Key Insights

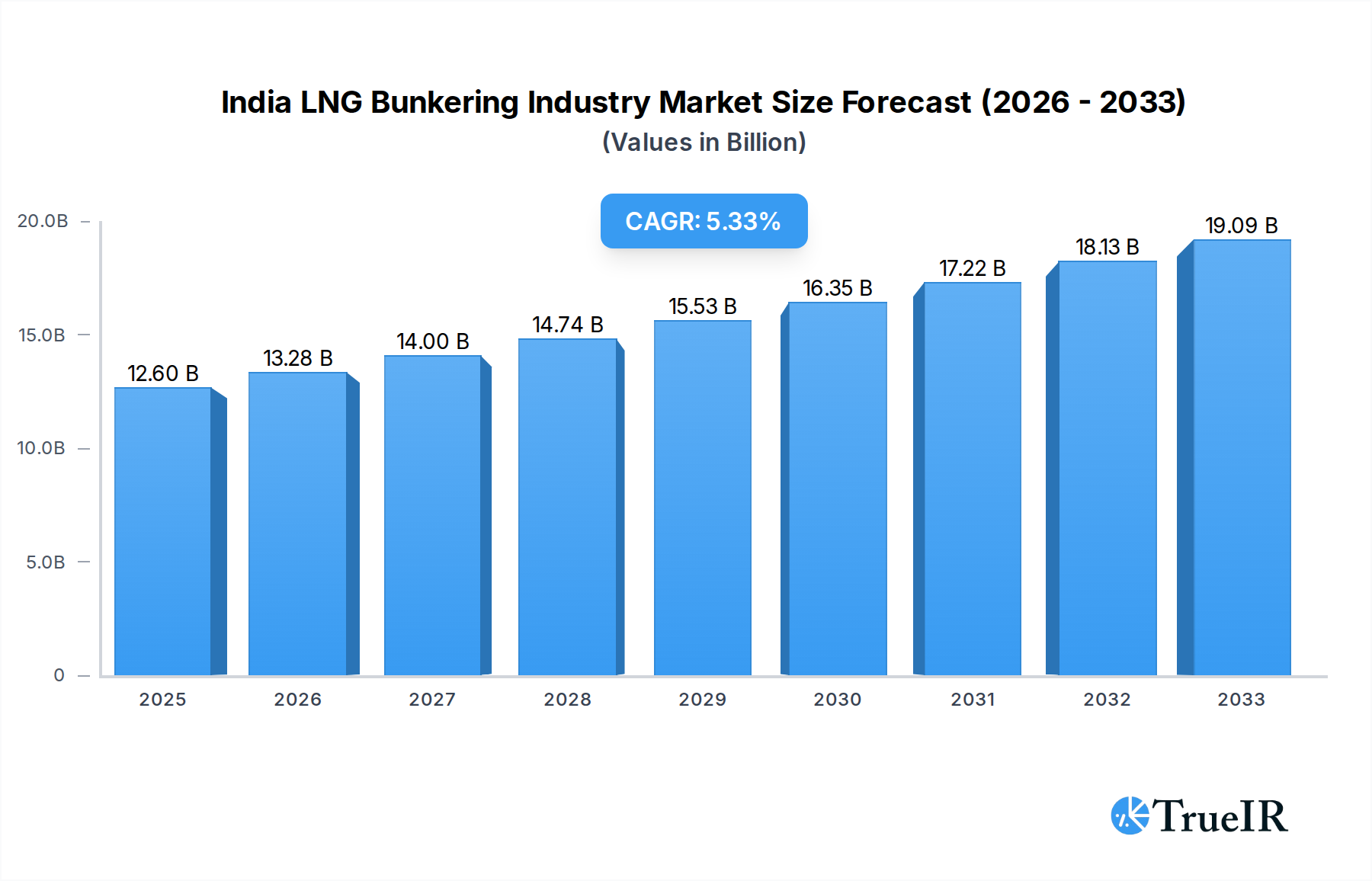

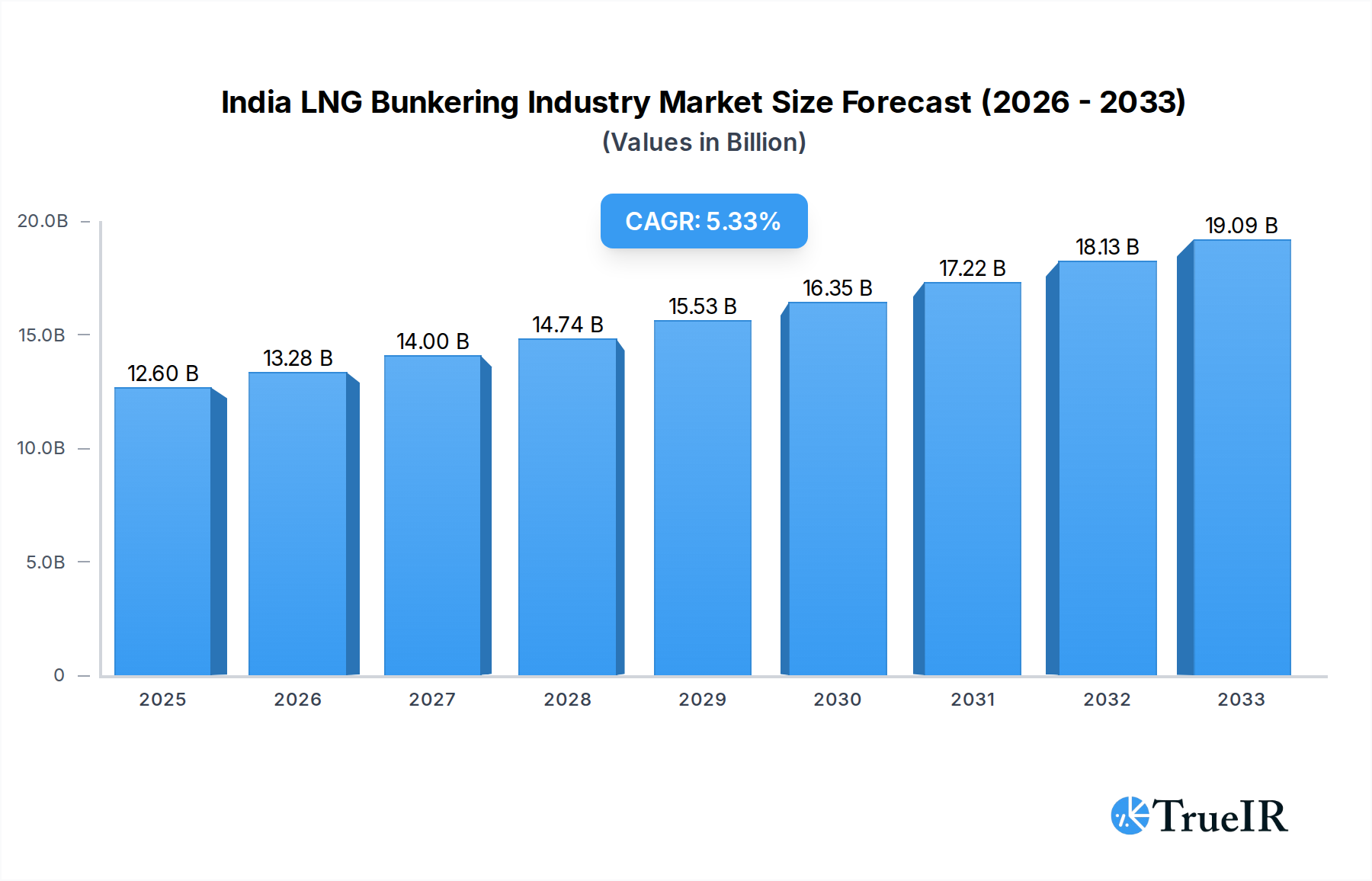

The Indian LNG bunkering industry is poised for substantial expansion, projected to reach USD 12.6 billion by 2025. This growth is fueled by a compelling Compound Annual Growth Rate (CAGR) of 5.3% anticipated over the forecast period of 2025-2033. The primary drivers behind this surge include the increasing adoption of Liquefied Natural Gas (LNG) as a cleaner and more cost-effective fuel for maritime vessels, driven by stringent environmental regulations and the push towards decarbonization within the shipping sector. India's strategic location and its expanding port infrastructure further contribute to this upward trajectory. The demand is particularly strong from the Tanker Fleet segment, which is increasingly opting for LNG to comply with international emissions standards and reduce operational expenses. The Container Fleet and Bulk and General Cargo Fleet segments are also showing significant interest in transitioning to LNG.

India LNG Bunkering Industry Market Size (In Billion)

The market will witness continued growth and innovation in the coming years. Key trends include the development of dedicated LNG bunkering infrastructure at major Indian ports, advancements in LNG-powered vessel technology, and the emergence of strategic partnerships between fuel suppliers and shipping companies. While the market is robust, potential restraints such as the initial high cost of LNG-powered vessels and the need for a comprehensive bunkering network could pose challenges. However, the long-term economic and environmental benefits associated with LNG are expected to outweigh these concerns. Companies like Indian Oil Corporation Ltd, Bharat Petroleum Corp Ltd, Adani Enterprises Ltd, Petronet LNG Ltd, and H-Energy Private Limited are actively investing and expanding their capabilities to capitalize on this burgeoning market, anticipating sustained demand across all major fleet segments.

India LNG Bunkering Industry Company Market Share

This comprehensive report provides an in-depth analysis of the burgeoning India LNG Bunkering Industry, encompassing market structure, competitive landscape, dynamic trends, and future outlook. Leveraging high-volume keywords such as "India LNG bunkering," "LNG for ships," "maritime fuel," "LNG infrastructure India," and "green shipping India," this report is optimized for search engines and tailored to engage industry professionals, investors, and policymakers. The study spans the Historical Period (2019–2024), Base Year (2025), Estimated Year (2025), and Forecast Period (2025–2033), offering a robust understanding of the market's evolution and projected trajectory.

India LNG Bunkering Industry Market Structure & Competitive Landscape

The India LNG Bunkering Industry is characterized by a dynamic and evolving market structure. While currently exhibiting moderate market concentration, the presence of major players like Indian Oil Corporation Ltd, Bharat Petroleum Corp Ltd, Adani Enterprises Ltd, Petronet LNG Ltd, and H-Energy Private Limited indicates a growing competitive intensity. Innovation drivers are primarily fueled by the global push for decarbonization in shipping and stringent environmental regulations, pushing for cleaner fuel alternatives. Regulatory impacts are significant, with government policies and initiatives actively shaping the adoption of LNG as a marine fuel. Product substitutes, such as conventional marine fuels (HFO, MGO), still hold a substantial share, but LNG's environmental advantages are increasingly recognized.

The end-user segmentation is diverse, with the Tanker Fleet, Container Fleet, and Bulk and General Cargo Fleet representing the most significant segments due to their extensive operational scope and fuel consumption. Ferries and OSV (Offshore Support Vessels) are emerging as key growth areas. Mergers and acquisitions (M&A) trends are anticipated to gain momentum as companies seek to secure market share, expand infrastructure, and leverage technological advancements. Currently, M&A volumes are estimated to be in the range of $1 billion to $5 billion, with projected increases as the market matures and consolidation opportunities arise. The industry is poised for substantial growth, driven by strategic investments and partnerships.

India LNG Bunkering Industry Market Trends & Opportunities

The India LNG Bunkering Industry is on an exponential growth trajectory, with a projected market size expected to reach hundreds of billions by the end of the forecast period. The Compound Annual Growth Rate (CAGR) is anticipated to be robust, exceeding 15% over the next decade. This rapid expansion is driven by a confluence of factors, including increasing environmental consciousness among shipping operators, stricter international and domestic regulations on sulfur and nitrogen oxide emissions, and the inherent cost-effectiveness of LNG as a fuel over the long term. Technological shifts are paramount, with advancements in liquefaction, transportation, and bunkering infrastructure playing a crucial role in facilitating wider adoption. The development of onshore and offshore LNG bunkering terminals at key Indian ports is a significant trend, enabling seamless refueling for vessels.

Consumer preferences are increasingly leaning towards sustainable and compliant fuel options. Shipping companies are actively seeking to reduce their carbon footprint and comply with International Maritime Organization (IMO) regulations, making LNG an attractive alternative. The competitive dynamics are intensifying, with both established oil and gas majors and new entrants vying for market share. Strategic partnerships and collaborations between fuel suppliers, port authorities, and shipping lines are becoming common, aiming to build a robust and efficient LNG bunkering ecosystem. Market penetration rates for LNG in the Indian maritime sector, currently estimated to be in the single digits, are projected to rise significantly, potentially reaching 20% to 30% of the total marine fuel market by 2033. Opportunities abound in developing innovative bunkering solutions, expanding the LNG supply chain, and supporting the retrofitting of vessels to dual-fuel capabilities. The significant market size and growth potential present a compelling case for investment and development within the India LNG bunkering sector.

Dominant Markets & Segments in India LNG Bunkering Industry

Within the India LNG Bunkering Industry, the Tanker Fleet segment is currently the dominant market, driven by the high fuel consumption of large vessels engaged in global and coastal trade. These tankers, responsible for transporting crude oil, refined petroleum products, and chemicals, represent a substantial portion of the demand for marine fuels. The operational patterns of these fleets, with frequent and substantial refueling needs, make them prime candidates for LNG bunkering solutions. Key growth drivers for this segment include the increasing global demand for oil and gas, necessitating more extensive tanker operations, and the growing pressure on shipping companies to adopt cleaner fuels to meet environmental standards.

The Container Fleet is emerging as a significant and rapidly growing segment. As global trade continues its upward trend, container shipping volumes are soaring, leading to a corresponding increase in fuel demand. Many major container shipping lines have already committed to incorporating LNG-powered vessels into their fleets, recognizing the long-term benefits of reduced emissions and potential cost savings. Policies aimed at promoting green shipping corridors and penalizing high-emission fuels are further accelerating this shift. The Bulk and General Cargo Fleet also presents a substantial opportunity, although adoption may be slower compared to tankers and container ships due to their diverse operational profiles and trading routes.

Ferries and OSV (Offshore Support Vessels) represent a crucial, albeit smaller, segment that is experiencing rapid growth. Many ferry operators, particularly those on fixed routes with predictable refueling schedules, are actively transitioning to LNG. Similarly, the offshore oil and gas industry's increasing focus on environmental responsibility is driving the adoption of LNG-powered OSVs. The development of dedicated LNG bunkering infrastructure at major ports, supported by government initiatives and private investments, is a critical enabler for all these segments. The projected market size for LNG bunkering in India is expected to exceed $50 billion by 2033, with the tanker and container fleets accounting for a significant majority of this value.

India LNG Bunkering Industry Product Analysis

The India LNG Bunkering Industry is witnessing significant product innovations centered around the safe, efficient, and cost-effective delivery of Liquefied Natural Gas (LNG) as a marine fuel. Key advancements include the development of smaller-scale, modular liquefaction plants and the design of specialized LNG bunker vessels, enhancing supply chain flexibility. Applications are primarily focused on powering a diverse range of maritime vessels, from large container ships and tankers to ferries and offshore support vessels. Competitive advantages of LNG as a marine fuel include its significantly lower sulfur and nitrogen oxide emissions compared to traditional heavy fuel oil, contributing to cleaner air and compliance with stringent environmental regulations. The inherent energy density of LNG also offers potential operational efficiencies.

Key Drivers, Barriers & Challenges in India LNG Bunkering Industry

Key Drivers propelling the India LNG Bunkering Industry include the global imperative to decarbonize shipping, driven by IMO regulations mandating reductions in greenhouse gas emissions. Technological advancements in liquefaction, transportation, and bunkering infrastructure are making LNG a more viable and accessible fuel. Government support through policy incentives, port development, and infrastructure investment is a significant catalyst. The inherent cost competitiveness of LNG over the long term, especially with the volatility of traditional fuel prices, is also a major driver.

Key Barriers & Challenges impacting the India LNG Bunkering Industry include the substantial upfront investment required for LNG bunkering infrastructure, which can be a significant hurdle for market entry. The limited global LNG bunkering network, though expanding, still presents logistical challenges for vessels on international voyages. Regulatory complexities and the need for standardized safety protocols for LNG handling and storage require continuous attention. Supply chain reliability and the availability of LNG at various ports are crucial concerns. Furthermore, the competitive pressure from other alternative fuels and the time lag in vessel retrofitting or new-build orders present ongoing challenges. The overall investment in new LNG bunkering infrastructure is estimated to be in the range of $5 billion to $10 billion over the forecast period.

Growth Drivers in the India LNG Bunkering Industry Market

Several key growth drivers are propelling the India LNG Bunkering Industry Market. Technologically, advancements in small-scale LNG liquefaction and regasification technologies are making LNG more accessible for bunkering operations. Economically, the price volatility of traditional marine fuels and the long-term cost advantage of LNG are significant attractions for shipping companies. Policy-driven factors are paramount, with the Indian government's commitment to cleaner energy and its vision for a blue economy actively supporting the development of LNG bunkering infrastructure and the adoption of cleaner fuels. Initiatives like the Sagarmala Programme are instrumental in facilitating port modernization and the establishment of LNG bunkering facilities. The increasing demand for environmentally friendly shipping solutions and the global push towards decarbonization are fundamental growth catalysts.

Challenges Impacting India LNG Bunkering Industry Growth

The India LNG Bunkering Industry faces several critical challenges that impact its growth trajectory. Regulatory complexities and the need for harmonized international standards for LNG bunkering can slow down adoption and create uncertainty. Supply chain fragmentation and the availability of LNG at various ports remain a concern, necessitating significant investment in infrastructure development and logistics. High capital expenditure for setting up LNG bunkering facilities presents a substantial barrier to entry for many players. Competitive pressures from other alternative fuels, such as methanol and ammonia, also pose a challenge. Furthermore, the time required for vessel retrofitting or the construction of new LNG-powered vessels creates a lag in market uptake. The estimated cost for developing adequate bunkering infrastructure across key Indian ports is in the range of $7 billion to $12 billion.

Key Players Shaping the India LNG Bunkering Industry Market

The following key players are instrumental in shaping the India LNG Bunkering Industry Market:

- Indian Oil Corporation Ltd

- Bharat Petroleum Corp Ltd

- Adani Enterprises Ltd

- Petronet LNG Ltd

- H-Energy Private Limited

Significant India LNG Bunkering Industry Industry Milestones

- 2019: Launch of pilot LNG bunkering projects at select Indian ports.

- 2020: Signing of MoUs between government entities and private players to promote LNG as a marine fuel.

- 2021: Commissioning of initial LNG bunkering facilities at major ports.

- 2022: Increased focus on developing LNG supply chain infrastructure and strategic partnerships.

- 2023: Government announces initiatives to promote LNG adoption in the maritime sector, with an estimated market size of $5 billion.

- 2024: Several shipping companies announce plans for LNG-powered new-builds and retrofits, projecting a market value of $8 billion.

Future Outlook for India LNG Bunkering Industry Market

The future outlook for the India LNG Bunkering Industry is exceptionally promising, driven by a confluence of global environmental mandates and India's strategic focus on sustainable energy solutions. The market is projected to witness exponential growth, with an estimated market size of $70 billion by 2033. Key growth catalysts include the increasing adoption of dual-fuel vessels, the expansion of LNG bunkering infrastructure at all major Indian ports, and the potential for India to become a regional hub for LNG bunkering. Strategic opportunities lie in developing innovative refueling solutions, fostering greater collaboration across the value chain, and leveraging technological advancements to enhance efficiency and safety. The ongoing commitment to decarbonization and the pursuit of cleaner shipping practices will continue to be the primary drivers shaping the industry's trajectory.

India LNG Bunkering Industry Segmentation

-

1. End-User

- 1.1. Tanker Fleet

- 1.2. Container Fleet

- 1.3. Bulk and General Cargo Fleet

- 1.4. Ferries and OSV

- 1.5. Others

India LNG Bunkering Industry Segmentation By Geography

- 1. India

India LNG Bunkering Industry Regional Market Share

Geographic Coverage of India LNG Bunkering Industry

India LNG Bunkering Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by End-User

- 5.1.1. Tanker Fleet

- 5.1.2. Container Fleet

- 5.1.3. Bulk and General Cargo Fleet

- 5.1.4. Ferries and OSV

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. India

- 5.1. Market Analysis, Insights and Forecast - by End-User

- 6. India LNG Bunkering Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by End-User

- 6.1.1. Tanker Fleet

- 6.1.2. Container Fleet

- 6.1.3. Bulk and General Cargo Fleet

- 6.1.4. Ferries and OSV

- 6.1.5. Others

- 6.1. Market Analysis, Insights and Forecast - by End-User

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Indian Oil Corporation Ltd

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Bharat Petroleum Corp Ltd

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Adani Enterprises Ltd

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Petronet LNG Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 H-Energy Private Limited

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.1 Indian Oil Corporation Ltd

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: India LNG Bunkering Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: India LNG Bunkering Industry Share (%) by Company 2025

List of Tables

- Table 1: India LNG Bunkering Industry Revenue billion Forecast, by End-User 2020 & 2033

- Table 2: India LNG Bunkering Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 3: India LNG Bunkering Industry Revenue billion Forecast, by End-User 2020 & 2033

- Table 4: India LNG Bunkering Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the India LNG Bunkering Industry?

The projected CAGR is approximately 5.3%.

2. Which companies are prominent players in the India LNG Bunkering Industry?

Key companies in the market include Indian Oil Corporation Ltd, Bharat Petroleum Corp Ltd, Adani Enterprises Ltd, Petronet LNG Ltd, H-Energy Private Limited.

3. What are the main segments of the India LNG Bunkering Industry?

The market segments include End-User.

4. Can you provide details about the market size?

The market size is estimated to be USD 12.6 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Gas Production and Infrastructure4.; Increasing Exploration and Production Activities.

6. What are the notable trends driving market growth?

Ferries and OSV Segment is Expected to Witness Significant Growth.

7. Are there any restraints impacting market growth?

4.; Increasing Adoption of Clean Power Sources.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "India LNG Bunkering Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the India LNG Bunkering Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the India LNG Bunkering Industry?

To stay informed about further developments, trends, and reports in the India LNG Bunkering Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence