Key Insights

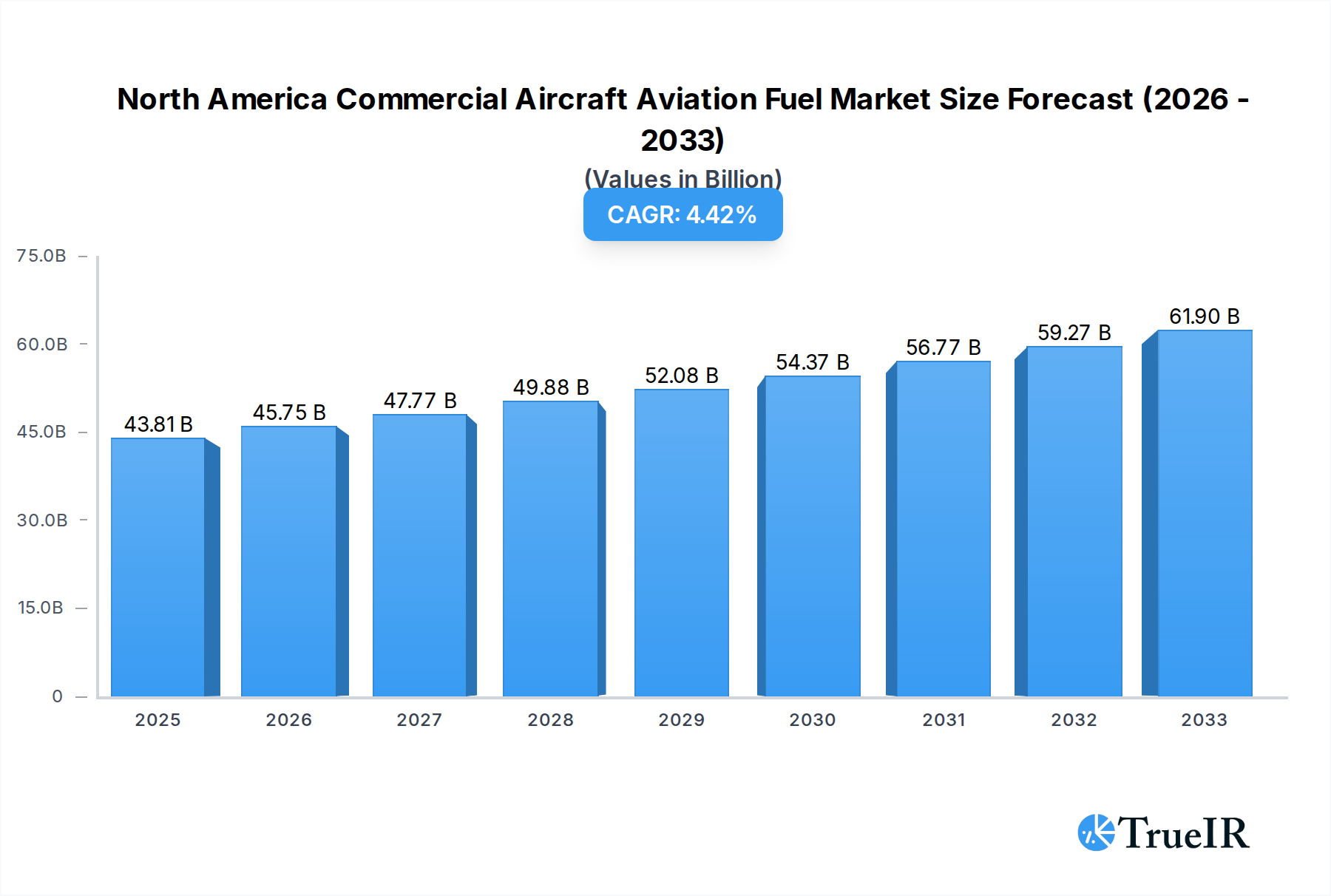

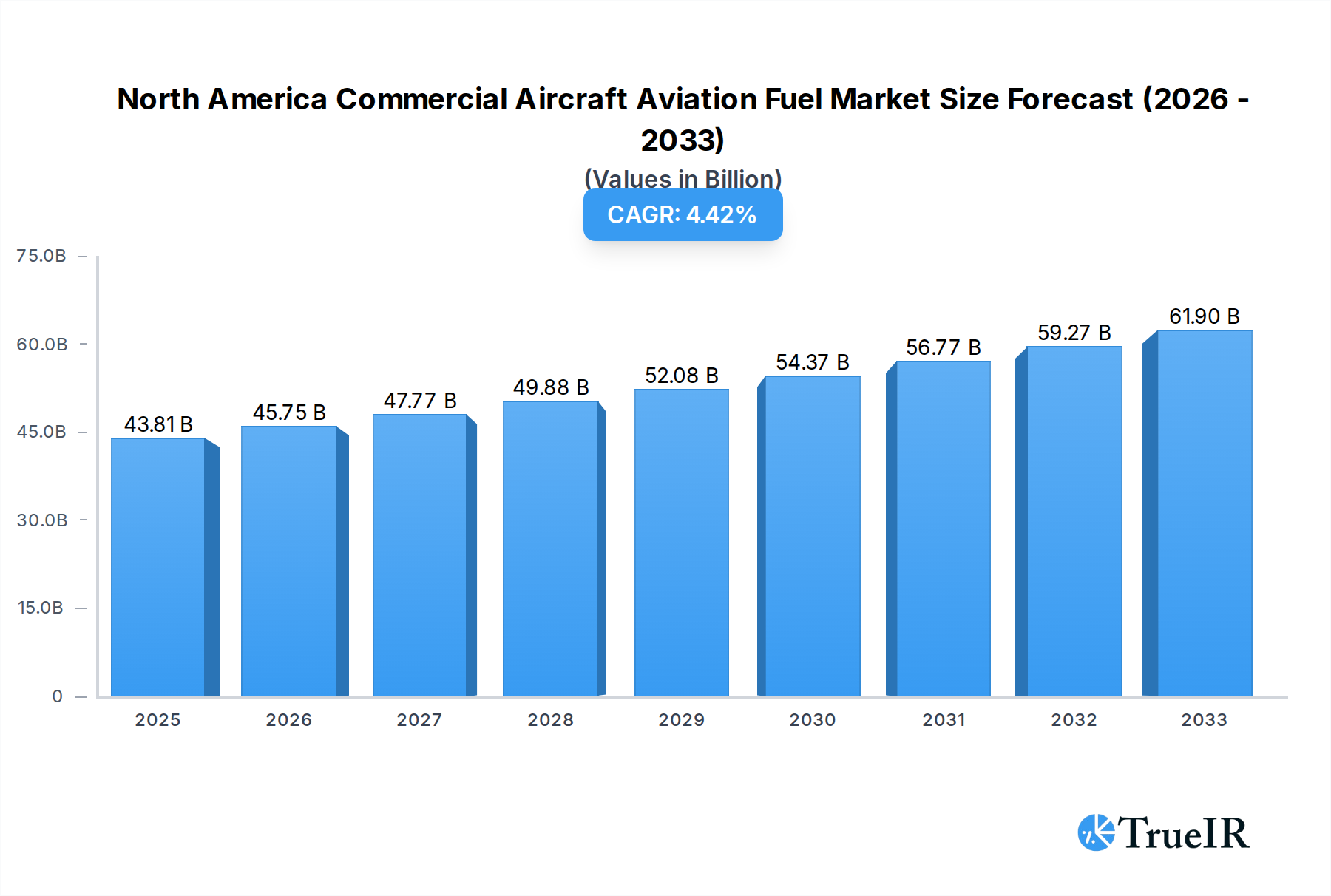

The North America Commercial Aircraft Aviation Fuel Market is poised for robust expansion, projected to reach an estimated $43.81 billion in 2025. This growth is driven by a CAGR of 4.4% over the forecast period of 2025-2033. A significant catalyst for this expansion is the increasing global demand for air travel, particularly in the commercial aviation sector, which necessitates a greater supply of aviation fuel. The recovery and subsequent surge in passenger traffic post-pandemic, coupled with the expansion of airline fleets to meet this demand, directly fuels the consumption of aviation fuel. Furthermore, technological advancements aimed at improving fuel efficiency in aircraft engines, while a long-term trend, are currently outweighed by the sheer volume of flights. The market is also seeing a gradual but significant shift towards more sustainable fuel options, with Aviation Biofuel emerging as a key growth segment, driven by environmental regulations and corporate sustainability initiatives.

North America Commercial Aircraft Aviation Fuel Market Market Size (In Billion)

The market is segmented by Fuel Type into Air Turbine Fuel (ATF), Aviation Biofuel, and Others, with ATF currently dominating due to its established infrastructure and widespread use. However, Aviation Biofuel is expected to witness the highest growth rate, reflecting a global push for decarbonization in the aviation industry. Geographically, the market is primarily concentrated within North America, comprising the United States, Canada, and the Rest of North America. The United States, as a major hub for both air travel and fuel production, holds the largest market share. Restraints for the market include the volatility of crude oil prices, which directly impact ATF costs, and the significant initial investment required for developing and scaling up sustainable aviation fuel (SAF) production. Despite these challenges, the industry's commitment to reducing its carbon footprint and the continuous innovation in fuel technology are expected to overcome these hurdles, ensuring sustained market growth.

North America Commercial Aircraft Aviation Fuel Market Company Market Share

This in-depth report delivers a dynamic and SEO-optimized analysis of the North America Commercial Aircraft Aviation Fuel Market. Focusing on high-volume keywords, we provide industry stakeholders with unparalleled insights into market structure, trends, dominant segments, and future growth trajectories. With a detailed study period from 2019 to 2033, a base year of 2025, and a forecast period extending from 2025 to 2033, this report offers critical data and strategic recommendations for navigating this evolving sector. We cover essential segments including Fuel Type (Air Turbine Fuel (ATF), Aviation Biofuel, Others) and Geography (The United States, Canada, Rest of North America), highlighting key industry developments and the competitive landscape shaped by leading global players.

North America Commercial Aircraft Aviation Fuel Market Market Structure & Competitive Landscape

The North America Commercial Aircraft Aviation Fuel Market is characterized by a moderately concentrated structure, with a few major integrated energy companies and specialized aviation fuel suppliers dominating supply chains. Innovation drivers are primarily focused on the development and scaling of Sustainable Aviation Fuels (SAF) to meet stringent environmental regulations and growing airline demand for decarbonization. Regulatory impacts are significant, with government incentives and mandates driving investment in greener aviation fuel technologies and infrastructure. Product substitutes are largely limited for conventional Air Turbine Fuel (ATF) in the short to medium term, though SAF is emerging as a direct, albeit premium, alternative. End-user segmentation is driven by airline fleet size, route networks, and sustainability commitments. Mergers and Acquisitions (M&A) trends are on the rise, particularly involving fuel producers and technology providers aiming to secure SAF production capabilities and market access. For instance, recent years have seen strategic partnerships and investments aimed at expanding SAF feedstock sourcing and refining capacity. The market concentration ratio for the top five players is estimated to be around 60-70%, indicating a substantial but not fully monopolistic landscape. The increasing focus on SAF production and distribution is fostering new entrants and joint ventures, potentially leading to a more fragmented competitive environment in the long term.

North America Commercial Aircraft Aviation Fuel Market Market Trends & Opportunities

The North America Commercial Aircraft Aviation Fuel Market is poised for significant expansion, driven by an escalating demand for air travel and an imperative shift towards sustainable aviation solutions. The market size is projected to grow from an estimated $xx billion in 2025 to $xx billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of xx%. This growth is underpinned by a confluence of technological advancements, evolving consumer preferences for eco-friendly travel, and intensified competitive dynamics. Technological shifts are prominently centered around the maturation and cost reduction of Sustainable Aviation Fuel (SAF) production technologies, including co-processing of renewable feedstocks with conventional jet fuel and dedicated SAF production pathways. Airlines are increasingly incorporating SAF into their fuel mix, driven by corporate sustainability goals and passenger awareness. Consumer preferences are evolving, with a growing willingness among travelers to support airlines with demonstrated environmental commitments. This trend is compelling fuel providers to innovate and diversify their offerings beyond traditional Jet A/A-1 fuels. Competitive dynamics are intensifying as major oil and gas companies, alongside new bio-energy ventures, vie for market share in the burgeoning SAF segment. Strategic alliances and collaborations are becoming commonplace, as companies seek to leverage each other's expertise in feedstock sourcing, refining, and distribution. The market penetration rate of SAF, while still nascent, is expected to accelerate, driven by supportive government policies and growing airline offtake agreements. Opportunities abound for companies that can offer cost-effective SAF solutions, secure sustainable feedstock supply chains, and develop innovative fuel blending and distribution infrastructure. The increasing focus on decarbonization within the aviation industry presents a substantial long-term opportunity for market growth and transformation. The projected market size for aviation biofuels is expected to reach $xx billion by 2033, signifying a substantial shift in fuel consumption patterns.

Dominant Markets & Segments in North America Commercial Aircraft Aviation Fuel Market

The United States stands as the dominant market within the North America Commercial Aircraft Aviation Fuel landscape, accounting for an estimated xx% of the total market share in 2025. This dominance is attributable to its extensive commercial aviation infrastructure, a vast network of domestic and international air routes, and proactive government policies aimed at promoting sustainable aviation fuel. Key growth drivers in the U.S. include substantial airline investments in fleet modernization and sustainability initiatives, coupled with federal and state-level incentives for SAF production and adoption. For instance, tax credits and renewable fuel standard programs are significantly encouraging the transition towards cleaner aviation fuels.

In terms of Fuel Type, Air Turbine Fuel (ATF) currently holds the largest market share, estimated at xx% in 2025. ATF, encompassing Jet A and Jet A-1, remains the primary fuel for commercial aircraft due to its established infrastructure and cost-effectiveness for a wide range of operations. However, Aviation Biofuel is the fastest-growing segment, with an anticipated CAGR of xx% during the forecast period. This rapid growth is propelled by increasing regulatory mandates, airline commitments to reduce carbon emissions, and advancements in SAF production technologies. The "Rest of North America" segment, primarily comprising Mexico, represents a developing market with growing potential, driven by expanding tourism and increasing airline capacity. Canada also plays a significant role, with a strong focus on sustainability and the development of its own SAF production capabilities.

Market dominance in the U.S. is further reinforced by the presence of major fuel suppliers and refiners who are investing heavily in SAF production and distribution networks. The infrastructure for ATF is well-established across the continent, facilitating its continued widespread use. However, the development of new infrastructure for SAF blending and distribution presents a significant opportunity for growth and market expansion. The transition towards SAF is not only a regulatory imperative but also a strategic move by airlines to enhance their brand reputation and attract environmentally conscious travelers. This dynamic underscores the multifaceted drivers shaping the North America Commercial Aircraft Aviation Fuel Market, with sustainability emerging as a paramount consideration.

North America Commercial Aircraft Aviation Fuel Market Product Analysis

The North America Commercial Aircraft Aviation Fuel Market is defined by continuous product innovation, primarily centered around enhancing sustainability and efficiency. Air Turbine Fuel (ATF), comprising Jet A and Jet A-1, remains the industry standard, offering reliable performance and a well-established supply chain. However, the transformative innovation lies in Aviation Biofuel, commonly known as Sustainable Aviation Fuel (SAF). SAF is produced from a variety of renewable feedstocks, including used cooking oil, agricultural waste, and forestry residues, offering a significant reduction in lifecycle greenhouse gas emissions compared to conventional jet fuel. Key competitive advantages of SAF include its "drop-in" capability, meaning it can be used in existing aircraft engines without modification, and its potential to meet stringent environmental regulations and corporate sustainability targets. The technological advancements in SAF production are focused on optimizing conversion processes, improving feedstock availability, and reducing production costs to achieve price parity with conventional fuels.

Key Drivers, Barriers & Challenges in North America Commercial Aircraft Aviation Fuel Market

Key Drivers:

- Environmental Regulations and Sustainability Mandates: Growing pressure from governments and international bodies to reduce aviation's carbon footprint is a primary catalyst. Policies like blended wing body mandates and carbon pricing mechanisms are incentivizing the adoption of cleaner fuels.

- Airline Sustainability Commitments: Major airlines are setting ambitious decarbonization targets, driving demand for Sustainable Aviation Fuel (SAF). This is exemplified by numerous offtake agreements for SAF.

- Technological Advancements in SAF Production: Continuous innovation in SAF production pathways, including advanced biofuels and synthetic fuels, is improving efficiency and reducing costs, making SAF more commercially viable.

- Growing Air Travel Demand: The post-pandemic recovery and projected long-term growth in air passenger numbers directly translate to increased demand for aviation fuel.

Barriers & Challenges:

- High Cost of Sustainable Aviation Fuel (SAF): Currently, SAF is significantly more expensive than conventional jet fuel, posing a major barrier to widespread adoption. The estimated cost premium can range from 50% to over 200%.

- Limited SAF Production Capacity and Feedstock Availability: The global production capacity for SAF is still nascent and insufficient to meet projected demand. Securing a consistent and sustainable supply of diverse feedstocks remains a significant challenge.

- Infrastructure Development for SAF Distribution: The existing infrastructure for fuel distribution is optimized for conventional jet fuel. Developing and investing in new infrastructure for SAF blending, storage, and delivery requires substantial capital.

- Regulatory Uncertainty and Policy Fragmentation: Inconsistent or evolving government policies across different regions can create uncertainty for investors and hinder long-term planning for SAF production and uptake. For example, varying tax credit structures can impact investment decisions.

Growth Drivers in the North America Commercial Aircraft Aviation Fuel Market Market

The North America Commercial Aircraft Aviation Fuel Market is propelled by a trifecta of technological, economic, and regulatory factors. Technologically, the maturation of various Sustainable Aviation Fuel (SAF) production pathways, such as HEFA (Hydroprocessed Esters and Fatty Acids) and Fischer-Tropsch, is crucial. Economically, the increasing investor confidence and substantial capital inflows into renewable energy sectors are facilitating investment in SAF production facilities and feedstock supply chains. Regulatory drivers are paramount, with the U.S. government's strategic plan for increasing SAF production and use, as well as initiatives like those from CEPSASigned, directly stimulating market growth.

Challenges Impacting North America Commercial Aircraft Aviation Fuel Market Growth

Challenges impacting North America Commercial Aircraft Aviation Fuel Market growth are primarily centered around the economic viability and scalability of sustainable alternatives. The high production cost of Sustainable Aviation Fuel (SAF) remains a significant barrier, often necessitating premium pricing that impacts airline operating budgets. Supply chain complexities for SAF, including the secure and consistent sourcing of diverse, sustainable feedstocks, present ongoing hurdles. Furthermore, the extensive infrastructure upgrades required to support widespread SAF distribution, from blending facilities to airport refueling systems, demand considerable investment. Competitive pressures from established conventional fuel suppliers and the need for robust, long-term policy support continue to shape the market's trajectory.

Key Players Shaping the North America Commercial Aircraft Aviation Fuel Market Market

- Targray Technology International Inc

- Valero Energy Corporation

- Irving Oil Ltd

- Shell Plc

- Phillips 66

- Chevron Corporation

- World Fuel Services Corp

- TotalEnergies SE

- Mercury Air Group Inc

- Vitol Holding BV

Significant North America Commercial Aircraft Aviation Fuel Market Industry Milestones

- January 2022: CEPSASigned an agreement with Iberia and Iberia Express for the development and large-scale production of sustainable aviation fuel, contemplating SAF production from waste, recycled oils, and second-generation plant-based bio feedstock. This signifies a crucial step towards commercializing SAF from diverse waste streams.

- September 2022: The U.S. Energy Department issued a plan detailing a government-wide strategy for ramping up the production and use of sustainable aviation fuels (SAF). This strategic directive aims to accelerate the transition to lower-carbon aviation fuels within the United States.

Future Outlook for North America Commercial Aircraft Aviation Fuel Market Market

The future outlook for the North America Commercial Aircraft Aviation Fuel Market is exceptionally positive, driven by an unwavering commitment to decarbonization within the aviation sector. Strategic opportunities lie in the continued scaling of Sustainable Aviation Fuel (SAF) production, driven by technological advancements and supportive government policies. The market potential for SAF is immense, with projections indicating it will capture a significant share of the aviation fuel market within the next decade. Investments in innovative SAF technologies, feedstock diversification, and robust distribution networks will be critical for sustained growth. The convergence of regulatory mandates, corporate sustainability goals, and increasing consumer demand for eco-friendly travel positions the North America Commercial Aircraft Aviation Fuel Market for substantial expansion and transformation.

North America Commercial Aircraft Aviation Fuel Market Segmentation

-

1. Fuel Type

- 1.1. Air Turbine Fuel (ATF)

- 1.2. Aviation Biofuel

- 1.3. Others

-

2. Geography

- 2.1. The United States

- 2.2. Canada

- 2.3. Rest of North America

North America Commercial Aircraft Aviation Fuel Market Segmentation By Geography

- 1. The United States

- 2. Canada

- 3. Rest of North America

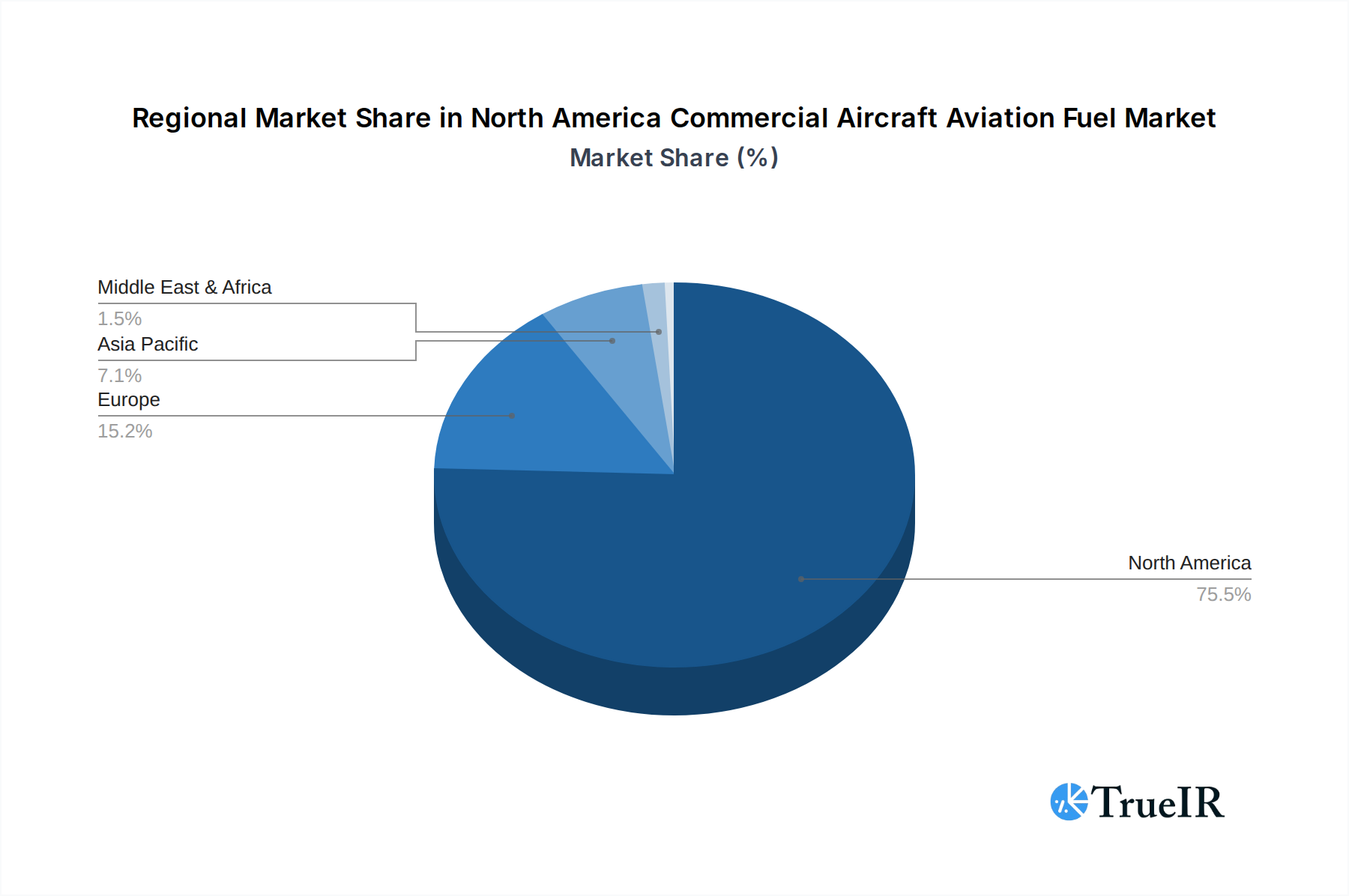

North America Commercial Aircraft Aviation Fuel Market Regional Market Share

Geographic Coverage of North America Commercial Aircraft Aviation Fuel Market

North America Commercial Aircraft Aviation Fuel Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Fuel Type

- 5.1.1. Air Turbine Fuel (ATF)

- 5.1.2. Aviation Biofuel

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Geography

- 5.2.1. The United States

- 5.2.2. Canada

- 5.2.3. Rest of North America

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. The United States

- 5.3.2. Canada

- 5.3.3. Rest of North America

- 5.1. Market Analysis, Insights and Forecast - by Fuel Type

- 6. North America Commercial Aircraft Aviation Fuel Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Fuel Type

- 6.1.1. Air Turbine Fuel (ATF)

- 6.1.2. Aviation Biofuel

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Geography

- 6.2.1. The United States

- 6.2.2. Canada

- 6.2.3. Rest of North America

- 6.1. Market Analysis, Insights and Forecast - by Fuel Type

- 7. The United States North America Commercial Aircraft Aviation Fuel Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Fuel Type

- 7.1.1. Air Turbine Fuel (ATF)

- 7.1.2. Aviation Biofuel

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Geography

- 7.2.1. The United States

- 7.2.2. Canada

- 7.2.3. Rest of North America

- 7.1. Market Analysis, Insights and Forecast - by Fuel Type

- 8. Canada North America Commercial Aircraft Aviation Fuel Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Fuel Type

- 8.1.1. Air Turbine Fuel (ATF)

- 8.1.2. Aviation Biofuel

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Geography

- 8.2.1. The United States

- 8.2.2. Canada

- 8.2.3. Rest of North America

- 8.1. Market Analysis, Insights and Forecast - by Fuel Type

- 9. Rest of North America North America Commercial Aircraft Aviation Fuel Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Fuel Type

- 9.1.1. Air Turbine Fuel (ATF)

- 9.1.2. Aviation Biofuel

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Geography

- 9.2.1. The United States

- 9.2.2. Canada

- 9.2.3. Rest of North America

- 9.1. Market Analysis, Insights and Forecast - by Fuel Type

- 10. Competitive Analysis

- 10.1. Company Profiles

- 10.1.1 Targray Technology International Inc

- 10.1.1.1. Company Overview

- 10.1.1.2. Products

- 10.1.1.3. Company Financials

- 10.1.1.4. SWOT Analysis

- 10.1.2 Valero Energy Corporation

- 10.1.2.1. Company Overview

- 10.1.2.2. Products

- 10.1.2.3. Company Financials

- 10.1.2.4. SWOT Analysis

- 10.1.3 Irving Oil Ltd

- 10.1.3.1. Company Overview

- 10.1.3.2. Products

- 10.1.3.3. Company Financials

- 10.1.3.4. SWOT Analysis

- 10.1.4 Shell Plc

- 10.1.4.1. Company Overview

- 10.1.4.2. Products

- 10.1.4.3. Company Financials

- 10.1.4.4. SWOT Analysis

- 10.1.5 Phillips 66

- 10.1.5.1. Company Overview

- 10.1.5.2. Products

- 10.1.5.3. Company Financials

- 10.1.5.4. SWOT Analysis

- 10.1.6 Chevron Corporation

- 10.1.6.1. Company Overview

- 10.1.6.2. Products

- 10.1.6.3. Company Financials

- 10.1.6.4. SWOT Analysis

- 10.1.7 World Fuel Services Corp

- 10.1.7.1. Company Overview

- 10.1.7.2. Products

- 10.1.7.3. Company Financials

- 10.1.7.4. SWOT Analysis

- 10.1.8 TotalEnergies SE

- 10.1.8.1. Company Overview

- 10.1.8.2. Products

- 10.1.8.3. Company Financials

- 10.1.8.4. SWOT Analysis

- 10.1.9 Mercury Air Group Inc

- 10.1.9.1. Company Overview

- 10.1.9.2. Products

- 10.1.9.3. Company Financials

- 10.1.9.4. SWOT Analysis

- 10.1.10 Vitol Holding BV

- 10.1.10.1. Company Overview

- 10.1.10.2. Products

- 10.1.10.3. Company Financials

- 10.1.10.4. SWOT Analysis

- 10.1.1 Targray Technology International Inc

- 10.2. Market Entropy

- 10.2.1 Company's Key Areas Served

- 10.2.2 Recent Developments

- 10.3. Company Market Share Analysis 2025

- 10.3.1 Top 5 Companies Market Share Analysis

- 10.3.2 Top 3 Companies Market Share Analysis

- 10.4. List of Potential Customers

- 11. Research Methodology

List of Figures

- Figure 1: North America Commercial Aircraft Aviation Fuel Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: North America Commercial Aircraft Aviation Fuel Market Share (%) by Company 2025

List of Tables

- Table 1: North America Commercial Aircraft Aviation Fuel Market Revenue billion Forecast, by Fuel Type 2020 & 2033

- Table 2: North America Commercial Aircraft Aviation Fuel Market Volume K Liters Forecast, by Fuel Type 2020 & 2033

- Table 3: North America Commercial Aircraft Aviation Fuel Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 4: North America Commercial Aircraft Aviation Fuel Market Volume K Liters Forecast, by Geography 2020 & 2033

- Table 5: North America Commercial Aircraft Aviation Fuel Market Revenue billion Forecast, by Region 2020 & 2033

- Table 6: North America Commercial Aircraft Aviation Fuel Market Volume K Liters Forecast, by Region 2020 & 2033

- Table 7: North America Commercial Aircraft Aviation Fuel Market Revenue billion Forecast, by Fuel Type 2020 & 2033

- Table 8: North America Commercial Aircraft Aviation Fuel Market Volume K Liters Forecast, by Fuel Type 2020 & 2033

- Table 9: North America Commercial Aircraft Aviation Fuel Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 10: North America Commercial Aircraft Aviation Fuel Market Volume K Liters Forecast, by Geography 2020 & 2033

- Table 11: North America Commercial Aircraft Aviation Fuel Market Revenue billion Forecast, by Country 2020 & 2033

- Table 12: North America Commercial Aircraft Aviation Fuel Market Volume K Liters Forecast, by Country 2020 & 2033

- Table 13: North America Commercial Aircraft Aviation Fuel Market Revenue billion Forecast, by Fuel Type 2020 & 2033

- Table 14: North America Commercial Aircraft Aviation Fuel Market Volume K Liters Forecast, by Fuel Type 2020 & 2033

- Table 15: North America Commercial Aircraft Aviation Fuel Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 16: North America Commercial Aircraft Aviation Fuel Market Volume K Liters Forecast, by Geography 2020 & 2033

- Table 17: North America Commercial Aircraft Aviation Fuel Market Revenue billion Forecast, by Country 2020 & 2033

- Table 18: North America Commercial Aircraft Aviation Fuel Market Volume K Liters Forecast, by Country 2020 & 2033

- Table 19: North America Commercial Aircraft Aviation Fuel Market Revenue billion Forecast, by Fuel Type 2020 & 2033

- Table 20: North America Commercial Aircraft Aviation Fuel Market Volume K Liters Forecast, by Fuel Type 2020 & 2033

- Table 21: North America Commercial Aircraft Aviation Fuel Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 22: North America Commercial Aircraft Aviation Fuel Market Volume K Liters Forecast, by Geography 2020 & 2033

- Table 23: North America Commercial Aircraft Aviation Fuel Market Revenue billion Forecast, by Country 2020 & 2033

- Table 24: North America Commercial Aircraft Aviation Fuel Market Volume K Liters Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Commercial Aircraft Aviation Fuel Market?

The projected CAGR is approximately 4.4%.

2. Which companies are prominent players in the North America Commercial Aircraft Aviation Fuel Market?

Key companies in the market include Targray Technology International Inc, Valero Energy Corporation, Irving Oil Ltd, Shell Plc, Phillips 66, Chevron Corporation, World Fuel Services Corp, TotalEnergies SE, Mercury Air Group Inc, Vitol Holding BV.

3. What are the main segments of the North America Commercial Aircraft Aviation Fuel Market?

The market segments include Fuel Type, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 43.81 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Investments in Offshore Wind Power Projects4.; Supportive Government Policies.

6. What are the notable trends driving market growth?

Air Turbine Fuel (ATF) Segment is Expected to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Increasing Adopting of Alternative Clean Energy Sources (Ex: Solar. Hydro).

8. Can you provide examples of recent developments in the market?

January 2022: Cepsasigned an agreement with Iberia and Iberia Express for the development and large-scale production of sustainable aviation fuel. The agreement contemplates SAF production from waste, recycled oils, and second-generation plant-based bio feedstock.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Liters.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Commercial Aircraft Aviation Fuel Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Commercial Aircraft Aviation Fuel Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Commercial Aircraft Aviation Fuel Market?

To stay informed about further developments, trends, and reports in the North America Commercial Aircraft Aviation Fuel Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence