Key Insights

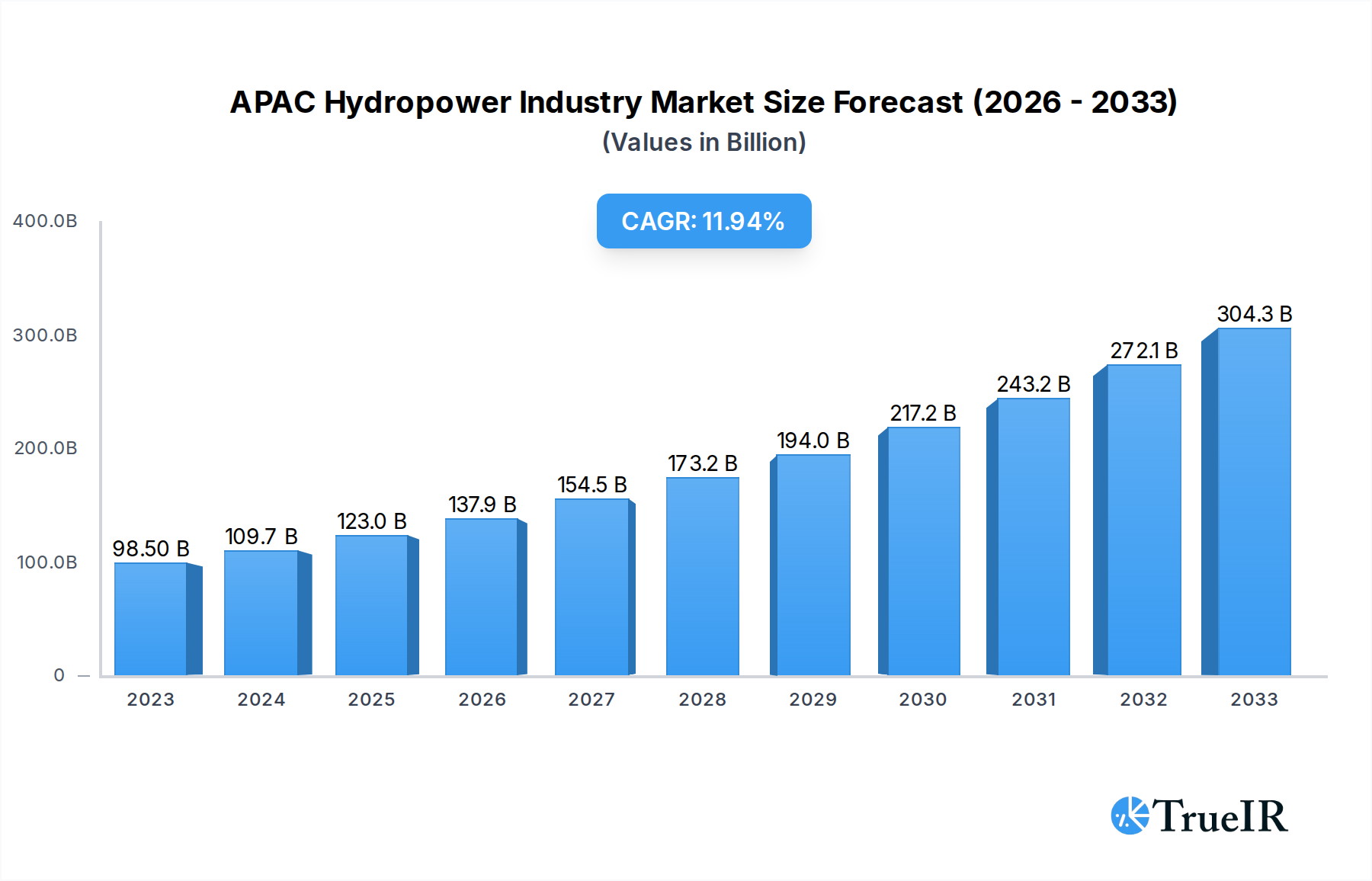

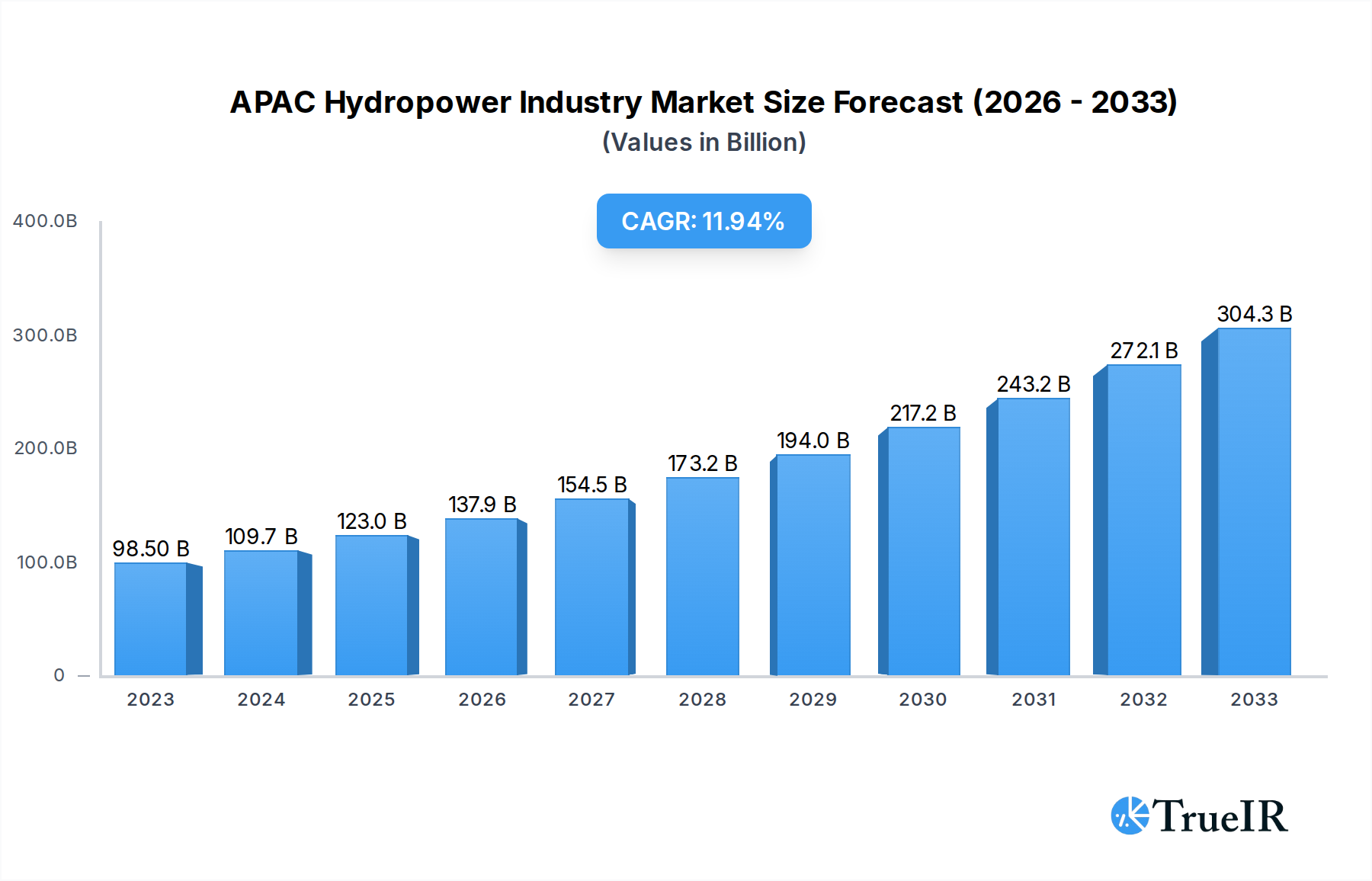

The APAC Hydropower Industry is poised for substantial growth, driven by the region's escalating energy demands and a concerted push towards renewable energy sources. The market, currently valued at an estimated USD 98.5 billion in 2023, is projected to expand at a robust CAGR of 12.1% through 2033. This remarkable expansion is fueled by several key factors, including government initiatives promoting clean energy, increasing investments in large-scale hydropower projects for baseload power, and the growing adoption of small hydropower for decentralized energy generation. Asia Pacific's vast river systems and mountainous terrains offer immense potential for hydropower development, positioning it as a critical contributor to the region's energy security and decarbonization goals. The region's commitment to reducing its carbon footprint and reliance on fossil fuels is a significant tailwind for hydropower, making it an attractive investment avenue.

APAC Hydropower Industry Market Size (In Billion)

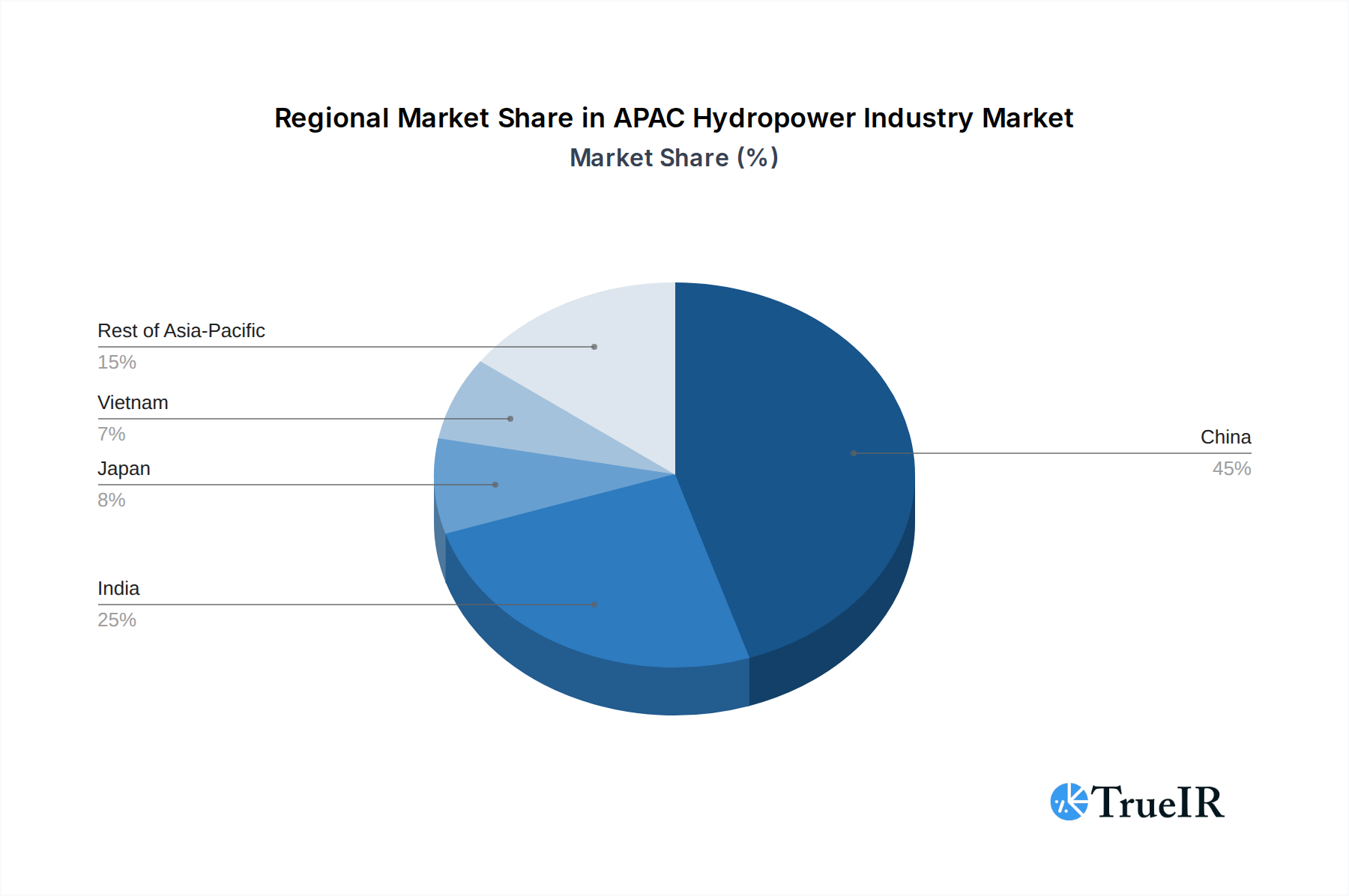

The market dynamics are further shaped by evolving trends such as technological advancements in turbine efficiency and dam construction, alongside a rising emphasis on environmental sustainability in project planning and execution. While the larger segments like Large Hydropower are expected to continue dominating, Small Hydropower is witnessing an accelerated growth trajectory due to its adaptability and suitability for remote areas. Geographically, China and India are leading the charge, owing to their substantial existing infrastructure and ambitious renewable energy targets. However, countries like Vietnam and Japan are also making significant strides in expanding their hydropower capacities. The competitive landscape features established global players and prominent regional companies, all vying for a share in this rapidly expanding market, indicating a vibrant and dynamic industry outlook.

APAC Hydropower Industry Company Market Share

This in-depth report provides a dynamic and SEO-optimized analysis of the APAC Hydropower Industry, leveraging high-volume keywords to enhance search rankings and deliver critical insights to industry stakeholders. Our comprehensive study, spanning from 2019 to 2033 with a base and estimated year of 2025, delves into market structure, trends, opportunities, dominant segments, product innovations, key drivers, barriers, and the competitive landscape.

APAC Hydropower Industry Market Structure & Competitive Landscape

The APAC Hydropower Industry exhibits a dynamic market structure characterized by a moderate to high degree of concentration in specific sub-regions, particularly driven by state-owned enterprises and a few dominant private players. Innovation drivers are primarily focused on enhancing efficiency in existing infrastructure, developing advanced turbine technologies, and exploring solutions for environmental sustainability. Regulatory impacts play a significant role, with government policies on renewable energy targets, grid integration, and environmental compliance shaping investment and development strategies. Product substitutes, while present in the broader renewable energy sector (solar, wind), are less direct for large-scale baseload power generation where hydropower excels. End-user segmentation is broadly categorized into industrial, commercial, and residential electricity demands, with grid stability and power supply security being paramount. Mergers and Acquisitions (M&A) trends are observed as companies seek to consolidate their market position, acquire new technologies, or expand their project portfolios. While specific M&A volumes are subject to real-time market fluctuations, strategic partnerships and asset acquisitions are consistent themes. Concentration ratios are influenced by the presence of large national utilities and international engineering firms, indicating a competitive yet strategically organized market.

APAC Hydropower Industry Market Trends & Opportunities

The APAC Hydropower Industry is projected for substantial growth, driven by the region's escalating energy demands and a strong push towards sustainable power generation. The market size is expected to expand significantly, fueled by government mandates and private sector investments aimed at decarbonizing energy portfolios. Technological shifts are at the forefront, with advancements in turbine design, digitalized monitoring systems, and pumped-storage hydropower solutions enhancing operational efficiency and grid flexibility. Consumer preferences are increasingly leaning towards reliable and renewable energy sources, positioning hydropower as a crucial component in meeting these demands, especially for baseload power. Competitive dynamics are evolving, with established players like PowerChina and PT Perusahaan Listrik Negara contending with innovative technology providers such as General Electric Company (GE Renewable Energy) and a growing number of regional developers. Opportunities lie in modernizing aging infrastructure, developing small hydropower projects in remote areas, and integrating hydropower with other renewable energy sources to create robust and resilient power grids. The market penetration rates for hydropower, while already substantial in some countries, have significant room for expansion, particularly in emerging economies within the Asia-Pacific region. The CAGR is anticipated to be robust, reflecting the sector's strategic importance in meeting future energy needs and climate goals.

Dominant Markets & Segments in APAC Hydropower Industry

Within the APAC Hydropower Industry, China stands out as the dominant market, driven by its immense energy consumption and ambitious renewable energy targets. Its extensive river systems and significant investments in both large and small hydropower projects solidify its leadership. India is another powerhouse, with substantial installed capacity and ongoing development, driven by the need to electrify its vast population and reduce reliance on fossil fuels. Japan, while a mature market, continues to invest in hydropower for its grid stability and the modernization of existing facilities. Vietnam is emerging as a significant player, with its growing economy demanding more electricity and a strategic focus on renewable energy, including hydropower. The Rest of Asia-Pacific encompasses a diverse range of countries with varying degrees of hydropower potential and development, from established markets to nascent ones actively seeking to harness their water resources.

Key Growth Drivers in Dominant Markets:

- Infrastructure Development: Massive government-led initiatives to build new dams, upgrade existing facilities, and expand transmission networks are central to growth.

- Renewable Energy Policies: Favorable feed-in tariffs, tax incentives, and renewable energy mandates are crucial for attracting investment.

- Energy Security Concerns: Reducing dependence on imported fossil fuels and ensuring a stable domestic energy supply are key motivators.

- Economic Growth: Rapid industrialization and urbanization in many APAC countries lead to escalating electricity demand, which hydropower can reliably meet.

- Technological Advancements: Improvements in turbine efficiency, digital monitoring, and environmental mitigation techniques make projects more viable and sustainable.

- Climate Change Commitments: National and international commitments to reduce carbon emissions are accelerating the shift towards cleaner energy sources like hydropower.

The Large Hydropower segment continues to dominate in terms of installed capacity, owing to its significant power generation potential. However, the Small Hydropower segment is experiencing rapid growth, particularly in areas with less extensive river systems or in decentralized energy generation contexts. Its lower environmental impact and quicker development timelines make it an attractive option for many nations. Other Sizes of hydropower projects, including mini and micro hydropower, are also gaining traction for specific applications and rural electrification efforts.

APAC Hydropower Industry Product Analysis

The APAC Hydropower Industry is characterized by a continuous drive for product innovation focused on enhancing efficiency, reliability, and environmental compatibility. Turbine technologies are at the forefront, with advancements in Kaplan, Francis, and Pelton turbines offering optimized performance across various head and flow conditions. Digitalization and smart grid integration are transforming operations, with predictive maintenance, remote monitoring, and automated control systems becoming standard. Furthermore, there is a growing emphasis on solutions for environmental sustainability, including fish-friendly turbines, sediment management systems, and retrofitting existing dams for pumped-storage capabilities. These innovations provide competitive advantages by reducing operational costs, minimizing environmental impact, and ensuring a more consistent and flexible power supply.

Key Drivers, Barriers & Challenges in APAC Hydropower Industry

Key Drivers:

- Surging Energy Demand: Rapid economic growth and population increase across APAC necessitate substantial new power generation capacity.

- Renewable Energy Targets: Government commitments to decarbonization and clean energy are a primary impetus for hydropower development.

- Technological Advancements: Improved turbine efficiency, digital monitoring, and environmentally conscious designs enhance project viability.

- Energy Security: Reducing reliance on volatile fossil fuel imports and securing stable domestic power supply are critical.

- Favorable Policy Frameworks: Government incentives, subsidies, and supportive regulations are crucial for attracting investment in hydropower projects.

Barriers & Challenges:

- Environmental Concerns: Opposition related to dam construction's impact on ecosystems, biodiversity, and local communities can lead to delays and increased costs.

- High Upfront Capital Costs: Hydropower projects require significant initial investment, posing financial challenges, especially for developing nations.

- Regulatory Hurdles and Permitting: Complex and lengthy approval processes, environmental impact assessments, and land acquisition issues can impede project timelines.

- Geographical Limitations: The availability of suitable sites with adequate water resources and topographical features is a natural constraint.

- Intermittency (for some types): While generally baseload, run-of-river projects can be affected by seasonal water flow variations.

- Competition from Other Renewables: The declining costs of solar and wind power present a competitive challenge, although hydropower offers distinct advantages in grid stability.

- Supply Chain Vulnerabilities: Dependence on specialized equipment and materials can lead to procurement delays and cost fluctuations. The estimated impact of these barriers can add 10-20% to project development timelines and costs.

Growth Drivers in the APAC Hydropower Industry Market

The APAC Hydropower Industry's growth is propelled by a confluence of critical factors. Economically, the relentless surge in energy demand across the region, driven by industrial expansion and a growing middle class, makes hydropower an indispensable component of the energy mix. Technologically, continuous innovation in turbine efficiency, materials science, and digital grid integration is making hydropower projects more cost-effective and environmentally responsible. Policy-wise, governments are increasingly prioritizing renewable energy to meet climate targets and enhance energy security, often providing substantial incentives, favorable regulations, and long-term power purchase agreements that de-risk investments. For instance, national renewable energy goals, such as Vietnam's commitment to increasing its renewable energy share, directly translate into significant opportunities for new hydropower developments.

Challenges Impacting APAC Hydropower Industry Growth

The expansion of the APAC Hydropower Industry faces significant hurdles. Environmental impact assessments and concerns regarding biodiversity, water quality, and social displacement often lead to protracted permitting processes and public opposition, sometimes adding years to project timelines. The substantial upfront capital required for large-scale hydropower projects remains a formidable barrier, particularly for smaller economies or projects with less predictable revenue streams. Regulatory complexities and inconsistent policy frameworks across different countries can create uncertainty for investors, leading to project delays. Furthermore, supply chain disruptions for specialized equipment and skilled labor shortages can impact project execution and cost control, potentially adding 10-15% to overall project expenses. Competitive pressures from rapidly evolving solar and wind technologies, which often have lower upfront costs and faster deployment times, also present a continuous challenge, necessitating that hydropower projects emphasize their unique advantages like grid stability and long operational lifespans.

Key Players Shaping the APAC Hydropower Industry Market

- PowerChina

- PT Perusahaan Listrik Negara

- General Electric Company (GE Renewable Energy)

- China Yangtze Power Co Ltd

- Electricity Generating Authority of Thailand

- Aboitiz Power Corporation

- NTPC Limited

- NHPC Ltd

- Tenaga Nasional Berhad

- Tokyo Electric Power Company Holdings Inc

Significant APAC Hydropower Industry Industry Milestones

- July 2022: The Development Bank of the Philippines (DBP) approved USD 11.7 million in funding for the 4.6 MW Dupinga Mini Hydropower project in Gabaldon, Nueva Ecija, Philippines, significantly contributing to the nation's 30% renewable energy goal by 2030.

- March 2022: International technology group ANDRITZ and the Electricity Generating Authority of Thailand (EGAT) signed a Memorandum of Understanding (MoU) to explore and expand business opportunities for hydropower projects in Thailand and surrounding countries, signaling a strategic move towards regional collaboration and development.

Future Outlook for APAC Hydropower Industry Market

The future outlook for the APAC Hydropower Industry is exceptionally positive, driven by a robust combination of escalating energy demands, aggressive renewable energy mandates, and technological advancements. Strategic opportunities abound in modernizing existing infrastructure to improve efficiency and longevity, alongside the continued development of both large-scale and small hydropower projects to meet diverse energy needs. The growing emphasis on pumped-storage hydropower for grid stabilization, particularly with the increasing penetration of intermittent solar and wind power, presents a significant growth catalyst. As nations in the Asia-Pacific continue to prioritize energy security and decarbonization, hydropower is poised to remain a cornerstone of their sustainable energy strategies, attracting substantial investment and driving innovation for decades to come. The market potential is further amplified by cross-border collaboration and the integration of hydropower into smart grid ecosystems.

APAC Hydropower Industry Segmentation

-

1. Size

- 1.1. Large Hydropower

- 1.2. Small Hydropower

- 1.3. Other Sizes

-

2. Geography

- 2.1. China

- 2.2. India

- 2.3. Japan

- 2.4. Vietnam

- 2.5. Rest of Asia-Pacific

APAC Hydropower Industry Segmentation By Geography

- 1. China

- 2. India

- 3. Japan

- 4. Vietnam

- 5. Rest of Asia Pacific

APAC Hydropower Industry Regional Market Share

Geographic Coverage of APAC Hydropower Industry

APAC Hydropower Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Size

- 5.1.1. Large Hydropower

- 5.1.2. Small Hydropower

- 5.1.3. Other Sizes

- 5.2. Market Analysis, Insights and Forecast - by Geography

- 5.2.1. China

- 5.2.2. India

- 5.2.3. Japan

- 5.2.4. Vietnam

- 5.2.5. Rest of Asia-Pacific

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. China

- 5.3.2. India

- 5.3.3. Japan

- 5.3.4. Vietnam

- 5.3.5. Rest of Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Size

- 6. Global APAC Hydropower Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Size

- 6.1.1. Large Hydropower

- 6.1.2. Small Hydropower

- 6.1.3. Other Sizes

- 6.2. Market Analysis, Insights and Forecast - by Geography

- 6.2.1. China

- 6.2.2. India

- 6.2.3. Japan

- 6.2.4. Vietnam

- 6.2.5. Rest of Asia-Pacific

- 6.1. Market Analysis, Insights and Forecast - by Size

- 7. China APAC Hydropower Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Size

- 7.1.1. Large Hydropower

- 7.1.2. Small Hydropower

- 7.1.3. Other Sizes

- 7.2. Market Analysis, Insights and Forecast - by Geography

- 7.2.1. China

- 7.2.2. India

- 7.2.3. Japan

- 7.2.4. Vietnam

- 7.2.5. Rest of Asia-Pacific

- 7.1. Market Analysis, Insights and Forecast - by Size

- 8. India APAC Hydropower Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Size

- 8.1.1. Large Hydropower

- 8.1.2. Small Hydropower

- 8.1.3. Other Sizes

- 8.2. Market Analysis, Insights and Forecast - by Geography

- 8.2.1. China

- 8.2.2. India

- 8.2.3. Japan

- 8.2.4. Vietnam

- 8.2.5. Rest of Asia-Pacific

- 8.1. Market Analysis, Insights and Forecast - by Size

- 9. Japan APAC Hydropower Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Size

- 9.1.1. Large Hydropower

- 9.1.2. Small Hydropower

- 9.1.3. Other Sizes

- 9.2. Market Analysis, Insights and Forecast - by Geography

- 9.2.1. China

- 9.2.2. India

- 9.2.3. Japan

- 9.2.4. Vietnam

- 9.2.5. Rest of Asia-Pacific

- 9.1. Market Analysis, Insights and Forecast - by Size

- 10. Vietnam APAC Hydropower Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Size

- 10.1.1. Large Hydropower

- 10.1.2. Small Hydropower

- 10.1.3. Other Sizes

- 10.2. Market Analysis, Insights and Forecast - by Geography

- 10.2.1. China

- 10.2.2. India

- 10.2.3. Japan

- 10.2.4. Vietnam

- 10.2.5. Rest of Asia-Pacific

- 10.1. Market Analysis, Insights and Forecast - by Size

- 11. Rest of Asia Pacific APAC Hydropower Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Size

- 11.1.1. Large Hydropower

- 11.1.2. Small Hydropower

- 11.1.3. Other Sizes

- 11.2. Market Analysis, Insights and Forecast - by Geography

- 11.2.1. China

- 11.2.2. India

- 11.2.3. Japan

- 11.2.4. Vietnam

- 11.2.5. Rest of Asia-Pacific

- 11.1. Market Analysis, Insights and Forecast - by Size

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 PowerChina

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 PT Perusahaan Listrik Negara

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 General Electric Company (GE Renewable Energy)

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 China Yangtze Power Co Ltd

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Electricity Generating Authority of Thailand

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Aboitiz Power Corporation

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 NTPC Limited

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 NHPC Ltd

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Tenaga Nasional Berhad

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Tokyo Electric Power Company Holdings Inc

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 PowerChina

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global APAC Hydropower Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global APAC Hydropower Industry Volume Breakdown (terawatt, %) by Region 2025 & 2033

- Figure 3: China APAC Hydropower Industry Revenue (billion), by Size 2025 & 2033

- Figure 4: China APAC Hydropower Industry Volume (terawatt), by Size 2025 & 2033

- Figure 5: China APAC Hydropower Industry Revenue Share (%), by Size 2025 & 2033

- Figure 6: China APAC Hydropower Industry Volume Share (%), by Size 2025 & 2033

- Figure 7: China APAC Hydropower Industry Revenue (billion), by Geography 2025 & 2033

- Figure 8: China APAC Hydropower Industry Volume (terawatt), by Geography 2025 & 2033

- Figure 9: China APAC Hydropower Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 10: China APAC Hydropower Industry Volume Share (%), by Geography 2025 & 2033

- Figure 11: China APAC Hydropower Industry Revenue (billion), by Country 2025 & 2033

- Figure 12: China APAC Hydropower Industry Volume (terawatt), by Country 2025 & 2033

- Figure 13: China APAC Hydropower Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: China APAC Hydropower Industry Volume Share (%), by Country 2025 & 2033

- Figure 15: India APAC Hydropower Industry Revenue (billion), by Size 2025 & 2033

- Figure 16: India APAC Hydropower Industry Volume (terawatt), by Size 2025 & 2033

- Figure 17: India APAC Hydropower Industry Revenue Share (%), by Size 2025 & 2033

- Figure 18: India APAC Hydropower Industry Volume Share (%), by Size 2025 & 2033

- Figure 19: India APAC Hydropower Industry Revenue (billion), by Geography 2025 & 2033

- Figure 20: India APAC Hydropower Industry Volume (terawatt), by Geography 2025 & 2033

- Figure 21: India APAC Hydropower Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 22: India APAC Hydropower Industry Volume Share (%), by Geography 2025 & 2033

- Figure 23: India APAC Hydropower Industry Revenue (billion), by Country 2025 & 2033

- Figure 24: India APAC Hydropower Industry Volume (terawatt), by Country 2025 & 2033

- Figure 25: India APAC Hydropower Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: India APAC Hydropower Industry Volume Share (%), by Country 2025 & 2033

- Figure 27: Japan APAC Hydropower Industry Revenue (billion), by Size 2025 & 2033

- Figure 28: Japan APAC Hydropower Industry Volume (terawatt), by Size 2025 & 2033

- Figure 29: Japan APAC Hydropower Industry Revenue Share (%), by Size 2025 & 2033

- Figure 30: Japan APAC Hydropower Industry Volume Share (%), by Size 2025 & 2033

- Figure 31: Japan APAC Hydropower Industry Revenue (billion), by Geography 2025 & 2033

- Figure 32: Japan APAC Hydropower Industry Volume (terawatt), by Geography 2025 & 2033

- Figure 33: Japan APAC Hydropower Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 34: Japan APAC Hydropower Industry Volume Share (%), by Geography 2025 & 2033

- Figure 35: Japan APAC Hydropower Industry Revenue (billion), by Country 2025 & 2033

- Figure 36: Japan APAC Hydropower Industry Volume (terawatt), by Country 2025 & 2033

- Figure 37: Japan APAC Hydropower Industry Revenue Share (%), by Country 2025 & 2033

- Figure 38: Japan APAC Hydropower Industry Volume Share (%), by Country 2025 & 2033

- Figure 39: Vietnam APAC Hydropower Industry Revenue (billion), by Size 2025 & 2033

- Figure 40: Vietnam APAC Hydropower Industry Volume (terawatt), by Size 2025 & 2033

- Figure 41: Vietnam APAC Hydropower Industry Revenue Share (%), by Size 2025 & 2033

- Figure 42: Vietnam APAC Hydropower Industry Volume Share (%), by Size 2025 & 2033

- Figure 43: Vietnam APAC Hydropower Industry Revenue (billion), by Geography 2025 & 2033

- Figure 44: Vietnam APAC Hydropower Industry Volume (terawatt), by Geography 2025 & 2033

- Figure 45: Vietnam APAC Hydropower Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 46: Vietnam APAC Hydropower Industry Volume Share (%), by Geography 2025 & 2033

- Figure 47: Vietnam APAC Hydropower Industry Revenue (billion), by Country 2025 & 2033

- Figure 48: Vietnam APAC Hydropower Industry Volume (terawatt), by Country 2025 & 2033

- Figure 49: Vietnam APAC Hydropower Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Vietnam APAC Hydropower Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: Rest of Asia Pacific APAC Hydropower Industry Revenue (billion), by Size 2025 & 2033

- Figure 52: Rest of Asia Pacific APAC Hydropower Industry Volume (terawatt), by Size 2025 & 2033

- Figure 53: Rest of Asia Pacific APAC Hydropower Industry Revenue Share (%), by Size 2025 & 2033

- Figure 54: Rest of Asia Pacific APAC Hydropower Industry Volume Share (%), by Size 2025 & 2033

- Figure 55: Rest of Asia Pacific APAC Hydropower Industry Revenue (billion), by Geography 2025 & 2033

- Figure 56: Rest of Asia Pacific APAC Hydropower Industry Volume (terawatt), by Geography 2025 & 2033

- Figure 57: Rest of Asia Pacific APAC Hydropower Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 58: Rest of Asia Pacific APAC Hydropower Industry Volume Share (%), by Geography 2025 & 2033

- Figure 59: Rest of Asia Pacific APAC Hydropower Industry Revenue (billion), by Country 2025 & 2033

- Figure 60: Rest of Asia Pacific APAC Hydropower Industry Volume (terawatt), by Country 2025 & 2033

- Figure 61: Rest of Asia Pacific APAC Hydropower Industry Revenue Share (%), by Country 2025 & 2033

- Figure 62: Rest of Asia Pacific APAC Hydropower Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global APAC Hydropower Industry Revenue billion Forecast, by Size 2020 & 2033

- Table 2: Global APAC Hydropower Industry Volume terawatt Forecast, by Size 2020 & 2033

- Table 3: Global APAC Hydropower Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 4: Global APAC Hydropower Industry Volume terawatt Forecast, by Geography 2020 & 2033

- Table 5: Global APAC Hydropower Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global APAC Hydropower Industry Volume terawatt Forecast, by Region 2020 & 2033

- Table 7: Global APAC Hydropower Industry Revenue billion Forecast, by Size 2020 & 2033

- Table 8: Global APAC Hydropower Industry Volume terawatt Forecast, by Size 2020 & 2033

- Table 9: Global APAC Hydropower Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 10: Global APAC Hydropower Industry Volume terawatt Forecast, by Geography 2020 & 2033

- Table 11: Global APAC Hydropower Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Global APAC Hydropower Industry Volume terawatt Forecast, by Country 2020 & 2033

- Table 13: Global APAC Hydropower Industry Revenue billion Forecast, by Size 2020 & 2033

- Table 14: Global APAC Hydropower Industry Volume terawatt Forecast, by Size 2020 & 2033

- Table 15: Global APAC Hydropower Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 16: Global APAC Hydropower Industry Volume terawatt Forecast, by Geography 2020 & 2033

- Table 17: Global APAC Hydropower Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 18: Global APAC Hydropower Industry Volume terawatt Forecast, by Country 2020 & 2033

- Table 19: Global APAC Hydropower Industry Revenue billion Forecast, by Size 2020 & 2033

- Table 20: Global APAC Hydropower Industry Volume terawatt Forecast, by Size 2020 & 2033

- Table 21: Global APAC Hydropower Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 22: Global APAC Hydropower Industry Volume terawatt Forecast, by Geography 2020 & 2033

- Table 23: Global APAC Hydropower Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 24: Global APAC Hydropower Industry Volume terawatt Forecast, by Country 2020 & 2033

- Table 25: Global APAC Hydropower Industry Revenue billion Forecast, by Size 2020 & 2033

- Table 26: Global APAC Hydropower Industry Volume terawatt Forecast, by Size 2020 & 2033

- Table 27: Global APAC Hydropower Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 28: Global APAC Hydropower Industry Volume terawatt Forecast, by Geography 2020 & 2033

- Table 29: Global APAC Hydropower Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 30: Global APAC Hydropower Industry Volume terawatt Forecast, by Country 2020 & 2033

- Table 31: Global APAC Hydropower Industry Revenue billion Forecast, by Size 2020 & 2033

- Table 32: Global APAC Hydropower Industry Volume terawatt Forecast, by Size 2020 & 2033

- Table 33: Global APAC Hydropower Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 34: Global APAC Hydropower Industry Volume terawatt Forecast, by Geography 2020 & 2033

- Table 35: Global APAC Hydropower Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 36: Global APAC Hydropower Industry Volume terawatt Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the APAC Hydropower Industry?

The projected CAGR is approximately 12.1%.

2. Which companies are prominent players in the APAC Hydropower Industry?

Key companies in the market include PowerChina, PT Perusahaan Listrik Negara, General Electric Company (GE Renewable Energy), China Yangtze Power Co Ltd, Electricity Generating Authority of Thailand, Aboitiz Power Corporation, NTPC Limited, NHPC Ltd, Tenaga Nasional Berhad, Tokyo Electric Power Company Holdings Inc.

3. What are the main segments of the APAC Hydropower Industry?

The market segments include Size, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 98.5 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Power Generation Capacity Plans and Increasing Electricity Demand4.; Rapidly Growing Industrial and Infrastructural Development Activities.

6. What are the notable trends driving market growth?

Small Hydropower Segment Anticipated to Dominate the Market During the Forecast Period.

7. Are there any restraints impacting market growth?

4.; Coal Substituted with Clean Energy Sources.

8. Can you provide examples of recent developments in the market?

In July 2022, the Development Bank of the Philippines (DBP) approved USD 11.7 million in funding to support the development of the 4.6 MW Dupinga Mini Hydropower project in Gabaldon, Nueva Ecija, in the Philippines. The DBP's financing of the Dupinga Project will help the government reach its 30% renewable energy goal by 2030.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in terawatt.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "APAC Hydropower Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the APAC Hydropower Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the APAC Hydropower Industry?

To stay informed about further developments, trends, and reports in the APAC Hydropower Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence