Key Insights

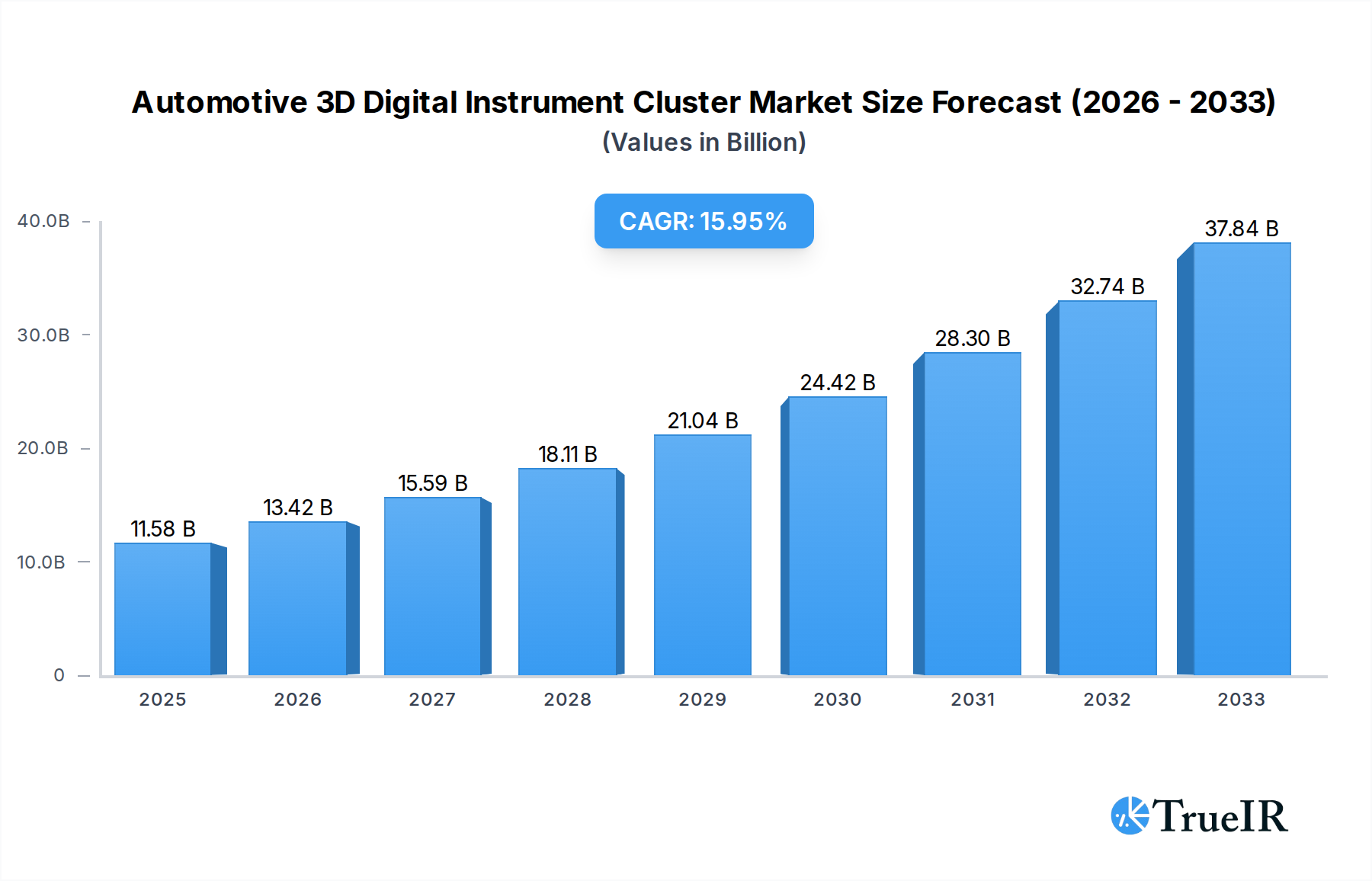

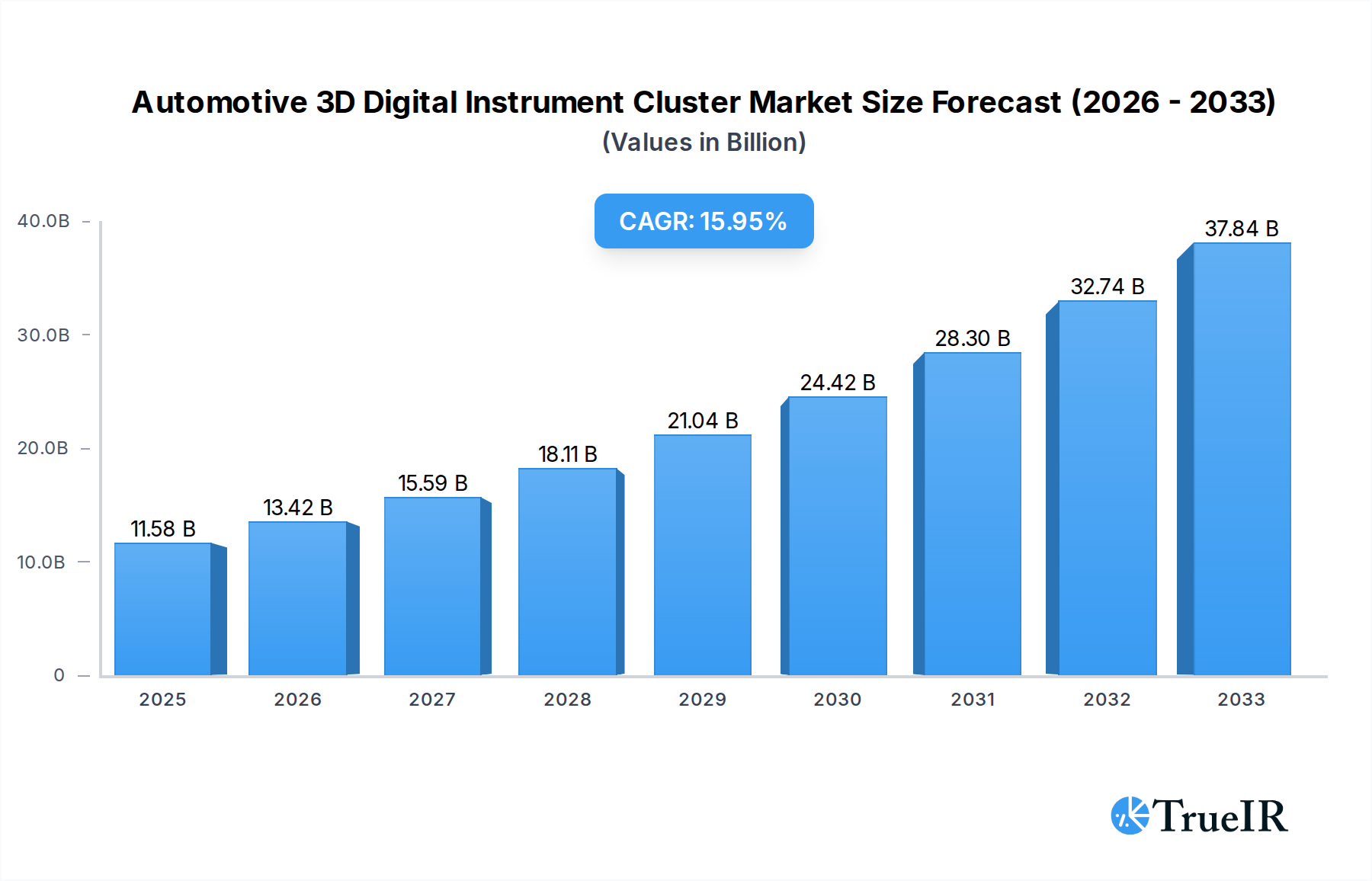

The global Automotive 3D Digital Instrument Cluster market is experiencing robust growth, driven by increasing demand for advanced driver-assistance systems (ADAS) and enhanced in-car digital experiences. The market size is projected to reach USD 11.58 billion in 2025, fueled by a compelling Compound Annual Growth Rate (CAGR) of 15.97% through 2033. This surge is primarily attributed to the growing adoption of sophisticated infotainment systems, the rising complexity of vehicle information display, and the continuous innovation in display technologies. As consumers increasingly expect personalized and immersive driving environments, 3D digital instrument clusters offer a premium visual appeal and improved functionality, making them a key differentiator for automotive manufacturers. The integration of AI and machine learning further enhances the capabilities of these clusters, enabling features like predictive analytics and context-aware information delivery, thereby pushing market expansion.

Automotive 3D Digital Instrument Cluster Market Size (In Billion)

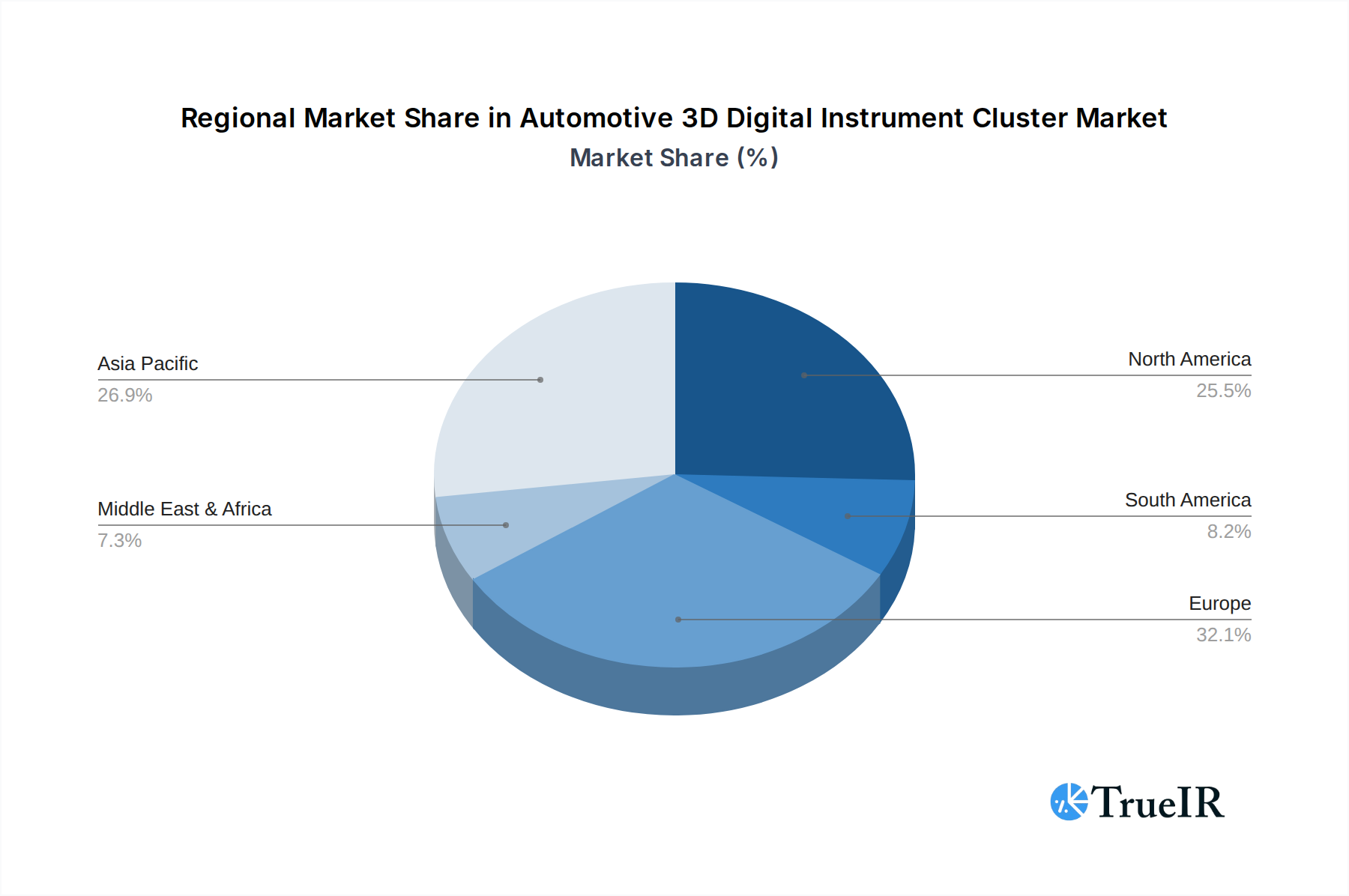

The market segmentation by application highlights a strong demand in passenger cars, driven by consumer preferences for advanced features and a desire for a technologically advanced cabin. Commercial vehicles are also witnessing growing adoption, as fleet managers recognize the potential for improved driver safety and operational efficiency through better data visualization. In terms of display size, segments ranging from 5-8 inches to above 11 inches are all poised for significant growth, catering to diverse vehicle models and design philosophies. Leading players such as Bosch, Continental, Delphi, Visteon, Magneti Marelli, and Nvidia are actively investing in research and development to offer cutting-edge solutions. Geographically, Asia Pacific, led by China and India, is expected to be a dominant region due to its large automotive production base and the rapid adoption of new technologies. North America and Europe also represent significant markets, driven by stringent safety regulations and a strong consumer inclination towards premium automotive features.

Automotive 3D Digital Instrument Cluster Company Market Share

This in-depth report provides a dynamic, SEO-optimized analysis of the global Automotive 3D Digital Instrument Cluster market. Leveraging high-volume keywords and detailed insights, this report is essential for industry stakeholders seeking to understand market dynamics, competitive landscapes, and future growth trajectories. The study period spans from 2019 to 2033, with a base year of 2025 and a forecast period of 2025–2033. Historical data from 2019–2024 is also included. We project the market to reach hundreds of billions in valuation by 2033, driven by technological advancements and evolving consumer demands.

Automotive 3D Digital Instrument Cluster Market Structure & Competitive Landscape

The global Automotive 3D Digital Instrument Cluster market exhibits a moderately concentrated structure, with leading players like Bosch, Continental, Delphi, Visteon, Magneti Marelli, and Nvidia holding significant market share. Innovation drivers are primarily fueled by advancements in display technologies, augmented reality (AR) integration, and sophisticated graphics processing capabilities, largely propelled by companies like Nvidia. Regulatory impacts are increasingly influencing the adoption of advanced safety features and user interface standards, contributing to market evolution. Product substitutes, such as traditional analog clusters or simpler digital displays, are steadily losing ground as the demand for immersive and feature-rich experiences grows. End-user segmentation primarily focuses on passenger cars and commercial vehicles, with passenger cars currently dominating the market due to higher production volumes and consumer willingness for premium features. Mergers and acquisitions (M&A) trends indicate strategic consolidations aimed at enhancing technological portfolios and expanding geographical reach. The market is expected to witness a concentration ratio of approximately 60% among the top five players by 2028, with an estimated billions in M&A deals over the forecast period.

Automotive 3D Digital Instrument Cluster Market Trends & Opportunities

The Automotive 3D Digital Instrument Cluster market is experiencing robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of over 15% from 2025 to 2033, reaching a market size of hundreds of billions by the end of the forecast period. This expansion is driven by a confluence of technological shifts, evolving consumer preferences, and increasing vehicle electrification. Advanced display technologies, including lenticular lenses and light field displays, are enabling true 3D visual experiences without the need for special glasses, significantly enhancing driver engagement and information delivery. The integration of augmented reality (AR) overlays for navigation, driver assistance systems (ADAS) alerts, and real-time vehicle diagnostics is a key trend, offering a more intuitive and safer driving experience. Consumer demand for premium, customizable, and information-rich in-cabin experiences is a significant driver, with drivers increasingly valuing connectivity, entertainment, and personalized interfaces. The rise of autonomous driving technologies further necessitates sophisticated instrument clusters capable of displaying complex environmental information and system status updates. The competitive dynamics are characterized by intense innovation, with established automotive suppliers collaborating with technology giants like Nvidia to develop cutting-edge solutions. Market penetration rates for 3D digital instrument clusters are expected to surge from approximately 30% in 2025 to over 70% by 2033, particularly in mid-range and premium vehicle segments. Emerging opportunities lie in the development of AI-powered adaptive interfaces that learn driver behavior and proactively display relevant information, as well as in the miniaturization and cost reduction of 3D display technologies to facilitate wider adoption in entry-level vehicles. The growing demand for sophisticated infotainment systems, coupled with the increasing sophistication of ADAS, is creating a fertile ground for the widespread adoption of 3D digital instrument clusters, promising a market valuation of hundreds of billions by the forecast period's end.

Dominant Markets & Segments in Automotive 3D Digital Instrument Cluster

The Passenger Car segment overwhelmingly dominates the Automotive 3D Digital Instrument Cluster market, accounting for an estimated 85% of the total market share in 2025, with projected revenues in the hundreds of billions. This dominance is attributed to higher production volumes of passenger vehicles globally and a strong consumer inclination towards advanced in-cabin technologies and premium features. Within the Passenger Car segment, the "Above 11 Inches" type of 3D digital instrument clusters is experiencing the fastest growth, driven by the trend towards larger, more integrated display architectures that encompass infotainment and digital cockpits. Countries like China, the United States, and Germany are the leading markets due to their robust automotive manufacturing bases, high per capita income, and early adoption of advanced automotive technologies. Key growth drivers in these regions include supportive government policies for vehicle safety and innovation, significant investments in automotive R&D, and a growing middle class with increasing disposable income.

Application: Passenger Car:

- Market Dominance: Expected to constitute over 85% of the market share by 2025.

- Growth Drivers: Increasing demand for advanced infotainment, ADAS integration, and premium cabin experiences.

- Technological Adoption: Higher penetration of sophisticated digital displays and interactive features.

Types: Above 11 Inches:

- Leading Segment: Experiencing the highest CAGR, driven by holistic digital cockpit designs.

- Key Features: Enables seamless integration of navigation, entertainment, and vehicle information.

- Consumer Preference: Enhances the perception of luxury and technological advancement in vehicles.

Leading Regions:

- Asia-Pacific (particularly China): Strong manufacturing hub, rapid adoption of new technologies, and significant government support.

- North America (particularly USA): High consumer demand for advanced features and a strong presence of premium vehicle manufacturers.

- Europe (particularly Germany): Home to major automotive OEMs with a focus on innovation and stringent safety standards.

The Commercial Vehicle segment, while smaller, is also showing promising growth, driven by the increasing need for enhanced driver information, fleet management integration, and compliance with evolving safety regulations. The development of advanced telematics and driver monitoring systems within commercial vehicles is creating further opportunities for sophisticated digital instrument clusters, projected to contribute billions to the overall market by 2033.

Automotive 3D Digital Instrument Cluster Product Analysis

Automotive 3D digital instrument clusters represent a significant leap in human-machine interface (HMI) technology within vehicles. Product innovations are centered on creating immersive, intuitive, and highly customizable driver experiences. Key advancements include the seamless integration of augmented reality overlays for navigation and ADAS warnings, holographic display capabilities, and advanced graphics processing for realistic rendering of speed, RPM, and other critical information. The competitive advantage of these clusters lies in their ability to enhance driver safety by providing critical information more effectively and to elevate the overall in-cabin aesthetic and user experience. Companies are focusing on developing clusters that can dynamically adapt to different driving scenarios and driver preferences, offering a personalized and engaging interface that contributes to the perception of a higher-value vehicle. The market is witnessing the introduction of displays that offer stereoscopic 3D without the need for special eyewear, a significant technological feat.

Key Drivers, Barriers & Challenges in Automotive 3D Digital Instrument Cluster

Key Drivers:

- Technological Advancements: The continuous evolution of display technologies, augmented reality, and advanced graphics processing is a primary catalyst. Companies like Nvidia are instrumental in providing the processing power.

- Increasing Demand for Advanced In-Cabin Experiences: Consumers are seeking more engaging, personalized, and visually rich interfaces, akin to their smartphones and tablets.

- Growth of ADAS and Autonomous Driving: Sophisticated displays are crucial for conveying complex information from advanced driver-assistance systems and future autonomous driving functionalities.

- Vehicle Electrification: Electric vehicles often feature innovative digital cockpits that align with their futuristic appeal, driving the adoption of 3D clusters.

- Regulatory Push for Safety: Enhanced visibility of warnings and critical information through 3D displays can contribute to improved road safety, aligning with regulatory goals.

Barriers & Challenges:

- High Development and Manufacturing Costs: The sophisticated technology involved currently leads to higher costs compared to traditional instrument clusters, potentially impacting adoption in budget segments.

- Supply Chain Complexities: The reliance on specialized components and advanced manufacturing processes can lead to supply chain vulnerabilities and potential disruptions.

- Regulatory Harmonization: Ensuring that 3D display functionalities comply with varying international safety and usability standards can be a complex challenge.

- Driver Distraction Concerns: While designed to be intuitive, the complexity and visual richness of 3D displays require careful design to avoid driver distraction.

- Software Development and Integration: The integration of complex software for 3D rendering, AR overlays, and connectivity requires significant expertise and ongoing updates.

Growth Drivers in the Automotive 3D Digital Instrument Cluster Market

The primary growth drivers for the Automotive 3D Digital Instrument Cluster market are rooted in technological innovation, particularly the advancements in display technologies and augmented reality integration, enabling richer and more intuitive driver interfaces. The increasing consumer demand for premium and customizable in-cabin experiences, similar to their smartphone ecosystems, further fuels this growth. Furthermore, the proliferation of advanced driver-assistance systems (ADAS) and the trajectory towards autonomous driving necessitate more sophisticated displays capable of conveying a wealth of real-time information and warnings effectively. The electrification trend in the automotive industry also contributes significantly, as EV manufacturers often adopt advanced digital cockpits to complement their futuristic vehicle designs.

Challenges Impacting Automotive 3D Digital Instrument Cluster Growth

Despite the strong growth potential, the Automotive 3D Digital Instrument Cluster market faces several challenges. The high cost associated with the development and manufacturing of these advanced systems remains a significant barrier to widespread adoption, especially in entry-level and mid-range vehicles. Supply chain disruptions for specialized electronic components and display materials can impact production volumes and timelines. Furthermore, ensuring that the complex visual information presented on 3D displays does not lead to driver distraction requires meticulous design and rigorous testing, posing a design and regulatory hurdle. The need for continuous software updates and the potential for obsolescence also add to the lifecycle management challenges.

Key Players Shaping the Automotive 3D Digital Instrument Cluster Market

- Bosch

- Continental

- Delphi

- Visteon

- Magneti Marelli

- Nvidia

Significant Automotive 3D Digital Instrument Cluster Industry Milestones

- 2019: Introduction of advanced AR-HUD integration in premium passenger vehicles, hinting at future 3D cluster capabilities.

- 2020: Nvidia announces significant advancements in its DRIVE platform, enabling more powerful automotive graphics for digital cockpits.

- 2021: Major Tier-1 suppliers showcase near-production-ready lenticular 3D display technologies for instrument clusters.

- 2022: Increased focus on customizable and AI-driven interfaces within digital instrument clusters by leading OEMs.

- 2023: Growing adoption of larger, integrated digital cockpit displays incorporating 3D elements in new vehicle launches.

- 2024: Emergence of advanced light-field display technologies promising glasses-free 3D experiences gaining traction.

Future Outlook for Automotive 3D Digital Instrument Cluster Market

The future outlook for the Automotive 3D Digital Instrument Cluster market is exceptionally bright, with projected sustained growth fueled by continuous technological innovation and evolving consumer expectations for in-cabin experiences. The increasing integration of AI and machine learning will enable clusters to offer predictive information and highly personalized interfaces. As display technologies mature and manufacturing costs decrease, we anticipate broader adoption across all vehicle segments. The development of advanced AR functionalities will further enhance safety and navigation, making 3D digital instrument clusters an indispensable component of future vehicles, driving market potential into the hundreds of billions.

Automotive 3D Digital Instrument Cluster Segmentation

-

1. Application

- 1.1. Passenger Car

- 1.2. Commercial Vehicle

-

2. Types

- 2.1. 5 - 8 Inches

- 2.2. 9 - 11 Inches

- 2.3. Above 11 Inches

Automotive 3D Digital Instrument Cluster Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Automotive 3D Digital Instrument Cluster Regional Market Share

Geographic Coverage of Automotive 3D Digital Instrument Cluster

Automotive 3D Digital Instrument Cluster REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 15.97% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Automotive 3D Digital Instrument Cluster Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Passenger Car

- 5.1.2. Commercial Vehicle

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. 5 - 8 Inches

- 5.2.2. 9 - 11 Inches

- 5.2.3. Above 11 Inches

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Automotive 3D Digital Instrument Cluster Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Passenger Car

- 6.1.2. Commercial Vehicle

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. 5 - 8 Inches

- 6.2.2. 9 - 11 Inches

- 6.2.3. Above 11 Inches

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Automotive 3D Digital Instrument Cluster Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Passenger Car

- 7.1.2. Commercial Vehicle

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. 5 - 8 Inches

- 7.2.2. 9 - 11 Inches

- 7.2.3. Above 11 Inches

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Automotive 3D Digital Instrument Cluster Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Passenger Car

- 8.1.2. Commercial Vehicle

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. 5 - 8 Inches

- 8.2.2. 9 - 11 Inches

- 8.2.3. Above 11 Inches

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Automotive 3D Digital Instrument Cluster Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Passenger Car

- 9.1.2. Commercial Vehicle

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. 5 - 8 Inches

- 9.2.2. 9 - 11 Inches

- 9.2.3. Above 11 Inches

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Automotive 3D Digital Instrument Cluster Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Passenger Car

- 10.1.2. Commercial Vehicle

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. 5 - 8 Inches

- 10.2.2. 9 - 11 Inches

- 10.2.3. Above 11 Inches

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Bosch

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Continental

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Delphi

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Visteon

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Magneti Marelli

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Nvidia

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.1 Bosch

List of Figures

- Figure 1: Global Automotive 3D Digital Instrument Cluster Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Automotive 3D Digital Instrument Cluster Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Automotive 3D Digital Instrument Cluster Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Automotive 3D Digital Instrument Cluster Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Automotive 3D Digital Instrument Cluster Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Automotive 3D Digital Instrument Cluster Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Automotive 3D Digital Instrument Cluster Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Automotive 3D Digital Instrument Cluster Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Automotive 3D Digital Instrument Cluster Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Automotive 3D Digital Instrument Cluster Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Automotive 3D Digital Instrument Cluster Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Automotive 3D Digital Instrument Cluster Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Automotive 3D Digital Instrument Cluster Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Automotive 3D Digital Instrument Cluster Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Automotive 3D Digital Instrument Cluster Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Automotive 3D Digital Instrument Cluster Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Automotive 3D Digital Instrument Cluster Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Automotive 3D Digital Instrument Cluster Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Automotive 3D Digital Instrument Cluster Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Automotive 3D Digital Instrument Cluster Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Automotive 3D Digital Instrument Cluster Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Automotive 3D Digital Instrument Cluster Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Automotive 3D Digital Instrument Cluster Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Automotive 3D Digital Instrument Cluster Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Automotive 3D Digital Instrument Cluster Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Automotive 3D Digital Instrument Cluster Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Automotive 3D Digital Instrument Cluster Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Automotive 3D Digital Instrument Cluster Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Automotive 3D Digital Instrument Cluster Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Automotive 3D Digital Instrument Cluster Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Automotive 3D Digital Instrument Cluster Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automotive 3D Digital Instrument Cluster Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Automotive 3D Digital Instrument Cluster Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Automotive 3D Digital Instrument Cluster Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Automotive 3D Digital Instrument Cluster Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Automotive 3D Digital Instrument Cluster Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Automotive 3D Digital Instrument Cluster Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Automotive 3D Digital Instrument Cluster Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Automotive 3D Digital Instrument Cluster Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Automotive 3D Digital Instrument Cluster Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Automotive 3D Digital Instrument Cluster Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Automotive 3D Digital Instrument Cluster Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Automotive 3D Digital Instrument Cluster Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Automotive 3D Digital Instrument Cluster Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Automotive 3D Digital Instrument Cluster Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Automotive 3D Digital Instrument Cluster Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Automotive 3D Digital Instrument Cluster Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Automotive 3D Digital Instrument Cluster Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Automotive 3D Digital Instrument Cluster Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Automotive 3D Digital Instrument Cluster Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Automotive 3D Digital Instrument Cluster Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Automotive 3D Digital Instrument Cluster Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Automotive 3D Digital Instrument Cluster Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Automotive 3D Digital Instrument Cluster Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Automotive 3D Digital Instrument Cluster Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Automotive 3D Digital Instrument Cluster Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Automotive 3D Digital Instrument Cluster Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Automotive 3D Digital Instrument Cluster Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Automotive 3D Digital Instrument Cluster Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Automotive 3D Digital Instrument Cluster Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Automotive 3D Digital Instrument Cluster Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Automotive 3D Digital Instrument Cluster Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Automotive 3D Digital Instrument Cluster Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Automotive 3D Digital Instrument Cluster Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Automotive 3D Digital Instrument Cluster Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Automotive 3D Digital Instrument Cluster Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Automotive 3D Digital Instrument Cluster Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Automotive 3D Digital Instrument Cluster Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Automotive 3D Digital Instrument Cluster Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Automotive 3D Digital Instrument Cluster Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Automotive 3D Digital Instrument Cluster Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Automotive 3D Digital Instrument Cluster Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Automotive 3D Digital Instrument Cluster Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Automotive 3D Digital Instrument Cluster Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Automotive 3D Digital Instrument Cluster Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Automotive 3D Digital Instrument Cluster Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Automotive 3D Digital Instrument Cluster Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive 3D Digital Instrument Cluster?

The projected CAGR is approximately 15.97%.

2. Which companies are prominent players in the Automotive 3D Digital Instrument Cluster?

Key companies in the market include Bosch, Continental, Delphi, Visteon, Magneti Marelli, Nvidia.

3. What are the main segments of the Automotive 3D Digital Instrument Cluster?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 11.58 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive 3D Digital Instrument Cluster," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive 3D Digital Instrument Cluster report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive 3D Digital Instrument Cluster?

To stay informed about further developments, trends, and reports in the Automotive 3D Digital Instrument Cluster, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence