Key Insights

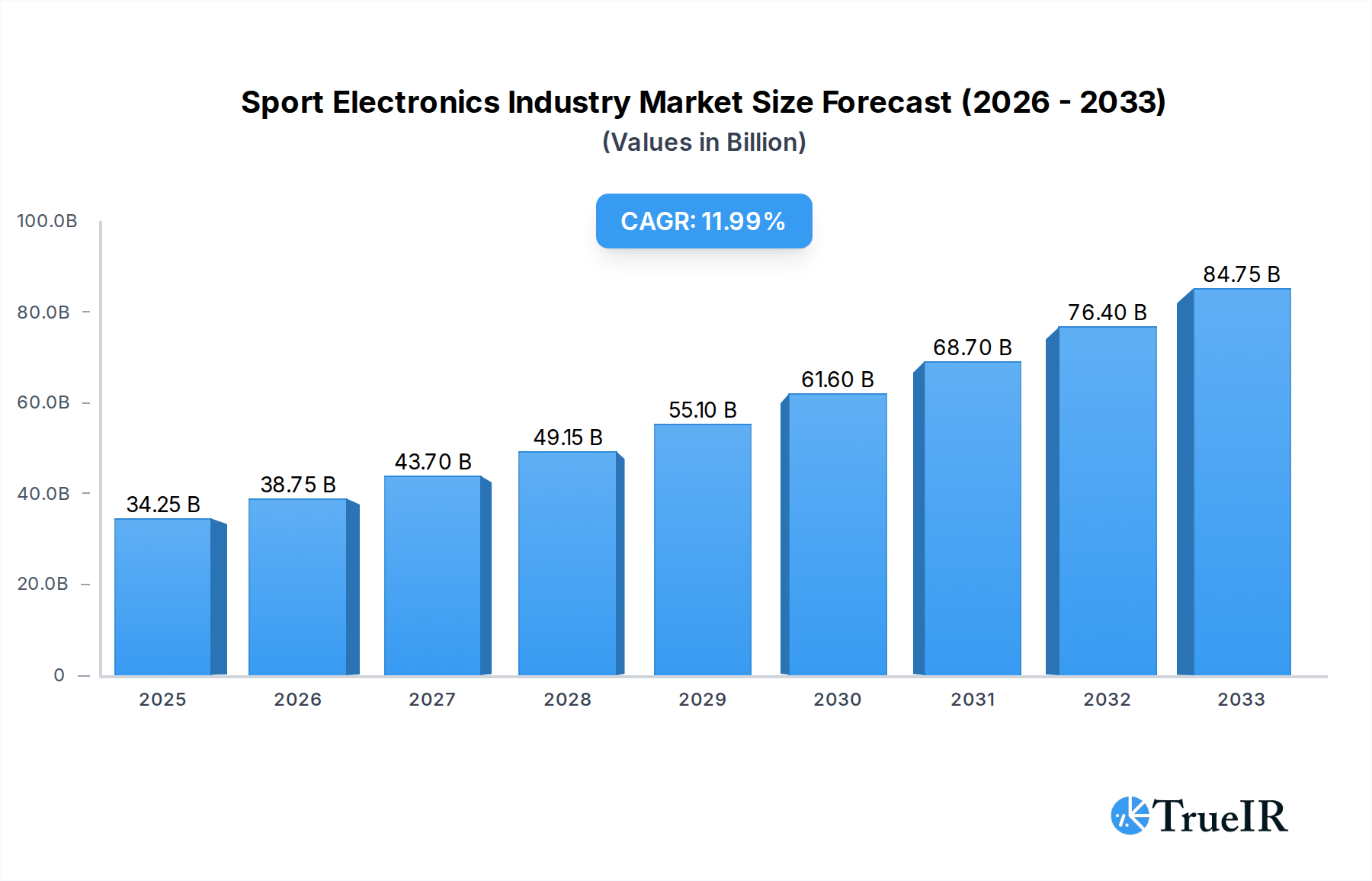

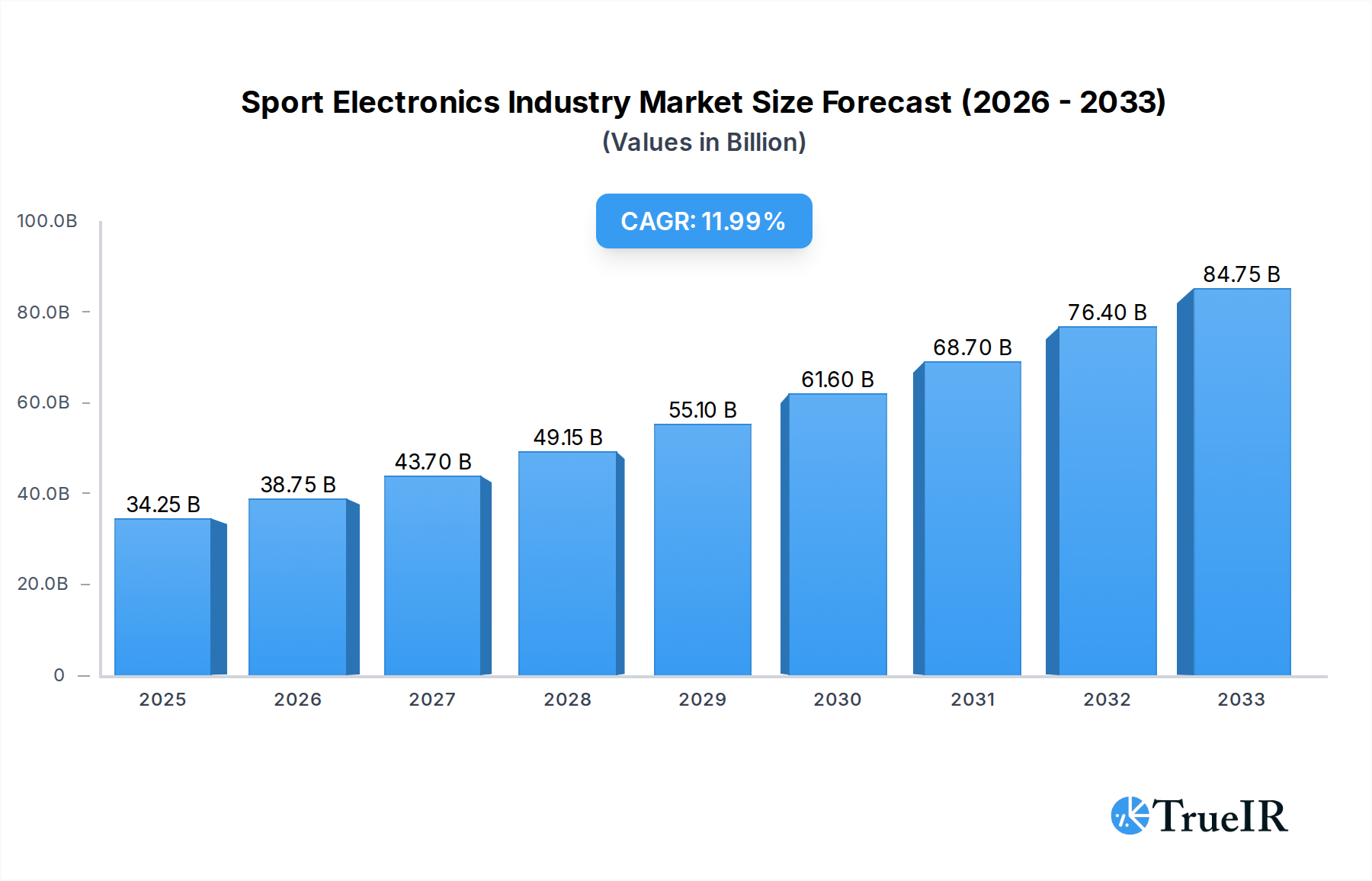

The global Sport Electronics market is poised for substantial expansion, projected to reach USD 34.25 billion by 2025, driven by a robust CAGR of 14.9% throughout the forecast period of 2025-2033. This remarkable growth is primarily fueled by the increasing adoption of wearable devices, including pedometers, activity monitors, and advanced fitness and heart rate monitors, by health-conscious consumers and professional athletes alike. The burgeoning trend of personalized fitness and performance tracking, coupled with significant technological advancements in sensor technology and data analytics, is further propelling market demand. Furthermore, the integration of smart fabrics into sportswear and the development of sophisticated standalone devices like cycling computers and high-resolution cameras are creating new avenues for market penetration and revenue generation. The market is witnessing a paradigm shift towards connected ecosystems, where devices seamlessly communicate to provide comprehensive insights into an individual's physical well-being and athletic performance.

Sport Electronics Industry Market Size (In Billion)

This dynamic market landscape is characterized by a healthy competitive environment, with major players like Apple Inc., Garmin Ltd., and Nike Inc. continually innovating to capture market share. The report highlights key market segments, including a strong emphasis on Wearable Devices, which are expected to dominate due to their convenience and advanced features. Standalone Devices also represent a significant segment, catering to niche sports and specific training needs. While the market benefits from widespread consumer interest in health and fitness, potential restraints such as the high cost of advanced devices and concerns over data privacy could influence adoption rates in certain demographics. However, the overall outlook remains exceptionally positive, with continuous innovation and the growing global emphasis on proactive health management acting as significant catalysts for sustained growth in the sport electronics industry.

Sport Electronics Industry Company Market Share

Here is a dynamic, SEO-optimized report description for the Sport Electronics Industry, designed for immediate use and maximum impact.

Sport Electronics Industry Market Structure & Competitive Landscape

The global Sport Electronics Industry is characterized by a dynamic and evolving market structure, marked by significant innovation and increasing competition. The market concentration varies across segments, with dominant players like Apple Inc, Garmin Ltd, and Nike Inc wielding considerable influence, particularly in the wearable devices sector. Key innovation drivers include the relentless pursuit of enhanced performance tracking, personalized health insights, and seamless user experiences. Regulatory impacts are becoming more pronounced, with data privacy (e.g., GDPR, CCPA) and product safety standards influencing product development and market entry strategies. Product substitutes, while present in lower-tech alternatives, are increasingly challenged by the advanced capabilities and integrated ecosystems offered by sport electronics. End-user segmentation spans from elite athletes seeking performance optimization to casual fitness enthusiasts and health-conscious individuals. Mergers & Acquisitions (M&A) trends indicate a strategic consolidation, with larger tech companies acquiring innovative startups to expand their portfolios and market reach. For instance, the acquisition of Fitbit by Google, though pending specific regulatory approvals, highlights this trend. The estimated M&A volume in the sport electronics sector is projected to be in the billions of dollars annually, reflecting significant investment and strategic realignment. The competitive landscape is fiercely contested, with a blend of established giants and agile startups vying for market share through continuous product development and strategic partnerships. This intense competition fosters rapid technological advancements and a focus on delivering superior value propositions to consumers.

Sport Electronics Industry Market Trends & Opportunities

The Sport Electronics Industry is experiencing a period of exponential growth, driven by a confluence of technological advancements, shifting consumer preferences, and a burgeoning health and wellness consciousness. The global market size is projected to reach hundreds of billions of dollars by 2033, with a Compound Annual Growth Rate (CAGR) of approximately xx% during the forecast period of 2025–2033. This robust expansion is underpinned by a significant increase in market penetration rates across developed and developing economies, as consumers increasingly embrace technology to monitor their fitness, enhance their athletic performance, and proactively manage their well-being.

Technological shifts are at the forefront of this growth. The miniaturization of sensors, advancements in AI and machine learning for data analysis, and the integration of sophisticated biometric tracking capabilities are revolutionizing the functionalities of sport electronics. From real-time gait analysis and recovery metrics for runners to advanced sleep tracking and stress monitoring for everyday users, the depth and accuracy of insights provided are continuously improving. The development of smart fabrics, embedded with conductive yarns and sensors, represents a significant frontier, promising to create truly integrated wearable solutions that blend seamlessly with athletic apparel.

Consumer preferences are evolving rapidly. There is a growing demand for personalized data-driven insights that go beyond basic step counting. Users are seeking actionable recommendations for training, nutrition, and recovery, tailored to their individual physiology and goals. The rise of the "quantified self" movement, coupled with an increased awareness of the long-term benefits of an active lifestyle, is fueling demand for devices that offer comprehensive health monitoring. Furthermore, the integration of these devices into broader digital health ecosystems, including telehealth platforms and personalized coaching apps, is enhancing their appeal and utility.

Competitive dynamics are intensifying, with established players like Adidas AG, Polar Electro Oy, Giant Manufacturing Co Ltd, Zepp US Inc, Garmin Ltd, SZ DJI Technology Co Ltd, Fitbit Inc, Catapult Sports Pty Ltd, Apple Inc, Nike Inc, and Under Armour continuously innovating and expanding their product lines. Emerging players, particularly in niche areas like smart fabrics (e.g., StretchSense Ltd), are also carving out significant market share. Strategic partnerships between technology companies, sports apparel brands, and health service providers are becoming increasingly common, aimed at creating comprehensive solutions and expanding market reach. The convergence of fitness, health, and technology is creating a fertile ground for sustained growth and innovation in the Sport Electronics Industry.

Dominant Markets & Segments in Sport Electronics Industry

The Sport Electronics Industry is witnessing robust growth across its diverse segments, with Wearable Devices emerging as the dominant category, accounting for a significant portion of the market's value. Within wearable devices, Fitness and Heart Rate Monitors are experiencing particularly strong demand, driven by their comprehensive health tracking capabilities and widespread adoption across various fitness levels. The market is further segmented into:

Wearable Devices:

- Pedometers & Activity Monitors: These foundational devices continue to appeal to a broad consumer base for basic activity tracking, with embedded GPS and advanced sensor technology enhancing their appeal.

- Smart Fabrics: This is a rapidly growing segment, offering seamless integration of sensors into clothing for highly accurate performance and physiological data collection, appealing to both elite athletes and tech-savvy consumers.

- Fitness and Heart Rate Monitors: These remain a cornerstone of the market, offering sophisticated insights into cardiovascular health, training intensity, and recovery.

- Other Wearable Devices: This encompasses a range of innovative products like smart rings, hearables with health tracking functionalities, and advanced sports-specific wearables.

Standalone Devices:

- Electronics Scales: Smart scales that offer body composition analysis and sync with health apps are seeing increased adoption.

- Cameras: Action cameras and specialized sports cameras continue to be relevant for capturing high-definition content during activities.

- Cycling Computers: These devices, essential for serious cyclists, are integrating more advanced navigation, performance metrics, and connectivity features.

- Other Standalone Devices: This includes a variety of niche electronics catering to specific sports and activities.

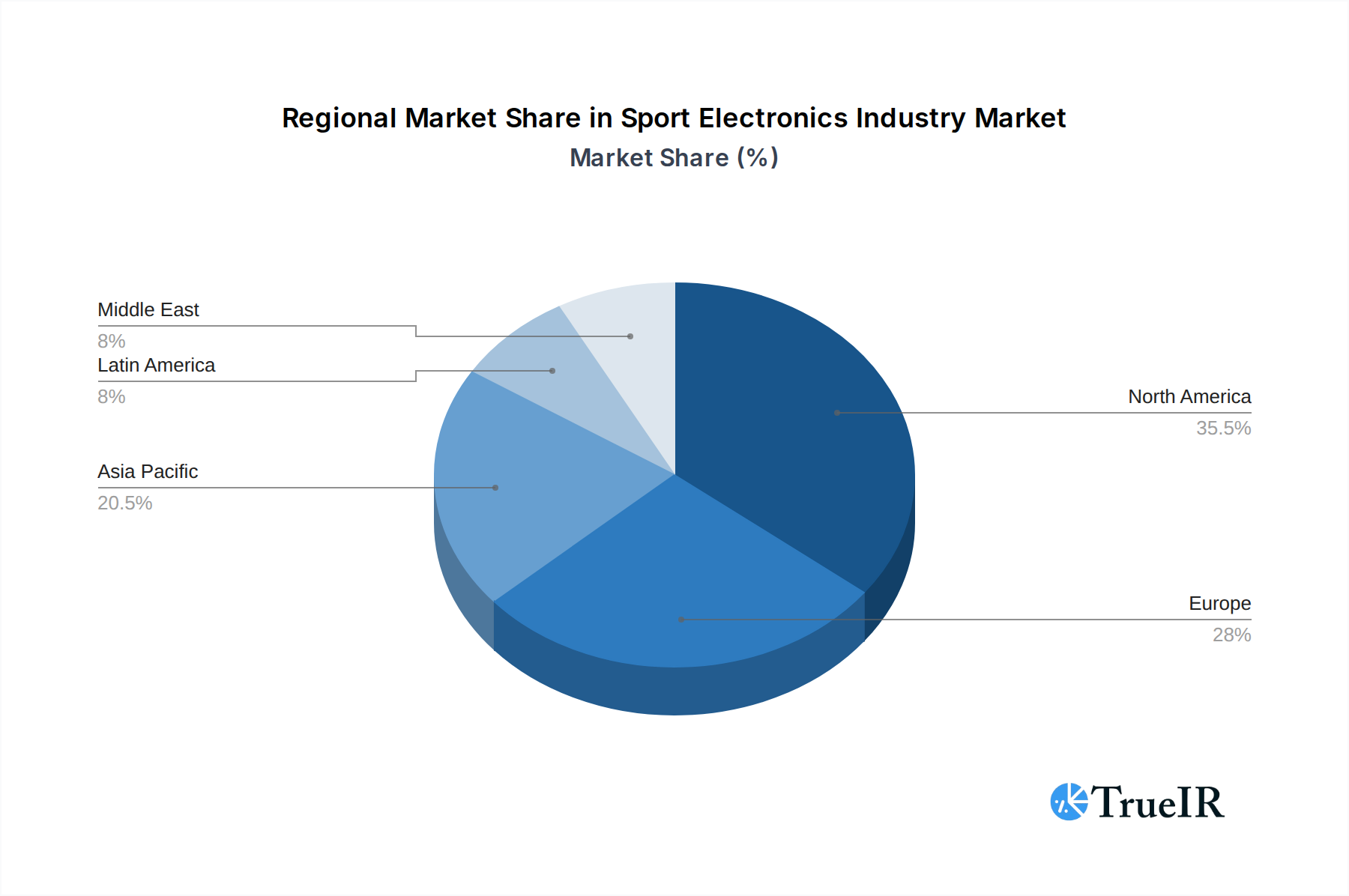

Geographically, North America continues to lead the market, driven by high disposable incomes, a strong sports culture, and early adoption of advanced technologies. The United States is a key country within this region, with a mature market for both fitness and performance-oriented sport electronics. However, Asia Pacific is projected to exhibit the fastest growth, fueled by increasing health awareness, a burgeoning middle class, and rising disposable incomes in countries like China and India. Government initiatives promoting health and fitness, coupled with the increasing availability of affordable yet feature-rich sport electronics, are significant growth drivers in this region. Infrastructure development, including the availability of high-speed internet for seamless data synchronization, also plays a crucial role in market expansion. Policies that encourage technological innovation and promote digital health adoption further bolster market dominance in leading regions.

Sport Electronics Industry Product Analysis

The Sport Electronics Industry is defined by continuous product innovation, focusing on enhanced accuracy, user experience, and holistic health insights. Key advancements include the integration of multi-frequency GPS for superior location tracking, advanced optical heart rate sensors, and non-invasive blood oxygen monitoring. Smart fabrics are revolutionizing apparel by embedding sensors directly into textiles, offering unobtrusive and highly precise data collection for biometrics, movement analysis, and even temperature regulation. The competitive advantage lies in creating devices that offer actionable data, personalized coaching, and seamless integration into users' daily lives, moving beyond mere data capture to deliver genuine performance and well-being enhancements.

Key Drivers, Barriers & Challenges in Sport Electronics Industry

Key Drivers, Barriers & Challenges in Sport Electronics Industry

The Sport Electronics Industry is propelled by several key drivers, including rapid technological advancements in sensor technology and AI, leading to more accurate and insightful data. The growing global health and wellness trend, coupled with increased participation in sports and fitness activities, is a significant market booster. Government initiatives promoting active lifestyles and technological adoption further fuel growth. Moreover, the increasing demand for personalized fitness experiences and data-driven performance optimization among both amateur and professional athletes is creating substantial market opportunities.

However, the industry faces several challenges. High research and development costs associated with cutting-edge technologies can be a barrier. The increasing complexity of data privacy regulations (e.g., data breaches and compliance) poses a significant hurdle for companies. Supply chain disruptions, particularly for specialized electronic components, can impact production volumes and lead times, potentially leading to millions in lost revenue due to stockouts. Intense competition from both established brands and new entrants can lead to price wars and reduced profit margins, impacting the overall profitability of companies. The rapid pace of technological change also necessitates continuous investment in product updates, creating a challenge to maintain market relevance and profitability.

Growth Drivers in the Sport Electronics Industry Market

The Sport Electronics Industry's growth is primarily fueled by rapid technological advancements, particularly in miniaturized sensors, AI-driven analytics, and enhanced battery life, enabling more sophisticated and user-friendly devices. The global surge in health consciousness and active lifestyles is a major catalyst, with consumers increasingly investing in tools to monitor fitness and well-being. Government support for digital health initiatives and sports participation, alongside increasing disposable incomes in emerging economies, creates a fertile ground for market expansion. The demand for personalized training insights and data-driven performance optimization by athletes of all levels further drives innovation and adoption.

Challenges Impacting Sport Electronics Industry Growth

Regulatory complexities surrounding data privacy and security remain a significant challenge, requiring substantial compliance investments and potentially limiting data utilization. Supply chain vulnerabilities, exacerbated by global geopolitical events and component shortages, can lead to production delays and increased costs, impacting market availability and revenue. Intense market competition from established giants and agile startups drives down profit margins and necessitates continuous, costly innovation. Furthermore, the rapid obsolescence of technology requires constant product development and marketing efforts, adding to the financial and operational pressures on companies within the sector.

Key Players Shaping the Sport Electronics Industry Market

- Adidas AG

- Polar Electro Oy

- Giant Manufacturing Co Ltd

- Zepp US Inc

- Garmin Ltd

- StretchSense Ltd

- SZ DJI Technology Co Ltd

- Fitbit Inc

- Catapult Sports Pty Ltd

- Apple Inc

- Nike Inc

- Under Armour

Significant Sport Electronics Industry Industry Milestones

- 2019: Launch of advanced GPS running watches with extended battery life and multi-band GPS by major manufacturers.

- 2020: Increased adoption of contactless payment features in smartwatches and fitness trackers.

- 2021: Significant advancements in smart fabric technology, enabling more integrated and discreet biometric monitoring.

- 2022: Introduction of sophisticated sleep tracking algorithms and recovery metrics across a wider range of wearable devices.

- 2023: Growing integration of AI-powered coaching and personalized training recommendations in sports electronics.

- 2024: Enhanced focus on mental wellness tracking, including stress monitoring and mindfulness features in wearable devices.

Future Outlook for Sport Electronics Industry Market

The future outlook for the Sport Electronics Industry remains exceptionally bright, driven by an ongoing convergence of technology, health, and performance. Strategic opportunities lie in the continued integration of AI for hyper-personalized coaching and predictive health analytics, as well as the expansion of smart fabric applications beyond athletic wear. The market potential is immense, with anticipated growth in connected fitness ecosystems, remote health monitoring solutions, and virtual reality-enhanced training experiences. The industry is poised for sustained expansion, with billions in future market value expected as innovation continues to redefine how individuals engage with their physical activity and overall well-being.

Sport Electronics Industry Segmentation

-

1. Product Type

-

1.1. Wearable Devices

- 1.1.1. Pedometers

- 1.1.2. Activity Monitors

- 1.1.3. Smart Fabrics

- 1.1.4. Fitness and Heart Rate Monitors

- 1.1.5. Other Wearable Devices

-

1.2. Standalone Devices

- 1.2.1. Electronics Scales

- 1.2.2. Cameras

- 1.2.3. Cycling Computers

- 1.2.4. Other Standalone Devices

-

1.1. Wearable Devices

Sport Electronics Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East

Sport Electronics Industry Regional Market Share

Geographic Coverage of Sport Electronics Industry

Sport Electronics Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 14.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Wearable Devices

- 5.1.1.1. Pedometers

- 5.1.1.2. Activity Monitors

- 5.1.1.3. Smart Fabrics

- 5.1.1.4. Fitness and Heart Rate Monitors

- 5.1.1.5. Other Wearable Devices

- 5.1.2. Standalone Devices

- 5.1.2.1. Electronics Scales

- 5.1.2.2. Cameras

- 5.1.2.3. Cycling Computers

- 5.1.2.4. Other Standalone Devices

- 5.1.1. Wearable Devices

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. Europe

- 5.2.3. Asia Pacific

- 5.2.4. Latin America

- 5.2.5. Middle East

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Global Sport Electronics Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Wearable Devices

- 6.1.1.1. Pedometers

- 6.1.1.2. Activity Monitors

- 6.1.1.3. Smart Fabrics

- 6.1.1.4. Fitness and Heart Rate Monitors

- 6.1.1.5. Other Wearable Devices

- 6.1.2. Standalone Devices

- 6.1.2.1. Electronics Scales

- 6.1.2.2. Cameras

- 6.1.2.3. Cycling Computers

- 6.1.2.4. Other Standalone Devices

- 6.1.1. Wearable Devices

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. North America Sport Electronics Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Wearable Devices

- 7.1.1.1. Pedometers

- 7.1.1.2. Activity Monitors

- 7.1.1.3. Smart Fabrics

- 7.1.1.4. Fitness and Heart Rate Monitors

- 7.1.1.5. Other Wearable Devices

- 7.1.2. Standalone Devices

- 7.1.2.1. Electronics Scales

- 7.1.2.2. Cameras

- 7.1.2.3. Cycling Computers

- 7.1.2.4. Other Standalone Devices

- 7.1.1. Wearable Devices

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. Europe Sport Electronics Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Wearable Devices

- 8.1.1.1. Pedometers

- 8.1.1.2. Activity Monitors

- 8.1.1.3. Smart Fabrics

- 8.1.1.4. Fitness and Heart Rate Monitors

- 8.1.1.5. Other Wearable Devices

- 8.1.2. Standalone Devices

- 8.1.2.1. Electronics Scales

- 8.1.2.2. Cameras

- 8.1.2.3. Cycling Computers

- 8.1.2.4. Other Standalone Devices

- 8.1.1. Wearable Devices

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Asia Pacific Sport Electronics Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Wearable Devices

- 9.1.1.1. Pedometers

- 9.1.1.2. Activity Monitors

- 9.1.1.3. Smart Fabrics

- 9.1.1.4. Fitness and Heart Rate Monitors

- 9.1.1.5. Other Wearable Devices

- 9.1.2. Standalone Devices

- 9.1.2.1. Electronics Scales

- 9.1.2.2. Cameras

- 9.1.2.3. Cycling Computers

- 9.1.2.4. Other Standalone Devices

- 9.1.1. Wearable Devices

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. Latin America Sport Electronics Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 10.1.1. Wearable Devices

- 10.1.1.1. Pedometers

- 10.1.1.2. Activity Monitors

- 10.1.1.3. Smart Fabrics

- 10.1.1.4. Fitness and Heart Rate Monitors

- 10.1.1.5. Other Wearable Devices

- 10.1.2. Standalone Devices

- 10.1.2.1. Electronics Scales

- 10.1.2.2. Cameras

- 10.1.2.3. Cycling Computers

- 10.1.2.4. Other Standalone Devices

- 10.1.1. Wearable Devices

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 11. Middle East Sport Electronics Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 11.1.1. Wearable Devices

- 11.1.1.1. Pedometers

- 11.1.1.2. Activity Monitors

- 11.1.1.3. Smart Fabrics

- 11.1.1.4. Fitness and Heart Rate Monitors

- 11.1.1.5. Other Wearable Devices

- 11.1.2. Standalone Devices

- 11.1.2.1. Electronics Scales

- 11.1.2.2. Cameras

- 11.1.2.3. Cycling Computers

- 11.1.2.4. Other Standalone Devices

- 11.1.1. Wearable Devices

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Adidas AG

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Polar Electro Oy

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Giant Manufacturing Co Ltd

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Zepp US Inc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Garmin Ltd

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 StretchSense Ltd

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 SZ DJI Technology Co Ltd

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Fitbit Inc

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Catapult Sports Pty Ltd

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Apple Inc

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Nike Inc

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Under Armour

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 Adidas AG

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Sport Electronics Industry Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Sport Electronics Industry Revenue (undefined), by Product Type 2025 & 2033

- Figure 3: North America Sport Electronics Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 4: North America Sport Electronics Industry Revenue (undefined), by Country 2025 & 2033

- Figure 5: North America Sport Electronics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: Europe Sport Electronics Industry Revenue (undefined), by Product Type 2025 & 2033

- Figure 7: Europe Sport Electronics Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 8: Europe Sport Electronics Industry Revenue (undefined), by Country 2025 & 2033

- Figure 9: Europe Sport Electronics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Asia Pacific Sport Electronics Industry Revenue (undefined), by Product Type 2025 & 2033

- Figure 11: Asia Pacific Sport Electronics Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 12: Asia Pacific Sport Electronics Industry Revenue (undefined), by Country 2025 & 2033

- Figure 13: Asia Pacific Sport Electronics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Latin America Sport Electronics Industry Revenue (undefined), by Product Type 2025 & 2033

- Figure 15: Latin America Sport Electronics Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 16: Latin America Sport Electronics Industry Revenue (undefined), by Country 2025 & 2033

- Figure 17: Latin America Sport Electronics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Middle East Sport Electronics Industry Revenue (undefined), by Product Type 2025 & 2033

- Figure 19: Middle East Sport Electronics Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 20: Middle East Sport Electronics Industry Revenue (undefined), by Country 2025 & 2033

- Figure 21: Middle East Sport Electronics Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Sport Electronics Industry Revenue undefined Forecast, by Product Type 2020 & 2033

- Table 2: Global Sport Electronics Industry Revenue undefined Forecast, by Region 2020 & 2033

- Table 3: Global Sport Electronics Industry Revenue undefined Forecast, by Product Type 2020 & 2033

- Table 4: Global Sport Electronics Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 5: Global Sport Electronics Industry Revenue undefined Forecast, by Product Type 2020 & 2033

- Table 6: Global Sport Electronics Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: Global Sport Electronics Industry Revenue undefined Forecast, by Product Type 2020 & 2033

- Table 8: Global Sport Electronics Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 9: Global Sport Electronics Industry Revenue undefined Forecast, by Product Type 2020 & 2033

- Table 10: Global Sport Electronics Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 11: Global Sport Electronics Industry Revenue undefined Forecast, by Product Type 2020 & 2033

- Table 12: Global Sport Electronics Industry Revenue undefined Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Sport Electronics Industry?

The projected CAGR is approximately 14.9%.

2. Which companies are prominent players in the Sport Electronics Industry?

Key companies in the market include Adidas AG, Polar Electro Oy, Giant Manufacturing Co Ltd , Zepp US Inc, Garmin Ltd, StretchSense Ltd, SZ DJI Technology Co Ltd, Fitbit Inc, Catapult Sports Pty Ltd, Apple Inc, Nike Inc, Under Armour.

3. What are the main segments of the Sport Electronics Industry?

The market segments include Product Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

; Technological Advancements in Wearable Sports Devices; Rising Demand for Round-The-Clock Monitoring.

6. What are the notable trends driving market growth?

Smartwatch is Expected to Register a Significant Growth.

7. Are there any restraints impacting market growth?

; High Cost of Wearable Devices.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Sport Electronics Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Sport Electronics Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Sport Electronics Industry?

To stay informed about further developments, trends, and reports in the Sport Electronics Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence