Key Insights

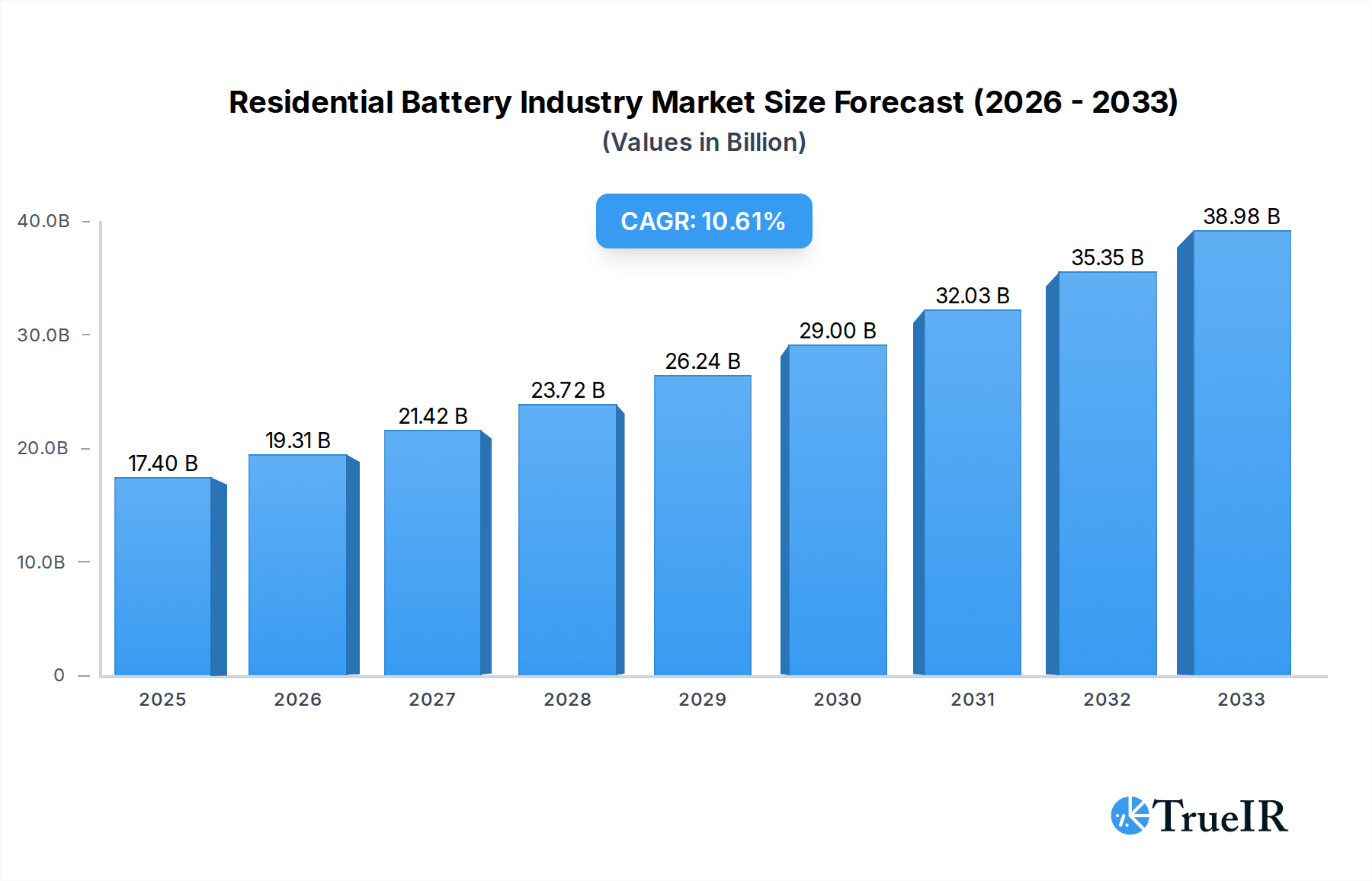

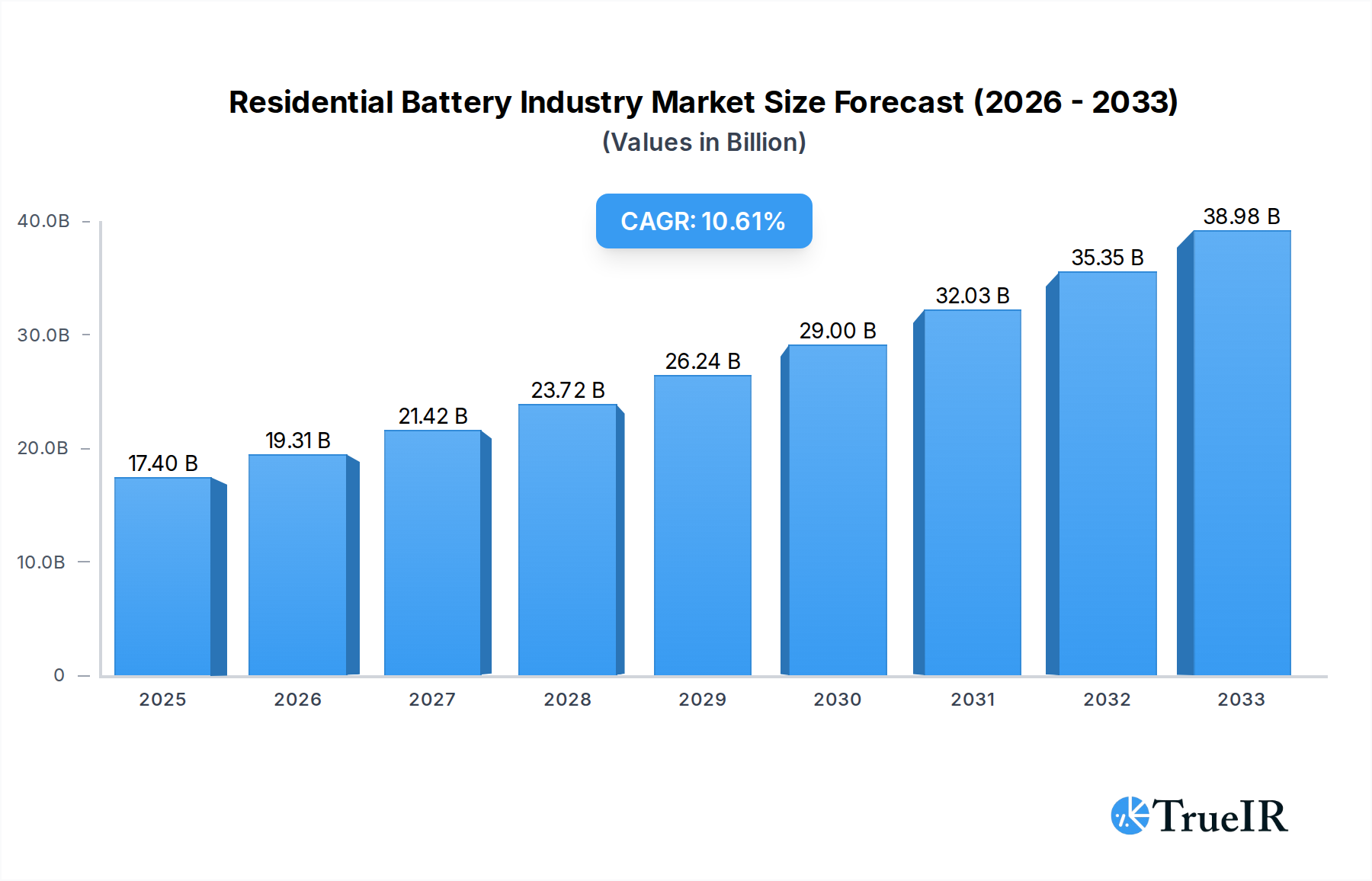

The residential battery market is poised for significant expansion, projected to reach $17.4 billion in 2025 and grow at a robust CAGR of 10.9% through 2033. This surge is primarily driven by increasing consumer demand for reliable and sustainable energy solutions, amplified by rising electricity prices and the growing adoption of renewable energy sources like solar power in homes. The desire for energy independence and grid resilience, especially in regions prone to power outages, further fuels this growth. Technological advancements are making batteries more efficient, longer-lasting, and cost-effective, broadening their appeal to homeowners. Key market segments include Lithium-ion batteries, which dominate due to their superior energy density and performance, and Lead-acid batteries, offering a more budget-friendly option. Emerging "Other Types" are also gaining traction with innovative chemistries and functionalities.

Residential Battery Industry Market Size (In Billion)

The competitive landscape features major players like BYD Co Ltd, Samsung SDI Co Ltd, and Tesla Inc, alongside established battery manufacturers and energy solution providers such as Amara Raja Batteries Ltd, Luminous Power Technologies Pvt Ltd, and LG Energy Solution Ltd. These companies are investing heavily in research and development to innovate and capture market share. While the market is experiencing strong tailwinds, potential restraints include high upfront costs for some advanced battery systems and evolving regulatory frameworks in different regions. Nonetheless, the overarching trend towards decarbonization and the decentralization of energy generation strongly supports the continued growth and evolution of the residential battery industry, making it a dynamic and attractive sector for investment and innovation.

Residential Battery Industry Company Market Share

Residential Battery Industry: Comprehensive Market Analysis and Future Outlook (2019-2033)

Gain unparalleled insights into the dynamic Residential Battery Industry with this in-depth report. Covering the period from 2019 to 2033, with a base and estimated year of 2025, this analysis delves into market structure, trends, opportunities, and key players. Explore the burgeoning demand for residential energy storage solutions, driven by renewable energy adoption and grid modernization efforts. This report is an essential resource for stakeholders seeking to understand the global residential battery market size, lithium-ion battery market share in residential applications, and the competitive landscape shaped by leading companies such as BYD Co Ltd, Amara Raja Batteries Ltd, Samsung SDI Co Ltd, Luminous Power Technologies Pvt Ltd, LG Energy Solution Ltd, FIMER SpA, Siemens AG, Tesla Inc, Delta Electronics Ltd, NEC Corporation, Energizer Holding Inc, Duracell Inc, and Panasonic Corporation.

Residential Battery Industry Market Structure & Competitive Landscape

The Residential Battery Industry exhibits a moderately concentrated market structure, with a handful of dominant players, including BYD Co Ltd, Samsung SDI Co Ltd, and LG Energy Solution Ltd, holding significant market share. Innovation serves as a primary driver, fueled by advancements in lithium-ion battery technology, enhanced energy density, and improved safety features. Regulatory impacts are substantial, with government incentives for renewable energy adoption and energy storage creating favorable market conditions. Product substitutes, primarily traditional grid-supplied electricity and emerging smart grid technologies, exert a secondary influence. End-user segmentation reveals a strong preference for reliable power backup and cost savings associated with self-consumption of solar energy. Merger and acquisition (M&A) trends are evident, with strategic consolidations aimed at expanding market reach and technological capabilities. The residential battery storage market growth is further propelled by increasing consumer awareness and demand for energy independence. A concentration ratio of approximately 65% is estimated for the top five players in 2025. M&A volumes are projected to reach over $5 billion during the forecast period, reflecting the industry's consolidation drive.

Residential Battery Industry Market Trends & Opportunities

The global Residential Battery Industry is poised for robust expansion, projected to reach a market size exceeding $80 billion by 2033, with a Compound Annual Growth Rate (CAGR) of approximately 18%. This substantial growth is underpinned by a confluence of evolving technological landscapes, shifting consumer preferences, and intensifying competitive dynamics. The dominant trend is the accelerated adoption of lithium-ion batteries for residential energy storage, driven by their superior energy density, longer lifespan, and decreasing costs compared to traditional lead-acid battery solutions. Technological advancements are continuously enhancing battery performance, including faster charging capabilities, improved thermal management systems, and the integration of sophisticated battery management systems (BMS) for optimized operation and safety.

Consumer preferences are increasingly shifting towards energy independence, reducing reliance on the grid, and leveraging self-generated renewable energy. The rising cost of electricity, coupled with growing environmental consciousness, further fuels this demand. Homeowners are actively seeking solutions that offer reliable backup power during outages, reduce their electricity bills through peak shaving and time-of-use arbitrage, and contribute to a sustainable energy future.

The competitive dynamics within the industry are characterized by intense innovation and strategic partnerships. Leading companies like Tesla Inc. with its Powerwall, LG Energy Solution Ltd, and BYD Co Ltd are continuously pushing the boundaries of technology and expanding their product portfolios to cater to diverse consumer needs. Market penetration rates are rapidly increasing, particularly in regions with strong government support for renewable energy and supportive grid policies. For instance, market penetration in North America and Europe is expected to exceed 35% of eligible households by 2030. The residential battery market forecast indicates significant opportunities for companies that can offer integrated solutions, competitive pricing, and robust customer support. Emerging opportunities also lie in the development of smart grid-compatible battery systems, vehicle-to-grid (V2G) integration, and advanced energy management software that optimizes battery usage in conjunction with solar power generation and grid dynamics. The home battery storage market is not just about power; it's about creating intelligent, resilient, and cost-effective energy ecosystems for households worldwide.

Dominant Markets & Segments in Residential Battery Industry

The Lithium-ion Battery segment is unequivocally dominant within the Residential Battery Industry, projected to capture over 85% of the market share by 2028. This dominance is propelled by a cascade of critical growth drivers and superior technological attributes that resonate strongly with residential energy storage needs.

Technological Superiority of Lithium-ion Batteries: Their high energy density allows for more power in a smaller footprint, crucial for space-constrained residential installations. Longer cycle life means fewer replacements over the system's lifespan, offering better long-term value. Faster charging and discharging rates are essential for effectively capturing solar energy and providing rapid power backup. Furthermore, continuous advancements in chemistries like Lithium Nickel Manganese Cobalt Oxide (NMC) and Lithium Iron Phosphate (LFP) are further enhancing safety, performance, and cost-effectiveness, making them the preferred choice for modern homes.

Favorable Government Policies and Incentives: Many countries and regions are actively promoting renewable energy adoption and energy independence through attractive subsidies, tax credits, and net metering policies. These initiatives directly reduce the upfront cost of residential solar and battery storage systems, significantly boosting market penetration. For example, the Inflation Reduction Act in the United States has provided substantial incentives for homeowners investing in clean energy technologies.

Increasing Cost-Effectiveness: The declining manufacturing costs of lithium-ion batteries, driven by economies of scale and technological improvements, are making residential battery storage increasingly affordable for a wider consumer base. This cost reduction is a pivotal factor in accelerating market adoption and achieving competitive parity with traditional energy sources in many regions.

Growing Awareness of Energy Security and Resilience: Frequent power outages due to extreme weather events and grid instability have heightened consumer awareness about the importance of reliable backup power. Residential batteries offer a compelling solution, ensuring uninterrupted power supply for essential appliances and maintaining household comfort and safety.

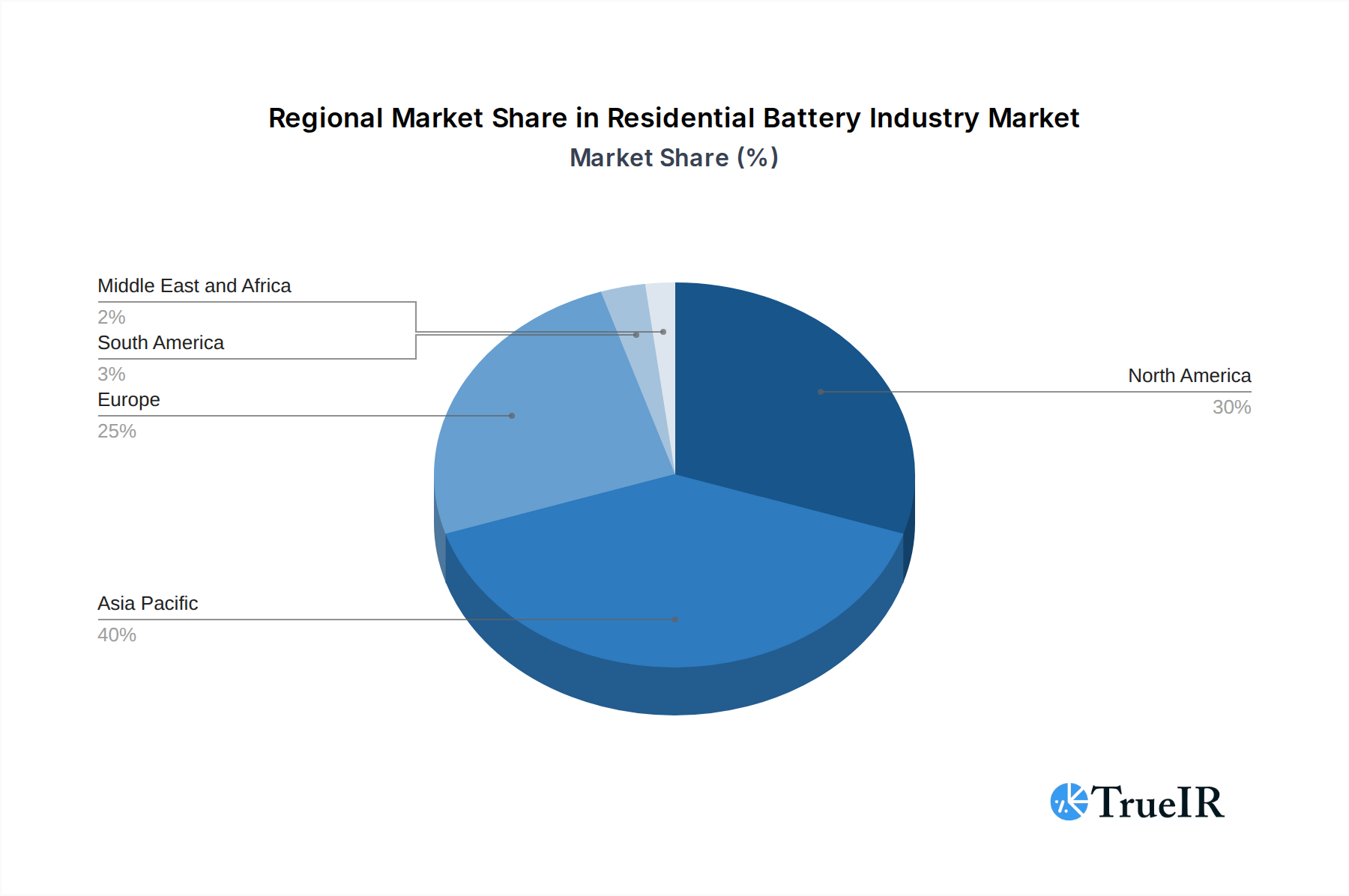

Regionally, North America and Europe currently lead the charge in residential battery adoption, owing to robust renewable energy infrastructure, supportive policies, and high electricity prices. Asia-Pacific, particularly countries like China and Australia, is emerging as a significant growth market, driven by rapid urbanization, increasing disposable incomes, and a strong focus on reducing carbon emissions. Countries like Germany, for instance, are expected to see over 2 million residential battery installations by 2027. The residential battery market growth in these dominant regions is further catalyzed by the availability of leading players like Tesla Inc., LG Energy Solution Ltd, and BYD Co Ltd, who are investing heavily in local manufacturing and distribution networks to meet the escalating demand for home battery storage systems.

Residential Battery Industry Product Analysis

The Residential Battery Industry is characterized by continuous product innovation focused on enhancing performance, safety, and integration. Lithium-ion batteries, particularly NMC and LFP chemistries, dominate due to their superior energy density and lifespan. Innovations are centered on faster charging/discharging capabilities, advanced thermal management systems for extended longevity, and sophisticated Battery Management Systems (BMS) for optimized efficiency and safety. Competitive advantages are derived from integrated solutions combining solar inverters with battery storage, smart home energy management features, and seamless grid connectivity. Applications range from backup power and solar self-consumption to peak shaving and participation in demand response programs, offering homeowners significant cost savings and energy independence.

Key Drivers, Barriers & Challenges in Residential Battery Industry

Key Drivers, Barriers & Challenges in Residential Battery Industry

Key Drivers: The Residential Battery Industry is propelled by several key drivers. Growing adoption of renewable energy sources, particularly solar PV, necessitates efficient energy storage solutions for self-consumption and grid stability. Increasing electricity prices and the desire for energy independence make battery storage an attractive investment for cost savings and resilience. Favorable government policies, including tax credits and subsidies for renewable energy and storage, significantly reduce upfront costs. Technological advancements in lithium-ion battery technology, leading to improved energy density, longer lifespan, and reduced costs, are making batteries more accessible and efficient. The escalating frequency of power outages due to climate change further fuels demand for reliable backup power.

Key Barriers & Challenges: Despite robust growth, the industry faces significant challenges. High upfront costs remain a primary barrier to widespread adoption, although prices are declining. Complex regulatory landscapes and permitting processes can delay installations and increase project complexity. Supply chain disruptions, particularly for key raw materials like lithium and cobalt, can impact production volumes and pricing. Grid interconnection challenges and varying utility policies can create uncertainties for installers and consumers. Consumer education and awareness regarding the benefits and complexities of battery storage are still developing. Competition from alternative energy solutions and the need for robust cybersecurity measures for connected systems also present ongoing challenges. The potential for supply chain bottlenecks, projected to impact 20% of raw material sourcing in the next three years, adds a layer of risk.

Growth Drivers in the Residential Battery Industry Market

The Residential Battery Industry is experiencing significant growth driven by a confluence of technological, economic, and policy factors. The accelerating integration of solar power systems is a primary catalyst, as homeowners seek to maximize self-consumption and reduce reliance on the grid. This is complemented by increasing consumer demand for energy independence and resilience, particularly in light of rising electricity prices and the growing frequency of power outages. Government incentives, such as tax credits and rebates for renewable energy and storage installations in regions like North America and Europe, play a crucial role in making these systems more affordable. Furthermore, advancements in lithium-ion battery technology are continuously improving energy density, cycle life, and safety while driving down manufacturing costs, making residential battery storage a more viable and attractive investment for a broader segment of the population. The projected market expansion of over $50 billion in the next decade is a testament to these powerful growth catalysts.

Challenges Impacting Residential Battery Industry Growth

The Residential Battery Industry faces several critical challenges that can impact its growth trajectory. High initial investment costs, although decreasing, still represent a significant barrier for many households compared to traditional electricity bills. Complex and varying regulatory frameworks across different municipalities and utility territories can lead to installation delays and uncertainty. Supply chain vulnerabilities, particularly concerning the sourcing of critical raw materials like lithium and cobalt, pose a risk of price volatility and production limitations, impacting the availability of batteries. Grid interconnection challenges, including lengthy approval processes and differing utility requirements, can hinder the seamless integration of battery systems. Furthermore, limited consumer awareness and understanding of the benefits and operational aspects of battery storage can slow down adoption rates, necessitating greater industry-led educational initiatives. Competitive pressures from emerging technologies and the need for robust cybersecurity for connected energy systems also present ongoing challenges to market expansion.

Key Players Shaping the Residential Battery Industry Market

- BYD Co Ltd

- Amara Raja Batteries Ltd

- Samsung SDI Co Ltd

- Luminous Power Technologies Pvt Ltd

- LG Energy Solution Ltd

- FIMER SpA

- Siemens AG

- Tesla Inc

- Delta Electronics Ltd

- NEC Corporation

- Energizer Holding Inc

- Duracell Inc

- Panasonic Corporation

Significant Residential Battery Industry Industry Milestones

- 2019: Increased government incentives for solar-plus-storage systems in several key markets, boosting early adoption.

- 2020: Significant price reductions in lithium-ion battery manufacturing due to economies of scale and technological improvements.

- 2021: Launch of new integrated residential energy storage solutions by major players like Tesla and LG Energy Solution, offering enhanced functionality and user experience.

- 2022: Growing consumer awareness regarding grid resilience and backup power needs, driven by an increase in extreme weather events.

- 2023: Expansion of manufacturing capacities for lithium-ion batteries globally, aimed at meeting rising demand and further reducing costs.

- 2024: Introduction of advanced battery management systems (BMS) with enhanced AI capabilities for optimized performance and predictive maintenance.

- 2025 (Estimated): Significant market penetration of residential battery storage systems exceeding 15% in leading markets like North America and Europe.

- 2026-2033 (Forecast): Continued innovation in battery chemistries, development of vehicle-to-grid (V2G) integration for residential applications, and potential emergence of new disruptive technologies.

Future Outlook for Residential Battery Industry Market

The future outlook for the Residential Battery Industry is exceptionally positive, driven by several key growth catalysts. The ongoing global transition towards renewable energy sources, coupled with the increasing need for grid modernization and energy resilience, will continue to fuel demand for residential battery storage. Technological advancements are expected to bring further cost reductions, enhanced performance, and improved safety features, making these systems more accessible and appealing to a wider consumer base. Government policies and supportive regulations in key markets will likely remain a significant driver, incentivizing adoption and creating a favorable investment climate. Emerging opportunities in smart grid integration, demand response programs, and the potential for vehicle-to-grid (V2G) applications will further expand the value proposition of residential batteries. The industry is projected for substantial market expansion, with strategic opportunities in developing integrated energy solutions, expanding into emerging markets, and fostering greater consumer education to unlock the full potential of a decentralized and sustainable energy future.

Residential Battery Industry Segmentation

-

1. Type

- 1.1. Lithium-ion Battery

- 1.2. Lead-acid Battery

- 1.3. Others Types

Residential Battery Industry Segmentation By Geography

- 1. North America

- 2. Asia Pacific

- 3. Europe

- 4. South America

- 5. Middle East and Africa

Residential Battery Industry Regional Market Share

Geographic Coverage of Residential Battery Industry

Residential Battery Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Lithium-ion Battery

- 5.1.2. Lead-acid Battery

- 5.1.3. Others Types

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. Asia Pacific

- 5.2.3. Europe

- 5.2.4. South America

- 5.2.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Residential Battery Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Lithium-ion Battery

- 6.1.2. Lead-acid Battery

- 6.1.3. Others Types

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America Residential Battery Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Lithium-ion Battery

- 7.1.2. Lead-acid Battery

- 7.1.3. Others Types

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Asia Pacific Residential Battery Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Lithium-ion Battery

- 8.1.2. Lead-acid Battery

- 8.1.3. Others Types

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Europe Residential Battery Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Lithium-ion Battery

- 9.1.2. Lead-acid Battery

- 9.1.3. Others Types

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. South America Residential Battery Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Lithium-ion Battery

- 10.1.2. Lead-acid Battery

- 10.1.3. Others Types

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Middle East and Africa Residential Battery Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Lithium-ion Battery

- 11.1.2. Lead-acid Battery

- 11.1.3. Others Types

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 BYD Co Ltd

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Amara Raja Batteries Ltd

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Samsung SDI Co Ltd

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Luminous Power Technologies Pvt Ltd

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 LG Energy Solution Ltd

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 FIMER SpA

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Siemens AG

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Tesla Inc

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Delta Electronics Ltd

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 NEC Corporation

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Energizer Holding Inc

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Duracell Inc

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Panasonic Corporation

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.1 BYD Co Ltd

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Residential Battery Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global Residential Battery Industry Volume Breakdown (K Tons, %) by Region 2025 & 2033

- Figure 3: North America Residential Battery Industry Revenue (billion), by Type 2025 & 2033

- Figure 4: North America Residential Battery Industry Volume (K Tons), by Type 2025 & 2033

- Figure 5: North America Residential Battery Industry Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Residential Battery Industry Volume Share (%), by Type 2025 & 2033

- Figure 7: North America Residential Battery Industry Revenue (billion), by Country 2025 & 2033

- Figure 8: North America Residential Battery Industry Volume (K Tons), by Country 2025 & 2033

- Figure 9: North America Residential Battery Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: North America Residential Battery Industry Volume Share (%), by Country 2025 & 2033

- Figure 11: Asia Pacific Residential Battery Industry Revenue (billion), by Type 2025 & 2033

- Figure 12: Asia Pacific Residential Battery Industry Volume (K Tons), by Type 2025 & 2033

- Figure 13: Asia Pacific Residential Battery Industry Revenue Share (%), by Type 2025 & 2033

- Figure 14: Asia Pacific Residential Battery Industry Volume Share (%), by Type 2025 & 2033

- Figure 15: Asia Pacific Residential Battery Industry Revenue (billion), by Country 2025 & 2033

- Figure 16: Asia Pacific Residential Battery Industry Volume (K Tons), by Country 2025 & 2033

- Figure 17: Asia Pacific Residential Battery Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Residential Battery Industry Volume Share (%), by Country 2025 & 2033

- Figure 19: Europe Residential Battery Industry Revenue (billion), by Type 2025 & 2033

- Figure 20: Europe Residential Battery Industry Volume (K Tons), by Type 2025 & 2033

- Figure 21: Europe Residential Battery Industry Revenue Share (%), by Type 2025 & 2033

- Figure 22: Europe Residential Battery Industry Volume Share (%), by Type 2025 & 2033

- Figure 23: Europe Residential Battery Industry Revenue (billion), by Country 2025 & 2033

- Figure 24: Europe Residential Battery Industry Volume (K Tons), by Country 2025 & 2033

- Figure 25: Europe Residential Battery Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Europe Residential Battery Industry Volume Share (%), by Country 2025 & 2033

- Figure 27: South America Residential Battery Industry Revenue (billion), by Type 2025 & 2033

- Figure 28: South America Residential Battery Industry Volume (K Tons), by Type 2025 & 2033

- Figure 29: South America Residential Battery Industry Revenue Share (%), by Type 2025 & 2033

- Figure 30: South America Residential Battery Industry Volume Share (%), by Type 2025 & 2033

- Figure 31: South America Residential Battery Industry Revenue (billion), by Country 2025 & 2033

- Figure 32: South America Residential Battery Industry Volume (K Tons), by Country 2025 & 2033

- Figure 33: South America Residential Battery Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: South America Residential Battery Industry Volume Share (%), by Country 2025 & 2033

- Figure 35: Middle East and Africa Residential Battery Industry Revenue (billion), by Type 2025 & 2033

- Figure 36: Middle East and Africa Residential Battery Industry Volume (K Tons), by Type 2025 & 2033

- Figure 37: Middle East and Africa Residential Battery Industry Revenue Share (%), by Type 2025 & 2033

- Figure 38: Middle East and Africa Residential Battery Industry Volume Share (%), by Type 2025 & 2033

- Figure 39: Middle East and Africa Residential Battery Industry Revenue (billion), by Country 2025 & 2033

- Figure 40: Middle East and Africa Residential Battery Industry Volume (K Tons), by Country 2025 & 2033

- Figure 41: Middle East and Africa Residential Battery Industry Revenue Share (%), by Country 2025 & 2033

- Figure 42: Middle East and Africa Residential Battery Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Residential Battery Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Global Residential Battery Industry Volume K Tons Forecast, by Type 2020 & 2033

- Table 3: Global Residential Battery Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Residential Battery Industry Volume K Tons Forecast, by Region 2020 & 2033

- Table 5: Global Residential Battery Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Residential Battery Industry Volume K Tons Forecast, by Type 2020 & 2033

- Table 7: Global Residential Battery Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 8: Global Residential Battery Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 9: Global Residential Battery Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 10: Global Residential Battery Industry Volume K Tons Forecast, by Type 2020 & 2033

- Table 11: Global Residential Battery Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Global Residential Battery Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 13: Global Residential Battery Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 14: Global Residential Battery Industry Volume K Tons Forecast, by Type 2020 & 2033

- Table 15: Global Residential Battery Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Global Residential Battery Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 17: Global Residential Battery Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Global Residential Battery Industry Volume K Tons Forecast, by Type 2020 & 2033

- Table 19: Global Residential Battery Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 20: Global Residential Battery Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 21: Global Residential Battery Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 22: Global Residential Battery Industry Volume K Tons Forecast, by Type 2020 & 2033

- Table 23: Global Residential Battery Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 24: Global Residential Battery Industry Volume K Tons Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Residential Battery Industry?

The projected CAGR is approximately 10.9%.

2. Which companies are prominent players in the Residential Battery Industry?

Key companies in the market include BYD Co Ltd, Amara Raja Batteries Ltd, Samsung SDI Co Ltd, Luminous Power Technologies Pvt Ltd, LG Energy Solution Ltd, FIMER SpA, Siemens AG, Tesla Inc, Delta Electronics Ltd, NEC Corporation, Energizer Holding Inc, Duracell Inc, Panasonic Corporation.

3. What are the main segments of the Residential Battery Industry?

The market segments include Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 17.4 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Investments in Water Treatment by Developing Countries4.; Growing Demand for the Various End-Use Sectors.

6. What are the notable trends driving market growth?

Lithium-ion Battery Segment Expected to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Availability of Cheap and Alternative Pumps.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Residential Battery Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Residential Battery Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Residential Battery Industry?

To stay informed about further developments, trends, and reports in the Residential Battery Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence