Key Insights

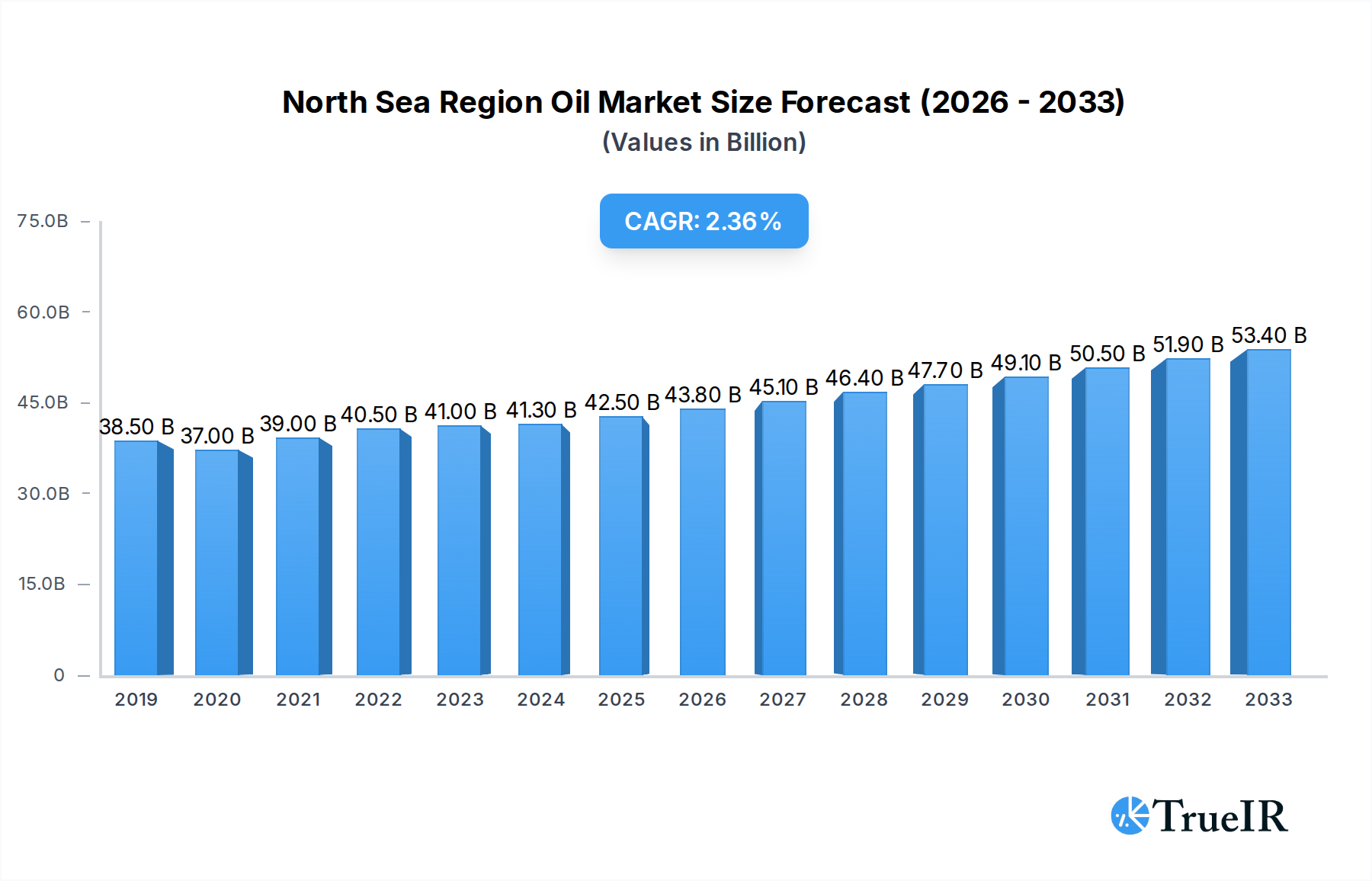

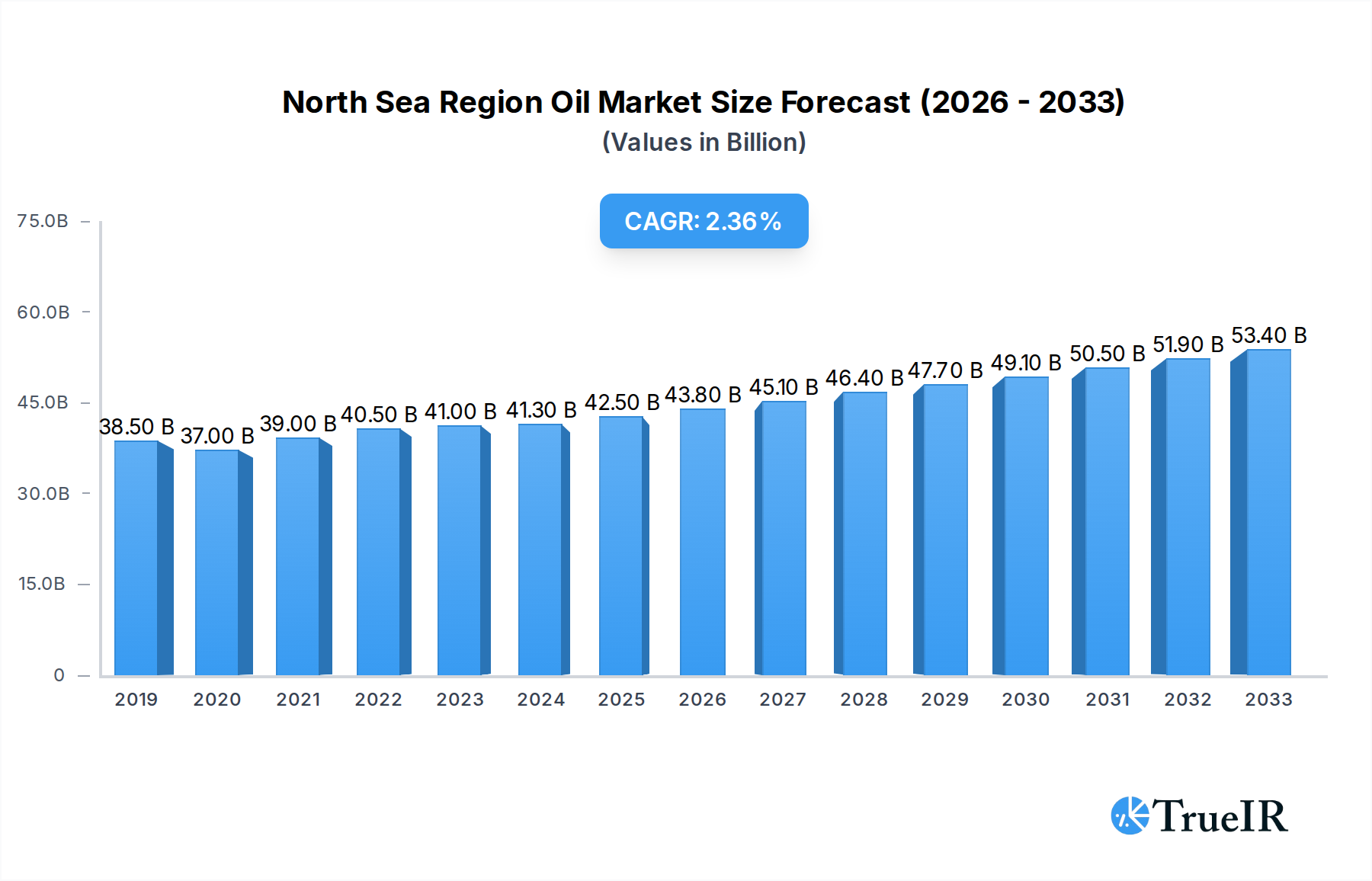

The North Sea Region Oil & Gas Industry is poised for steady expansion, projected to reach an estimated market size of $41.3 billion in 2024, exhibiting a compound annual growth rate (CAGR) of 4% through the forecast period ending in 2033. This growth is primarily fueled by increasing energy demand, coupled with significant investments in upstream exploration and production activities. Key drivers include the development of new fields, advancements in extraction technologies enhancing recovery rates from mature reservoirs, and the ongoing focus on optimizing existing infrastructure. The midstream sector is witnessing expansion through the development of new pipelines and storage facilities to support increased production and efficient transportation of hydrocarbons. Furthermore, the downstream segment is benefiting from refined product demand, with investments in upgrading refineries and petrochemical plants to meet evolving market needs. The region's strategic importance as a major oil and gas hub underpins these positive market dynamics, with companies actively engaged in both maintaining current production levels and exploring new frontiers.

North Sea Region Oil & Gas Industry Market Size (In Billion)

Despite the overall positive trajectory, the North Sea Oil & Gas Industry faces several challenges. Fluctuations in global crude oil prices, while a perennial factor, can significantly impact investment decisions and project profitability. Stringent environmental regulations and increasing pressure for decarbonization are compelling companies to invest heavily in sustainable practices, carbon capture technologies, and the exploration of renewable energy sources, which can divert capital from traditional oil and gas projects. Moreover, the aging infrastructure in some parts of the North Sea necessitates substantial maintenance and upgrade investments, adding to operational costs. Labor shortages and the need for specialized skill sets in a highly technical industry also present potential restraints. Nevertheless, technological innovations, such as enhanced oil recovery techniques and digital transformation in operations, are expected to mitigate some of these challenges, ensuring the continued resilience and adaptation of the North Sea's oil and gas sector. The region's commitment to innovation and responsible resource management will be crucial in navigating these complexities.

North Sea Region Oil & Gas Industry Company Market Share

Here's a dynamic, SEO-optimized report description for the North Sea Region Oil & Gas Industry, designed for immediate use without modification.

North Sea Region Oil & Gas Industry Market Structure & Competitive Landscape

The North Sea Region Oil & Gas Industry is characterized by a dynamic market structure and a competitive landscape shaped by significant investments, technological advancements, and evolving regulatory frameworks. Market concentration remains notable, with major integrated energy companies like Equinor ASA, Total S.A., BP Plc, and Royal Dutch Shell Plc holding substantial upstream and downstream assets. These giants, alongside specialized service providers such as Schlumberger Limited, Halliburton Company, and Baker Hughes Company, drive innovation and maintain a strong presence. The industry faces increasing scrutiny regarding environmental impact, leading to a greater emphasis on sustainable practices and carbon capture technologies, influencing product substitution dynamics and the adoption of cleaner energy alternatives. End-user segmentation is broad, spanning industrial manufacturing, transportation, and power generation. Mergers and acquisitions (M&A) activity, though potentially tempered by economic uncertainties, continues to be a significant trend, with an estimated M&A volume in the tens of billions of dollars over the historical period 2019-2024. Recent M&A deals have focused on consolidating existing assets, acquiring new exploration licenses, and investing in decarbonization technologies, with specific transaction values often reaching hundreds of millions to billions of dollars, reflecting strategic shifts towards portfolio optimization and future energy resilience. The competitive intensity is high, driven by the need to optimize production from mature fields while exploring new frontiers and adapting to the energy transition.

North Sea Region Oil & Gas Industry Market Trends & Opportunities

The North Sea Region Oil & Gas Industry is poised for significant evolution, driven by a confluence of technological innovation, shifting global energy demands, and a robust commitment to sustainability. The market size is projected to grow substantially from an estimated \$400 billion in 2025, reflecting sustained investment in both conventional and emerging energy solutions. Technological shifts are paramount, with advancements in digitalization, artificial intelligence, and enhanced oil recovery (EOR) techniques enabling more efficient extraction from existing reserves, estimated to contribute billions in improved yields. Furthermore, the increasing integration of renewable energy sources and the development of offshore wind power, often leveraging existing oil and gas infrastructure, present a significant diversification opportunity, with investments projected in the hundreds of billions over the forecast period. Consumer preferences are increasingly leaning towards lower-carbon energy sources, influencing downstream product development and investment strategies towards petrochemicals with reduced environmental footprints and biofuels. Competitive dynamics are intensifying, with companies like Equinor ASA, Total S.A., BP Plc, and Royal Dutch Shell Plc leading the charge in embracing both hydrocarbon optimization and the energy transition. The market penetration rate of sustainable energy solutions is expected to rise significantly, driven by regulatory mandates and corporate sustainability goals, potentially reaching double-digit growth percentages annually within the forecast period. Opportunities abound in areas such as offshore carbon capture and storage (CCS), hydrogen production utilizing offshore gas reserves, and the development of advanced offshore power generation technologies, with billions of dollars in potential investment and market creation. The resilience of the industry will be determined by its ability to adapt to these multifaceted trends, capitalizing on its extensive offshore expertise and infrastructure to navigate the complexities of a rapidly changing energy landscape.

Dominant Markets & Segments in North Sea Region Oil & Gas Industry

The North Sea Region Oil & Gas Industry exhibits distinct dominance across its key segments, with the Upstream sector typically representing the largest share of market value, estimated at over \$250 billion in 2025. This dominance is fueled by the continued strategic importance of hydrocarbon extraction from mature yet prolific fields, alongside ongoing exploration and development activities.

Upstream Dominance:

- Infrastructure: Extensive subsea infrastructure, including pipelines and production platforms, underpins efficient extraction. Investments in maintaining and upgrading this infrastructure are in the billions annually.

- Policies: Favorable licensing rounds, tax incentives, and government support for mature field development in countries like Norway and the UK contribute to sustained upstream activity.

- Technological Advancements: Continuous innovation in drilling techniques, reservoir management, and EOR technologies significantly boosts production from existing reserves, adding billions in value.

- Major Players: Companies such as Equinor ASA, Total S.A., BP Plc, and Royal Dutch Shell Plc are central to the upstream landscape, managing vast portfolios of assets.

Midstream Significance:

- Transportation Networks: A well-established network of pipelines and terminals is crucial for transporting oil and gas to refineries and export hubs. Investment in pipeline integrity and expansion is ongoing, with billions committed to maintaining and upgrading these vital arteries.

- Storage Facilities: Strategic storage capacity ensures supply chain stability and market responsiveness.

Downstream Evolution:

- Refining Capacity: While facing evolving demand patterns, downstream refining remains critical for producing fuels and petrochemicals. Refineries in the region process billions of barrels of crude oil annually.

- Petrochemical Production: A growing focus on high-value petrochemicals and sustainable chemical production represents a significant opportunity for downstream diversification, with substantial investment in new plants and technologies.

The dominance of the upstream segment is intrinsically linked to the region's geological endowment and the industry's ability to extract these resources efficiently and responsibly. However, significant opportunities and strategic investments are increasingly directed towards midstream and downstream segments, particularly those that support decarbonization efforts and the development of lower-carbon products. The interplay between these segments is vital for the overall health and future trajectory of the North Sea oil and gas industry, with a projected market value of over \$600 billion by 2033.

North Sea Region Oil & Gas Industry Product Analysis

The North Sea Region Oil & Gas Industry is characterized by a diverse product portfolio and ongoing innovation. Crude oil and natural gas remain core products, with ongoing efforts to optimize extraction and processing. Product innovations focus on enhanced oil recovery techniques, leading to higher yields from existing fields, and the development of cleaner fuels and petrochemical feedstocks. Applications span energy generation, industrial processes, and the production of essential materials. Competitive advantages stem from the region's established infrastructure, experienced workforce, and increasing adoption of digital technologies for efficiency.

Key Drivers, Barriers & Challenges in North Sea Region Oil & Gas Industry

The North Sea Region Oil & Gas Industry is propelled by several key drivers. Technological advancements in extraction and processing, particularly in areas like subsea robotics and digital reservoir management, are crucial. Economic factors, including sustained global energy demand and favorable commodity prices, also play a significant role, with the industry contributing billions to regional economies. Policy support for energy security and investment in infrastructure, such as carbon capture and storage (CCS) projects, further stimulates growth.

Conversely, the industry faces substantial barriers and challenges. Stringent environmental regulations and increasing pressure for decarbonization necessitate significant investment in cleaner technologies, representing billions in potential compliance costs. Supply chain disruptions and rising operational costs due to inflation and geopolitical instability impact project timelines and profitability. Furthermore, the competitive pressure from lower-cost production regions and the accelerating global shift towards renewable energy sources pose long-term challenges to hydrocarbon market dominance.

Growth Drivers in the North Sea Region Oil & Gas Industry Market

Key growth drivers in the North Sea Region Oil & Gas Industry include sustained global demand for energy, particularly for natural gas as a transition fuel. Technological innovation in enhanced oil recovery (EOR) and advanced drilling techniques is unlocking previously inaccessible reserves, contributing billions in potential production. Favorable fiscal regimes and government incentives in key North Sea nations, such as Norway and the UK, encourage continued investment in exploration and production. The development of offshore wind energy, often leveraging existing oil and gas infrastructure and expertise, presents a synergistic growth avenue, with billions in projected investment.

Challenges Impacting North Sea Region Oil & Gas Industry Growth

Significant challenges impacting North Sea Region Oil & Gas Industry growth include increasing regulatory complexity and evolving environmental standards, demanding substantial investments in emissions reduction technologies, potentially costing billions. Geopolitical instability and supply chain disruptions contribute to escalating operational costs and project delays. The competitive pressure from emerging energy sources and the global imperative for decarbonization necessitate a strategic shift towards lower-carbon solutions, requiring significant capital reallocation and innovation. Aging infrastructure also presents a considerable challenge, demanding substantial investments in maintenance and upgrades to ensure safe and efficient operations.

Key Players Shaping the North Sea Region Oil & Gas Industry Market

- Equinor ASA

- Total S.A.

- BP Plc

- Royal Dutch Shell Plc

- Transocean Ltd

- Baker Hughes Company

- Halliburton Company

- Seadrill Ltd

- Schlumberger Limited

- Valaris PLC

Significant North Sea Region Oil & Gas Industry Industry Milestones

- 2019: Major oil discoveries announced in the Norwegian Continental Shelf, potentially adding billions to future reserves.

- 2020: Increased investment in carbon capture and storage (CCS) projects across the region, signaling a commitment to decarbonization.

- 2021: Significant offshore wind farm development milestones achieved, integrating with existing energy infrastructure.

- 2022: Volatility in global energy prices drives increased production focus and strategic asset acquisitions.

- 2023: Advancements in digital twin technology adopted for optimizing offshore platform operations, promising billions in efficiency gains.

- 2024: Increased focus on hydrogen production from offshore natural gas and renewable sources, with pilot projects underway.

Future Outlook for North Sea Region Oil & Gas Industry Market

The future outlook for the North Sea Region Oil & Gas Industry is one of strategic transformation and sustained relevance. While facing the global energy transition, the region is poised to leverage its established infrastructure, expertise, and resource base. Growth catalysts include continued demand for natural gas as a transition fuel, significant investments in offshore carbon capture and storage (CCS), and the synergistic development of offshore renewable energy projects. Innovations in digitalization and automation will further enhance efficiency and reduce operational costs, ensuring the economic viability of existing assets. The industry's adaptability and commitment to decarbonization will be crucial in capitalizing on market potential, projected to reach over \$700 billion by 2033, and maintaining its position as a critical energy provider.

North Sea Region Oil & Gas Industry Segmentation

-

1. Sector

- 1.1. Upstream

- 1.2. Midstream

- 1.3. Downstream

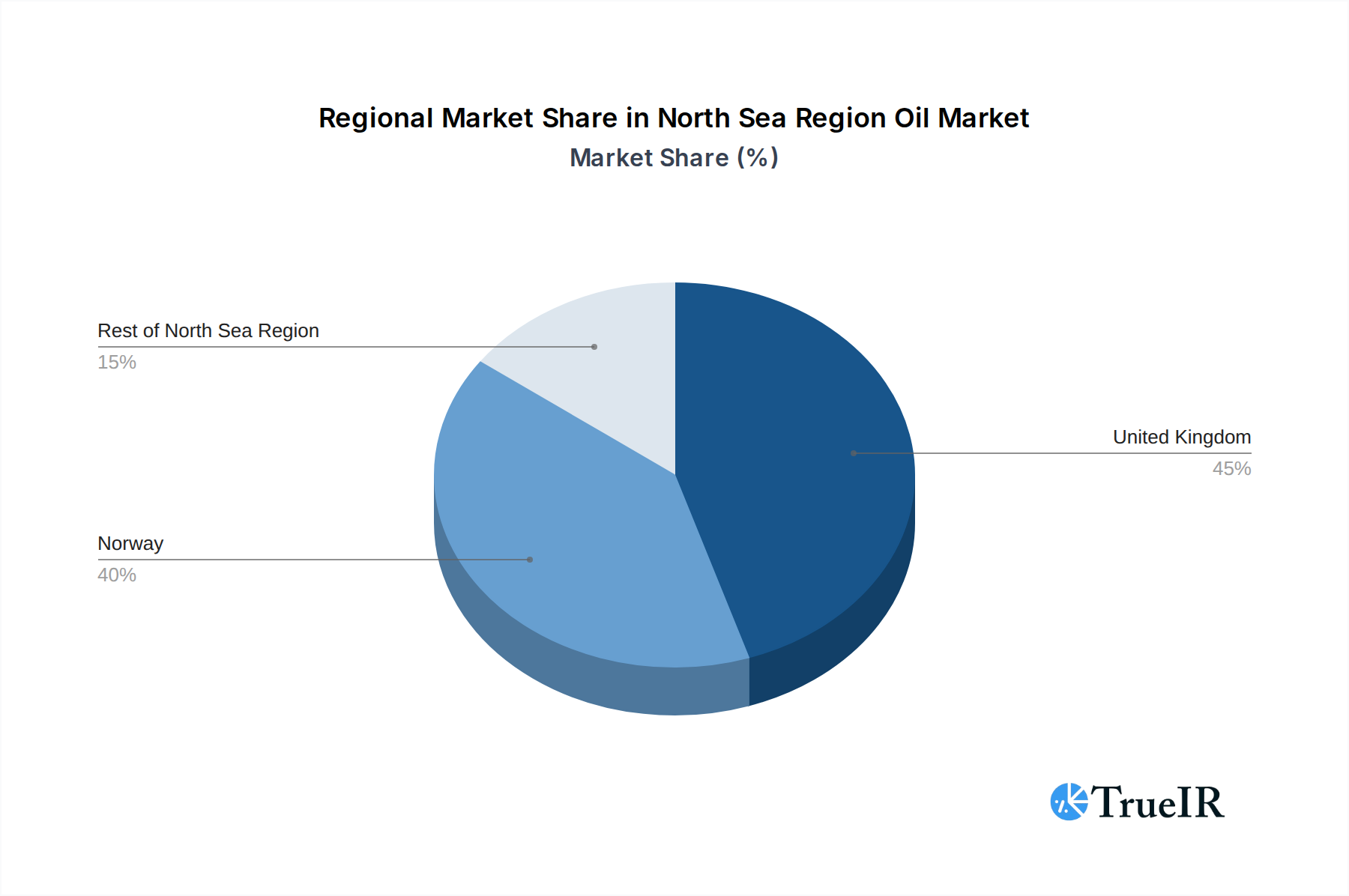

North Sea Region Oil & Gas Industry Segmentation By Geography

- 1. United Kingdom

- 2. Norway

- 3. Rest of North Sea Region

North Sea Region Oil & Gas Industry Regional Market Share

Geographic Coverage of North Sea Region Oil & Gas Industry

North Sea Region Oil & Gas Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Sector

- 5.1.1. Upstream

- 5.1.2. Midstream

- 5.1.3. Downstream

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. United Kingdom

- 5.2.2. Norway

- 5.2.3. Rest of North Sea Region

- 5.1. Market Analysis, Insights and Forecast - by Sector

- 6. Global North Sea Region Oil & Gas Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Sector

- 6.1.1. Upstream

- 6.1.2. Midstream

- 6.1.3. Downstream

- 6.1. Market Analysis, Insights and Forecast - by Sector

- 7. United Kingdom North Sea Region Oil & Gas Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Sector

- 7.1.1. Upstream

- 7.1.2. Midstream

- 7.1.3. Downstream

- 7.1. Market Analysis, Insights and Forecast - by Sector

- 8. Norway North Sea Region Oil & Gas Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Sector

- 8.1.1. Upstream

- 8.1.2. Midstream

- 8.1.3. Downstream

- 8.1. Market Analysis, Insights and Forecast - by Sector

- 9. Rest of North Sea Region North Sea Region Oil & Gas Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Sector

- 9.1.1. Upstream

- 9.1.2. Midstream

- 9.1.3. Downstream

- 9.1. Market Analysis, Insights and Forecast - by Sector

- 10. Competitive Analysis

- 10.1. Company Profiles

- 10.1.1 Equinor ASA

- 10.1.1.1. Company Overview

- 10.1.1.2. Products

- 10.1.1.3. Company Financials

- 10.1.1.4. SWOT Analysis

- 10.1.2 Total S A *List Not Exhaustive

- 10.1.2.1. Company Overview

- 10.1.2.2. Products

- 10.1.2.3. Company Financials

- 10.1.2.4. SWOT Analysis

- 10.1.3 BP Plc

- 10.1.3.1. Company Overview

- 10.1.3.2. Products

- 10.1.3.3. Company Financials

- 10.1.3.4. SWOT Analysis

- 10.1.4 Royal Dutch Shell Plc

- 10.1.4.1. Company Overview

- 10.1.4.2. Products

- 10.1.4.3. Company Financials

- 10.1.4.4. SWOT Analysis

- 10.1.5 Transocean Ltd

- 10.1.5.1. Company Overview

- 10.1.5.2. Products

- 10.1.5.3. Company Financials

- 10.1.5.4. SWOT Analysis

- 10.1.6 Baker Hughes Company

- 10.1.6.1. Company Overview

- 10.1.6.2. Products

- 10.1.6.3. Company Financials

- 10.1.6.4. SWOT Analysis

- 10.1.7 Halliburton Company

- 10.1.7.1. Company Overview

- 10.1.7.2. Products

- 10.1.7.3. Company Financials

- 10.1.7.4. SWOT Analysis

- 10.1.8 Seadrill Ltd

- 10.1.8.1. Company Overview

- 10.1.8.2. Products

- 10.1.8.3. Company Financials

- 10.1.8.4. SWOT Analysis

- 10.1.9 Schlumberger Limited

- 10.1.9.1. Company Overview

- 10.1.9.2. Products

- 10.1.9.3. Company Financials

- 10.1.9.4. SWOT Analysis

- 10.1.10 Valaris PLC

- 10.1.10.1. Company Overview

- 10.1.10.2. Products

- 10.1.10.3. Company Financials

- 10.1.10.4. SWOT Analysis

- 10.1.1 Equinor ASA

- 10.2. Market Entropy

- 10.2.1 Company's Key Areas Served

- 10.2.2 Recent Developments

- 10.3. Company Market Share Analysis 2025

- 10.3.1 Top 5 Companies Market Share Analysis

- 10.3.2 Top 3 Companies Market Share Analysis

- 10.4. List of Potential Customers

- 11. Research Methodology

List of Figures

- Figure 1: Global North Sea Region Oil & Gas Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: United Kingdom North Sea Region Oil & Gas Industry Revenue (billion), by Sector 2025 & 2033

- Figure 3: United Kingdom North Sea Region Oil & Gas Industry Revenue Share (%), by Sector 2025 & 2033

- Figure 4: United Kingdom North Sea Region Oil & Gas Industry Revenue (billion), by Country 2025 & 2033

- Figure 5: United Kingdom North Sea Region Oil & Gas Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: Norway North Sea Region Oil & Gas Industry Revenue (billion), by Sector 2025 & 2033

- Figure 7: Norway North Sea Region Oil & Gas Industry Revenue Share (%), by Sector 2025 & 2033

- Figure 8: Norway North Sea Region Oil & Gas Industry Revenue (billion), by Country 2025 & 2033

- Figure 9: Norway North Sea Region Oil & Gas Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Rest of North Sea Region North Sea Region Oil & Gas Industry Revenue (billion), by Sector 2025 & 2033

- Figure 11: Rest of North Sea Region North Sea Region Oil & Gas Industry Revenue Share (%), by Sector 2025 & 2033

- Figure 12: Rest of North Sea Region North Sea Region Oil & Gas Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Rest of North Sea Region North Sea Region Oil & Gas Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global North Sea Region Oil & Gas Industry Revenue billion Forecast, by Sector 2020 & 2033

- Table 2: Global North Sea Region Oil & Gas Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Global North Sea Region Oil & Gas Industry Revenue billion Forecast, by Sector 2020 & 2033

- Table 4: Global North Sea Region Oil & Gas Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 5: Global North Sea Region Oil & Gas Industry Revenue billion Forecast, by Sector 2020 & 2033

- Table 6: Global North Sea Region Oil & Gas Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Global North Sea Region Oil & Gas Industry Revenue billion Forecast, by Sector 2020 & 2033

- Table 8: Global North Sea Region Oil & Gas Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North Sea Region Oil & Gas Industry?

The projected CAGR is approximately 4%.

2. Which companies are prominent players in the North Sea Region Oil & Gas Industry?

Key companies in the market include Equinor ASA, Total S A *List Not Exhaustive, BP Plc, Royal Dutch Shell Plc, Transocean Ltd, Baker Hughes Company, Halliburton Company, Seadrill Ltd, Schlumberger Limited, Valaris PLC.

3. What are the main segments of the North Sea Region Oil & Gas Industry?

The market segments include Sector.

4. Can you provide details about the market size?

The market size is estimated to be USD 40 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Increased Government Regulations for Greenhouse Gas Emissions 4.; Encouraging Production and Consumption of Renewable Aviation Fuel.

6. What are the notable trends driving market growth?

Upstream Sector to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; The High Costs of Renewable Aviation Fuel.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North Sea Region Oil & Gas Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North Sea Region Oil & Gas Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North Sea Region Oil & Gas Industry?

To stay informed about further developments, trends, and reports in the North Sea Region Oil & Gas Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence