Key Insights

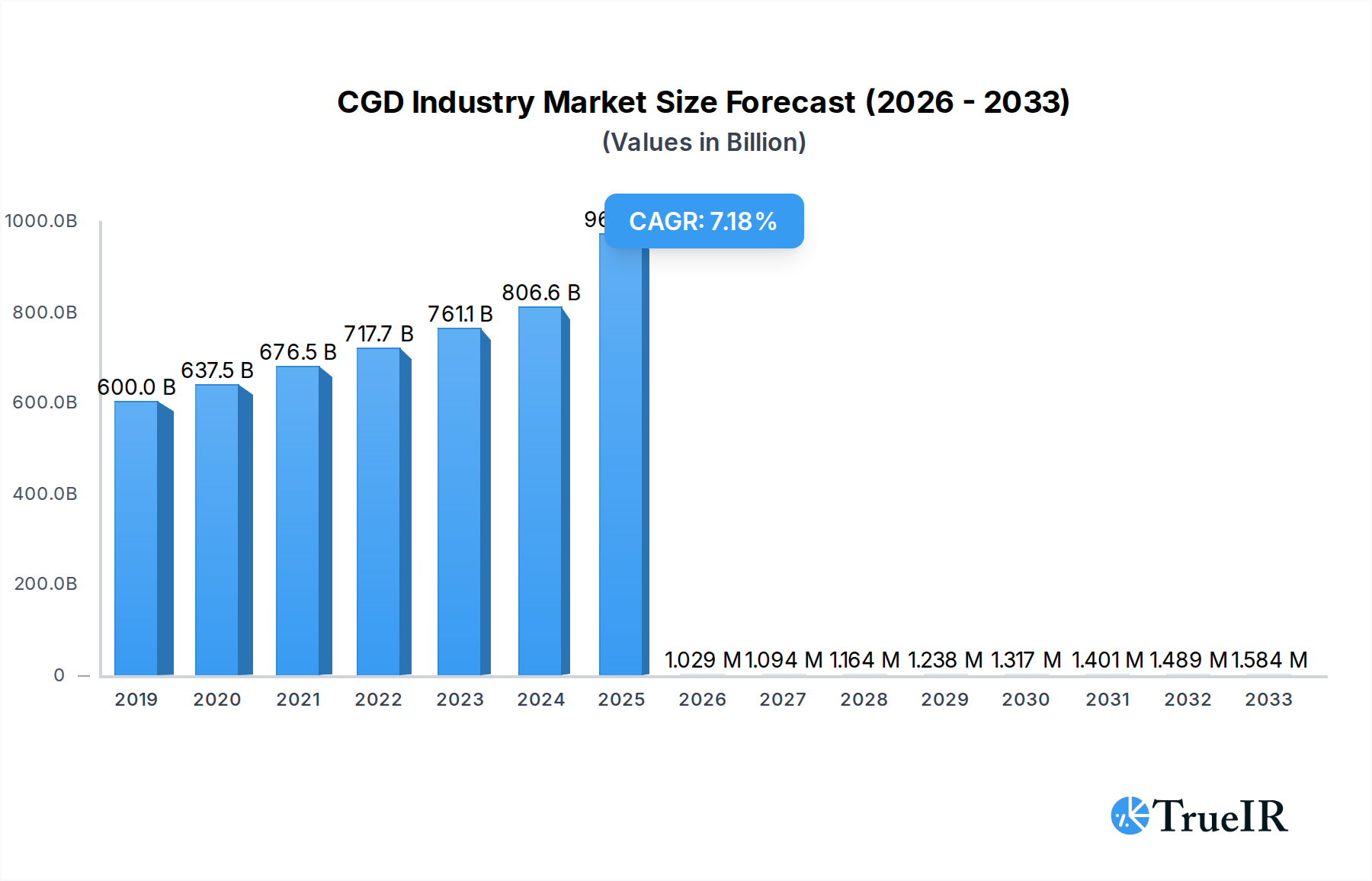

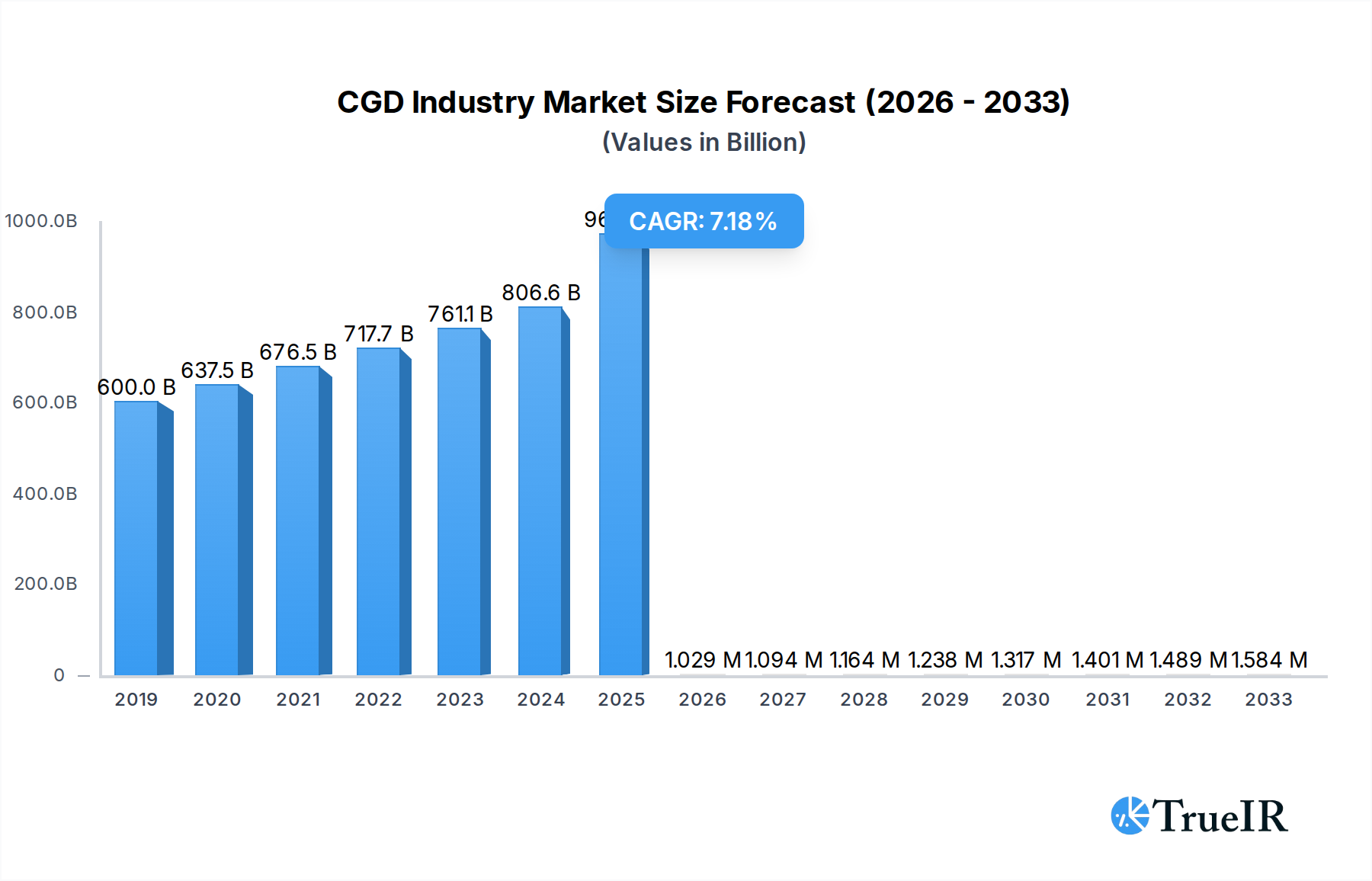

The City Gas Distribution (CGD) industry is poised for significant expansion, projected to reach a market size of USD 967.58 billion in 2025. This robust growth is underpinned by a compelling Compound Annual Growth Rate (CAGR) of 6.4% forecasted between 2019 and 2033. Several powerful drivers are fueling this upward trajectory. The increasing demand for cleaner and more efficient energy sources, coupled with government initiatives promoting the use of natural gas in transportation and domestic applications, is a primary catalyst. Furthermore, the expansion of gas infrastructure, including pipelines and refueling stations, is crucial for meeting this escalating demand. The rising adoption of Compressed Natural Gas (CNG) for the automotive sector, driven by cost-effectiveness and environmental regulations, and the growing preference for Piped Natural Gas (PNG) in residential and commercial segments for cooking and heating, are key trends shaping the market.

CGD Industry Market Size (In Billion)

Despite this optimistic outlook, certain restraints could influence the pace of growth. These include the high capital expenditure required for establishing extensive CGD networks and the challenges associated with land acquisition and regulatory approvals. Additionally, the price volatility of natural gas in the global market can impact its competitiveness against other energy sources. However, the industry is actively addressing these challenges through technological advancements in gas distribution, innovative financing models, and strategic partnerships. The market is segmented into distinct categories based on connection type (PNG and CNG) and end-user industries (automotive, residential, commercial, and industrial), each presenting unique growth opportunities. Leading companies are actively investing in expanding their reach and enhancing their service offerings to capitalize on the burgeoning demand across key global regions.

CGD Industry Company Market Share

Unveiling the Future: Comprehensive Report on India's City Gas Distribution (CGD) Industry

This in-depth report provides an unparalleled analysis of India's burgeoning City Gas Distribution (CGD) industry, forecasting its trajectory from 2019 to 2033, with a detailed examination of the base year 2025 and a comprehensive forecast period from 2025 to 2033. Delving into the historical landscape of 2019-2024, this report offers critical insights into market dynamics, technological advancements, regulatory influences, and the competitive forces shaping this vital sector. With a focus on high-volume keywords such as "Natural Gas Distribution," "CNG Stations," "PNG Connections," "City Gas Networks," and "Energy Transition," this report is meticulously designed for industry stakeholders seeking a strategic advantage.

CGD Industry Market Structure & Competitive Landscape

The Indian CGD industry is characterized by a dynamic market structure with significant growth potential. Market concentration is evolving, with key players vying for dominance in expanding geographical areas. Innovation drivers are largely centered on improving infrastructure efficiency, enhancing safety protocols, and developing advanced metering solutions for both Pipeline Natural Gas (PNG) and Compressed Natural Gas (CNG) segments. Regulatory impacts are profound, with government policies promoting natural gas adoption playing a crucial role in market expansion. Product substitutes, primarily LPG and electricity, present a competitive challenge, though natural gas offers distinct advantages in terms of cost-effectiveness and environmental benefits, particularly for industrial and automotive end-users. The end-user segmentation spans automotive, residential, commercial, and industrial sectors, each with unique demand drivers. Mergers and acquisitions (M&A) trends are anticipated to increase as companies seek to consolidate their market positions, expand their geographical reach, and leverage economies of scale. Concentration ratios are projected to see a gradual decrease in specific regions due to the entry of new players and the expansion of existing networks, fostering a more competitive environment. The overall M&A volume is expected to grow by over $5 billion in the forecast period as companies look to acquire new licenses and strengthen their infrastructure.

- Market Concentration: Moderate to high in established regions, with increasing fragmentation in newly awarded geographical areas.

- Innovation Drivers: Infrastructure upgrades, digital metering, enhanced safety technologies, and customer service improvements.

- Regulatory Impacts: Favorable policies, government incentives, and stringent environmental regulations are key determinants of market growth.

- Product Substitutes: LPG, electricity, and other cleaner fuels.

- End-User Segmentation: Automotive (CNG), Residential (PNG), Commercial (PNG/CNG), Industrial (PNG).

- M&A Trends: Consolidation for geographical expansion, portfolio diversification, and infrastructure acquisition.

CGD Industry Market Trends & Opportunities

The City Gas Distribution (CGD) industry in India is poised for extraordinary growth, driven by a confluence of favorable market trends and substantial opportunities. The market size is projected to witness a Compound Annual Growth Rate (CAGR) of over 15% during the forecast period, fueled by increasing natural gas consumption and infrastructure development. Technological shifts are prominently visible in the evolution of smart metering technologies, enabling remote monitoring and more efficient billing for both PNG and CNG. Advanced distribution network management systems are also being adopted to enhance operational efficiency and reduce losses. Consumer preferences are increasingly leaning towards cleaner and more affordable energy sources, making natural gas an attractive alternative to traditional fuels, especially for residential and automotive applications. The automotive sector, in particular, is experiencing a surge in CNG vehicle adoption due to its cost-effectiveness and lower emissions, leading to a robust demand for CNG stations. Competitive dynamics are intensifying, with established public sector undertakings and private players actively expanding their footprints across new geographical areas. Opportunities abound in developing integrated energy solutions, exploring alternative fuels like hydrogen blends within existing CGD infrastructure, and leveraging digital platforms for enhanced customer engagement and service delivery. The increasing focus on reducing carbon footprints across all end-user segments presents a significant opportunity for CGD players to capture market share. Furthermore, government initiatives aimed at increasing the share of natural gas in India's energy mix are creating a conducive environment for sustained growth and investment. The expansion of CGD networks into Tier-2 and Tier-3 cities represents a massive untapped market potential, promising significant returns for early movers.

Dominant Markets & Segments in CGD Industry

The Indian CGD industry exhibits a clear dominance in specific regions and segments, driven by robust infrastructure development, supportive government policies, and a growing demand for cleaner energy. The Pipeline Natural Gas (PNG) Connections segment, particularly for Residential and Commercial end-users, is a major growth driver, accounting for over 60% of the market in terms of connection volume. This dominance is bolstered by extensive pipeline network expansion and government push for household gas connectivity. In parallel, the Compressed Natural Gas (CNG) Connections segment, primarily serving the Automotive sector, is experiencing rapid expansion. The government's ambitious plan to establish thousands of new CNG stations across the country is a testament to the strategic importance of this segment. The Industrial end-user segment, utilizing PNG for manufacturing processes, also represents a significant and growing market due to cost advantages and environmental regulations.

- Dominant Region/Country: India, with a strong focus on urban and semi-urban agglomerations.

- Leading Segment: Pipeline Natural Gas (PNG) Connections, followed closely by Compressed Natural Gas (CNG) Connections.

- Key Growth Drivers for PNG:

- Government initiatives for household gas penetration.

- Expansion of pipeline infrastructure into new cities and towns.

- Increasing adoption by commercial establishments for cooking and heating.

- Cost-effectiveness and environmental benefits compared to LPG.

- Key Growth Drivers for CNG:

- Government mandate for increased CNG stations nationwide.

- Growing demand for cleaner and cheaper fuel for public transport and commercial vehicles.

- Favorable economics for fleet operators.

- Subsidies and incentives promoting CNG vehicle adoption.

- Market Dominance Analysis:

- Residential PNG: Driven by a growing middle class seeking convenient and cleaner cooking fuel, supported by widespread urbanisation and government housing schemes.

- Automotive CNG: Fueled by the rising number of CNG-powered vehicles, especially in public transportation and commercial fleets, to curb pollution and reduce operating costs.

- Commercial PNG: Significant adoption in hotels, restaurants, and other businesses for their energy needs due to reliability and cost efficiency.

- Industrial PNG: Essential for various manufacturing processes requiring consistent and clean energy, with growth linked to industrial expansion and stricter emission norms.

CGD Industry Product Analysis

The CGD industry's product landscape is defined by its core offerings: Pipeline Natural Gas (PNG) and Compressed Natural Gas (CNG). PNG, delivered directly to end-users through an extensive network of pipelines, offers unparalleled convenience and reliability for residential, commercial, and industrial applications. Innovations focus on enhancing pipeline integrity, leak detection technology, and smart metering for precise consumption tracking. CNG, a compressed form of natural gas, is primarily utilized as a cleaner and more economical fuel for vehicles. Advancements in CNG fueling infrastructure, including the development of faster dispensing technologies and a broader network of CNG stations, are key. The competitive advantage of both products lies in their lower carbon emissions compared to conventional fuels, cost-effectiveness, and the vast natural gas reserves being tapped into through enhanced exploration and import strategies.

Key Drivers, Barriers & Challenges in CGD Industry

The CGD industry's expansion is propelled by several key drivers, including strong government support for natural gas adoption, increasing environmental consciousness, and the economic advantage of natural gas over other fuels for various applications. Technological advancements in pipeline construction and gas distribution further facilitate growth.

However, significant barriers and challenges exist. The capital-intensive nature of developing extensive pipeline networks requires substantial investment. Regulatory complexities and land acquisition hurdles can lead to project delays. Supply chain disruptions and the availability of skilled labor for infrastructure development also pose challenges. Intense competition from established energy providers and alternative fuels like LPG can impact market penetration rates.

Growth Drivers in the CGD Industry Market

The growth of the CGD industry is significantly propelled by government policies aimed at increasing natural gas usage in India's energy mix, offering substantial incentives for infrastructure development and network expansion. Technological advancements in gas exploration, extraction, and distribution, coupled with innovations in smart metering and network management, are enhancing operational efficiency. Economically, the increasing price volatility of crude oil makes natural gas a more stable and cost-effective alternative for consumers across residential, commercial, and automotive sectors. The rising environmental awareness and stringent emission norms are also creating a robust demand for cleaner fuels like natural gas, driving its adoption.

Challenges Impacting CGD Industry Growth

Regulatory complexities and the lengthy approval processes for new pipeline projects present significant hurdles, often leading to project delays and increased costs. Supply chain issues related to the timely procurement of materials and equipment for network construction can impact project timelines. The immense capital investment required for building extensive CGD networks acts as a substantial barrier to entry and expansion, especially in remote or less commercially viable areas. Intense competition from alternative energy sources like LPG and electricity, along with the existing infrastructure of these fuels, poses a continuous competitive pressure. Additionally, ensuring adequate gas supply to meet the growing demand requires robust import infrastructure and long-term supply agreements, which can be subject to geopolitical and market fluctuations.

Key Players Shaping the CGD Industry Market

- Adani Total Gas Ltd

- Aavantika Gas Ltd

- IndianOil-Adani Gas Pvt Ltd

- Mahanagar Gas Ltd

- Indraprastha Gas Limited

- Assam Gas Company Ltd

- Sabarmati Gas Ltd

- GAIL Gas Limited

- SKN-Haryana City Gas Distribution Pvt Ltd

- Gujarat Gas Ltd

- Torrent Group

Significant CGD Industry Industry Milestones

- July 2022: Petroleum ministry announces plans to establish 3,500 CNG stations in India over the next two years. GAIL and nine of its CGD companies will set up these CNG stations in 41 geographical areas spread across 14 states.

- January 2022: Bharat Petroleum Corporation Ltd (BPCL) announces an investment of USD 1.35 billion over the next five years in setting up city gas distribution networks in cities for which it secured licenses in the 11th bidding round.

Future Outlook for CGD Industry Market

The future outlook for India's CGD industry is exceptionally bright, characterized by sustained high growth driven by aggressive government policies, increasing consumer preference for cleaner energy, and significant infrastructure expansion. Strategic opportunities lie in leveraging technological advancements to enhance network efficiency and customer experience, exploring blended gas solutions, and expanding into untapped geographical areas. The industry is poised to play a pivotal role in India's energy transition, contributing to reduced emissions and energy security, with an estimated market expansion exceeding $100 billion by 2033.

CGD Industry Segmentation

-

1. Type

- 1.1. Pipeline Natural Gas (PNG) Connections

- 1.2. Compressed Natural Gas (CNG) Connections

-

2. End User

- 2.1. Automotive

- 2.2. Residential

- 2.3. Commercial

- 2.4. Industrial

CGD Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

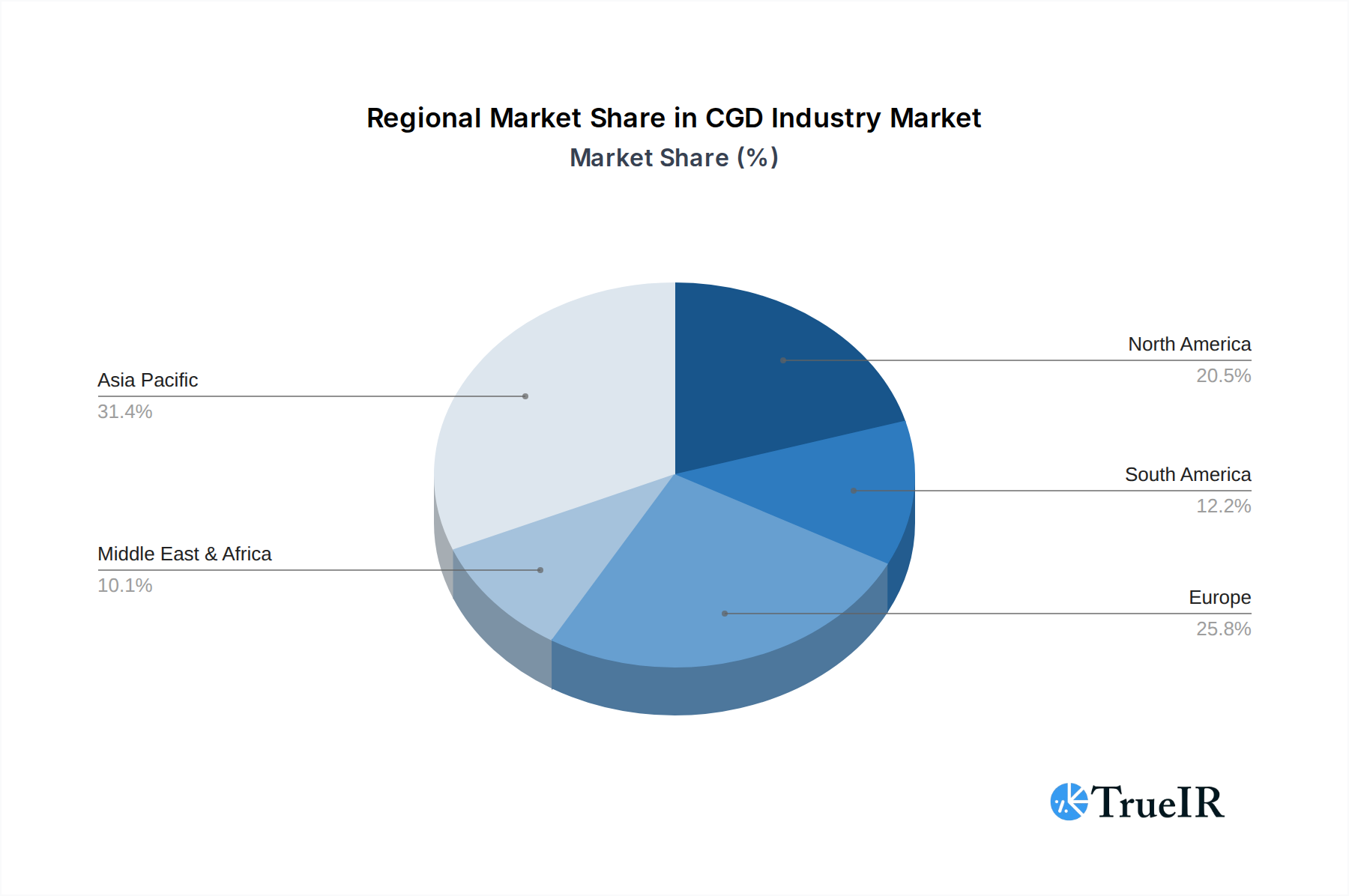

CGD Industry Regional Market Share

Geographic Coverage of CGD Industry

CGD Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Pipeline Natural Gas (PNG) Connections

- 5.1.2. Compressed Natural Gas (CNG) Connections

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Automotive

- 5.2.2. Residential

- 5.2.3. Commercial

- 5.2.4. Industrial

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global CGD Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Pipeline Natural Gas (PNG) Connections

- 6.1.2. Compressed Natural Gas (CNG) Connections

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Automotive

- 6.2.2. Residential

- 6.2.3. Commercial

- 6.2.4. Industrial

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America CGD Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Pipeline Natural Gas (PNG) Connections

- 7.1.2. Compressed Natural Gas (CNG) Connections

- 7.2. Market Analysis, Insights and Forecast - by End User

- 7.2.1. Automotive

- 7.2.2. Residential

- 7.2.3. Commercial

- 7.2.4. Industrial

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. South America CGD Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Pipeline Natural Gas (PNG) Connections

- 8.1.2. Compressed Natural Gas (CNG) Connections

- 8.2. Market Analysis, Insights and Forecast - by End User

- 8.2.1. Automotive

- 8.2.2. Residential

- 8.2.3. Commercial

- 8.2.4. Industrial

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Europe CGD Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Pipeline Natural Gas (PNG) Connections

- 9.1.2. Compressed Natural Gas (CNG) Connections

- 9.2. Market Analysis, Insights and Forecast - by End User

- 9.2.1. Automotive

- 9.2.2. Residential

- 9.2.3. Commercial

- 9.2.4. Industrial

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Middle East & Africa CGD Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Pipeline Natural Gas (PNG) Connections

- 10.1.2. Compressed Natural Gas (CNG) Connections

- 10.2. Market Analysis, Insights and Forecast - by End User

- 10.2.1. Automotive

- 10.2.2. Residential

- 10.2.3. Commercial

- 10.2.4. Industrial

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Asia Pacific CGD Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Pipeline Natural Gas (PNG) Connections

- 11.1.2. Compressed Natural Gas (CNG) Connections

- 11.2. Market Analysis, Insights and Forecast - by End User

- 11.2.1. Automotive

- 11.2.2. Residential

- 11.2.3. Commercial

- 11.2.4. Industrial

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Adani Total Gas Ltd

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Aavantika Gas Ltd

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 IndianOil-Adani Gas Pvt Ltd

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Mahanagar Gas Ltd

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Indraprastha Gas Limited

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Assam Gas Company Ltd

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Sabarmati Gas Ltd

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 GAIL Gas Limited

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 SKN-Haryana City Gas Distribution Pvt Ltd

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Gujarat Gas Ltd

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Torrent Group

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.1 Adani Total Gas Ltd

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global CGD Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America CGD Industry Revenue (billion), by Type 2025 & 2033

- Figure 3: North America CGD Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America CGD Industry Revenue (billion), by End User 2025 & 2033

- Figure 5: North America CGD Industry Revenue Share (%), by End User 2025 & 2033

- Figure 6: North America CGD Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America CGD Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America CGD Industry Revenue (billion), by Type 2025 & 2033

- Figure 9: South America CGD Industry Revenue Share (%), by Type 2025 & 2033

- Figure 10: South America CGD Industry Revenue (billion), by End User 2025 & 2033

- Figure 11: South America CGD Industry Revenue Share (%), by End User 2025 & 2033

- Figure 12: South America CGD Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: South America CGD Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe CGD Industry Revenue (billion), by Type 2025 & 2033

- Figure 15: Europe CGD Industry Revenue Share (%), by Type 2025 & 2033

- Figure 16: Europe CGD Industry Revenue (billion), by End User 2025 & 2033

- Figure 17: Europe CGD Industry Revenue Share (%), by End User 2025 & 2033

- Figure 18: Europe CGD Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe CGD Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa CGD Industry Revenue (billion), by Type 2025 & 2033

- Figure 21: Middle East & Africa CGD Industry Revenue Share (%), by Type 2025 & 2033

- Figure 22: Middle East & Africa CGD Industry Revenue (billion), by End User 2025 & 2033

- Figure 23: Middle East & Africa CGD Industry Revenue Share (%), by End User 2025 & 2033

- Figure 24: Middle East & Africa CGD Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa CGD Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific CGD Industry Revenue (billion), by Type 2025 & 2033

- Figure 27: Asia Pacific CGD Industry Revenue Share (%), by Type 2025 & 2033

- Figure 28: Asia Pacific CGD Industry Revenue (billion), by End User 2025 & 2033

- Figure 29: Asia Pacific CGD Industry Revenue Share (%), by End User 2025 & 2033

- Figure 30: Asia Pacific CGD Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific CGD Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global CGD Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Global CGD Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 3: Global CGD Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global CGD Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 5: Global CGD Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 6: Global CGD Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States CGD Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada CGD Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico CGD Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global CGD Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 11: Global CGD Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 12: Global CGD Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil CGD Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina CGD Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America CGD Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global CGD Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 17: Global CGD Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 18: Global CGD Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom CGD Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany CGD Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France CGD Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy CGD Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain CGD Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia CGD Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux CGD Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics CGD Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe CGD Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global CGD Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 29: Global CGD Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 30: Global CGD Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey CGD Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel CGD Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC CGD Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa CGD Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa CGD Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa CGD Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global CGD Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 38: Global CGD Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 39: Global CGD Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China CGD Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India CGD Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan CGD Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea CGD Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN CGD Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania CGD Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific CGD Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the CGD Industry?

The projected CAGR is approximately 6.4%.

2. Which companies are prominent players in the CGD Industry?

Key companies in the market include Adani Total Gas Ltd, Aavantika Gas Ltd, IndianOil-Adani Gas Pvt Ltd, Mahanagar Gas Ltd, Indraprastha Gas Limited, Assam Gas Company Ltd, Sabarmati Gas Ltd, GAIL Gas Limited, SKN-Haryana City Gas Distribution Pvt Ltd, Gujarat Gas Ltd, Torrent Group.

3. What are the main segments of the CGD Industry?

The market segments include Type, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 967.58 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Growing Vehicle Ownership4.; Government Initiatives.

6. What are the notable trends driving market growth?

PNG Connections are Likely to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Volatile Crude Oil Prices.

8. Can you provide examples of recent developments in the market?

In July 2022, the petroleum ministry announced that it planned to set up 3,500 CNG stations in India in the next two years. GAIL and nine of its CGD companies will set up these CNG stations in 41 geographical areas spread across 14 states.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "CGD Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the CGD Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the CGD Industry?

To stay informed about further developments, trends, and reports in the CGD Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence