Key Insights

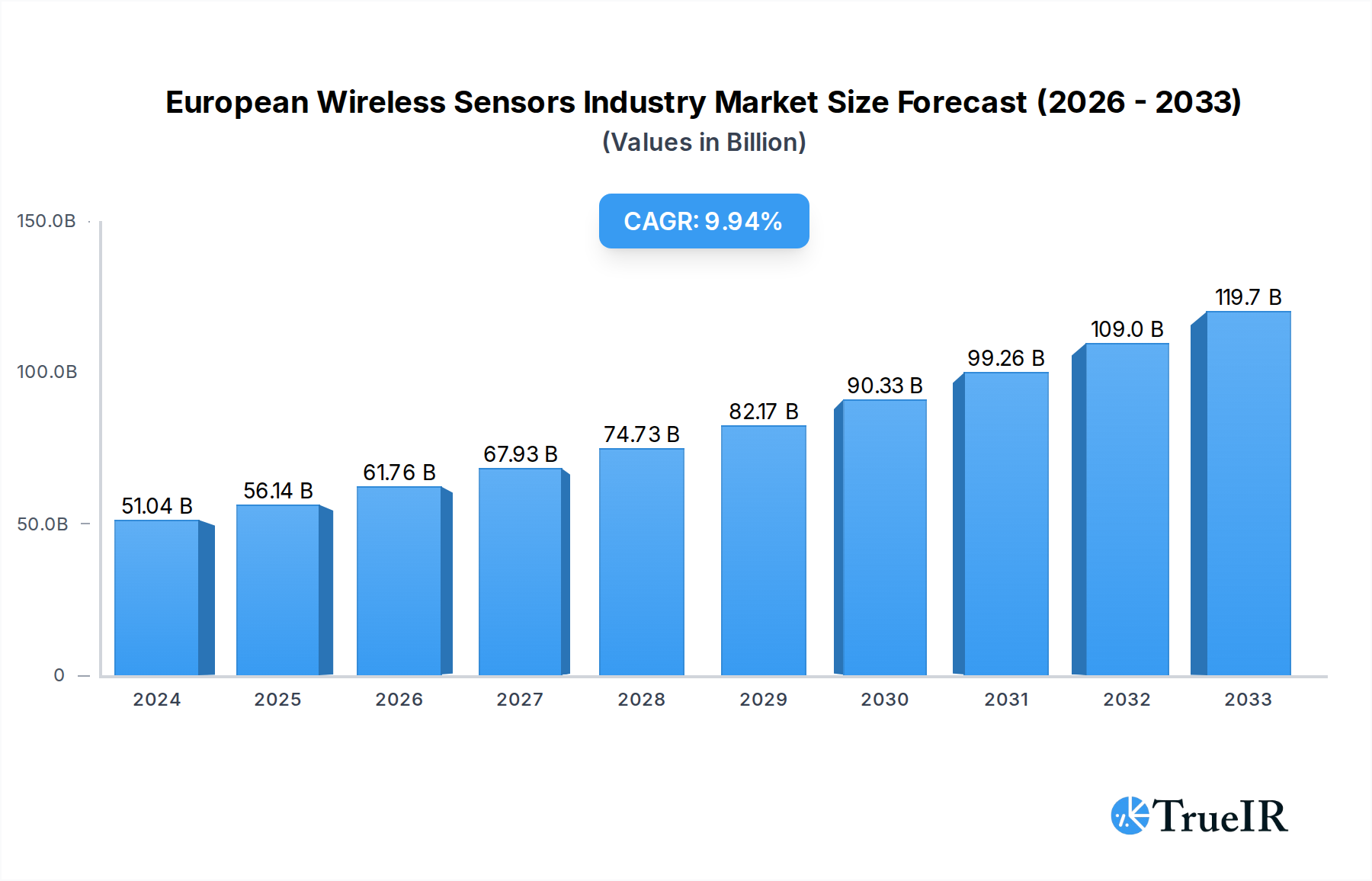

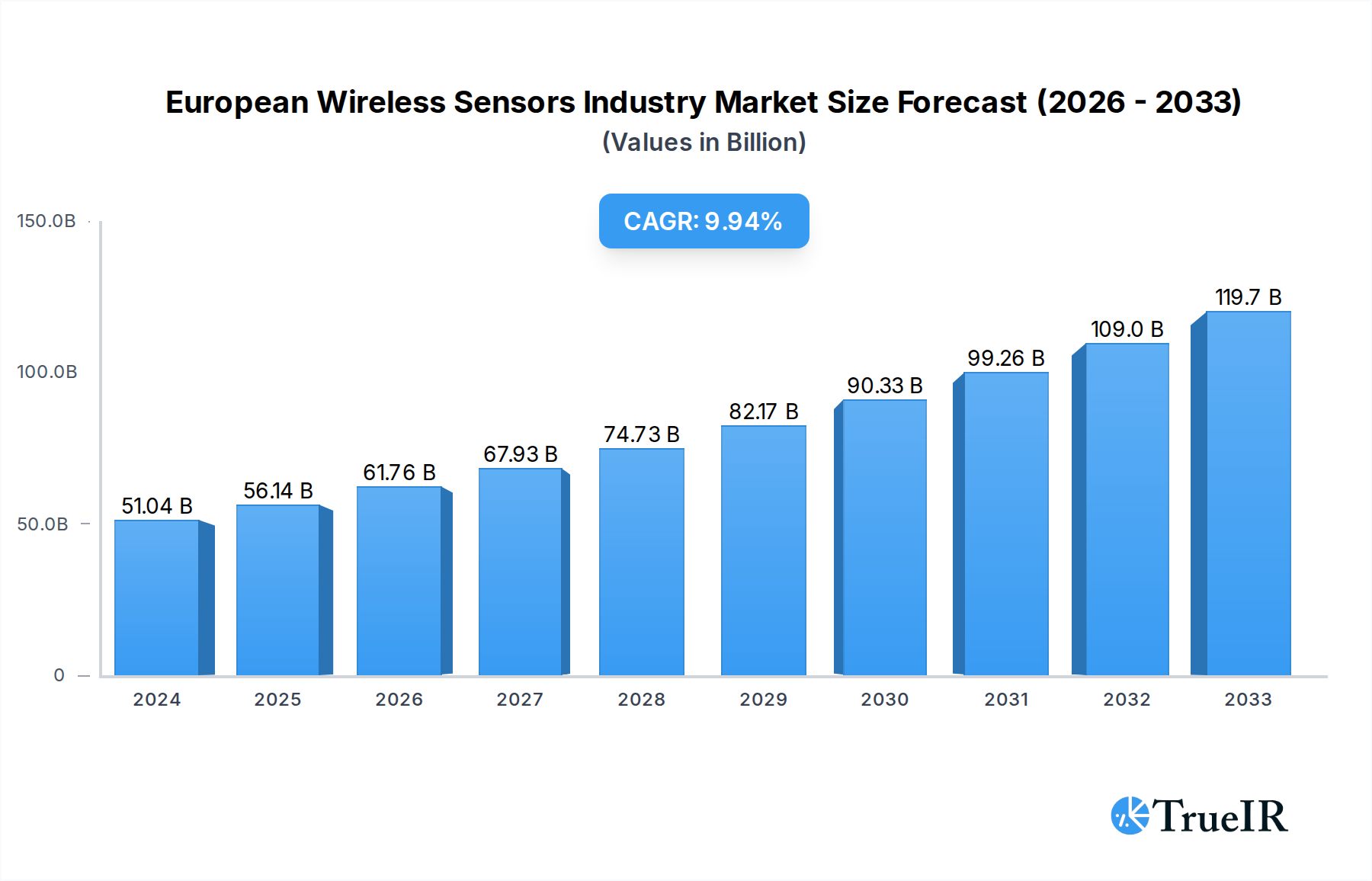

The European Wireless Sensors market is poised for significant expansion, driven by an increasing adoption of IoT technologies across various sectors. With a robust market size of USD 51.04 billion in 2024, the industry is projected to experience a substantial Compound Annual Growth Rate (CAGR) of 11% during the forecast period of 2025-2033. This growth is underpinned by advancements in sensor technology, miniaturization, and the development of more efficient power solutions, enabling wider deployment in industrial automation, smart homes, environmental monitoring, and healthcare. The demand for pressure, temperature, chemical, gas, and position sensors is escalating as businesses and governments invest heavily in smart infrastructure and data-driven decision-making. Key end-user industries like Automotive, Healthcare, and Energy & Power are leading this surge, leveraging wireless sensors for enhanced efficiency, safety, and predictive maintenance. Europe, with its strong industrial base and forward-thinking regulatory environment, is a critical hub for this market's development.

European Wireless Sensors Industry Market Size (In Billion)

The market's upward trajectory is further fueled by several key trends. The proliferation of 5G networks is creating a more robust ecosystem for real-time data transmission from wireless sensors, enabling sophisticated applications in areas like autonomous driving and remote patient monitoring. Furthermore, the growing emphasis on sustainability and energy efficiency is driving the adoption of wireless sensors for optimizing energy consumption in buildings and industrial processes. Despite these drivers, potential restraints such as cybersecurity concerns and the initial cost of implementing large-scale wireless sensor networks need to be addressed. However, ongoing research and development, coupled with strategic collaborations among major players like Honeywell International Inc., ABB Ltd., and Siemens AG, are expected to mitigate these challenges and unlock the full potential of the European Wireless Sensors market, solidifying its position as a vital component of the digital transformation across the continent.

European Wireless Sensors Industry Company Market Share

This comprehensive report provides an in-depth analysis of the European Wireless Sensors Industry, projecting a market value exceeding one billion Euros by 2033. The study covers the historical period from 2019 to 2024, with 2025 as the base and estimated year, and forecasts growth through 2033. Leveraging high-volume keywords such as "wireless sensors Europe," "industrial IoT sensors," "smart sensor market," and "connected devices," this report is meticulously crafted for maximum SEO impact and to engage a diverse industry audience including manufacturers, technology providers, and end-users.

European Wireless Sensors Industry Market Structure & Competitive Landscape

The European Wireless Sensors Industry is characterized by a moderately concentrated market, driven by continuous innovation in IoT integration and advanced sensing technologies. Key innovation drivers include the increasing demand for real-time data acquisition, predictive maintenance, and enhanced operational efficiency across various sectors. Regulatory impacts, such as evolving environmental standards and data security mandates, are shaping product development and market entry strategies. Product substitutes, while present in some niche applications, are increasingly being overshadowed by the versatility and cost-effectiveness of wireless sensor solutions. The end-user segmentation highlights a strong reliance on manufacturing, energy, and automotive sectors. Mergers and acquisitions (M&A) trends indicate a consolidation phase, with a growing number of strategic partnerships aimed at expanding market reach and technological capabilities. Quantitative analysis of M&A volumes suggests a steady increase in deal activity, reflecting the industry's maturity and the pursuit of market leadership. The concentration ratios in key segments are carefully examined to provide insights into competitive intensity.

European Wireless Sensors Industry Market Trends & Opportunities

The European Wireless Sensors Industry is poised for robust growth, with an estimated market size exceeding one billion Euros and a projected Compound Annual Growth Rate (CAGR) of XX% between 2025 and 2033. This expansion is fueled by several significant market trends, including the pervasive adoption of the Industrial Internet of Things (IIoT), the escalating demand for smart city infrastructure, and the growing imperative for energy efficiency in industrial and residential applications. Technological shifts are marked by advancements in miniaturization, power efficiency, and the integration of artificial intelligence (AI) and machine learning (ML) for enhanced data analytics. Consumer preferences are increasingly leaning towards solutions that offer seamless connectivity, user-friendly interfaces, and actionable insights derived from sensor data. Competitive dynamics are intensifying, with established players investing heavily in R&D to maintain a competitive edge and new entrants focusing on specialized applications and disruptive technologies. Market penetration rates for wireless sensors in critical infrastructure and manufacturing are expected to reach new heights, driven by the tangible ROI and operational improvements they enable. The opportunities for market expansion lie in emerging applications such as precision agriculture, advanced healthcare monitoring, and sophisticated supply chain management.

Dominant Markets & Segments in European Wireless Sensors Industry

Within the European Wireless Sensors Industry, several key segments and end-user industries exhibit significant dominance and growth potential.

Dominant Sensor Types:

- Temperature Sensors: Consistently high demand driven by industrial process control, HVAC systems, and cold chain logistics. Their ubiquity in monitoring and maintaining optimal conditions makes them foundational.

- Pressure Sensors: Crucial for automation in manufacturing, automotive systems, and fluid management, contributing significantly to operational safety and efficiency.

- Chemical and Gas Sensors: Experiencing rapid growth due to increased environmental monitoring regulations, industrial safety requirements, and smart home applications for air quality.

- Position and Proximity Sensors: Essential for automation, robotics, and safety systems in manufacturing and automotive sectors.

Dominant End-user Industries:

- Automotive: Extensive use in engine management, safety systems, infotainment, and increasingly, in autonomous driving technologies. The push for electric vehicles also drives demand for specialized battery monitoring sensors.

- Energy and Power: Critical for grid management, renewable energy monitoring (solar, wind), predictive maintenance of power generation equipment, and smart metering. The transition to sustainable energy sources significantly boosts this segment.

- Manufacturing: The backbone of the IIoT, enabling smart factories, predictive maintenance, quality control, and optimized production lines. Demand for sensors that can withstand harsh industrial environments is particularly high.

- Healthcare: Growing adoption for remote patient monitoring, asset tracking within hospitals, and environmental control in sensitive medical facilities.

- Aerospace and Defense: High-reliability sensors for critical applications, including structural health monitoring, environmental control in aircraft, and advanced surveillance systems.

Market dominance is further influenced by geographical factors, with countries like Germany, France, and the UK leading in adoption due to their robust industrial bases and investment in smart technologies. Government policies supporting digitalization and Industry 4.0 initiatives are key growth drivers, alongside substantial private sector investment in automation and connected solutions. The infrastructure for widespread IoT deployment, including robust communication networks, is also a critical enabler of market dominance.

European Wireless Sensors Industry Product Analysis

Product innovations in the European Wireless Sensors Industry are primarily focused on miniaturization, enhanced power efficiency, and increased data processing capabilities at the edge. Advances in materials science and semiconductor technology are enabling smaller, more robust sensors that can operate reliably in extreme environments, from sub-zero temperatures to explosive atmospheres. The integration of AI and machine learning directly into sensor modules allows for real-time anomaly detection and predictive analytics, reducing the burden on cloud infrastructure and enabling faster decision-making. Key applications span industrial automation, environmental monitoring, smart homes, and advanced automotive systems. Competitive advantages are increasingly derived from superior accuracy, extended battery life, seamless connectivity protocols (e.g., LoRaWAN, NB-IoT), and robust cybersecurity features, making them ideal for demanding IIoT deployments.

Key Drivers, Barriers & Challenges in European Wireless Sensors Industry

Key Drivers:

- Technological Advancements: The continuous evolution of IoT, AI, and miniaturization technologies is a primary growth catalyst.

- Demand for IIoT and Automation: Industrial sectors are increasingly adopting wireless sensors to enhance operational efficiency, reduce downtime through predictive maintenance, and improve safety.

- Government Initiatives and Regulations: Support for Industry 4.0, smart city projects, and stricter environmental monitoring mandates are driving adoption.

- Cost-Effectiveness: Reduced installation costs and wiring complexities compared to wired solutions make wireless sensors an attractive option.

Key Barriers & Challenges:

- Connectivity and Network Infrastructure: While improving, consistent and reliable connectivity across all regions and industrial settings remains a challenge.

- Cybersecurity Concerns: Protecting sensitive data transmitted by wireless sensors from cyber threats is a critical concern for end-users.

- Interoperability and Standardization: A lack of universal standards can lead to compatibility issues between different sensor brands and systems.

- Power Consumption and Battery Life: Despite advancements, achieving extremely long battery life in certain demanding applications remains an ongoing challenge.

- Regulatory Compliance: Navigating diverse and evolving regulatory landscapes, especially concerning data privacy and environmental impact, can be complex.

Growth Drivers in the European Wireless Sensors Industry Market

Key growth drivers in the European Wireless Sensors Industry are predominantly technological, economic, and policy-driven. The relentless march of the Industrial Internet of Things (IIoT) is arguably the most significant catalyst, compelling industries to adopt smart sensing solutions for enhanced automation, efficiency, and predictive maintenance. Economic factors, such as the pursuit of operational cost reduction and improved asset utilization across sectors like manufacturing and energy, further fuel demand. Government initiatives promoting digitalization, smart city development, and sustainability goals provide a supportive policy framework. For instance, the European Green Deal indirectly encourages the adoption of sensors for monitoring emissions and optimizing energy consumption. The increasing need for real-time data in sectors like healthcare for remote patient monitoring and in logistics for supply chain visibility are also substantial growth engines.

Challenges Impacting European Wireless Sensors Industry Growth

Several challenges impact the growth trajectory of the European Wireless Sensors Industry. Regulatory complexities, particularly concerning data privacy (e.g., GDPR) and the varying standards across member states, can create hurdles for widespread deployment. Supply chain issues, including the availability of critical components and the potential for geopolitical disruptions, can affect production and lead times, impacting market responsiveness. Competitive pressures are intense, with a crowded marketplace requiring continuous innovation and strategic pricing to maintain market share. Furthermore, the perceived upfront investment cost for some advanced wireless sensor solutions, despite long-term ROI, can be a barrier for smaller enterprises. Ensuring robust cybersecurity for connected devices and mitigating the risks of data breaches remain paramount concerns for potential adopters.

Key Players Shaping the European Wireless Sensors Industry Market

- Honeywell International Inc

- ABB Ltd

- Monnit Corporation

- Schneider Electric

- Phoenix Sensors LLC

- Texas Instruments Incorporated

- Pasco Scientific

- Emerson Electric Co

- Siemens AG

Significant European Wireless Sensors Industry Industry Milestones

- January 2021: Disruptive Technologies (DT) collaborated with Ex-tech Group, introducing smallest wireless sensors with IP68 ratings for extreme temperatures and explosive atmospheres, enabling accurate monitoring of humidity, temperature, and proximity/presence directly on Ex-protected equipment. This development significantly expands deployment possibilities in hazardous environments.

- June 2020: ABB announced a wireless condition monitoring solution for rotating equipment on an industrial scale. This innovation drastically reduces the expense and complexity of sensor installation, enabling large sites like automotive plants and processing facilities to collect valuable operational data from rotating equipment using ABB Ability™ Smart Sensor technology and Aruba Wi-Fi infrastructure.

Future Outlook for European Wireless Sensors Industry Market

The future outlook for the European Wireless Sensors Industry is exceptionally bright, driven by the continued digital transformation across all major economic sectors. Strategic opportunities abound in the expansion of smart grids, the growth of electric vehicle infrastructure, and the increasing adoption of predictive maintenance in manufacturing and critical infrastructure. The market potential is further amplified by the ongoing miniaturization and integration of AI capabilities into sensors, paving the way for more sophisticated and autonomous data collection and analysis. Emerging trends such as the metaverse and advanced augmented reality applications will likely create new avenues for sensor integration. The industry is set to witness substantial growth as businesses across Europe increasingly rely on real-time data to optimize operations, enhance safety, and drive innovation.

European Wireless Sensors Industry Segmentation

-

1. Type

- 1.1. Pressure Sensor

- 1.2. Temperature Sensor

- 1.3. Chemical and Gas Sensor

- 1.4. Position and Proximity Sensor

- 1.5. Other Types

-

2. End-user Industry

- 2.1. Automotive

- 2.2. Healthcare

- 2.3. Aerospace and Defense

- 2.4. Energy and Power

- 2.5. Food and Beverage

- 2.6. Other End-user Industries

European Wireless Sensors Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

European Wireless Sensors Industry Regional Market Share

Geographic Coverage of European Wireless Sensors Industry

European Wireless Sensors Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Pressure Sensor

- 5.1.2. Temperature Sensor

- 5.1.3. Chemical and Gas Sensor

- 5.1.4. Position and Proximity Sensor

- 5.1.5. Other Types

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Automotive

- 5.2.2. Healthcare

- 5.2.3. Aerospace and Defense

- 5.2.4. Energy and Power

- 5.2.5. Food and Beverage

- 5.2.6. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. European Wireless Sensors Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Pressure Sensor

- 6.1.2. Temperature Sensor

- 6.1.3. Chemical and Gas Sensor

- 6.1.4. Position and Proximity Sensor

- 6.1.5. Other Types

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Automotive

- 6.2.2. Healthcare

- 6.2.3. Aerospace and Defense

- 6.2.4. Energy and Power

- 6.2.5. Food and Beverage

- 6.2.6. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Honeywell International Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 ABB Ltd

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Monnit Corporation

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Schneider Electric

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Phoenix Sensors LLC

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Texas Instruments Incorporated*List Not Exhaustive

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Pasco Scientific

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Emerson Electric Co

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Siemens AG

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 Honeywell International Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: European Wireless Sensors Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: European Wireless Sensors Industry Share (%) by Company 2025

List of Tables

- Table 1: European Wireless Sensors Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: European Wireless Sensors Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 3: European Wireless Sensors Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: European Wireless Sensors Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 5: European Wireless Sensors Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 6: European Wireless Sensors Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United Kingdom European Wireless Sensors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Germany European Wireless Sensors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: France European Wireless Sensors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Italy European Wireless Sensors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Spain European Wireless Sensors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Netherlands European Wireless Sensors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Belgium European Wireless Sensors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Sweden European Wireless Sensors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Norway European Wireless Sensors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Poland European Wireless Sensors Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Denmark European Wireless Sensors Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the European Wireless Sensors Industry?

The projected CAGR is approximately 11%.

2. Which companies are prominent players in the European Wireless Sensors Industry?

Key companies in the market include Honeywell International Inc, ABB Ltd, Monnit Corporation, Schneider Electric, Phoenix Sensors LLC, Texas Instruments Incorporated*List Not Exhaustive, Pasco Scientific, Emerson Electric Co, Siemens AG.

3. What are the main segments of the European Wireless Sensors Industry?

The market segments include Type, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 51.04 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Adoption of Wireless Technologies (Especially in Harsh Environments); Emergence of Smart Factory Concepts (Industrial Automation).

6. What are the notable trends driving market growth?

Automotive is Expected to Hold Significant Market Share.

7. Are there any restraints impacting market growth?

False Triggering of Switch and Inconsistency Issues Associated with Wireless Network Systems.

8. Can you provide examples of recent developments in the market?

January 2021 - Disruptive Technologies (DT), a Norwegian developer smallest wireless sensors, collaborated with Ex-tech Group, an expert in the ex-area. Sensors from Disruptive Technologies have an IP68 rating and can withstand extremely high temperatures. Moreover, sensors can measure critical humidity, temperature, and proximity/presence in explosive atmospheres. Owing to the ex-protection, they can be deployed directly on/in other Ex-protected equipment. The sensor solution provides accurate monitoring and reporting of operational data continuously.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "European Wireless Sensors Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the European Wireless Sensors Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the European Wireless Sensors Industry?

To stay informed about further developments, trends, and reports in the European Wireless Sensors Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence