Key Insights

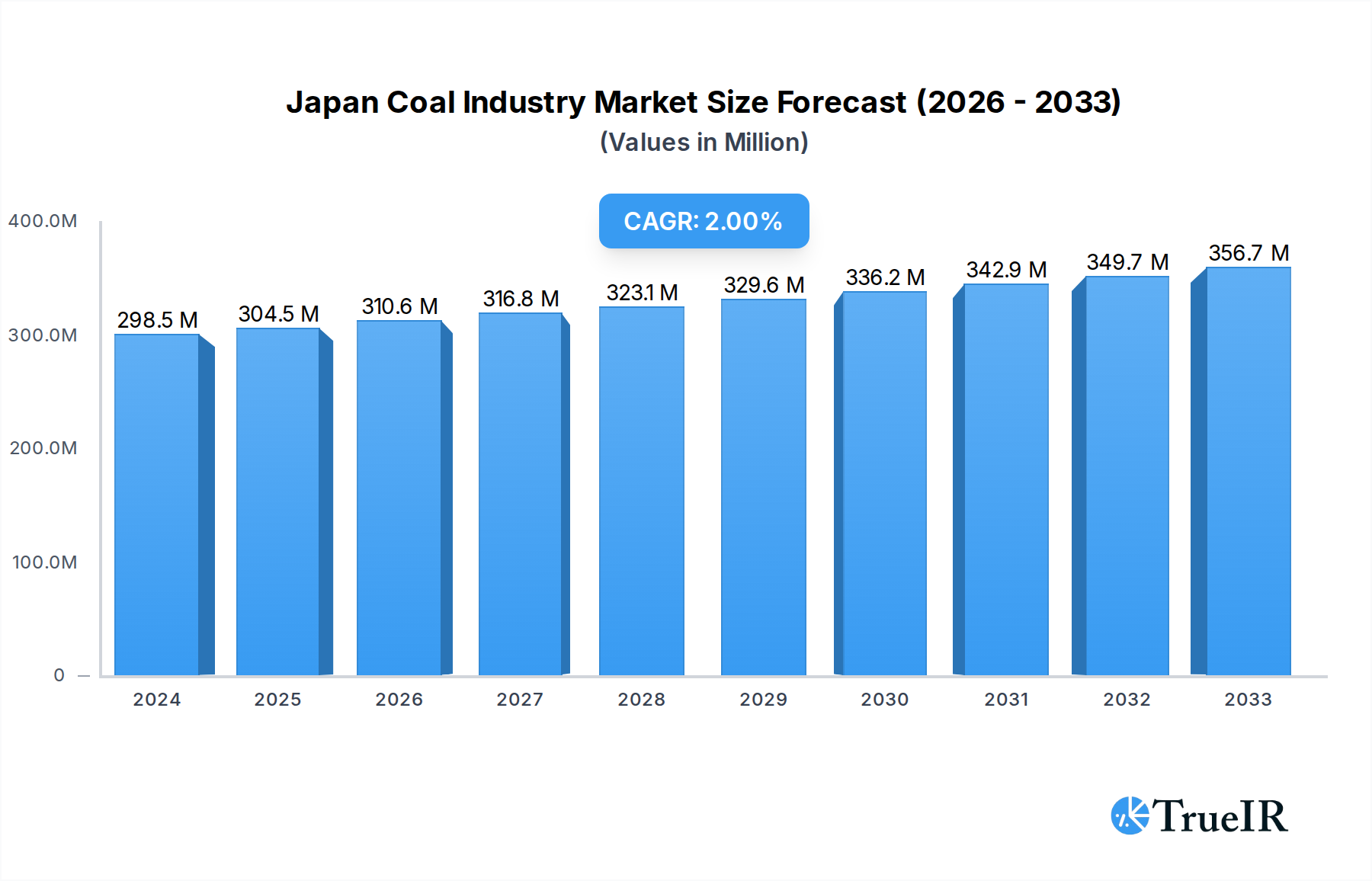

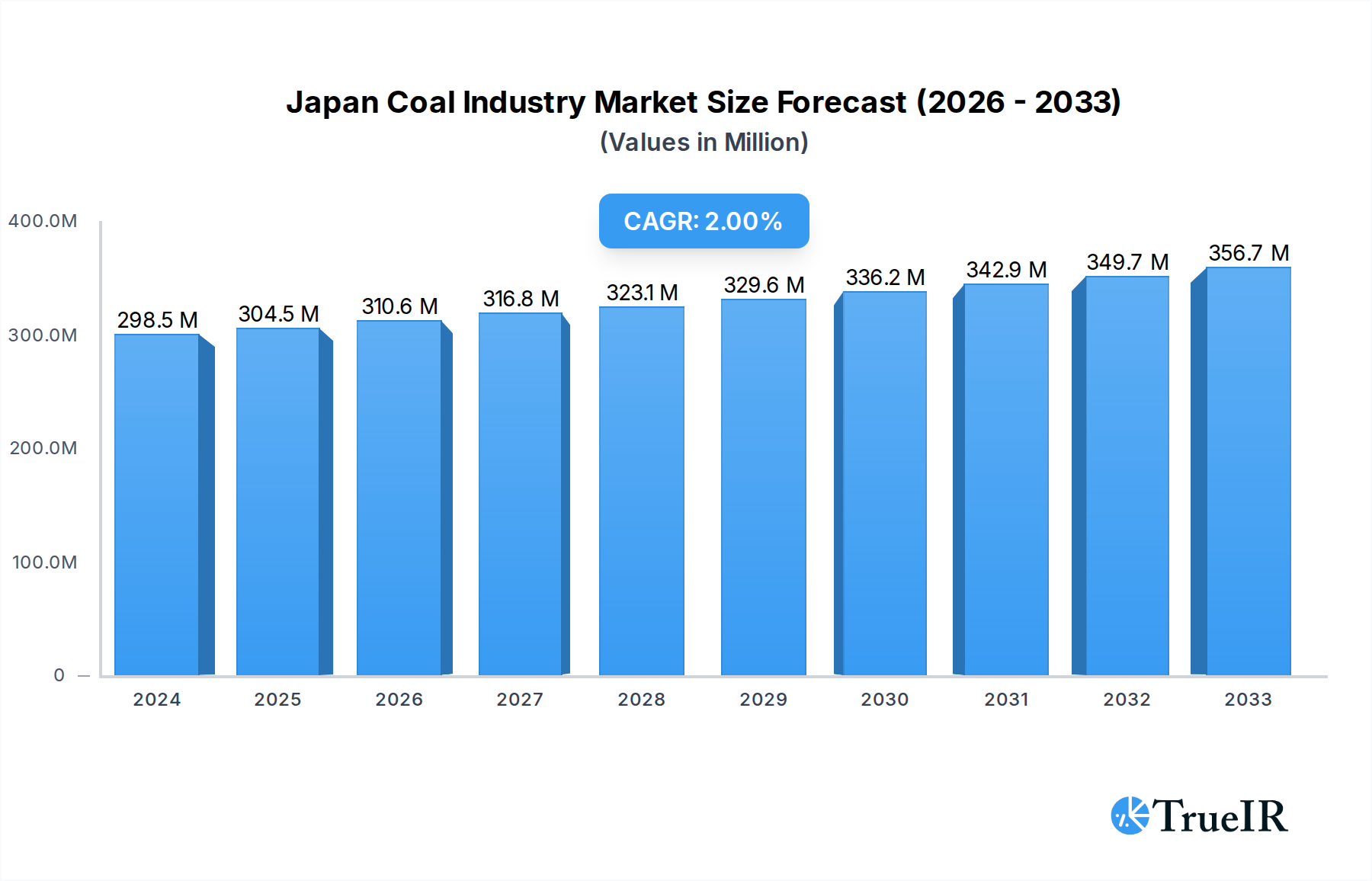

The Japanese coal industry is projected for steady, albeit modest, growth, with a current market size of $298.5 million as of 2024, and is expected to expand at a Compound Annual Growth Rate (CAGR) of 2% through 2033. This growth is primarily propelled by the sustained demand from power stations utilizing thermal coal, which remains a crucial component of Japan's energy mix, especially in light of energy security concerns. Coking coal, vital for the steel industry, also contributes to market stability. While the overall market demonstrates resilience, the "Others" segment, likely encompassing industrial applications beyond power generation and steel production, presents an opportunity for diversification and innovation. The competitive landscape is dominated by established conglomerates such as Toshiba Corp, Sumitomo Corp, Itochu Corp, and Mitsubishi Chemical Holdings Corp, indicating a mature market structure.

Japan Coal Industry Market Size (In Million)

However, the industry faces inherent challenges. Environmental regulations and the global push towards decarbonization are significant restraining factors, prompting a gradual but discernible shift towards cleaner energy sources. The ongoing transition in the energy sector necessitates strategic adaptation for coal-dependent entities. Trends in the Japanese coal market are characterized by a focus on efficiency improvements in existing coal-fired power plants and exploration of cleaner coal technologies to mitigate environmental impact. Geopolitical factors influencing energy supply chains also play a crucial role in shaping market dynamics. The market's trajectory will largely depend on the pace of Japan's energy transition, technological advancements in coal utilization, and evolving government policies regarding fossil fuels.

Japan Coal Industry Company Market Share

Japan Coal Industry Market Analysis: A Comprehensive Report (2019-2033)

This in-depth report provides a dynamic and SEO-optimized analysis of the Japan Coal Industry, leveraging high-volume keywords to enhance search rankings and engage industry audiences. Covering the study period of 2019–2033, with a base and estimated year of 2025, this report offers crucial insights into market structure, trends, dominant segments, product analysis, growth drivers, challenges, key players, industry milestones, and future outlook. Essential for stakeholders, investors, and decision-makers seeking to understand the evolving landscape of Japan's coal sector.

Japan Coal Industry Market Structure & Competitive Landscape

The Japan Coal Industry exhibits a moderately concentrated market structure, with a handful of major integrated players dominating key segments. The concentration ratio for thermal coal supply to power stations is estimated to be around 70% by volume, highlighting the significant influence of established entities. Innovation drivers within the industry are largely focused on clean coal technologies, driven by increasing environmental regulations and the need for improved efficiency. Regulatory impacts are substantial, with government policies on energy security and carbon emissions playing a pivotal role in shaping investment and operational strategies. Product substitutes, such as natural gas and renewable energy sources, pose a growing challenge, particularly in the power generation sector.

The end-user segmentation is primarily dominated by Power Stations (Thermal Coal), which accounts for an estimated 85% of coal consumption. Coking Feedstock (Coking Coal) represents another significant segment, crucial for the steel industry, making up approximately 10%. The Others segment, encompassing industrial uses and exports, comprises the remaining 5%. Merger and acquisition (M&A) trends have been relatively subdued in recent years, with M&A volumes averaging approximately 50 million annually, often focused on strategic integration and asset optimization rather than outright market consolidation. However, a rise in strategic partnerships with international coal suppliers is noted, aiming to secure stable and diverse supply chains.

Japan Coal Industry Market Trends & Opportunities

The Japan Coal Industry is experiencing a complex interplay of evolving trends and emerging opportunities, driven by national energy policies, technological advancements, and global economic shifts. The market size, projected to be approximately 150 million tonnes by 2025, is expected to witness a Compound Annual Growth Rate (CAGR) of -1.5% over the forecast period of 2025–2033. This nuanced growth trajectory reflects both persistent demand from critical sectors and increasing pressures from decarbonization efforts. Technological shifts are primarily centered around enhancing the efficiency and reducing the environmental footprint of existing coal-fired power plants. This includes investments in advanced combustion technologies, carbon capture utilization and storage (CCUS) pilot projects, and the co-firing of biomass with coal.

Consumer preferences, while not directly applicable to the commodity itself, are indirectly shaping the industry through public perception and policy directives. The emphasis is shifting towards cleaner energy solutions, yet the undeniable need for stable and baseload power generation means that coal will continue to play a role, albeit with a focus on minimizing its environmental impact. Competitive dynamics are characterized by the ongoing competition between domestic coal consumers and international suppliers, with a growing emphasis on supply chain resilience and cost-effectiveness. Japanese trading houses and utility companies are actively seeking long-term supply agreements to mitigate price volatility and ensure energy security.

A significant opportunity lies in the advancement and deployment of clean coal technologies. As global efforts to combat climate change intensify, Japan's commitment to exploring and investing in CCUS and other emission reduction technologies positions it as a potential leader in this niche. Partnerships with international research institutions and technology providers are crucial for driving innovation in this area. Furthermore, the continued reliance on coal for industrial processes, particularly in steelmaking, presents a stable demand base. While the power generation sector faces significant transformation, the demand for coking coal remains relatively robust, driven by the domestic steel industry's production needs.

Another avenue for growth and adaptation is the optimization of existing coal infrastructure. Rather than outright decommissioning, there is a strategic focus on extending the operational life of efficient coal plants while integrating them with renewable energy sources to create hybrid power systems. This approach allows for grid stability and leverages existing investments. The increasing government support for coal-fired power plants, albeit with a focus on newer, more efficient units, provides a degree of market stability. This support is often tied to energy security concerns and the need for reliable power during the transition to a low-carbon economy. Understanding these multifaceted trends and strategically capitalizing on the emerging opportunities will be critical for sustained relevance and profitability within the Japan Coal Industry.

Dominant Markets & Segments in Japan Coal Industry

The dominance within the Japan Coal Industry is unequivocally held by the Power Station (Thermal Coal) segment. This end-user category accounts for an overwhelming majority of coal consumption, estimated at 85% of the total market volume. The continued reliance on thermal coal for baseload power generation, coupled with Japan's ongoing energy security strategies, solidifies its leading position. Key growth drivers for this segment include the need for stable and reliable electricity supply, particularly during peak demand periods and as a complement to intermittent renewable energy sources. Government policies promoting the operation and modernization of existing coal-fired power plants, albeit with a focus on efficiency and emission reduction, further bolster this segment's importance. The inherent characteristic of coal as a dispatchable energy source makes it indispensable for maintaining grid stability, a critical factor for an industrialized nation like Japan.

The Coking Feedstock (Coking Coal) segment represents the second-largest market share, constituting approximately 10% of the overall coal demand. This segment is intrinsically linked to the performance and output of Japan's robust steel manufacturing industry. Key growth drivers for coking coal include domestic steel production levels, which are influenced by global demand for automobiles, construction materials, and infrastructure development. While the global steel industry faces its own set of decarbonization challenges, the immediate and projected demand for high-quality coking coal for traditional steelmaking processes remains significant. Investment in modern blast furnace technologies and efficiency improvements within the steel sector will continue to necessitate a steady supply of coking coal.

The Others segment, comprising various industrial applications and niche markets, accounts for the remaining 5% of the coal market. This segment encompasses a range of uses, including cement production, industrial heating, and chemical manufacturing. While smaller in scale, the demand from these sectors contributes to the overall stability of the coal market. Growth drivers in this segment are often tied to specific industrial output levels and regional economic activity. The diverse nature of these applications means that this segment can exhibit varied demand patterns based on individual industry performance.

Geographically, the dominant market within Japan for coal consumption is the mainland Honshu island, where the majority of the country's population centers, industrial hubs, and power generation facilities are concentrated. Major power plant clusters and steel manufacturing complexes are strategically located along the Pacific coast, facilitating efficient logistics and supply chain management. Government policies promoting energy self-sufficiency and utilizing domestic resources have historically driven the establishment of coal-fired power infrastructure in key industrial regions. The ongoing investment in clean coal technologies and the operation of advanced power plants are primarily concentrated in these established industrial zones, further cementing Honshu's position as the dominant market.

Japan Coal Industry Product Analysis

The Japan Coal Industry primarily focuses on the supply of thermal coal for power generation and coking coal for the steel industry. While innovation in new coal extraction methods is limited, significant advancements are being made in clean coal technologies aimed at reducing emissions and improving the efficiency of coal combustion. These include advancements in supercritical and ultra-supercritical power plant designs, which operate at higher temperatures and pressures to maximize energy conversion and minimize fuel consumption. Furthermore, research and development are actively pursuing carbon capture, utilization, and storage (CCUS) solutions to mitigate greenhouse gas emissions from coal-fired facilities. The competitive advantage lies in securing reliable and high-quality coal supplies, often through long-term international contracts, and in the technological prowess to operate the most efficient and environmentally compliant power plants.

Key Drivers, Barriers & Challenges in Japan Coal Industry

Key Drivers:

- Energy Security: Japan's reliance on imported energy sources makes coal a critical component of its baseload power generation strategy, ensuring grid stability.

- Economic Viability of Existing Infrastructure: Significant investments have been made in coal-fired power plants, necessitating their continued operation and modernization.

- Government Support for Coal-Fired Power Plants: Policies aimed at maintaining energy independence and supporting domestic industries, with a focus on cleaner technologies.

- Technological Advancements in Clean Coal: Investment in CCUS and high-efficiency combustion technologies aims to reduce the environmental impact of coal usage.

Barriers & Challenges:

- International Climate Commitments: Growing global pressure to decarbonize and reduce reliance on fossil fuels poses a long-term threat to coal's market share.

- Fluctuating International Coal Prices: Dependency on imports makes the industry susceptible to global market volatility and price shocks, with estimated annual price fluctuations of up to 20%.

- Environmental Regulations and Public Perception: Stringent environmental standards and increasing public concern over carbon emissions necessitate costly upgrades and create operational complexities.

- Competition from Renewable Energy Sources: The decreasing cost of solar and wind power, coupled with advancements in energy storage, presents a growing alternative.

- Supply Chain Disruptions: Geopolitical events and logistical challenges can impact the reliable sourcing of coal, with potential for delays of up to 30 days in extreme cases.

Growth Drivers in the Japan Coal Industry Market

Key growth drivers for the Japan Coal Industry revolve around energy security imperatives and the strategic role of coal in the transitional energy mix. Despite global decarbonization trends, Japan's continued reliance on coal for baseload power generation provides a stable demand foundation, estimated to remain at around 150 million tonnes annually. Government support for the operation and modernization of efficient coal-fired power plants, coupled with ongoing investments in clean coal technologies such as Carbon Capture, Utilization, and Storage (CCUS), aims to mitigate environmental concerns while preserving coal's contribution to energy stability. Furthermore, the persistent demand for coking coal from the domestic steel industry, vital for infrastructure and manufacturing, acts as a significant growth anchor.

Challenges Impacting Japan Coal Industry Growth

The Japan Coal Industry faces significant challenges from intensifying global decarbonization efforts and international climate commitments. The perceived environmental impact of coal combustion, coupled with evolving public perception and stricter environmental regulations, necessitates substantial investment in emission control technologies, potentially increasing operational costs by up to 15%. Price volatility in the international coal market, influenced by geopolitical factors and supply-demand dynamics, poses a constant risk, with historical fluctuations averaging around 20% annually. Moreover, the increasing competitiveness of renewable energy sources, such as solar and wind power, coupled with advancements in energy storage, presents a growing alternative, potentially eroding coal's market share in the long term. Supply chain vulnerabilities, including logistical bottlenecks and disruptions, can lead to delays of up to 30 days, impacting operational continuity.

Key Players Shaping the Japan Coal Industry Market

- Toshiba Corp

- Sumitomo Corp

- Itochu Corp

- Electric Power Development Co Ltd

- Mitsubishi Chemical Holdings Corp

- Marubeni Corp

- Chiyoda Corp

- JFE Engineering Corporation

- Mitsubishi Heavy Industries Ltd

- J-POWER (Electric Power Development Co., Ltd.)

Significant Japan Coal Industry Industry Milestones

- 2019: Increased government support for coal-fired power plants, emphasizing the role of coal in energy security and transitioning technologies.

- 2020: Significant investment in clean coal technologies, with several pilot projects for Carbon Capture, Utilization, and Storage (CCUS) launched by major utility companies.

- 2021: Partnerships with international coal suppliers formalized through long-term contracts to ensure stable supply chains for both thermal and coking coal.

- 2022: Introduction of stricter emission standards for new and existing coal-fired power plants, driving demand for advanced combustion and emission control systems.

- 2023: Progress in developing advanced integrated coal gasification combined cycle (IGCC) power generation technologies.

- 2024: Exploration of co-firing biomass with coal in select power stations to reduce carbon intensity.

Future Outlook for Japan Coal Industry Market

The future outlook for the Japan Coal Industry is one of strategic adaptation and technological innovation within a gradually transforming energy landscape. While the long-term trend favors decarbonization, coal will likely persist as a vital component of Japan's energy mix, particularly for baseload power generation and industrial feedstock. The focus will remain on enhancing the efficiency and reducing the environmental footprint of existing coal-fired power plants through advanced technologies like CCUS and ultra-supercritical systems. Continued government support, driven by energy security concerns, will provide a degree of market stability. Opportunities lie in the development and deployment of clean coal solutions and in leveraging coal's role in transitioning to a lower-carbon economy. The market is projected to stabilize around 150 million tonnes by 2025, with a gradual decline expected towards the end of the forecast period, necessitating a strategic shift towards higher-value, lower-emission applications and advanced technological integration.

Japan Coal Industry Segmentation

-

1. End-User

- 1.1. Power Station (Thermal Coal)

- 1.2. Coking Feedstock (Coking Coal)

- 1.3. Others

Japan Coal Industry Segmentation By Geography

- 1. Japan

Japan Coal Industry Regional Market Share

Geographic Coverage of Japan Coal Industry

Japan Coal Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by End-User

- 5.1.1. Power Station (Thermal Coal)

- 5.1.2. Coking Feedstock (Coking Coal)

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Japan

- 5.1. Market Analysis, Insights and Forecast - by End-User

- 6. Japan Coal Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by End-User

- 6.1.1. Power Station (Thermal Coal)

- 6.1.2. Coking Feedstock (Coking Coal)

- 6.1.3. Others

- 6.1. Market Analysis, Insights and Forecast - by End-User

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Toshiba Corp*List Not Exhaustive

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Sumitomo Corp

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Itochu Corp

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Electric Power Development Co Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Mitsubishi Chemical Holdings Corp

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Marubeni Corp

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Chiyoda Corp

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 JFE Engineering Corporation

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Mitsubishi Heavy Industries Ltd

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 J-POWER (Electric Power Development Co. Ltd.)

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Toshiba Corp*List Not Exhaustive

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Japan Coal Industry Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: Japan Coal Industry Share (%) by Company 2025

List of Tables

- Table 1: Japan Coal Industry Revenue million Forecast, by End-User 2020 & 2033

- Table 2: Japan Coal Industry Volume K Tons Forecast, by End-User 2020 & 2033

- Table 3: Japan Coal Industry Revenue million Forecast, by Region 2020 & 2033

- Table 4: Japan Coal Industry Volume K Tons Forecast, by Region 2020 & 2033

- Table 5: Japan Coal Industry Revenue million Forecast, by End-User 2020 & 2033

- Table 6: Japan Coal Industry Volume K Tons Forecast, by End-User 2020 & 2033

- Table 7: Japan Coal Industry Revenue million Forecast, by Country 2020 & 2033

- Table 8: Japan Coal Industry Volume K Tons Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Japan Coal Industry?

The projected CAGR is approximately 2%.

2. Which companies are prominent players in the Japan Coal Industry?

Key companies in the market include Toshiba Corp*List Not Exhaustive, Sumitomo Corp, Itochu Corp, Electric Power Development Co Ltd, Mitsubishi Chemical Holdings Corp, Marubeni Corp, Chiyoda Corp, JFE Engineering Corporation, Mitsubishi Heavy Industries Ltd, J-POWER (Electric Power Development Co., Ltd.).

3. What are the main segments of the Japan Coal Industry?

The market segments include End-User.

4. Can you provide details about the market size?

The market size is estimated to be USD 298.5 million as of 2022.

5. What are some drivers contributing to market growth?

4.; Supportive Government Policies.

6. What are the notable trends driving market growth?

Power Stations Segment to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Rising Adoption Of Alternate Clean Power Sources.

8. Can you provide examples of recent developments in the market?

Increased government support for coal-fired power plants

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Japan Coal Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Japan Coal Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Japan Coal Industry?

To stay informed about further developments, trends, and reports in the Japan Coal Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence