Key Insights

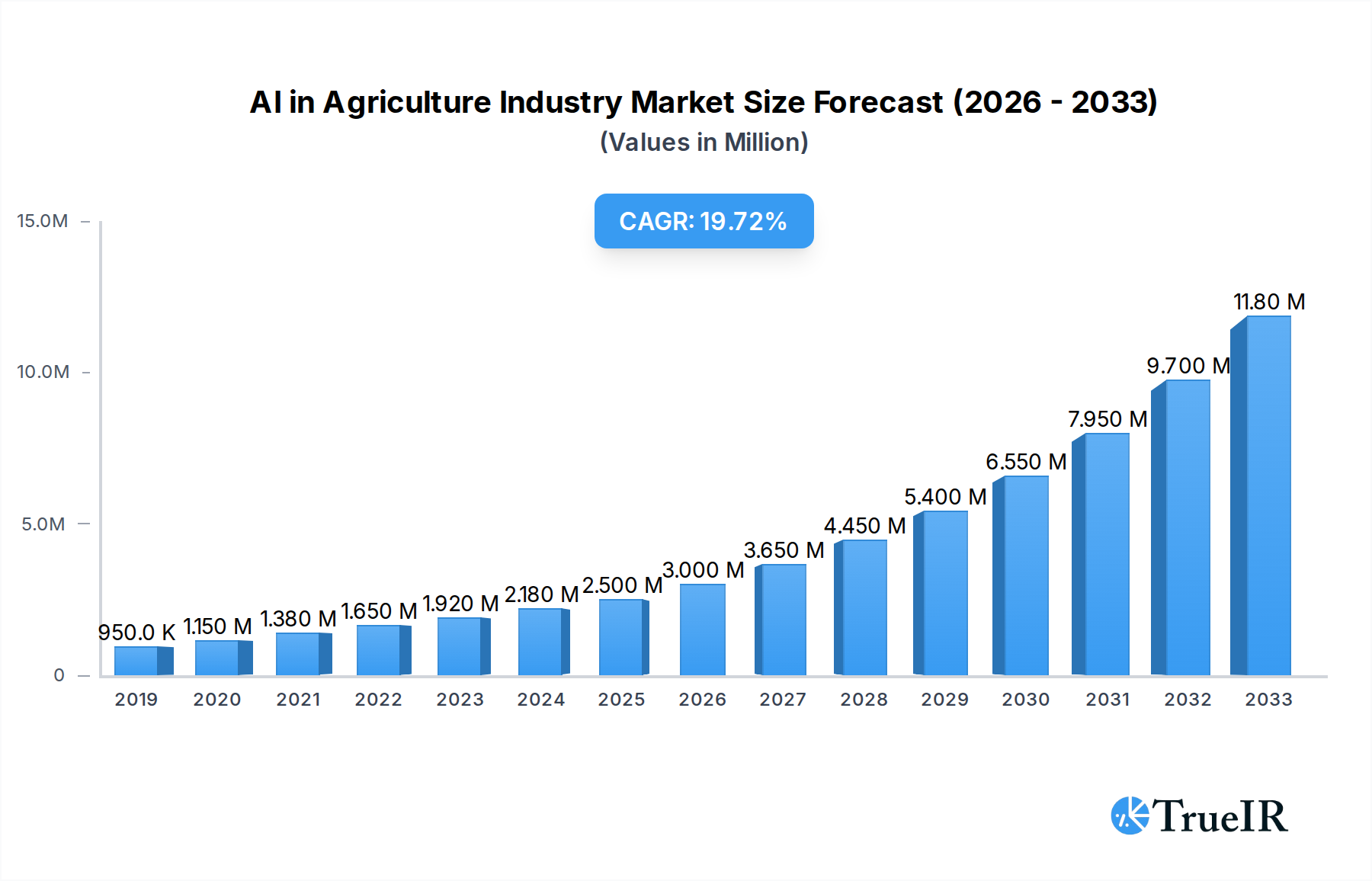

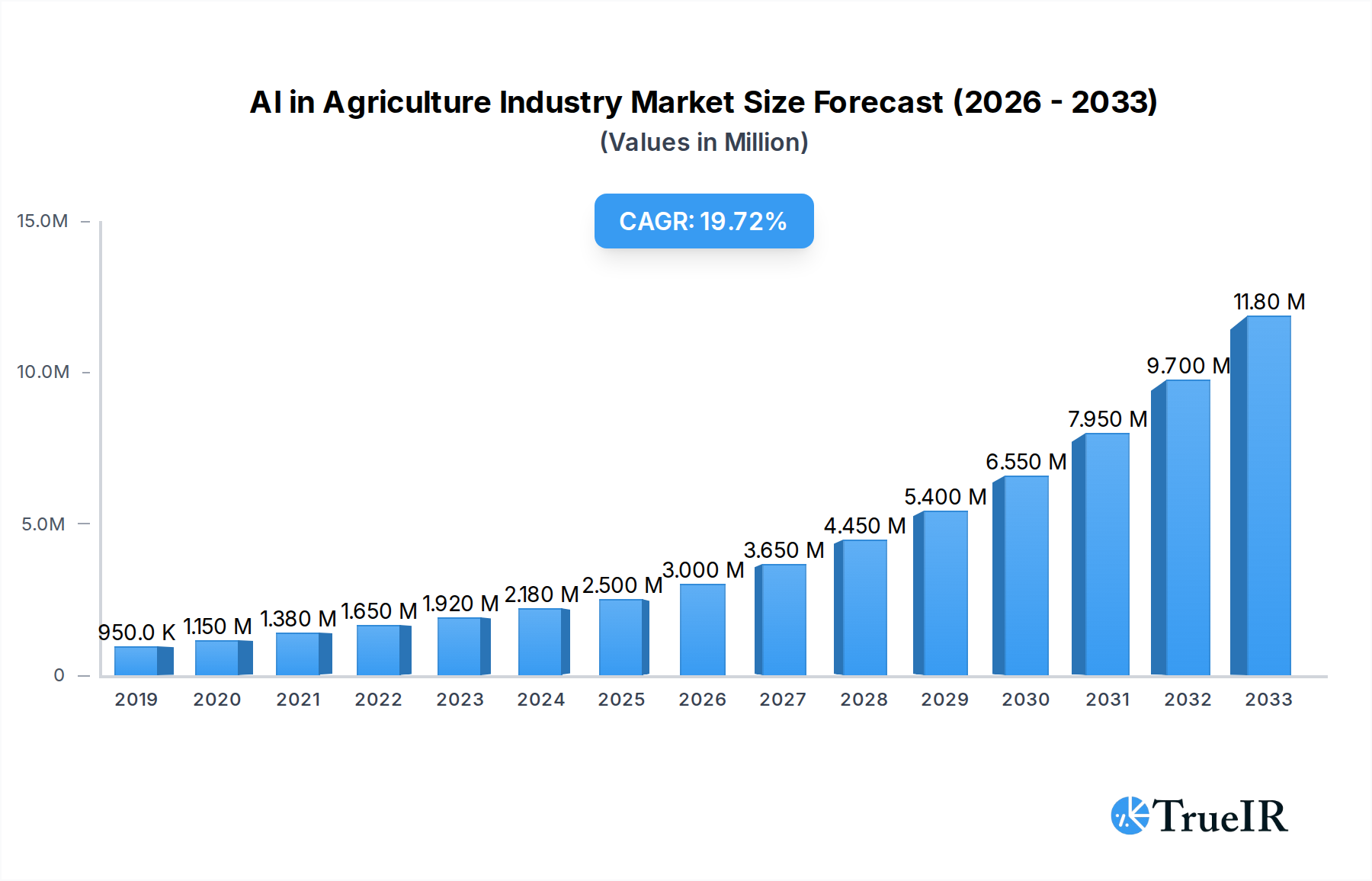

The AI in Agriculture market is poised for exceptional growth, currently valued at 2.08 Billion USD and projected to expand at a robust CAGR of 22.55% through 2033. This rapid ascent is fueled by a confluence of powerful drivers, including the escalating need for enhanced crop yields to feed a burgeoning global population, the critical imperative to optimize resource utilization (water, fertilizers, and pesticides) in the face of environmental challenges, and the increasing adoption of smart farming technologies to mitigate labor shortages. Furthermore, the rising awareness of sustainable agricultural practices and government initiatives supporting technological advancements in the sector are acting as significant catalysts. Key applications like Weather Tracking and Precision Farming are at the forefront, leveraging AI for real-time data analysis and actionable insights. The dominant deployment models are Cloud and Hybrid solutions, offering scalability and accessibility to a wider range of agricultural operations.

AI in Agriculture Industry Market Size (In Million)

The market's trajectory is further shaped by several influential trends. The integration of IoT devices and sensors is providing an unprecedented volume of granular data, which AI algorithms are adept at transforming into predictive analytics and automated decision-making. Advanced drone analytics are revolutionizing crop monitoring, pest detection, and targeted spraying, leading to significant cost savings and environmental benefits. The development of AI-powered robotics for tasks such as autonomous planting, harvesting, and weed control is also gaining momentum, promising to address labor scarcity and improve operational efficiency. While the market enjoys strong growth, potential restraints include the high initial investment costs for advanced AI systems, the need for specialized technical expertise among farmers, and concerns surrounding data privacy and security. However, the continuous innovation from leading companies like IBM Corporation, Microsoft Corporation, and PrecisionHawk Inc. is actively working to overcome these challenges, solidifying AI's indispensable role in the future of agriculture.

AI in Agriculture Industry Company Market Share

This in-depth report delves into the rapidly evolving AI in Agriculture Industry, providing critical insights into market dynamics, technological advancements, and future growth trajectories. Designed for industry professionals, investors, and policymakers, this analysis leverages high-volume keywords to enhance SEO visibility and deliver actionable intelligence. The study period spans from 2019 to 2033, with a base and estimated year of 2025, and a comprehensive forecast period from 2025 to 2033, building upon historical data from 2019-2024.

AI in Agriculture Industry Market Structure & Competitive Landscape

The AI in Agriculture Industry exhibits a dynamic market structure characterized by both established giants and emerging innovators. Market concentration is moderate, with key players like IBM Corporation and Microsoft Corporation dominating significant market shares due to their extensive R&D investments and integrated solutions. However, a surge in specialized startups such as Prospera Technologies Ltd, Cainthus Corp, and ec2ce fosters intense competition and drives innovation. Innovation drivers are primarily fueled by the increasing demand for sustainable farming practices, the need for enhanced crop yields, and the reduction of operational costs. Regulatory impacts are evolving, with governments worldwide establishing frameworks to encourage the adoption of agricultural technology while ensuring data privacy and ethical AI deployment. Product substitutes are limited in their ability to replicate the comprehensive insights and automation offered by AI solutions, but traditional farming methods still represent a significant portion of the market. End-user segmentation reveals a growing adoption across large-scale commercial farms, medium-sized operations, and increasingly, smaller, specialized agricultural enterprises. Merger and acquisition (M&A) trends are on the rise, with an estimated volume of over 100 Million in the historical period, as larger companies seek to acquire innovative technologies and expand their market reach. Analyzing these intricate market dynamics is crucial for understanding competitive advantages and future growth opportunities.

AI in Agriculture Industry Market Trends & Opportunities

The AI in Agriculture Industry is experiencing an unprecedented growth phase, with a projected market size to exceed 50 Billion by the end of the forecast period. This robust expansion is driven by a convergence of technological shifts, evolving consumer preferences for sustainably sourced food, and a growing awareness of the critical role AI plays in addressing global food security challenges. The Compound Annual Growth Rate (CAGR) is estimated to be a remarkable 25%, underscoring the rapid adoption and transformative potential of AI in this sector. Key technological shifts include the democratization of advanced analytics, the proliferation of IoT devices on farms, and the increasing accuracy of predictive modeling for crop health and yield optimization. Consumer preferences are increasingly leaning towards transparency, reduced environmental impact, and higher quality produce, all of which are significantly enhanced by AI-driven farming techniques. This has opened up substantial opportunities for AI solution providers to develop and deploy platforms that offer tangible benefits such as optimized resource allocation, reduced pesticide and water usage, and improved farm management efficiency. The competitive landscape is characterized by strategic partnerships and the continuous development of novel AI applications, from early disease detection to autonomous farming operations. Market penetration rates are expected to climb from an estimated 20% in the base year to over 60% by 2033, indicating a significant shift towards AI-integrated agriculture. The opportunity lies in leveraging these trends to create solutions that address specific agricultural pain points, thereby fostering a more efficient, sustainable, and profitable agricultural ecosystem worldwide.

Dominant Markets & Segments in AI in Agriculture Industry

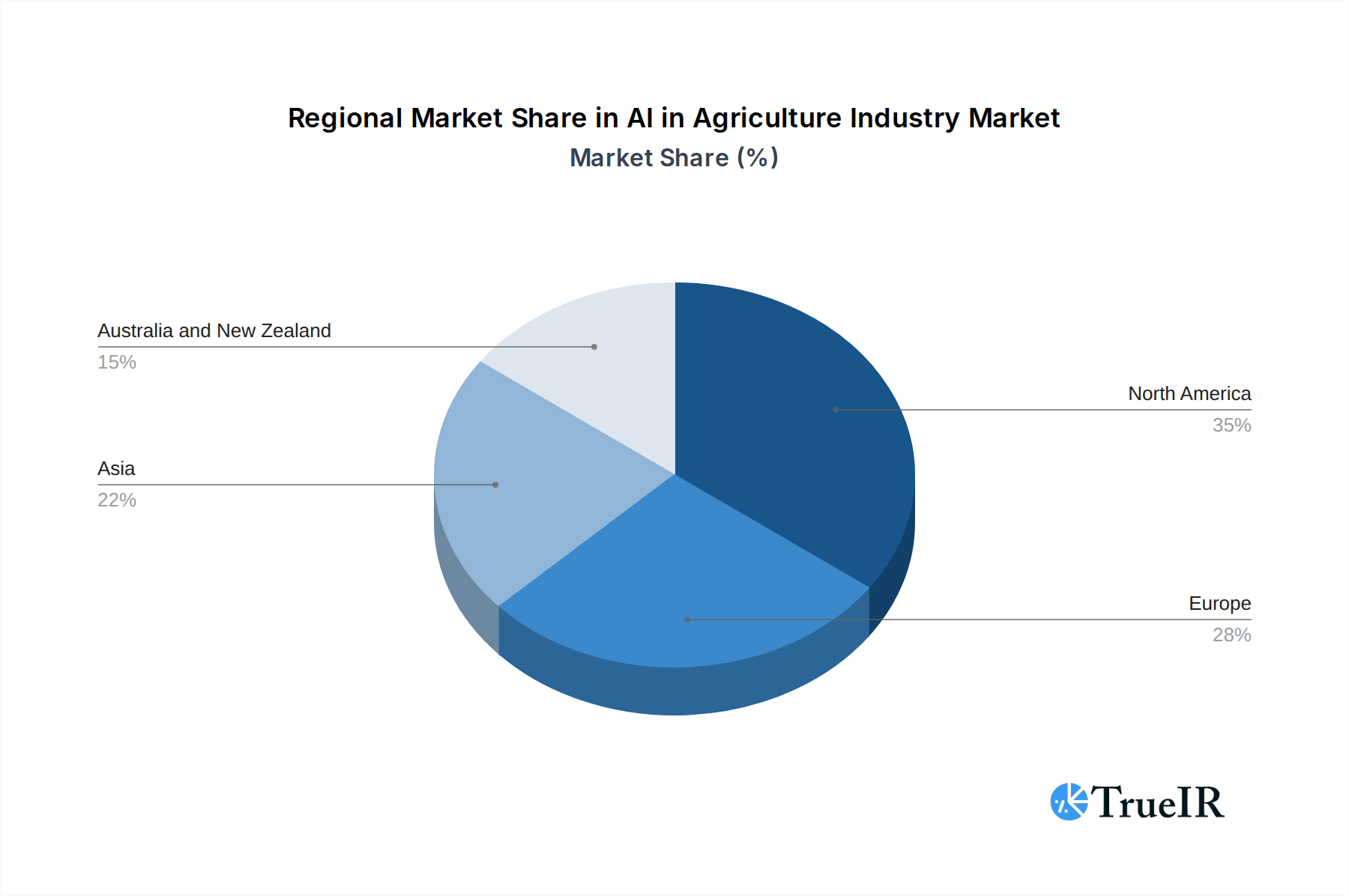

The AI in Agriculture Industry is witnessing pronounced dominance in specific regions and application segments, reflecting varying levels of technological adoption and infrastructural development. North America and Europe currently lead the market, driven by advanced agricultural infrastructure, significant government support, and a high concentration of AI technology providers. Within these regions, the Precision Farming segment is the most dominant application, accounting for an estimated 60% of the market share. This is propelled by the critical need for optimizing resource utilization, improving crop yields, and minimizing environmental impact. Key growth drivers for precision farming include government subsidies for precision agriculture technologies, the availability of high-speed internet and cloud infrastructure, and a strong farmer willingness to invest in advanced solutions. Drone Analytics is another rapidly growing segment, projected to capture over 25% of the market by the end of the forecast period. The increasing affordability and capability of drones, coupled with sophisticated AI-powered image analysis for crop health monitoring, pest detection, and yield estimation, are fueling this expansion. The Weather Tracking segment, while foundational, is increasingly integrated with other AI applications, providing crucial data for predictive analytics and decision-making, and is estimated to hold a 15% market share. In terms of deployment, Cloud-based solutions are experiencing the most significant growth, offering scalability, accessibility, and cost-effectiveness, estimated to account for over 70% of deployments. Hybrid deployments are also gaining traction, catering to diverse farm needs and connectivity limitations. On-premise solutions, while still relevant for specific use cases, are seeing slower growth. Understanding these dominant markets and segments is vital for strategic market entry and resource allocation, enabling stakeholders to capitalize on areas of high demand and rapid innovation within the AI in Agriculture Industry.

AI in Agriculture Industry Product Analysis

Product innovations in the AI in Agriculture Industry are revolutionizing farming practices through sophisticated technological advancements. These solutions leverage machine learning and computer vision to offer unparalleled insights and automation. Key product applications include intelligent irrigation systems that optimize water usage based on real-time weather data and soil moisture levels, predictive analytics for disease and pest identification to enable early intervention, and autonomous farming machinery for tasks like planting, harvesting, and spraying. Competitive advantages are derived from the precision, efficiency, and data-driven decision-making capabilities these products provide. For instance, multispectral imaging drones, like the DJI Mavic 3 Multispectral, offer rapid crop growth information, enhancing production quality and efficiency. AI-powered nutrient scanners, such as those integrating trinamiX's hardware with AgroCares' solutions, enable on-site analysis for optimized fertilization. These advancements are not just about improving yields but also about promoting sustainable practices and reducing the environmental footprint of agriculture.

Key Drivers, Barriers & Challenges in AI in Agriculture Industry

The AI in Agriculture Industry is propelled by several key drivers, including the escalating global demand for food security, the urgent need for sustainable agricultural practices to mitigate climate change, and the imperative to increase farm profitability through enhanced efficiency and reduced waste. Technological advancements in AI, IoT, and data analytics are making sophisticated solutions more accessible and effective. Government initiatives promoting agricultural modernization and data-driven farming further accelerate adoption.

However, significant barriers and challenges impede widespread growth. High initial investment costs for AI technologies can be a major restraint for small and medium-sized farms. Limited digital literacy and a shortage of skilled labor capable of operating and maintaining AI systems present a substantial hurdle. Regulatory complexities surrounding data privacy, ownership, and the ethical use of AI in agriculture can create uncertainty and slow down adoption. Furthermore, the fragmented nature of the agricultural sector and resistance to change among some farming communities require targeted education and demonstrable ROI. Supply chain issues related to the availability of advanced hardware and reliable internet connectivity in rural areas also pose challenges.

Growth Drivers in the AI in Agriculture Industry Market

Several key factors are driving robust growth within the AI in Agriculture Industry Market. Technologically, continuous advancements in machine learning algorithms, computer vision, and sensor technologies are leading to more accurate and efficient AI solutions. Economically, the increasing pressure on farmers to maximize yields while minimizing input costs (water, fertilizer, pesticides) makes AI-driven optimization a highly attractive proposition. Policy-driven factors, such as government incentives for adopting precision agriculture and sustainability initiatives, are also playing a crucial role. For example, the development of open-source AI platforms like Microsoft's FarmVibes.AI democratizes access to advanced agricultural technologies. The growing global population and the associated demand for food security further underscore the need for innovative solutions that AI provides.

Challenges Impacting AI in Agriculture Industry Growth

Despite significant growth drivers, the AI in Agriculture Industry faces several impactful challenges. Regulatory complexities, including evolving data privacy laws and ethical guidelines for AI deployment, can create uncertainty and slow down market penetration. Supply chain issues, particularly the availability of reliable high-speed internet and robust sensor networks in remote agricultural regions, remain a persistent problem. Competitive pressures are increasing as more companies enter the market, necessitating continuous innovation and differentiation. Furthermore, the significant upfront investment required for many AI solutions can be a barrier for farmers, especially those with limited capital. The need for specialized technical expertise to operate and maintain these advanced systems also presents a challenge, highlighting a gap in the agricultural workforce.

Key Players Shaping the AI in Agriculture Industry Market

- IBM Corporation

- Prospera Technologies Ltd

- Cainthus Corp

- Microsoft Corporation

- ec2ce

- PrecisionHawk Inc

- aWhere Inc

- Tule Technologies Inc

- Gamaya SA

- Granular Inc

Significant AI in Agriculture Industry Industry Milestones

- November 2022: DJI Agriculture Launches the Mavic 3 Multispectral, equipped with a multispectral imaging system that quickly captures crop growth information to achieve more effective crop production for a broad scope of application scenarios in the fields of precision agriculture and environmental monitoring that will help farmers around the world to improve the quality and efficiency of their production, reducing costs and increasing income.

- October 2022: Microsoft announced, FarmVibes open-sourced by Microsoft Research.AI, a collection of machine-learning models and technologies for sustainable agriculture. FarmVibes.AI comprises data processing methods for merging several kinds of spatiotemporal and geographic data, such as weather data and satellite and drone footage.

- September 2022: AgroCares announced a partnership for integrating trinamiX's high-performance hardware into AgroCares' next-generation nutrient scanner solution for next-generation solution for onsite nutrient analysis. TrinamiX is built on mobile NIR spectroscopy, combining robust hardware with flexible software to enhance onsite decision-making across various industries in on-the-spot nutrient testing.

Future Outlook for AI in Agriculture Industry Market

The future outlook for the AI in Agriculture Industry is exceptionally bright, marked by continuous innovation and increasing adoption. Growth catalysts include the further integration of AI with robotics for fully autonomous farming operations, the development of advanced AI models for hyper-personalized crop management, and the expansion of AI-powered solutions for supply chain optimization and food traceability. Strategic opportunities lie in leveraging AI to address climate change resilience in agriculture, developing AI-driven solutions for vertical farming and controlled environment agriculture, and creating platforms that empower smallholder farmers with accessible and affordable technology. The market potential is vast, promising a future where agriculture is more efficient, sustainable, and capable of feeding a growing global population. The continued investment in research and development, coupled with supportive government policies, will ensure AI remains at the forefront of agricultural transformation.

AI in Agriculture Industry Segmentation

-

1. Application

- 1.1. Weather Tracking

- 1.2. Precision Farming

- 1.3. Drone Analytics

-

2. Deployment

- 2.1. Cloud

- 2.2. On-premise

- 2.3. Hybrid

AI in Agriculture Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia

- 4. Australia and New Zealand

AI in Agriculture Industry Regional Market Share

Geographic Coverage of AI in Agriculture Industry

AI in Agriculture Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 22.55% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Weather Tracking

- 5.1.2. Precision Farming

- 5.1.3. Drone Analytics

- 5.2. Market Analysis, Insights and Forecast - by Deployment

- 5.2.1. Cloud

- 5.2.2. On-premise

- 5.2.3. Hybrid

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia

- 5.3.4. Australia and New Zealand

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global AI in Agriculture Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Weather Tracking

- 6.1.2. Precision Farming

- 6.1.3. Drone Analytics

- 6.2. Market Analysis, Insights and Forecast - by Deployment

- 6.2.1. Cloud

- 6.2.2. On-premise

- 6.2.3. Hybrid

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America AI in Agriculture Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Weather Tracking

- 7.1.2. Precision Farming

- 7.1.3. Drone Analytics

- 7.2. Market Analysis, Insights and Forecast - by Deployment

- 7.2.1. Cloud

- 7.2.2. On-premise

- 7.2.3. Hybrid

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe AI in Agriculture Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Weather Tracking

- 8.1.2. Precision Farming

- 8.1.3. Drone Analytics

- 8.2. Market Analysis, Insights and Forecast - by Deployment

- 8.2.1. Cloud

- 8.2.2. On-premise

- 8.2.3. Hybrid

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Asia AI in Agriculture Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Weather Tracking

- 9.1.2. Precision Farming

- 9.1.3. Drone Analytics

- 9.2. Market Analysis, Insights and Forecast - by Deployment

- 9.2.1. Cloud

- 9.2.2. On-premise

- 9.2.3. Hybrid

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Australia and New Zealand AI in Agriculture Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Weather Tracking

- 10.1.2. Precision Farming

- 10.1.3. Drone Analytics

- 10.2. Market Analysis, Insights and Forecast - by Deployment

- 10.2.1. Cloud

- 10.2.2. On-premise

- 10.2.3. Hybrid

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 IBM Corporation

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Prospera Technologies Ltd

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Cainthus Corp

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Microsoft Corporation

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 ec2ce

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 PrecisionHawk Inc

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 aWhere Inc

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Tule Technologies Inc *List Not Exhaustive

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Gamaya SA

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Granular Inc

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.1 IBM Corporation

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global AI in Agriculture Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America AI in Agriculture Industry Revenue (Million), by Application 2025 & 2033

- Figure 3: North America AI in Agriculture Industry Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America AI in Agriculture Industry Revenue (Million), by Deployment 2025 & 2033

- Figure 5: North America AI in Agriculture Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 6: North America AI in Agriculture Industry Revenue (Million), by Country 2025 & 2033

- Figure 7: North America AI in Agriculture Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe AI in Agriculture Industry Revenue (Million), by Application 2025 & 2033

- Figure 9: Europe AI in Agriculture Industry Revenue Share (%), by Application 2025 & 2033

- Figure 10: Europe AI in Agriculture Industry Revenue (Million), by Deployment 2025 & 2033

- Figure 11: Europe AI in Agriculture Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 12: Europe AI in Agriculture Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Europe AI in Agriculture Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia AI in Agriculture Industry Revenue (Million), by Application 2025 & 2033

- Figure 15: Asia AI in Agriculture Industry Revenue Share (%), by Application 2025 & 2033

- Figure 16: Asia AI in Agriculture Industry Revenue (Million), by Deployment 2025 & 2033

- Figure 17: Asia AI in Agriculture Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 18: Asia AI in Agriculture Industry Revenue (Million), by Country 2025 & 2033

- Figure 19: Asia AI in Agriculture Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Australia and New Zealand AI in Agriculture Industry Revenue (Million), by Application 2025 & 2033

- Figure 21: Australia and New Zealand AI in Agriculture Industry Revenue Share (%), by Application 2025 & 2033

- Figure 22: Australia and New Zealand AI in Agriculture Industry Revenue (Million), by Deployment 2025 & 2033

- Figure 23: Australia and New Zealand AI in Agriculture Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 24: Australia and New Zealand AI in Agriculture Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Australia and New Zealand AI in Agriculture Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global AI in Agriculture Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 2: Global AI in Agriculture Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 3: Global AI in Agriculture Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global AI in Agriculture Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 5: Global AI in Agriculture Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 6: Global AI in Agriculture Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: Global AI in Agriculture Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 8: Global AI in Agriculture Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 9: Global AI in Agriculture Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 10: Global AI in Agriculture Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 11: Global AI in Agriculture Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 12: Global AI in Agriculture Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Global AI in Agriculture Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 14: Global AI in Agriculture Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 15: Global AI in Agriculture Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the AI in Agriculture Industry?

The projected CAGR is approximately 22.55%.

2. Which companies are prominent players in the AI in Agriculture Industry?

Key companies in the market include IBM Corporation, Prospera Technologies Ltd, Cainthus Corp, Microsoft Corporation, ec2ce, PrecisionHawk Inc, aWhere Inc, Tule Technologies Inc *List Not Exhaustive, Gamaya SA, Granular Inc.

3. What are the main segments of the AI in Agriculture Industry?

The market segments include Application, Deployment.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.08 Million as of 2022.

5. What are some drivers contributing to market growth?

Maximize Crop Yield Using Machine Learning technique; Increase in the Adoption of Cattle Face Recognition Technology; Increase Use of Unmanned Aerial Vehicles (UAVs) Across Agricultural Farms.

6. What are the notable trends driving market growth?

Drone Analytics Application Segment is Expected to Hold Significant Market Share.

7. Are there any restraints impacting market growth?

Lack of Standardization in Data Collection.

8. Can you provide examples of recent developments in the market?

November 2022 - DJI Agriculture Launches the Mavic 3 Multispectral, equipped with a multispectral imaging system that quickly captures crop growth information to achieve more effective crop production for a broad scope of application scenarios in the fields of precision agriculture and environmental monitoring that will help farmers around the world to improve the quality and efficiency of their production, reducing costs and increasing income.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "AI in Agriculture Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the AI in Agriculture Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the AI in Agriculture Industry?

To stay informed about further developments, trends, and reports in the AI in Agriculture Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence