Key Insights

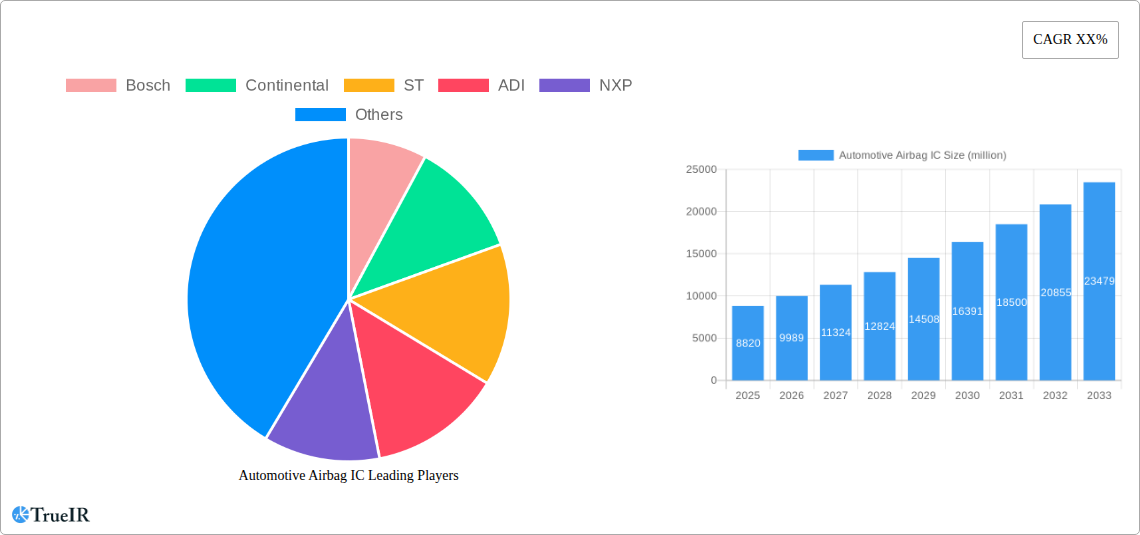

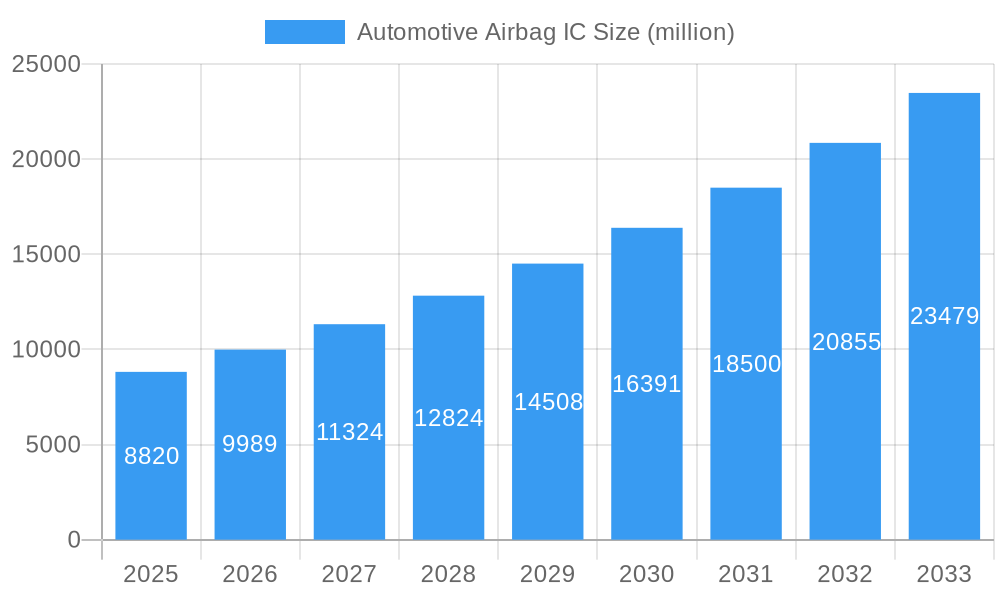

The global Automotive Airbag IC market is poised for significant expansion, projected to reach USD 8.82 billion in 2025. This robust growth is fueled by a remarkable Compound Annual Growth Rate (CAGR) of 13.79% during the forecast period of 2025-2033. A primary driver for this surge is the escalating demand for advanced safety features in vehicles, directly correlating with stricter government regulations worldwide mandating the inclusion of multiple airbags per vehicle. Passenger vehicles, in particular, represent a dominant application segment due to the sheer volume of production and the increasing consumer preference for enhanced personal safety. Integrated System Chips (ISCs) are gaining traction as they offer more compact, efficient, and cost-effective solutions compared to independent chips, streamlining the complex circuitry required for modern airbag deployment systems. The automotive industry's ongoing shift towards electric vehicles (EVs) and autonomous driving technologies also contributes, as these sophisticated systems necessitate advanced electronic components, including highly reliable airbag ICs.

Automotive Airbag IC Market Size (In Billion)

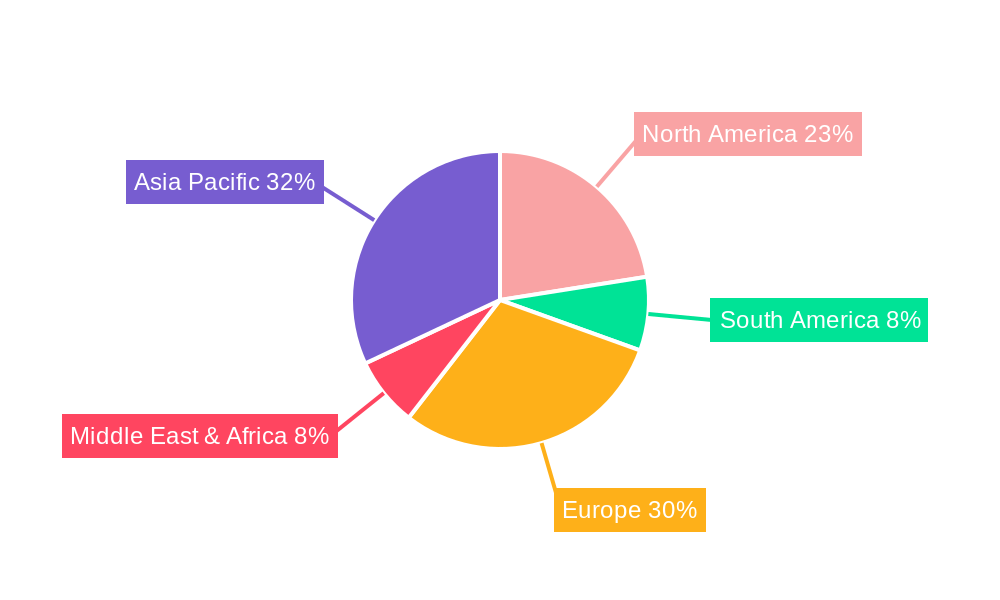

The market's impressive trajectory is supported by key trends such as the development of more intelligent airbag systems capable of adapting deployment based on occupant size, position, and impact severity. Furthermore, miniaturization of components and the integration of additional safety functionalities within a single IC are driving innovation. However, the market does face certain restraints, including the high research and development costs associated with developing next-generation safety technologies and the potential for supply chain disruptions, particularly for specialized semiconductor components. Geographically, Asia Pacific, led by China and India, is expected to be a key growth engine, driven by a rapidly expanding automotive production base and increasing consumer awareness of vehicle safety. Europe and North America, with their mature automotive markets and stringent safety standards, will continue to hold substantial market share. Major players like Bosch, Continental, STMicroelectronics, Analog Devices, NXP Semiconductors, Infineon Technologies, and Denso are actively investing in R&D to capture this dynamic market.

Automotive Airbag IC Company Market Share

Automotive Airbag IC Market Structure & Competitive Landscape

The global automotive airbag Integrated Circuit (IC) market exhibits a moderate to high degree of concentration, with a handful of billion-dollar semiconductor giants dominating the landscape. Leading players such as Bosch, Continental, STMicroelectronics, Analog Devices, NXP Semiconductors, Infineon Technologies, and Denso collectively hold a significant share, estimated to be over 75% in 2025. This concentration is driven by substantial R&D investments, complex manufacturing processes, and stringent automotive qualification requirements. Innovation is a critical differentiator, with companies continually developing more sophisticated ICs that support advanced safety features, including multi-stage airbags, occupant detection systems, and integrated vehicle dynamics control. Regulatory impacts are profound, with evolving safety standards across major automotive markets mandating enhanced airbag functionalities and, consequently, more advanced IC solutions. The threat of product substitutes is relatively low due to the critical safety function of airbags and the established reliability of IC-based solutions. End-user segmentation primarily revolves around passenger vehicles and commercial vehicles, with the former representing a considerably larger market volume due to higher production numbers. Mergers and acquisitions (M&A) activity, while not constant, is observed as companies seek to expand their product portfolios, gain market access, or acquire cutting-edge technologies. In the historical period (2019-2024), notable M&A activities have focused on consolidating capabilities in sensing and control technologies vital for airbag systems, with a combined deal value exceeding $1 billion. The study period (2019-2033) anticipates continued consolidation driven by the increasing complexity and integration demands within automotive safety systems.

Automotive Airbag IC Market Trends & Opportunities

The automotive airbag IC market is poised for robust growth, projected to expand from an estimated $5 billion in 2025 to over $10 billion by 2033, showcasing a Compound Annual Growth Rate (CAGR) of approximately 8.5%. This significant expansion is fueled by a confluence of technological advancements, evolving consumer preferences for enhanced safety, and increasingly stringent regulatory mandates across the globe. The base year of 2025 marks a pivotal point, with the market already well-established and anticipating accelerated adoption of next-generation airbag technologies.

Technological shifts are a primary growth catalyst. The evolution from basic airbag deployment controllers to highly integrated system-on-chip (SoC) solutions is a dominant trend. These advanced ICs are capable of processing data from multiple sensors, including occupant detection systems (ODS), seatbelt pretensioners, and vehicle dynamics sensors, enabling more precise and adaptive airbag deployment. The integration of AI and machine learning algorithms within these ICs is becoming increasingly prevalent, allowing for real-time analysis of crash scenarios and personalized safety responses. This not only enhances occupant safety but also opens up new avenues for data-driven automotive services.

Consumer preferences are strongly gravitating towards vehicles with advanced safety features, driven by heightened awareness of road safety and a desire for comprehensive protection. This demand directly translates into a higher penetration rate for advanced airbag systems, which in turn necessitates more sophisticated and feature-rich airbag ICs. The market penetration rate of advanced airbag systems, which was around 70% in 2024, is expected to climb above 90% by 2033.

Competitive dynamics are characterized by intense innovation and strategic partnerships. Key players are heavily investing in R&D to develop ICs that are not only more performant but also more cost-effective and energy-efficient. The trend towards zonal architectures in vehicles, where specific ECUs manage localized functions, is also influencing airbag IC design, leading to a greater demand for modular and scalable solutions. The competitive landscape is fiercely contested, with companies vying for market share through technological leadership, strategic alliances with Tier 1 suppliers and OEMs, and expanding their intellectual property portfolios. The market size is projected to grow from $5 billion in 2025 to $10 billion by 2033, with an estimated CAGR of 8.5%.

Dominant Markets & Segments in Automotive Airbag IC

The Passenger Vehicle segment unequivocally dominates the automotive airbag IC market, representing an estimated 85% of the total market value in 2025. This dominance stems from the sheer volume of passenger vehicle production globally, which dwarfs that of commercial vehicles. The stringent safety regulations implemented by major automotive markets, such as North America, Europe, and Asia-Pacific, specifically target passenger vehicle safety, mandating the inclusion of multiple airbags and advanced deployment systems.

Within the Passenger Vehicle segment, Integrated System Chips (ISCs) are increasingly becoming the preferred type of automotive airbag IC. ISCs integrate multiple functionalities onto a single chip, including microcontrollers, memory, communication interfaces, and sensor interfaces, thereby reducing system complexity, component count, and overall cost. The market share of ISCs is projected to grow from approximately 60% in 2025 to over 80% by 2033, reflecting the industry's drive towards greater integration and miniaturization. Independent Chips, while still present, are gradually being phased out in favor of these more comprehensive solutions.

Regional Dominance: North America and Europe currently represent the most dominant regions in the automotive airbag IC market due to their mature automotive industries, strong regulatory frameworks, and high consumer demand for advanced safety features. However, the Asia-Pacific region is exhibiting the fastest growth rate, driven by the burgeoning automotive production in countries like China, India, and South Korea, coupled with a growing emphasis on vehicle safety and evolving regulations. By 2033, Asia-Pacific is expected to surpass North America and Europe in terms of market share.

Key growth drivers within these dominant segments include:

- Stringent Regulatory Mandates: Continuous updates and enforcement of safety standards (e.g., NHTSA in the US, Euro NCAP in Europe) pushing for more airbags and advanced passive safety features.

- Technological Advancements: Development of more sophisticated ICs supporting multi-stage airbags, occupant detection systems, and intelligent restraint systems.

- OEM Push for Advanced Safety: Automakers actively promoting vehicles with superior safety packages to attract safety-conscious consumers.

- Electrification and Autonomous Driving: The integration of advanced safety systems, including airbags, is crucial for the development of next-generation vehicles that will incorporate new sensor suites and control architectures.

- Cost Optimization through Integration: The shift towards ISCs allows for significant cost savings in terms of component count, board space, and assembly, making advanced safety systems more accessible.

The Commercial Vehicle segment, while smaller, is also experiencing growth, driven by increasing safety regulations for trucks, buses, and other heavy-duty vehicles, particularly in developed markets. The focus here is on protecting occupants in more severe accident scenarios and for longer operational durations.

Automotive Airbag IC Product Analysis

Automotive airbag ICs are central to vehicle occupant safety, orchestrating the precise deployment of airbags during a collision. Recent product innovations focus on highly integrated system-on-chips (SoCs) that consolidate multiple functionalities, reducing component count and system complexity. These advanced ICs leverage sophisticated algorithms to analyze data from an array of sensors – including occupant weight and position sensors, seatbelt status, and vehicle dynamics – to determine the optimal airbag deployment strategy. Competitive advantages lie in the processing power, low power consumption, high reliability under extreme conditions, and adherence to stringent automotive safety standards (e.g., ISO 26262 ASIL D). Companies are increasingly embedding advanced diagnostic capabilities and secure communication protocols within these ICs to enhance overall system integrity and support evolving vehicle architectures.

Key Drivers, Barriers & Challenges in Automotive Airbag IC

Key Drivers: The automotive airbag IC market is propelled by several critical factors. Technological advancements in semiconductor technology enable the development of more sophisticated and integrated ICs, supporting advanced safety features like multi-stage airbags and occupant detection systems. Stringent government regulations globally, mandating higher safety standards and increased airbag coverage, are significant drivers. Growing consumer awareness and demand for enhanced vehicle safety features also play a crucial role. Furthermore, the increasing production of vehicles worldwide directly translates to a higher demand for airbag systems and their core components. The trend towards electrification and autonomous driving necessitates more advanced and integrated safety systems, further boosting the need for innovative airbag ICs.

Key Barriers & Challenges: Despite the positive growth trajectory, the market faces several hurdles. Regulatory complexities and evolving standards require continuous adaptation and significant R&D investment from manufacturers, impacting development timelines and costs. Supply chain disruptions, as witnessed in recent years, can lead to component shortages and price volatility, affecting production schedules. Intense competitive pressure among established players and emerging entrants drives down profit margins. High development and qualification costs for automotive-grade semiconductors are substantial barriers, especially for smaller companies. Finally, consumer price sensitivity can limit the adoption of the most advanced (and therefore potentially more expensive) airbag systems in lower-segment vehicles.

Growth Drivers in the Automotive Airbag IC Market

The automotive airbag IC market's growth is primarily fueled by a trifecta of technological innovation, regulatory imperatives, and evolving consumer demand. Technological advancements are continuously pushing the boundaries of airbag system capabilities, enabling more precise and adaptive deployment through integrated sensors and advanced processing within ICs. Stringent government safety regulations worldwide are a consistent driver, mandating enhanced airbag coverage and performance for both passenger and commercial vehicles. This regulatory push forces OEMs to adopt more sophisticated airbag IC solutions to meet compliance. Growing consumer awareness and preference for advanced safety features also play a significant role, as buyers increasingly prioritize vehicles equipped with comprehensive protection systems. The increasing complexity of modern vehicle architectures, driven by electrification and autonomous driving technologies, necessitates advanced and integrated safety solutions, including sophisticated airbag control ICs.

Challenges Impacting Automotive Airbag IC Growth

The expansion of the automotive airbag IC market is tempered by several significant challenges. Navigating complex and evolving global safety regulations requires substantial investment in R&D and rigorous certification processes, impacting time-to-market and increasing development costs. Supply chain volatility and potential component shortages, particularly for critical semiconductor materials, pose a persistent threat to production continuity and can lead to price fluctuations, estimated to impact production by up to 15% in challenging periods. Intense competitive pressure within the semiconductor industry can lead to price erosion and necessitate continuous innovation to maintain market share. High initial investment and long qualification cycles for automotive-grade ICs create substantial barriers to entry for new players. Furthermore, consumer price sensitivity, especially in emerging markets, can limit the adoption of higher-end, more feature-rich airbag systems, thereby impacting the full potential of advanced IC solutions.

Key Players Shaping the Automotive Airbag IC Market

- Bosch

- Continental

- STMicroelectronics

- Analog Devices

- NXP Semiconductors

- Infineon Technologies

- Denso

Significant Automotive Airbag IC Industry Milestones

- 2019: Introduction of advanced occupant detection systems integrated with airbag control ICs, enabling more personalized safety responses.

- 2020: Increased adoption of ASIL D certified airbag ICs to meet stringent functional safety requirements under ISO 26262.

- 2021: Major semiconductor manufacturers announce significant investments in advanced manufacturing processes for automotive-grade ICs, responding to market demand.

- 2022: Emergence of AI and machine learning capabilities within airbag ICs for predictive crash analysis and adaptive deployment.

- 2023: Growing trend towards zonal ECUs in vehicles, leading to demand for modular and scalable airbag IC solutions.

- 2024: Expansion of airbag systems to include new deployment locations, such as knee airbags and center airbags, driving demand for more versatile ICs.

Future Outlook for Automotive Airbag IC Market

The future outlook for the automotive airbag IC market remains exceptionally positive, driven by an ongoing commitment to enhanced vehicle safety and rapid technological evolution. Growth catalysts include the relentless push for increasingly sophisticated passive safety systems, the integration of advanced sensing and diagnostic capabilities within ICs, and the expanding scope of airbag applications beyond traditional frontal and side deployments. The transition towards electric and autonomous vehicles will further accelerate demand for highly integrated and intelligent safety control ICs. Strategic opportunities lie in developing solutions for advanced driver-assistance systems (ADAS) integration, catering to the growing market for commercial vehicle safety, and expanding presence in rapidly growing automotive markets. The market is projected to witness sustained innovation and strategic partnerships as companies vie to provide the most advanced, reliable, and cost-effective airbag IC solutions to meet future mobility demands, with market value expected to exceed $10 billion by 2033.

Automotive Airbag IC Segmentation

-

1. Application

- 1.1. Passenger Vehicle

- 1.2. Commercial Vehicle

-

2. Types

- 2.1. Integrated System Chip

- 2.2. Independent Chip

Automotive Airbag IC Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Automotive Airbag IC Regional Market Share

Geographic Coverage of Automotive Airbag IC

Automotive Airbag IC REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 13.79% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Passenger Vehicle

- 5.1.2. Commercial Vehicle

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Integrated System Chip

- 5.2.2. Independent Chip

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Automotive Airbag IC Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Passenger Vehicle

- 6.1.2. Commercial Vehicle

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Integrated System Chip

- 6.2.2. Independent Chip

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Automotive Airbag IC Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Passenger Vehicle

- 7.1.2. Commercial Vehicle

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Integrated System Chip

- 7.2.2. Independent Chip

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Automotive Airbag IC Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Passenger Vehicle

- 8.1.2. Commercial Vehicle

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Integrated System Chip

- 8.2.2. Independent Chip

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Automotive Airbag IC Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Passenger Vehicle

- 9.1.2. Commercial Vehicle

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Integrated System Chip

- 9.2.2. Independent Chip

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Automotive Airbag IC Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Passenger Vehicle

- 10.1.2. Commercial Vehicle

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Integrated System Chip

- 10.2.2. Independent Chip

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Automotive Airbag IC Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Passenger Vehicle

- 11.1.2. Commercial Vehicle

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Integrated System Chip

- 11.2.2. Independent Chip

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Bosch

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Continental

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 ST

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 ADI

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 NXP

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Infineon

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Denso

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.1 Bosch

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Automotive Airbag IC Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Automotive Airbag IC Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Automotive Airbag IC Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Automotive Airbag IC Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Automotive Airbag IC Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Automotive Airbag IC Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Automotive Airbag IC Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Automotive Airbag IC Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Automotive Airbag IC Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Automotive Airbag IC Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Automotive Airbag IC Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Automotive Airbag IC Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Automotive Airbag IC Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Automotive Airbag IC Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Automotive Airbag IC Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Automotive Airbag IC Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Automotive Airbag IC Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Automotive Airbag IC Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Automotive Airbag IC Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Automotive Airbag IC Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Automotive Airbag IC Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Automotive Airbag IC Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Automotive Airbag IC Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Automotive Airbag IC Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Automotive Airbag IC Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Automotive Airbag IC Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Automotive Airbag IC Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Automotive Airbag IC Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Automotive Airbag IC Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Automotive Airbag IC Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Automotive Airbag IC Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automotive Airbag IC Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Automotive Airbag IC Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Automotive Airbag IC Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Automotive Airbag IC Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Automotive Airbag IC Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Automotive Airbag IC Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Automotive Airbag IC Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Automotive Airbag IC Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Automotive Airbag IC Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Automotive Airbag IC Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Automotive Airbag IC Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Automotive Airbag IC Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Automotive Airbag IC Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Automotive Airbag IC Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Automotive Airbag IC Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Automotive Airbag IC Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Automotive Airbag IC Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Automotive Airbag IC Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Automotive Airbag IC Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Automotive Airbag IC Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Automotive Airbag IC Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Automotive Airbag IC Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Automotive Airbag IC Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Automotive Airbag IC Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Automotive Airbag IC Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Automotive Airbag IC Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Automotive Airbag IC Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Automotive Airbag IC Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Automotive Airbag IC Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Automotive Airbag IC Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Automotive Airbag IC Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Automotive Airbag IC Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Automotive Airbag IC Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Automotive Airbag IC Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Automotive Airbag IC Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Automotive Airbag IC Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Automotive Airbag IC Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Automotive Airbag IC Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Automotive Airbag IC Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Automotive Airbag IC Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Automotive Airbag IC Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Automotive Airbag IC Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Automotive Airbag IC Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Automotive Airbag IC Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Automotive Airbag IC Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Automotive Airbag IC Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Airbag IC?

The projected CAGR is approximately 13.79%.

2. Which companies are prominent players in the Automotive Airbag IC?

Key companies in the market include Bosch, Continental, ST, ADI, NXP, Infineon, Denso.

3. What are the main segments of the Automotive Airbag IC?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Airbag IC," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Airbag IC report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Airbag IC?

To stay informed about further developments, trends, and reports in the Automotive Airbag IC, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence