Key Insights

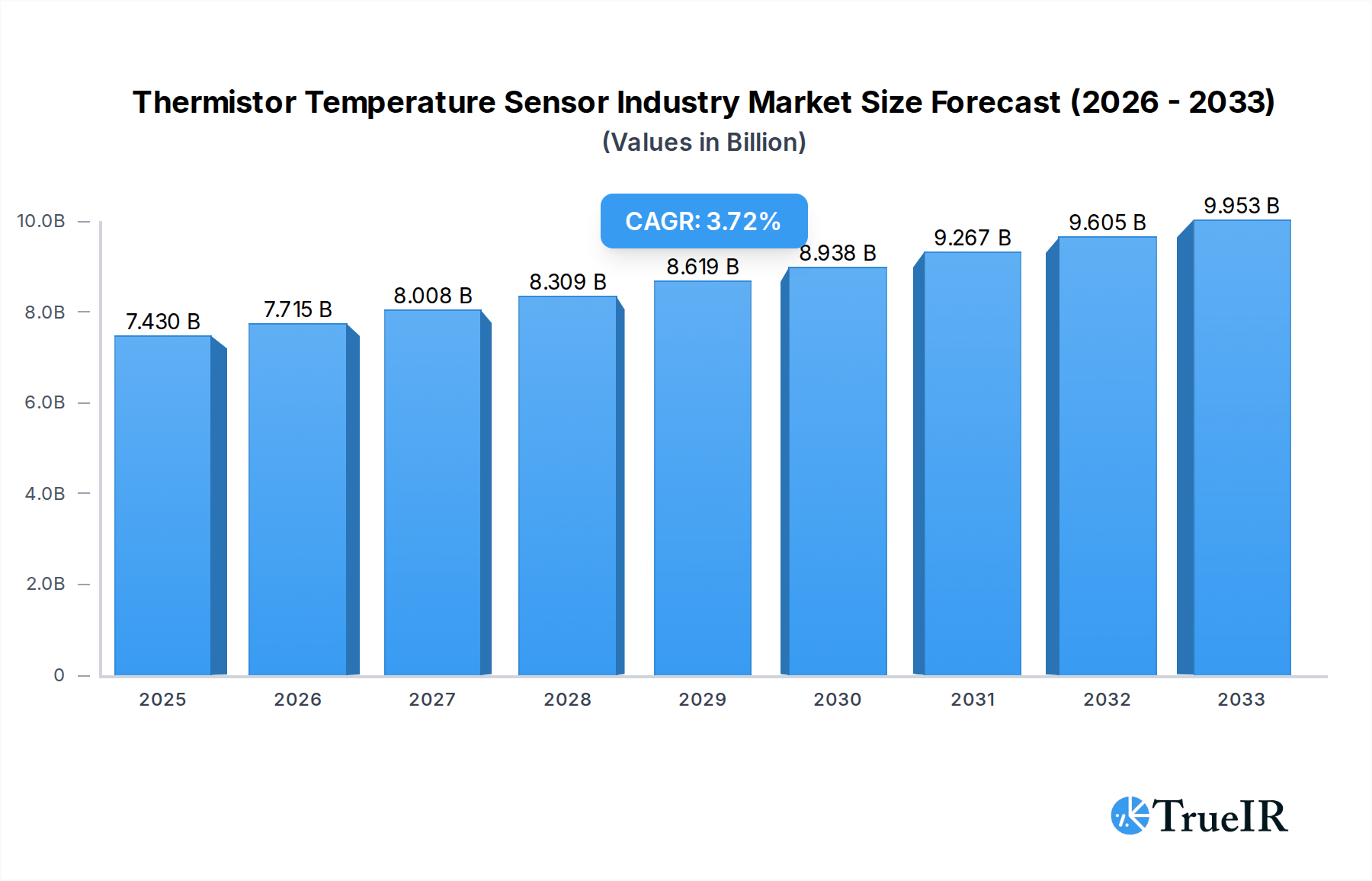

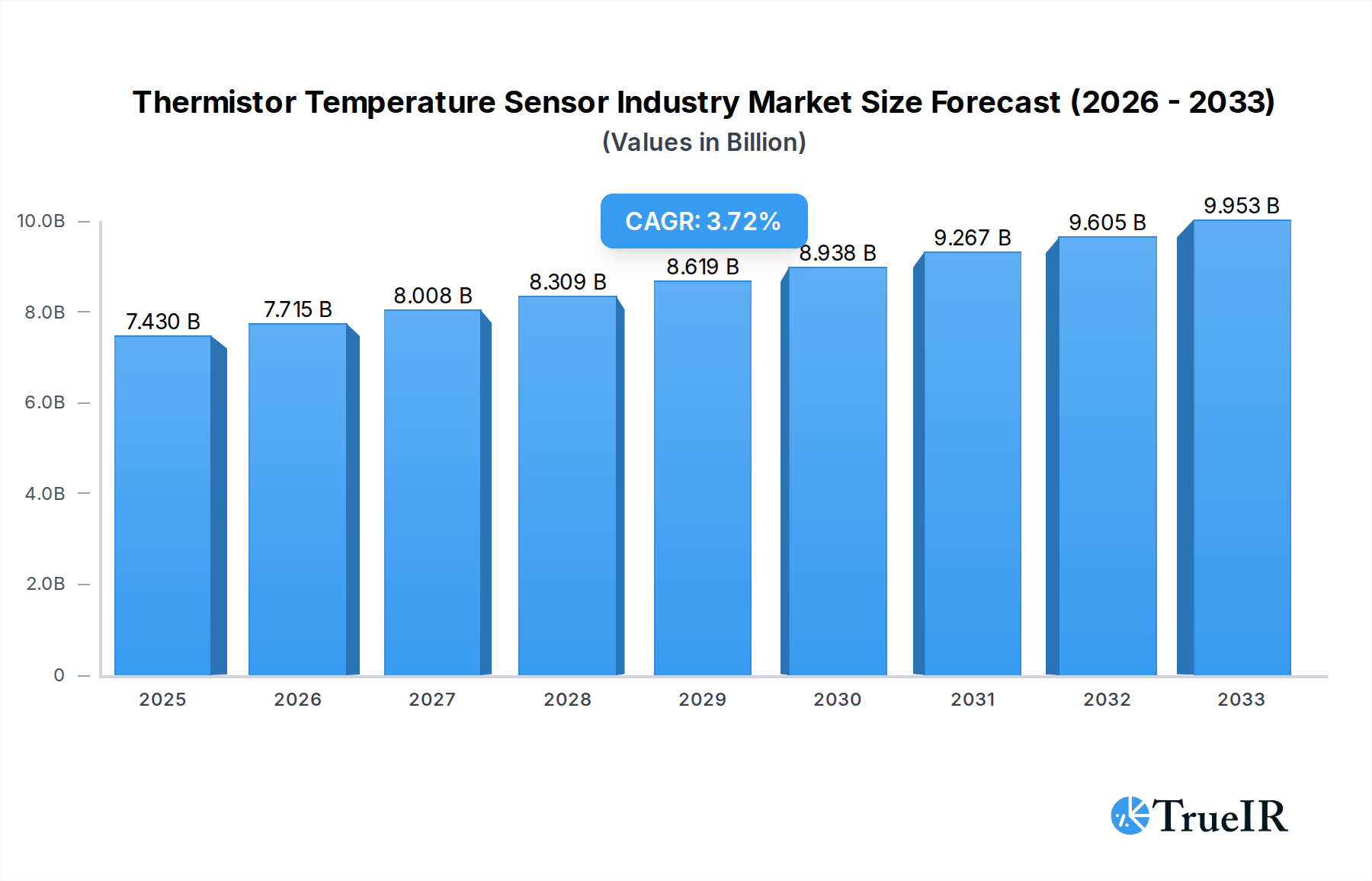

The global Thermistor Temperature Sensor market is poised for significant expansion, projected to reach $7.43 billion by 2025. Driven by an increasing demand for precise temperature monitoring and control across a multitude of industries, the market is expected to grow at a Compound Annual Growth Rate (CAGR) of 3.8% during the forecast period of 2025-2033. Key growth drivers include the burgeoning adoption of IoT devices, stringent safety regulations mandating accurate temperature management, and the continuous innovation in miniaturization and enhanced accuracy of thermistor technology. Sectors like Automotive, Life Sciences, and HVAC are leading this surge, with substantial investments in advanced temperature sensing solutions. The increasing complexity of electronic systems and the need for robust thermal management in power-intensive applications further fuel this upward trajectory.

Thermistor Temperature Sensor Industry Market Size (In Billion)

The market's robust growth is further bolstered by advancements in thermistor types, with both Positive Temperature Coefficient (PTC) and Negative Temperature Coefficient (NTC) sensors finding extensive applications. The Semiconductor, Automotive, and Life Sciences segments are demonstrating particularly strong adoption rates due to the critical nature of temperature control in these areas. While opportunities abound, the market does face certain restraints, including intense price competition and the emergence of alternative sensing technologies. However, the inherent cost-effectiveness and reliability of thermistors continue to maintain their strong market position. Geographically, the Asia Pacific region is expected to emerge as a dominant force, fueled by rapid industrialization and a burgeoning electronics manufacturing base, alongside significant growth in North America and Europe driven by technological advancements and regulatory compliance.

Thermistor Temperature Sensor Industry Company Market Share

This comprehensive report offers an in-depth analysis of the global Thermistor Temperature Sensor Industry. Spanning a study period from 2019 to 2033, with a base year of 2025, this report leverages high-volume keywords to provide actionable insights for industry stakeholders. We delve into market dynamics, emerging trends, and competitive landscapes, forecasting a robust CAGR of approximately 6.5% from 2025 to 2033, with the global market size projected to reach a staggering $8.2 billion by 2025, expanding to over $13.7 billion by the end of the forecast period. This meticulously researched report is designed for immediate use without further modification, offering unparalleled clarity and strategic guidance.

Thermistor Temperature Sensor Industry Market Structure & Competitive Landscape

The Thermistor Temperature Sensor Industry exhibits a moderately consolidated market structure, with leading players holding a significant share of the global market, estimated at around 65% in 2025. Innovation drivers are primarily fueled by advancements in material science, miniaturization, and the increasing demand for high-precision temperature sensing solutions across diverse applications. Regulatory impacts, particularly concerning environmental compliance and product safety standards in sectors like Life Sciences and Aerospace, are also shaping market dynamics. Product substitutes, such as RTDs and thermocouples, offer alternative temperature measurement technologies, but thermistors maintain a competitive edge due to their cost-effectiveness and sensitivity in specific temperature ranges. End-user segmentation reveals a strong reliance on Automotive, HVAC, and Semiconductor applications, which collectively accounted for over 50% of the market revenue in 2025. Mergers and Acquisitions (M&A) trends, while not dominating, are observed as strategic moves for market expansion and technological integration, with an estimated volume of 5-7 significant deals annually between 2019 and 2024, and projected to continue at a similar pace.

- Market Concentration: Moderately consolidated with top 5 players holding approximately 45% market share in 2025.

- Innovation Drivers: Material science advancements, miniaturization, AI integration for predictive maintenance.

- Regulatory Impacts: Growing emphasis on RoHS, REACH compliance, and industry-specific safety certifications.

- Product Substitutes: RTDs, Thermocouples, Infrared sensors.

- End-User Segmentation Dominance (2025): Automotive (20%), HVAC (18%), Semiconductor (15%).

- M&A Activity: Steady, focusing on technology acquisition and market penetration.

Thermistor Temperature Sensor Industry Market Trends & Opportunities

The global Thermistor Temperature Sensor Industry is poised for substantial growth, driven by an ever-increasing demand for precise and reliable temperature monitoring across a multitude of sectors. The market size, estimated at $8.2 billion in 2025, is projected to witness a Compound Annual Growth Rate (CAGR) of approximately 6.5% during the forecast period of 2025–2033, culminating in a market value exceeding $13.7 billion by 2033. This expansion is underpinned by several key trends. Firstly, the pervasive adoption of the Internet of Things (IoT) and Industry 4.0 initiatives is creating unprecedented opportunities for smart, connected temperature sensors that enable real-time data acquisition and analysis for optimized operations and predictive maintenance. The automotive industry, in particular, is a significant growth engine, with the increasing electrification of vehicles, advanced driver-assistance systems (ADAS), and stringent emission control regulations necessitating sophisticated thermal management solutions. Thermistors, with their excellent sensitivity and fast response times, are crucial components in battery management systems, powertrain control, and cabin climate control in electric vehicles.

Furthermore, the burgeoning Life Sciences sector, encompassing healthcare and pharmaceuticals, presents a substantial opportunity. The need for accurate temperature monitoring in medical devices, pharmaceutical storage and transportation, and laboratory equipment is paramount, driving demand for high-accuracy and validated thermistor solutions. Similarly, the growing emphasis on energy efficiency and sustainability across industries such as Power Generation, Oil and Gas, and HVAC is fueling the adoption of thermistors for monitoring and controlling industrial processes, optimizing energy consumption, and ensuring operational safety. Technological advancements are also playing a pivotal role. Innovations in sensor materials, such as advanced ceramic and polymer compositions, are leading to enhanced performance characteristics, including wider operating temperature ranges, improved accuracy, and increased durability. The miniaturization of thermistors is another key trend, enabling their integration into increasingly compact devices and systems, further broadening their application scope. Consumer preferences are also evolving, with a growing demand for smart home devices and energy-efficient appliances, both of which rely heavily on accurate temperature sensing for optimal performance and user comfort. The competitive landscape is characterized by continuous product development, strategic partnerships, and a focus on catering to niche application requirements. Market penetration rates are expected to rise, particularly in emerging economies where industrialization and technological adoption are accelerating. The increasing complexity of industrial processes and the need for granular control further amplify the importance of accurate and responsive thermistor technology.

Dominant Markets & Segments in Thermistor Temperature Sensor Industry

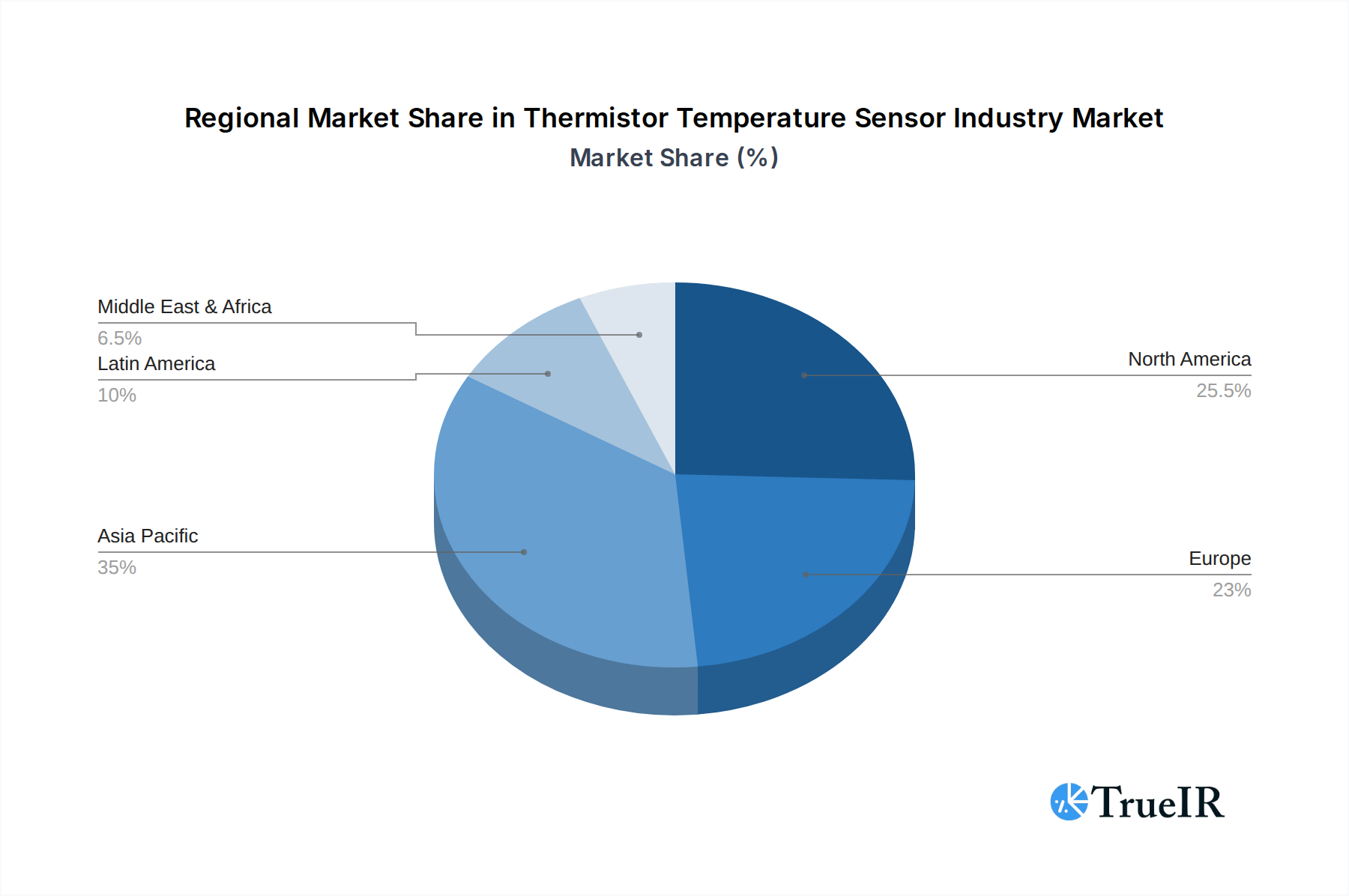

The global Thermistor Temperature Sensor Industry exhibits distinct regional dominance and segment leadership, driven by a confluence of industrial development, technological adoption, and regulatory frameworks. North America and Europe currently lead the market, primarily due to their established industrial bases, high adoption rates of advanced technologies, and stringent quality and safety standards. However, the Asia-Pacific region is emerging as the fastest-growing market, propelled by rapid industrialization, significant investments in manufacturing, and the burgeoning automotive and consumer electronics sectors in countries like China, South Korea, and India.

Within the Type segment, Negative Temperature Coefficient (NTC) thermistors currently hold a larger market share, estimated at around 60% in 2025. This dominance is attributed to their widespread use in consumer electronics, automotive applications, and general industrial temperature monitoring due to their cost-effectiveness and sensitivity over a broad temperature range. Positive Temperature Coefficient (PTC) thermistors, while currently holding a smaller share, are experiencing robust growth, driven by their self-regulating properties and application in overcurrent protection, motor starting, and heating elements.

In terms of End-user Applications, the Automotive sector is a dominant and rapidly expanding segment, projected to account for approximately 22% of the market revenue in 2025, with a strong CAGR of 7.0% during the forecast period. This growth is fueled by the increasing complexity of vehicle systems, particularly in electric vehicles (EVs) requiring sophisticated battery thermal management, engine control, and cabin climate systems. The HVAC sector, a traditional strong contender, is also a significant driver, representing around 18% of the market in 2025, with ongoing demand for energy-efficient building management systems and smart thermostats. The Semiconductor industry, with its insatiable need for precise temperature control in manufacturing processes and sensitive electronic components, represents another key segment, estimated at 16% of the market in 2025 and expected to grow at a CAGR of 6.8%. The Life Sciences sector, encompassing medical devices, diagnostics, and pharmaceutical cold chain logistics, is also a high-growth area, driven by an aging global population and advancements in healthcare technology, projected to grow at a CAGR of 7.2%. The Oil and Gas and Power Generation industries continue to rely heavily on thermistors for process monitoring and safety in harsh environments, while the Food and Beverage sector utilizes them for quality control and supply chain integrity.

- Dominant Regions:

- North America & Europe: Mature markets with high technological adoption.

- Asia-Pacific: Fastest-growing region driven by industrial expansion and consumer electronics.

- Dominant Segments (2025 Market Share Estimates):

- Type:

- Negative Temperature Coefficient (NTC): ~60%

- Positive Temperature Coefficient (PTC): ~40%

- End-user Application:

- Automotive: ~22% (High Growth CAGR: 7.0%)

- HVAC: ~18%

- Semiconductor: ~16% (Strong Growth CAGR: 6.8%)

- Life Sciences: ~10% (Very High Growth CAGR: 7.2%)

- Power Generation: ~8%

- Oil and Gas: ~7%

- Food and Beverage: ~6%

- Aerospace and Military: ~5%

- Chemical and Petrochemical: ~4%

- Metal and Mining: ~3%

- Other End-user Applications: ~1%

- Type:

Thermistor Temperature Sensor Industry Product Analysis

Product innovations in the Thermistor Temperature Sensor Industry are characterized by an ongoing pursuit of enhanced accuracy, miniaturization, and ruggedness for demanding environments. NTC thermistors continue to evolve with improved material formulations, leading to wider operating temperature ranges and reduced self-heating effects, crucial for high-precision applications in medical devices and analytical instrumentation. PTC thermistors are seeing advancements in their switching characteristics and current-carrying capacity, making them more effective for advanced motor protection and solid-state circuit breakers. The integration of thermistors with digital interfaces and embedded microcontrollers is enabling smarter, more communicative sensor solutions that can provide not just temperature readings but also diagnostic information and predictive maintenance alerts. Competitive advantages are being carved out through specialized product designs tailored to specific industry needs, such as automotive-grade thermistors that meet stringent environmental and vibration standards, or medical-grade sensors offering biocompatibility and enhanced sterilization resistance.

Key Drivers, Barriers & Challenges in Thermistor Temperature Sensor Industry

The Thermistor Temperature Sensor Industry is propelled by several key drivers, including the exponential growth of IoT devices and the increasing demand for smart, connected solutions that necessitate reliable temperature monitoring. The rapid expansion of the electric vehicle market is a significant catalyst, as thermistors are critical for battery thermal management and overall vehicle performance. Government initiatives promoting energy efficiency and industrial automation also contribute to market growth. Technological advancements in materials science and sensor miniaturization are enabling more sophisticated and cost-effective thermistor solutions.

However, the industry faces notable challenges and restraints. Supply chain disruptions, particularly for critical raw materials, can impact production and lead times, leading to increased costs and potential shortages, with estimated global impact on production capacity of up to 15% during periods of severe disruption. Intense price competition among numerous manufacturers, especially for standard NTC thermistors, puts pressure on profit margins. Regulatory hurdles and the need for continuous compliance with evolving environmental and safety standards add to operational costs. The presence of alternative temperature sensing technologies, such as RTDs and thermocouples, in certain niche applications, also poses a competitive challenge.

Growth Drivers in the Thermistor Temperature Sensor Industry Market

The growth of the Thermistor Temperature Sensor Industry is primarily fueled by technological advancements and the expanding applications across diverse sectors. The increasing penetration of IoT devices worldwide, projected to exceed 29 billion by 2025, creates a massive demand for cost-effective and reliable temperature sensors for data collection and control. The robust expansion of the automotive industry, particularly the surge in electric vehicle production and the implementation of advanced driver-assistance systems (ADAS), requires sophisticated thermal management solutions where thermistors play a crucial role. Furthermore, government policies promoting energy efficiency and industrial automation across sectors like manufacturing, power generation, and smart buildings are significant growth catalysts, driving the adoption of advanced temperature sensing technologies for process optimization and predictive maintenance. The growing healthcare sector, with its increasing reliance on temperature-sensitive medical devices and pharmaceuticals, also presents substantial growth opportunities.

Challenges Impacting Thermistor Temperature Sensor Industry Growth

The Thermistor Temperature Sensor Industry faces several critical challenges that can impact its growth trajectory. Intense price competition, especially in the high-volume NTC thermistor segment, often leads to shrinking profit margins for manufacturers, necessitating a strong focus on operational efficiency and cost management. Global supply chain vulnerabilities, as evidenced by recent disruptions impacting critical raw material availability and logistics, can lead to increased lead times and production costs, potentially hindering timely order fulfillment. Navigating complex and evolving regulatory landscapes, including environmental standards and product safety certifications across different regions, adds to compliance costs and can create barriers to market entry for smaller players. The constant threat of substitution by alternative temperature sensing technologies like RTDs and thermocouples in certain high-precision or specialized applications requires continuous innovation and differentiation to maintain market share.

Key Players Shaping the Thermistor Temperature Sensor Industry Market

- Shibaura Electronics Co Ltd

- Honeywell International Inc

- Lattron Company Limited

- KOA Corporation

- Mitsubishi Materials Corporation

- Ohizumi Manufacturing Company Limited

- Texas Instruments Incorporated

- TE Connectivity

- Panasonic Corporation

- Emerson Electric Company

Significant Thermistor Temperature Sensor Industry Industry Milestones

- 2019 Q1: Increased adoption of AI-driven predictive maintenance in industrial settings, boosting demand for smart thermistors.

- 2020 Q3: Global supply chain disruptions highlight vulnerabilities, prompting increased focus on regional sourcing strategies for thermistor components.

- 2021 Q2: Significant advancements in material science lead to the development of thermistors with wider operating temperature ranges and enhanced accuracy.

- 2022 Q1: Surge in electric vehicle production accelerates demand for specialized automotive-grade thermistors.

- 2022 Q4: Panasonic Corporation announces strategic investment in high-precision sensor technology for the life sciences sector.

- 2023 Q3: TE Connectivity expands its portfolio of miniaturized thermistors for IoT and wearable device applications.

- 2024 Q1: Honeywell International Inc. showcases integrated sensor solutions with enhanced connectivity for smart building management systems.

Future Outlook for Thermistor Temperature Sensor Industry Market

The future outlook for the Thermistor Temperature Sensor Industry remains exceptionally bright, driven by the relentless march of digital transformation and the increasing imperative for precision temperature control. The proliferation of IoT devices, coupled with the expanding capabilities of smart technologies, will continue to be a primary growth catalyst, demanding more intelligent and interconnected thermistor solutions. The automotive sector, especially with the ongoing transition to electric mobility and autonomous driving technologies, will remain a key market, requiring advanced thermal management systems where thermistors are indispensable. Furthermore, the growing emphasis on healthcare innovation, energy efficiency, and sustainable industrial practices will create sustained demand for high-performance and reliable temperature sensing. Strategic opportunities lie in the development of advanced materials, enhanced sensor integration with data analytics platforms, and the expansion into emerging economies where industrialization and technological adoption are rapidly accelerating. The industry is poised for continued innovation and significant market expansion in the coming years.

Thermistor Temperature Sensor Industry Segmentation

-

1. Type

- 1.1. Positive Temperature Coefficient (PTC)

- 1.2. Negative Temperature Coefficient (NTC)

-

2. End-user Application

- 2.1. Chemical and Petrochemical

- 2.2. Power Generation

- 2.3. Metal and Mining

- 2.4. Semiconductor

- 2.5. Automotive

- 2.6. Oil and Gas

- 2.7. Food and Beverage

- 2.8. Life Sciences

- 2.9. Aerospace and Military (includes Aviation)

- 2.10. HVAC

- 2.11. Other End-user Applications

Thermistor Temperature Sensor Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

Thermistor Temperature Sensor Industry Regional Market Share

Geographic Coverage of Thermistor Temperature Sensor Industry

Thermistor Temperature Sensor Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Positive Temperature Coefficient (PTC)

- 5.1.2. Negative Temperature Coefficient (NTC)

- 5.2. Market Analysis, Insights and Forecast - by End-user Application

- 5.2.1. Chemical and Petrochemical

- 5.2.2. Power Generation

- 5.2.3. Metal and Mining

- 5.2.4. Semiconductor

- 5.2.5. Automotive

- 5.2.6. Oil and Gas

- 5.2.7. Food and Beverage

- 5.2.8. Life Sciences

- 5.2.9. Aerospace and Military (includes Aviation)

- 5.2.10. HVAC

- 5.2.11. Other End-user Applications

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Latin America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Thermistor Temperature Sensor Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Positive Temperature Coefficient (PTC)

- 6.1.2. Negative Temperature Coefficient (NTC)

- 6.2. Market Analysis, Insights and Forecast - by End-user Application

- 6.2.1. Chemical and Petrochemical

- 6.2.2. Power Generation

- 6.2.3. Metal and Mining

- 6.2.4. Semiconductor

- 6.2.5. Automotive

- 6.2.6. Oil and Gas

- 6.2.7. Food and Beverage

- 6.2.8. Life Sciences

- 6.2.9. Aerospace and Military (includes Aviation)

- 6.2.10. HVAC

- 6.2.11. Other End-user Applications

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America Thermistor Temperature Sensor Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Positive Temperature Coefficient (PTC)

- 7.1.2. Negative Temperature Coefficient (NTC)

- 7.2. Market Analysis, Insights and Forecast - by End-user Application

- 7.2.1. Chemical and Petrochemical

- 7.2.2. Power Generation

- 7.2.3. Metal and Mining

- 7.2.4. Semiconductor

- 7.2.5. Automotive

- 7.2.6. Oil and Gas

- 7.2.7. Food and Beverage

- 7.2.8. Life Sciences

- 7.2.9. Aerospace and Military (includes Aviation)

- 7.2.10. HVAC

- 7.2.11. Other End-user Applications

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe Thermistor Temperature Sensor Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Positive Temperature Coefficient (PTC)

- 8.1.2. Negative Temperature Coefficient (NTC)

- 8.2. Market Analysis, Insights and Forecast - by End-user Application

- 8.2.1. Chemical and Petrochemical

- 8.2.2. Power Generation

- 8.2.3. Metal and Mining

- 8.2.4. Semiconductor

- 8.2.5. Automotive

- 8.2.6. Oil and Gas

- 8.2.7. Food and Beverage

- 8.2.8. Life Sciences

- 8.2.9. Aerospace and Military (includes Aviation)

- 8.2.10. HVAC

- 8.2.11. Other End-user Applications

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Asia Pacific Thermistor Temperature Sensor Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Positive Temperature Coefficient (PTC)

- 9.1.2. Negative Temperature Coefficient (NTC)

- 9.2. Market Analysis, Insights and Forecast - by End-user Application

- 9.2.1. Chemical and Petrochemical

- 9.2.2. Power Generation

- 9.2.3. Metal and Mining

- 9.2.4. Semiconductor

- 9.2.5. Automotive

- 9.2.6. Oil and Gas

- 9.2.7. Food and Beverage

- 9.2.8. Life Sciences

- 9.2.9. Aerospace and Military (includes Aviation)

- 9.2.10. HVAC

- 9.2.11. Other End-user Applications

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Latin America Thermistor Temperature Sensor Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Positive Temperature Coefficient (PTC)

- 10.1.2. Negative Temperature Coefficient (NTC)

- 10.2. Market Analysis, Insights and Forecast - by End-user Application

- 10.2.1. Chemical and Petrochemical

- 10.2.2. Power Generation

- 10.2.3. Metal and Mining

- 10.2.4. Semiconductor

- 10.2.5. Automotive

- 10.2.6. Oil and Gas

- 10.2.7. Food and Beverage

- 10.2.8. Life Sciences

- 10.2.9. Aerospace and Military (includes Aviation)

- 10.2.10. HVAC

- 10.2.11. Other End-user Applications

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Shibaura Electronics Co Ltd

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Honeywell International Inc

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Lattron Company Limited

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 KOA Corporation

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Mitsubishi Materials Corporation

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Ohizumi Manufacturing Company Limited

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Texas Instruments Incorporated

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 TE Connectivity*List Not Exhaustive

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Panasonic Corporation

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Emerson Electric Company

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.1 Shibaura Electronics Co Ltd

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Thermistor Temperature Sensor Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Thermistor Temperature Sensor Industry Revenue (billion), by Type 2025 & 2033

- Figure 3: North America Thermistor Temperature Sensor Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America Thermistor Temperature Sensor Industry Revenue (billion), by End-user Application 2025 & 2033

- Figure 5: North America Thermistor Temperature Sensor Industry Revenue Share (%), by End-user Application 2025 & 2033

- Figure 6: North America Thermistor Temperature Sensor Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Thermistor Temperature Sensor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Thermistor Temperature Sensor Industry Revenue (billion), by Type 2025 & 2033

- Figure 9: Europe Thermistor Temperature Sensor Industry Revenue Share (%), by Type 2025 & 2033

- Figure 10: Europe Thermistor Temperature Sensor Industry Revenue (billion), by End-user Application 2025 & 2033

- Figure 11: Europe Thermistor Temperature Sensor Industry Revenue Share (%), by End-user Application 2025 & 2033

- Figure 12: Europe Thermistor Temperature Sensor Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe Thermistor Temperature Sensor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Thermistor Temperature Sensor Industry Revenue (billion), by Type 2025 & 2033

- Figure 15: Asia Pacific Thermistor Temperature Sensor Industry Revenue Share (%), by Type 2025 & 2033

- Figure 16: Asia Pacific Thermistor Temperature Sensor Industry Revenue (billion), by End-user Application 2025 & 2033

- Figure 17: Asia Pacific Thermistor Temperature Sensor Industry Revenue Share (%), by End-user Application 2025 & 2033

- Figure 18: Asia Pacific Thermistor Temperature Sensor Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Asia Pacific Thermistor Temperature Sensor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Latin America Thermistor Temperature Sensor Industry Revenue (billion), by Type 2025 & 2033

- Figure 21: Latin America Thermistor Temperature Sensor Industry Revenue Share (%), by Type 2025 & 2033

- Figure 22: Latin America Thermistor Temperature Sensor Industry Revenue (billion), by End-user Application 2025 & 2033

- Figure 23: Latin America Thermistor Temperature Sensor Industry Revenue Share (%), by End-user Application 2025 & 2033

- Figure 24: Latin America Thermistor Temperature Sensor Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Latin America Thermistor Temperature Sensor Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Thermistor Temperature Sensor Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Global Thermistor Temperature Sensor Industry Revenue billion Forecast, by End-user Application 2020 & 2033

- Table 3: Global Thermistor Temperature Sensor Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Thermistor Temperature Sensor Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 5: Global Thermistor Temperature Sensor Industry Revenue billion Forecast, by End-user Application 2020 & 2033

- Table 6: Global Thermistor Temperature Sensor Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Global Thermistor Temperature Sensor Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 8: Global Thermistor Temperature Sensor Industry Revenue billion Forecast, by End-user Application 2020 & 2033

- Table 9: Global Thermistor Temperature Sensor Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 10: Global Thermistor Temperature Sensor Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 11: Global Thermistor Temperature Sensor Industry Revenue billion Forecast, by End-user Application 2020 & 2033

- Table 12: Global Thermistor Temperature Sensor Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Global Thermistor Temperature Sensor Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 14: Global Thermistor Temperature Sensor Industry Revenue billion Forecast, by End-user Application 2020 & 2033

- Table 15: Global Thermistor Temperature Sensor Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Thermistor Temperature Sensor Industry?

The projected CAGR is approximately 3.8%.

2. Which companies are prominent players in the Thermistor Temperature Sensor Industry?

Key companies in the market include Shibaura Electronics Co Ltd, Honeywell International Inc, Lattron Company Limited, KOA Corporation, Mitsubishi Materials Corporation, Ohizumi Manufacturing Company Limited, Texas Instruments Incorporated, TE Connectivity*List Not Exhaustive, Panasonic Corporation, Emerson Electric Company.

3. What are the main segments of the Thermistor Temperature Sensor Industry?

The market segments include Type, End-user Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 7.43 billion as of 2022.

5. What are some drivers contributing to market growth?

; Demand for Cost Effective and Improved Response Rate Sensors; Growing Applications in Consumer Electronics and Connected Devices.

6. What are the notable trends driving market growth?

Automotive Segment is Expected to Hold Significant Market Share.

7. Are there any restraints impacting market growth?

; Unsuitability of Thermistors for Wide Temperature Range and Price Point of Raw Materials.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Thermistor Temperature Sensor Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Thermistor Temperature Sensor Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Thermistor Temperature Sensor Industry?

To stay informed about further developments, trends, and reports in the Thermistor Temperature Sensor Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence