Key Insights

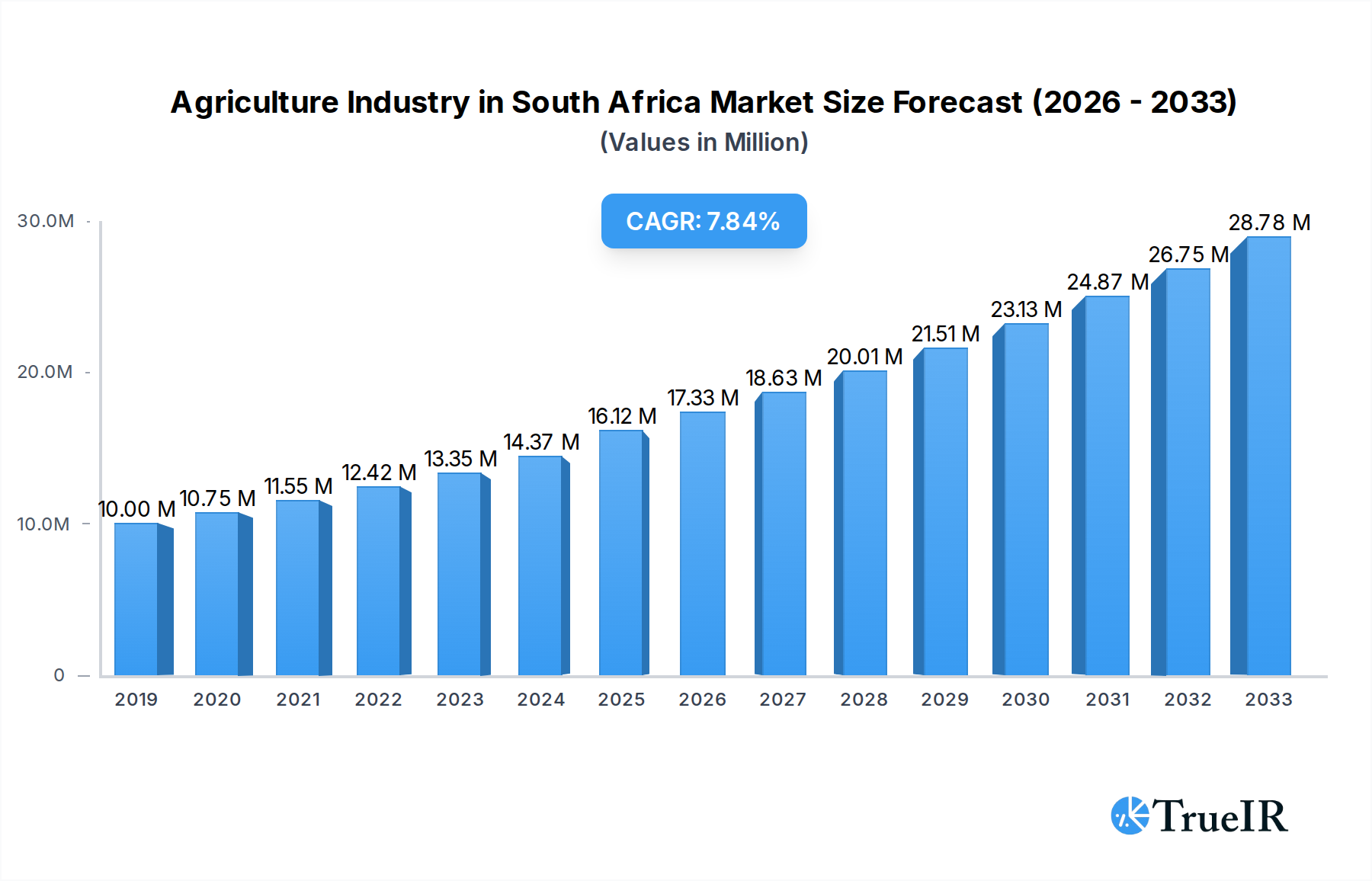

The South African agriculture industry is poised for significant expansion, projected to reach a market size of 16.12 Million by 2025, with a robust compound annual growth rate (CAGR) of 7.60% expected throughout the forecast period of 2025-2033. This impressive growth trajectory is fueled by a confluence of strategic drivers. A key impetus is the increasing adoption of advanced agricultural technologies, including precision farming techniques, mechanization, and the use of high-yielding seed varieties. Growing consumer demand for diverse and higher-quality produce, driven by a rising middle class and evolving dietary preferences, also plays a crucial role. Furthermore, supportive government policies aimed at enhancing agricultural productivity, ensuring food security, and promoting export market access are significantly contributing to the sector's positive outlook. The expansion of irrigation infrastructure and investment in research and development for climate-resilient crops will further bolster the industry's capacity to meet growing domestic and international demand.

Agriculture Industry in South Africa Market Size (In Million)

Despite these positive indicators, certain restraints could influence the pace of growth. Climate change, characterized by unpredictable weather patterns, droughts, and extreme events, presents a persistent challenge, impacting crop yields and necessitating greater investment in adaptation strategies. Fluctuations in global commodity prices can also affect farmer profitability and investment decisions. Additionally, challenges related to land access, water scarcity in certain regions, and the need for continuous skills development within the agricultural workforce are areas requiring ongoing attention. The industry is actively addressing these by focusing on sustainable practices, water-efficient farming methods, and fostering innovation to mitigate risks and capitalize on the abundant opportunities presented by both domestic consumption and international trade, particularly within the cereals, fruits, vegetables, and oilseeds segments.

Agriculture Industry in South Africa Company Market Share

Agriculture Industry in South Africa Market Structure & Competitive Landscape

The South African agriculture industry, a vital contributor to the nation's economy, exhibits a moderately concentrated market structure. Key players like Bayer Crop Science, Syngenta, Pioneer Foods, Tiger Brands, and historically Monsanto (now part of Bayer) exert significant influence. Innovation drivers include the adoption of advanced agricultural technologies, precision farming techniques, and the development of drought-resistant crop varieties to combat the country's arid climate challenges. Regulatory impacts are substantial, with government policies on land reform, trade agreements, and food safety regulations shaping market dynamics. Product substitutes are present, particularly in processed food markets, though primary agricultural commodities remain distinct. End-user segmentation spans large-scale commercial farms, emerging smallholder farmers, food processing companies, and direct consumer markets. Mergers and acquisitions (M&A) activity, while subject to regulatory scrutiny, has been a consistent feature, consolidating market share and expanding product portfolios. For instance, the acquisition of Monsanto by Bayer in 2018 significantly reshaped the global agrochemical and seed landscape. Market concentration is estimated at a Herfindahl-Hirschman Index (HHI) of around 1800, indicating a moderately concentrated market. M&A volumes in the past five years are estimated to be in the range of 50-75 transactions, valued at several hundred million dollars.

Agriculture Industry in South Africa Market Trends & Opportunities

The South African agriculture industry is on a robust growth trajectory, with a projected market size exceeding $30 Billion by 2033. This expansion is underpinned by a compound annual growth rate (CAGR) of approximately 5.5% during the forecast period of 2025-2033. Technological shifts are revolutionizing farming practices, with a significant increase in the adoption of artificial intelligence (AI) for crop monitoring, drone-based precision spraying, and the widespread integration of IoT devices for real-time data analysis. These advancements are leading to improved yields, reduced resource wastage, and enhanced farm management efficiency. Consumer preferences are increasingly leaning towards healthier, sustainably produced, and locally sourced food products. This trend presents a burgeoning opportunity for organic farming, niche crop cultivation, and direct-to-consumer models. The competitive dynamics are intensifying, with both established multinational corporations and agile local enterprises vying for market share. Companies are investing heavily in R&D to develop climate-resilient crops and innovative biopesticides. Market penetration rates for digital farming solutions are estimated to have reached 40% by 2024, with a projected increase to 70% by 2033. The demand for high-value fruits and vegetables is surging, driven by export markets and growing domestic awareness of nutritional benefits. Furthermore, the increasing demand for animal feed is a significant growth catalyst. The industry is also witnessing a rise in the adoption of protected agriculture, such as greenhouses, to mitigate the impact of erratic weather patterns and enhance crop quality. Investments in cold chain infrastructure are crucial for reducing post-harvest losses and expanding market reach for perishable goods. The focus on value addition through processing of agricultural produce is also creating new avenues for growth and employment. The increasing use of crop protection chemicals and fertilizers, albeit with a growing emphasis on sustainable alternatives, continues to drive market value. The government's commitment to supporting the agricultural sector through various policy initiatives and subsidies is a key enabler of this growth.

Dominant Markets & Segments in Agriculture Industry in South Africa

The dominant markets and segments within the South African agriculture industry are characterized by the significant contributions of Cereals and Fruits.

Cereals hold a commanding position due to their staple food status and widespread cultivation across various provinces.

- Key Growth Drivers for Cereals:

- Food Security: High domestic demand for maize, wheat, and sorghum as primary food sources ensures consistent market volume.

- Export Potential: South Africa is a net exporter of certain grains, particularly maize, to neighboring African countries, driving revenue.

- Government Support: Subsidies and policy frameworks aimed at enhancing grain production and storage contribute to market stability.

- Technological Advancements: Adoption of improved seed varieties and mechanization are boosting yields and reducing production costs.

- Animal Feed Industry: The growing livestock sector creates a substantial demand for cereal-based animal feed.

Fruits represent another highly lucrative segment, driven by both domestic consumption and strong international demand. South Africa is renowned for its high-quality citrus, deciduous fruits, and berries.

- Key Growth Drivers for Fruits:

- Export Markets: Significant export volumes of apples, pears, grapes, citrus, and berries to Europe, Asia, and other international destinations generate substantial foreign exchange.

- Consumer Health Trends: Growing consumer preference for healthy diets boosts demand for fresh fruits.

- Value-Added Products: The processing of fruits into juices, jams, and dried products further expands market reach and revenue.

- Favorable Climate Zones: Diverse agro-climatic regions in South Africa are conducive to the cultivation of a wide variety of fruits.

- Investment in Post-Harvest Infrastructure: Continuous investment in cold storage and logistics ensures fruit quality and extends shelf life for export.

While Vegetables and Oilseeds are also crucial, their market dominance is comparatively less pronounced than Cereals and Fruits. However, they present substantial growth opportunities. The vegetable sector benefits from increasing urbanization and a rising demand for fresh produce. Oilseeds, particularly soybeans and sunflower seeds, are vital for the edible oil and animal feed industries, with growing potential driven by import substitution efforts and domestic processing capacity. The continued focus on diversifying agricultural production and embracing climate-smart practices will further shape the dominance and growth trajectories of these segments.

Agriculture Industry in South Africa Product Analysis

Product innovations in the South African agriculture industry are increasingly focused on enhancing crop resilience and sustainability. Advancements in seed technology, such as the development of genetically modified (GM) and conventionally bred drought-tolerant and disease-resistant varieties of maize and other staple crops, are providing farmers with more reliable yields in challenging climatic conditions. The application of precision agriculture tools, including GPS-guided machinery, variable rate application of fertilizers and pesticides, and drone-based monitoring systems, allows for optimized resource utilization and reduced environmental impact. Biopesticides and bio-fertilizers are gaining traction as environmentally friendly alternatives to conventional chemical inputs. Competitive advantages stem from superior seed genetics, advanced crop protection solutions, and the ability to provide integrated farming solutions that enhance productivity and profitability for growers.

Key Drivers, Barriers & Challenges in Agriculture Industry in South Africa

The South African agriculture industry is propelled by several key drivers including technological advancements such as precision farming and AI-driven analytics, which enhance efficiency and yields. Economic factors, like strong domestic and export demand for agricultural commodities and government support through incentives and infrastructure development, also play a crucial role. Policy initiatives, including land reform aimed at broader participation and trade agreements, further stimulate growth.

However, significant barriers and challenges exist. Supply chain disruptions, exacerbated by logistical inefficiencies and infrastructure limitations, lead to increased costs and post-harvest losses, estimated at 15-20% for certain high-value produce. Regulatory hurdles, including complex land ownership regulations and stringent import/export requirements, can impede market access and investment. Competitive pressures from international markets with lower production costs and established distribution networks pose a constant threat. Water scarcity due to climate change and over-allocation remains a critical constraint, impacting irrigation and overall farm productivity. The cost of inputs, such as fuel and fertilizers, also continues to be a significant challenge for farmers, with price volatility impacting profitability.

Growth Drivers in the Agriculture Industry in South Africa Market

Growth in the South African agriculture sector is primarily driven by technological innovation, including the adoption of digital farming tools for improved decision-making and resource management, and the development of climate-resilient crop varieties. Economic factors, such as a robust demand from both domestic consumers and international export markets for key commodities like fruits and grains, are critical. Government policies, including support for emerging farmers, investment in agricultural infrastructure, and trade facilitation, further stimulate expansion. The increasing focus on value addition through agricultural processing also opens new avenues for revenue generation.

Challenges Impacting Agriculture Industry in South Africa Growth

Challenges impacting the South African agriculture industry are multifaceted. Regulatory complexities, particularly around land reform and environmental compliance, can create uncertainty and hinder investment. Significant supply chain issues, including underdeveloped logistics and inadequate cold chain infrastructure, result in substantial post-harvest losses, estimated to affect up to 20% of perishable produce. Competitive pressures from global markets with more favorable production costs and established trade networks also exert considerable influence. Furthermore, climate change-induced water scarcity and the increasing cost of essential inputs like fertilizers and energy significantly impact farm profitability and sustainability.

Key Players Shaping the Agriculture Industry in South Africa Market

- Pioneer Foods

- Bayer Crop Science

- Syngenta

- Tiger Brands

Significant Agriculture Industry in South Africa Industry Milestones

- 2019: Launch of the Comprehensive Rural Development Programme (CRDP) by the Department of Rural Development and Land Reform to address land redistribution and agricultural support.

- 2020: Significant increase in the adoption of precision farming technologies by large-scale commercial farms, driven by efficiency gains and climate change adaptation.

- 2021: Introduction of new drought-resistant maize varieties by major seed companies to combat recurring dry spells.

- 2022: Growth in the organic produce market, with increasing consumer demand for sustainably produced fruits and vegetables.

- 2023: Enhanced focus on aquaculture development as a diversification strategy within the broader agricultural sector.

- 2024: Continued investment in cold chain infrastructure to reduce post-harvest losses for export-oriented fruit and vegetable producers.

Future Outlook for Agriculture Industry in South Africa Market

The future outlook for the South African agriculture industry is optimistic, driven by sustained demand, technological advancements, and a growing emphasis on sustainability. Strategic opportunities lie in further expanding export markets for high-value produce, investing in value-addition processing to capture more of the supply chain, and accelerating the adoption of climate-smart and digital farming solutions. The market potential is significant for innovative products and services that address water scarcity, improve soil health, and reduce the environmental footprint of farming. The continued integration of emerging farmers into the commercial agricultural landscape will also be a crucial aspect of future growth and inclusivity.

Agriculture Industry in South Africa Segmentation

-

1. Crop Type

- 1.1. Cereals

- 1.2. Fruits

- 1.3. Vegetables

- 1.4. Oilseeds

-

2. Crop Type

- 2.1. Cereals

- 2.2. Fruits

- 2.3. Vegetables

- 2.4. Oilseeds

Agriculture Industry in South Africa Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

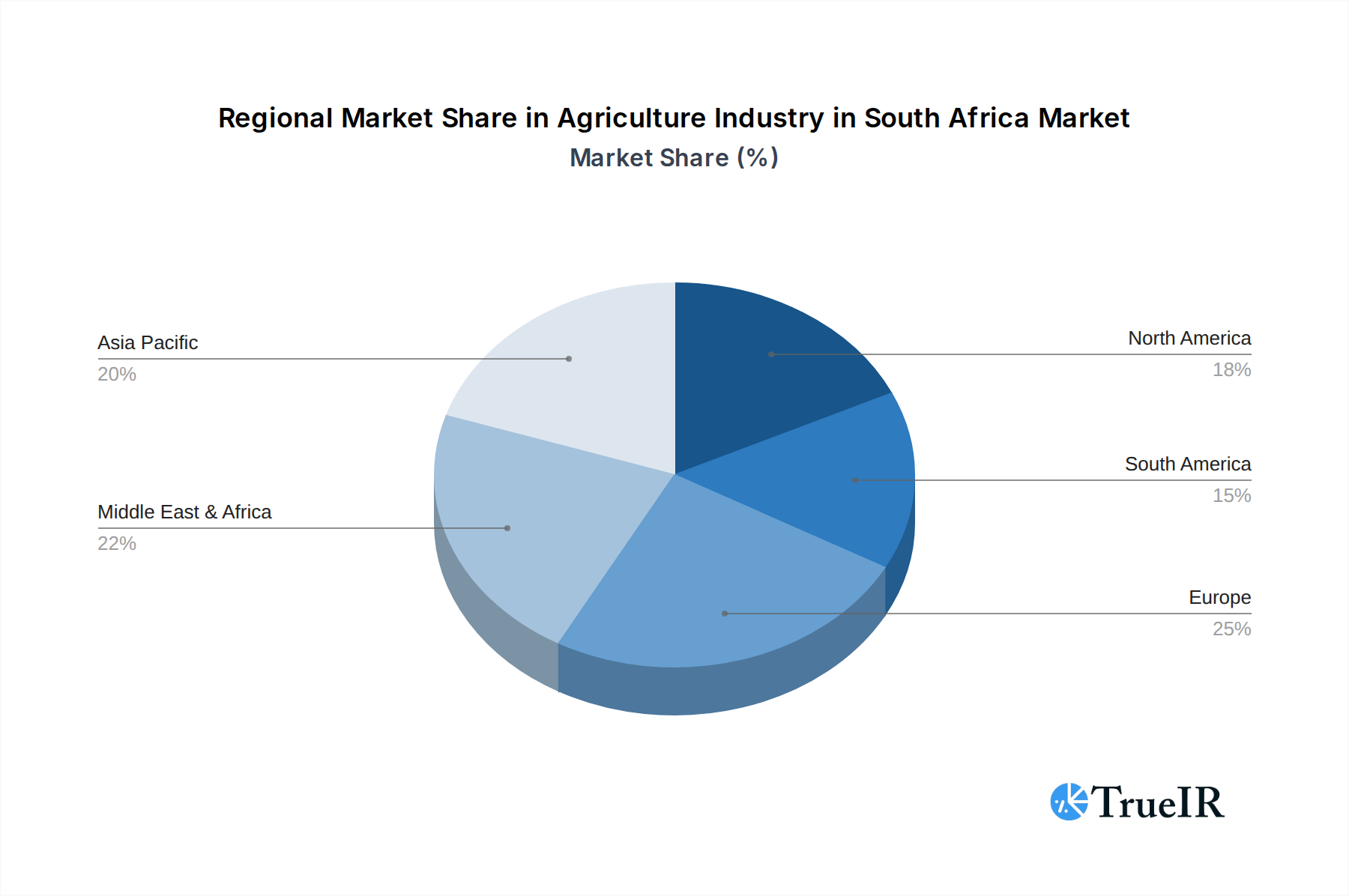

Agriculture Industry in South Africa Regional Market Share

Geographic Coverage of Agriculture Industry in South Africa

Agriculture Industry in South Africa REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.60% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Crop Type

- 5.1.1. Cereals

- 5.1.2. Fruits

- 5.1.3. Vegetables

- 5.1.4. Oilseeds

- 5.2. Market Analysis, Insights and Forecast - by Crop Type

- 5.2.1. Cereals

- 5.2.2. Fruits

- 5.2.3. Vegetables

- 5.2.4. Oilseeds

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Crop Type

- 6. Global Agriculture Industry in South Africa Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Crop Type

- 6.1.1. Cereals

- 6.1.2. Fruits

- 6.1.3. Vegetables

- 6.1.4. Oilseeds

- 6.2. Market Analysis, Insights and Forecast - by Crop Type

- 6.2.1. Cereals

- 6.2.2. Fruits

- 6.2.3. Vegetables

- 6.2.4. Oilseeds

- 6.1. Market Analysis, Insights and Forecast - by Crop Type

- 7. North America Agriculture Industry in South Africa Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Crop Type

- 7.1.1. Cereals

- 7.1.2. Fruits

- 7.1.3. Vegetables

- 7.1.4. Oilseeds

- 7.2. Market Analysis, Insights and Forecast - by Crop Type

- 7.2.1. Cereals

- 7.2.2. Fruits

- 7.2.3. Vegetables

- 7.2.4. Oilseeds

- 7.1. Market Analysis, Insights and Forecast - by Crop Type

- 8. South America Agriculture Industry in South Africa Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Crop Type

- 8.1.1. Cereals

- 8.1.2. Fruits

- 8.1.3. Vegetables

- 8.1.4. Oilseeds

- 8.2. Market Analysis, Insights and Forecast - by Crop Type

- 8.2.1. Cereals

- 8.2.2. Fruits

- 8.2.3. Vegetables

- 8.2.4. Oilseeds

- 8.1. Market Analysis, Insights and Forecast - by Crop Type

- 9. Europe Agriculture Industry in South Africa Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Crop Type

- 9.1.1. Cereals

- 9.1.2. Fruits

- 9.1.3. Vegetables

- 9.1.4. Oilseeds

- 9.2. Market Analysis, Insights and Forecast - by Crop Type

- 9.2.1. Cereals

- 9.2.2. Fruits

- 9.2.3. Vegetables

- 9.2.4. Oilseeds

- 9.1. Market Analysis, Insights and Forecast - by Crop Type

- 10. Middle East & Africa Agriculture Industry in South Africa Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Crop Type

- 10.1.1. Cereals

- 10.1.2. Fruits

- 10.1.3. Vegetables

- 10.1.4. Oilseeds

- 10.2. Market Analysis, Insights and Forecast - by Crop Type

- 10.2.1. Cereals

- 10.2.2. Fruits

- 10.2.3. Vegetables

- 10.2.4. Oilseeds

- 10.1. Market Analysis, Insights and Forecast - by Crop Type

- 11. Asia Pacific Agriculture Industry in South Africa Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Crop Type

- 11.1.1. Cereals

- 11.1.2. Fruits

- 11.1.3. Vegetables

- 11.1.4. Oilseeds

- 11.2. Market Analysis, Insights and Forecast - by Crop Type

- 11.2.1. Cereals

- 11.2.2. Fruits

- 11.2.3. Vegetables

- 11.2.4. Oilseeds

- 11.1. Market Analysis, Insights and Forecast - by Crop Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Pioneer Foods

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Bayer Crop Science

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Syngenta

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Monsanto

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Tiger Brands

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.1 Pioneer Foods

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Agriculture Industry in South Africa Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Agriculture Industry in South Africa Revenue (Million), by Crop Type 2025 & 2033

- Figure 3: North America Agriculture Industry in South Africa Revenue Share (%), by Crop Type 2025 & 2033

- Figure 4: North America Agriculture Industry in South Africa Revenue (Million), by Crop Type 2025 & 2033

- Figure 5: North America Agriculture Industry in South Africa Revenue Share (%), by Crop Type 2025 & 2033

- Figure 6: North America Agriculture Industry in South Africa Revenue (Million), by Country 2025 & 2033

- Figure 7: North America Agriculture Industry in South Africa Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Agriculture Industry in South Africa Revenue (Million), by Crop Type 2025 & 2033

- Figure 9: South America Agriculture Industry in South Africa Revenue Share (%), by Crop Type 2025 & 2033

- Figure 10: South America Agriculture Industry in South Africa Revenue (Million), by Crop Type 2025 & 2033

- Figure 11: South America Agriculture Industry in South Africa Revenue Share (%), by Crop Type 2025 & 2033

- Figure 12: South America Agriculture Industry in South Africa Revenue (Million), by Country 2025 & 2033

- Figure 13: South America Agriculture Industry in South Africa Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Agriculture Industry in South Africa Revenue (Million), by Crop Type 2025 & 2033

- Figure 15: Europe Agriculture Industry in South Africa Revenue Share (%), by Crop Type 2025 & 2033

- Figure 16: Europe Agriculture Industry in South Africa Revenue (Million), by Crop Type 2025 & 2033

- Figure 17: Europe Agriculture Industry in South Africa Revenue Share (%), by Crop Type 2025 & 2033

- Figure 18: Europe Agriculture Industry in South Africa Revenue (Million), by Country 2025 & 2033

- Figure 19: Europe Agriculture Industry in South Africa Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Agriculture Industry in South Africa Revenue (Million), by Crop Type 2025 & 2033

- Figure 21: Middle East & Africa Agriculture Industry in South Africa Revenue Share (%), by Crop Type 2025 & 2033

- Figure 22: Middle East & Africa Agriculture Industry in South Africa Revenue (Million), by Crop Type 2025 & 2033

- Figure 23: Middle East & Africa Agriculture Industry in South Africa Revenue Share (%), by Crop Type 2025 & 2033

- Figure 24: Middle East & Africa Agriculture Industry in South Africa Revenue (Million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Agriculture Industry in South Africa Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Agriculture Industry in South Africa Revenue (Million), by Crop Type 2025 & 2033

- Figure 27: Asia Pacific Agriculture Industry in South Africa Revenue Share (%), by Crop Type 2025 & 2033

- Figure 28: Asia Pacific Agriculture Industry in South Africa Revenue (Million), by Crop Type 2025 & 2033

- Figure 29: Asia Pacific Agriculture Industry in South Africa Revenue Share (%), by Crop Type 2025 & 2033

- Figure 30: Asia Pacific Agriculture Industry in South Africa Revenue (Million), by Country 2025 & 2033

- Figure 31: Asia Pacific Agriculture Industry in South Africa Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Agriculture Industry in South Africa Revenue Million Forecast, by Crop Type 2020 & 2033

- Table 2: Global Agriculture Industry in South Africa Revenue Million Forecast, by Crop Type 2020 & 2033

- Table 3: Global Agriculture Industry in South Africa Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Agriculture Industry in South Africa Revenue Million Forecast, by Crop Type 2020 & 2033

- Table 5: Global Agriculture Industry in South Africa Revenue Million Forecast, by Crop Type 2020 & 2033

- Table 6: Global Agriculture Industry in South Africa Revenue Million Forecast, by Country 2020 & 2033

- Table 7: United States Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Canada Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Global Agriculture Industry in South Africa Revenue Million Forecast, by Crop Type 2020 & 2033

- Table 11: Global Agriculture Industry in South Africa Revenue Million Forecast, by Crop Type 2020 & 2033

- Table 12: Global Agriculture Industry in South Africa Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Brazil Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Global Agriculture Industry in South Africa Revenue Million Forecast, by Crop Type 2020 & 2033

- Table 17: Global Agriculture Industry in South Africa Revenue Million Forecast, by Crop Type 2020 & 2033

- Table 18: Global Agriculture Industry in South Africa Revenue Million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Germany Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: France Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Italy Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: Spain Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: Russia Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Global Agriculture Industry in South Africa Revenue Million Forecast, by Crop Type 2020 & 2033

- Table 29: Global Agriculture Industry in South Africa Revenue Million Forecast, by Crop Type 2020 & 2033

- Table 30: Global Agriculture Industry in South Africa Revenue Million Forecast, by Country 2020 & 2033

- Table 31: Turkey Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Israel Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 33: GCC Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 37: Global Agriculture Industry in South Africa Revenue Million Forecast, by Crop Type 2020 & 2033

- Table 38: Global Agriculture Industry in South Africa Revenue Million Forecast, by Crop Type 2020 & 2033

- Table 39: Global Agriculture Industry in South Africa Revenue Million Forecast, by Country 2020 & 2033

- Table 40: China Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 41: India Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: Japan Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Agriculture Industry in South Africa Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Agriculture Industry in South Africa?

The projected CAGR is approximately 7.60%.

2. Which companies are prominent players in the Agriculture Industry in South Africa?

Key companies in the market include Pioneer Foods , Bayer Crop Science , Syngenta , Monsanto , Tiger Brands.

3. What are the main segments of the Agriculture Industry in South Africa?

The market segments include Crop Type, Crop Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 16.12 Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Consumption of Cashew Nuts as a Healthy Snack; Increasing Government initiatives; Growing Cashew Nut Imports in The United States.

6. What are the notable trends driving market growth?

High Demand for Food Crops with the rising population.

7. Are there any restraints impacting market growth?

Hazardous Climatic Condition Hinders Cashew Production; Stringent Regulations Related To Food Quality Standards.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Agriculture Industry in South Africa," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Agriculture Industry in South Africa report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Agriculture Industry in South Africa?

To stay informed about further developments, trends, and reports in the Agriculture Industry in South Africa, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence