Key Insights

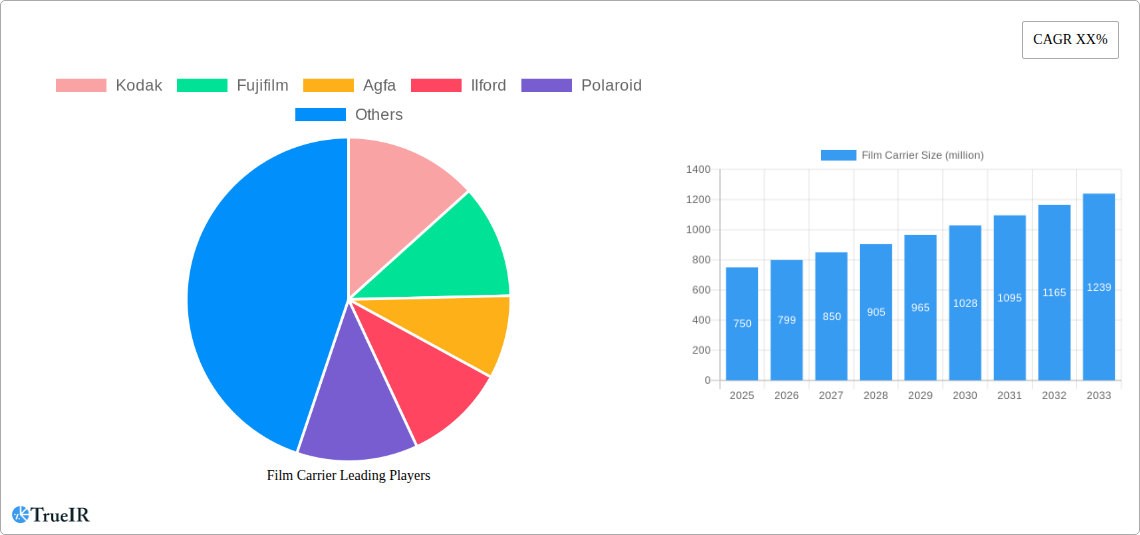

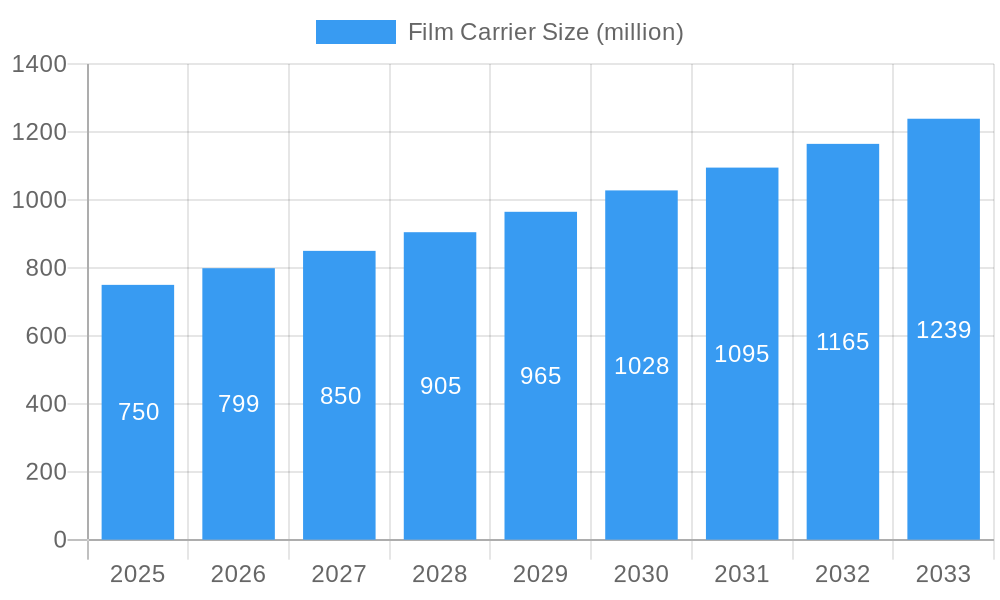

The global Film Carrier market is projected for substantial growth, forecasted to reach approximately $115.5 billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of 5%. This expansion is primarily driven by escalating demand from advanced manufacturing sectors, including Flat Panel Display (FPD) fabrication, Micro-Electro-Mechanical Systems (MEMS) production, and Photovoltaic cell manufacturing. The increasing complexity and miniaturization of electronic components underscore the necessity for highly precise and reliable film handling solutions, making advanced film carriers essential. Additionally, a resurgence in analog photography and the growing market for premium optical components contribute to positive market dynamics. The market size was estimated at $750 million in the base year of 2025, with anticipated growth reflecting robust year-on-year expansion.

Film Carrier Market Size (In Billion)

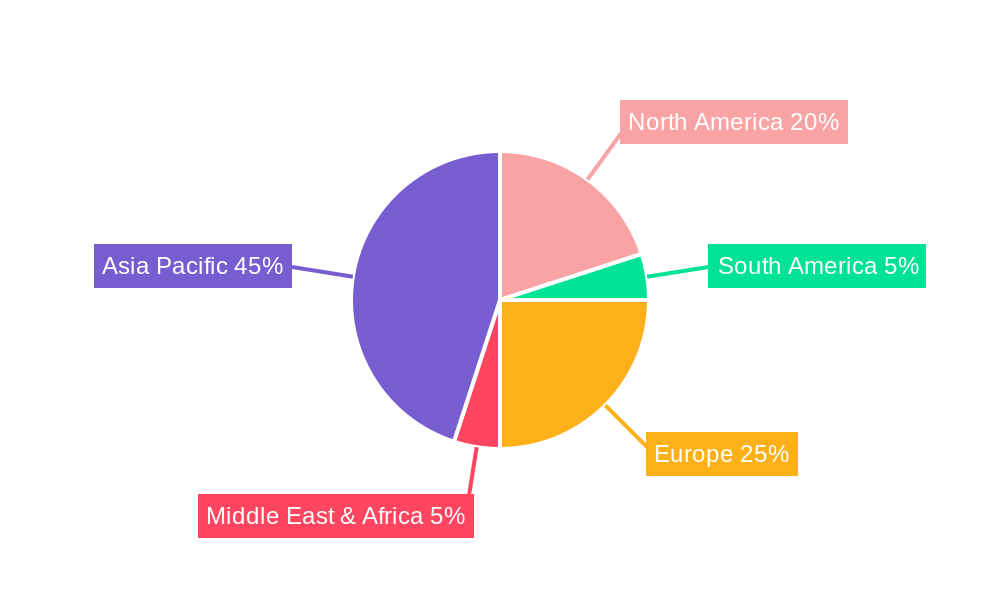

While established manufacturers dominate, opportunities exist for innovation in material science and design to improve film carrier performance and cost-effectiveness. Challenges include significant initial investment for advanced manufacturing equipment and stringent quality control requirements leading to extended development cycles. However, the inherent precision and reliability of specialized film carriers, particularly those crafted from quartz and silicon, are critical for optimizing yields in sensitive manufacturing processes. The Asia Pacific region, led by China and Japan, is anticipated to be the primary consumer due to its robust manufacturing infrastructure, followed by North America and Europe, which are increasingly focusing on high-tech production and specialized optical components.

Film Carrier Company Market Share

Film Carrier Market Structure & Competitive Landscape

The film carrier market, a critical component in advanced manufacturing processes, exhibits a moderately consolidated structure with a blend of established global players and niche specialists. The competitive landscape is shaped by intense innovation, particularly in material science and precision engineering to meet the exacting demands of industries like semiconductor and display manufacturing. Regulatory impacts, primarily stemming from environmental compliance and safety standards, play a significant role in market entry and product development. Product substitutes, though limited due to the specialized nature of film carriers, can emerge from advancements in alternative handling technologies. End-user segmentation is crucial, with demand driven by the stringent requirements of Flat Panel Display Manufacturing, Optical Component Manufacturing, Micro-Electro-Mechanical Systems (MEMS) Manufacturing, and Photovoltaic (solar) Cell Manufacturing. Mergers and acquisitions (M&A) activity, while not consistently high, are strategic moves by larger entities to acquire technological expertise or expand market reach. Concentration ratios are estimated to be in the xx% range, indicating that the top five players command a substantial portion of the market share. M&A volumes are projected to be in the xx million range annually, reflecting a strategic consolidation driven by the need for integrated solutions and economies of scale in this high-value sector.

- Market Concentration: Moderately consolidated with key players holding significant market share.

- Innovation Drivers: Material science advancements, precision engineering, and ultra-clean manufacturing processes.

- Regulatory Impacts: Environmental compliance, safety standards, and import/export regulations.

- Product Substitutes: Limited, but emerging from alternative automated handling systems and advanced material solutions.

- End-User Segmentation: Dominance of advanced manufacturing sectors.

- M&A Trends: Strategic acquisitions for technological integration and market expansion.

- Quantitative Data: Concentration Ratios: xx%; M&A Volumes: xx million annually.

Film Carrier Market Trends & Opportunities

The global film carrier market is poised for substantial growth, driven by the relentless advancement and miniaturization in key technology sectors. Projected to experience a Compound Annual Growth Rate (CAGR) of xx% from 2025 to 2033, the market is expected to reach a value exceeding xx million by the end of the forecast period. This upward trajectory is fueled by the ever-increasing demand for sophisticated electronic devices, from high-resolution displays to intricate MEMS devices and next-generation solar cells. Technological shifts are paramount, with a continuous push towards carriers that offer enhanced precision, superior chemical resistance, and improved thermal stability. The development of novel materials, such as advanced ceramics and specialized polymers, is enabling the creation of carriers that can withstand harsher processing environments and accommodate increasingly delicate components.

Consumer preferences, indirectly influencing the film carrier market, are leaning towards smaller, more powerful, and energy-efficient devices, necessitating tighter manufacturing tolerances and, consequently, more advanced film carriers. This translates into a growing demand for ultra-clean and highly specialized carriers that minimize contamination and ensure product integrity throughout complex fabrication processes. The competitive dynamics are intensifying, with companies investing heavily in research and development to secure a competitive edge. This includes the development of custom-designed carriers tailored to specific manufacturing workflows and the integration of smart features for improved tracking and process control. The market penetration rate for high-performance film carriers is expected to rise as manufacturers increasingly recognize the cost-savings and yield improvements associated with utilizing superior handling solutions. Opportunities abound for companies that can offer bespoke solutions, leverage advanced manufacturing techniques, and adapt to the rapidly evolving needs of the high-tech industries they serve. The market is witnessing a significant push towards sustainable manufacturing practices, presenting an opportunity for film carrier manufacturers to develop eco-friendly and recyclable materials without compromising on performance. Furthermore, the expansion of emerging economies into advanced manufacturing will create new geographical markets and demand centers for film carriers, further contributing to the market's robust growth.

Dominant Markets & Segments in Film Carrier

The film carrier market is experiencing significant dominance from the Flat Panel Display Manufacturing application segment. This segment's leadership is underpinned by the insatiable global demand for high-definition televisions, smartphones, tablets, and other electronic devices that rely heavily on advanced display technologies. The intricate manufacturing processes involved in producing these displays, such as photolithography and vacuum deposition, necessitate film carriers of exceptional purity, flatness, and dimensional stability to handle delicate substrate materials without causing defects. The market for these carriers within this segment is estimated to be in the hundreds of millions of dollars, with a significant portion of the overall market's value concentrated here.

Optical Component Manufacturing also represents a substantial and growing segment. The production of lenses, prisms, and other optical elements for cameras, scientific instruments, and advanced imaging systems demands carriers that offer precise positioning and protection against particulate contamination. The increasing sophistication of optical technologies, including augmented reality (AR) and virtual reality (VR) devices, is further fueling demand for specialized film carriers within this domain. The Micro-Electro-Mechanical Systems (MEMS) Manufacturing segment, while smaller in absolute market size compared to displays, is characterized by extremely high growth potential and stringent material requirements. MEMS devices, used in sensors, actuators, and microfluidic systems, are often fabricated using highly sensitive processes that require carriers with near-perfect flatness and minimal outgassing. The forecast period is expected to see substantial growth in this segment as MEMS technology finds broader applications across various industries.

Photovoltaic (solar) Cell Manufacturing represents another crucial application, particularly with the global push towards renewable energy sources. The production of solar panels involves the handling of large substrate materials, and film carriers are essential for ensuring consistent quality and maximizing yield. The development of more efficient and cost-effective solar cells directly influences the demand for robust and high-throughput film carrier solutions.

In terms of product types, Quartz Slides are paramount due to their exceptional thermal stability, chemical inertness, and ultra-low thermal expansion, making them ideal for high-temperature and corrosive manufacturing environments. Silicon Slides, while offering excellent mechanical properties and semiconductor compatibility, are also highly sought after for specific applications, particularly in MEMS and semiconductor fabrication where silicon substrates are commonly used. The overall market is estimated to be valued at over xx million, with the forecast period expecting a CAGR of xx%.

- Dominant Application Segment: Flat Panel Display Manufacturing, driven by consumer electronics.

- Key Growth Driver in Displays: Demand for higher resolution and thinner displays requiring extreme precision.

- Significant Application Segment: Optical Component Manufacturing, fueled by advancements in imaging and AR/VR.

- Emerging High-Growth Application: Micro-Electro-Mechanical Systems (MEMS) Manufacturing, due to increasing sensor adoption.

- Renewable Energy Driver: Photovoltaic (solar) Cell Manufacturing, benefiting from global energy transition.

- Dominant Product Type: Quartz Slides, owing to superior thermal and chemical resistance.

- Important Product Type: Silicon Slides, crucial for semiconductor and MEMS fabrication.

- Market Value (Estimated): Over xx million.

- Forecasted CAGR: xx%.

Film Carrier Product Analysis

Film carriers are engineered with exceptional precision and material integrity to facilitate the delicate handling of substrates in advanced manufacturing. Innovations focus on enhanced dimensional stability, superior chemical resistance, and ultra-low particle generation. These carriers are critical for applications demanding micron-level accuracy, such as in photolithography for semiconductor and display production. Competitive advantages lie in tailored material compositions, advanced surface treatments, and robust designs that minimize stress and prevent contamination, thereby improving yield and product reliability in sectors like MEMS and photovoltaic manufacturing.

Key Drivers, Barriers & Challenges in Film Carrier

Key Drivers: The film carrier market is propelled by relentless technological advancements in the semiconductor, display, and solar industries, demanding ever-increasing precision and purity in handling sensitive substrates. The global push towards renewable energy, particularly solar power, is a significant growth catalyst. Furthermore, the miniaturization of electronic components and the expansion of MEMS applications are creating new avenues for demand. Government initiatives and investments in high-tech manufacturing infrastructure globally also play a crucial role.

Barriers & Challenges: High manufacturing costs associated with specialized materials and stringent quality control processes present a barrier. Supply chain complexities for raw materials and the need for highly skilled labor contribute to challenges. Intense competition from established players and potential emergence of novel handling technologies can exert pricing pressure. Regulatory hurdles related to environmental compliance and international trade can also impact market dynamics.

Growth Drivers in the Film Carrier Market

The film carrier market's growth is fundamentally driven by the relentless innovation cycle in its core end-use industries. The exponential demand for more powerful and compact electronic devices, spanning smartphones, wearable technology, and advanced computing, necessitates continuous improvements in semiconductor fabrication. This directly translates to a higher need for film carriers that can accommodate smaller wafer sizes and enable finer lithographic features. The global commitment to sustainable energy solutions is a powerful growth driver, with the photovoltaic industry's expansion requiring large-scale, high-throughput handling of solar cells, thereby increasing the demand for durable and cost-effective film carriers. Technological advancements in materials science, leading to carriers with superior thermal stability, chemical inertness, and reduced particulate contamination, offer enhanced process yields and product reliability. Policy-driven incentives and government investments in domestic semiconductor and clean energy manufacturing further accelerate market expansion by fostering local production and innovation.

Challenges Impacting Film Carrier Growth

The film carrier market faces several significant challenges that can impede its growth trajectory. The intricate and highly specialized nature of film carrier manufacturing demands substantial capital investment in advanced machinery and cleanroom facilities, creating a barrier to entry for new players and increasing production costs. Supply chain disruptions, particularly for rare earth elements or specialized polymers used in advanced carriers, can lead to price volatility and production delays, impacting delivery timelines and profitability. The stringent quality control and defect-free production required for these components also contribute to higher manufacturing overheads. Furthermore, evolving regulatory landscapes concerning environmental impact and the disposal of manufacturing waste can impose additional compliance costs and necessitate the development of more sustainable materials and processes. Intense competition among established players and the constant threat of disruptive technologies, such as advanced robotic handling systems, can lead to price erosion and necessitate continuous innovation to maintain market share.

Key Players Shaping the Film Carrier Market

- Kodak

- Fujifilm

- Agfa

- Ilford

- Polaroid

- Konica Minolta

- 3M

- Orwo

- Lomography

- Rollei

- Adox

- Ferrania

- Bergger

- Kentmere

Significant Film Carrier Industry Milestones

- 2019: Launch of next-generation quartz carriers with enhanced thermal uniformity for advanced semiconductor lithography.

- 2020: Introduction of bio-compatible film carriers for emerging medical device manufacturing applications.

- 2021: Development of self-cleaning ceramic carriers reducing contamination in high-vacuum deposition processes.

- 2022: Strategic acquisition of a niche MEMS carrier manufacturer by a major display component supplier, indicating market consolidation.

- 2023: Significant investment in R&D for sustainable and recyclable film carrier materials by leading chemical companies.

- 2024: Release of AI-enabled carriers with integrated tracking and diagnostic capabilities for improved process monitoring.

- 2025 (Estimated): Widespread adoption of advanced composite materials for lightweight yet robust film carriers in solar panel manufacturing.

- 2025 (Estimated): Increased focus on modular and customizable carrier designs to meet specific end-user requirements across various industries.

Future Outlook for Film Carrier Market

The future outlook for the film carrier market is exceptionally bright, driven by a confluence of technological innovation and expanding industrial applications. The persistent drive for miniaturization and enhanced performance in sectors like semiconductors, displays, and MEMS will continue to fuel demand for ultra-precise and high-purity carriers. The accelerating global transition towards renewable energy sources, particularly solar, represents a significant growth catalyst, with substantial investments expected in solar cell manufacturing infrastructure. Emerging applications in fields such as advanced optics, biotechnology, and quantum computing are poised to create entirely new demand segments for specialized film carriers. Companies that focus on developing advanced material solutions, incorporating smart technologies for enhanced process control, and adopting sustainable manufacturing practices are well-positioned to capitalize on the immense market potential in the coming years. The market is projected to witness continuous innovation, leading to carriers with even greater precision, durability, and cost-effectiveness.

Film Carrier Segmentation

-

1. Application

- 1.1. Flat Panel Display Manufacturing

- 1.2. Optical Component Manufacturing

- 1.3. Micro-Electro-Mechanical Systems (MEMS) Manufacturing

- 1.4. Photovoltaic (solar) Cell Manufacturing

- 1.5. Others

-

2. Types

- 2.1. Quartz Slide

- 2.2. Silicon Slide

Film Carrier Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Film Carrier Regional Market Share

Geographic Coverage of Film Carrier

Film Carrier REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Flat Panel Display Manufacturing

- 5.1.2. Optical Component Manufacturing

- 5.1.3. Micro-Electro-Mechanical Systems (MEMS) Manufacturing

- 5.1.4. Photovoltaic (solar) Cell Manufacturing

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Quartz Slide

- 5.2.2. Silicon Slide

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Film Carrier Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Flat Panel Display Manufacturing

- 6.1.2. Optical Component Manufacturing

- 6.1.3. Micro-Electro-Mechanical Systems (MEMS) Manufacturing

- 6.1.4. Photovoltaic (solar) Cell Manufacturing

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Quartz Slide

- 6.2.2. Silicon Slide

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Film Carrier Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Flat Panel Display Manufacturing

- 7.1.2. Optical Component Manufacturing

- 7.1.3. Micro-Electro-Mechanical Systems (MEMS) Manufacturing

- 7.1.4. Photovoltaic (solar) Cell Manufacturing

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Quartz Slide

- 7.2.2. Silicon Slide

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Film Carrier Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Flat Panel Display Manufacturing

- 8.1.2. Optical Component Manufacturing

- 8.1.3. Micro-Electro-Mechanical Systems (MEMS) Manufacturing

- 8.1.4. Photovoltaic (solar) Cell Manufacturing

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Quartz Slide

- 8.2.2. Silicon Slide

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Film Carrier Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Flat Panel Display Manufacturing

- 9.1.2. Optical Component Manufacturing

- 9.1.3. Micro-Electro-Mechanical Systems (MEMS) Manufacturing

- 9.1.4. Photovoltaic (solar) Cell Manufacturing

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Quartz Slide

- 9.2.2. Silicon Slide

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Film Carrier Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Flat Panel Display Manufacturing

- 10.1.2. Optical Component Manufacturing

- 10.1.3. Micro-Electro-Mechanical Systems (MEMS) Manufacturing

- 10.1.4. Photovoltaic (solar) Cell Manufacturing

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Quartz Slide

- 10.2.2. Silicon Slide

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Film Carrier Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Flat Panel Display Manufacturing

- 11.1.2. Optical Component Manufacturing

- 11.1.3. Micro-Electro-Mechanical Systems (MEMS) Manufacturing

- 11.1.4. Photovoltaic (solar) Cell Manufacturing

- 11.1.5. Others

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Quartz Slide

- 11.2.2. Silicon Slide

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Kodak

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Fujifilm

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Agfa

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Ilford

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Polaroid

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Konica Minolta

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 3M

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Orwo

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Lomography

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Rollei

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Adox

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Ferrania

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Bergger

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Kentmere

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.1 Kodak

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Film Carrier Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Film Carrier Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Film Carrier Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Film Carrier Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Film Carrier Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Film Carrier Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Film Carrier Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Film Carrier Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Film Carrier Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Film Carrier Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Film Carrier Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Film Carrier Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Film Carrier Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Film Carrier Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Film Carrier Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Film Carrier Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Film Carrier Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Film Carrier Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Film Carrier Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Film Carrier Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Film Carrier Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Film Carrier Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Film Carrier Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Film Carrier Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Film Carrier Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Film Carrier Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Film Carrier Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Film Carrier Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Film Carrier Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Film Carrier Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Film Carrier Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Film Carrier Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Film Carrier Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Film Carrier Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Film Carrier Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Film Carrier Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Film Carrier Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Film Carrier Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Film Carrier Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Film Carrier Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Film Carrier Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Film Carrier Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Film Carrier Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Film Carrier Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Film Carrier Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Film Carrier Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Film Carrier Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Film Carrier Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Film Carrier Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Film Carrier Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Film Carrier Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Film Carrier Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Film Carrier Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Film Carrier Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Film Carrier Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Film Carrier Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Film Carrier Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Film Carrier Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Film Carrier Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Film Carrier Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Film Carrier Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Film Carrier Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Film Carrier Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Film Carrier Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Film Carrier Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Film Carrier Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Film Carrier Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Film Carrier Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Film Carrier Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Film Carrier Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Film Carrier Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Film Carrier Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Film Carrier Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Film Carrier Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Film Carrier Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Film Carrier Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Film Carrier Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Film Carrier?

The projected CAGR is approximately 5%.

2. Which companies are prominent players in the Film Carrier?

Key companies in the market include Kodak, Fujifilm, Agfa, Ilford, Polaroid, Konica Minolta, 3M, Orwo, Lomography, Rollei, Adox, Ferrania, Bergger, Kentmere.

3. What are the main segments of the Film Carrier?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 115.5 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Film Carrier," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Film Carrier report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Film Carrier?

To stay informed about further developments, trends, and reports in the Film Carrier, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence