Key Insights

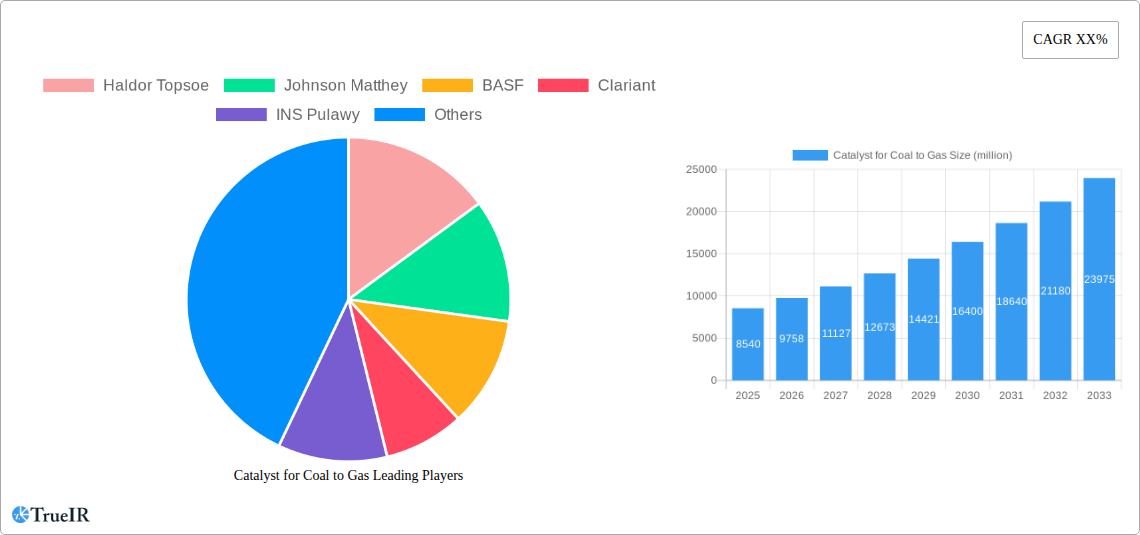

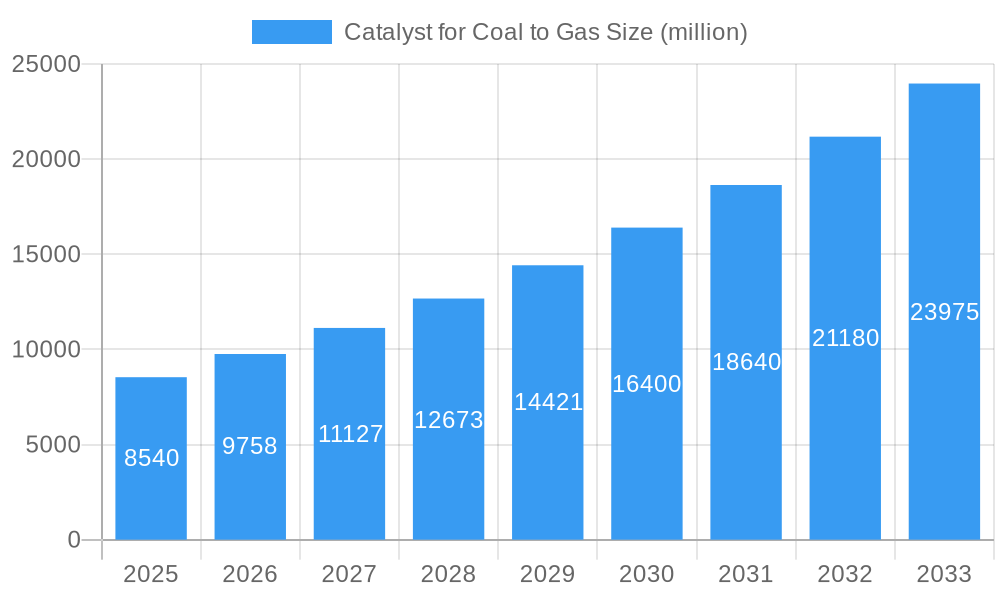

The Catalyst for Coal to Gas market is poised for significant expansion, projected to reach an estimated $8.54 billion by 2025, driven by a robust compound annual growth rate of 14.07% from 2019 to 2033. This dynamic growth is primarily fueled by the escalating demand for cleaner energy alternatives and the inherent efficiency of converting coal into synthesis gas (syngas) for subsequent production of natural gas and other valuable chemicals. Key applications within this market span across industrial production, where syngas is a crucial intermediate in various chemical synthesis processes, and scientific research institutions, exploring novel catalytic pathways for enhanced efficiency and reduced environmental impact. The market's trajectory is further bolstered by advancements in catalyst technology, leading to improved performance, selectivity, and durability.

Catalyst for Coal to Gas Market Size (In Billion)

The market is segmented by types into Aluminum Oxide Carrier, Composite Carrier, and Others, each offering distinct advantages in terms of catalytic activity and operational stability. The Aluminum Oxide Carrier segment, known for its high surface area and thermal stability, is expected to maintain a strong presence. Composite carriers, integrating multiple materials, are emerging as a key area of innovation, promising superior performance in demanding applications. The dominance of regions like Asia Pacific, particularly China and India, is anticipated due to their substantial coal reserves and increasing reliance on syngas technology for energy security and chemical production. Major players such as Haldor Topsoe, Johnson Matthey, and BASF are actively investing in research and development to innovate next-generation catalysts, addressing challenges like sulfur poisoning and optimizing process economics, thus shaping the future landscape of coal-to-gas conversion.

Catalyst for Coal to Gas Company Market Share

This comprehensive report provides an in-depth analysis of the Catalyst for Coal to Gas Market, a critical sector supporting global energy transition and industrial advancement. Leveraging high-volume keywords such as "coal gasification catalysts," "syngas production," "methanation catalysts," "FT synthesis catalysts," and "industrial gasification technologies," this report is meticulously designed for SEO optimization and to provide actionable insights to industry stakeholders.

The study encompasses a robust Study Period from 2019 to 2033, with the Base Year and Estimated Year both set at 2025, and a detailed Forecast Period from 2025 to 2033, building upon a comprehensive Historical Period of 2019–2024. The market is projected to reach an estimated value of $XX billion by 2025, with significant growth anticipated throughout the forecast period.

Catalyst for Coal to Gas Market Structure & Competitive Landscape

The Catalyst for Coal to Gas market is characterized by a moderate to high level of concentration, with a few key players dominating innovation and supply. Key innovation drivers include the pursuit of higher conversion efficiencies, reduced operational costs, and enhanced catalyst lifespan to meet stringent environmental regulations and economic demands for cleaner energy solutions. Regulatory impacts are significant, with governments worldwide pushing for decarbonization, influencing demand for advanced catalysts in coal gasification for synthesis gas production and subsequent conversion to valuable chemicals and fuels. Product substitutes, while present in broader energy sectors, are less direct within the specific coal-to-gas pathway, making catalyst development crucial. End-user segmentation highlights the dominance of Industrial Production applications, which account for an estimated XX% of the market, driven by large-scale chemical manufacturing and energy generation. Scientific Research Institutions represent a smaller but growing segment, focused on novel catalyst development. Mergers and Acquisitions (M&A) are notable, with XX M&A deals recorded during the historical period, totaling an estimated $XX billion, aimed at consolidating market share, acquiring proprietary technologies, and expanding geographical reach. The average concentration ratio among the top five players is estimated at XX%.

Catalyst for Coal to Gas Market Trends & Opportunities

The global Catalyst for Coal to Gas market is experiencing a dynamic surge in growth, projected to expand at a Compound Annual Growth Rate (CAGR) of XX% from 2025 to 2033, reaching an estimated market size of $XX billion by the end of the forecast period. This growth is propelled by a confluence of technological advancements, evolving consumer preferences for cleaner energy sources, and shifting competitive landscapes. The primary trend is the increasing adoption of advanced gasification technologies that necessitate highly efficient and durable catalysts. For instance, breakthroughs in Fischer-Tropsch (FT) synthesis, a key downstream process utilizing syngas derived from coal, are creating new avenues for catalyst manufacturers. These catalysts are crucial for converting syngas into liquid fuels and chemicals, thereby reducing reliance on crude oil.

Technological shifts are focusing on developing catalysts with improved selectivity, lower operating temperatures, and resistance to deactivation from impurities in syngas. This includes the development of novel Aluminum Oxide Carrier and Composite Carrier based catalysts, which offer superior mechanical strength and thermal stability compared to traditional formulations. The market penetration rate for high-performance catalysts is steadily increasing as industries seek to optimize their coal-to-gas conversion processes for economic viability and environmental compliance.

Consumer preferences are increasingly leaning towards sustainable and lower-emission energy solutions. While coal gasification itself has environmental considerations, the output can be used to produce cleaner fuels and chemicals, positioning it as a transition technology. This demand for cleaner downstream products from coal gasification fuels the innovation in catalysts that enhance the efficiency and reduce the environmental footprint of these processes.

Competitive dynamics are intensifying, with established chemical companies and specialized catalyst manufacturers vying for market leadership. Strategic partnerships and R&D collaborations are common, as companies aim to accelerate the development and commercialization of next-generation catalysts. The global push towards energy diversification and security further bolsters opportunities for coal-to-gas technologies, especially in regions with abundant coal reserves seeking to maximize their resource utilization while minimizing environmental impact. The market is ripe with opportunities for companies that can offer cost-effective, high-performance catalysts tailored to specific industrial applications and evolving regulatory frameworks. The market size is expected to grow from an estimated $XX billion in 2025 to $XX billion by 2033.

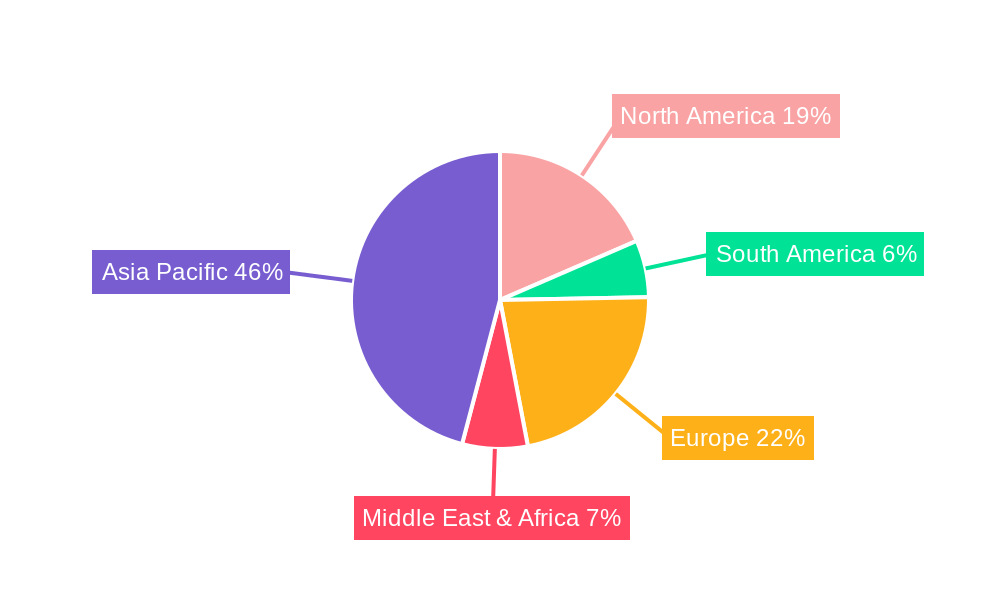

Dominant Markets & Segments in Catalyst for Coal to Gas

The Catalyst for Coal to Gas Market exhibits distinct regional and segment dominance, driven by unique economic, political, and technological factors.

Leading Region and Country

The Asia Pacific region currently dominates the global Catalyst for Coal to Gas market, driven primarily by China. China’s immense coal reserves, coupled with significant government investment in coal-to-chemical and coal-to-gas projects aimed at energy security and industrial upgrading, positions it as the largest consumer and developer of these catalysts. Other significant contributors within the region include India and Southeast Asian nations, actively exploring coal gasification for power generation and chemical feedstock. The region's dominance is further cemented by its large industrial base and the ongoing expansion of synthetic natural gas (SNG) production facilities.

Dominant Segments

- Application: Industrial Production: This segment is the largest by a significant margin, accounting for an estimated XX% of the total market value in 2025. The demand is fueled by large-scale chemical manufacturing plants that utilize syngas derived from coal as a feedstock for producing methanol, ammonia, olefins, and other valuable chemicals. Energy production, including coal-to-power and coal-to-SNG, also falls under this broad application, driving substantial catalyst consumption. Infrastructure development and the need for stable, domestically sourced energy and chemical supplies are key growth drivers.

- Types: Aluminum Oxide Carrier and Composite Carrier: While Aluminum Oxide Carrier catalysts have historically been prevalent due to their cost-effectiveness and established performance, Composite Carrier catalysts are gaining significant traction. These advanced carriers offer superior mechanical strength, thermal stability, and resistance to poisoning, leading to longer catalyst life and improved process efficiency. The growing demand for high-performance catalysts in demanding industrial environments, coupled with ongoing R&D into novel composite materials, is propelling the growth of this segment. The "Others" category, encompassing novel support materials and formulations, represents a niche but rapidly evolving area of innovation.

The combination of robust industrial activity in the Asia Pacific, particularly in China, and the critical role of catalysts in the Industrial Production segment, underpins the market's current structure. Growth drivers such as supportive government policies promoting coal utilization for value-added products, increasing investments in advanced gasification technologies, and the continuous pursuit of operational efficiency by end-users are shaping the dominance of these segments and regions.

Catalyst for Coal to Gas Product Analysis

Catalyst innovations in the coal-to-gas sector are primarily focused on enhancing conversion efficiency, selectivity, and lifespan. Key advancements include novel Aluminum Oxide Carrier and Composite Carrier formulations that offer superior mechanical and thermal stability, crucial for high-temperature gasification processes. These catalysts are designed to withstand harsh operating conditions, reducing downtime and operational costs. Applications range from syngas production for methanol and ammonia synthesis to Fischer-Tropsch synthesis for producing synthetic fuels and chemicals. Competitive advantages are being gained by manufacturers who can offer catalysts with improved resistance to sulfur poisoning and coking, thereby extending their service life and ensuring consistent performance.

Key Drivers, Barriers & Challenges in Catalyst for Coal to Gas

Key Drivers

The Catalyst for Coal to Gas Market is propelled by several key drivers. Foremost is the ongoing demand for energy security, especially in countries with abundant coal reserves, providing a stable feedstock for domestic fuel and chemical production. Technological advancements in gasification and downstream synthesis processes necessitate the development and adoption of more efficient and durable catalysts, leading to improved conversion rates and reduced operational costs. Government policies supporting clean coal technologies and the production of valuable chemicals from coal also play a crucial role. Furthermore, the rising global demand for petrochemical alternatives and synthetic fuels creates significant opportunities for coal-to-gas routes.

Barriers & Challenges

Despite the drivers, significant barriers and challenges exist. The primary challenge is the environmental impact associated with coal utilization, including greenhouse gas emissions, which are under increasing scrutiny from regulatory bodies and the public. Stringent environmental regulations necessitate substantial investment in emission control technologies, increasing the overall cost of coal-to-gas operations. Supply chain complexities for raw materials and specialized catalyst components, coupled with geopolitical factors, can lead to price volatility and availability issues. High capital investment required for establishing coal gasification facilities and the competitive pressure from alternative energy sources like natural gas and renewables also pose considerable challenges. The decline in coal-fired power generation in some developed nations could also indirectly impact the broader coal utilization ecosystem.

Growth Drivers in the Catalyst for Coal to Gas Market

The growth of the Catalyst for Coal to Gas Market is primarily driven by the global imperative for energy security, particularly in regions with substantial coal reserves, enabling domestic production of synthetic fuels and chemicals. Technological innovation in gasification and synthesis processes is a significant catalyst, demanding more efficient, selective, and durable catalysts that reduce operational costs and improve conversion rates. Supportive government policies aimed at diversifying energy portfolios and promoting the production of high-value chemicals from coal are also instrumental. Moreover, the increasing demand for petrochemical substitutes and synthetic fuels provides a robust market for the outputs of coal-to-gas processes. The development of advanced Aluminum Oxide Carrier and Composite Carrier technologies, offering enhanced performance under harsh conditions, further fuels market expansion.

Challenges Impacting Catalyst for Coal to Gas Growth

Several challenges significantly impact the growth of the Catalyst for Coal to Gas Market. The most prominent is the environmental concern surrounding coal usage, including carbon emissions, which are subject to increasingly strict global regulations and public opposition. This necessitates substantial investment in emission control technologies, raising operational costs. Regulatory hurdles, such as carbon pricing mechanisms and stricter environmental standards, can make coal-to-gas projects less economically attractive compared to cleaner alternatives. Supply chain disruptions for key raw materials and the inherent volatility in raw material prices add further complexity and risk. Additionally, the high initial capital expenditure for building coal gasification plants and the strong competition from readily available natural gas and renewable energy sources pose significant restraint.

Key Players Shaping the Catalyst for Coal to Gas Market

- Haldor Topsoe

- Johnson Matthey

- BASF

- Clariant

- INS Pulawy

- JGC C&C

- Jiangxi Huihua

- Anchun

- CAS KERRY

- Sichuan Shutai

- Dalian Catalytic

Significant Catalyst for Coal to Gas Industry Milestones

- 2019: Increased R&D investment in high-efficiency syngas conversion catalysts for FT synthesis.

- 2020: Launch of new generation methanation catalysts with improved thermal stability.

- 2021: Strategic partnerships formed between catalyst manufacturers and large chemical conglomerates for integrated coal-to-chemical projects.

- 2022: Significant advancements in composite carrier catalyst technology demonstrated improved resistance to sulfur poisoning.

- 2023: Growing emphasis on catalysts for producing sustainable aviation fuels from syngas.

- 2024: Introduction of advanced catalyst regeneration techniques to extend operational life.

- 2025 (Projected): Expected commercialization of novel catalysts for direct coal liquefaction and advanced gasification technologies.

Future Outlook for Catalyst for Coal to Gas Market

The future outlook for the Catalyst for Coal to Gas Market is characterized by a strong emphasis on efficiency and sustainability. While environmental pressures will continue to shape the industry, the demand for coal-to-gas technologies as a transition pathway for energy security and the production of essential chemicals is expected to persist, particularly in developing economies. Strategic opportunities lie in the development of next-generation catalysts with even higher selectivity, lower operating temperatures, and extended lifespans, capable of minimizing emissions. Innovations in composite carrier materials and novel catalyst support structures will be critical. Furthermore, the integration of carbon capture and utilization (CCU) technologies with coal gasification processes, enabled by advanced catalysts, presents a significant avenue for growth and environmental compliance. The market is poised for continued innovation, driven by the need for cost-effective, reliable, and increasingly cleaner solutions in the global energy and chemical landscape.

Catalyst for Coal to Gas Segmentation

-

1. Application

- 1.1. Industrial Production

- 1.2. Scientific Research Institutions

-

2. Types

- 2.1. Aluminum Oxide Carrier

- 2.2. Composite Carrier

- 2.3. Others

Catalyst for Coal to Gas Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Catalyst for Coal to Gas Regional Market Share

Geographic Coverage of Catalyst for Coal to Gas

Catalyst for Coal to Gas REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 14.07% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Catalyst for Coal to Gas Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Industrial Production

- 5.1.2. Scientific Research Institutions

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Aluminum Oxide Carrier

- 5.2.2. Composite Carrier

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Catalyst for Coal to Gas Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Industrial Production

- 6.1.2. Scientific Research Institutions

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Aluminum Oxide Carrier

- 6.2.2. Composite Carrier

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Catalyst for Coal to Gas Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Industrial Production

- 7.1.2. Scientific Research Institutions

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Aluminum Oxide Carrier

- 7.2.2. Composite Carrier

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Catalyst for Coal to Gas Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Industrial Production

- 8.1.2. Scientific Research Institutions

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Aluminum Oxide Carrier

- 8.2.2. Composite Carrier

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Catalyst for Coal to Gas Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Industrial Production

- 9.1.2. Scientific Research Institutions

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Aluminum Oxide Carrier

- 9.2.2. Composite Carrier

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Catalyst for Coal to Gas Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Industrial Production

- 10.1.2. Scientific Research Institutions

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Aluminum Oxide Carrier

- 10.2.2. Composite Carrier

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Haldor Topsoe

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Johnson Matthey

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 BASF

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Clariant

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 INS Pulawy

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 JGC C&C

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Jiangxi Huihua

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Anchun

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 CAS KERRY

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Sichuan Shutai

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Dalian Catalytic

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.1 Haldor Topsoe

List of Figures

- Figure 1: Global Catalyst for Coal to Gas Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Catalyst for Coal to Gas Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Catalyst for Coal to Gas Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Catalyst for Coal to Gas Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Catalyst for Coal to Gas Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Catalyst for Coal to Gas Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Catalyst for Coal to Gas Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Catalyst for Coal to Gas Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Catalyst for Coal to Gas Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Catalyst for Coal to Gas Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Catalyst for Coal to Gas Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Catalyst for Coal to Gas Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Catalyst for Coal to Gas Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Catalyst for Coal to Gas Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Catalyst for Coal to Gas Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Catalyst for Coal to Gas Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Catalyst for Coal to Gas Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Catalyst for Coal to Gas Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Catalyst for Coal to Gas Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Catalyst for Coal to Gas Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Catalyst for Coal to Gas Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Catalyst for Coal to Gas Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Catalyst for Coal to Gas Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Catalyst for Coal to Gas Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Catalyst for Coal to Gas Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Catalyst for Coal to Gas Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Catalyst for Coal to Gas Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Catalyst for Coal to Gas Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Catalyst for Coal to Gas Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Catalyst for Coal to Gas Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Catalyst for Coal to Gas Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Catalyst for Coal to Gas Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Catalyst for Coal to Gas Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Catalyst for Coal to Gas Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Catalyst for Coal to Gas Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Catalyst for Coal to Gas Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Catalyst for Coal to Gas Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Catalyst for Coal to Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Catalyst for Coal to Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Catalyst for Coal to Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Catalyst for Coal to Gas Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Catalyst for Coal to Gas Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Catalyst for Coal to Gas Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Catalyst for Coal to Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Catalyst for Coal to Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Catalyst for Coal to Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Catalyst for Coal to Gas Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Catalyst for Coal to Gas Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Catalyst for Coal to Gas Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Catalyst for Coal to Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Catalyst for Coal to Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Catalyst for Coal to Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Catalyst for Coal to Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Catalyst for Coal to Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Catalyst for Coal to Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Catalyst for Coal to Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Catalyst for Coal to Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Catalyst for Coal to Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Catalyst for Coal to Gas Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Catalyst for Coal to Gas Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Catalyst for Coal to Gas Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Catalyst for Coal to Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Catalyst for Coal to Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Catalyst for Coal to Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Catalyst for Coal to Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Catalyst for Coal to Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Catalyst for Coal to Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Catalyst for Coal to Gas Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Catalyst for Coal to Gas Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Catalyst for Coal to Gas Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Catalyst for Coal to Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Catalyst for Coal to Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Catalyst for Coal to Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Catalyst for Coal to Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Catalyst for Coal to Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Catalyst for Coal to Gas Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Catalyst for Coal to Gas Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Catalyst for Coal to Gas?

The projected CAGR is approximately 14.07%.

2. Which companies are prominent players in the Catalyst for Coal to Gas?

Key companies in the market include Haldor Topsoe, Johnson Matthey, BASF, Clariant, INS Pulawy, JGC C&C, Jiangxi Huihua, Anchun, CAS KERRY, Sichuan Shutai, Dalian Catalytic.

3. What are the main segments of the Catalyst for Coal to Gas?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Catalyst for Coal to Gas," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Catalyst for Coal to Gas report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Catalyst for Coal to Gas?

To stay informed about further developments, trends, and reports in the Catalyst for Coal to Gas, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence