furthermore, the shortage of skilled IT professionals capable of managing cloud environments can slow down adoption. Supply chain issues, particularly for hardware components, can indirectly impact the scalability and cost-efficiency of IaaS offerings, although providers often have robust procurement strategies to mitigate these risks. Competitive pressures are intense, leading to price sensitivity and a constant need for service differentiation.

Growth Drivers in the Infrastructure-as-a-Service Industry Market

The Infrastructure-as-a-Service (IaaS) market is propelled by several key growth drivers. Economically, the shift from capital expenditure (CapEx) to operational expenditure (OpEx) offers significant cost savings and budget predictability for businesses. Technologically, the accelerating adoption of AI, machine learning, big data analytics, and IoT applications necessitates highly scalable and powerful computing resources that IaaS readily provides. Regulatory drivers, such as government mandates for digital transformation and data modernization, further encourage cloud adoption. Moreover, the increasing need for business continuity and disaster recovery solutions is driving demand for IaaS-based DRaaS offerings, ensuring resilience and minimizing downtime for critical operations.

Challenges Impacting Infrastructure-as-a-Service Industry Growth

Challenges impacting Infrastructure-as-a-Service (IaaS) industry growth are multifaceted. Regulatory complexities surrounding data sovereignty, privacy, and compliance (e.g., GDPR, HIPAA) necessitate careful navigation and robust security measures, which can increase operational costs for providers and introduce potential barriers for certain industries. Supply chain disruptions for essential hardware components can affect service delivery and cost structures, although established providers often have sophisticated global sourcing strategies. Competitive pressures are relentless, with numerous players vying for market share, leading to price wars and a constant need for innovation and service differentiation. The potential for vendor lock-in also poses a concern for businesses, prompting demand for interoperability and open standards. Furthermore, the cybersecurity landscape is a perpetual challenge, requiring continuous investment in advanced threat detection, prevention, and response capabilities to safeguard client data.

Key Players Shaping the Infrastructure-as-a-Service Industry Market

- Amazon Web Services Inc

- Microsoft Corporation

- Google Inc

- IBM Corporation

- Oracle Corporation

- VMWare Inc

- RedHat Inc

- Rackspace Hosting Inc

- EMC Corporation

- RedCentric PLC

Significant Infrastructure-as-a-Service Industry Industry Milestones

- August 2023: Cisco and Kyndryl extended their partnership to integrate Kyndryl's cyber resilience solution with Cisco's comprehensive Security Cloud platform, enhancing enterprise capabilities in identifying and addressing cyber risks, specifically by unifying security and policy across private and public clouds with solutions like Multicloud Defense and Duo access control.

- May 2023: Kyndryl Holdings, Inc. partnered with Cloudflare, Inc. to help businesses modernize and scale their corporate networks by offering managed WAN-as-a-Service and Cloudflare Zero Trust, enabling more efficient cloud connectivity through Cloudflare's technology and Kyndryl's networking services.

Future Outlook for Infrastructure-as-a-Service Industry Market

The future outlook for the Infrastructure-as-a-Service (IaaS) market is exceptionally bright, driven by sustained demand for digital transformation, the proliferation of AI and edge computing, and the ongoing migration of enterprise workloads to the cloud. Strategic opportunities lie in further specialization of IaaS offerings to cater to niche industry needs, the development of more advanced security and compliance solutions, and the expansion of hybrid and multi-cloud management services. The increasing adoption of cloud-native technologies and the growing emphasis on sustainability within data center operations will also shape the market. As businesses continue to prioritize agility, scalability, and cost-efficiency, the IaaS market is poised for continued robust growth, with innovations in areas like quantum computing and serverless architectures potentially unlocking new frontiers.

Infrastructure-as-a-Service Industry Segmentation

-

1. Deployment Mode

- 1.1. Public Cloud

- 1.2. Private Cloud

- 1.3. Hybrid Cloud

-

2. Service

- 2.1. Managed Hosting

- 2.2. Disaster Recovery as a Service ( DRaaS)

- 2.3. Communication as a Service (CaaS)

- 2.4. Database as a Service (DBaaS)

- 2.5. Storage as a Service (SaaS)

-

3. End-user Industry

- 3.1. BFSI

- 3.2. IT & Telecom

- 3.3. Healthcare

- 3.4. Media & Entertainment

- 3.5. Retail

- 3.6. Other End-user Industries

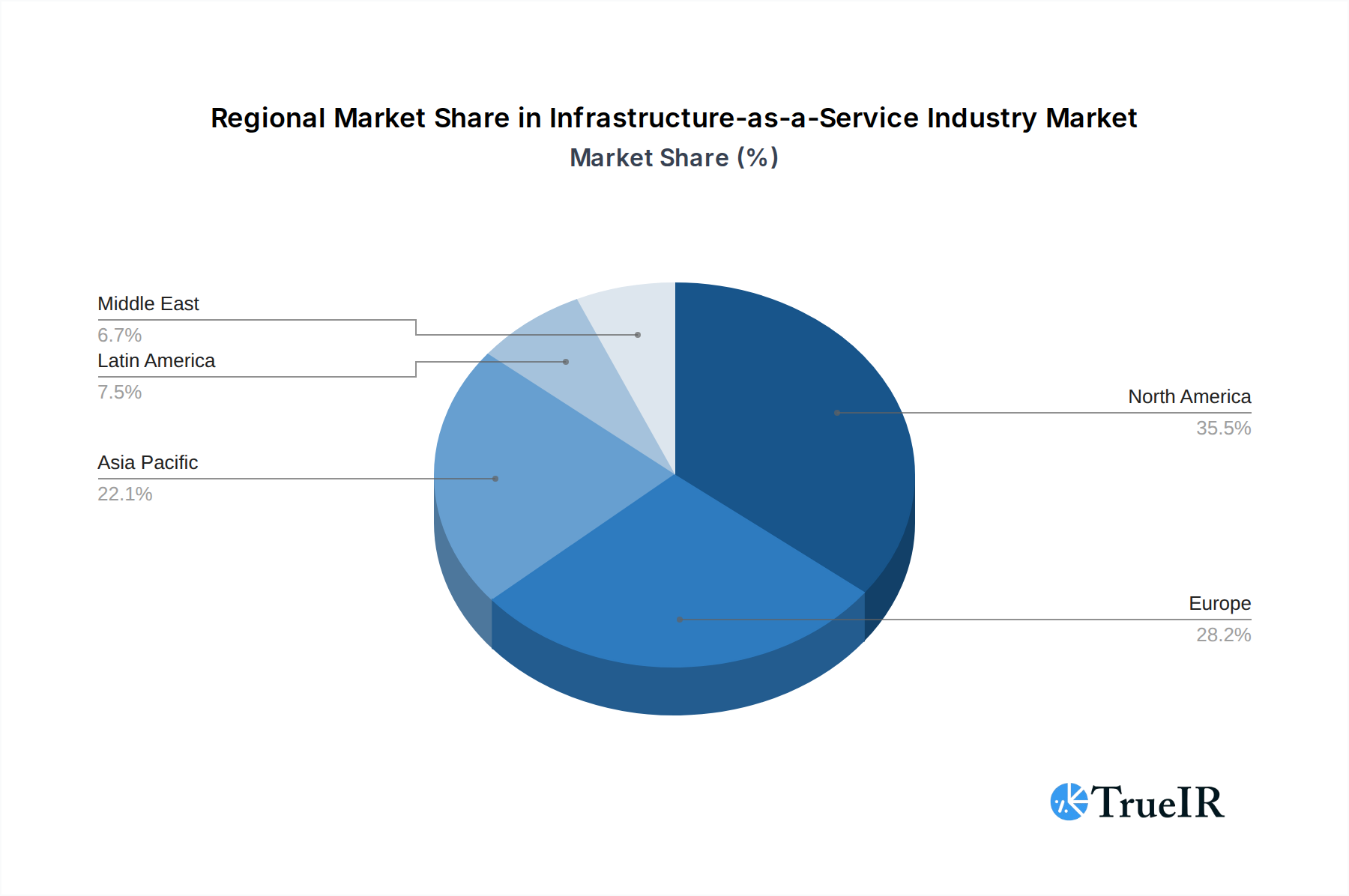

Infrastructure-as-a-Service Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East

Infrastructure-as-a-Service Industry Regional Market Share

Geographic Coverage of Infrastructure-as-a-Service Industry

Infrastructure-as-a-Service Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 20.01% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Deployment Mode

- 5.1.1. Public Cloud

- 5.1.2. Private Cloud

- 5.1.3. Hybrid Cloud

- 5.2. Market Analysis, Insights and Forecast - by Service

- 5.2.1. Managed Hosting

- 5.2.2. Disaster Recovery as a Service ( DRaaS)

- 5.2.3. Communication as a Service (CaaS)

- 5.2.4. Database as a Service (DBaaS)

- 5.2.5. Storage as a Service (SaaS)

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. BFSI

- 5.3.2. IT & Telecom

- 5.3.3. Healthcare

- 5.3.4. Media & Entertainment

- 5.3.5. Retail

- 5.3.6. Other End-user Industries

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Latin America

- 5.4.5. Middle East

- 5.1. Market Analysis, Insights and Forecast - by Deployment Mode

- 6. Global Infrastructure-as-a-Service Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Deployment Mode

- 6.1.1. Public Cloud

- 6.1.2. Private Cloud

- 6.1.3. Hybrid Cloud

- 6.2. Market Analysis, Insights and Forecast - by Service

- 6.2.1. Managed Hosting

- 6.2.2. Disaster Recovery as a Service ( DRaaS)

- 6.2.3. Communication as a Service (CaaS)

- 6.2.4. Database as a Service (DBaaS)

- 6.2.5. Storage as a Service (SaaS)

- 6.3. Market Analysis, Insights and Forecast - by End-user Industry

- 6.3.1. BFSI

- 6.3.2. IT & Telecom

- 6.3.3. Healthcare

- 6.3.4. Media & Entertainment

- 6.3.5. Retail

- 6.3.6. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Deployment Mode

- 7. North America Infrastructure-as-a-Service Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Deployment Mode

- 7.1.1. Public Cloud

- 7.1.2. Private Cloud

- 7.1.3. Hybrid Cloud

- 7.2. Market Analysis, Insights and Forecast - by Service

- 7.2.1. Managed Hosting

- 7.2.2. Disaster Recovery as a Service ( DRaaS)

- 7.2.3. Communication as a Service (CaaS)

- 7.2.4. Database as a Service (DBaaS)

- 7.2.5. Storage as a Service (SaaS)

- 7.3. Market Analysis, Insights and Forecast - by End-user Industry

- 7.3.1. BFSI

- 7.3.2. IT & Telecom

- 7.3.3. Healthcare

- 7.3.4. Media & Entertainment

- 7.3.5. Retail

- 7.3.6. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by Deployment Mode

- 8. Europe Infrastructure-as-a-Service Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Deployment Mode

- 8.1.1. Public Cloud

- 8.1.2. Private Cloud

- 8.1.3. Hybrid Cloud

- 8.2. Market Analysis, Insights and Forecast - by Service

- 8.2.1. Managed Hosting

- 8.2.2. Disaster Recovery as a Service ( DRaaS)

- 8.2.3. Communication as a Service (CaaS)

- 8.2.4. Database as a Service (DBaaS)

- 8.2.5. Storage as a Service (SaaS)

- 8.3. Market Analysis, Insights and Forecast - by End-user Industry

- 8.3.1. BFSI

- 8.3.2. IT & Telecom

- 8.3.3. Healthcare

- 8.3.4. Media & Entertainment

- 8.3.5. Retail

- 8.3.6. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by Deployment Mode

- 9. Asia Pacific Infrastructure-as-a-Service Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Deployment Mode

- 9.1.1. Public Cloud

- 9.1.2. Private Cloud

- 9.1.3. Hybrid Cloud

- 9.2. Market Analysis, Insights and Forecast - by Service

- 9.2.1. Managed Hosting

- 9.2.2. Disaster Recovery as a Service ( DRaaS)

- 9.2.3. Communication as a Service (CaaS)

- 9.2.4. Database as a Service (DBaaS)

- 9.2.5. Storage as a Service (SaaS)

- 9.3. Market Analysis, Insights and Forecast - by End-user Industry

- 9.3.1. BFSI

- 9.3.2. IT & Telecom

- 9.3.3. Healthcare

- 9.3.4. Media & Entertainment

- 9.3.5. Retail

- 9.3.6. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by Deployment Mode

- 10. Latin America Infrastructure-as-a-Service Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Deployment Mode

- 10.1.1. Public Cloud

- 10.1.2. Private Cloud

- 10.1.3. Hybrid Cloud

- 10.2. Market Analysis, Insights and Forecast - by Service

- 10.2.1. Managed Hosting

- 10.2.2. Disaster Recovery as a Service ( DRaaS)

- 10.2.3. Communication as a Service (CaaS)

- 10.2.4. Database as a Service (DBaaS)

- 10.2.5. Storage as a Service (SaaS)

- 10.3. Market Analysis, Insights and Forecast - by End-user Industry

- 10.3.1. BFSI

- 10.3.2. IT & Telecom

- 10.3.3. Healthcare

- 10.3.4. Media & Entertainment

- 10.3.5. Retail

- 10.3.6. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by Deployment Mode

- 11. Middle East Infrastructure-as-a-Service Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Deployment Mode

- 11.1.1. Public Cloud

- 11.1.2. Private Cloud

- 11.1.3. Hybrid Cloud

- 11.2. Market Analysis, Insights and Forecast - by Service

- 11.2.1. Managed Hosting

- 11.2.2. Disaster Recovery as a Service ( DRaaS)

- 11.2.3. Communication as a Service (CaaS)

- 11.2.4. Database as a Service (DBaaS)

- 11.2.5. Storage as a Service (SaaS)

- 11.3. Market Analysis, Insights and Forecast - by End-user Industry

- 11.3.1. BFSI

- 11.3.2. IT & Telecom

- 11.3.3. Healthcare

- 11.3.4. Media & Entertainment

- 11.3.5. Retail

- 11.3.6. Other End-user Industries

- 11.1. Market Analysis, Insights and Forecast - by Deployment Mode

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 EMC Corporation

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 RedCentric PLC

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 IBM Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 RedHat Inc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Microsoft Corporation

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 VMWare Inc

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Amazon Web Services Inc

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Rackspace Hosting Inc

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Oracle Corporation

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Google Inc

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 EMC Corporation

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Infrastructure-as-a-Service Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Global Infrastructure-as-a-Service Industry Volume Breakdown (K Unit, %) by Region 2025 & 2033

- Figure 3: North America Infrastructure-as-a-Service Industry Revenue (Million), by Deployment Mode 2025 & 2033

- Figure 4: North America Infrastructure-as-a-Service Industry Volume (K Unit), by Deployment Mode 2025 & 2033

- Figure 5: North America Infrastructure-as-a-Service Industry Revenue Share (%), by Deployment Mode 2025 & 2033

- Figure 6: North America Infrastructure-as-a-Service Industry Volume Share (%), by Deployment Mode 2025 & 2033

- Figure 7: North America Infrastructure-as-a-Service Industry Revenue (Million), by Service 2025 & 2033

- Figure 8: North America Infrastructure-as-a-Service Industry Volume (K Unit), by Service 2025 & 2033

- Figure 9: North America Infrastructure-as-a-Service Industry Revenue Share (%), by Service 2025 & 2033

- Figure 10: North America Infrastructure-as-a-Service Industry Volume Share (%), by Service 2025 & 2033

- Figure 11: North America Infrastructure-as-a-Service Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 12: North America Infrastructure-as-a-Service Industry Volume (K Unit), by End-user Industry 2025 & 2033

- Figure 13: North America Infrastructure-as-a-Service Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 14: North America Infrastructure-as-a-Service Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 15: North America Infrastructure-as-a-Service Industry Revenue (Million), by Country 2025 & 2033

- Figure 16: North America Infrastructure-as-a-Service Industry Volume (K Unit), by Country 2025 & 2033

- Figure 17: North America Infrastructure-as-a-Service Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: North America Infrastructure-as-a-Service Industry Volume Share (%), by Country 2025 & 2033

- Figure 19: Europe Infrastructure-as-a-Service Industry Revenue (Million), by Deployment Mode 2025 & 2033

- Figure 20: Europe Infrastructure-as-a-Service Industry Volume (K Unit), by Deployment Mode 2025 & 2033

- Figure 21: Europe Infrastructure-as-a-Service Industry Revenue Share (%), by Deployment Mode 2025 & 2033

- Figure 22: Europe Infrastructure-as-a-Service Industry Volume Share (%), by Deployment Mode 2025 & 2033

- Figure 23: Europe Infrastructure-as-a-Service Industry Revenue (Million), by Service 2025 & 2033

- Figure 24: Europe Infrastructure-as-a-Service Industry Volume (K Unit), by Service 2025 & 2033

- Figure 25: Europe Infrastructure-as-a-Service Industry Revenue Share (%), by Service 2025 & 2033

- Figure 26: Europe Infrastructure-as-a-Service Industry Volume Share (%), by Service 2025 & 2033

- Figure 27: Europe Infrastructure-as-a-Service Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 28: Europe Infrastructure-as-a-Service Industry Volume (K Unit), by End-user Industry 2025 & 2033

- Figure 29: Europe Infrastructure-as-a-Service Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 30: Europe Infrastructure-as-a-Service Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 31: Europe Infrastructure-as-a-Service Industry Revenue (Million), by Country 2025 & 2033

- Figure 32: Europe Infrastructure-as-a-Service Industry Volume (K Unit), by Country 2025 & 2033

- Figure 33: Europe Infrastructure-as-a-Service Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Europe Infrastructure-as-a-Service Industry Volume Share (%), by Country 2025 & 2033

- Figure 35: Asia Pacific Infrastructure-as-a-Service Industry Revenue (Million), by Deployment Mode 2025 & 2033

- Figure 36: Asia Pacific Infrastructure-as-a-Service Industry Volume (K Unit), by Deployment Mode 2025 & 2033

- Figure 37: Asia Pacific Infrastructure-as-a-Service Industry Revenue Share (%), by Deployment Mode 2025 & 2033

- Figure 38: Asia Pacific Infrastructure-as-a-Service Industry Volume Share (%), by Deployment Mode 2025 & 2033

- Figure 39: Asia Pacific Infrastructure-as-a-Service Industry Revenue (Million), by Service 2025 & 2033

- Figure 40: Asia Pacific Infrastructure-as-a-Service Industry Volume (K Unit), by Service 2025 & 2033

- Figure 41: Asia Pacific Infrastructure-as-a-Service Industry Revenue Share (%), by Service 2025 & 2033

- Figure 42: Asia Pacific Infrastructure-as-a-Service Industry Volume Share (%), by Service 2025 & 2033

- Figure 43: Asia Pacific Infrastructure-as-a-Service Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 44: Asia Pacific Infrastructure-as-a-Service Industry Volume (K Unit), by End-user Industry 2025 & 2033

- Figure 45: Asia Pacific Infrastructure-as-a-Service Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 46: Asia Pacific Infrastructure-as-a-Service Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 47: Asia Pacific Infrastructure-as-a-Service Industry Revenue (Million), by Country 2025 & 2033

- Figure 48: Asia Pacific Infrastructure-as-a-Service Industry Volume (K Unit), by Country 2025 & 2033

- Figure 49: Asia Pacific Infrastructure-as-a-Service Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Asia Pacific Infrastructure-as-a-Service Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: Latin America Infrastructure-as-a-Service Industry Revenue (Million), by Deployment Mode 2025 & 2033

- Figure 52: Latin America Infrastructure-as-a-Service Industry Volume (K Unit), by Deployment Mode 2025 & 2033

- Figure 53: Latin America Infrastructure-as-a-Service Industry Revenue Share (%), by Deployment Mode 2025 & 2033

- Figure 54: Latin America Infrastructure-as-a-Service Industry Volume Share (%), by Deployment Mode 2025 & 2033

- Figure 55: Latin America Infrastructure-as-a-Service Industry Revenue (Million), by Service 2025 & 2033

- Figure 56: Latin America Infrastructure-as-a-Service Industry Volume (K Unit), by Service 2025 & 2033

- Figure 57: Latin America Infrastructure-as-a-Service Industry Revenue Share (%), by Service 2025 & 2033

- Figure 58: Latin America Infrastructure-as-a-Service Industry Volume Share (%), by Service 2025 & 2033

- Figure 59: Latin America Infrastructure-as-a-Service Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 60: Latin America Infrastructure-as-a-Service Industry Volume (K Unit), by End-user Industry 2025 & 2033

- Figure 61: Latin America Infrastructure-as-a-Service Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 62: Latin America Infrastructure-as-a-Service Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 63: Latin America Infrastructure-as-a-Service Industry Revenue (Million), by Country 2025 & 2033

- Figure 64: Latin America Infrastructure-as-a-Service Industry Volume (K Unit), by Country 2025 & 2033

- Figure 65: Latin America Infrastructure-as-a-Service Industry Revenue Share (%), by Country 2025 & 2033

- Figure 66: Latin America Infrastructure-as-a-Service Industry Volume Share (%), by Country 2025 & 2033

- Figure 67: Middle East Infrastructure-as-a-Service Industry Revenue (Million), by Deployment Mode 2025 & 2033

- Figure 68: Middle East Infrastructure-as-a-Service Industry Volume (K Unit), by Deployment Mode 2025 & 2033

- Figure 69: Middle East Infrastructure-as-a-Service Industry Revenue Share (%), by Deployment Mode 2025 & 2033

- Figure 70: Middle East Infrastructure-as-a-Service Industry Volume Share (%), by Deployment Mode 2025 & 2033

- Figure 71: Middle East Infrastructure-as-a-Service Industry Revenue (Million), by Service 2025 & 2033

- Figure 72: Middle East Infrastructure-as-a-Service Industry Volume (K Unit), by Service 2025 & 2033

- Figure 73: Middle East Infrastructure-as-a-Service Industry Revenue Share (%), by Service 2025 & 2033

- Figure 74: Middle East Infrastructure-as-a-Service Industry Volume Share (%), by Service 2025 & 2033

- Figure 75: Middle East Infrastructure-as-a-Service Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 76: Middle East Infrastructure-as-a-Service Industry Volume (K Unit), by End-user Industry 2025 & 2033

- Figure 77: Middle East Infrastructure-as-a-Service Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 78: Middle East Infrastructure-as-a-Service Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 79: Middle East Infrastructure-as-a-Service Industry Revenue (Million), by Country 2025 & 2033

- Figure 80: Middle East Infrastructure-as-a-Service Industry Volume (K Unit), by Country 2025 & 2033

- Figure 81: Middle East Infrastructure-as-a-Service Industry Revenue Share (%), by Country 2025 & 2033

- Figure 82: Middle East Infrastructure-as-a-Service Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Infrastructure-as-a-Service Industry Revenue Million Forecast, by Deployment Mode 2020 & 2033

- Table 2: Global Infrastructure-as-a-Service Industry Volume K Unit Forecast, by Deployment Mode 2020 & 2033

- Table 3: Global Infrastructure-as-a-Service Industry Revenue Million Forecast, by Service 2020 & 2033

- Table 4: Global Infrastructure-as-a-Service Industry Volume K Unit Forecast, by Service 2020 & 2033

- Table 5: Global Infrastructure-as-a-Service Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 6: Global Infrastructure-as-a-Service Industry Volume K Unit Forecast, by End-user Industry 2020 & 2033

- Table 7: Global Infrastructure-as-a-Service Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 8: Global Infrastructure-as-a-Service Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 9: Global Infrastructure-as-a-Service Industry Revenue Million Forecast, by Deployment Mode 2020 & 2033

- Table 10: Global Infrastructure-as-a-Service Industry Volume K Unit Forecast, by Deployment Mode 2020 & 2033

- Table 11: Global Infrastructure-as-a-Service Industry Revenue Million Forecast, by Service 2020 & 2033

- Table 12: Global Infrastructure-as-a-Service Industry Volume K Unit Forecast, by Service 2020 & 2033

- Table 13: Global Infrastructure-as-a-Service Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 14: Global Infrastructure-as-a-Service Industry Volume K Unit Forecast, by End-user Industry 2020 & 2033

- Table 15: Global Infrastructure-as-a-Service Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Global Infrastructure-as-a-Service Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 17: Global Infrastructure-as-a-Service Industry Revenue Million Forecast, by Deployment Mode 2020 & 2033

- Table 18: Global Infrastructure-as-a-Service Industry Volume K Unit Forecast, by Deployment Mode 2020 & 2033

- Table 19: Global Infrastructure-as-a-Service Industry Revenue Million Forecast, by Service 2020 & 2033

- Table 20: Global Infrastructure-as-a-Service Industry Volume K Unit Forecast, by Service 2020 & 2033

- Table 21: Global Infrastructure-as-a-Service Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 22: Global Infrastructure-as-a-Service Industry Volume K Unit Forecast, by End-user Industry 2020 & 2033

- Table 23: Global Infrastructure-as-a-Service Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 24: Global Infrastructure-as-a-Service Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 25: Global Infrastructure-as-a-Service Industry Revenue Million Forecast, by Deployment Mode 2020 & 2033

- Table 26: Global Infrastructure-as-a-Service Industry Volume K Unit Forecast, by Deployment Mode 2020 & 2033

- Table 27: Global Infrastructure-as-a-Service Industry Revenue Million Forecast, by Service 2020 & 2033

- Table 28: Global Infrastructure-as-a-Service Industry Volume K Unit Forecast, by Service 2020 & 2033

- Table 29: Global Infrastructure-as-a-Service Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 30: Global Infrastructure-as-a-Service Industry Volume K Unit Forecast, by End-user Industry 2020 & 2033

- Table 31: Global Infrastructure-as-a-Service Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 32: Global Infrastructure-as-a-Service Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 33: Global Infrastructure-as-a-Service Industry Revenue Million Forecast, by Deployment Mode 2020 & 2033

- Table 34: Global Infrastructure-as-a-Service Industry Volume K Unit Forecast, by Deployment Mode 2020 & 2033

- Table 35: Global Infrastructure-as-a-Service Industry Revenue Million Forecast, by Service 2020 & 2033

- Table 36: Global Infrastructure-as-a-Service Industry Volume K Unit Forecast, by Service 2020 & 2033

- Table 37: Global Infrastructure-as-a-Service Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 38: Global Infrastructure-as-a-Service Industry Volume K Unit Forecast, by End-user Industry 2020 & 2033

- Table 39: Global Infrastructure-as-a-Service Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 40: Global Infrastructure-as-a-Service Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 41: Global Infrastructure-as-a-Service Industry Revenue Million Forecast, by Deployment Mode 2020 & 2033

- Table 42: Global Infrastructure-as-a-Service Industry Volume K Unit Forecast, by Deployment Mode 2020 & 2033

- Table 43: Global Infrastructure-as-a-Service Industry Revenue Million Forecast, by Service 2020 & 2033

- Table 44: Global Infrastructure-as-a-Service Industry Volume K Unit Forecast, by Service 2020 & 2033

- Table 45: Global Infrastructure-as-a-Service Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 46: Global Infrastructure-as-a-Service Industry Volume K Unit Forecast, by End-user Industry 2020 & 2033

- Table 47: Global Infrastructure-as-a-Service Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 48: Global Infrastructure-as-a-Service Industry Volume K Unit Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Infrastructure-as-a-Service Industry?

The projected CAGR is approximately 20.01%.

2. Which companies are prominent players in the Infrastructure-as-a-Service Industry?

Key companies in the market include EMC Corporation, RedCentric PLC, IBM Corporation, RedHat Inc, Microsoft Corporation, VMWare Inc, Amazon Web Services Inc, Rackspace Hosting Inc, Oracle Corporation, Google Inc.

3. What are the main segments of the Infrastructure-as-a-Service Industry?

The market segments include Deployment Mode, Service, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 157.12 Million as of 2022.

5. What are some drivers contributing to market growth?

Increased Demand For Hybrid Cloud Platform; Growing Need For High Speed Interaction Between Various Networks.

6. What are the notable trends driving market growth?

IT & Telecom Expected to Hold Significant Growth.

7. Are there any restraints impacting market growth?

Stringent Government Regulations.

8. Can you provide examples of recent developments in the market?

August 2023 - Cisco, a global technology company, and Kyndryl, an IT infrastructure services provider, have extended the partnership to include new services to assist enterprise clients more effectively in identifying and addressing cyber risks. More specifically, Kyndryl will integrate its cyber resilience solution with Cisco's comprehensive Security Cloud platform, comprising security elements like Multicloud Defense, which unifies security and policy across private and public clouds, Cisco's Duo access control, and extended detection and response features.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Infrastructure-as-a-Service Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Infrastructure-as-a-Service Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Infrastructure-as-a-Service Industry?

To stay informed about further developments, trends, and reports in the Infrastructure-as-a-Service Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence